Sorbitol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

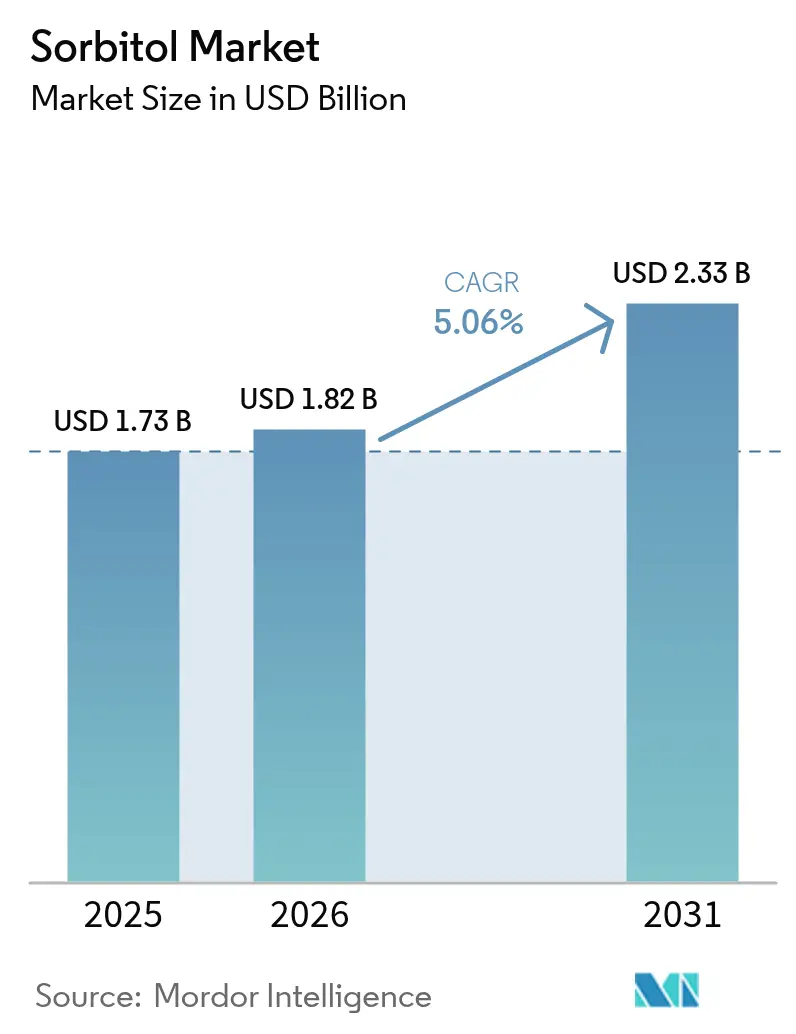

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.33 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

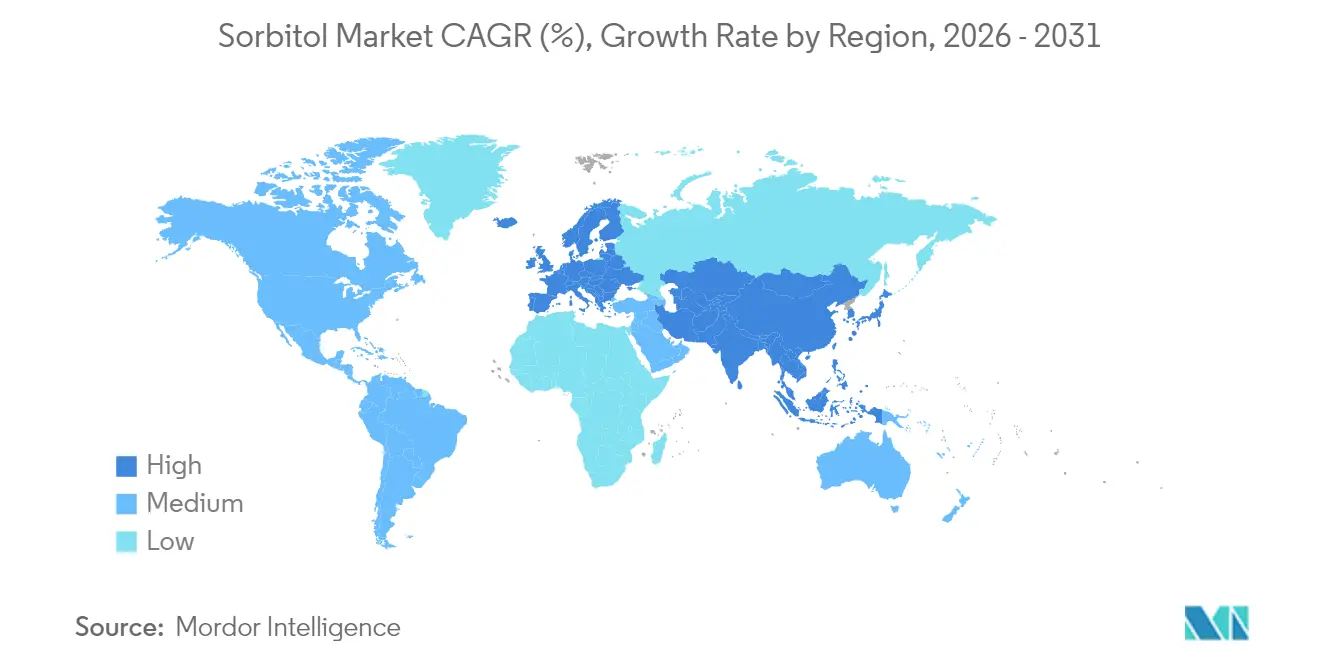

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

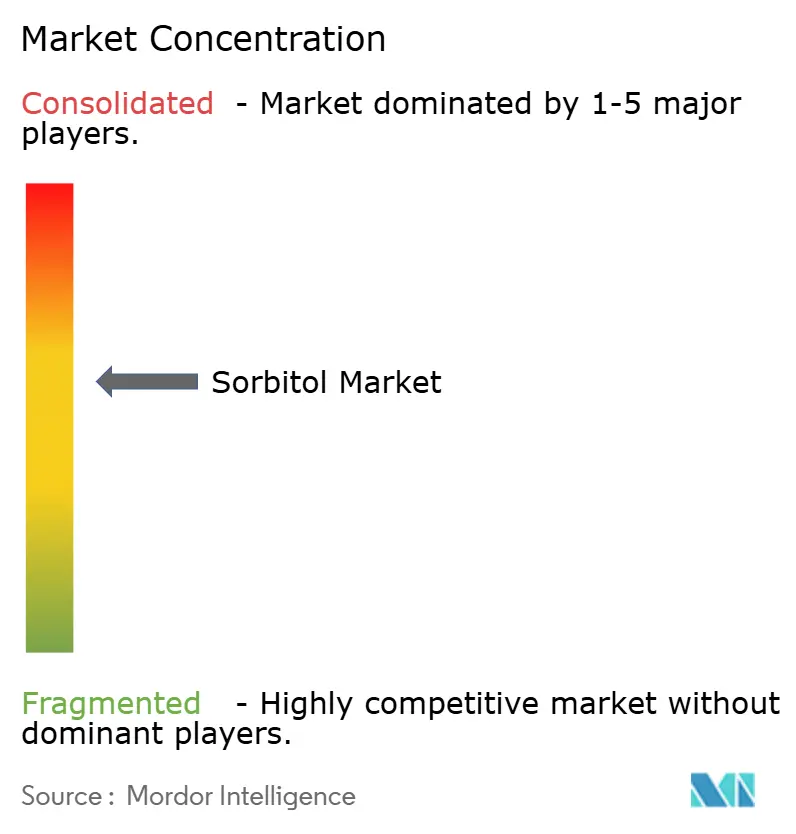

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sorbitol Market Analysis by Mordor Intelligence

Sorbitol market size in 2026 is estimated at USD 1.82 billion, growing from 2025 value of USD 1.73 billion with 2031 projections showing USD 2.33 billion, growing at 5.06% CAGR over 2026-2031. Growth rests on sorbitol’s dual role as sweetener and humectant, which lets manufacturers cut sugar content while preserving product moisture, a balance now demanded by regulators and consumers alike. Strong demand also comes from vitamin C synthesis, tablet excipients, and clean-label food and drink. Cost‐efficient production in Asia-Pacific, emerging biorefinery investments in South America, and rising deployment in premium personal care have diversified revenue streams and buffered price swings. At the same time, supply chains are adapting to corn price volatility by trialing sugarcane and cassava feedstocks, helping to maintain margins as biofuel policies tighten corn availability. Medium-term growth opportunities now cluster in value-added pharmaceutical grades, moisture-retentive cosmetics, and shelf-stable functional foods that can travel without cold-chain logistics.

Key Report Takeaways

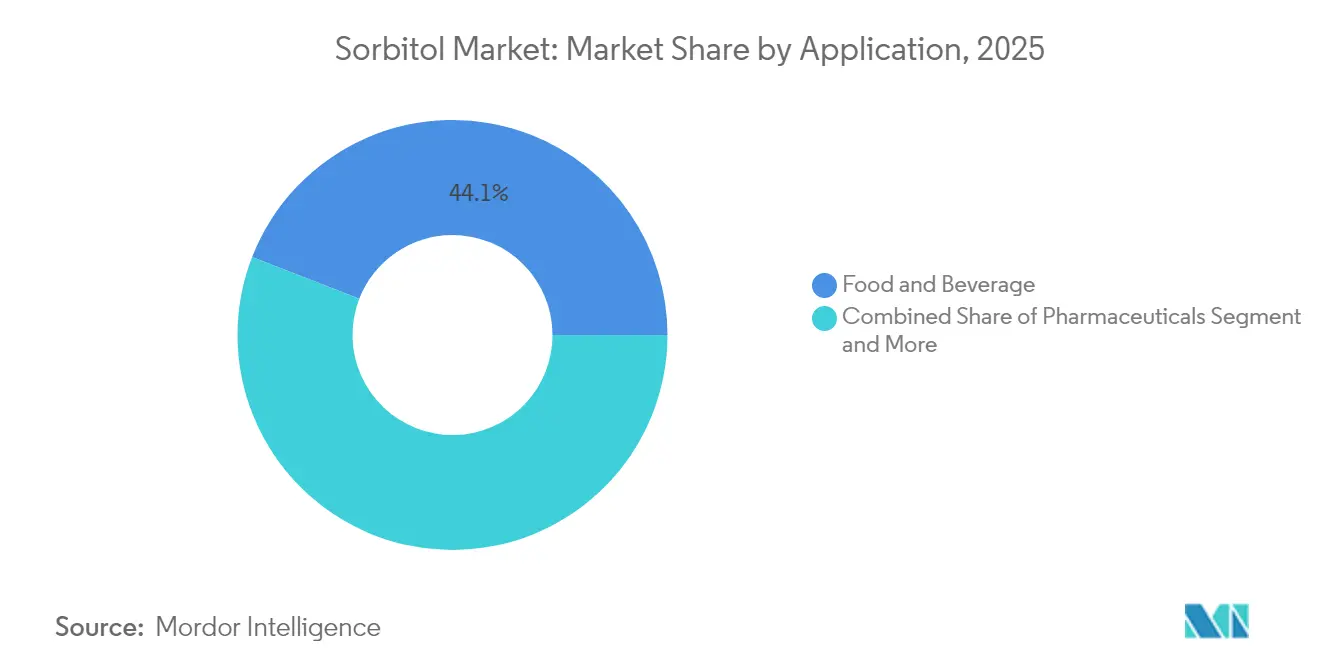

- By product type, liquid sorbitol led with 75.12% of the sorbitol market share in 2025, while powder/crystal forms are on track for a 6.45% CAGR through 2031.

- By application, food and beverage held 44.10% of the sorbitol market size in 2025; dietary supplements are projected to expand at a 6.74% CAGR to 2031.

- By region, Asia-Pacific commanded 38.55% of the sorbitol market in 2025; South America is the fastest-growing region at a 6.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sorbitol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Use of Liquid Sorbitol as a Humectant in Personal Care Products | +0.80% | Global, with North America & EU leading premium segments | Medium term (3-4 years) |

| Rising Demand for Sorbitol as a Non-Cariogenic Sweetener in Sugar-Free Confectionary | +1.20% | Europe & North America core, expanding to APAC | Long term (≥ 5 years) |

| Growing Popularity of Clean Label and Natural Sugar Alternatives Elevating Sorbitol Demand | +0.90% | Global, with premium markets driving adoption | Medium term (3-4 years) |

| Sorbitol's Non-Fermentable Properties Enabling Shelf Life in Functional Foods | +0.60% | North America & EU, spill-over to emerging markets | Long term (≥ 5 years) |

| Adoption of Sorbitol in Animal Nutrition as a Stabilizer and Energy Source | +0.30% | APAC core, expanding to Latin America | Short term (≤ 2 years) |

| Versatility of Sorbitol as a Bulking Agent in the Pharmaceutical Industry | +0.70% | Global, with regulatory-compliant markets prioritized | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Expanding Use of Liquid Sorbitol as a Humectant in Personal Care Products

Personal care manufacturers increasingly leverage liquid sorbitol's hygroscopic properties to enhance product texture and moisture retention, particularly in premium skincare formulations targeting aging demographics. Liquid sorbitol, known for its moisture-retaining properties, is widely utilized in products such as lotions, creams, and shampoos to enhance hydration and improve texture. According to data from the United States Food and Drug Administration (FDA), sorbitol is recognized as a safe ingredient for use in cosmetics and personal care formulations. Additionally, the European Chemicals Agency (ECHA) highlights its non-toxic and biodegradable nature, further boosting its adoption in the personal care industry. Furthermore, the rising awareness of skin health and the demand for products that cater to sensitive skin types are driving manufacturers to incorporate liquid sorbitol into their offerings. This trend is expected to significantly contribute to the growth of the global sorbitol market during the forecast period.

Rising Demand for Sorbitol as a Non-Cariogenic Sweetener in Sugar-Free Confectionary

The increasing demand for sorbitol as a non-carcinogenic sweetener is driving the growth of the market. Sorbitol, a sugar alcohol, is widely used in sugar-free confectionery due to its ability to provide sweetness without contributing to tooth decay. Sorbitol is recognized as safe for consumption and is commonly used in sugar-free gums, candies, and other confectionery products. According to the United States Food and Drug Administration (FDA), sorbitol is classified as a Generally Recognized as Safe (GRAS) substance, further supporting its widespread use in food products. The compound's unique crystallization properties allow manufacturers to achieve traditional candy textures impossible with high-intensity sweeteners, particularly in hard candies and chewing gums, where structural integrity determines consumer acceptance. This positioning becomes increasingly valuable as governments implement sugar taxes and dental associations recommend reduced-sugar alternatives. For instance, the Centers for Disease Control and Prevention (CDC) reports that nearly 50% of adults in the United States suffer from some form of periodontal disease, emphasizing the need for oral health-friendly products [1]Centers for Disease Control and Prevention, "About Periodontal (Gum) Disease-March 2024", www.cdc.gov. The rising awareness of oral health and the increasing prevalence of diabetes globally are also contributing to this trend. As a result, manufacturers are increasingly incorporating sorbitol into their product formulations to cater to health-conscious consumers, thereby driving market growth during the forecast period.

Growing Popularity of Clean label and Natual Sugar Alternatives Elevating Sorbitol Demand

Food manufacturers embrace sorbitol as a bridge ingredient that satisfies both clean label requirements and functional performance needs, particularly in applications where sugar reduction cannot compromise product stability. The compound's derivation from renewable corn glucose through established hydrogenation processes enables "natural" labeling claims under most regulatory frameworks, contrasting favorably with synthetic alternatives. Consumer research indicates sorbitol's familiar name recognition reduces purchase hesitation compared to chemical-sounding alternatives like acesulfame potassium or sucralose. The trend intensifies as retailers implement clean label mandates for private label products, forcing suppliers to reformulate using recognizable ingredients. Sorbitol's multifunctional properties as sweetener, humectant, and texturizer enable manufacturers to reduce ingredient lists while maintaining product performance, addressing the dual consumer demand for simplicity and functionality.

Sorbitol's Non-Fermentable Properties Enabling Shelf Life in Functional Foods

The non-fermentable properties of sorbitol play a significant role in enhancing the shelf life of functional foods, making it a key driver in the global sorbitol market. Sorbitol, a sugar alcohol, resists microbial fermentation, which helps prevent spoilage and extends the usability of food products. Additionally, the Food and Agriculture Organization highlights that sorbitol's hygroscopic nature aids in maintaining moisture levels in food products, further enhancing their texture and shelf life. The U.S. Food and Drug Administration has also recognized sorbitol as a safe food additive, which has encouraged its widespread use in the food and beverage industry. The growing adoption of functional foods, particularly in regions like North America, Europe, and parts of Asia-Pacific, is expected to drive the demand for sorbitol during the forecast period. Furthermore, the increasing prevalence of lifestyle-related diseases, such as diabetes and obesity, has led to a surge in demand for low-calorie and sugar-free products, where sorbitol serves as an ideal sugar substitute. For instance, according to the Office of Disease Prevention and Health Promotion, approximately 30 million people in the U.S. were suffering from diabetes in 2024, which makes it about 10% of the population [2]U.S. Department of Health and Human Services, "Office of Disease Prevention and Health Promotion-Diabetes", www.odphp.health.gov. As manufacturers continue to innovate in the functional food segment, the non-fermentable characteristics of sorbitol will remain a critical factor in its market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Raw Material Impacting Sorbitol Production Cost | -0.60% | Global, with corn-dependent regions most affected | Short term (≤ 2 years) |

| Regulatory Restrictions on Sugar Substitutes Impact Market Growth | -0.40% | Europe & North America, expanding globally | Medium term (3-4 years) |

| High Production Costs Impact Market Competitiveness of Crystalline Sorbitol | -0.30% | North America & EU, high-cost manufacturing regions | Medium term (3-4 years) |

| Concern Over GMO-Derived Raw Materials Affecting Demand of Natural Product | -0.20% | Europe core, spill-over to premium markets globally | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Fluctuating Raw Material Impacting Sorbitional Production Cost

The fluctuating prices of raw materials, such as corn and starch, are significantly impacting the production costs of sorbitol. These raw materials are essential inputs in sorbitol manufacturing, and their price volatility creates uncertainty for producers. This unpredictability in costs can lead to reduced profit margins and hinder the competitiveness of manufacturers in the global market. Additionally, the dependency on agricultural commodities, which are subject to seasonal variations, geopolitical tensions, and supply chain disruptions, further exacerbates the issue. For instance, adverse weather conditions or trade restrictions can lead to supply shortages, driving up raw material costs. Furthermore, the increasing demand for these raw materials in other industries, such as biofuels and food production, adds to the competition for resources, further inflating prices. As a result, the instability in raw material prices acts as a major restraint on the growth of the global sorbitol market, limiting its potential during the forecast period.

Regulatory Restrictions on Sugar Substitutes Impact Market Growth

Evolving regulatory frameworks create compliance complexity that constrains market expansion, particularly as health authorities reassess safety profiles for all sugar substitutes including natural alternatives like sorbitol. Regulatory bodies, such as the US Food and Drug Administration (FDA) and the European Food Safety Authority, have implemented strict guidelines regarding the use and labeling of sugar substitutes, including sorbitol. For instance, the FDA mandates that products containing sorbitol must include a warning label if consumption exceeds 50 grams per day, as it may cause a laxative effect [3]Center for Science in the Public Interest, "Consumer Group Petitions FDA to Require "Diarrhea" Notice on Foods that Contain Sorbitol", www.cspinet.org. Similarly, EFSA has set specific acceptable daily intake (ADI) levels for sorbitol to ensure consumer safety. Additionally, the Codex Alimentarius Commission, an international food standards organization, has established global standards for sugar alcohols, including sorbitol, to regulate their use in food products. These regulations create challenges for manufacturers, limiting the widespread adoption of sorbitol in various applications, such as food and beverages, pharmaceuticals, and personal care products. Furthermore, regional differences in regulatory frameworks, such as stricter labeling requirements in the European Union compared to the United States, add complexity for global manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Dominance Faces Crystal Momentum

In 2025, liquid sorbitol commanded a dominant 75.12% share of the sorbitol market, thanks to its pump-friendly logistics and immediate dissolution in food, pharmaceutical, and oral-care applications. Its ease of handling and compatibility with automated systems make it a preferred choice for large-scale manufacturing processes. Meanwhile, crystalline sorbitol is witnessing a robust annual growth rate of 6.45%, driven by its demand in tablet excipients that require precise particle sizing and in cosmetic powders that demand humidity resistance. Researchers at the University of Wisconsin-Madison have refined advanced crystallization processes, achieving narrower size distributions that enhance tablet compression yields, thereby improving production efficiency.

Additionally, the burgeoning field of 3D food printing is leaning towards the powder form of sorbitol, valuing its structural stability during layer deposition, which is critical for maintaining the integrity of complex designs. As pharmaceutical production surges in India and Japan, there's a marked preference for crystalline sorbitol. Its consistent flow through high-speed presses minimizes downtime, ensuring smoother operations and higher output. In the personal-care sector, some brands are rolling out innovative powder-to-cream products. These activate on-skin hydration through moisture, a feature made possible by the use of fine sorbitol crystals, which enhance the sensory experience and product performance.

By Application: Food Leadership Challenged by Supplement Surge

In 2025, the food and beverage sector commanded a substantial 44.10% share of the market revenue. Leading the charge, sugar-free confectionery took the spotlight, closely trailed by baked goods that require moisture retention during freeze-thaw cycles to maintain their texture and quality. Meanwhile, dietary supplements are on an upward trajectory, expanding at a 6.74% CAGR. This growth is largely driven by the rising demand for chewable vitamins and protein powders, both of which benefit from taste masking to enhance consumer appeal. A common ingredient in these products is sorbitol, utilized not just as a sweetener but also as a bulking agent. This dual role of sorbitol significantly reduces the per-unit formulation cost, especially when compared to using separate ingredients, making it a cost-effective solution for manufacturers.

In the pharmaceutical realm, sorbitol's unique properties play a pivotal role. Its compressibility is harnessed in crafting sustained-release tablets, particularly those aimed at the geriatric demographic, as these tablets ensure a controlled release of medication over time. Additionally, its osmotic laxative effect finds application in various oral solutions, providing effective relief for constipation. The cosmetics industry, too, has found value in sorbitol. Its humectant properties are prominently featured in anti-aging serums, which tout the benefit of 24-hour hydration, helping to improve skin moisture levels and reduce the appearance of fine lines. While industrial applications of sorbitol remain limited, they are noteworthy. One such use is its conversion into isosorbide, a bio-based monomer. This conversion holds promise as a potential alternative to PET, with the added benefit of possibly enhancing greenhouse gas profiles in packaging solutions, thereby contributing to more sustainable packaging practices.

Geography Analysis

In 2025, Asia-Pacific commands a dominant 38.55% share of the market, largely due to China's status as the globe's leading sorbitol producer. China primarily caters to vitamin C manufacturing, where sorbitol plays a pivotal role as an intermediate in the Reichstein synthesis process. The region's concentrated manufacturing hubs foster supply chain efficiencies, allowing for competitive pricing in global exports. Simultaneously, a burgeoning domestic demand, fueled by the expanding food processing and pharmaceutical sectors, bolsters market stability. Japan's cutting-edge pharmaceutical industry fuels a heightened demand for premium-grade sorbitol, especially for excipient applications. Here, the stringent quality standards command margins that surpass those of standard food-grade products.

South America, with a robust 6.18% CAGR projected through 2031, emerges as the fastest-growing regional market. This surge is propelled by Brazil's burgeoning sugarcane-based biorefineries and Argentina's ramped-up investments in pharmaceutical manufacturing. The region's edge lies in its abundant renewable feedstocks and production costs that undercut North America's and Europe's corn-based alternatives. Brazil's integrated complexes, spanning sugar, ethanol, and chemicals, harness sorbitol production as a value-added byproduct. This not only bolsters the economics of the facilities but also curtails environmental impacts by optimizing waste streams.

North America and Europe, with their mature markets, boast established regulatory landscapes and sophisticated applications, especially in pharmaceuticals and personal care. Here, quality premiums often counterbalance elevated production costs. The regions enjoy proximity to major players in pharmaceuticals and cosmetics, who value supply chain reliability over mere cost savings. Noteworthy recent expansions include Roquette's new polyol production facility in Keokuk, Iowa, which aims to cater to the surging demand for functional and health-centric food ingredients in North America. In Europe, there's a marked uptick in demand for sustainably sourced sorbitol. In response, manufacturers are channeling investments into renewable energy and embracing circular economy principles, aligning with both corporate sustainability goals and regulatory mandates aimed at curbing carbon footprints.

Regulatory Landscape

Sorbitol is broadly permitted as a food additive and sweetener, but compliance hinges on additive specifications and labeling rules that vary by region. In the United States, D-sorbitol (CAS 50-70-4) is affirmed as GRAS under 21 CFR 184.1835 for use in food under current good manufacturing practices, with category-specific maximum use levels (for example, up to 99% in hard candy/cough drops and 75% in chewing gum). The same regulation also ties labeling to consumer exposure, requiring a warning statement when reasonably foreseeable intake reaches 50 g/day ("Excess consumption may have a laxative effect"), which influences serving size design and product claims in sugar-free confectionery and related formats.

In Europe, sorbitol is regulated under the E-number system as E 420(i) (sorbitol) and E 420(ii) (sorbitol syrup), with specifications defined in Commission Regulation (EU) No 231/2012 (including minimum purity thresholds for total glycitols and D-sorbitol on a dry-weight basis). At the international level, JECFA (FAO/WHO) assigns sorbitol an ADI of "not specified," supporting its continued use across Codex-aligned markets while keeping attention on quality conformance and harmonized documentation for global supply chains.

Value Chain Analysis

The sorbitol value chain begins with agricultural feedstocks (most commonly corn, but also wheat, cassava, and potatoes) that are milled and hydrolyzed to produce glucose, followed by catalytic hydrogenation to convert glucose into sorbitol and downstream refining to deliver liquid grades or further crystallization for powder/crystal grades. Large integrated starch and sweetener producers such as Archer Daniels Midland, Cargill, Ingredion, Roquette, and Tereos typically participate across multiple steps, leveraging scale in wet milling, glucose production, and hydrogenation to improve utilization and cost control. Specialized producers also operate in regional hubs, including cassava-linked production initiatives in Africa, reflecting efforts to diversify raw material exposure.

Key constraints and cost drivers sit around feedstock price volatility (corn and, in some regions, cassava), energy intensity of hydrogenation, and lead times in bulk logistics, which can extend into multi-week planning cycles for industrial users. Quality management and traceability add additional steps for pharmaceutical and personal-care grade sorbitol, where tighter specifications and validated systems raise barriers to entry and encourage vertical integration or long-term supply agreements, especially for crystalline grades used in tablet excipients.

Competitive Landscape

The sorbitol market is moderately concentrated, with established players leveraging vertical integration and regional production advantages to maintain their competitive positioning. Key market leaders such as Roquette, Cargill, and ADM benefit from diversified product portfolios, which allow them to capitalize on cross-selling opportunities and reduce their dependence on sorbitol price fluctuations. These companies also focus on innovation and strategic partnerships to strengthen their foothold in the market, ensuring sustained growth and resilience against market volatility.

Specialized producers, such as Gulshan Polyols, concentrate on high-purity pharmaceutical-grade sorbitol, which commands premium pricing due to its stringent quality standards and critical applications in industries like pharmaceuticals and personal care. By targeting niche segments, these players differentiate themselves from larger competitors and cater to specific customer needs, thereby carving out a unique position in the market. This focus on high-value products enables them to achieve higher profit margins despite operating on a smaller scale.

The competitive intensity in the global sorbitol market is driven by significant barriers to entry. These include the substantial capital investments required for establishing glucose hydrogenation facilities and the high costs associated with meeting regulatory compliance for food and pharmaceutical applications. Additionally, established players benefit from economies of scale, robust supply chains, and long-standing customer relationships, which further solidify their market dominance. These factors make it challenging for new entrants to compete effectively, resulting in a market landscape that favors established players.

Sorbitol Industry Leaders

-

Tereos Group

-

Roquette Frères

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are forming around supply localization and higher-value grades as buyers balance cost, quality, and resilience. A concrete example is Southeast Asia: SOFAVI (Sorbitol France-Vietnam Joint Stock Company) restarted its 30,000-ton-per-year sorbitol plant in Tay Ninh, Vietnam in May 2026 to serve food, pharmaceutical, and cosmetic customers, indicating whitespace for regional production that reduces import dependency and shortens replenishment cycles. In oral care, Unilever launched a dedicated liquid sorbitol line at its Cu Chi, Ho Chi Minh City plant in April 2026 (14,000 tons per year) for internal toothpaste use, underscoring the strategic value of captive supply for consistent quality and continuity in high-throughput formulations.

On the demand side, premiumization in pharmaceutical excipients and personal care supports differentiation beyond commodity food use, especially for crystalline sorbitol that enables controlled particle sizing and consistent tableting performance. At the same time, scrutiny of sweeteners in public discourse and ongoing safety re-evaluations in major jurisdictions reinforce the importance of compliant labeling, serving-size engineering, and clear product positioning, particularly in sugar-free confectionery and supplements where intake can be higher and laxation warnings become formulation constraints.

Recent Industry Developments

- May 2026: Riddhi Siddhi Gluco Biols Ltd. completed the acquisition of Cargill India Pvt. Ltd.'s corn wet milling plant and related starch and sweeteners assets in Davangere, Karnataka. The transfer includes manufacturing facilities and corn silos, strengthening regional integration across glucose-derived products that feed polyols production. The move reshapes competitive positioning in India by shifting a large wet-milling footprint to a domestic operator with room to align output with downstream sweeteners and polyols demand.

- May 2025: Roquette completed its acquisition of IFF Pharma Solutions, expanding its presence in pharmaceutical excipients and oral dosage capabilities. The combination supports deeper participation in high-purity applications where sorbitol and related polyols are used as excipients and functional ingredients. It also signals portfolio emphasis on value-added healthcare and nutrition segments alongside core food ingredients.

- October 2024: Sanstar Limited announced a capacity expansion at its Dhule facility, adding 1,000 tons per day of maize-based specialty products including sorbitol. The investment increases upstream starch-to-sorbitol availability and improves responsiveness for customers seeking plant-based ingredient supply. Expanded domestic capacity also provides a hedge for buyers against feedstock and logistics volatility in cross-border sourcing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the sorbitol market is defined as the value of sorbitol sold in liquid/syrup and powder/crystal forms for use as a sweetener, humectant, and functional ingredient across food and beverage, pharmaceuticals, dietary supplements, and personal care.

Scope exclusions: Sugar alcohols other than sorbitol (such as xylitol and maltitol) are excluded even when they are used in the same end products.

Segmentation Overview

-

By Product Type

- Liquid Sorbitol

- Powder/Crystal Sorbitol

-

By Application

-

Food and Beverage

- Bakery and Confectionary

- Frozen Food

- Beverage

- Others

-

Cosmetics & Personal Care

- Oral Care

- Skin Care

- Hair Care

- Others

- Dietary Supplements

- Pharmaceuticals

- Others

-

Food and Beverage

-

By Geography

-

United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Netherlands

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia Pacific

-

South America

- Brazil

- Argentina

- Chile

- Columbia

- Peru

- Rest of South America

-

Middle East & Africa

- Saudi Arabia

- South Africa

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East & Africa

-

United States

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base of the model and to avoid building assumptions in isolation. We leaned on public statistics and scientific references to understand sorbitol production routes (starch and glucose based), typical end uses, and how demand moves with packaged food, oral care, and pharma excipients.

Common source types included government industry and trade datasets such as USITC DataWeb, UN Comtrade, and Eurostat, along with reference material from bodies such as the FAO. We also reviewed peer reviewed journals for application and formulation trends, then cross checked with company filings, investor presentations, and reputable press coverage. Where needed, paid subscriptions were used for company financials and intelligence, shipment level import export checks, and patent databases to sense new capacity and application activity. The sources listed here are illustrative, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming how sorbitol volumes and pricing behave in real buying cycles, and on separating food grade from pharma and personal care grade demand where secondary signals are not clean. We spoke with a mix of producers, distributors, formulators, and large end users across APAC, EMEA, and the Americas, so assumptions on utilization, trade flows, and grade mix could be tested and adjusted based on what they report in procurement and sales.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 39% |

| Mid tier: 55% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 19% | Managers: 54% | Americas: 27% |

Market-Sizing & Forecasting

The market was first reconstructed using a top-down approach where production capacity, operating rates, and trade data were translated into an apparent consumption pool by region, and then mapped to the main downstream uses. Once that regional total was stable, selective bottom-up checks were run using sampled supplier revenues, channel feedback, and typical ASP by grade to see whether totals were drifting away from what companies actually ship and bill.

Inputs that mattered most included regional starch and glucose availability, corn price direction as a feedstock signal, sorbitol utilization in confectionery and bakery recipes, personal care and oral care product output trends, and the grade mix shift between food and pharma uses. For forecasting, scenario analysis was applied because demand is sensitive to both input cost swings and reformulation cycles in packaged foods, and then the scenarios were sanity checked with primary respondents to keep growth paths realistic. Where bottom-up visibility was weaker for smaller markets, the gap was handled through trade based sizing and conservative adoption ratios tied to relevant end use output.

Data Validation & Update Cycle

Model outputs were validated using multiple checks, including region level consistency between capacity, trade, and implied consumption, followed by price sanity checks against observed contract ranges shared during interviews. Variances that looked unusual were reviewed again, and in many cases a second round of expert follow ups was triggered to confirm whether a new plant, outage, or demand shift explained the move.

Before sign off, the work goes through a multi step analyst review so assumptions, units, and currency conversions are consistent across regions and years. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity additions, feedstock shocks, or sharp demand changes. Right before delivery, we do a fresh pass so clients receive the most current view available at that time.

Mordor Intelligence's Sorbitol Market Estimate Compared With Other Published Estimates

Published sorbitol market numbers often do not match because the scope line is drawn differently, and the year used for sizing is not always the same. Differences also come from how prices are averaged across liquid versus powder forms, and whether grade mix is treated as a real price divider or blended into one number.

Polyols other than sorbitol sit outside Mordor Intelligence's scope, which removes spillover value that some estimates keep when they describe the wider sugar alcohol space. The spread also reflects timing, since some sources anchor the market in 2025, and then apply higher growth assumptions tied to aggressive reformulation and premium personal care demand without the same level of capacity and trade cross checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.82 B (2026) | |

| Global Consultancy A | USD 2.10 B (2025) | Uses an earlier base year and a faster growth arc, and typically blends pricing across forms and grades, which can lift the starting value when higher priced uses are averaged in. |

| Industry Publisher B | USD 2.31 B (2025) | Includes broader functional buckets and can apply a wider application set with blended assumptions, and the base year value can rise if chemicals and adjacent uses are counted more fully. |

Taken together, the main takeaway is that year selection, form and grade price treatment, and how tightly sorbitol is separated from adjacent polyols explain most of the gap. By keeping inputs tied to capacity signals, trade flow checks, and interview backed utilization and pricing ranges, the final market size stays traceable to simple variables that can be revisited each update cycle.

Key Questions Answered in the Report

What is the current size of the sorbitol market?

The sorbitol market was valued at USD 1.82 billion in 2026 and is projected to grow to USD 2.33 billion by 2031.

Which region holds the largest sorbitol market share?

Asia-Pacific leads with 38.55% of global volume, mainly because of China’s vitamin C production complexes.

Which application segment is growing fastest?

Dietary supplements are expanding at a 6.74% CAGR, driven by chewable vitamins and protein powders.

Why is liquid sorbitol dominant?

Liquid form accounts for 75.12% of sales due to its easy pumping, zero dissolution time, and low crystallization risk during storage.

How are raw-material price swings affecting manufacturers?

Corn price volatility erodes margins, prompting producers to trial sugarcane and cassava feedstocks and to use flexible contracting.

Page last updated on: