Atipamezole Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

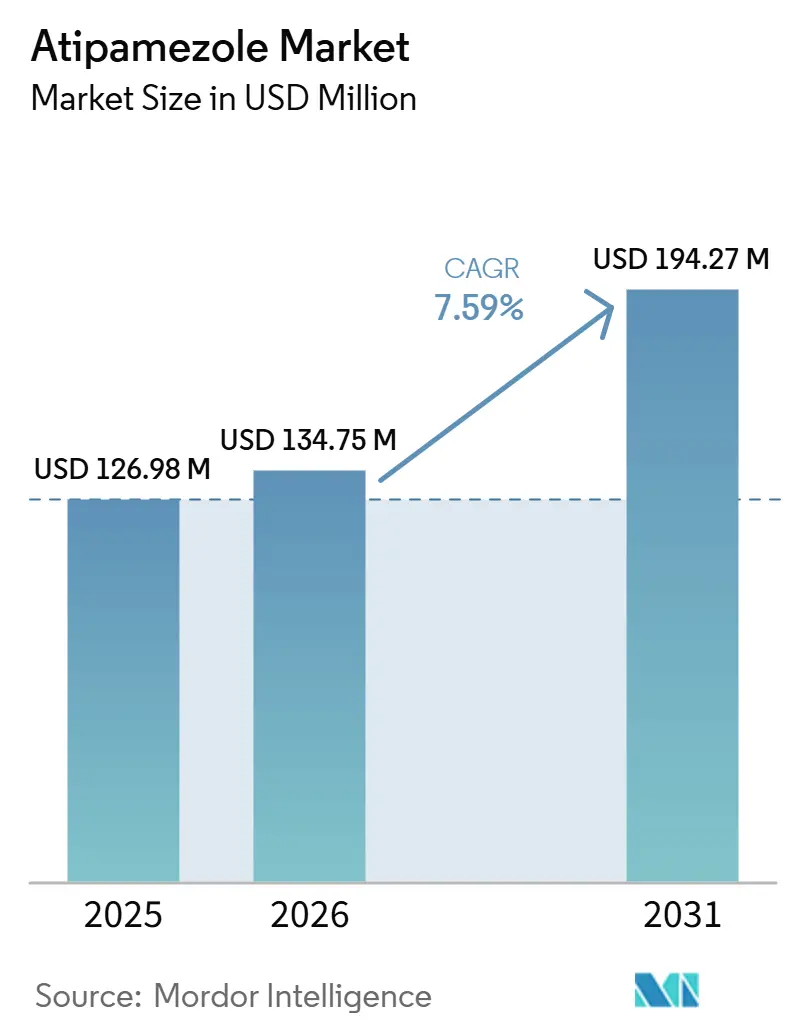

| Market Size (2026) | USD 134.75 Million |

| Market Size (2031) | USD 194.27 Million |

| Growth Rate (2026 - 2031) | 7.59% CAGR |

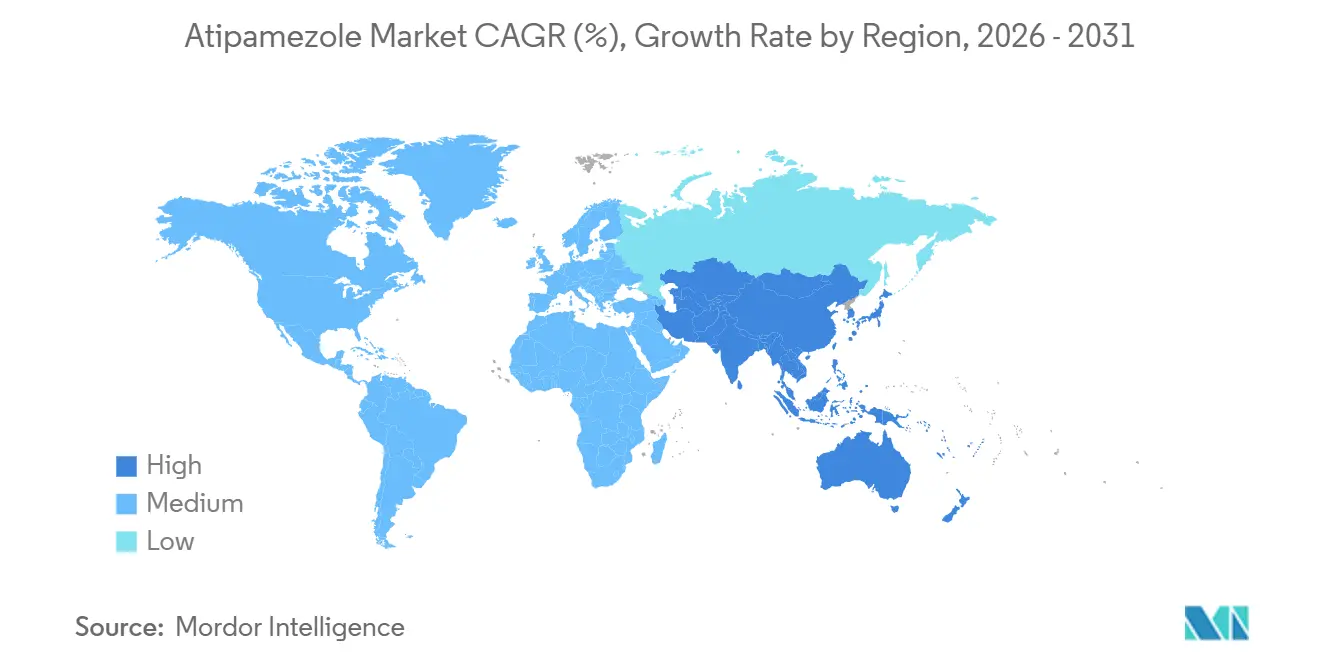

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

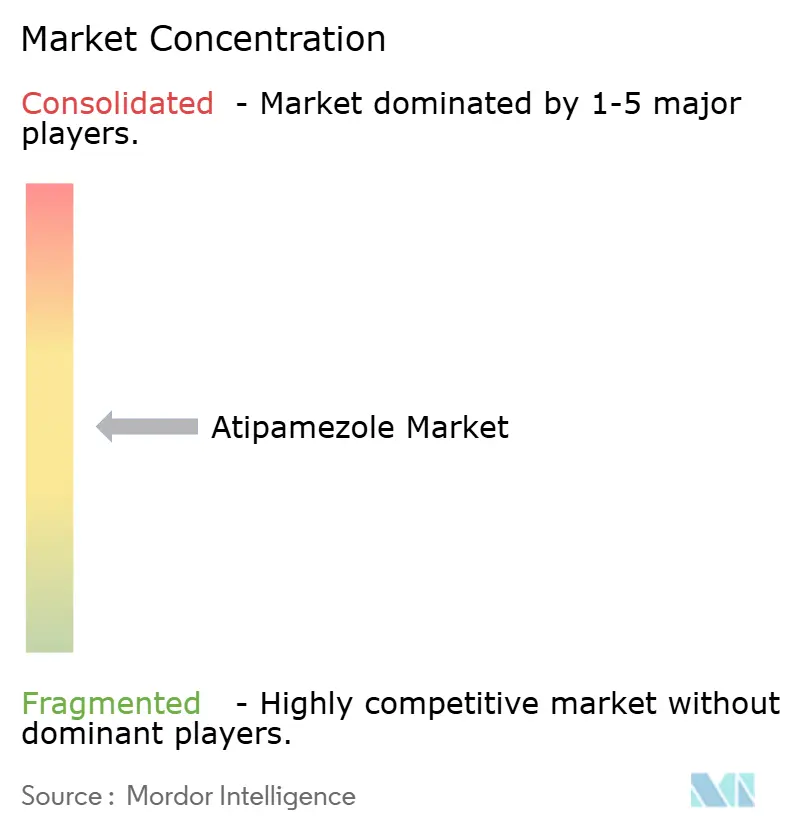

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Atipamezole Market Analysis by Mordor Intelligence

The Atipamezole Market size is projected to be USD 126.98 million in 2025, USD 134.75 million in 2026, and reach USD 194.27 million by 2031, growing at a CAGR of 7.59% from 2026 to 2031.

Demand rose with the broader companion animal care base, as the United States counted 163.6 million cats and dogs in 2025, while U.S. pet industry spending reached USD 158 billion in 2025 and is projected at USD 165 billion in 2026[1]American Veterinary Medical Association, “Evolving Pet Owner Economics: What Data Reveal for Veterinary Teams,” AVMA, avma.org. The Atipamezole market is expanding alongside wider use of dexmedetomidine and medetomidine in small animal practice, because a larger installed base of alpha-2 agonist sedation lifts demand for the matching reversal agent. The Atipamezole market is also becoming more price competitive, as FDA approvals for generic entrants since 2024 have widened access in clinics that are more sensitive to drug cost and stocking efficiency. The Atipamezole market still faces limits from narrow approved indications and strict veterinary drug labeling rules, but rising procedure volumes and deeper protocol standardization should keep growth steady through 2031.

Key Report Takeaways

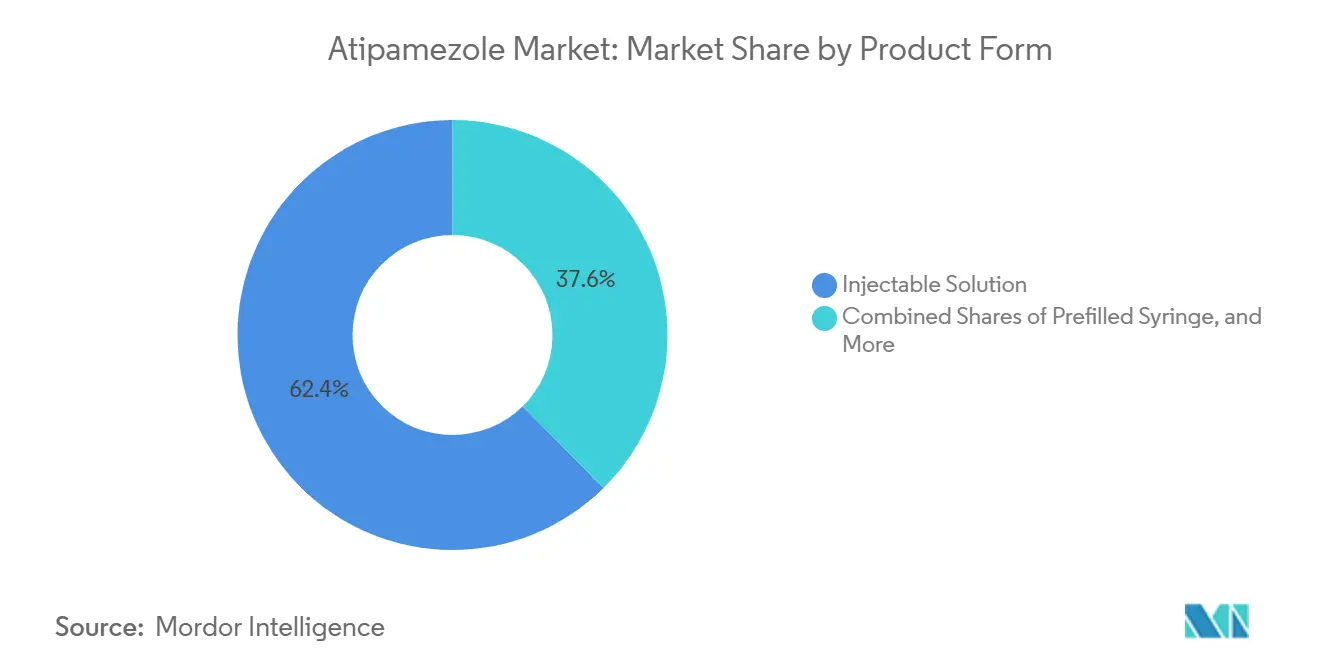

- By product form, injectable solutions held the largest 62.43% share in 2025, while compounded injectable formulations are projected to record the fastest 8.42% CAGR through 2031.

- By route of administration, intramuscular use held the largest 65.76% share in 2025, while intravenous use is projected to post the fastest 8.45% CAGR through 2031.

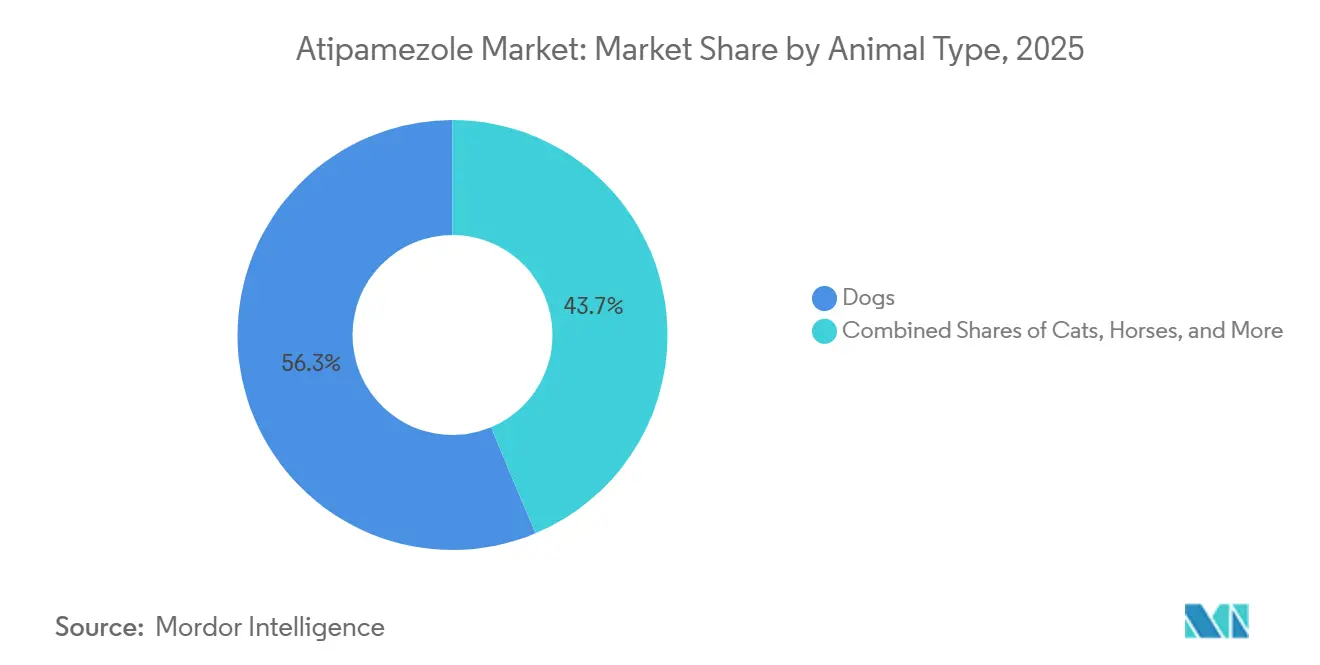

- By animal type, dogs held the largest 56.32% share in 2025, while cats are projected to expand at the fastest 8.69% CAGR through 2031.

- By application, veterinary sedation reversal accounted for the largest 41.21% share in 2025, while emergency and post-procedural recovery is projected to grow at the fastest 8.83% CAGR through 2031.

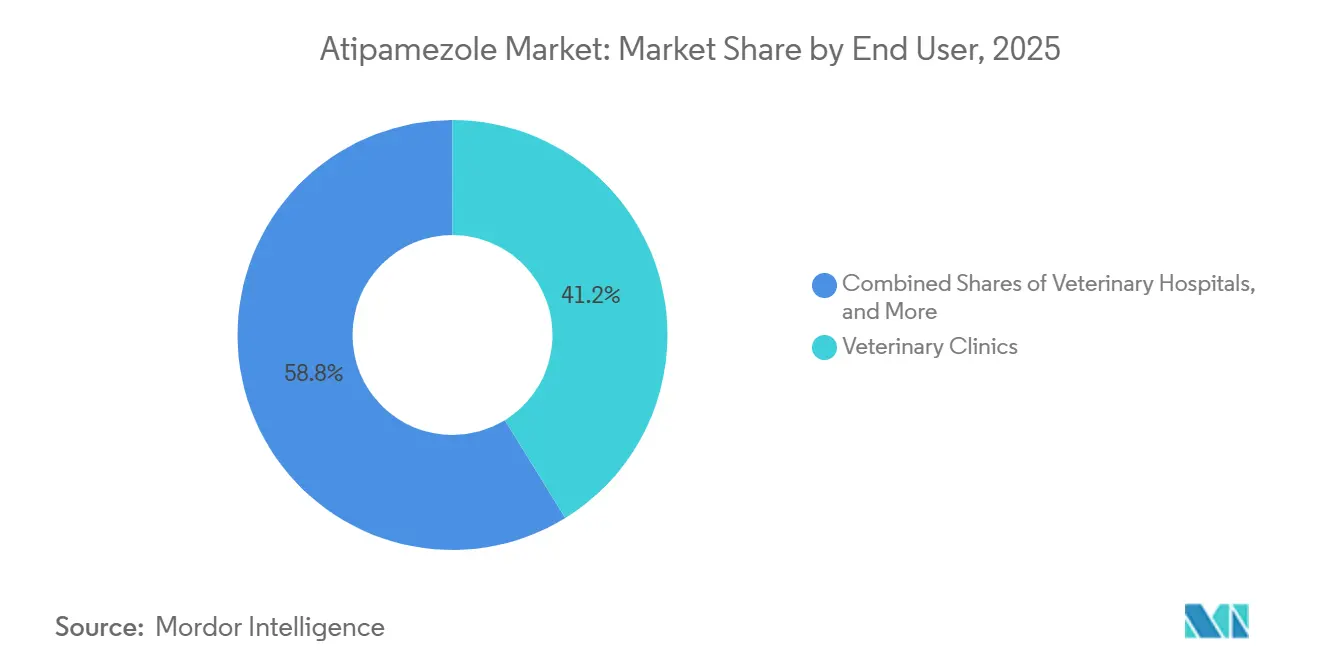

- By end user, veterinary clinics held the leading 49.45% share in 2025, while research institutes are projected to record the fastest 8.84% CAGR through 2031.

- By distribution channel, direct sales held the largest 39.25% share in 2025, while online pharmacies are projected to grow at the fastest 8.92% CAGR through 2031.

- By geography, North America held the largest 37.45% share in 2025, while Asia-Pacific is projected to grow at the fastest 8.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Atipamezole Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Companion Animal Sedation Reversal Demand | +2.1% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Expansion of Veterinary Surgical Throughput | +1.8% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Higher Protocol Standardization in Small Animal Clinics | +1.5% | North America, Europe, Australia | Medium term (2-4 years) |

| Growth in Pre-Measured Veterinary Drug Formats | +1.2% | North America, Europe, expanding into APAC | Medium term (2-4 years) |

| Wider Use in Research and Laboratory Animal Protocols | +0.8% | North America, Europe, Japan, China | Long term (≥ 4 years) |

| Faster Clinic Turnaround From Rapid Recovery Agents | +1.0% | Global, concentration in high-volume urban clinics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Sedation Reversal Demand

Companion animal ownership kept rising in the United States in 2025, with 95 million households owning pets, dog ownership at 53% of households, and cat ownership reaching 39% after a 5% year-over-year increase[2]American Pet Products Association, “U.S. Pet Industry Reaches $158 Billion in 2025, Poised for Continued Growth in 2026,” APPA, americanpetproducts.org. That larger pet base increases the number of animals moving through preventive care, diagnostics, and elective procedures where sedation is commonly used. The pattern is reinforced by access to care, because 83.4% of U.S. pet owners reported having a regular veterinarian in 2025, which supports recurring procedure volumes across routine practice. Spending patterns also matter, as dog owners spent an average of USD 598 on veterinary care in 2025, which signals continued willingness to pay for controlled and reversible anesthesia plans. The atipamezole market benefits directly because approved use is tied to medetomidine and exmedetomidine reversal, so higher use of those sedatives lifts follow-on demand for atipamezole.

Expansion of Veterinary Surgical Throughput

The atipamezole market is supported by the rising need to move sedated patients through surgery and recovery with less delay in busy clinics. Recovery speed matters because the product information shows that improvement begins quickly after dosing, with animals typically recovering in minutes and regaining mobility within a short period[3]Health Products Regulatory Authority, “SPC, Atipamezole Hydrochloride 5.0 mg/mL, Laboratorios SYVA S.A.,” HPRA, hpra.ie. That shorter recovery window frees cage space, staff time, and observation capacity, which makes reversible sedation more attractive in clinics handling several anesthetic cases each day. The benefit is not limited to efficiency, because a more predictable return from sedation also supports patient monitoring and helps clinics manage peri-anesthetic risk more consistently. As surgical throughput rises in urban veterinary networks, the atipamezole market should continue to gain from its role in closing the procedure cycle with a faster recovery path.

Higher Protocol Standardization in Small Animal Clinics

The atipamezole market is also being shaped by more formal anesthesia protocols in small animal practice. Clinical guidance from BSAVA places intramuscular atipamezole in a standard reversal role for medetomidine and dexmedetomidine, which gives the drug a stable place in day-to-day sedation workflows[4]British Small Animal Veterinary Association, “Canine and Feline Sedation/Immobilization Protocols,” BSAVA Library, bsavalibrary.com. Once a drug is embedded in an approved clinic protocol, use tends to become routine across all eligible procedures rather than depending on individual clinician preference. Recent clinical evidence has also widened comfort with administration choices, as a 2024 study in healthy dogs found effective reversal across tested routes, including intranasal delivery. The atipamezole market benefits from this pattern because stronger protocol discipline usually increases stocking regularity, dosing consistency, and repeat use across companion animal settings.

Growth in Pre-Measured Veterinary Drug Formats

The Atipamezole market has room to benefit from growing interest in pre-measured injectable formats, even though the dominant commercial standard remains the conventional vial. This matters because atipamezole dosing is linked to the previously administered sedative dose, which creates a real calculation step under time pressure in clinical practice. A pre-measured presentation can cut preparation time and reduce arithmetic error in weight-based dosing, which is useful in emergency care and high-throughput clinics. The FDA’s updated GFI #256 also gives clearer operating rules for compounded animal drugs from bulk drug substances, which supports interest in more tailored sterile injectable formats when a medical need is established. The Atipamezole market is therefore seeing a practical push toward ready-to-use presentations, even though labeled injectable solutions still anchor the segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Narrow Species and Indication Dependence | -1.4% | Global | Long term (≥ 4 years) |

| Stringent Veterinary Drug Approval and Labeling Requirements | -0.8% | North America, Europe | Medium term (2-4 years) |

| Competitive Pressure From Alternative Sedation Regimens | -0.6% | Global, especially North America | Medium term (2-4 years) |

| Limited Awareness in Small and Mid-Tier Veterinary Practices | -0.5% | APAC, MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Narrow Species And Indication Dependence

The atipamezole market remains limited by the drug’s narrow approved role, because commercial use is still tied mainly to reversal of medetomidine and dexmedetomidine in dogs and cats. U.S. and European product labels show that this is not a broad-spectrum anesthetic product, but a specific reversal agent with clear species and indication boundaries. Off-label use in other species exists, and recent research confirms continuing use in laboratory animals, but that volume remains much smaller than the core companion animal base. The atipamezole market is therefore highly dependent on the continued place of alpha-2 agonists in routine sedation protocols. If clinicians shift more procedures toward other anesthetic pathways that avoid medetomidine or dexmedetomidine, demand for atipamezole falls at the same time.

Stringent Veterinary Drug Approval And Labeling Requirements

The atipamezole market also faces friction from the time and documentation needed for animal drug approval, generic entry, label maintenance, and compounded use. In the United States, the generic pathway still requires a formal ANADA process linked to the reference product, even when a sterile injectable can use a simplified bioequivalence route. In Europe, product changes remain tightly controlled under the current veterinary medicines framework, and even routine label updates must move through regulatory review and approval. The FDA’s August 2024 update to GFI #256 also adds operational discipline for compounded animal drugs, including documentation and beyond-use dating expectations. These rules do not stop growth, but they do slow how quickly the Atipamezole market can add new presentations, fresh suppliers, and broader route options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Injectable Solutions Hold The Core, Compounded Formats Are Gaining Ground

Injectable solutions held 62.43% of the atipamezole market share in 2025, reflecting their long-established role as the standard commercial format in veterinary use. This lead comes from regulatory familiarity, routine clinic stocking, and the fact that approved products are positioned around sterile injectable use rather than alternative oral or transdermal options.

The atipamezole market size for compounded injectable formulations is projected to expand at an 8.42% CAGR through 2031, making this the fastest-growing product form in the segment. That growth is tied to clearer U.S. compounding rules after the August 2024 FDA update to GFI #256, which gives veterinary compounders more defined operating conditions for office-stock and patient-specific use when medical need is met.

By Route Of Administration: Intramuscular Use Remains the Standard, While Intravenous Use Is Expanding In Higher-Acuity Care

Intramuscular administration held 65.76% of 2025 revenue, which reflects the fact that approved product labeling consistently centers on intramuscular reversal after sedation. This route remains dominant because it is the labeled standard in major markets and is embedded in routine anesthesia guidance for dogs and cats.

The atipamezole market size for intravenous administration is projected to rise at 8.45% CAGR through 2031, making it the fastest-growing route segment. Growth here is linked to referral hospitals and critical care settings, where clinicians may need quicker or more controlled reversal during acute post-anesthetic management. Product information from Zoetis also shows that response can begin quickly after dosing, which supports the logic for closer route optimization in high-acuity settings.

By Animal Type: Dogs Drive Current Revenue, While Cats Are Advancing Faster

Dogs held 56.32% share of the Atipamezole market size in 2025, which reflects their large companion animal base and high veterinary care use. U.S. pet data showed strong dog ownership in 2025, while AVMA spending data also confirmed meaningful annual veterinary expenditure per dog-owning household. Dogs also anchor the segment because approved atipamezole use is firmly established in canine sedation reversal, which keeps demand tied to routine dentistry, diagnostics, surgery, and recovery care.

Cats are projected to record the fastest 8.69% CAGR through 2031, and that stronger ownership trends and clear labeled use in several markets support growth. APPA reported a 5% year-over-year increase in U.S. cat ownership in 2025, which points to a larger treatment base entering veterinary care pathways.

By Application: Core Sedation Reversal Leads, While Emergency Recovery Is Rising Faster

Veterinary sedation reversal accounted for 41.21% share in 2025, making it the leading application in the Atipamezole market. That result is fully aligned with the drug’s pharmacology and labeled role as a selective reversal agent after medetomidine or dexmedetomidine use. Practice guidance also supports this position, because BSAVA protocols place atipamezole directly within companion animal sedation workflows rather than as a rare rescue-only option.

Emergency and post-procedural recovery is projected to post the fastest 8.83% CAGR through 2031, showing that the drug’s role is moving deeper into higher-acuity care. This segment grows because rapid return from sedation can be clinically important when a patient needs quick reassessment, airway control, or shortened observation time.

By End User: Veterinary Clinics Lead Demand, While Research Institutes Are Expanding More Quickly

Veterinary clinics held 49.45% of 2025 end-user revenue, which places them at the center of the Atipamezole market. Clinics remain the largest end-user group because they handle routine companion animal procedures at the highest frequency and are where standard sedation protocols are most regularly applied. The segment also benefits from the fact that clinic workflows favor must-stock reversal agents when dexmedetomidine or medetomidine use is common in surgery, dental care, and diagnostics.

Research institutes are projected to grow at the fastest 8.84% CAGR through 2031, making them the fastest-expanding end-user segment. This pattern is supported by a steady 2024-2025 research record in rodents and rabbits, where atipamezole remains a defined component of injectable anesthesia and reversal protocols.

By Distribution Channel: Direct Sales Stay Largest, While Online Pharmacies Continue to Scale

Direct sales held 39.25% share in 2025, keeping this as the largest distribution channel in the Atipamezole market. That dominance reflects the prescription-only nature of the drug and the long-standing veterinarian-to-distributor purchasing pattern that still drives animal health procurement. Regulatory structures in the United States and Europe reinforce this setup because approved animal drugs move through licensed channels with clear control over labeling, dispensing, and pharmacovigilance.

Online pharmacies are projected to grow at the fastest 8.92% CAGR through 2031, making them the most dynamic distribution segment. Growth in this channel is tied to more digital prescription handling, broader comfort with remote ordering, and the steady integration of medication fulfillment into veterinary care pathways. The channel is especially relevant in mature pet care markets where owners are more accustomed to managed prescription purchase outside the clinic counter.

Geography Analysis

North America held 37.45% of the Atipamezole market share in 2025, making it the largest regional contributor. The region leads because veterinary infrastructure is well developed, per-pet healthcare spending is high, and reversible sedation protocols are widely established in companion animal practice. In the United States, 83.4% of pet owners had a regular veterinarian in 2025, while dog owners spent an average of USD 598 on veterinary care, which supports steady procedural demand and repeat drug use. Europe remains a strong regional block for the Atipamezole market because multiple locally authorized products compete across national markets under a harmonized regulatory structure.

Asia-Pacific is projected to record the fastest 8.73% CAGR through 2031, making it the fastest-growing regional segment in the Atipamezole market. Growth there is tied to urbanization, higher disposable income, and expansion of private veterinary clinics, all of which raise the number of companion animals moving into formal sedation and recovery pathways. Japan offers a premium but tightly regulated market, while China, India, and South Korea provide stronger volume upside as clinic networks and pet care spending continue to deepen.

Competitive Landscape

The Atipamezole market remains moderately concentrated around the originator product base, but it is becoming less tightly held as more generic suppliers enter and regional brand portfolios expand. Orion Corporation still holds the historic innovator position through Antisedan, while Zoetis distributes the product in the United States and regional partners such as Vetoquinol support European market presence.

Generic participation is the clearest competitive change in the Atipamezole market. Parnell’s CONTRASED received FDA approval in March 2024 as a generic equivalent to Antisedan, which widened the U.S. field and gave clinics another approved purchasing option. The atipamezole market should therefore remain competitive, but the most durable players are likely to be those with strong injectable manufacturing, dependable regulatory execution, and broad veterinary distribution partnerships.

Atipamezole Industry Leaders

Zoetis Inc.

Orion Corporation

Boehringer Ingelheim International GmbH

Parnell Pharmaceuticals Holdings Ltd.

Cronus Pharma LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: FelixVet announced the commercial launch of Atipamezole Hydrochloride Injection, a veterinary prescription product indicated for the reversal of the sedative and analgesic effects of dexmedetomidine and medetomidine in dogs.

- June 2025: Bimeda commenced the first phase of a multi-phase manufacturing expansion at its Monte Mor facility in Brazil, extending its South American production capacity across its animal health portfolio.

Global Atipamezole Market Report Scope

As per the scope of the report, atipamezole is a selective alpha-2 adrenergic receptor antagonist primarily used in veterinary medicine to reverse the sedative and analgesic effects of alpha-2 agonists such as dexmedetomidine and medetomidine in animals. It is commonly administered as an injectable formulation under veterinary supervision to facilitate rapid recovery following sedation, diagnostic procedures, or surgical interventions.

The atipamezole market report segments the market by product form, including injectable solution, prefilled syringe, multi-dose vial, and compounded injectable formulations. It also categorizes the market by route of administration, covering intramuscular, intravenous, and subcutaneous administration. Based on animal type, the market is segmented into dogs, cats, horses, exotic and zoo animals, and others. By application, the market is segmented into veterinary sedation reversal, research and experimental use, diagnostic and imaging support, and emergency and post-procedural recovery. The end-user segmentation includes veterinary clinics, veterinary hospitals, research institutes and others. Additionally, the distribution channel segment comprises direct sales, veterinary pharmacies, online pharmacies, and others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 key countries across these major regions. For each segment, the market size and forecasts are provided in terms of value (USD).

| Injectable Solution |

| Prefilled Syringe |

| Multi-Dose Vial |

| Compounded Injectable Formulations |

| Intramuscular |

| Intravenous |

| Subcutaneous |

| Dogs |

| Cats |

| Horses |

| Exotic and Zoo Animals |

| Others (Cattle, Sheep, Goats, etc.) |

| Veterinary Sedation Reversal |

| Research and Experimental Use |

| Diagnostic and Imaging Support |

| Emergency and Post-Procedural Recovery |

| Veterinary Clinics |

| Veterinary Hospitals |

| Research Institutes |

| Other End Users |

| Direct Sales |

| Veterinary Pharmacies |

| Online Pharmacies |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Form | Injectable Solution | |

| Prefilled Syringe | ||

| Multi-Dose Vial | ||

| Compounded Injectable Formulations | ||

| By Route of Administration | Intramuscular | |

| Intravenous | ||

| Subcutaneous | ||

| By Animal Type | Dogs | |

| Cats | ||

| Horses | ||

| Exotic and Zoo Animals | ||

| Others (Cattle, Sheep, Goats, etc.) | ||

| By Application | Veterinary Sedation Reversal | |

| Research and Experimental Use | ||

| Diagnostic and Imaging Support | ||

| Emergency and Post-Procedural Recovery | ||

| By End User | Veterinary Clinics | |

| Veterinary Hospitals | ||

| Research Institutes | ||

| Other End Users | ||

| By Distribution Channel | Direct Sales | |

| Veterinary Pharmacies | ||

| Online Pharmacies | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for atipamezole sales?

The Atipamezole market is forecast to reach USD 194.27 million by 2031, up from USD 126.98 million in 2025, at a 7.59% CAGR over 2026-2031.

Which product form currently leads demand?

Injectable solutions led with a 62.43% share in 2025 because they remain the standard approved and clinic-friendly format for sedation reversal.

Which animal group is growing fastest for atipamezole use?

Cats are projected to grow the fastest at 8.69% CAGR through 2031, supported by rising ownership and labeled use in several markets.

Which application is expanding fastest beyond routine reversal?

Emergency and post-procedural recovery is growing fastest at 8.83% CAGR through 2031, showing rising use in higher-acuity recovery and urgent care settings.

Why does North America lead current revenue?

North America held 37.45% share in 2025 due to strong veterinary infrastructure, high pet healthcare spending, and a more active approved generic landscape.

What is changing competition in this space?

FDA approval of generic products, stable branded portfolios from firms such as Orion and Dechra, and investment in sterile injectable capacity are making competition broader and more price aware.

Page last updated on: