Single Cell Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

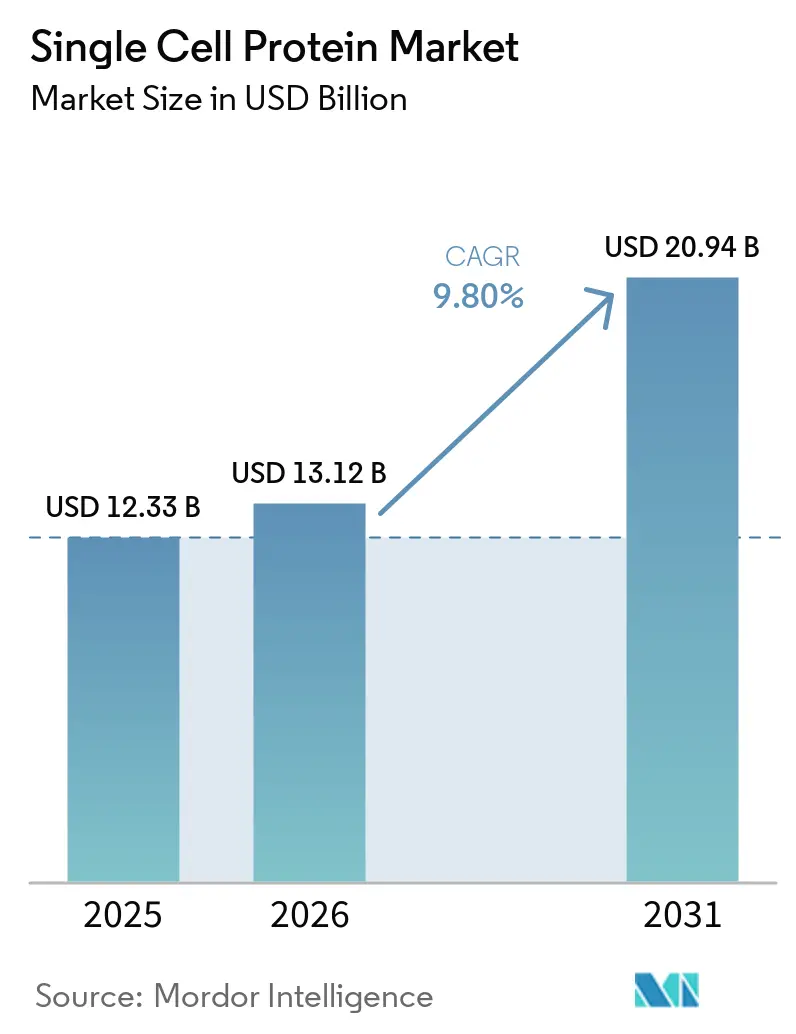

| Market Size (2026) | USD 13.12 Billion |

| Market Size (2031) | USD 20.94 Billion |

| Growth Rate (2026 - 2031) | 9.80% CAGR |

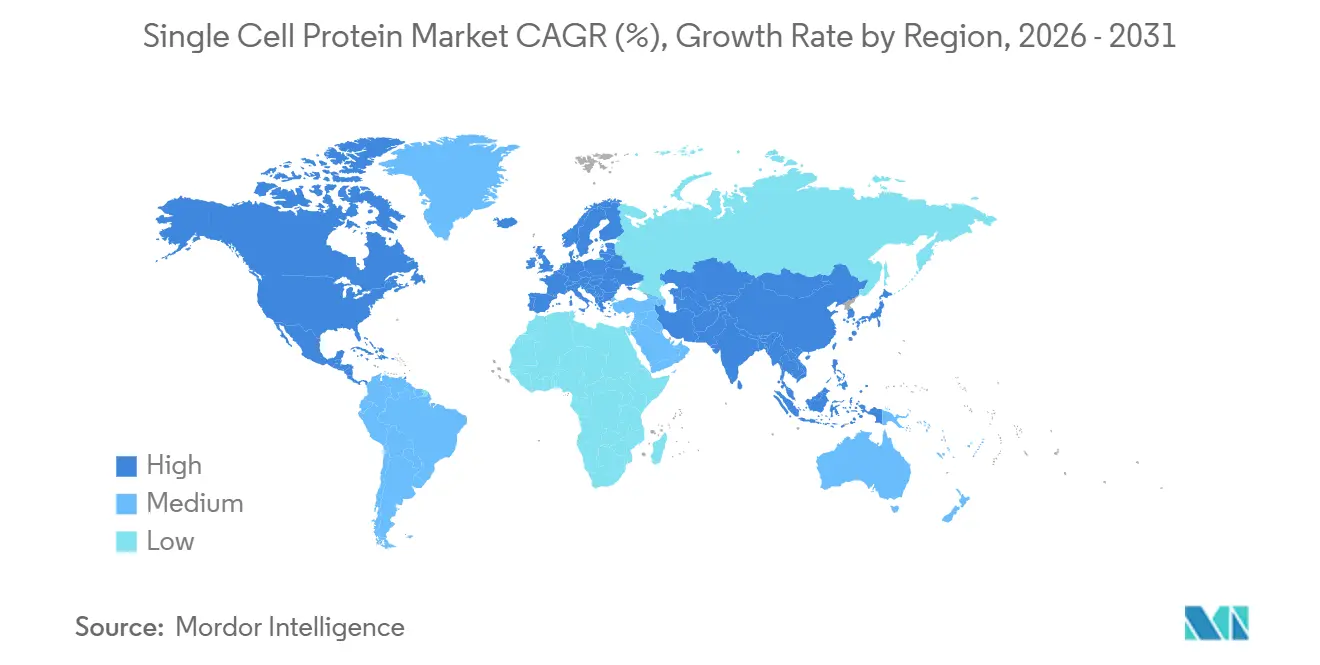

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Single Cell Protein Market Analysis by Mordor Intelligence

The single-cell protein market was valued at 12.33 billion in 2025, and is expected to grow from USD 13.12 billion in 2026 to USD 20.94 billion by 2031, registering a CAGR of 9.80% over 2026-2031. Precision-fermentation scale-up, carbon-capture bioprocessing, and supportive regulatory frameworks in Singapore, the United States, and the European Union are rewriting global protein supply chains. Production is decoupling from agricultural land through localized facilities integrated with industrial CO₂ emitters and renewable-energy hubs, which lowers logistics costs and reduces greenhouse-gas footprints. Early-moving brands are embedding microbial protein in familiar foods and beverages, accelerating mainstream acceptance among consumers who value sustainability and nutrition. Incumbent yeast and mycoprotein producers are fortifying capacity while gas-fermentation start-ups form alliances with energy companies to finance gigaton-scale plants that monetize waste methane and captured carbon.

Key Report Takeaways

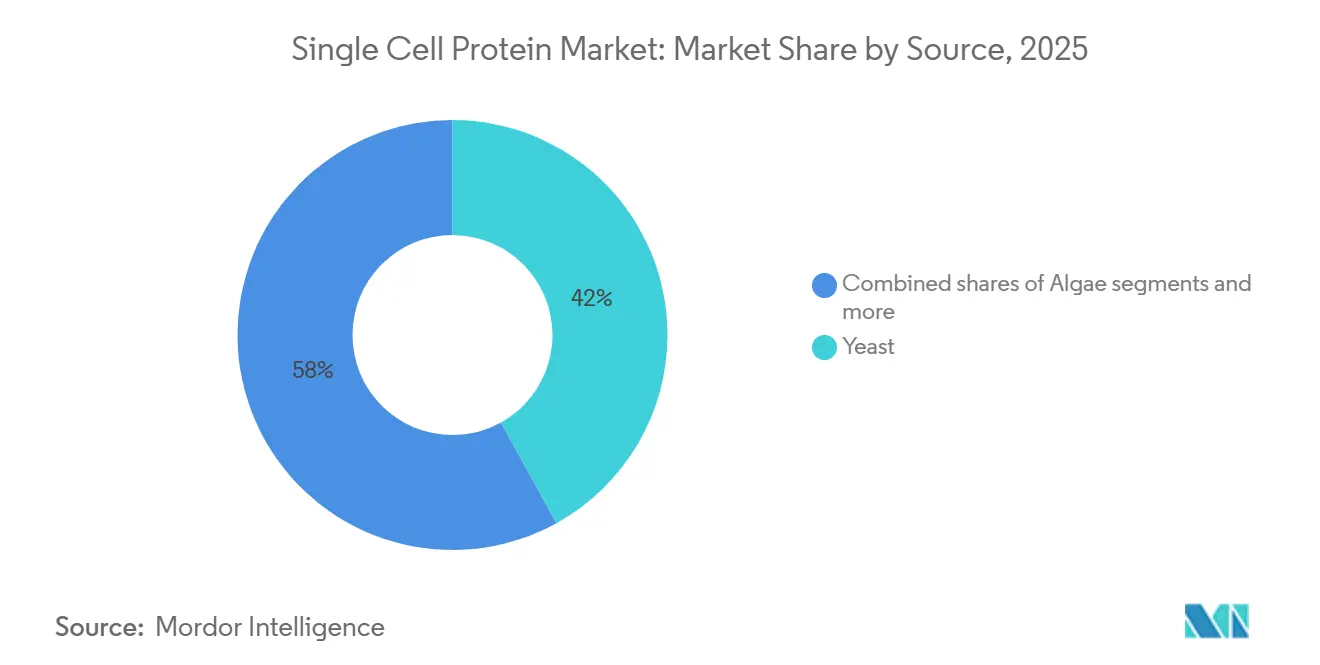

- By source, yeast dominated with 41.96% of the single cell protein market share in 2025, while bacterial protein posted the fastest 10.71% CAGR to 2031.

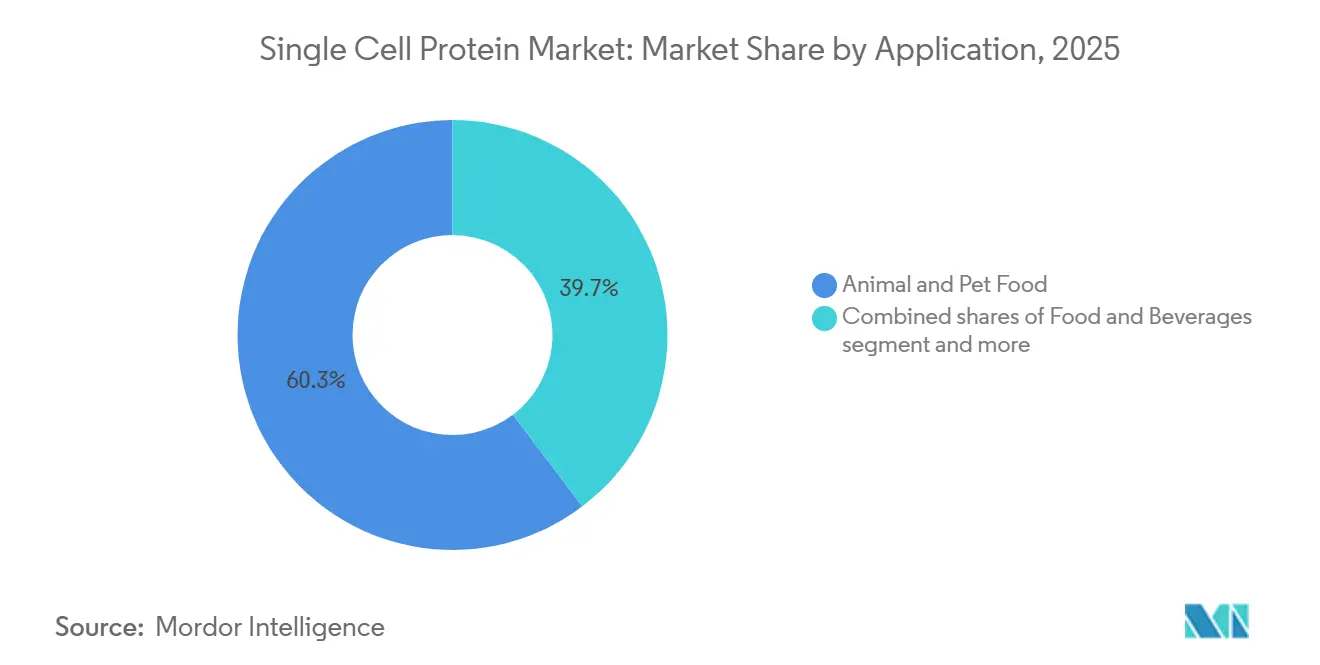

- By application, animal feed and pet food captured 60.32% of the single cell protein market size in 2025, and food and beverage applications are set to expand at an 11.82% CAGR between 2026 and 2031.

- By geography, Europe led with 32.86% of the single cell protein market share in 2025; Asia-Pacific is advancing at an 11.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Single Cell Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for alternative protein sources | +2.1% | Global, with concentration in Asia-Pacific (China, India, Singapore) and North America | Medium term (2-4 years) |

| Sustainability and environmental concerns | +1.8% | Global, particularly European Union (EU) and North America driven by carbon-reduction mandates | Long term (≥ 4 years) |

| Expansion of aqua-/animal feed and pet-food industry | +1.6% | Global, with strong uptake in Asia-Pacific aquaculture markets and North America pet food | Medium term (2-4 years) |

| Advancements in precision-fermentation technology | +1.4% | North America, EU, Singapore, Australia (regulatory-forward jurisdictions) | Short term (≤ 2 years) |

| Carbon-capture based single cell protein production economics | +1.2% | EU (Horizon-funded projects), Middle East (Saudi Arabia), North America (DOE grants) | Long term (≥ 4 years) |

| Custom amino-acid profile products for sports nutrition | +0.9% | North America, EU, urban Asia-Pacific markets (premium sports nutrition adoption) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for alternative protein sources

Population growth and shifting dietary preferences are widening the global protein gap, and single-cell protein offers a land- and water-efficient solution that fits national food-security agendas in China, India, and Singapore. Import-reliant economies view microbial protein as a hedge against soybean and fishmeal volatility, while leading producers such as Angel Yeast and Calysta are reaching cost parity with traditional feed proteins at scale. Angel Yeast's AngeoPro yeast protein, with 96% protein utilization and 47% essential amino acid content, is positioned to substitute whey and soy in protein bars, cereals, and alternative meats. Singapore's Food Agency approved multiple mycoprotein and precision-fermented ingredients in 2024, enabling rapid commercialization in a market targeting 30% nutritional self-sufficiency by 2030[1]Source: Singapore Food Agency, "Singapore Food Statistics 2024", sfa.gov.sg. The convergence of food-security mandates, import-substitution policies, and consumer willingness to adopt blended meat products is accelerating procurement by multinational food companies and regional brands.

Sustainability and environmental concerns

Life-cycle studies indicate that microbial protein can cut greenhouse-gas emissions by up to 97% relative to beef, attracting companies racing to meet science-based targets. EU farm-to-fork strategies favor low-emission ingredients, and the European Food Safety Authority's 2025 positive opinion for Fermotein illustrates momentum toward carbon-negative proteins in the mainstream food supply. Steel mills and refineries are piloting LanzaTech’s CO₂-to-protein modules, turning pollution into revenue while earning carbon credits. Horizon-funded initiatives such as SynoProtein are validating forest-residue feedstocks, broadening the sustainability narrative, and strengthening the single-cell protein market. Regulatory frameworks such as the International Standard Organization's 2021 revision of "protein fibre" definitions to include synthetically produced proteins are formalizing microbial protein as a recognized ingredient category, reducing approval friction and enabling corporate sustainability commitments to translate into procurement mandates.

Expansion of aqua-/animal feed and pet-food industry

Aquaculture alone will require an extra 100 million tonnes of feed protein by 2050, and microbial alternatives with superior digestibility are already filling premium niches. Calysta’s 20,000-tonne FeedKind facility in China supplies both aquafeed and pet-food makers, while United States pet owners spend more on hypoallergenic formulations that highlight sustainable protein sources, which are gaining traction in premium pet food formulations, with NovoNutrients shifting focus toward pet food adoption due to faster regulatory pathways and higher willingness to pay. The Better Meat Co. secured Singapore Food Agency approval for Rhiza mycoprotein in October 2024 and holds a commercial collaboration with Perdue Farms for "Chicken Plus" hybrid products in the United States, demonstrating how single-cell protein can reduce meat content while maintaining sensory attributes and improving margin structure.

Advancements in precision-fermentation technology

Precision fermentation is enabling the production of functional proteins with Protein Digestibility Corrected Amino Acid Score (PDCAAS) scores of 1.0, matching or exceeding whey and casein benchmarks, and regulatory approvals are accelerating commercialization timelines. The United States Food and Drug Administration (U.S. FDA) issued Generally Recognized As Safe (GRAS) letters for All G's bovine lactoferrin and Vivici's whey protein in 2024, demonstrating that precision fermentation can reach industrial productivity levels that reduce downstream processing costs and improve unit economics. Hydrogen-oxidizing bacteria platforms achieved 100% hydrogen efficiency in electrolytic gas-lift reactors, eliminating H₂ transfer losses and reducing explosion risk, with biomass productivity of 0.20 grams per liter per day and 58.3% protein content. These advances are compressing strain development cycles from years to months through high-throughput biofoundries and evolutionary engineering, enabling rapid customization of amino acid profiles for sports nutrition, infant formula, and elderly nutrition applications.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from established soy/fishmeal proteins | -1.3% | Global, particularly in price-sensitive aquafeed and livestock feed markets | Medium term (2-4 years) |

| High CAPEX and operating costs of large-scale bioreactors | -1.1% | Global, with acute impact in regions lacking biomanufacturing infrastructure | Long term (≥ 4 years) |

| Regulatory and consumer-acceptance hurdles | -0.8% | EU (novel food timelines), North America (GRAS variability), Asia-Pacific (fragmented frameworks) | Short term (≤ 2 years) |

| Feed-gas and molasses price volatility | -0.6% | Regions dependent on imported methanol, molasses, or natural gas (e.g., Europe, import-reliant Asia-Pacific markets) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from established soy/fishmeal proteins

Soybean meal remains the dominant protein source in livestock and aquafeed due to established supply chains, agronomic scale, and commodity pricing mechanisms. Single-cell protein must achieve cost parity or demonstrate superior functional performance (digestibility, amino acid profile, pathogen-free status) to displace incumbent ingredients in price-sensitive feed markets. Calysta's FeedKind positions itself competitively with fishmeal, but scaling beyond niche applications requires multi-year supply agreements and validation trials that delay market penetration. DSM-Firmenich's rainbow trout trials demonstrated that 20% single-cell protein inclusion performs comparably to fishmeal, yet feed formulators remain conservative in adopting novel ingredients without long-term performance data and regulatory clarity across export markets. The aquafeed market's CAGR through 2031, and single-cell protein's share will depend on securing anchor customers willing to absorb transition risk and co-invest in supply-chain integration.

Regulatory and consumer-acceptance hurdles

Novel food approval timelines in the European Union can exceed five years, and the Protein Brewery filed its Fermotein dossier over five years before receiving the European Food Safety Authority's positive opinion in 2025, with European Commission and member-state approval still pending. United States Food and Drug Administration (U.S. FDA) Generally Recognized As Safe (GRAS) processes vary in duration and stringency depending on self-affirmation versus "No Questions" letter pathways, and companies such as Verley and All G are pursuing both routes to accelerate market entry. The United States Food and Drug Administration (U.S. FDA) fragmented regulatory frameworks across Asia-Pacific jurisdictions create duplication of safety studies and delay regional launches, though Singapore's Food Agency has emerged as a first-mover market by approving multiple microbial proteins in 2024. Labeling requirements for genetically modified microorganisms and allergen declarations (e.g., beta-casein as a milk allergen) add compliance complexity and may trigger negative consumer perceptions in markets with low Genetically Modified Organisms (GMOs) acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Established Yeast Capacity Leads Amid Rapid Bacterial Gains

In 2025, yeast-based single-cell protein commanded a 41.96% market share, driven by several key developments in the industry. Angel Yeast's newly commissioned 11,000-tonne-per-year facility in Yichang (operational from November 2025) significantly contributed to this growth. Additionally, Quorn's mycoprotein production capacity, which is approximately 24,000 tonnes annually, and Lallemand's extensive global portfolio of yeast extracts and nutritional products further strengthened the segment's position. Yeast protein production benefits from a combination of factors, including decades of industrial fermentation expertise, a robust and well-established downstream processing infrastructure, and widespread consumer familiarity with yeast-derived ingredients.

Bacterial protein is rapidly emerging as the fastest-growing source segment, with a projected compound annual growth rate (CAGR) of 10.71% from 2026 to 2031. This remarkable growth is primarily driven by advancements in gas-fermentation platforms, which efficiently convert carbon dioxide (CO₂), methane, and hydrogen into high-protein biomass. A notable example of this innovation is NovoNutrients, which raised USD 18 million in Series A funding in July 2024, with Woodside Energy leading the investment. This funding aims to scale NovoNutrients' CO₂-to-protein technology. These developments highlight the growing potential of bacterial proteins as a sustainable and scalable alternative in the protein market.

By Application: Animal Feed Anchored by Aquaculture Economics

Animal feed and pet food applications commanded a 60.32% share in 2025, driven by aquaculture's global growth and pet food's premium pricing tolerance for hypoallergenic and sustainable ingredients. Calysta's FeedKind methanotrophic protein is operational at 20,000 tonnes per year in China and targets 70% market penetration in pet food protein, approaching cost parity with fishmeal in high-volume contracts. In animal feed, the proven nutritional equivalence and cost benefits are evident, with inclusion levels tailored between 10-80%, contingent on species needs and regulatory stipulations.

Food and beverage applications are expanding at an 11.82% CAGR from 2026 to 2031, supported by regulatory approvals for precision-fermented whey, mycoprotein, and yeast protein in sports nutrition, dairy alternatives, and hybrid meat products. Starbucks India and SuperYou launched protein cold foam in January 2026, embedding protein into familiar beverage formats to lower adoption barriers. Regulatory advancements further fuel this growth, highlighted by the European Food Safety Authority's (EFSA's)[2]Source: European Food Safety Authority, "Navigating Novel Foods to Europe in 2025: Insights into the Latest EFSA Guidance", efsa.europea.eu updated guidance on novel foods, set to take effect in February 2025, which streamlines the approval process for microbial proteins

Geography Analysis

In 2025, Europe holds a 32.86% market share, reflecting its advanced regulatory frameworks and well-established industrial infrastructure. Countries such as the Netherlands are leading efforts with national protein strategies aimed at reducing import reliance and enhancing domestic microbial protein production. The region benefits from strong consumer acceptance of alternative proteins and sustainability-driven policies that support single-cell protein adoption. Key developments include EU approvals for novel protein sources and significant investments in fermentation capacity, such as Solar Foods' Factory01 in Finland, which produces 160 tons of Solein annually. However, Europe's growth rate lags behind that of the Asia-Pacific due to complex regulatory processes and the constraints of a mature market.

Asia-Pacific is the fastest-growing region, with an 11.91% CAGR projected through 2031. This growth is driven by China's advancements in biomanufacturing infrastructure and government support for protein fermentation. India's animal feed growth and consumption over recent years have also boosted market demand[3]Source: U.S Department of Agriculture 2025, "The Growing Demand for Animal Products and Feed in India: Future Prospects for Production, Trade, and Technology Innovation", ers.usda.gov. Singapore has established itself as a regional innovation hub through its leadership in alternative protein regulatory approvals, enabling multiple companies to secure manufacturing licenses and novel food authorizations. Japan and South Korea are enhancing their precision fermentation capabilities through government programs and corporate investments, while Australia is implementing comprehensive strategies to commercialize alternative proteins.

North America benefits from a favorable regulatory environment and substantial venture capital investments. Companies have secured significant funding, such as NovoNutrients' USD 18 million Series A round, alongside multiple Generally Recognized as Safe (GRAS) approvals for microbial proteins. The region's dynamic innovation ecosystem fosters rapid commercialization through partnerships between biotech startups and established food companies. Meanwhile, South America and the Middle East and Africa are emerging as promising markets, driven by increasing protein demand and growing investment interest. For instance, Unibio secured USD 70 million from the Saudi Industrial Investment Group to expand its production capacity. These regions offer significant opportunities for Single Cell Protein adoption in animal feed and potential human nutrition markets, contingent on the development of their regulatory frameworks.

Competitive Landscape

The single-cell protein market showcases moderate fragmentation. This score allows both established players and innovative startups to carve out their niches through unique positioning and strategic alliances. While market leaders draw on decades of commercial and regulatory expertise, newcomers are channeling their efforts into novel production methods and specialized applications. A notable trend is vertical integration, where companies not only manage fermentation and downstream processes but also cultivate direct relationships with customers to maximize value. Successful players stand out through technology differentiation, focusing on feedstock use, production efficiency, and product functionality, often boasting advantages in cost or performance. The market is further characterized by its adaptability to evolving consumer demands and regulatory landscapes, which drive innovation and competition.

Partnerships play a pivotal role in expediting market entry and scaling. A case in point is Cargill's strategic investment in ENOUGH, coupled with a commercial deal for distributing the ABUNDA mycoprotein, tapping into established food industry networks for swift market access. There's a burgeoning interest in specialized areas like human nutrition, where regulatory approvals offer temporary competitive edges, and in innovative feedstock uses that not only cut production costs but also bolster sustainability credentials.

Disruptors are gravitating towards advanced technologies, including gas and precision fermentation, which facilitate production from CO2 and industrial waste. The flurry of patent filings in metabolic engineering and fermentation optimization underscores a heated race for innovation, with firms vying for exclusive advantages in both production efficiency and product attributes. Additionally, the market is witnessing increased investments in research and development activities, aimed at enhancing production scalability and addressing global protein demand, which is expected to grow significantly during the forecast period.

Single Cell Protein Industry Leaders

-

Angel Yeast Co. Ltd.

-

Calysta Inc.

-

Unibio A/S

-

Solar Foods

-

3FBIO Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Danish biotech firm Unibio partnered with Saudi Arabia's Saudi Industrial Investment Group (SIIG) in a joint venture to construct a single-cell protein plant in Al Jubail, Saudi Arabia, with an estimated investment of USD 373 million. Leveraging Unibio's patented U-Loop bioreactor technology, the facility will utilize natural gas as its feedstock to produce the Uniprotei ingredient.

- March 2025: Solar Foods Partnered with Superb Food in the United States. This agreement represents a strategic step for Solar Foods as it aims to expand its footprint in the region and cater to the growing demand for sustainable protein alternatives.

- October 2024: LanzaTech expanded biorefining platform capabilities to include commercial-scale nutritional protein production directly from CO2, targeting the USD 1 trillion alternative protein market.

- November 2023: MicroHarvest GmbH launched a single-cell protein pilot plant in Lisbon, Portugal, with an initial capacity of 25 kg per day. Prior to its planned product launch of HILIX, a protein-rich feed product for aquaculture scheduled for early 2024, the start-up produced test samples mainly for the feed industry.

Global Single Cell Protein Market Report Scope

Single Cell Protein (SCP), sourced from microbial biomass such as bacteria, algae, yeast, and fungi, is emerging as a sustainable and carbon-neutral alternative to traditional protein sources. The market is segmented by source, application, and geography. By source, the market covers algae, yeast, fungi, and bacteria. By application, the market is segmented into animal feed/pet food, food and beverages, dietary supplements, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The report offers market size and forecasts in value (USD million) for the above-mentioned segments.

| Algae |

| Yeast |

| Fungi |

| Bacteria |

| Animal Feed and Pet Food |

| Food and Beverages |

| Dietary Supplements |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| Source | Algae | |

| Yeast | ||

| Fungi | ||

| Bacteria | ||

| Application | Animal Feed and Pet Food | |

| Food and Beverages | ||

| Dietary Supplements | ||

| Other Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the single cell protein market expected to grow?

The single cell protein market size is projected to rise from USD 13.12 billion in 2026 to USD 20.94 billion by 2031 at a 9.8% CAGR.

Which source leads current adoption?

Yeast maintained 41.96% share in 2025, thanks to capacity additions such as Angel Yeast’s 11,000-tonne Yichang plant and Quorn’s long-running mycoprotein facilities.

Which region will register the highest growth?

Asia-Pacific, led by China, Singapore, and India, is set to grow at 11.91% CAGR on the back of national alternative-protein strategies and new large-scale fermentation plants.

What challenges could slow market expansion?

High bioreactor CAPEX, feedstock price swings, and competition with low-cost soy and fishmeal constrain near-term economics, while lengthy EU novel-food reviews and variable consumer acceptance add regulatory risk.

Page last updated on: