Security Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

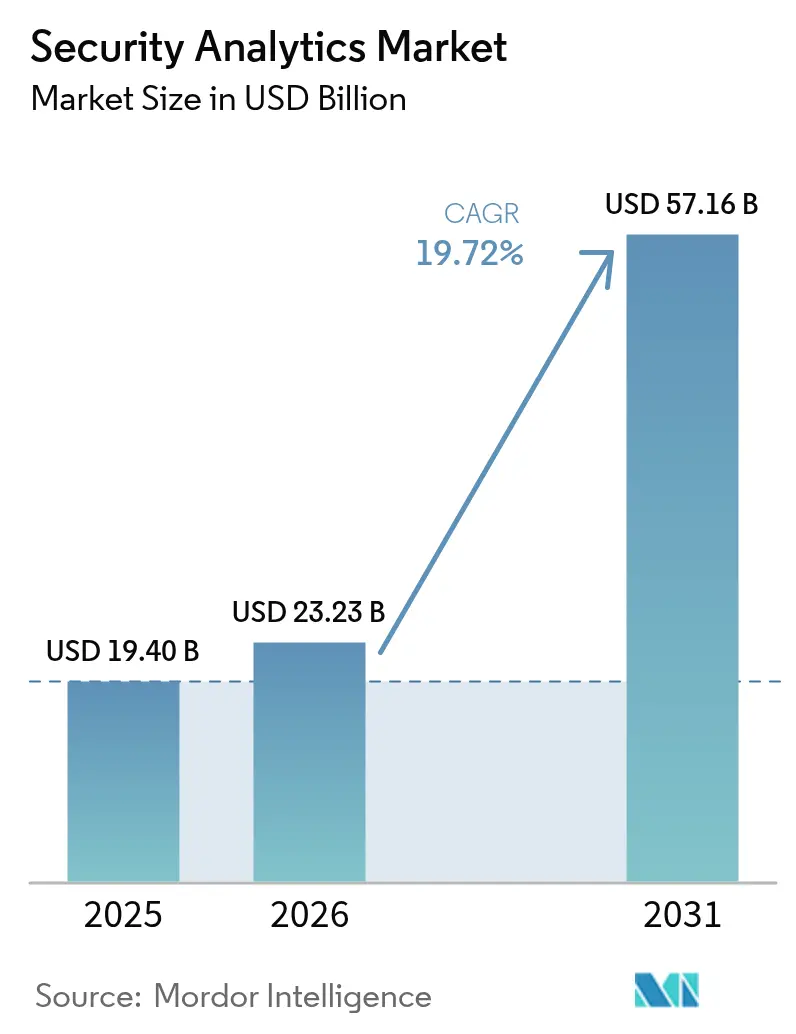

| Market Size (2026) | USD 23.23 Billion |

| Market Size (2031) | USD 57.16 Billion |

| Growth Rate (2026 - 2031) | 19.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Analytics Market Analysis by Mordor Intelligence

security analytics market size in 2026 is estimated at USD 23.23 billion, growing from 2025 value of USD 19.40 billion with 2031 projections showing USD 57.16 billion, growing at 19.72% CAGR over 2026-2031. The surge reflects enterprises’ drive to neutralize sophisticated cyber-attacks with AI-led platforms that analyze billions of events in real time. Growth stems from an explosion of IoT endpoints, cloud-first transformation projects, and tightening compliance regimes that require automated analytics. Demand is further amplified by platform consolidation: large vendors now bundle SIEM, SOAR, UEBA, and threat-intelligence into single suites to simplify operations and counter tool sprawl. CrowdStrike, Palo Alto Networks, Microsoft, IBM, and Cisco compete aggressively on analytics breadth, speed, and native automation while niche specialists maintain traction through differentiated AI models and cloud-native architectures.

Key Report Takeaways

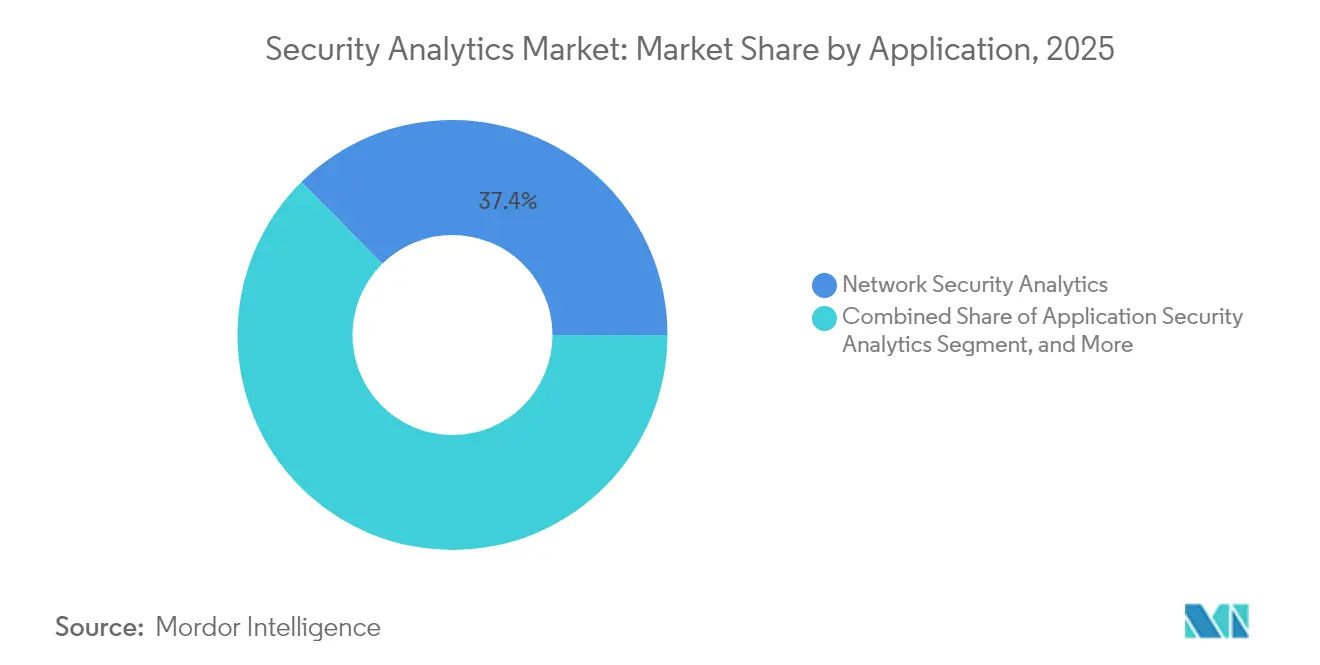

- By application, network security analytics led with 37.40% of security analytics market share in 2025; cloud security analytics is projected to grow at 16.85% CAGR through 2031.

- By deployment, on-premise models held 53.60% share of the security analytics market size in 2025, while cloud deployment is slated to expand at 20.45% CAGR to 2031.

- By organization size, large enterprises accounted for 68.10% of revenue in 2025, whereas small and medium enterprises are set to grow at 20.85% CAGR through 2031.

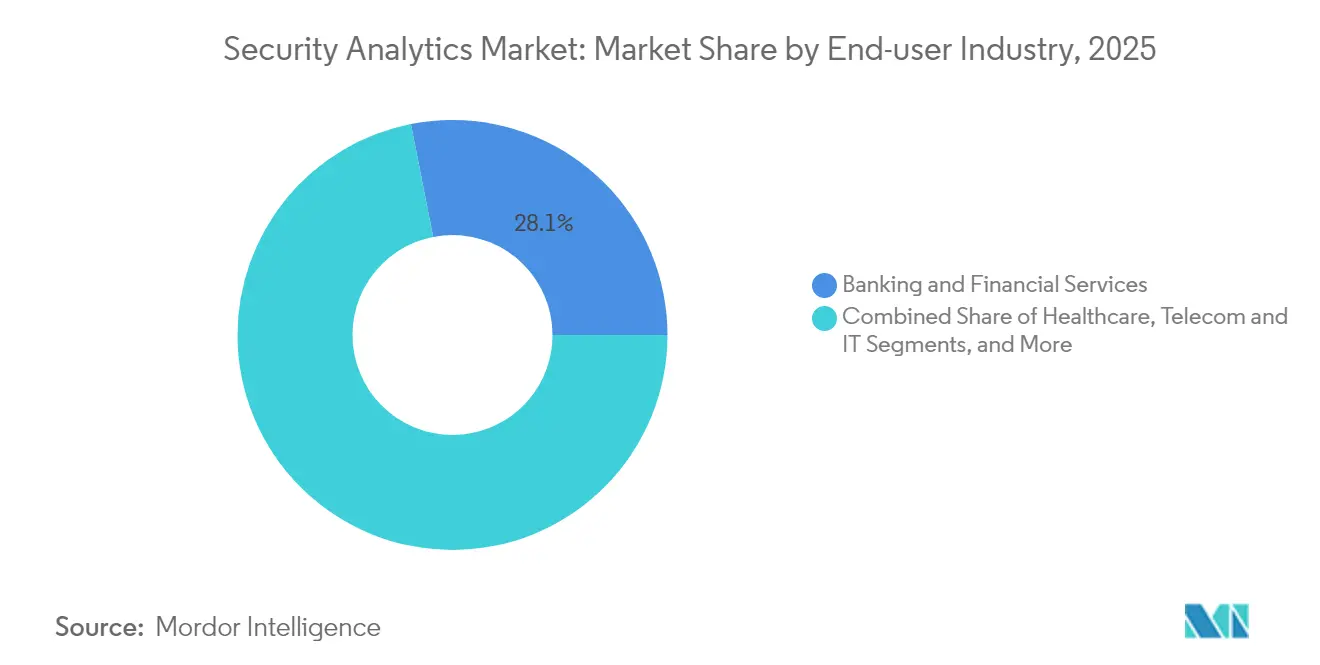

- By end-user, banking and financial services captured 28.10% of the security analytics market share in 2025; healthcare will accelerate at 16.05% CAGR to 2031.

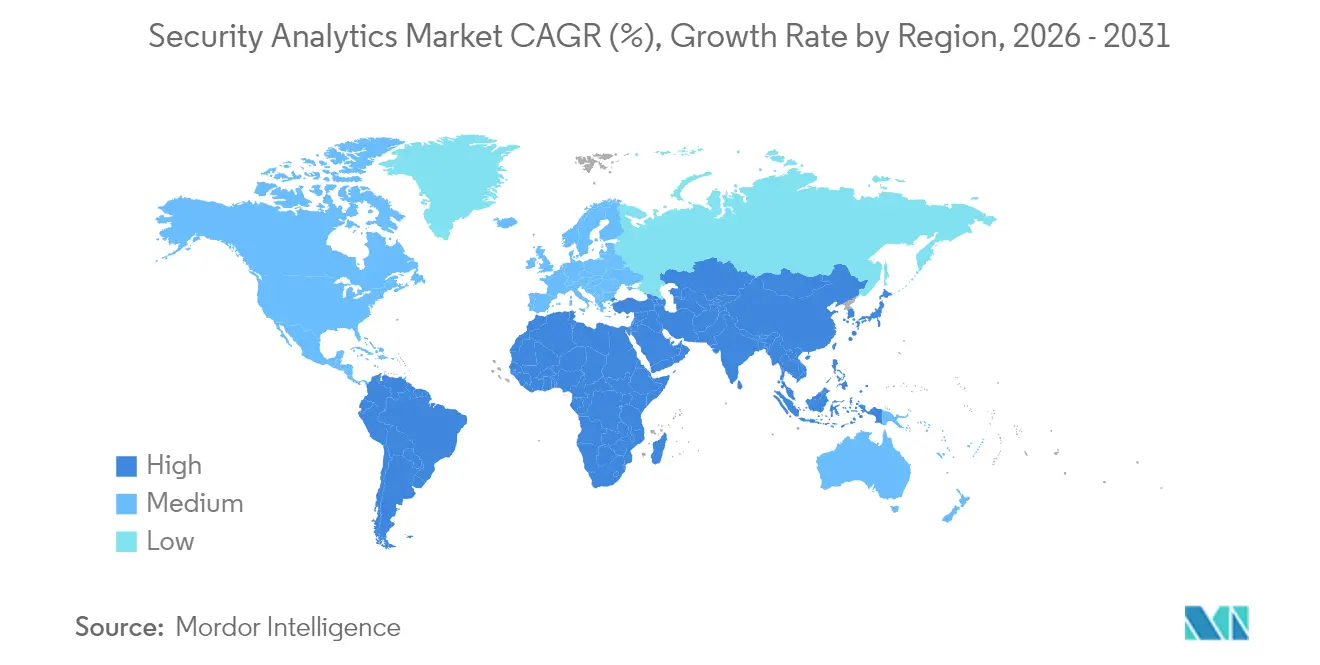

- By geography, North America retained 41.50% revenue share in 2025; Asia-Pacific is forecast to register a 13.25% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Security Analytics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sophistication of cyber-threat landscape | +4.2% | Global, with heightened impact in North America and EU | Medium term (2-4 years) |

| Explosive growth of IoT and BYOD endpoints | +3.8% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| Cloud-first digital-transformation programs | +5.1% | Global, led by North America and EU, accelerating in Asia-Pacific | Short term (≤ 2 years) |

| Expanding global cybersecurity-compliance regimes | +3.4% | EU and North America primary, extending to Asia-Pacific and MEA | Medium term (2-4 years) |

| AI-driven polymorphic malware emergence | +2.7% | Global, concentrated in developed markets initially | Medium term (2-4 years) |

| Surge in unmanaged machine-to-machine identities | +2.9% | Global, particularly in manufacturing and IoT-heavy sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sophistication of cyber-threat landscape

Nation-state actors now deploy automated toolchains that evade signature-based defenses, pushing enterprises toward behavioral analytics that detect lateral movement and zero-day exploits. The FBI cited a spike in state-sponsored attacks on telecom carriers aimed at surveillance and data exfiltration. [1]RSM US, “Nation-State Threat Landscape,” rsmus.comSecurity teams therefore favor platforms with machine-learning models that self-learn network baselines and flag anomalous paths in milliseconds. Vendors integrate UEBA and threat-intel feeds directly into SIEM engines, shrinking dwell time and improving mean time to detect. This arms race rewards suppliers able to retrain models continuously without manual feature engineering.

Explosive growth of IoT and BYOD endpoints

Industrial sensors, medical devices, and remote-work laptops have swollen the attack surface, leaving perimeter controls ineffective. Research in Scientific Reports found that more than 60% of organizations suffered insider threats tied to unmanaged devices. [2]Scientific Reports, “Behavioral Analysis of Insider Threats,” nature.com Modern analytics ingest telemetry from OT gateways, mobile EDR agents, and edge nodes, applying unsupervised learning to classify device behaviors. Edge processing cuts latency and keeps operations running when connectivity drops. Vendors now embed lightweight agents in firmware and combine them with cloud-side graph analytics to correlate anomalies across fleets of millions of endpoints.

Cloud-first digital-transformation programs

Lift-and-shift strategies and green-field SaaS adoption accelerate the pivot from on-prem SIEM to cloud-delivered analytics. The AT&T–Palo Alto Networks collaboration bundles connectivity with real-time threat detection inside a unified SASE fabric. [3]AT&T, “AT&T and Palo Alto Networks Deliver SASE,” att.com Cloud-native platforms elastically scale log ingestion and run AI models without customer hardware, enabling continuous inspection across AWS, Azure, and Google Cloud. Serverless and container workloads add new telemetry types—API calls, sidecar communications, and cold-start logs—that require purpose-built data collectors and context enrichment at ingest.

Expanding global cybersecurity-compliance regimes

The EU Cyber Resilience Act obliges manufacturers to patch connected devices throughout their lifecycle, driving demand for analytics that confirm vulnerability remediation. [4]Secure Privacy, “EU Cyber Resilience Act Overview,” secureprivacy.ai Financial regulators now insist on live anomaly detection for fraud, making advanced analytics unavoidable in banking stacks. GDPR’s extraterritorial scope forces granular audit trails and orchestrated data-subject-access reporting, so vendors bake compliance modules and automated evidence generation into dashboards. As mandates proliferate across healthcare, telecom, and critical infrastructure, buyers prefer platforms that map detections directly to frameworks such as NIS2, ISO 27001, and HIPAA.

Restraints Impact Analysis of Security Analytics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-integration and tool-sprawl challenges | -2.8% | Global, particularly acute in large enterprises | Short term (≤ 2 years) |

| Global shortage of SOC analysts | -3.1% | Global, most severe in North America and EU | Medium term (2-4 years) |

| High alert-fatigue and false-positive rates | -2.4% | Global, concentrated in mature markets | Short term (≤ 2 years) |

| Data-sovereignty rules restricting analytics | -1.9% | EU primary, extending to Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-integration and tool-sprawl challenges

Most enterprises juggle 25–50 security tools that emit disjointed log schemas, forcing custom parsers and delaying correlation. CSO Online reports that integration overhead drains analyst capacity and obscures cross-vector attacks. Buyers are replacing point solutions with converged analytics suites, yet fear of vendor lock-in slows rip-and-replace projects. As cloud migration compounds complexity, platforms must normalize on-prem Syslog, cloud API metadata, and SaaS audit trails within a single data lake, or risk perpetuating silos.

Global shortage of SOC analysts

ISC² estimates a workforce gap of 4 million practitioners, leaving many security analytics deployments underutilized. TechXplore highlights that advanced threat-hunting skills are especially scarce, prolonging incident response and inflating managed-service costs. Vendors counter with autonomous triage, natural-language playbooks, and AI-generated forensic narratives, but buyers still need personnel to validate alerts and tune models. SMEs feel the crunch most acutely, steering them toward outsourced MDR and fully managed XDR offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Security Analytics Market Segment Analysis

By Application:

Network Security Dominates Traditional InfrastructureNetwork security analytics generated 37.40% of 2025 revenue, underscoring the enduring role of deep-packet inspection and NetFlow analysis in the security analytics market. Cloud security analytics is advancing at 16.85% CAGR to 2031 as enterprises shift workloads off-premises and seek cross-cloud visibility. Application, web, and endpoint analytics together broaden detection coverage, while insider-threat modules employ UEBA to profile user behavior.

The convergence of these sub-segments pushes vendors to embed microservices-based collectors that ingest diverse telemetry into unified data fabrics. Platforms offering AI-driven policy recommendations and automated remediation now achieve a 59% drop in false positives versus legacy rule engines. Integrated suites therefore appeal to security leaders aiming to slash alert noise while protecting network, application, and identity layers in one console.

By Deployment Mode:

Cloud Transformation AcceleratesOn-premise implementations held 53.60% revenue in 2025, reflecting sunk investments and sovereign-data rules that keep sensitive logs inside firewalls. Yet the security analytics market size for cloud deployments is forecast to expand at a 20.45% CAGR through 2031 as firms adopt SASE and zero-trust mandates. Hybrid models are emerging as a pragmatic bridge—critical logs remain local while burst analysis occurs in secure clouds.

The U.S. Department of Defense’s Zero Trust Architecture 2.0 targets full coverage by 2027, leaning on commercial cloud analytics for scalability. Consumption-based licensing and managed ingestion pipelines erase capital expenditure hurdles, enticing even regulated industries to offload compute-intensive correlation tasks. Vendors also deploy regional cloud “cells” to meet data-residency directives without sacrificing analytic depth.

By Organization Size:

SME Adoption Drives GrowthLarge enterprises comprised 68.10% of sector value in 2025, but SMEs will propel incremental growth at 20.85% CAGR. Cloud-delivered analytics democratize tooling by bundling sensors, storage, and machine learning into subscription tiers accessible to lean IT teams. Techaisle notes that 21% of high-growth SMEs planned ≥15% budget hikes for cybersecurity in 2025.

Managed detection and response services top SME wish-lists because they remove the need for 24×7 SOC staffing. European vendors such as WithSecure now tailor AI-assisted threat-hunting packages to mid-market buyers concerned with local data privacy requirements. As a result, suppliers compete on automated investigations, intuitive UIs, and fixed-fee offerings aligned to SME cash-flow constraints.

By End-user Industry:

Financial Services Lead, Healthcare AcceleratesBanking and financial services captured 28.10% of the security analytics market in 2025, driven by real-time fraud mandates and high breach remediation costs. Healthcare is fastest at 16.05% CAGR as ransomware targets electronic health records and patient-care continuity. IBM’s Cost of a Data Breach study shows healthcare breach expenses averaging USD 4.88 million, nudging providers toward AI-driven anomaly detection.

Manufacturing now ranks second in attack volume, motivating investments in OT security analytics that map industrial protocols and detect suspicious command bursts. Government, telecom, and retail domains likewise accelerate adoption to meet zero-trust executive orders, 5G core protection, and omnichannel fraud prevention, respectively.

By Organization Size:

SMEs Challenge Enterprise DominanceLarge enterprises contributed 68.10% of 2025 revenue, leveraging complex toolchains and sizeable budgets. SMEs, though, are scaling adoption faster at 20.85% CAGR, benefiting from subscription-based cloud platforms that remove capital barriers. Simplified onboarding workflows and prescriptive analytics dashboards allow smaller teams to act swiftly on prioritized alerts.

As vendors adapt feature sets and pricing to mid-market needs, the security analytics market is likely to experience wider geographic and vertical diffusion, enhancing overall market resilience.

Geography Analysis

North America Security Analytics Market

North America commanded 41.50% revenue in 2025, benefitting from sizable cyber-budgets and early uptake of AI-enhanced SIEM. Federal directives such as Executive Order 14028 force continuous diagnostics and disclosure, further fueling spend.

APAC Security Analytics Market

Asia-Pacific is projected to grow at 13.25% CAGR, propelled by cloud migrations, cyber-insurance penetration jumps, and government-backed digital programs. Gallagher Re reports Asia-Pacific cyber-insurance premiums climbing nearly 50% annually. Australia, Singapore, Japan, and South Korea spearhead spending, yet India and China add the largest volume of new deployments as domestic tech champions scale globally.

EMEA and LATAM Security Analytics Market

Latin America eyes 64% IT-budget expansion for 2025, prioritizing analytics that handle a region-wide average of 1,600 attacks per second. EMEA growth remains steady; Europe leans on GDPR and the forthcoming Cyber Resilience Act, while Middle East and North Africa security outlays are set to exceed USD 3 billion in 2025, spurred by AI adoption in oil, gas, and government sectors.

Regulatory Landscape

Security analytics demand is being shaped by tighter, more prescriptive cyber standards and reporting requirements across major jurisdictions. In the United States, NIST released Cybersecurity Framework (CSF) 2.0 in February 2024, adding the Govern function to strengthen executive oversight, and NIST finalized SP 800-172 Rev. 3 in May 2026 with enhanced requirements to protect Controlled Unclassified Information (CUI) in nonfederal systems against advanced threats. As these updates land, buyers are prioritizing analytics platforms that can map detections and evidence to NIST-aligned controls while maintaining audit-ready logs.

2026 also brought sector and national-security anchors that raise expectations for detection and monitoring. In March 2026, FERC approved NERC CIP-003-11 to enhance security management controls for low-impact bulk electric system cyber systems, including requirements tied to remote user authentication and malicious communications detection. In June 2026, the White House issued NSPM-12 for National Security Systems, requiring systems to meet or exceed NIST cybersecurity standards and directing the CNSS to establish secure cloud configuration baselines. This reinforces demand for continuous configuration and telemetry analytics within regulated and defense-adjacent environments.

Value Chain Analysis

The security analytics value chain begins with telemetry production (endpoint, identity, network, application, cloud, and OT logs) and moves through data collection, normalization, enrichment, storage, correlation, visualization, and response automation, delivered as software and increasingly as integrated services. Upstream dependencies include sensor coverage (agents, API connectors, packet and flow sources), threat intelligence feeds, and cloud infrastructure for scalable ingestion and analytics compute. Midstream work focuses on data engineering and detection content, including parsers, schemas, rule logic, and ML models, while downstream value is realized through SOC workflows, investigations, orchestration, and packaged offerings such as MDR and XDR that help operationalize analytics for customers facing SOC staffing constraints.

Partnerships with hyperscalers and service providers are taking on more weight in distribution and operationalization, particularly as buyers pursue consolidated platforms and regional deployment options. In 2026, several collaborations reflected this shift: CrowdStrike and IBM expanded work to coordinate agentic SOC operations (Charlotte AI with IBM ATOM), SentinelOne deepened collaboration with Google Cloud with regional integrations (including Frankfurt and Saudi Arabia), and Securonix signed a strategic collaboration with AWS focused on agentic AI for security operations. On remediation, IBM, Red Hat, and Palo Alto Networks expanded Project Lightwell in June 2026 to connect virtual patching with open-source software remediation, tightening the link between analytics-driven findings and vulnerability-response execution.

Competitive Landscape

The security analytics market sits in moderate consolidation. The top five suppliers—Microsoft, Palo Alto Networks, IBM, Cisco (post-Splunk), and CrowdStrike hold a significant share, while dozens of challengers innovate in niche functions. Palo Alto Networks recorded USD 4.8 billion in next-generation security ARR on 15% growth, crediting its platform strategy. Cisco’s acquisition of Splunk lifted its security revenue 117% to USD 2.1 billion by integrating SIEM telemetry into SecureX.

Google’s proposed USD 32 billion purchase of Wiz underscores hyperscale appetite for cloud-centric analytics. Microsoft continued M&A by absorbing RiskIQ for USD 500 million, adding external-attack-surface mapping to its Sentinel SIEM.

Emerging rivals differentiate through graph databases, LLM-based playbook generation, and privacy-preserving edge analytics. QOMPLX patents on distributed graph computation accelerate risk scoring by 7.4× while shrinking storage. CrowdStrike’s GraphWeaver technology claims 99% alert correlation accuracy across petabyte-scale datasets. Vendors now publicize ROI metrics—mean-time-to-respond reductions and analyst-hour savings—to court CFO scrutiny and win displacements of legacy SIEM.

Security Analytics Industry Leaders

Alert Logic, Inc.

Broadcom Inc. (Symantec Enterprise Division)

Cisco Systems, Inc.

RSA Security LLC

Hewlett Packard Enterprise Company

- *Disclaimer: Major Players sorted in no particular order

Security Analytics Market Companies Covered in this Report

- Alert Logic, Inc.

- Arbor Networks, Inc. (NETSCOUT Systems, Inc.)

- Broadcom Inc. (Symantec Enterprise Division)

- Cisco Systems, Inc.

- RSA Security LLC

- Hewlett Packard Enterprise Company

- International Business Machines Corporation

- LogRhythm, Inc.

- Mandiant, Inc.

- Splunk Inc.

- Fortinet, Inc.

- McAfee, LLC

- Micro Focus International plc

- Securonix, Inc.

- Exabeam, Inc.

- Devo Technology, Inc.

- Microsoft Corporation

- Palo Alto Networks, Inc.

- CrowdStrike Holdings, Inc.

- Elastic N.V.

Market Opportunities and Future Outlook

Interoperability and schema standardization continue to create opportunities for vendors that reduce integration overhead and improve cross-domain correlation across network, endpoint, identity, and cloud. The Open Cybersecurity Schema Framework (OCSF) released v1.8.0 in March 2026, adding enhancements around AI observability and network packet visibility. That update reinforces customer preference for platforms that can normalize multi-source telemetry into a consistent data model and share detection content across tools, supporting consolidation of SIEM, UEBA, SOAR, and XDR without inheriting bespoke parsing and brittle pipelines.

Another near-term opportunity sits at the intersection of AI governance and time-bound incident response, where analytics can convert policy requirements into operational workflows. In the United States, more states enacted comprehensive privacy laws in 2026 (including Indiana, Kentucky, and Rhode Island), raising obligations around sensitive data handling and breach response documentation, while federal initiatives, including NIST updates and national-security cloud baseline work, emphasize evidence-driven control verification. On the threat side, telecom and digital-service providers are increasing AI-enabled detection for fraud and threat identification, including Openmind Networks reporting that 90% of operator AI deployments focus on fraud detection and Verizon citing adoption of Anthropic's Mythos for threat detection (July 2026). These signals point to security analytics suppliers packaging AI-driven detection with explainability, policy mapping, and workflow outputs that operations teams can execute under reporting and governance timelines.

Recent Industry Developments in Security Analytics Market

- July 2026: Verizon adopted Anthropic's Mythos for threat detection across its network. The deployment strengthens AI-driven detection and accelerates incident response for its security operations, signaling a major US telecom scaling of AI-assisted security analytics.

- January 2026: LevelBlue and Fortra launched a strategic managed services partnership that included LevelBlue acquiring Fortra's Alert Logic MDR, XDR, and WAF managed services business. The partnership strengthens platform-plus-services delivery for security analytics outcomes, aligning tooling with 24x7 operational coverage.

- June 2025: Fortinet unveiled an AI-powered workspace security suite that secures email, browsers, and collaboration tools. The release broadens telemetry sources feeding analytics by adding visibility into collaboration and productivity channels that are heavily targeted in phishing and account takeover campaigns.

Security Analytics Market Report Scope and Research Methodology

Market Definition and Coverage

In this methodology, the security analytics market covers software and related services used to collect, normalize, correlate, and visualize security data from environments like endpoint, network, cloud, identity, and applications, so threats can be detected and prioritized for action.

Scope exclusions: Stand-alone managed security service provider revenue is excluded when it is not bundled with an analytics platform.

Segments Covered in This Report

- By Application

- Network Security Analytics

- Application Security Analytics

- Web Security Analytics

- Endpoint Security Analytics

- Cloud Security Analytics

- Insider Threat Analytics

- By Deployment Mode

- On-Premise

- Cloud

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-user Industry

- Banking and Financial Services

- Healthcare

- Defense and Security

- Telecom and IT

- Retail and E-Commerce

- Manufacturing

- Government

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the boundaries of the security analytics scope and to build the first set of demand and supply signals. We relied on public and official source types such as NIST cybersecurity guidance, CISA advisories, FBI IC3 reports, ENISA threat landscape publications, and ITU cybersecurity statistics. These inputs help explain adoption drivers and the most common use cases we saw across security programs.

To translate those signals into market numbers, we also reviewed company annual reports, investor presentations, product documentation, and reputable press coverage. The goal was to capture pricing language, packaging changes, and customer mix cues that affect revenue attribution.

In a few places, we cross-checked vendor revenue disclosures and deal activity using paid subscriptions focused on company financials and intelligence, and we used a patent database to track where analytics capabilities were being built. This list is indicative, and we also referenced other sources for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work was used to pressure-test assumptions from desk research and to fill gaps around typical pricing, deployment mix, and buying triggers. We spoke with solution and service-side participants, channel partners, and enterprise users, and we kept inputs balanced across major regions so regional adoption differences did not get averaged out too early.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 18% | APAC: 38% |

| Mid tier: 51% | Functional/Unit leaders: 27% | EMEA: 37% |

| Smaller Players: 18% | Managers: 55% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where overall cybersecurity spend signals are narrowed into the analytics portion using observed adoption patterns across SIEM modernization, UEBA-style behavior analytics, cloud security monitoring, and response automation demand. Those shares are anchored using public indicators and then refined using interview feedback on what organizations actually purchase as a security analytics program.

To keep the total grounded, we corroborate the results with selective bottom-up approximations such as sampled average annual contract values by organization size, estimated installed base movement from on-premises to cloud delivery, and checks on services attach rates (professional and managed analytics services tied to platform deployments). When a supplier does not disclose clean revenue splits, we handle the gap using product mix cues, segment notes, and conservative allocation ranges, then recheck through follow-up expert inputs.

For forecasting, scenario analysis is used because budget cycles and threat events can shift timing quickly. Key inputs that we track include cloud workload growth, security alert volumes and automation rates, log retention and telemetry expansion, regulatory pressure on monitoring and reporting, and expected pricing changes from packaging moves (for example, platform bundles versus point tools).

Data Validation & Update Cycle

Validation is done through triangulation across multiple signals, then by reviewing variances that are too large to be explained by normal regional and vertical differences. We compare totals against independent indicators such as enterprise security budget direction, cloud migration pace, and tooling consolidation trends, and we route outliers through more than one analyst pass before sign-off.

The report is refreshed annually, and interim updates are made when material events change pricing, packaging, or demand patterns. Before delivery, a final review pass is completed so the model reflects the latest available currency timing, disclosed results, and newly confirmed assumptions from recent expert re-contacts.

Mordor Intelligence's Security Analytics Market Estimate Compared With Other Published Estimates

Published market sizes for security analytics often vary because the refresh timing, the USD conversion point used for global revenues, and how pricing progression is handled can change the final total by a noticeable amount. Differences also come from whether services are treated as a direct part of the market or kept separate, which changes what gets counted as market revenue.

In our checks, the biggest gap drivers were currency timing on multinational revenues, whether managed and professional services attached to analytics platforms were included, and how fast average contract values were assumed to rise as more cloud data sources get added. By revalidating pricing and attach rates close to the final model cut and locking FX timing consistently, Mordor Intelligence keeps the 2026 value aligned with what buyers actually pay for analytics programs in that year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 23.23 B (2026) | |

| Global Consultancy A | USD 13.49 B (2024) | Uses a 2024 base year and a faster growth curve, and the scope emphasis leans toward component splits that can treat some attached services differently, which shifts the headline total versus a platform-plus-attached-services view. |

| Industry Research Firm B | USD 13.87 B (2024) | Anchors the market in 2024 and extends a longer horizon forecast, and differences in how solution categories are grouped (for example, web and endpoint analytics) and how pricing uplift is applied can change the size even when regions look similar. |

The table shows that part of the spread is simply the year being measured, but the larger swings come from service attachment choices and pricing and FX handling. Using a consistent year cut, clear inclusion rules for bundled analytics services, and repeatable pricing checks makes the estimate easier to trace back to practical buying and deployment patterns.

Key Questions Answered in the Report

What is the current value of the security analytics market?

The security analytics market stands at USD 23.23 billion in 2026 and is projected to climb to USD 57.16 billion by 2031.

Which application segment grows fastest in security analytics?

Cloud security analytics is the fastest, registering a forecast CAGR of 16.85% through 2031.

Why are SMEs adopting security analytics rapidly?

Cloud-delivered platforms lower upfront costs and automate oversight, enabling SMEs to access enterprise-grade protection without dedicated SOC teams.

Which region will see the highest growth rate?

Asia-Pacific is expected to post a 13.25% CAGR on the back of accelerated digitalization, cyber-insurance uptake, and regulatory focus.

How are vendors addressing the SOC talent gap?

Suppliers integrate AI-driven triage, natural-language playbooks, and managed detection services to ease reliance on scarce in-house analysts.

What impact will data-sovereignty laws have on deployment models?

Vendors are deploying regional data centers and edge analytics nodes to comply with residency mandates while sustaining real-time threat detection.

Page last updated on: