Crystalline Fructose Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

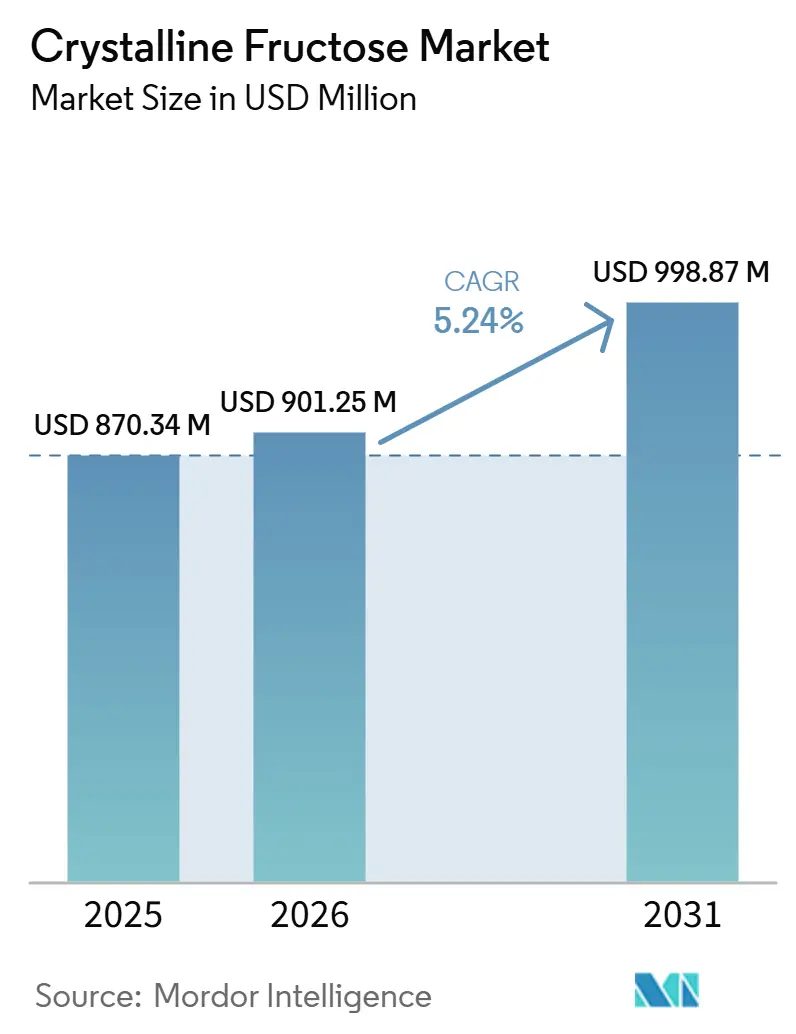

| Market Size (2026) | USD 901.25 Million |

| Market Size (2031) | USD 998.87 Million |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crystalline Fructose Market Analysis by Mordor Intelligence

The crystalline fructose market size is projected to be USD 870.34 million in 2025, USD 901.25 million in 2026, and reach USD 998.87 million by 2031, growing at a CAGR of 5.24% from 2026 to 2031. The crystalline fructose market is benefiting from product reformulation in food and beverage, where manufacturers are looking for sugar reduction without losing sweetness, mouthfeel, or label simplicity. The crystalline fructose market is also gaining support from pharmaceutical and nutraceutical demand, where high-purity ingredients are valued for taste masking, stability, and specification compliance. Export-oriented corn and sugar processing hubs are expanding the supply base, which is helping the crystalline fructose market serve both food-grade and higher-value applications. Competition is becoming more focused on solution selling, formulation support, and quality validation, rather than on bulk supply alone. At the same time, alternative sweeteners such as stevia, erythritol, and monk fruit are raising the need for differentiated positioning in clean-label, cold beverage, and premium formulation uses.

Key Report Takeaways

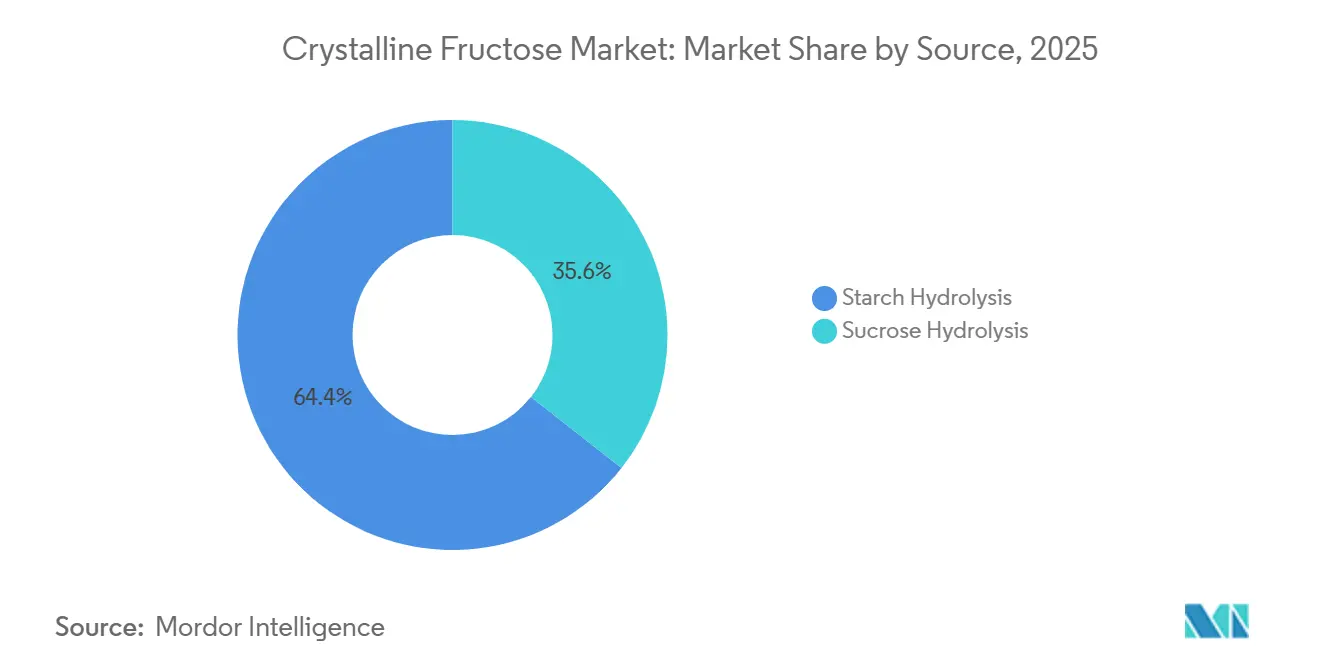

- By source, starch hydrolysis held 64.38% revenue share in 2025, while sucrose hydrolysis is forecast to expand at a 6.73% CAGR through 2031.

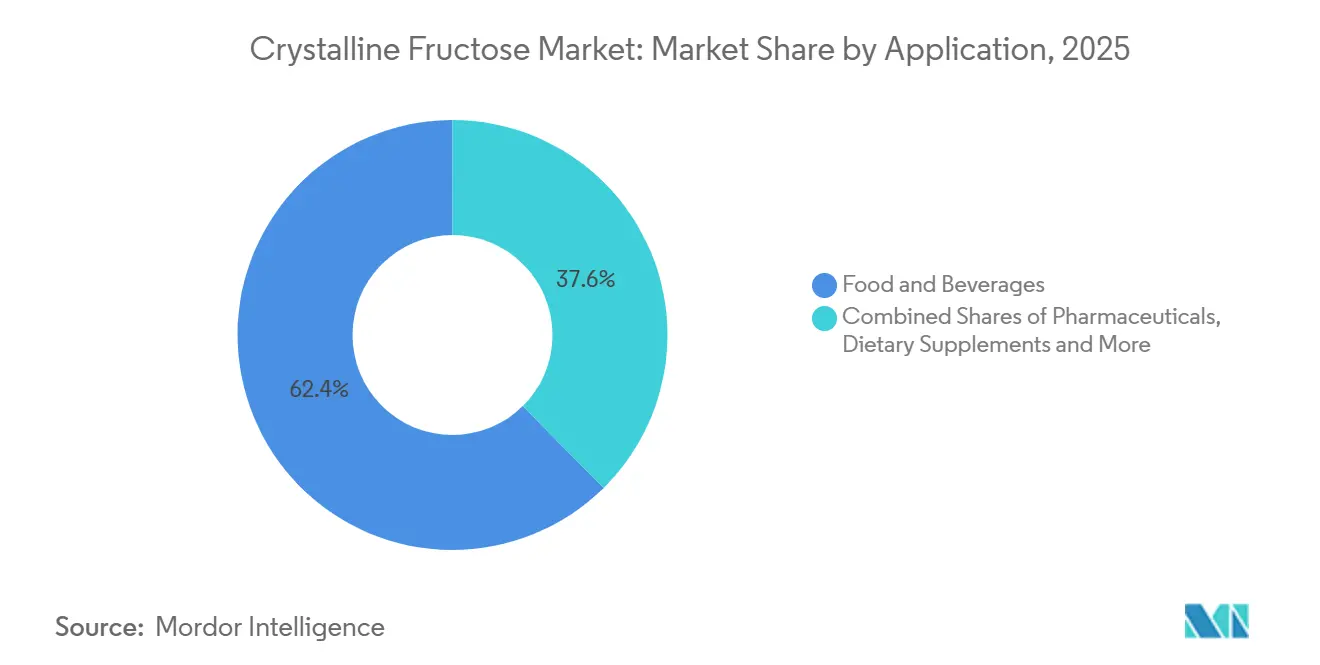

- By application, food and beverages accounted for 62.41% of revenue in 2025, while pharmaceuticals recorded the highest projected CAGR at 6.68% through 2031.

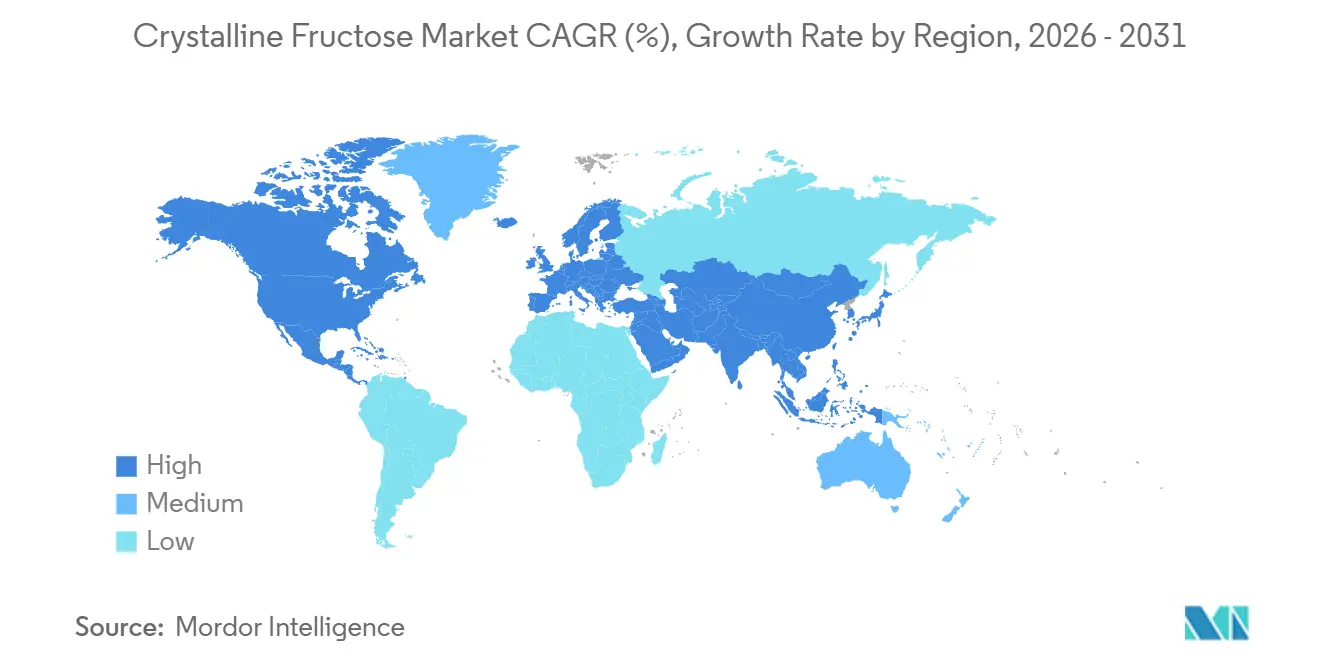

- By geography, Asia-Pacific held 32.48% of revenue in 2025, while Europe is advancing at a 6.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Crystalline Fructose Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-Calorie Sweetening Demand in Reformulated Foods | +1.30% | Global, led by North America and Europe | Medium term (2-4 years) |

| High-Purity Ingredient Demand in Nutraceutical and Pharmaceutical Formulations | +1.10% | Asia-Pacific, especially India and China, and North America | Long term (≥ 4 years) |

| Clean-Label Shift in Premium Beverage Formulations | +0.90% | Europe and North America, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Export-Led Growth From Corn and Sugar Processing Hubs | +0.70% | Asia-Pacific, with spillover into Middle East and Africa | Medium term (2-4 years) |

| Precision Crystallization and Enzymatic Yield Improvements | +0.50% | Global, concentrated in Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Co-Formulation Demand With Sugar Reduction Blends and Masking Systems | +0.40% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Low-Calorie Sweetening Systems in Reformulated Foods

Product reformulation has moved into routine sourcing decisions, and that shift is supporting the crystalline fructose market in packaged food and beverage. ADM reported in January 2026 that more than 80% of U.S. consumers preferred reformulated better-for-you products, and 83% of global consumers were reducing sugar intake, which is pushing manufacturers to revisit their sweetener systems. Crystalline fructose remains useful in these programs because Tate & Lyle states that its glycemic index is close to 15 compared with 65 for sucrose, while its sweetness efficiency can support a 20.00% to 30.00% reduction in sweetener mass in suitable formulations[1]Source: European Commission, “Regulation (EC) No 1924/2006 on Nutrition and Health Claims Made on Foods,” eur-lex.europa.eu. The crystalline fructose market is also helped by the fact that sweetness perception increases in colder and more acidic conditions, which gives formulators a practical tool in chilled beverages and functional drinks where some alternatives do not perform as well. That combination of reduced sugar load, technical performance, and easier claim support is making crystalline fructose a more relevant input for mid-tier manufacturers that do not want highly complex multi-sweetener systems.

Increase in Demand for High-Purity Ingredients in Nutraceutical and Pharmaceutical Formulations

The crystalline fructose market is gaining from the tighter quality needs of pharmaceutical and nutraceutical formulations. Pharmaceutical-grade supply depends on validated production, controlled impurity levels, and compliance with formal purity standards, which narrows the field of suppliers that can serve this demand. Ingredion announced in May 2026 that it partnered with Sanstar Limited and backed a greenfield specialty ingredient plant in India, a move aimed at pharmaceutical excipient and clean-label food demand. This matters because pediatric oral products, chewables, syrups, and dispersible formats need taste masking and consistent quality, and those needs support the use of crystalline fructose beyond ordinary food sweetening. The crystalline fructose market is therefore seeing demand that is less tied to short-term consumer cycles and more tied to specification-driven formulation work in regulated end uses.

Clean-Label Replacement of Artificial Sweeteners in Premium Beverage Formats

Premium beverage reformulation is increasingly centered on ingredient transparency, and that is creating room for the crystalline fructose market. Manufacturers moving away from acesulfame-K and sucralose still need sweetness balance, acid stability, and a cleaner taste curve, and Galam positions crystalline fructose as a practical option in those uses. Galam states that crystalline fructose can deliver 1.20 to 1.70 times the sweetness of sucrose depending on application conditions, and that when paired with sc-FOS it can support a 30.00% to 40.00% calorie reduction in flavored water and other low-pH beverages while preserving freezing-point depression, browning, and moisture retention. These functional benefits matter because clean-label beverage design depends on processing behavior as much as ingredient naming. The crystalline fructose market is also supported by Galam’s statements on regulatory acceptability for its beet sugar-derived pathway, which reduces adoption risk in tightly managed food applications.

Precision Crystallization and Enzymatic Yield Improvements

Process upgrades are improving efficiency, and that is strengthening the cost position of the crystalline fructose market over time. The draft shows that Chinese producers have been scaling capacity, and it also points to tighter process control as an important factor in improving yield, purity, and operating consistency. Xiwang reported in November 2025 that it completed targeted upgrades at its fructose factory, including packaging improvements and precision optimization of crystallization cooling parameters to improve crystal yield consistency and production continuity. The crystalline fructose market benefits from these changes because better yield stability can narrow the cost gap between standard food-grade material and higher-purity grades. Over time, that can make regulated and premium applications more accessible to producers that can combine scale with more disciplined crystallization control.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock Price Volatility Across Corn, Sugar Cane, and Sugar Beet Chains | -0.80% | Global, most acute in North America and Asia-Pacific | Medium term (2-4 years) |

| Competition From Stevia, Erythritol, Monk Fruit, and HFCS | -0.70% | Global, strongest in Europe and North America premium segments | Long term (≥ 4 years) |

| Energy-Intensive Refining, Drying, and Purification Economics | -0.40% | Global, with stronger impact in Europe | Long term (≥ 4 years) |

| Consumer Pushback on Fructose-Heavy Sweetener Perception | -0.30% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility in Corn, Sugar Cane, and Sugar Beet Supply Chains

Feedstock volatility remains a direct restraint on the crystalline fructose market because production economics are tied to agricultural cycles and competing end uses. The U.S. EPA’s 2026 and 2027 Renewable Fuel Standard supports corn use in ethanol, which can tighten starch availability for wet millers during high-demand periods and affect sweetener margins[2]Source: U.S. Environmental Protection Agency, “Renewable Fuel Standard Program Standards for 2026 and 2027,” epa.gov. The draft also shows that large producers are responding through vertical integration and plant modernization. ADM announced a USD 103 million modernization of its Decatur, Illinois operations in 2026, while Xiwang highlights its large annual corn processing base in Shandong, which helps both companies manage sourcing risk more effectively than smaller standalone producers. The crystalline fructose market therefore remains more exposed where suppliers lack long-term feedstock control or integrated processing systems.

Competition From Stevia, Erythritol, Monk Fruit, and High Fructose Corn Syrup

Competitive pressure is rising because alternatives are improving in taste, blend flexibility, and formulation economics, which affects the crystalline fructose market in mainstream food uses. Stevia, erythritol, and monk fruit blends are giving formulators more ways to cut sugar while managing taste, and that reduces dependence on a single bulk sweetener. High fructose corn syrup also remains a lower-cost option in industrial food production where label positioning carries less weight than sweetness cost. The response from major suppliers is moving into adjacent categories, as shown by Roquette’s July 2024 cooperation agreement with Bonumose to develop tagatose using enzymatic technology and starch processing expertise. That move shows that the crystalline fructose market is being defended not only through price and scale, but also through broader sweetener portfolio positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Starch Hydrolysis Anchors Scale While Sucrose Pathway Commands Premium

Starch hydrolysis accounted for 64.38% of revenue in 2025, giving it the leading position in the crystalline fructose market because of its long-established base in corn wet milling. The segment benefits from accumulated infrastructure in the U.S. Corn Belt and major Chinese starch clusters, where integrated milling and sweetener processing support scale economics. Xiwang states that its sugar business operates China’s first domestically developed large-scale corn fructose production line, processes 3 million tonnes of corn annually, and holds 5 pharmaceutical approval numbers, which shows how scale and product range can sit inside one production platform. The crystalline fructose industry continues to rely on this route for broad commercial supply because starch-based processing supports both food-grade output and the gradual move into higher-purity grades.

The sucrose hydrolysis route is forecast to expand at a 6.73% CAGR through 2031, making it the faster-growing pathway in the crystalline fructose market. This growth is tied to demand for non-GMO and beet sugar-derived material, especially in Europe and North America, where feedstock provenance carries commercial value beyond sweetness alone. Galam states that Fruitose® is produced from non-GMO European sugar beet and delivers purity of at least 99.50% on a dry-weight basis, which supports its use in premium food, supplement, and clean-label channels. Galam also renewed its Non-GMO Project certifications in March 2026, reinforcing the premium position of this route in channels where documentation and ingredient origin matter.

By Application: Food and Beverages Leads Volume, Pharmaceutical Premiumization Accelerates

Food and beverages held 62.41% of revenue in 2025, which means this segment accounted for the largest share of the crystalline fructose market size in that year. The segment spans beverages, bakery, dairy, confectionery, and sports nutrition, and its scale comes from both sweetness and multi-functional performance. Tate & Lyle states that crystalline fructose supports humectancy, browning, and freezing-point depression, while also performing strongly in low-temperature and acidic beverage systems. ADM’s January 2026 investment in Erlanger also highlighted its Less Sugars strategy, showing that supplier investment continues to follow food and beverage reformulation demand.

Pharmaceuticals is projected to expand at a 6.68% CAGR through 2031, which makes it the fastest-growing application in the crystalline fructose market. This segment is supported by generic drug growth, pediatric oral dosage formats, and the need for validated high-purity excipients that can meet tighter quality requirements. Galam’s nutraceutical material shows how crystalline fructose can also be paired with sc-FOS to deliver both sweetening and prebiotic functionality, which raises the value of formulation-ready systems over commodity supply alone. The crystalline fructose industry is therefore seeing a clearer split between high-volume food use and smaller but more protected regulated use, with dietary supplements and personal care adding further diversity to the demand base.

Geography Analysis

Asia-Pacific held 32.48% of revenue in 2025, which gave the region the largest share of the crystalline fructose market. China anchors that position through deep starch processing capacity and integrated corn-based production, while India is becoming more relevant through pharmaceutical and specialty ingredient demand. Xiwang states that it processes 3 million tonnes of corn annually and holds the leading domestic position in Chinese crystalline fructose capacity, output, and share, which highlights the scale available in the region. The crystalline fructose market in Asia-Pacific also benefits from a wider mix of end uses, including food reformulation, functional products, and ingredient exports. India is becoming a more important demand node because Ingredion’s May 2026 partnership with Sanstar directly targets pharmaceutical excipient and clean-label ingredient needs in the country.

North America remained the second-largest regional market in the crystalline fructose market, supported by the depth of corn wet milling infrastructure in the United States. ADM’s Decatur complex is undergoing USD 103 million in modernization in 2026, which strengthens an already important sweetener supply base for domestic and export demand[3]Source: Office of the Governor of Illinois, “Gov. Pritzker Announces ADM to Invest USD 103 Million to Modernize Decatur Operations,” gov-pritzker-newsroom.prezly.com. Tate & Lyle’s Lafayette, Indiana facility has also long been a reference point for North American food-grade and industrial crystalline fructose supply. The crystalline fructose market in the region continues to benefit from reformulation work in beverages, dairy, and broader processed food categories.

Europe is projected to expand at a 6.57% CAGR through 2031, making it the fastest-growing regional part of the crystalline fructose market size in the forecast period. The region’s growth comes from demand for natural, non-GMO, and transparent sweetener positioning in food and beverage labels. EU rules on nutrition and health claims support reduced-sugar product development, and the mass reduction advantage of crystalline fructose can fit that direction in suitable applications. Galam’s beet sugar-derived product line is well aligned with this environment because provenance and documentation are important in premium European channels.

Competitive Landscape

The crystalline fructose market is concentrated among a small group of producers because the business requires integrated feedstock access, specialized processing, and quality validation for higher-value uses. Large companies compete on more than basic sweetener output, since customers increasingly expect application support, reformulation advice, and reliable documentation. ADM and Cargill have an advantage in cost control because their models are tied to broad corn origination and wet milling systems, while Tate & Lyle has remained relevant through application-focused product positioning in specialty sweeteners. The crystalline fructose market is therefore shaped by a mix of scale, process control, and customer-facing technical support. That keeps barriers high for smaller firms that can distribute product but cannot validate performance across food, supplement, and pharmaceutical uses.

Recent strategic moves show how leading companies are protecting position in the crystalline fructose market through plant investment and application expansion. ADM invested USD 26 million in Erlanger in January 2026 to strengthen reformulation capabilities, and it also announced USD 103 million in Decatur modernization in 2026, linking customer-facing development with core processing infrastructure. Ingredion’s May 2026 partnership with Sanstar shows another route, which is to build closer access to pharmaceutical and specialty food demand in India. Galam has stayed differentiated by pairing beet sugar-derived crystalline fructose with clean-label positioning and documentation such as Non-GMO Project renewal.

White space in the crystalline fructose market remains strongest in premium non-GMO supply, pharmaceutical-grade production in Asia-Pacific, and co-formulated systems that combine sweetening with digestive or masking functionality. Galam’s product mix shows how suppliers can create a stronger position by linking crystalline fructose to broader formulation systems instead of selling it only as a standalone sweetener. Chinese producers such as Xiwang have strong scale in food-grade output, but wider access to regulated export channels still depends on validation, documentation, and product consistency. Roquette’s work with Bonumose on tagatose also shows that some leading players are preparing for a future where adjacent monosaccharides compete more directly with the crystalline fructose market in selected applications.

Crystalline Fructose Industry Leaders

Archer Daniels Midland Company

Tate & Lyle Plc

Ingredion Incorporated

Cargill, Incorporated

Galam Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Ingredion Incorporated announced a joint venture with Sanstar Limited, India's leading corn-based specialty products manufacturer, along with a 9% equity investment. The agreement commissions a greenfield specialty pharmaceutical and food ingredient plant in India, combining Sanstar's local corn-processing infrastructure with Ingredion's global formulation expertise to serve pharmaceutical excipient and clean-label food markets.

- March 2026: ADM announced a USD 103 million investment to modernize its flagship corn processing complex in Decatur, Illinois, one of the world's largest corn wet mills, creating 50 new full-time jobs and retaining over 1,000, supported by the Illinois EDGE economic development program. The investment strengthens the facility's position as a starch sweetener supply anchor for North American and export markets.

Global Crystalline Fructose Market Report Scope

| Starch Hydrolysis |

| Sucrose Hydrolysis |

| Food and Beverages |

| Pharmaceuticals |

| Dietary Supplements |

| Personal Care and Cosmetics |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| Source | Starch Hydrolysis | |

| Sucrose Hydrolysis | ||

| Application | Food and Beverages | |

| Pharmaceuticals | ||

| Dietary Supplements | ||

| Personal Care and Cosmetics | ||

| Other Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current market size of Crystalline Fructose Market?

The market was valued at USD 870.34 million in 2025 and expands to USD 901.25 million in 2026, with a trajectory toward USD 998.87 million by 2031 at a 5.24% CAGR.

What is driving demand for crystalline fructose in food and beverages?

Food and beverages held 62.41% of revenue in 2025, and demand is being supported by sugar reduction programs, cold beverage performance, and functional benefits such as humectancy and browning.

Why is pharmaceuticals the fastest-growing application for crystalline fructose?

Pharmaceuticals is forecast to grow at a 6.68% CAGR through 2031 because high-purity excipients are needed for pediatric oral products, generic formulations, and specification-driven regulated uses.

Why is Europe growing faster than other regions?

Europe is projected to expand at a 6.57% CAGR through 2031 because natural, non-GMO, and reduced-sugar positioning fits both consumer demand and label claim rules.

Page last updated on: