Liquid Sugar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

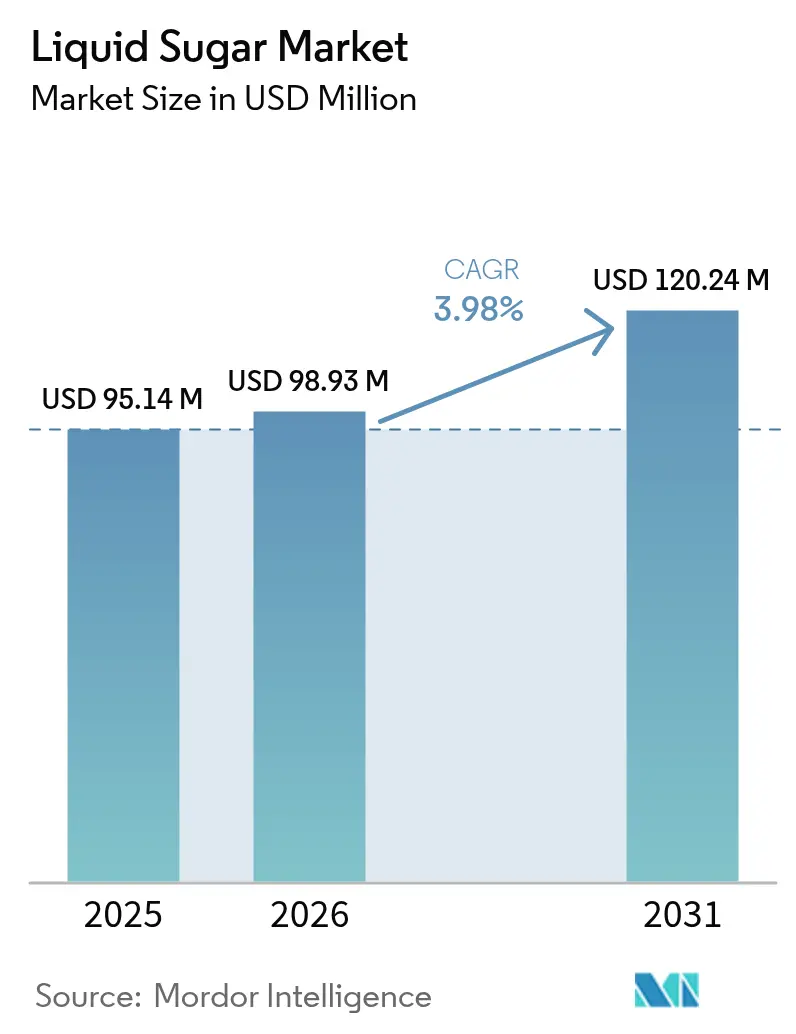

| Market Size (2026) | USD 98.93 Million |

| Market Size (2031) | USD 120.24 Million |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

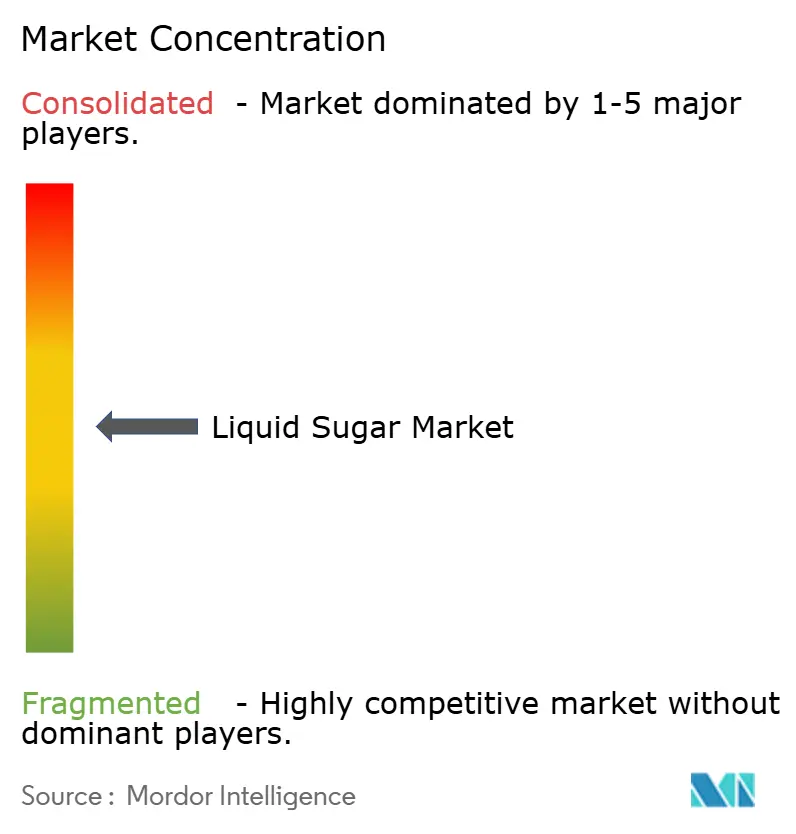

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Liquid Sugar Market Analysis by Mordor Intelligence

The liquid sugar market size was valued at USD 95.14 million in 2025 and estimated to grow from USD 98.93 million in 2026 to reach USD 120.24 million by 2031, at a CAGR of 3.98% during the forecast period (2026-2031). The expansion stems from beverage producers’ decisive pivot toward ready-to-drink formats, where liquid sugar’s fast solubility eases cold-processing bottlenecks and trims energy use. Convenience-oriented consumption patterns reinforce this shift, while regulatory scrutiny on labeling accuracy favors liquid formulations that deliver consistent Brix values. Certified-organic variants gain traction as processors match rising consumer health concerns, although supply constraints temper short-term growth. Meanwhile, pharmaceutical excipient demand offers a second engine for the liquid sugar market, given liquid sugar’s proven compliance with current Good Manufacturing Practices. Raw-sugar price swings and health-driven sugar-reduction policies remain the principal headwinds.

Key Report Takeaways

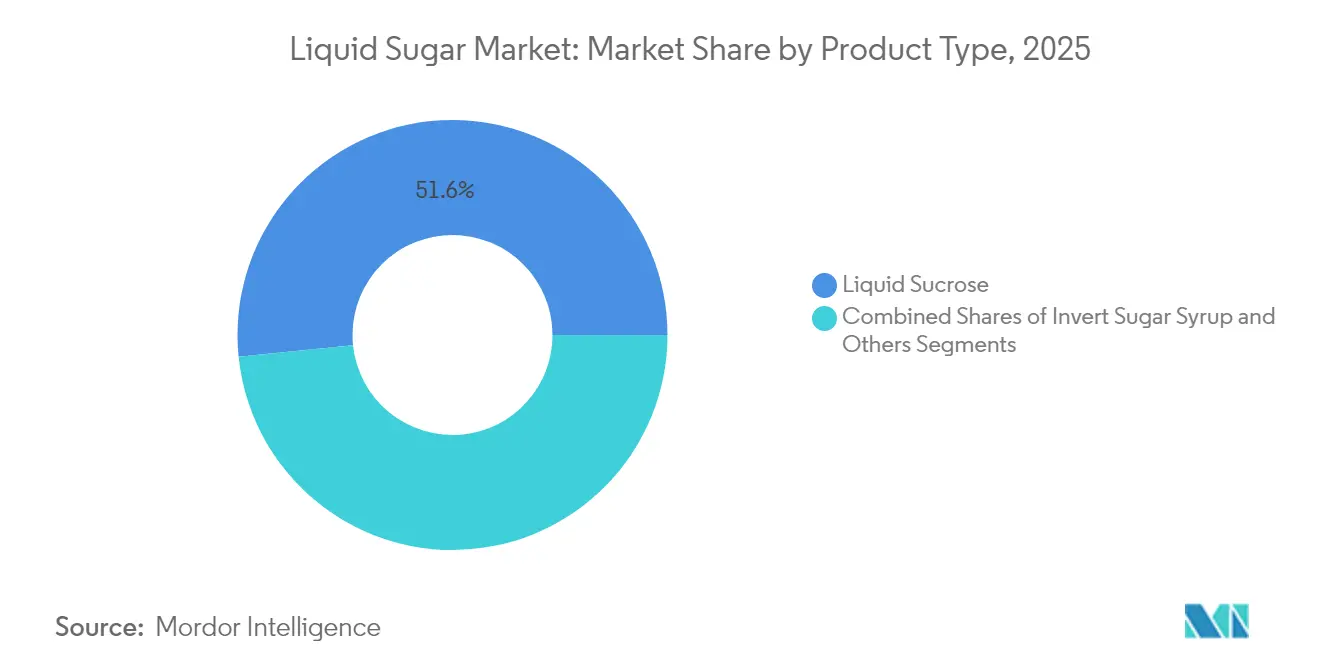

- By product type, liquid sucrose led with 51.62% revenue share in 2025, whereas invert sugar syrup is forecast to expand at a 5.12% CAGR through 2031.

- By origin, conventional grades accounted for 75.45% of 2025 revenues, while organic liquid sugar is poised for a 7.48% CAGR between 2026 and 2031.

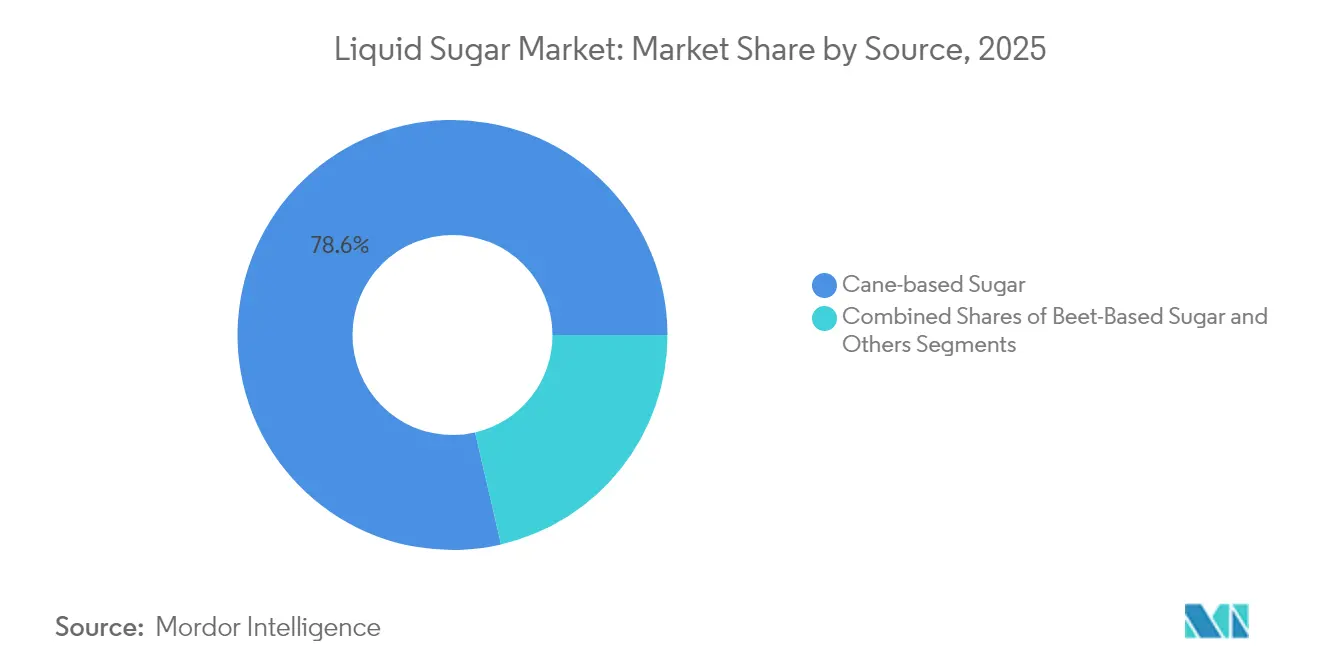

- By source, cane-derived variants captured 78.63% of 2025 output; beet-based liquid sugar is projected to grow at a 5.43% CAGR over the same horizon.

- By application, beverages commanded a 45.23% share of the liquid sugar market size in 2025 and are advancing at a 5.91% CAGR through 2031.

- By geography, North America held 34.12% of global 2025 sales, whereas Asia-Pacific records the fastest regional CAGR at 5.61% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquid Sugar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand in the beverage industry | +1.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising adoption in bakery and confectionery applications | +0.8% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Uniform mixing capabilities in food and beverage manufacturing | +0.6% | Global industrial food processing regions | Short term (≤ 2 years) |

| Rising demand from pharmaceutical industry | +0.4% | North America and Europe regulatory-compliant markets | Long term (≥ 4 years) |

| RTD coffee and cold-brew market boom raises liquid sugar usage | +0.7% | North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Easy handling and storage compared to granulated sugar | +0.3% | Global industrial food processing facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand in the Beverage Industry

The beverage sector's structural transformation toward convenience-oriented products creates sustained demand for liquid sugar applications that traditional crystalline alternatives cannot match. According to the Centers for Disease Control and Prevention[1]Centers for Disease Control and Prevention, " Sugary Drinks Consumption in the United States", www.cdc.gov, data from 2024, 68% of people in the Northeast United States consumed sugary drinks at least once per day. This shift reflects deeper industry recognition that liquid sugar eliminates dissolution-related production delays while ensuring homogeneous sweetness distribution in cold-processed beverages. The adoption of liquid sugar in high-volume beverage production leads to increased manufacturing efficiency through streamlined handling, reduced labor costs, and improved process control, providing economic benefits that drive market growth. The FDA's labeling requirements for precise added sugar declarations make liquid sugar more advantageous due to its consistent composition and standardized concentration levels compared to crystalline alternatives, which can vary in quality and dissolution rates.

Rising Adoption in Bakery and Confectionery Applications

Bakery and confectionery manufacturers increasingly recognize liquid sugar's technical advantages in achieving consistent moisture retention and texture profiles that crystalline sugar cannot deliver reliably. The Asia-Pacific chocolate market expansion, particularly in China and India, drives demand for liquid sugar applications where precise sweetness control enables manufacturers to adapt products to local taste preferences. Industrial bakery operations benefit from liquid sugar's ability to integrate seamlessly with automated mixing systems, reducing production variability and waste rates. Quality control standards established by organizations like the Asian Productivity Organization emphasize the importance of consistent ingredient performance in processed foods, making liquid sugar an attractive option for manufacturers seeking ISO and HACCP compliance. The confectionery sector's adoption accelerates as manufacturers discover liquid sugar's superior performance in temperature-sensitive applications where crystalline sugar's dissolution characteristics create processing complications. European and North American markets lead this trend, with Asia-Pacific manufacturers rapidly adopting similar approaches to meet export quality requirements.

Uniform Mixing Capabilities in Food and Beverage Manufacturing

Manufacturing efficiency considerations drive liquid sugar adoption as food processors seek to eliminate the dissolution bottlenecks that plague crystalline sugar applications in industrial-scale production. United Sugars Corporation's liquid sucrose specifications demonstrate the technical precision achievable with liquid formulations, including 99.85% sucrose content and 67.5% Brix consistency that ensures predictable performance across diverse applications. Cold-processing applications particularly benefit from liquid sugar's immediate integration capabilities, eliminating the energy costs and time delays associated with crystalline sugar dissolution. Food safety protocols increasingly favor liquid sugar systems that reduce contamination risks through enclosed handling systems compared to open crystalline sugar transfer methods. The pharmaceutical industry's stringent manufacturing requirements create additional demand for liquid sugar's consistent performance characteristics in drug formulation applications. Industrial food processors report a reduction in mixing times when switching from crystalline to liquid sugar systems, translating directly to increased production capacity and reduced energy consumption.

Rising Demand from Pharmaceutical Industry

Pharmaceutical manufacturers increasingly specify liquid sugar for excipient applications where FDA compliance requirements demand consistent performance characteristics that crystalline alternatives cannot reliably deliver. The FDA's guidance on pharmaceutical excipients emphasizes the critical importance of safety evaluation and consistent quality for ingredients used in drug formulations, creating regulatory advantages for liquid sugar systems with documented purity profiles. Liquid sugar's superior dissolution characteristics eliminate the particle size variability issues that can compromise drug bioavailability in crystalline sugar applications. Pharmaceutical-grade liquid sugar production requires adherence to current Good Manufacturing Practices (cGMP) that favor liquid processing systems over crystalline handling operations prone to contamination risks. The infant formula sector represents a particularly demanding application where FDA regulations require precise nutrient control and safety standards that liquid sugar formulations can meet more consistently than crystalline alternatives. Regulatory compliance costs for pharmaceutical applications often justify liquid sugar's premium pricing through reduced validation requirements and simplified quality control procedures.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to excessive sugar consumption and rising diabetes rates | -0.9% | Global, with highest impact in developed markets | Long term (≥ 4 years) |

| Growing consumer preference for natural and artificial sweetener alternatives | -0.6% | North America and Europe leading, spreading to Asia-Pacific | Medium term (2-4 years) |

| Strict government regulations on sugar content in food and beverages | -0.4% | Developed markets with established regulatory frameworks | Long term (≥ 4 years) |

| Price volatility in raw sugar commodities | -0.3% | Global supply chain dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health Concerns Related to Excessive Sugar Consumption and Rising Diabetes Rates

Public health initiatives targeting sugar consumption create regulatory and consumer pressures that constrain the liquid sugar market expansion across developed economies. The FDA's establishment of a 50-gram daily reference value for added sugars reflects mounting scientific evidence linking excessive sugar intake to diabetes and obesity, creating labeling requirements that discourage high-sugar product formulations. Healthcare cost pressures drive government policies that increasingly target sugar consumption through taxation and labeling mandates, with liquid sugar applications facing particular scrutiny due to their industrial-scale usage. The Dietary Guidelines for Americans' recommendation to limit added sugars to less than 10% of daily calories creates formulation constraints for food manufacturers that directly impact liquid sugar demand, according to the U.S. Food and Drug Administration[2]U.S. Food and Drug Administration, “Dietary Guidelines for Americans 2025-2030—Policy Document,” www.fda.gov. Consumer awareness campaigns linking sugar consumption to chronic disease outcomes create market headwinds that force manufacturers to reformulate products with reduced sugar content.

Growing Consumer Preference for Natural and Artificial Sweetener Alternatives

Consumer health consciousness drives sustained demand for sugar alternatives that offer sweetening functionality without the caloric and health implications associated with traditional sugar products. The prebiotic beverage trend demonstrates how manufacturers respond to consumer preferences by developing products that eliminate added sugars while maintaining sweetness through alternative ingredients. Stevia and other natural sweetener alternatives gain market acceptance as processing technologies improve their taste profiles and reduce off-flavors that previously limited adoption. Artificial sweetener technologies continue advancing, with new compounds offering improved stability and functionality that compete directly with liquid sugar applications. The organic food movement creates consumer expectations for "clean label" products that avoid processed sugar ingredients, favoring natural alternatives despite higher costs. Food manufacturers increasingly reformulate products to meet consumer demands for reduced sugar content, often substituting liquid sugar with alternative sweetening systems. Regulatory approval processes for new sweetener alternatives accelerate as health authorities recognize the public health benefits of sugar reduction strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Invert Sugar Syrup Gains Despite Sucrose Dominance

Liquid sucrose maintains commanding market leadership with a 51.62% share in 2025, reflecting its established position in traditional food processing applications where manufacturers prioritize proven performance over specialized functionality. However, invert sugar syrup emerges as the fastest-growing segment at 5.12% CAGR through 2031, driven by its superior performance in applications requiring enhanced moisture retention and crystallization prevention. The pharmaceutical industry's increasing adoption of invert sugar syrup for drug formulations creates premium-priced demand that justifies the additional processing costs compared to standard liquid sucrose. Bakery applications particularly favor invert sugar syrup's ability to extend product shelf life through improved moisture binding, creating competitive advantages for manufacturers serving retail distribution channels.

Other liquid sugar variants capture the remaining market share through specialized applications in confectionery and pharmaceutical manufacturing where unique functional properties justify premium pricing. The beverage industry's continued expansion drives sustained demand for liquid sucrose, while specialty food processors increasingly specify invert sugar syrup for applications requiring enhanced stability. Manufacturing efficiency considerations favor liquid sucrose for high-volume applications, while invert sugar syrup gains traction in premium product formulations where functional benefits outweigh cost considerations. Quality control standards in food processing increasingly recognize invert sugar syrup's consistent performance characteristics, driving adoption among manufacturers seeking to minimize production variability.

By Origin: Organic Segment Accelerates, While Conventional Dominates the Market

The organic liquid sugar segment demonstrates exceptional growth momentum at 7.48% CAGR through 2031, despite conventional products maintaining 75.45% market share in 2025. This growth trajectory reflects the broader organic food processing expansion, where manufacturers require certified organic sweetening ingredients to maintain product certifications and meet consumer expectations. The infant formula industry's increasing focus on organic formulations drives specialized demand for organic liquid sugar that meets stringent FDA safety and quality requirements.Conventional liquid sugar maintains market dominance through established supply chains and cost advantages that prove decisive in price-sensitive applications like industrial beverage production.

However, the organic segment's rapid growth creates opportunities for processors willing to invest in organic certification and supply chain development. Food manufacturers increasingly specify organic liquid sugar for premium product lines where organic certification justifies higher ingredient costs. The Asia-Pacific region's expanding organic food market creates additional growth opportunities for organic liquid sugar suppliers who can navigate complex international certification requirements. Supply chain constraints for organic raw materials create periodic shortages that limit organic liquid sugar availability, supporting premium pricing for qualified suppliers.

By Source: Cane-Based Sugar Dominance Faces Beet-Based Competition

Strategic supply chain diversification drives beet-based liquid sugar growth at 5.43% CAGR through 2031, despite cane-based products maintaining 78.63% market share in 2025. The USDA's forecast of declining sugar production creates supply security concerns that favor processors with diversified raw material sources, making beet-based alternatives increasingly attractive for risk management. Climate change impacts on sugarcane production regions create additional incentives for manufacturers to develop beet-based supply chains as insurance against weather-related disruptions. European food processors particularly favor beet-based liquid sugar due to regional supply chain advantages and reduced transportation costs compared to imported cane-based alternatives.

Cane-based liquid sugar maintains market leadership through established processing infrastructure and consumer preference for traditional sugar sources in many applications. However, technical performance differences between cane and beet-based liquid sugar prove minimal in most applications, creating opportunities for substitution based on economic and supply chain considerations. The pharmaceutical industry's stringent quality requirements create specialized demand for both cane and beet-based liquid sugar variants that meet specific purity standards. Other sugar sources, including corn-based alternatives, capture niche market segments where specialized functionality or cost advantages justify their use despite limited availability.

By Application: Beverages Lead Market Growth and Share

The beverage sector's dual role as market leader and growth driver creates unique dynamics where a 45.23% market share in 2025 combines with a 5.91% CAGR through 2031 to reinforce the segment's strategic importance. Ready-to-drink coffee and cold-brew applications drive this growth through specialized requirements for liquid sweetening systems that function effectively in cold-processing environments. The prebiotic beverage trend demonstrates how manufacturers leverage liquid sugar's consistent performance to achieve complex flavor profiles while maintaining production efficiency. Bakery applications benefit from liquid sugar's moisture retention properties that extend product shelf life, while confectionery manufacturers value its ability to prevent crystallization in temperature-sensitive formulations.

Baby food applications represent a high-growth niche where FDA safety requirements create barriers for alternative sweetening systems, favoring liquid sugar's documented safety profile and consistent quality characteristics. Pharmaceutical applications command premium pricing through specialized requirements for excipient-grade liquid sugar that meets stringent purity and safety standards. Other applications, including dairy and processed food manufacturing, provide steady demand for liquid sugar systems that offer operational advantages over crystalline alternatives. The beverage industry's continued innovation in functional and health-focused products creates sustained demand for liquid sugar applications that can integrate with complex ingredient systems while maintaining regulatory compliance.

Geography Analysis

North America commands 34.12% market share in 2025, driven by established beverage manufacturing infrastructure and regulatory frameworks that favor liquid sugar applications in food processing. The region's mature food processing industry creates sustained demand for liquid sugar systems that offer operational efficiency advantages over crystalline alternatives. FDA regulations requiring precise added sugar labeling create competitive advantages for liquid sugar applications where consistent composition enables accurate nutritional declarations. Major beverage manufacturers like Coca-Cola demonstrate continued innovation in liquid sugar applications through product launches that leverage liquid sweetening systems for enhanced functionality. The ready-to-drink coffee segment's expansion creates specialized demand for liquid sugar applications that function effectively in cold-processing environments. However, health consciousness trends and regulatory pressures targeting sugar consumption create headwinds that may constrain long-term growth in developed North American markets.

Asia-Pacific emerges as the fastest-growing region at 5.61% CAGR through 2031, reflecting the rapid industrialization of food processing capabilities and rising disposable incomes that drive packaged food consumption. China's food processing industry expansion creates substantial demand for liquid sugar applications in beverage and confectionery manufacturing, supported by growing consumer acceptance of packaged food products. India's developing food processing infrastructure creates opportunities for liquid sugar suppliers who can navigate complex regulatory requirements and establish reliable supply chains. Japan's emphasis on quality control standards in food processing creates premium-priced demand for liquid sugar applications that meet stringent safety and consistency requirements Asian Productivity Organization. The region's expanding chocolate and confectionery markets drive specialized demand for liquid sugar applications that enable manufacturers to adapt products to local taste preferences. Supply chain development challenges and regulatory complexity create barriers for international liquid sugar suppliers seeking to enter Asia-Pacific markets, favoring regional processors with established distribution networks.

Europe maintains steady market presence through established food processing industries and regulatory frameworks that support liquid sugar applications in traditional manufacturing sectors. The region's emphasis on organic food processing creates premium-priced demand for certified organic liquid sugar that meets stringent European Union organic standards. Brexit-related supply chain disruptions create opportunities for European liquid sugar processors to capture market share from UK-based competitors facing trade barriers. Germany's advanced food processing technology creates demand for liquid sugar applications that integrate with automated manufacturing systems. The region's mature beverage industry provides stable demand for liquid sugar applications, while emerging health consciousness trends create challenges for sugar-based ingredients across European markets.

Regulatory Landscape

Globally, liquid sugar used in food and beverages is handled under a mix of compositional standards, food safety systems, and labeling rules that increasingly emphasize measurable solids content and added-sugars transparency. In the United States, sweetening agents fall under 21 CFR Part 168, and FDA added-sugars labeling requirements heighten the need for consistent Brix control and documentation. FDA also listed a 2026 priority deliverable to advance a proposed rule that would require submission of GRAS notices for new food substances, tightening the compliance pathway for novel sweetener systems that may compete with or be blended into liquid sugar formulations.

In Asia, China implemented QB/T 4093-2023 for liquid sugar effective July 1, 2024, which sets requirements for sensory and chemical characteristics, testing, and labeling for liquid sugar derived from cane, beet, or raw sugar. In Europe, labeling for glucose and glucose-fructose syrups is defined under Directive 2001/111/EC based on fructose content, while trade and processing policy shifts can affect raw material economics. The EU set updated molasses import duties and representative prices via Implementing Regulation (EU) 2026/1003 and suspended inward processing arrangements for certain raw cane sugar codes for white sugar production in May 2026, effective until May 27, 2027, which can influence how refiners source and optimize inputs for liquid sugar and related syrups.

Value Chain Analysis

The liquid sugar value chain begins with agricultural feedstocks (primarily sugarcane and sugar beet) and the procurement of raw or refined sugar, followed by refining and liquid conversion. Refining typically includes remelting, clarification (such as carbonatation or phosphatation), decolorization (for example via ion exchange resins or carbon), and filtration before standardizing concentration to customer specifications. For liquid sugar, the process often proceeds with controlled dissolution in water and tight Brix management to produce a uniform, pumpable sweetener stream for enclosed handling.

Downstream, bulk logistics and storage are key differentiators versus crystalline sugar, requiring dedicated tanker trucks or rail tank cars, appropriate food-grade tanks, and contamination controls to maintain product integrity from refinery to beverage, bakery, confectionery, infant nutrition, and pharmaceutical customers. Integrated refiners (milling plus refining) and standalone raw sugar refineries both supply liquid sugar, but plants located near high-volume manufacturing clusters can reduce freight cost and help manage temperature or microbial risk during transport. HACCP-based controls, traceability, and organic or pharma-grade documentation where applicable create supplier qualification barriers, while diversification across cane and beet inputs is used to manage supply disruptions and regional trade volatility.

Competitive Landscape

The liquid sugar market maintains moderate concentration, with established sugar processors dominating the industry. These processors utilize their existing refining infrastructure to capture liquid sugar premiums while maintaining cost advantages through integrated supply chains. Key market players include Cargill Inc., Archer Daniels Midland Company, Tate & Lyle Plc, Südzucker AG, and ASR Group. Companies now focus their competitive strategies on technological capabilities and regulatory compliance rather than cost leadership, as customers prioritize quality consistency and supply chain reliability. The pharmaceutical-grade liquid sugar segment offers growth opportunities, where strict FDA compliance requirements create entry barriers for smaller competitors while enabling premium pricing for qualified suppliers.

The organic liquid sugar segment presents growth potential for processors who invest in certification and supply chain development, despite increased operational complexity. New market entrants target specialized applications, particularly infant formula and pharmaceutical excipients, where regulatory requirements favor established companies with proven safety records. The market dynamics are shifting towards value-added products and specialized applications, creating opportunities for companies with strong research and development capabilities. Companies are increasingly focusing on developing sustainable and traceable supply chains to meet growing consumer demands for transparency and environmental responsibility. The ability to maintain consistent quality while meeting stringent regulatory requirements has become a key differentiator in the market.

Companies are investing in automated handling systems and quality control technologies to reduce contamination risks and improve production efficiency. Successful manufacturers implement enclosed processing systems that comply with pharmaceutical manufacturing standards. The integration of advanced technologies has become crucial for maintaining a competitive advantage in the market. Market leaders are developing innovative solutions to address specific customer requirements and enhance operational efficiency. The focus on technological advancement and quality control measures continues to shape the competitive landscape of the liquid sugar market.

Liquid Sugar Industry Leaders

-

Cargill Inc

-

Archer Daniels Midland Company

-

Tate & Lyle Plc

-

Südzucker AG

-

ASR Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and modernization projects in 2026 point to whitespace for suppliers able to deliver reliable, industrial-scale liquid sugar and related syrup streams to beverage and food manufacturers with tighter processing and traceability requirements. Examples include Sucro Can Canada completing construction of a CAD 135 million sugar refinery at the Port of Hamilton in April 2026, and ASR Group starting the first phase of a nearly USD 800 million expansion at the Domino Sugar Chalmette Refinery in Louisiana in May 2026, both of which signal continued investment in North American refining infrastructure that can support expanded liquid sugar supply into regional manufacturing corridors.

Opportunities also track energy-efficient and regionally anchored refining builds that reduce delivered-cost volatility and support consistent liquid formulations for cold-processing and automated plants. In India, Shri Dutt India Private Limited completed an expansion at Kandla from 1,000 to 2,500 tonnes per day using process-efficiency technologies (Mechanical Vapour Recompression and Honeycomb Calandria Batch Pans). In Oman, the first sugar refinery at Sohar Port began phased commercial production in January 2026 with an annual capacity of one million tonnes, strengthening regional availability for industrial users. On the supply side, more formal raw sugar procurement to stabilize operations is also emerging, such as Sucro Limiteds March 2026 raw sugar supply agreement with HMC Farms LLC supporting its University Park, Illinois, refinery plan, which reinforces the value of long-term supply structures for liquid sugar producers serving high-throughput customers.

Recent Industry Developments

- May 2026: American Sugar Refining, Inc. (ASR Group) broke ground on the first phase of a USD 785 million modernization project at the Domino Sugar Chalmette Refinery in St. Bernard Parish, Louisiana. The initial phase exceeds USD 200 million and targets upgraded refining infrastructure that supports higher efficiency and reliability for industrial sugar and liquid sugar supply into North American food and beverage manufacturing.

- March 2025: Saraswati Sugar Mills (SSM) commenced production of invert liquid sugar, with the plant established by the Indian Sugar and General Engineering Corporation (ISGEC). The commissioning adds specialized liquid sugar capability in India and supports formulation demand in beverages, bakery, and confectionery where invert syrups are used for crystallization control and moisture management.

- February 2024: Sucro Ltd. announced plans to construct a cane sugar refinery in the greater Chicago area, including specialty liquid sugar production and organic refining capabilities alongside other specialty sugar lines. The project underscores continued investment in liquid sugar capacity close to large food and beverage end markets, reducing dependence on customer-side melting of crystalline sugar.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The liquid sugar market is defined as revenue earned from commercially sold sugar solutions, where sucrose is dissolved in water to a controlled concentration, and then supplied for use in food and beverage production and similar industrial uses.

Scope exclusions: It excludes dry granulated sugar, raw sugar, and alternative liquid sweeteners that are not sucrose-based sugar solutions.

Segmentation Overview

-

By Product Type

- Liquid Sucrose

- Invert Sugar Syrup

- Others

-

By Origin

- Organic

- Conventional

-

By Source

- Cane-based Sugar

- Beet-based Sugar

- Others

-

By Application

- Beverages

- Bakery

- Confectionery

- Baby Foods

- Pharmaceuticals

- Other Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public production and trade signals to map the supply base for sugar and syrups, then looks at how much is typically directed into industrial channels. Sources used for this foundation include USDA sugar statistics, FAOSTAT production series, UN Comtrade trade data, and national customs and agriculture ministry releases in major producing and consuming countries.

To link supply with demand, we also reviewed standards and reference notes from Codex Alimentarius and relevant food safety agencies, alongside peer-reviewed food science papers on syrup concentration and handling. Company annual reports, investor presentations, and reputable press coverage were then used to corroborate capacity moves, plant utilization commentary, and end-use demand signals. Where needed, paid subscriptions were used for company financials and intelligence, and patent databases plus shipment-level import and export checks were used for extra cross-checking. These sources are not exhaustive, and we relied on other public references for additional verification and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with sugar processors, ingredient distributors, and procurement or quality teams at large food and beverage users. Respondent input was used to confirm concentration ranges, typical contract and spot pricing behavior, and how often buyers shift between liquid and dry formats, which then helped tighten conversion factors and regional adoption assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 45% |

| Mid tier: 57% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 17% | Managers: 53% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where sugar processing output, trade flows, and industrial use indicators are reconstructed into a liquid sugar demand pool by region, and then expressed in value terms using observed pricing ranges. Results are then corroborated with selective bottom-up approximations, using sampled supplier volumes, distributor channel checks, and indicative ASP times volume for key applications to validate totals and adjust outliers.

Key inputs tracked in the model include refined sugar production trends, beverage and bakery output indicators, industrial sugar use shares, typical Brix or concentration ranges used in manufacturing, and price movements for refined sugar and liquid sugar contracts. When bottom-up checks have gaps, the missing pieces are filled through ratio-based allocation across applications and regions, based on interview-confirmed adoption patterns and practical logistics constraints.

Forecasting is carried out using scenario analysis supported by trend smoothing on the key drivers, since demand can move with food output cycles and sugar price changes. Assumptions on adoption and pricing progression are checked with expert consensus from interviews before finalizing the year-by-year outlook.

Data Validation & Update Cycle

Validation is done in layers, starting with unit consistency checks and conversion reviews, and then moving to variance checks against independent signals such as sugar production, imports, and downstream food and beverage output. If a region shows an unusual swing, we revisit the assumptions, re-check the source series, and where needed re-contact industry participants to understand whether the shift is structural or temporary.

Before sign-off, the model is reviewed by another analyst to confirm calculations, scope alignment, and whether key assumptions can be traced to a clear source or an interview input. The report is refreshed on an annual cycle, and material developments like major capacity additions, trade policy changes, or sharp price movements are incorporated through interim updates. Right before delivery, a final pass is done so clients receive the most current view available.

Mordor Intelligence's Liquid Sugar Market Size Measured Against Other Published Estimates

Published market values for liquid sugar can vary even when the same terms are used, because teams may count different product types, treat geography differently, or apply different price timing and conversion factors. In practice, the spread is usually linked to how liquid sugar is separated from adjacent sweeteners, plus whether pricing is taken from refined sugar benchmarks or from realized industrial syrup pricing.

The main gap comes from whether non-sucrose liquid sweeteners or broader industrial syrup families are included, where Mordor Intelligence counts only sucrose-based liquid sugar solutions priced to the industrial ingredient channel and then cross-checks the total with concentration assumptions and food and beverage output indicators.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 98.93 M (2026) | |

| Industry Publisher A | USD 85.80 M (2026) | Uses a narrower demand pool that emphasizes selected product variants and end uses, and can rely more on stated base-year values with limited evidence of price normalization across regions. |

| Industry Publisher B | USD 81.60 M (2024) | Anchors the estimate to an earlier year and may not fully normalize currency timing and industrial pricing progression, which can understate the current market when sugar prices and mix shift. |

Across the three figures, the differences mainly track back to what is counted as liquid sugar versus nearby syrup categories, and how price and year selection are handled. Keeping the scope tied to sucrose solution sales, and then validating it using production, trade, and end-use output checks, makes the market number easier to follow and repeat when the model is updated.

Key Questions Answered in the Report

What is the current size of the liquid sugar market and its growth outlook?

The liquid sugar market size is USD 98.93 million in 2026 and is projected to reach USD 120.24 million by 2031, yielding a 3.98% CAGR.

Which application segment leads demand for liquid sugar?

Beverages dominate with 45.23% 2025 share and maintain the fastest growth at a 5.91% CAGR through 2031, driven by ready-to-drink coffee, functional soda, and flavored water lines.

How fast is organic liquid sugar expanding compared with conventional grades?

Organic liquid sugar records a 7.48% CAGR for 2026-2031, more than double the overall market pace, as brand owners pursue clean-label certifications.

Which region shows the highest growth rate for liquid sugar?

Asia-Pacific leads with a 5.61% CAGR to 2031, propelled by expanding food-processing capacity and rising middle-class consumption.

Page last updated on: