Superfoods Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

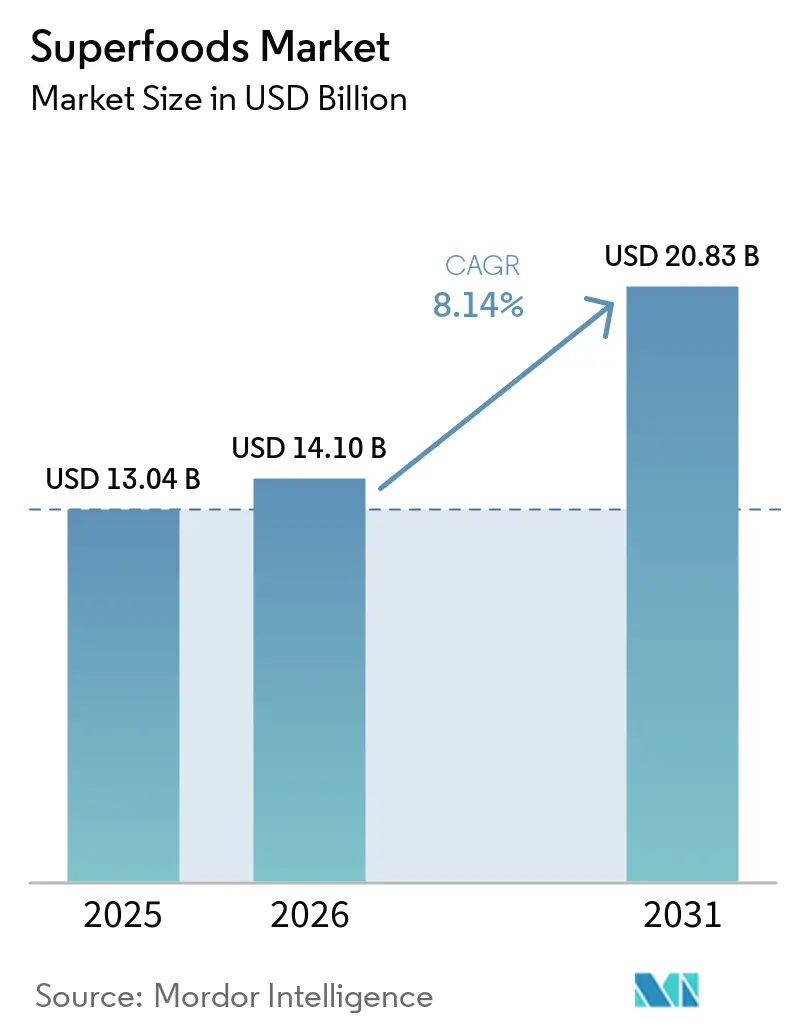

| Market Size (2026) | USD 14.10 Billion |

| Market Size (2031) | USD 20.83 Billion |

| Growth Rate (2026 - 2031) | 8.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Superfoods Market Analysis by Mordor Intelligence

The superfoods market size was valued at USD 13.04 billion in 2025 and is estimated to grow from USD 14.1 billion in 2026 to reach USD 20.83 billion by 2031, at a CAGR of 8.14% during the forecast period (2026-2031). This growth trajectory reflects fundamental shifts in consumer behavior toward preventive healthcare and nutrient-dense foods, supported by the wider adoption of functional ingredients across everyday diets and increasing consumer focus on proactive nutrition. The market's resilience stems from its ability to capitalize on multiple demographic trends, including aging populations seeking longevity solutions and younger consumers prioritizing wellness over traditional convenience, a trend reshaping the global superfoods market. Macro forces reshaping the superfoods landscape include regulatory modernization, with the FDA's updated "healthy" claim definition, allowing nutrient-dense foods like avocados, nuts, and salmon to qualify for health labeling [1]Source: Food and Drug Administration, “Food Labeling: Nutrient Content Claims,” fda.gov.

Key Report Takeaways

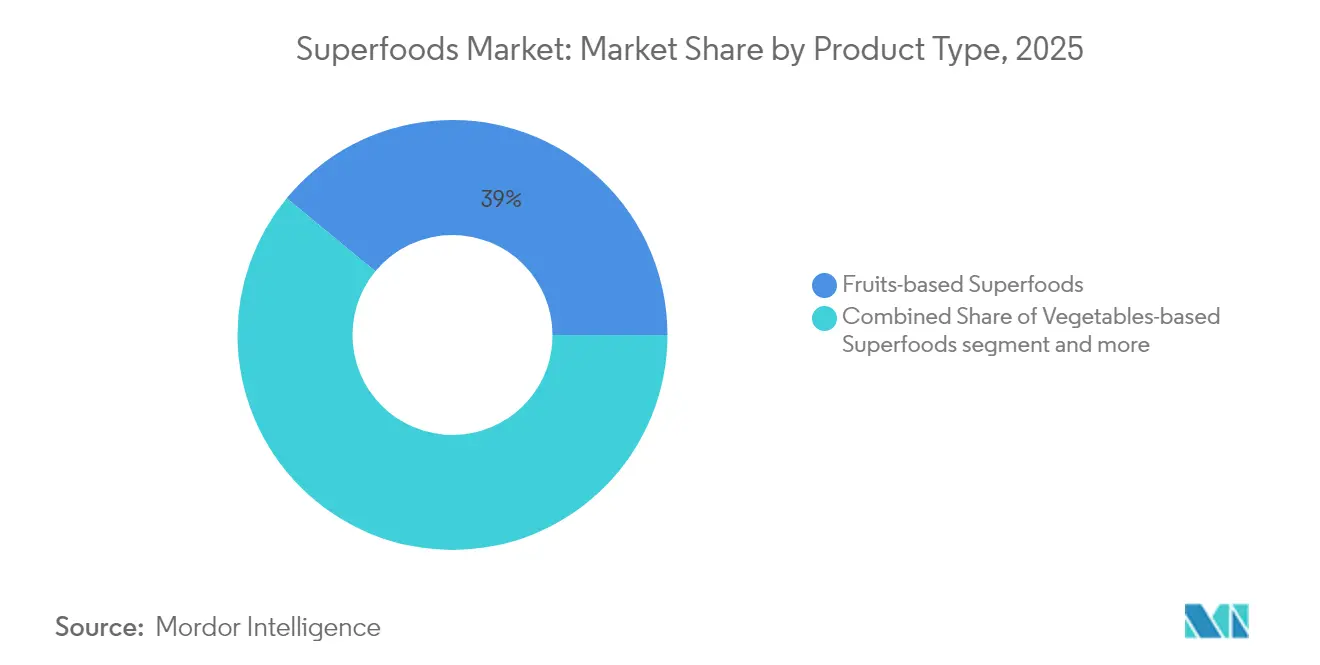

- By product type, fruit-based superfoods led with a 39.02% 2025 revenue share, while algae-based superfoods are projected to expand at a 10.33% CAGR through 2031.

- By form, powders captured 42.01% of the 2025 revenue share, and liquids are the fastest riser at a 9.66% CAGR to 2031.

- By nature, conventional products held 57.55% in 2025; organic lines outpace with an 11.49% CAGR for 2026-2031.

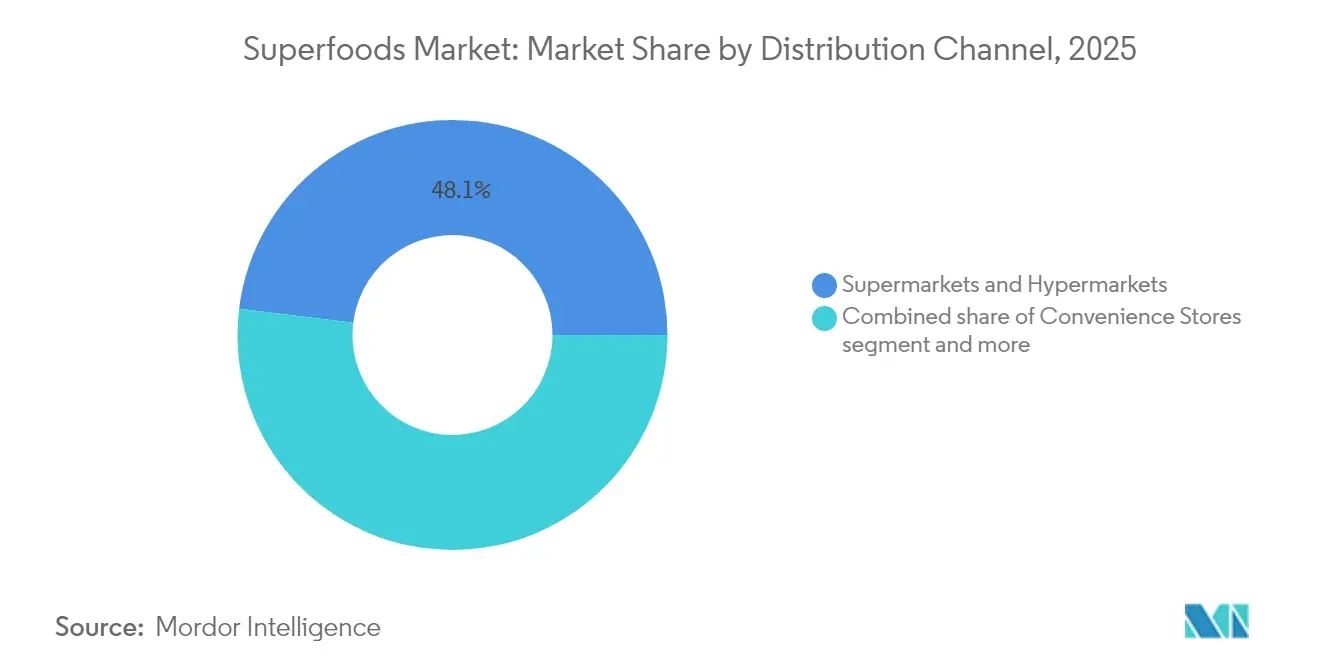

- By distribution channel, supermarkets retained 48.05% of 2025 sales; online platforms are set to grow at a 12.61% CAGR within the Superfoods market.

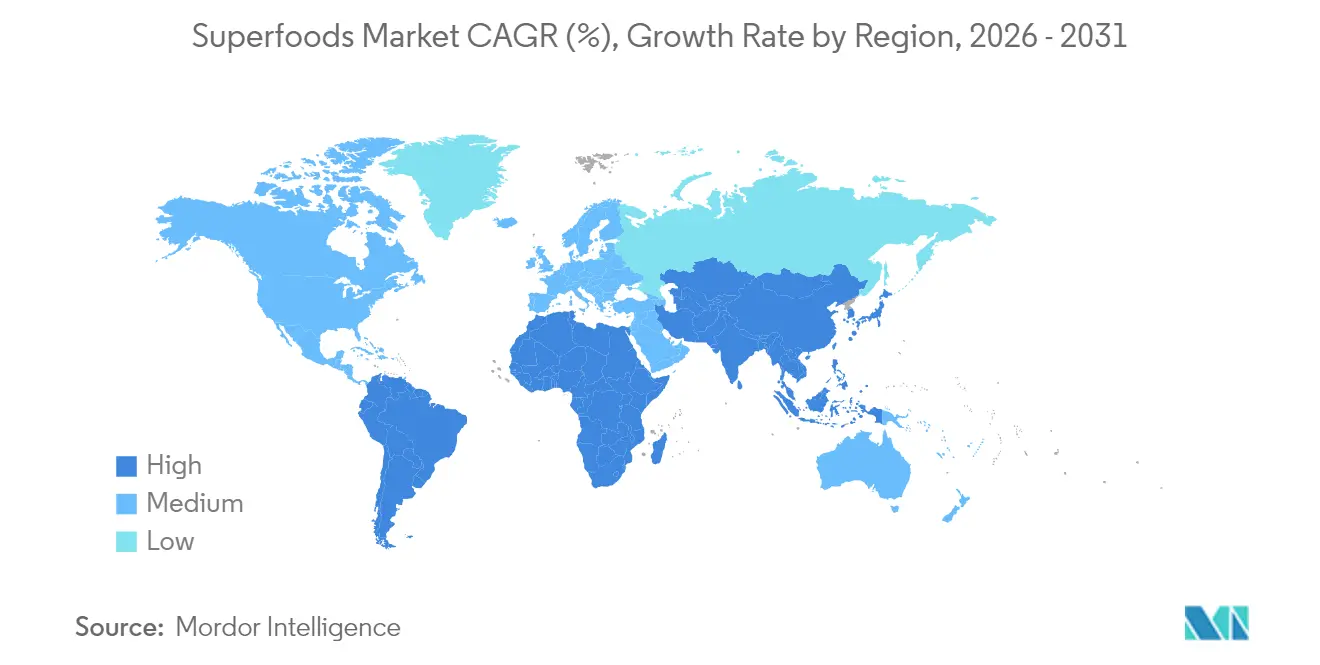

- By geography, North America commanded 43.62% of 2025 global sales, whereas Asia-Pacific is on course for a 10.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Superfoods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevating Health Consciousness Among Consumers | +1.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Expanding Demand for Nutrient-Dense Superfoods | +1.5% | Global, particularly Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Surging Popularity of Plant-Based and Vegan Diets | +1.2% | North America, Europe, urban Asia-Pacific centers | Medium term (2-4 years) |

| Increasing Demand for Preventive Healthcare Solutions | +1.1% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Accelerating Demand for Functional Foods | +0.9% | Global, strongest in North America & Europe | Short term (≤ 2 years) |

| Widening Accessibility of Superfoods in Emerging Markets | +0.7% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevating Health Consciousness Among Consumers

Consumer health awareness has increased significantly, with over 95% of households purchasing organic products in 2024 [2]Source: Organic Trade Association, “2025 Industry Survey,” naturallynetwork.org. This trend has expanded food purchasing decisions beyond price and quality considerations, as consumers increasingly prioritize nutritional value and health impact. Consumers now demonstrate greater nutritional knowledge through detailed label reading, ingredient verification, and research into food production methods, which directly influences their buying patterns. They are willing to pay higher prices for products with proven health benefits, particularly those supported by scientific research and transparent sourcing. The consumption of superfoods has become associated with lifestyle choices and personal values, reflecting a broader shift in how people view food's role in their overall well-being. Many consumers now integrate superfoods into their daily diets, viewing them as essential components of preventive health care rather than luxury items within the superfoods market. This growing health consciousness has particularly benefited algae-based superfoods, as consumers' understanding of their comprehensive nutritional profile - including high protein content, essential fatty acids, and micronutrients - helps overcome initial resistance to taste and texture. The increased awareness of algae's sustainability benefits and minimal environmental impact has further strengthened its market position among environmentally conscious consumers in the global superfoods market.

Expanding Demand for Nutrient-Dense Superfoods

Nutrient density has emerged as the primary value proposition distinguishing superfoods from conventional alternatives, with consumers increasingly seeking maximum nutritional return per calorie consumed. Scientific validation of bioactive compounds in foods like spirulina, which contains 60-70% protein alongside essential fatty acids and antioxidants, provides evidence-based justification for premium pricing. Technological advances in extraction and processing enable manufacturers to concentrate and preserve bioactive compounds, creating products with measurably superior nutritional profiles. This trend particularly benefits microalgae-based products, where innovations in fermentation and extraction can enhance insulin sensitivity and glucose regulation properties. The demand extends beyond individual nutrients to encompass synergistic compound interactions, driving research into optimal superfood combinations and processing methods across the superfoods market.

Surging Popularity of Plant-Based and Vegan Diets

Plant-based diet adoption has transcended niche markets to become a mainstream dietary pattern, with over 75% of consumers valuing food seasonality and local plant sources according to the 2025 trends analysis [3]Source: BIOFACH, “Global Plant-Based Market Trends 2025,” biofach.de. This shift creates sustained demand for plant-derived superfoods that provide complete amino acid profiles and essential nutrients traditionally sourced from animal products. The movement gains momentum from environmental sustainability concerns, where plant-based superfoods offer lower carbon footprints compared to animal-derived alternatives. Technological innovations enable plant-based alternatives to achieve sensory parity with traditional foods, exemplified by AlgaeCore Technologies' spirulina-based salmon alternative, which achieves 74% protein content while mimicking traditional seafood texture. The trend particularly benefits algae-based and seed-based superfoods, which provide concentrated nutrition in formats compatible with diverse dietary preferences, fueling growth in the superfoods market.

Increasing Demand for Preventive Healthcare Solutions

Healthcare cost escalation drives consumer investment in preventive nutrition, with Asian markets demonstrating particular receptivity to foods positioned as health maintenance tools rather than mere sustenance. The aging population demographic in Asia creates sustained demand for foods supporting healthy aging and cognitive function. Functional ingredients like magnesium and lion's mane mushroom are gaining prominence as consumers seek targeted nutritional interventions for specific health concerns. This preventive approach particularly benefits superfoods with documented bioactive properties, where scientific research supports specific health claims. The integration of technology enables personalized nutrition approaches, where consumers can select superfoods based on individual health profiles and genetic predispositions, a rising trend in the superfoods market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Premium Superfoods Limiting Adoption | -1.4% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) |

| Competition from Affordable Conventional Foods | -1.1% | Global, strongest in developing economies | Medium term (2-4 years) |

| Seasonal Supply Constraints of Certain Superfoods | -0.8% | Global, with regional variations by crop type | Medium term (2-4 years) |

| Preservation Challenges of Perishable Superfoods | -0.6% | Global, particularly tropical and subtropical regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium Superfoods Limiting Adoption

Premium pricing remains the primary barrier to mass market penetration, with superfoods commanding price premiums of 200-400% over conventional alternatives, limiting accessibility for price-sensitive consumer segments. Consumer research indicates high price sensitivity, with buyers frequently switching brands for discounts, demonstrating that premium positioning creates vulnerability to economic downturns [4]Source: Organic Trade Association, “2025 Industry Survey,” naturallynetwork.org. The cost structure reflects multiple factors, including specialized cultivation requirements, limited production scales, and complex supply chains requiring cold storage and rapid transportation. However, technological innovations in production and processing offer pathways to cost reduction, with companies like Brevel launching commercial-scale microalgae protein facilities capable of producing hundreds of tons annually at improved cost efficiency. Scale economies in emerging markets, particularly Asia-Pacific, where local production reduces transportation costs and import duties, create opportunities for price optimization. The challenge intensifies as inflation affects healthy eating choices, requiring strategic positioning to maintain accessibility while preserving premium brand equity in the competitive superfoods market.

Seasonal Supply Constraints of Certain Superfoods

Seasonal availability creates supply-demand imbalances that drive price volatility and limit consistent market access, particularly affecting fresh superfoods dependent on specific growing conditions and harvest windows. Climate change exacerbates these constraints through unpredictable weather patterns affecting crop yields and quality, while geographic concentration of production creates vulnerability to regional disruptions. The perishable nature of many superfoods compounds seasonal challenges, requiring sophisticated cold chain logistics and rapid distribution networks to maintain quality and nutritional integrity. However, technological solutions, including controlled environment agriculture and year-round cultivation methods, offer mitigation strategies, while preservation technologies like freeze-drying enable seasonal products to maintain nutritional value throughout the year. Supply chain diversification across multiple geographic regions reduces dependency on single-source suppliers, though this approach requires significant coordination and quality standardization efforts. The development of shelf-stable superfood formats through advanced processing technologies provides alternative product forms that overcome seasonal limitations while maintaining nutritional benefits within the broader Superfoods market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Algae Innovation Drives Future Growth

In 2025, fruit-based superfoods command a dominant 39.02% market share, underscoring consumer familiarity and robust distribution networks for staples like goji berries, açaí, and pomegranate extracts. Meanwhile, algae-based superfoods are making waves as the fastest-growing segment, boasting a 10.33% CAGR projected through 2031. This surge is fueled by technological advancements in cultivation and processing, paving the way for scalable production. Vegetable-based superfoods, represented by kale chips and spirulina powders, hold a notable market presence. At the same time, grains and seed-based superfoods, such as quinoa, chia, and flaxseeds, ride the wave of rising plant-based diet trends and an increasing demand for protein.

The rapid growth of the algae segment is bolstered by scientific endorsements of their nutritional advantages. For instance, spirulina is lauded for its complete amino acid profile, while chlorella is recognized for its concentrated, bioavailable vitamins and minerals. The commercial landscape is evolving, with companies like Brevel spearheading dedicated microalgae protein facilities, underscoring the industrial scalability of what were once considered niche products. Moreover, innovation is pushing boundaries; AlgaeCore Technologies is pioneering spirulina-infused seafood alternatives, boasting an impressive 74% protein content, thus broadening the horizons of algae applications beyond their conventional powder forms in the evolving superfoods market.

By Form: Liquid Formats Gain Momentum

Powder formats dominate with 42.01% market share in 2025, benefiting from extended shelf life, concentrated nutrition, and versatile application in smoothies, baking, and meal preparation. Liquid superfoods accelerate at 9.66% CAGR through 2031, driven by convenience preferences and ready-to-consume product demand among time-constrained consumers. Other formats, including capsules, bars, and whole foods, maintain steady growth through specialized applications and consumer preference diversity.

The liquid segment's growth reflects evolving consumption patterns where convenience intersects with nutrition, particularly in functional beverages and ready-to-drink superfood blends. Technological advances in liquid preservation and packaging enable extended shelf life without compromising nutritional integrity, while cold-pressed and flash-pasteurization techniques maintain bioactive compound potency. Innovation in liquid formats includes probiotic-enhanced superfood drinks and adaptogenic beverages targeting specific health outcomes, expanding beyond traditional juice-based products to encompass sophisticated functional formulations driving adoption in the superfoods market.

By Nature: Organic Certification Drives Premium Growth

Conventional superfoods hold 57.55% market share in 2025, reflecting broader market accessibility and established supply chains, while organic variants accelerate at 11.49% CAGR through 2031, significantly outpacing conventional alternatives. This growth differential reflects consumer willingness to pay premiums for certified organic products. Organic certification provides quality assurance and environmental sustainability credentials that resonate with health-conscious consumers seeking transparency in food production.

The organic segment benefits from expanding certification frameworks, including new USDA standards for organic mushroom production and pet food handling, broadening the scope of products eligible for organic labeling. The premium pricing of organic superfoods creates margin opportunities for producers while establishing quality differentiation in increasingly competitive markets across the Superfoods market.

By Distribution Channel: E-commerce Transformation Accelerates

Supermarkets and hypermarkets maintain 48.05% market share in 2025 through established consumer relationships and broad product accessibility, while online channels emerge as the fastest-growing segment at 12.61% CAGR through 2031. This digital acceleration reflects fundamental shifts in consumer shopping behavior, where health-conscious buyers seek specialized products and detailed nutritional information available through e-commerce platforms. Convenience stores and specialty stores maintain niche positions serving immediate consumption needs and expert consultation, respectively.

E-commerce growth benefits from enhanced consumer education capabilities, where online platforms provide detailed product information, nutritional data, and user reviews that support informed purchasing decisions for premium-priced superfoods. The COVID-19 pandemic permanently altered shopping patterns, with significant increases in online food purchasing across Asia-Pacific markets creating sustained demand for digital channels. Direct-to-consumer models enable superfood brands to maintain premium positioning while building customer relationships through subscription services and personalized nutrition recommendations within the superfoods market.

Geography Analysis

North America continues to dominate the global superfood market, holding a significant 43.62% share in 2025. This leadership is underpinned by a combination of high health awareness among consumers, robust purchasing power, and well-established distribution networks that ensure product availability. The region's mature market environment and consumer preference for health-oriented products further solidify its position as a key player in the superfood industry.

The Asia-Pacific region emerges as the fastest-growing segment in the superfood market, with a projected CAGR of 10.16% through 2031. This growth is driven by a rising middle-class population, increasing health consciousness, and proactive government initiatives aimed at promoting functional foods to combat noncommunicable diseases. Demographic transitions, such as urbanization, higher disposable incomes, and aging populations seeking health-supporting nutrition, further contribute to the region's rapid expansion. Additionally, the cultural familiarity with traditional functional foods provides a strong foundation for the adoption of modern superfoods, while younger consumers increasingly embrace dietary supplements and superfoods as part of their daily routines, a trend accelerating across the superfoods industry.

Emerging markets, including South America, the Middle East, and Africa, are gradually adopting superfoods, driven by urbanization and growing health awareness. These regions present significant long-term growth opportunities as economic development progresses and consumer health consciousness evolves. Locally-sourced superfoods, which leverage indigenous nutritional traditions while adhering to modern quality and safety standards, are particularly well-positioned to capture market share in these areas. As these markets mature, they are expected to play an increasingly important role in the global superfood industry.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

The superfoods market remains relatively fragmented, offering opportunities for both well-established food companies and emerging niche brands to establish their presence. This dynamic environment allows businesses to differentiate themselves through unique positioning strategies within the superfoods industry. Leading players in the market, such as Navitas Organics, Sunfood Superfoods, Nature’s Superfoods LLP, and OMG Superfoods, are actively leveraging advancements in technology. For instance, innovations like isochoric freezing are being utilized to enhance food preservation and processing efficiency, reduce energy consumption, and retain nutritional value, ensuring high-quality offerings for consumers.

Technological advancements are playing a transformative role in shaping the superfoods market. Companies are increasingly adopting artificial intelligence to create personalized nutrition solutions, tailoring products to meet the specific needs of individual consumers. The rapid growth of e-commerce and direct-to-consumer business models has further revolutionized the market, enabling brands to connect with a wider audience and respond swiftly to shifting consumer preferences. Additionally, the competitive landscape is becoming more dynamic with strategic initiatives such as partnerships, acquisitions—such as Chobani’s acquisition of Daily Harvest—and a strong emphasis on research and development to drive innovation and growth.

Personalized nutrition represents a significant growth opportunity in the superfoods market, as companies explore the use of genetic data and health metrics to develop customized superfood blends tailored to individual health requirements driving innovation in the superfoods industry. At the same time, new entrants are driving innovation by exploring alternative protein sources and advanced processing techniques. For example, AlgaeCore Technologies is focusing on the development of spirulina-based seafood substitutes, while Brevel is making notable progress with its large-scale microalgae protein production systems. These advancements highlight the market's potential for innovation and its ability to address evolving consumer demands throughout the Superfoods industry.

Superfoods Industry Leaders

Navitas Organics

Sunfood Superfoods

OMG Superfoods

Glanbia PLC

Nature’s Superfoods LLP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Chobani acquired Daily Harvest to enter the ready-to-eat superfood meals Industry, responding to growing consumer demand for healthy, convenient food options.

- April 2025: AlgaeCore Technologies commercialized its spirulina-based seafood alternative, achieving 74% protein content, securing USD 19 million in seed funding plus USD 4 million from Israel Innovation Authority for global market expansion.

- June 2024: Brevel Ltd. opened its first commercial microalgae protein facility in Israel, covering 27,000 sq. ft. and capable of producing hundreds of tons of chlorella-derived protein powder for global food manufacturers.

Global Superfoods Market Report Scope

Superfoods are nutrient-dense foods that are rich in nutrients, antioxidants, probiotics, fiber, and other health-promoting compounds that offer numerous health benefits beyond basic nutrition.

The market is segmented by type, distribution channel, and geography. By type, the market is segmented into fruits, vegetables, grains and seeds, herbs and roots, and other types. By distribution channel, the market studied is segmented into hypermarkets/supermarkets, online channels, convenience stores/traditional grocery stores, and other distribution channels. The report also analyzes the market in emerging and established regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. Market sizing and forecasts have been conducted for each segment, measured in terms of value (USD).

| Fruits-based Superfoods |

| Vegetables-based Superfoods |

| Grains and Seeds-based Superfoods |

| Algae-based Superfoods |

| Others |

| Powder |

| Liquid |

| Others |

| Conventional |

| Organic |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Channels |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Fruits-based Superfoods | |

| Vegetables-based Superfoods | ||

| Grains and Seeds-based Superfoods | ||

| Algae-based Superfoods | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Nature | Conventional | |

| Organic | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Channels | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the superfoods market?

The superfoods market size reached USD 14.1 billion in 2026 and is projected to reach USD 20.83 billion by 2031 at an 8.14% CAGR.

Which product category is growing the fastest?

Algae-based superfoods are forecast to post the highest growth, advancing at a 10.33% CAGR through 2031.

Why is Asia-Pacific considered the growth engine for superfoods?

Rising middle-class income, government support for nutraceuticals, and rapid e-commerce adoption are propelling Asia-Pacific at a 10.16% CAGR.

Which distribution channel will gain the most share by 2031?

Online platforms are set to grow at a 12.61% CAGR, reflecting consumer preference for direct-to-consumer convenience and detailed product information.

Page last updated on: