Enterprise AI Workplace Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

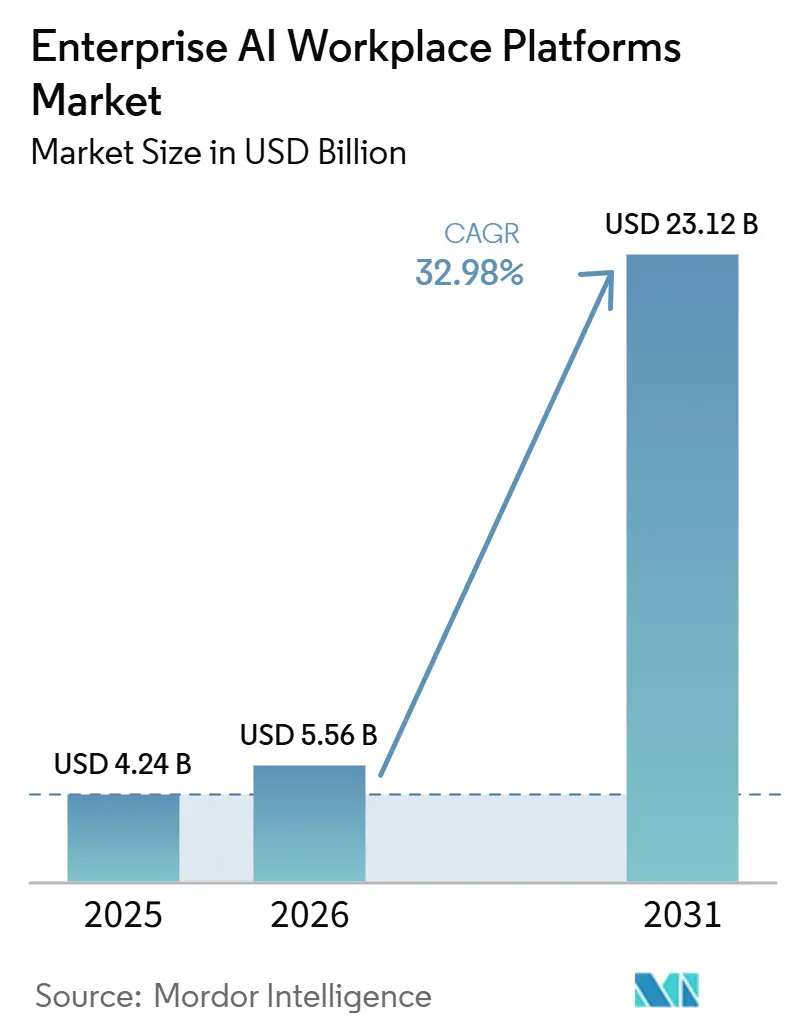

| Market Size (2026) | USD 5.56 Billion |

| Market Size (2031) | USD 23.12 Billion |

| Growth Rate (2026 - 2031) | 32.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise AI Workplace Platforms Market Analysis by Mordor Intelligence

The enterprise AI workplace platforms market size is projected to be USD 4.24 billion in 2025, USD 5.56 billion in 2026, and reach USD 23.12 billion by 2031, growing at a CAGR of 32.98% from 2026 to 2031. Robust adoption by financial services and technology firms that view autonomous agents as competitive enablers, rather than labor substitutes, is compressing purchase cycles. Outcome-based contracts that tie fees to measurable business metrics are replacing per-seat licenses, lowering procurement friction and rewarding vendors that deliver rapid productivity gains. Labor cost inflation in traditional outsourcing hubs is eroding the offshore advantage, repositioning the enterprise AI workplace platform market as a strategic hedge against wage volatility. Environmental, social, and governance scrutiny over compute-intensive inference workloads is nudging buyers toward power-efficient model architectures, adding a new performance dimension to vendor selection.

Key Report Takeaways

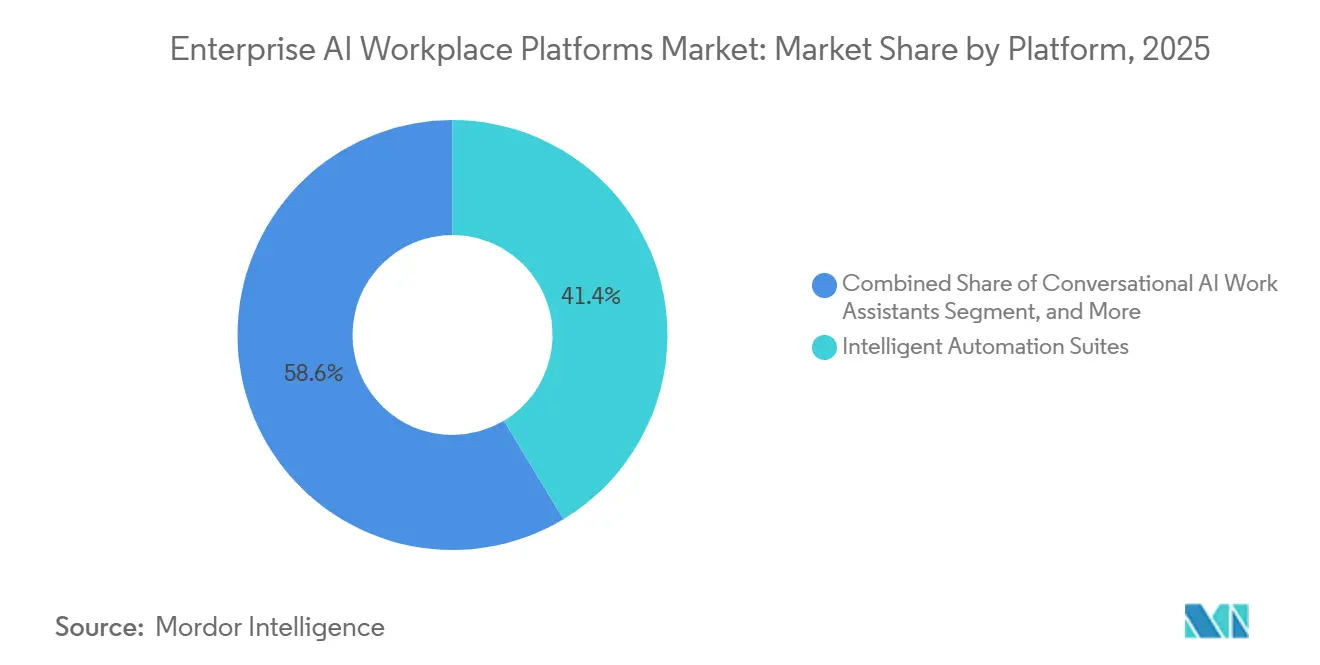

- By platform, intelligent automation suites led with 41.37% revenue share in 2025, while skill development platforms are expanding at a 33.98% CAGR to 2031.

- By deployment model, cloud captured 63.52% of spending in 2025, yet hybrid is expected to be the fastest-growing architecture at a 33.38% CAGR through 2031.

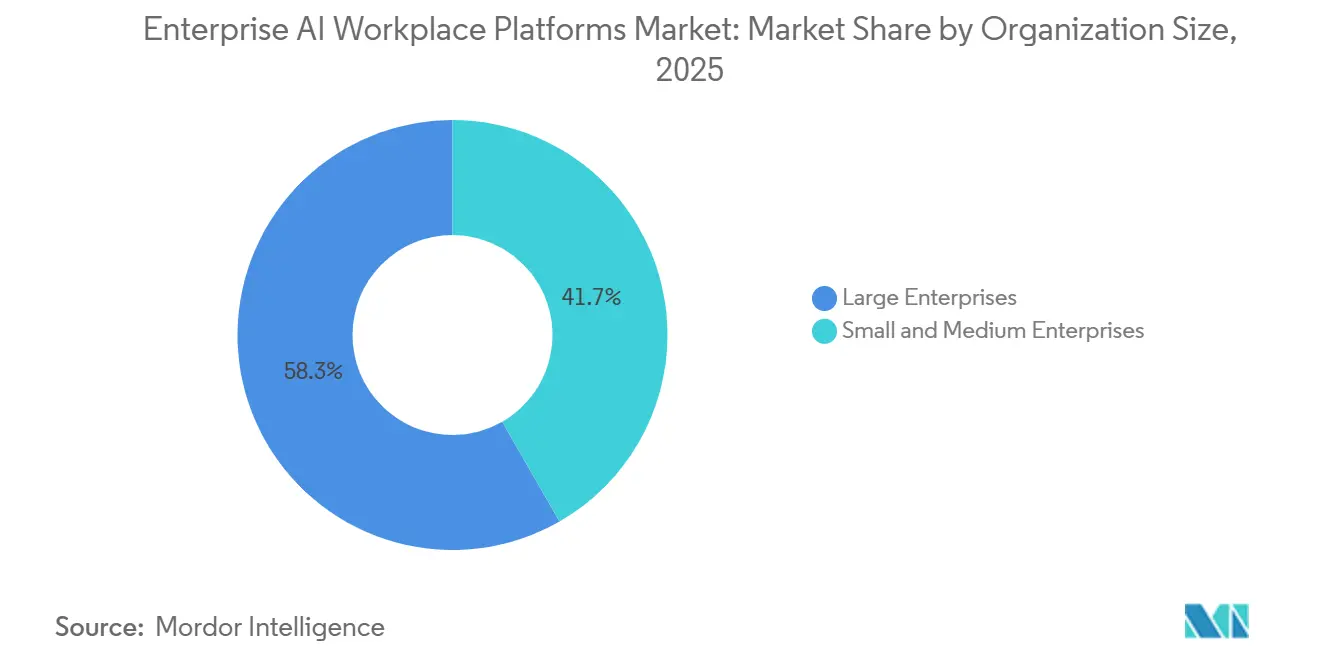

- By organization size, large enterprises accounted for 58.29% of outlays in 2025, whereas small and medium enterprises are expected to advance at a 33.57% CAGR to 2031.

- By end-user industry, IT and telecom accounted for 23.43% of revenue in 2025; healthcare and life sciences posted the highest forecast growth at a 34.28% CAGR through 2031.

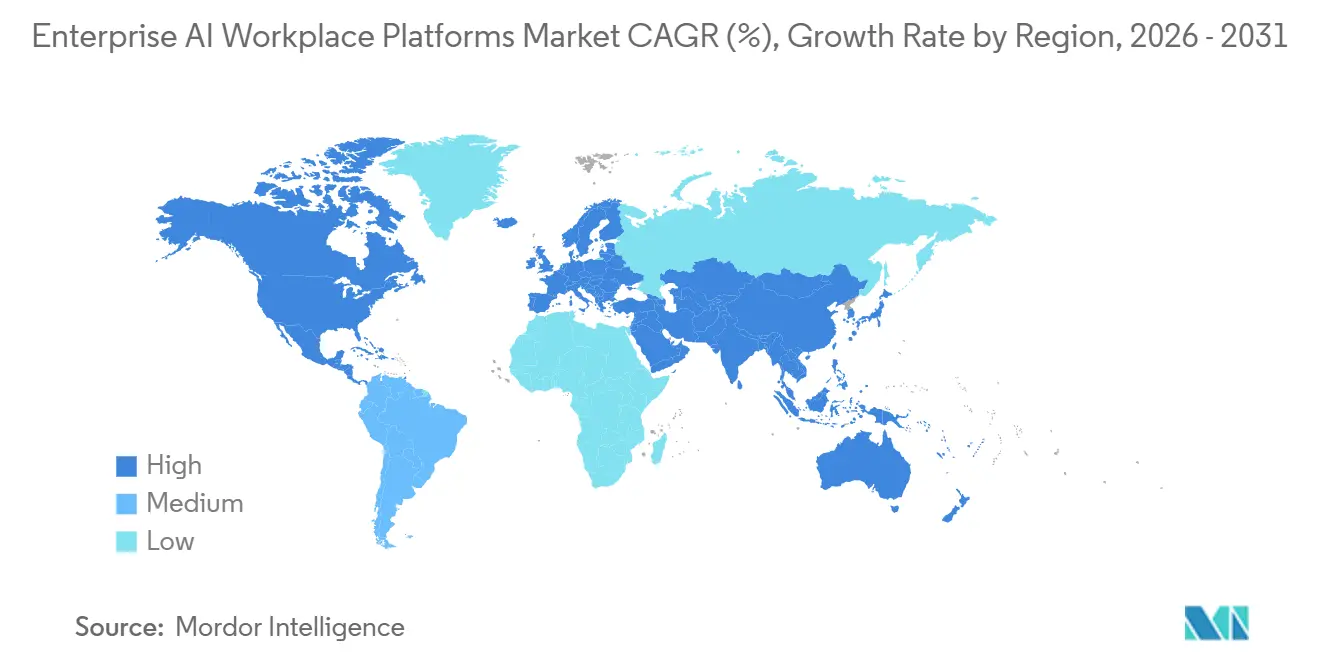

- By geography, North America accounted for 35.73% of sales in 2025, while Asia-Pacific is projected to expand at a 33.98% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise AI Workplace Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Enterprise Adoption of Generative AI Assistants | 9.2% | Global, with North America and Europe leading deployment density | Short term (≤ 2 years) |

| Advances in Multimodal Large Language Models Enhancing Collaboration | 8.5% | Global, concentrated in North America, Europe, and Asia-Pacific technology hubs | Medium term (2-4 years) |

| Rising Demand for Hybrid-Work Orchestration Platforms | 7.8% | Global, particularly North America, Europe, and urban Asia-Pacific markets | Short term (≤ 2 years) |

| Integration of RPA Bots with Conversational Agents | 6.4% | Global, with early adoption in North America, Europe, and manufacturing-heavy Asia-Pacific regions | Medium term (2-4 years) |

| Availability of Low-Code and No-Code AI Development Tools | 5.1% | Global, accelerating SME adoption in Asia-Pacific, South America, and Middle East | Short term (≤ 2 years) |

| Growing Compliance Mandates for AI Auditability and Transparency | 4.3% | Europe (EU AI Act), North America (NIST AI RMF), and Asia-Pacific (Singapore AI Verify) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration of Generative AI Co-Pilots into Enterprise Productivity Suites

Embedding co-pilots inside familiar collaboration tools removes the hand-off between task identification and automation, allowing workers to invoke agents without leaving the application of record. Microsoft reported 1 million paying Copilot subscribers by January 2025 and indicated 29% time savings on document creation and meeting summarization tasks. Salesforce followed up with Agentforce, enabling non-technical staff to launch autonomous customer service agents that shortened resolution time by 40% in pilots. Tight integration raises switching costs because enterprises prefer bundled upgrades over separate procurement cycles. Compliance frameworks such as ISO/IEC 42001 are pushing vendors to certify embedded co-pilots, further cementing incumbent productivity-suite providers on buyer shortlists. Collectively, these dynamics front-load demand and support premium pricing during the first wave of adoption.

Rising Labor Cost Inflation Accelerating Automation ROI

Annual wage growth of 8-10% in India’s IT services sector and 7-9% in the Philippines’ call-center workforce during 2025 shrank the economic spread between human labor and autonomous agents. Breakeven periods for invoice-processing automation contracts are projected to decrease from 24 months in 2023 to 14 months in 2025. Vietnam’s government reacted by creating a USD 200 million incentive fund for industrial AI deployments, signifying policy alignment with enterprise automation goals.[1]Department Notice, “AI Adoption Fund,” MPI.GOV.VN As a result, CFOs now frame AI workplace investments as inflation hedges that stabilize operating margins. The fiscal logic reinforces multi-year budget allocations, especially within back-office functions where repetitive workflows dominate cost structures.

Rapid Adoption of Low-Code and No-Code AI Orchestration Platforms for Citizen Developers

UiPath’s Autopilot converts plain-language prompts into executable scripts, collapsing build phases from weeks to hours. A Deloitte survey found that 62% of mid-market businesses cited skill shortages as the main barrier to automation, yet almost half reported successful deployments once low-code tools became available. Visual builders transfer design authority to process owners who understand pain points, thereby broadening the internal constituency for AI workforce rollouts. M&A activity is accelerating as platform players acquire niche connectors that extend drag-and-drop workflows to legacy systems. Regulators are starting to appreciate the transparency advantage of low-code, because autogenerated audit logs satisfy documentation mandates under the EU AI Act.

Availability of Pre-Built AI Workforce Skill Libraries from Independent ISVs

Automation Anywhere’s Bot Store surpassed 1,200 certified components in late 2025, including skills for SAP, Salesforce, and ServiceNow integrations. Deployment cycles were observed to be 35% faster when enterprises used pre-built skills rather than developing automations from scratch. Libraries create a two-sided marketplace where developers monetize specialized expertise and enterprises de-risk adoption through peer-rated assets. System integrators are packaging vertical skill bundles, such as insurance claims robots, to chase annuity revenues from configuration and support. Privacy regulations are pushing vendors to embed consent logic within each skill, reducing compliance overhead for end users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Standardized Human-AI Interaction Protocols | -3.7% | Global, with acute challenges in regulated industries across North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Data-Privacy Concerns Limiting Cross-Team Data Sharing | -4.1% | Europe (GDPR enforcement), North America (state-level privacy laws), and Asia-Pacific (emerging frameworks) | Short term (≤ 2 years) |

| High Upfront Integration and Training Costs | -2.9% | Global, disproportionately affecting SMEs in South America, Middle East, Africa, and rural Asia-Pacific | Short term (≤ 2 years) |

| Workforce Resistance Due to Job-Displacement Anxiety | -3.5% | Global, with higher intensity in manufacturing-heavy regions and public-sector organizations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data Residency and Sovereignty Concerns Limiting Cross-Border Deployments

The EU General Data Protection Regulation, China’s Cybersecurity Law, and India’s Digital Personal Data Protection Act prohibit unrestricted data transfer, compelling enterprises to adopt hybrid topologies with sovereign partitions. Compliance overhead elevates the total cost of ownership by requiring redundant stacks, contractual safeguards, and localized support teams. An International Association of Privacy Professionals survey found that 58% of multinationals postponed AI workplace deployments due to lingering uncertainty over legal transfer mechanisms.[2]Policy Library, “General Data Protection Regulation,” EC.EUROPA.EU Vendors have responded with regionalized control planes and edge options, but premium pricing and maintenance complexity neutralize some of the cost savings that cloud models promise. The fragmentation risk is greatest in sectors that hold sensitive data, such as healthcare, banking, and public administration.

Shortage of Domain-Specific AI Training Data for Non-English Knowledge Work

Stanford researchers recorded 30-40% performance drops on legal summarization tasks in Spanish, Arabic, and Hindi when compared with English, underscoring data scarcity in those languages. UNDP estimated that only 12% of publicly available automation datasets include non-English examples, suppressing adoption in emerging markets. Enterprises must either bankroll expensive data annotation projects or tolerate higher error rates that erode automation ROI. Startups offering synthetic data face verification hurdles, because domain experts are needed to validate machine-generated labels. Public-sector funding in Africa and ASEAN nations is beginning to address the gap, but progress is incremental relative to rising demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Automation Suites Anchor Spending While Skill Platforms Surge

Intelligent automation suites held 41.37% of 2025 revenue, confirming their role as the first step on most transformation roadmaps. Enterprises value the suites’ integrated process mining and document intelligence modules, which surface high-ROI use cases and supply training data to models that handle exceptions. Vendors are folding conversational AI work assistants into the same stack, enabling the enterprise AI workplace platforms market size for agentic chatbots to climb rapidly in customer-facing scenarios. Skill development platforms, however, register the steepest climb at a 33.98% CAGR, reflecting a strategic pivot toward reskilling workers displaced by automation. Coursera logged a 180% enrollment jump in generative AI courses during 2025. That surge signals institutional commitment to internal talent marketplaces that match verified competencies with project needs across business lines.

Workforce analytics platforms now fuse predictive modeling with real-time productivity telemetry, encouraging proactive interventions before attrition or performance dips occur. Integrated talent marketplaces blend these insights with gig-style assignments, reducing idle time and improving internal mobility. Microsoft Viva’s crossover success, 40 million monthly active users by late 2025, shows that employers want a unified pane of glass for learning, engagement, and analytics.[3]Investor Relations, “Viva Adoption Data,” MICROSOFT.COM Cross-suite convergence is intensifying competition,because buyers prefer end-to-end provisioning over stitching together point solutions. As convergence advances, the enterprise AI workplace platforms market share for standalone point products is likely to compress.

By Deployment Model: Hybrid Gains as Sovereignty Trumps Cloud Economics

Cloud remained dominant at 63.52% in 2025 thanks to elastic consumption billing and rapid onboarding. Yet stricter localization laws and real-time inference needs are pushing organizations toward hybrid solutions, which are registering a 33.38% CAGR. Financial institutions now keep sensitive workloads on-premise while leveraging public clouds for analytics that fall outside supervisory scope. The EU AI Act’s high-risk classification is catalyzing European buyers to enact similar split architectures, forcing vendors to offer compliance toolkits that span edge and cloud.

Manufacturers and hospitals are adopting edge servers for latency-critical inspection and diagnostic tasks, forwarding anonymized data to cloud clusters for retraining. A significant portion of AI workplace adopters prefer a hybrid approach to balance cost, compliance, and performance. Infrastructure vendors such as Dell Technologies and HPE are bundling AI-optimized hardware with orchestration software, opening a parallel revenue stream adjacent to hyperscaler services. Vendors that supply single-pane policy management across deployment types stand to gain incremental stickiness as enterprises avoid siloed admin consoles.

By Organization Size: SMEs Close Gap Through Democratized Tooling

Large enterprises still accounted for 58.29% of 2025 spending, armed with dedicated centers of excellence and bargaining power that secure favorable terms of consumption. These firms codify playbooks, enforce tight governance, and negotiate outcome-linked service-level agreements that reduce vendor lock-in. The enterprise AI workplace platforms market, however, is growing faster for small and medium enterprises as low-code tooling helps flatten the skills gap. SMEs forecast a 33.57% CAGR, helped by per-use billing that eliminates upfront license commitments.

BCG research reveals productivity gains of 25-35% within twelve months among mid-market adopters, mirroring outcomes at large multinationals. Still, failure rates remain higher for SMEs when change management resources are scarce. Managed-service providers are filling that void, offering turnkey deployments and shared support centers. Large corporations are experimenting with delegated procurement, letting individual business units buy platforms within corporate guardrails that maintain security standards while encouraging agile experimentation.

By End-User Industry: Healthcare Surges as Regulatory Tailwinds Unlock Use Cases

IT and telecom accounted for 23.43% of 2025 demand, leveraging automation for network management and customer onboarding. In contrast, healthcare and life sciences register the fastest growth at a 34.28% CAGR through 2031, catalyzed by new reimbursement codes for AI-assisted documentation from the U.S. Centers for Medicare and Medicaid Services. Conversational scribes reduce physician charting time by 2 hours per day, boosting patient throughput and clinician satisfaction.

Banks employ natural-language processing to automate anti-money-laundering checks, while manufacturers link workforce analytics to industrial IoT telemetry to predict skill shortages during planned equipment downtime. Retailers deploy AI agents that handle product inquiries and returns, freeing human staff for value-adding consultative roles. Public-sector adoption remains limited due to heightened bias and transparency concerns, but pilot programs in Estonia and the United Arab Emirates demonstrate material service improvements, as cited by the World Economic Forum. Cross-industry momentum suggests widening horizontal applicability, yet compliance mandates shape the solution mix in every vertical.

Geography Analysis

North America accounted for 35.73% of global revenue in 2025, maintaining its position as a leading region in the market. This dominance is attributed to several factors, including high wages that drive demand for automation, a well-established, mature cloud ecosystem, and the rapid adoption of productivity-suite co-pilots. These co-pilots enhance operational efficiency and streamline workflows, making them highly sought after by enterprises in the region. Additionally, North America benefits from a robust venture capital ecosystem that actively supports the development and supply of specialized orchestration add-ons. These add-ons further enhance platform functionality and utilization rates, solidifying the region's leadership in the market.

Asia-Pacific is the fastest-growing region, with a 33.98% CAGR projected for 2026-2031. Wage inflation in traditional outsourcing centers is shrinking the labor arbitrage cushion, prompting companies in India, the Philippines, and Vietnam to automate back-office tasks. Government programs reinforce demand. India’s National Strategy for Artificial Intelligence earmarked USD 1.2 billion for sectoral AI adoption incentives, while Japan’s subsidy program reimburses up to 50% of platform costs for small manufacturers.[4]Strategy Paper, “AI for All,” NITI.GOV.IN In China, local vendors integrate AI workplace tools into domestic collaboration suites, sidestepping foreign cloud restrictions.

Europe faces a more nuanced path. The EU AI Act imposes conformity assessments, documentation, and post-market monitoring for high-risk deployments, adding six-to-twelve-month lead times and inflating compliance budgets. Still, public funding for trustworthy AI research ensures that enterprises view automation as inevitable, not optional. South America’s growth is concentrated in Brazil and Argentina, where currency volatility motivates CFOs to hedge with productivity gains. Middle East buyers, led by Saudi Arabia and the United Arab Emirates, embed AI agents in e-government services to raise service delivery standards. Africa remains nascent, although South Africa and Kenya display early momentum through partnerships with regional system integrators.

Competitive Landscape

The top ten vendors captured roughly 55% of the market share in 2025, signaling moderate concentration. Pure-play robotic process automation incumbents are re-architecting platforms around generative AI to fend off productivity-suite behemoths. Microsoft is embedding Copilot across Office, Dynamics, and the Power Platform, allowing it to bundle orchestration into existing subscriptions and pressure standalone providers. Salesforce’s Agentforce integrates autonomous agents directly into its CRM, effectively blurring the line between customer-experience software and automation platforms.

Disruptive startups fill white spaces such as IT service management, employee support, and multilingual conversational agents. Aisera focuses on target ticket triage and capacity, while Hyperscience focuses on intelligent document processing for regulated industries. Patent filings underscore the innovation race. UiPath logged 47 multi-agent orchestration patents in 2025, highlighting a pivot toward adaptive learning systems. Strategic partnerships extend reach. AWS, Google Cloud, and Microsoft Azure feature marketplace listings that offer co-sell incentives, expanding the channel footprint for smaller vendors.

Mergers and acquisitions accelerate portfolio convergence. NICE acquired Hyperscience to fold document intelligence into its contact-center automation suite. Automation Anywhere bought Soroco to deepen process discovery capabilities. Investors favor capital-efficient growth models that leverage consumption revenue, reflecting buyer preference for variable cost structures. As enterprises rationalize technology stacks to minimize integration toil, platform breadth and governance maturity will become decisive differentiators.

Enterprise AI Workplace Platforms Industry Leaders

UiPath Inc.

Automation Anywhere, Inc.

SS&C Blue Prism Group Ltd.

NICE Ltd.

Pegasystems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: UiPath partnered with SAP to embed automation directly in SAP S/4HANA Cloud, streamlining procure-to-pay and order-to-cash workflows.

- February 2026: Microsoft extended Copilot for Microsoft 365 with autonomous multi-app workflow agents that cut meeting coordination time by 35%.

- January 2026: Automation Anywhere acquired Soroco for USD 250 million, adding desktop process intelligence to its discovery stack.

- December 2025: Salesforce released Agentforce 2.0 with verticalized autonomous agents for healthcare, finance, and retail.

Global Enterprise AI Workplace Platforms Market Report Scope

The Enterprise AI Workplace Platforms Market Report is Segmented by Deployment Mode (On-Premise, Cloud, and Hybrid), Component (Software and Services), End-User Industry (IT and Telecom, Healthcare and Life Sciences, Manufacturing, BFSI, Retail and E-Commerce, Education, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Intelligent Automation Suites |

| Conversational AI Work Assistants |

| AI-Driven Skill Development Platforms |

| Workforce Analytics and Optimization Platforms |

| Integrated Talent Marketplace Platforms |

| Cloud |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing |

| Public Sector |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Platform | Intelligent Automation Suites | ||

| Conversational AI Work Assistants | |||

| AI-Driven Skill Development Platforms | |||

| Workforce Analytics and Optimization Platforms | |||

| Integrated Talent Marketplace Platforms | |||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Public Sector | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the enterprise AI workplace platforms market in 2026?

The market is expected to reach USD 5.56 billion in 2026 with momentum toward USD 23.12 billion by 2031.

Which platform type currently commands the highest revenue share?

Intelligent automation suites accounted for 41.37% of 2025 revenue due to integrated process discovery and orchestration capabilities.

What is the fastest-growing end-user industry for these platforms?

Healthcare and life sciences show the highest forecast growth, advancing at a 34.28% CAGR through 2031 on the back of new reimbursement incentives.

Why are hybrid deployment models gaining prominence?

Data-sovereignty regulations and real-time inference needs lead enterprises to split workloads between on-premise and cloud, driving hybrid growth at a 33.38% CAGR.

How are small and medium enterprises adopting AI workforce tools?

SMEs leverage low-code platforms and managed services to overcome skill gaps, fueling a 33.57% CAGR in their spending on these solutions.

Which region is forecast to grow the fastest?

Asia-Pacific is projected to expand at a 33.98% CAGR from 2026 to 2031 as wage inflation and government incentives accelerate automation adoption.

Page last updated on: