Information Security Consulting Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

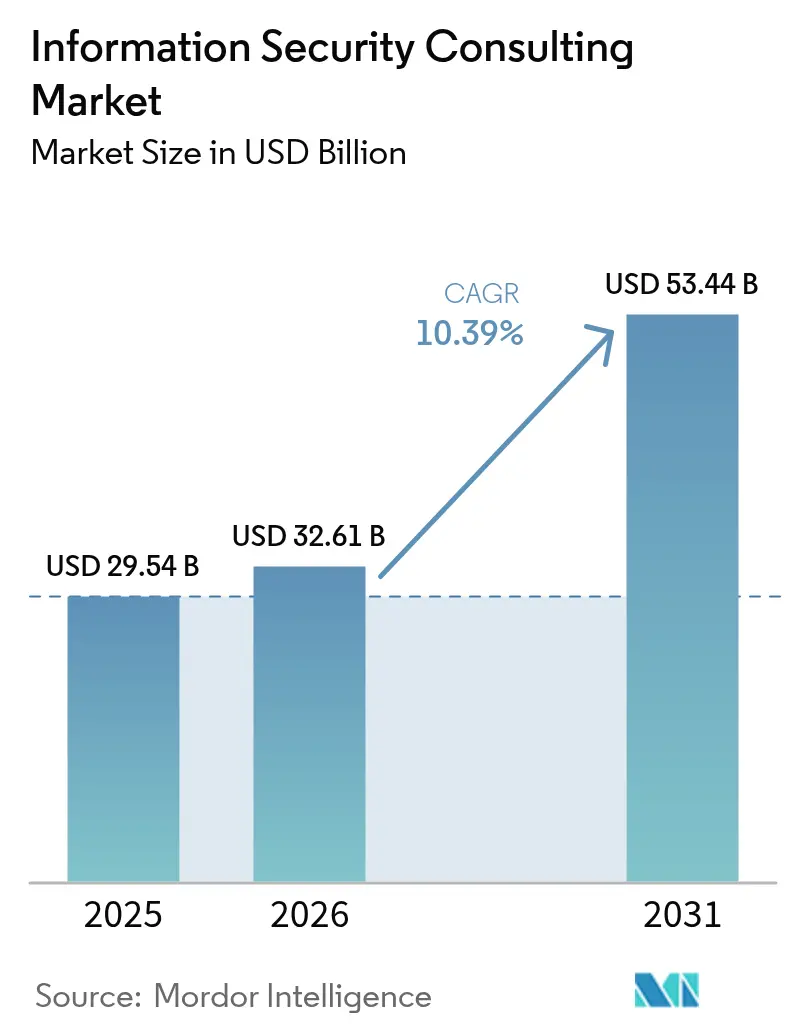

| Market Size (2026) | USD 32.61 Billion |

| Market Size (2031) | USD 53.44 Billion |

| Growth Rate (2026 - 2031) | 10.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

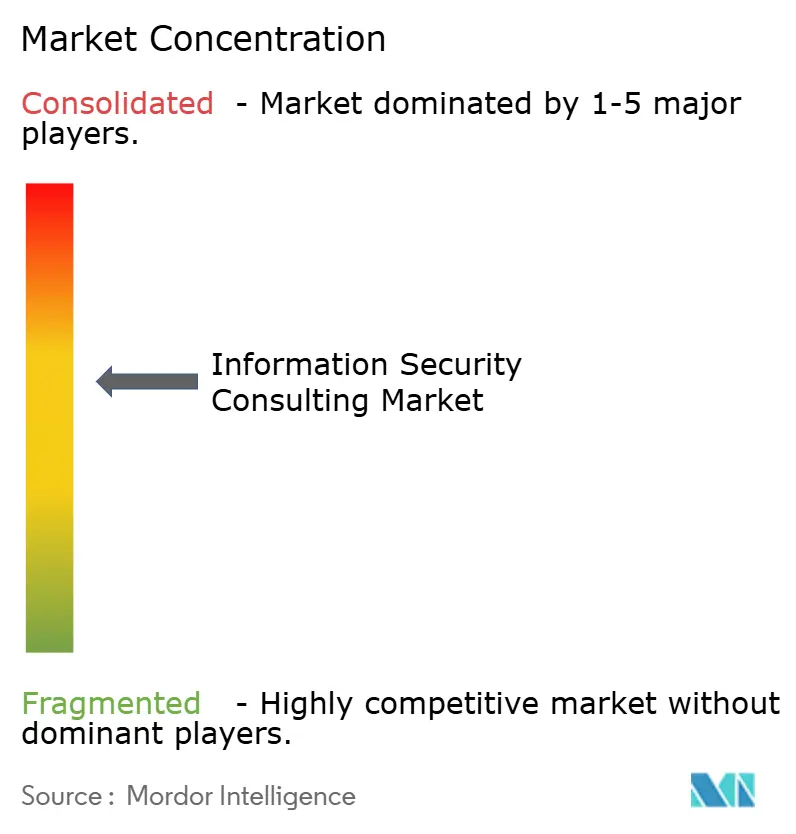

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Information Security Consulting Market Analysis by Mordor Intelligence

The information security consulting market size was valued at USD 29.54 billion in 2025 and estimated to grow from USD 32.61 billion in 2026 to reach USD 53.44 billion by 2031, at a CAGR of 10.39% during the forecast period (2026-2031). Heightened attack sophistication, far-reaching regulatory mandates, and hybrid work environments continue to shift spending from reactive breach response toward proactive threat intelligence, zero-trust design, and risk management advisory. Demand intensifies as artificial intelligence-enabled attacks, looming quantum risks, and sprawling multi-cloud estates outpace the in-house expertise of most enterprises. Strategic alliances between consultants and technology vendors accelerate platform-enabled service delivery, allowing firms to bundle assessment, implementation, and managed detection capabilities in a single engagement. At the same time, buyers increasingly favor outcome-based contracts that promise measurable reductions in dwell time, breach cost, and compliance exposure.

Key Report Takeaways

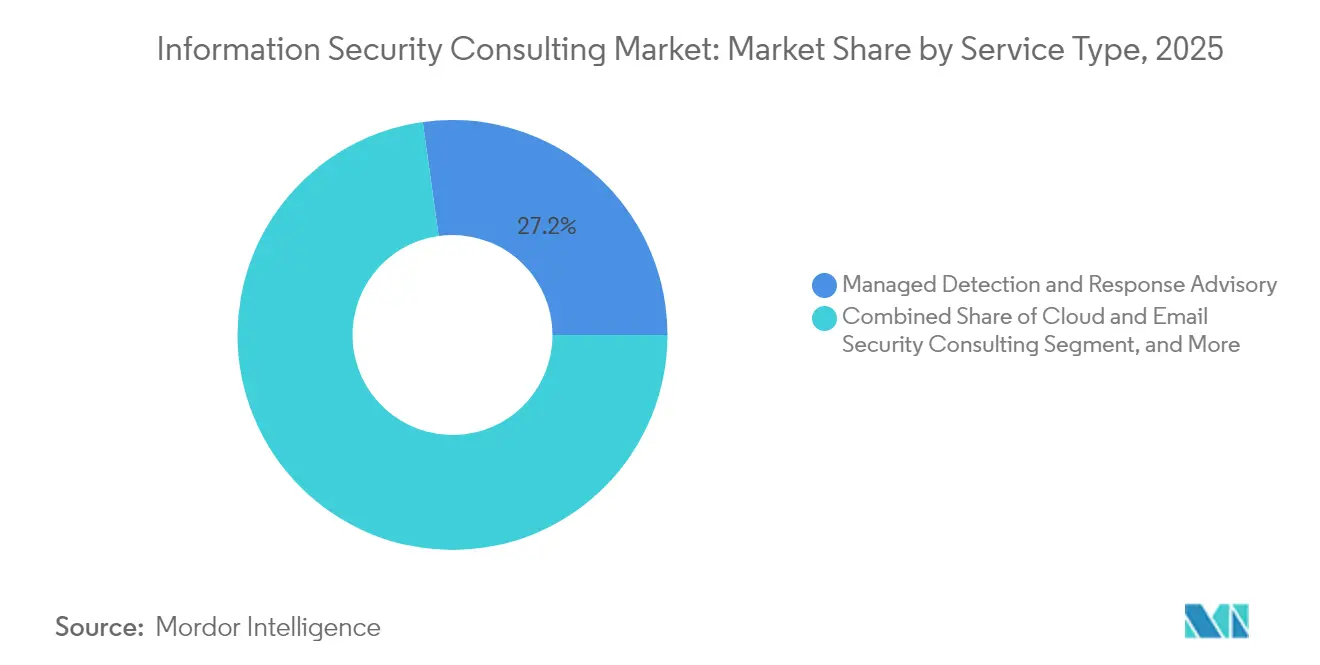

- By service type, managed detection and response advisory led with 27.21% information security consulting market share in 2025, while Cloud and Email Security consulting is advancing at a 10.66% CAGR through 2031.

- By deployment mode, cloud delivery accounted for 61.05% of the information security consulting market size in 2025 and is expanding at an 11.34% CAGR to 2031.

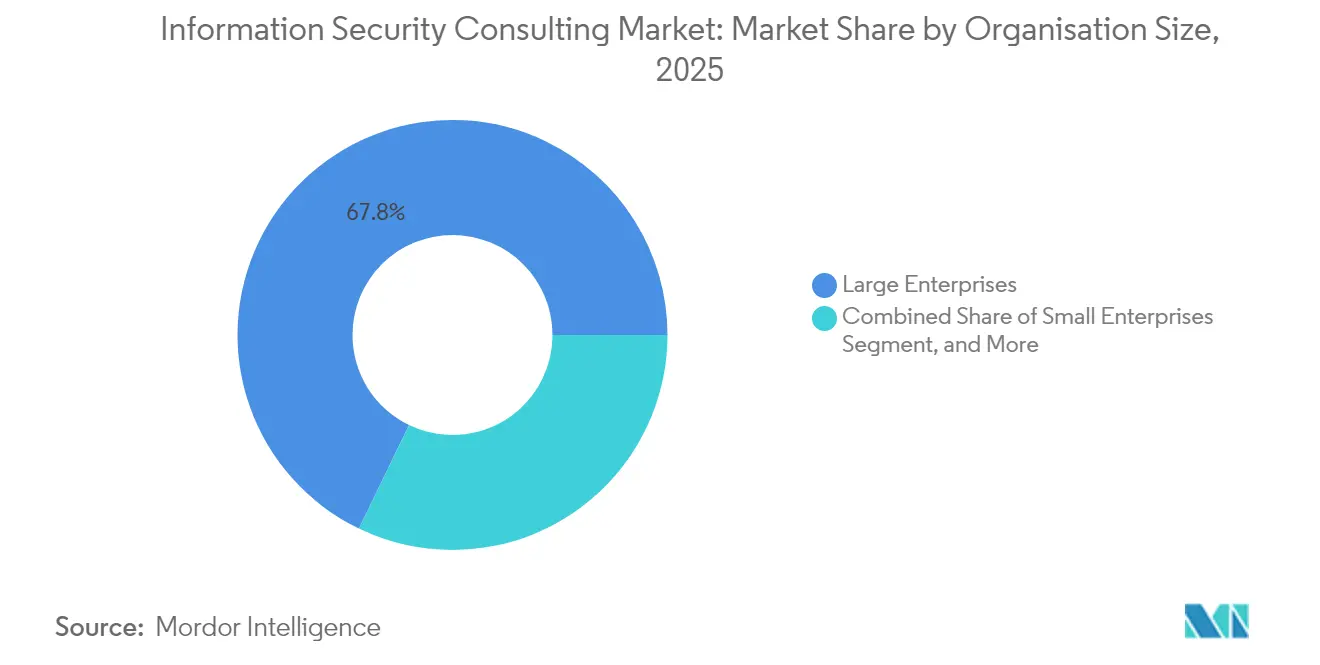

- By organization size, large enterprises commanded 67.84% share of the information security consulting market size in 2025; small and medium enterprises are pacing the field with an 11.28% CAGR through 2031.

- By vertical, BFSI held 24.41% revenue share in 2025 in the information security consulting market; healthcare and life sciences is forecast to expand at a 10.71% CAGR between 2026 and 2031.

- By geography, North America retained 39.55 of % information security consulting market share in 2025, while the Asia-Pacific is projected to post the fastest 10.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Information Security Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising network and cloud complexities | +2.8% | Global, strongest in North America and EU | Medium term (2-4 years) |

| Escalating regulatory and compliance mandates | +2.1% | EU, North America, Asia-Pacific core markets | Long term (≥ 4 years) |

| Accelerated digital transformation and hybrid work adoption | +1.9% | Global, emerging-market acceleration | Short term (≤ 2 years) |

| GenAI safety and model governance advisory demand | +1.7% | North America, EU, spillover to APAC | Medium term (2-4 years) |

| Cyber-insurance underwriting requirements for SMEs | +1.4% | North America, EU, Australia | Short term (≤ 2 years) |

| Quantum readiness and post-quantum cryptography migration | +0.7% | Global, early uptake in government and finance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Network and Cloud Complexities

Sprawling multi-cloud estates, identity sprawl, and API interconnections multiply blind spots that traditional perimeter safeguards miss, fuelling premium demand for architects who can implement zero-trust frameworks and cloud-native controls. Advisory engagements increasingly bundle continuous posture management, workload segmentation, and DevSecOps enablement so clients can remediate misconfigurations before attackers exploit them. Deloitte’s MDR expansion illustrates how integrators pair consulting with always-on monitoring to shrink detection backlogs and reduce incident cost. Industrial IoT rollouts compound the complexity problem as operational-technology devices ship without embedded security, requiring consultants to converge IT and OT defenses. With cloud security projected to grow more than 25% annually through 2027, advisory partners that master container hardening, serverless protection, and platform automation secure first-mover advantage.[1]European Union Agency for Cybersecurity, “Cybersecurity Investments 2024,” enisa.europa.eu

Escalating Regulatory and Compliance Mandates

The European Union’s NIS2 Directive and Digital Operational Resilience Act jointly extend cybersecurity obligations to more than 100,000 entities, mandating incident reporting inside 24 hours and imposing stiff penalties for non-compliance. Organizations straddling multiple jurisdictions require gap assessments, remediation roadmaps, and automated evidence gathering to satisfy both frameworks without duplicating cost. Financial institutions face dual filings where DORA and NIS2 overlap, sharpening demand for advisory playbooks that reconcile encryption, logging, and third-party oversight provisions.[2]Vanta, “DORA and NIS 2 Explained,” vanta.com Outside Europe, the U.S. Securities and Exchange Commission’s cyber-disclosure rule and Australia’s critical-infrastructure reforms have similar ripple effects, pushing boards to seek independent assurance and continuous attestation services. As legislators revisit privacy, AI, and critical-supply-chain statutes, compliance complexity will remain a long-term growth flywheel for the information security consulting market.

Accelerated Digital Transformation and Hybrid Work Adoption

Hybrid work dissolves fixed perimeters and forces enterprises to elevate identity as the new control plane. Consulting demand surges for zero-trust strategy design, privileged-access cleanup, and high-assurance authentication rollouts that span SaaS, on-premises, and mobile users. Boards increasingly request KPI-driven metrics, such as lateral-movement dwell time or credential-stuffing success rate, when approving transformation budgets, placing added pressure on advisers to quantify risk reduction. Organizational change management emerges as a critical success factor; consultants must re-engineer processes so distributed workforces uphold least-privilege, resiliency, and data-residency mandates simultaneously. The information security consulting market thereby shifts from technology blueprints to holistic operating-model realignment that embeds security guardrails into DevOps, finance, and HR workflows.

GenAI Safety and Model Governance Advisory Demand

Enterprises racing to embed generative AI into products discover new threats: prompt injection, training-set poisoning, and model output manipulation. Consulting teams now blend data-science, privacy, and threat-hunting skills to craft AI-security frameworks covering model lifecycle, supply-chain vetting, and bias mitigation. A 2025 collaboration among Google, Microsoft, and the Polish government underscores the public-sector push to operationalize AI securely, opening doors for consultants versed in national-security standards. Advisory briefs increasingly include red-team simulations against large-language models and policy templates that align algorithmic decision-making with sector-specific regulations such as HIPAA or PSD2. As vendors release AI-enabled security operations platforms, consultants pivot to outcome-oriented service-level agreements that tie model-risk reductions to business KPIs, deepening recurring-revenue streams within the information security consulting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints among SMEs | -1.8% | Global, highest in emerging markets | Short term (≤ 2 years) |

| Shortage of qualified security talent | -1.2% | Global, acute in specialist domains | Medium term (2-4 years) |

| Tool-sprawl fatigue driving vendor consolidation | -0.9% | North America, EU mature markets | Medium term (2-4 years) |

| Rising liability exposure deterring smaller consultancies | -0.6% | North America, EU, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints among SMEs

Regulatory expansion pushes smaller firms to seek guidance, yet 34% of respondents in a 2024 ENISA study lacked funds to implement even basic NIS2 controls. To bridge that gap, advisers roll out subscription-based compliance-as-a-service bundles combining baseline assessments, virtual CISO hours, and automated evidence capture at predictable monthly rates. SaaS pricing lowers entry barriers, but margin pressure rises as consultancies absorb tooling and talent costs. Governments in Canada, Singapore, and Germany partially offset the restraint through tax incentives and matching grants, yet access varies widely, leaving emerging-market SMEs most vulnerable. Over the next two years, vendors that refine repeatable playbooks and leverage AI co-pilots for documentation stand to unlock underserved micro-segments of the information security consulting market.

Shortage of Qualified Security Talent

By 2025, global unfilled cyber positions exceed 4 million, with specialist gaps in cloud forensics, quantum-safe cryptography, and operational-technology defense. Consulting firms compete directly with hyperscalers and fintechs, forcing them to double intern cohorts, subsidize advanced certifications, and roll out skill-share alliances with universities. Talent scarcity lengthens engagement timelines and inflates day-rates, complicating fixed-fee bids. To counter headcount bottlenecks, leading advisers embed playbook automation, reusable infrastructure-as-code templates, and AI-driven control verifiers, enabling junior analysts to handle tasks once reserved for senior architects. While these strategies soften supply constraints, the talent gap will continue to shave roughly 1.2 percentage points off the long-run CAGR of the information security consulting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: MDR Advisory Dominates Amid Cloud-Security Surge

Managed Detection and Response advisory captured 27.21% information security consulting market share in 2025, reflecting client preference for outcome-based engagements that bundle 24×7 monitoring, threat hunting, and incident-response playbooks. The segment benefits from ransomware’s persistence, insurance demands for continual surveillance, and board-level pressure to demonstrate time-to-contain KPIs. MDR advisers increasingly integrate backup immutability, automated isolation, and forensic triage to shorten response cycles and prove return on investment. Conversely, standalone firewall or network-hardening projects face commoditization as cloud platforms embed baseline controls. Cloud and Email Security consulting, projected to grow at 10.66% annually, capitalizes on identity sprawl, misconfigured storage buckets, and business-email compromise attacks that proliferate in remote-work settings. Consultants differentiating through DevSecOps enablement, API visibility, and context-rich phishing simulations secure larger share-of-wallet. Governance, Risk, and Compliance retains stable demand as overlapping statutes multiply; however, forward-leaning firms now wrap continuous control monitoring and regulatory change-tracking into retainer contracts, creating stickier revenue. Finally, emerging sub-segments such as quantum-readiness, OT threat modeling, and AI-safety governance offer premium margins but require scarce expertise, positioning early movers to outperform the broader information security consulting market.

By Deployment Mode: Cloud Supremacy Accelerates Platform Consolidation

Cloud deployments accounted for 61.05% of the information security consulting market size in 2025 and are projected to expand at an 11.34% CAGR through 2031 as enterprises re-platform ERP, analytics, and dev environments. Consultants with deep hyperscaler alliances help clients align native security-reference architectures, identity governance, and workload segmentation, slashing time-to-production. Data-residency mandates and latency-sensitive OT workloads sustain a residual on-premises niche, yet even those projects increasingly embed cloud-delivered analytics and backup. Hybrid deployments therefore evolve toward unified control planes where cloud security posture management dashboards ingest signals from legacy firewalls, CASBs, and endpoint-detection agents. This convergence drives vendor consolidation: buyers favor advisers who prescriptively rationalize overlapping toolsets and streamline license portfolios. As a result, the information security consulting market gravitates toward multi-year transformation roadmaps that blend migration planning, control orchestration, and managed operations under shared success metrics.

By Organization Size: Enterprise Dominance Masks SME Growth Acceleration

Large enterprises remained the single largest client group at 67.84% in 2025, sustaining complex programs that span zero-trust blueprints, red-team testing, and supply-chain assurance. They routinely engage global consultancies capable of coordinating regulatory harmonization, multi-cloud telemetry integration, and continuous control validation across hundreds of subsidiaries. However, SMEs represent the fastest-expanding cohort, posting an 11.28% CAGR as cyber-insurance underwriting clauses mandate formal risk assessments, privileged-access baselines, and incident-response runbooks. To serve price-sensitive buyers, advisers deploy templated policy libraries, virtual audit rooms, and AI-assisted questionnaire auto-fill that compress delivery cost without diluting quality. Medium-sized firms sit at the innovation frontier: they pilot secure-coding guilds, infrastructure-as-code security gates, and usage-based MDR subscriptions before such models scale upward. Across all tiers, outcome-based fee structures tied to audit-finding closure rates and SLA adherence gain popularity, reshaping cash-flow profiles within the information security consulting market.

By End-User Vertical: Healthcare Disruption Challenges BFSI Leadership

Financial-services clients held a 24.41% revenue share in 2025, underpinned by payment-system criticality, strict supervisory stress tests, and mandatory 24-hour incident reporting. Banks demand layered controls, transaction integrity monitoring, fraud analytics, and quantum-safe key management, creating annuity-like consulting pipelines. Yet healthcare’s 10.71% CAGR through 2031 marks the sector as the most lucrative expansion arena. Hospitals grapple with Internet-connected diagnostic equipment, electronic-health-record interoperability, and ransomware that threatens patient safety, compelling boards to enlist advisers fluent in HIPAA, FDA premarket guidance, and medical-device hardening. Telecommunications, government, and energy operators likewise seek sector-specific blueprints: 5G core slicing security, classified-network segmentation, and substation anomaly detection, respectively. Consultants able to tailor control catalogs and threat models to each domain earn premium bill rates, advancing the competitive stratification of the information security consulting market.

Geography Analysis

North America retained 39.55% information security consulting market share in 2025, buoyed by mature enterprise budgets, a USD 13 billion federal civilian-cyber allocation, and an active venture-capital pipeline that catalyzes start-up partnerships. U.S. critical-infrastructure mandates and Canada’s national quantum-strategy funding channel sustained demand for post-quantum readiness and operational-technology segmentation projects. Cross-border data-flow agreements, such as the U.S.-EU Data Privacy Framework, further elevated advisory revenue as multinationals sought harmonized compliance roadmaps.

Asia-Pacific is forecast to post an 10.90% CAGR through 2031, reflecting digital-government initiatives, 5G rollouts, and heightened nation-state threats. Japan’s active-defense doctrine and record cyber budget expand the addressable consulting pool for incident-readiness, while India’s Digital Personal Data Protection Act fuels demand for privacy-impact assessments and data-localization strategies. Australia’s updated Critical Infrastructure Act widens coverage to more than 11 sectors, prompting small utilities and ports to solicit outsourced CISO services. Rapid cloud adoption across Southeast Asia simultaneously amplifies advisory needs for identity federations, workload encryption, and regional SOC integration.

Europe maintains steady momentum as NIS2 and DORA propel multi-year compliance roadmaps; more than 100,000 entities must re-architect governance, risk, and third-party oversight programs, ensuring robust consulting pipelines. Germany’s subsidized cyber-resilience grants and France’s post-ransomware hospital funding open fresh vertical niches. Meanwhile, Central and Eastern Europe benefit from substantial technology investments: Google and Microsoft pledged significant capital to Polish cyber-ecosystem development, creating spillover opportunities for local and international advisers. Although South America and the Middle East and Africa presently capture smaller revenue pools, aggressive digitalization plans in Brazil, Saudi Arabia, and Kenya, including sovereign cloud projects and smart-city rollouts, set the stage for above-average consulting spend once economic conditions stabilize. Together, these regional dynamics underscore the globally distributed yet locally nuanced growth profile of the information security consulting market.

Competitive Landscape

The information security consulting market is highly fragmented, with more than 600 firms marketing managed detection and response offerings that range from true 24×7 analyst services to re-branded tooling. Global systems integrators, Accenture, IBM, Deloitte, PwC, and KPMG, anchor the upper tier through multi-disciplinary practices, proprietary threat-intelligence units, and global delivery centers. Yet specialized boutiques thrive by focusing on sector niches such as medical-device security, OT threat modeling, or quantum-readiness assessments, often capturing Fortune 1000 logos through demonstrable depth rather than breadth.

Strategic technology alliances define the current competitive battleground. NTT DATA’s expanded Rubrik partnership integrates immutable backup and ransomware containment into consulting playbooks, offering clients implementation plus ongoing recovery orchestration in a single statement of work. Protiviti’s integration of CYFIRMA threat intelligence feeds into its risk dashboards exemplifies the pivot toward platform-enabled advisory powered by external telemetry. Similarly, BlueVoyant’s cloud-native cyber-defense platform underpins its Japanese expansion via a reseller agreement with Marubeni, illustrating how partnerships accelerate in-region credibility.

Automation and AI differentiate emerging disruptors that promise rapid control validation, continuous compliance evidence gathering, and real-time risk scoring. Established firms counter by injecting machine-aided content generation for policy libraries and deploying low-code connectors to unify disparate telemetry sources. As buyers demand measurable outcomes, reduction in mean-time-to-detect, policy-exception closure, insurance-premium discounts, competition shifts away from hourly billing toward milestone-based or shared-risk pricing. Looking forward, white-space opportunities in AI model-red-team engagements, quantum-risk migration, and supply-chain software bill-of-materials assurance will favor consultancies that develop scarce skill sets early, reinforcing the dynamism of the information security consulting market.

Information Security Consulting Industry Leaders

Ernst & Young Global Limited

International Business Machines Corporation

Accenture PLC

Atos SE

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Persol Cross Technology partnered with VarioSecure to harden Japanese medical institutions against ransomware and regulatory scrutiny.

- April 2025: BlueVoyant expanded operations in Japan and inked a reseller pact with Marubeni I-DIGIO to address supply-chain cyber risks.

- March 2025: NTT DATA deepened its Rubrik alliance to deliver ransomware-protection advisory, implementation, and managed services for Fortune 500 clients.

- February 2025: Google and Microsoft announced AI-driven cybersecurity investments totaling USD 700 million to bolster Poland’s national resilience.

Global Information Security Consulting Market Report Scope

Information security consulting offers an extensive range of consulting services designed to enhance the existing security infrastructure of businesses based on specific business requirements. The vendors in the market assist customers in conducting a thorough assessment to identify any possible risks their business or organization may be exposed to, followed by the development of a security plan and course of implementation to safeguard against potential damage or loss in the event of any crisis.

The market is segmented by type (security and compliance, firewall management, e-mail, and cloud security), deployment mode (on-premises, cloud), organization size (small and medium enterprises, large enterprises), end-user vertical (banking, financial services, and insurance, IT and telecom, aerospace and defense, and healthcare) and geography. The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

| Governance, Risk and Compliance (GRC) Consulting |

| Firewall and Network Security Consulting |

| Cloud and Email Security Consulting |

| Identity and Access Management Consulting |

| Penetration Testing and Vulnerability Assessment |

| Incident Response and Digital Forensics |

| Managed Detection and Response Advisory |

| Other Service Types |

| On-Premises |

| Cloud |

| Hybrid |

| Small Enterprises |

| Medium Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| IT and Telecommunications |

| Government and Defense |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing and Industrial |

| Energy and Utilities |

| Other End-user Verticals |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Governance, Risk and Compliance (GRC) Consulting | ||

| Firewall and Network Security Consulting | |||

| Cloud and Email Security Consulting | |||

| Identity and Access Management Consulting | |||

| Penetration Testing and Vulnerability Assessment | |||

| Incident Response and Digital Forensics | |||

| Managed Detection and Response Advisory | |||

| Other Service Types | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Small Enterprises | ||

| Medium Enterprises | |||

| Large Enterprises | |||

| By End-user Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| IT and Telecommunications | |||

| Government and Defense | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Manufacturing and Industrial | |||

| Energy and Utilities | |||

| Other End-user Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the information security consulting market?

The information security consulting market size is USD 32.61 billion in 2026, on track to reach USD 53.44 billion by 2031.

Which service line generates the highest revenue?

Managed Detection and Response advisory holds the lead with 27.21% market share in 2025.

Which region is growing fastest in consulting demand?

Asia-Pacific is forecast to expand at an 10.90% CAGR through 2031, outpacing all other regions.

How is cloud adoption influencing consulting engagements?

Cloud deployments already account for 61.05% of industry revenue and drive requests for multi-cloud posture management, container security, and zero-trust design.

Why are SMEs investing more in external security advice?

Cyber-insurance underwriting and expanding regulations such as NIS2 compel SMEs to adopt formal risk assessments and incident-response plans, fueling an 11.28% CAGR in SME consulting spend.

Page last updated on: