Abrasion Wear Resistant Steel Plates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5 Billion |

| Market Size (2031) | USD 7.62 Billion |

| Growth Rate (2026 - 2031) | 8.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Abrasion Wear Resistant Steel Plates Market Analysis by Mordor Intelligence

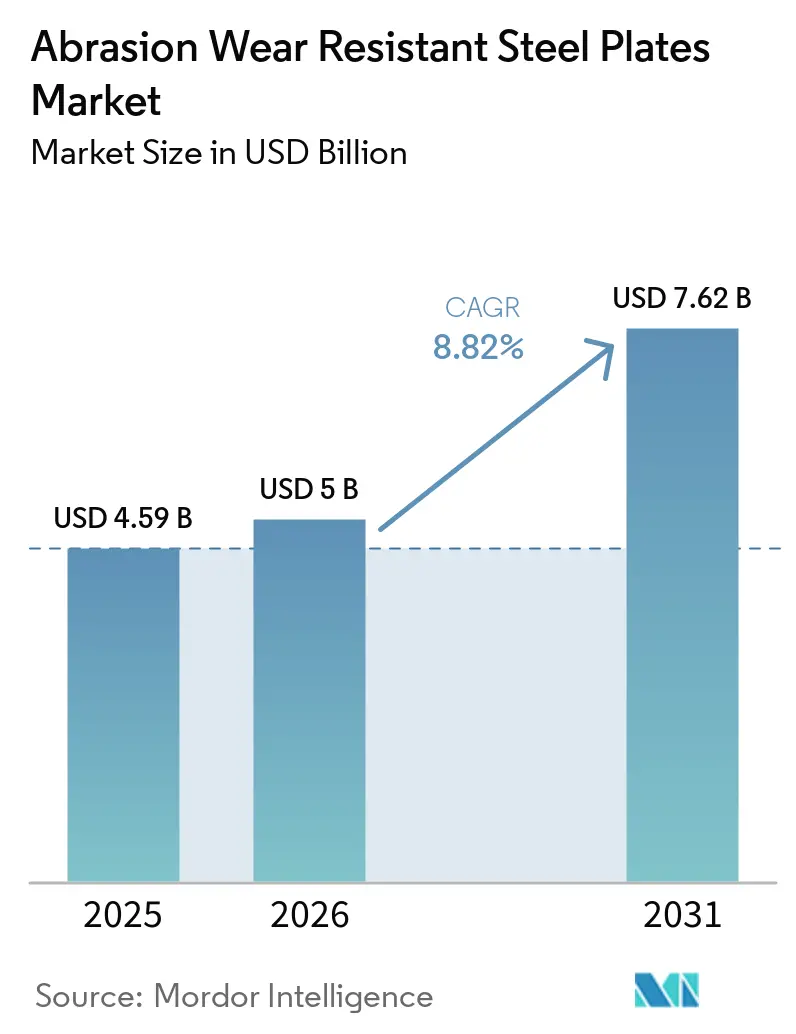

The Abrasion Wear Resistant Steel Plates Market size is projected to be USD 4.59 billion in 2025, USD 5 billion in 2026, and reach USD 7.62 billion by 2031, growing at a CAGR of 8.82% from 2026 to 2031. The mining and construction sectors are driving up average selling prices and accelerating capacity expansions, thanks to strong demand, unified safety standards, and steelmakers' shift towards premium-grade flat products. The Asia-Pacific region, led by China's infrastructure stimulus and India's "Make in India" initiative favoring locally certified ISAR-series grades, stands at the forefront. Original Equipment Manufacturers (OEMs) are now incorporating wear-plate selection in the design phase to cut life-cycle costs. Meanwhile, mills such as SSAB, POSCO, and Baosteel are investing heavily in downstream service centers and forming co-engineering partnerships, bolstering brand loyalty. Digital-twin analytics and sensor-equipped fleets have facilitated a shift from time-based to predictive replacement schedules, with a clear emphasis on ultra-hard grades surpassing HB 500. Additionally, early adopters are utilizing Electric Arc Furnace (EAF) conversions and scrap-based feedstock strategies, allowing them to command price premiums on low-carbon plates, especially in light of the mandatory Scope 3 reporting in the European Union and several U.S. states.

Key Report Takeaways

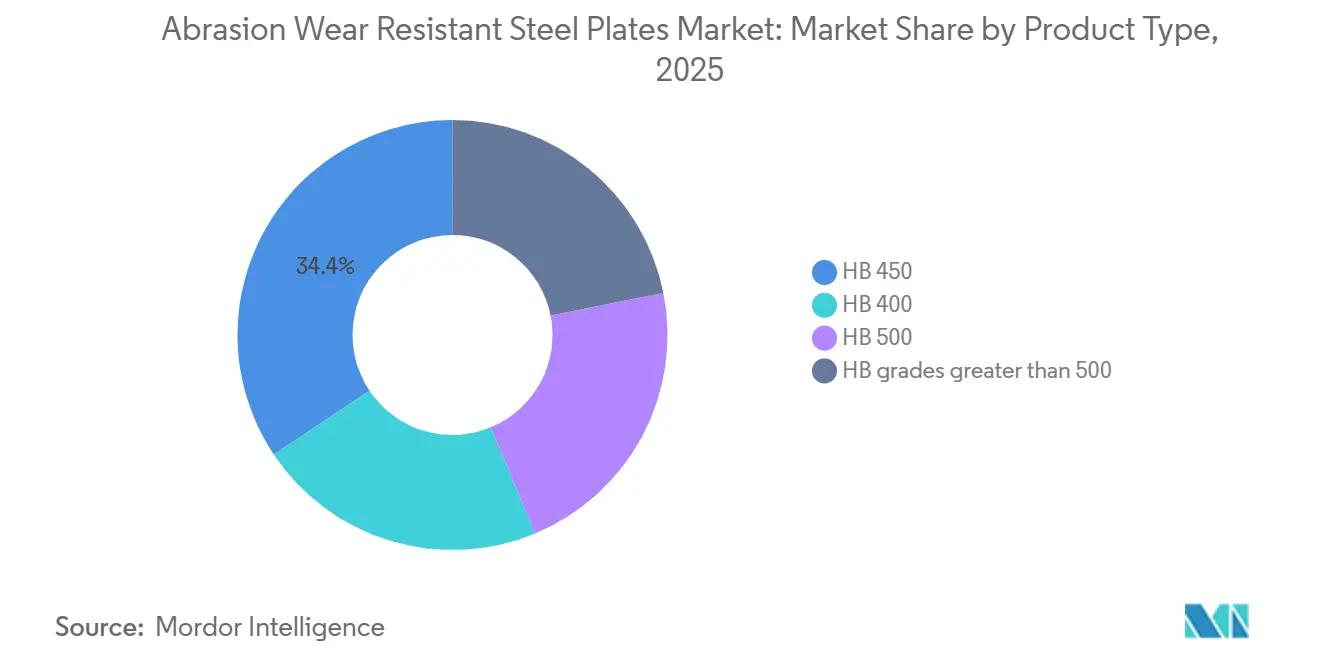

- By product type, HB 450 captured 34.39% of the abrasion wear-resistant steel plates market share in 2025, while HB grades greater than 500 are projected to post the fastest 10.47% CAGR from 2026 to 2031.

- By customer type, distributors held 48.47% share in 2025; OEM purchases are forecast to expand at a 9.66% CAGR between 2026 and 2031.

- By end-user industry, mining generated 41.65% demand in 2025, yet the recycling segment is set to grow at a 10.97% CAGR between 2026 and 2031.

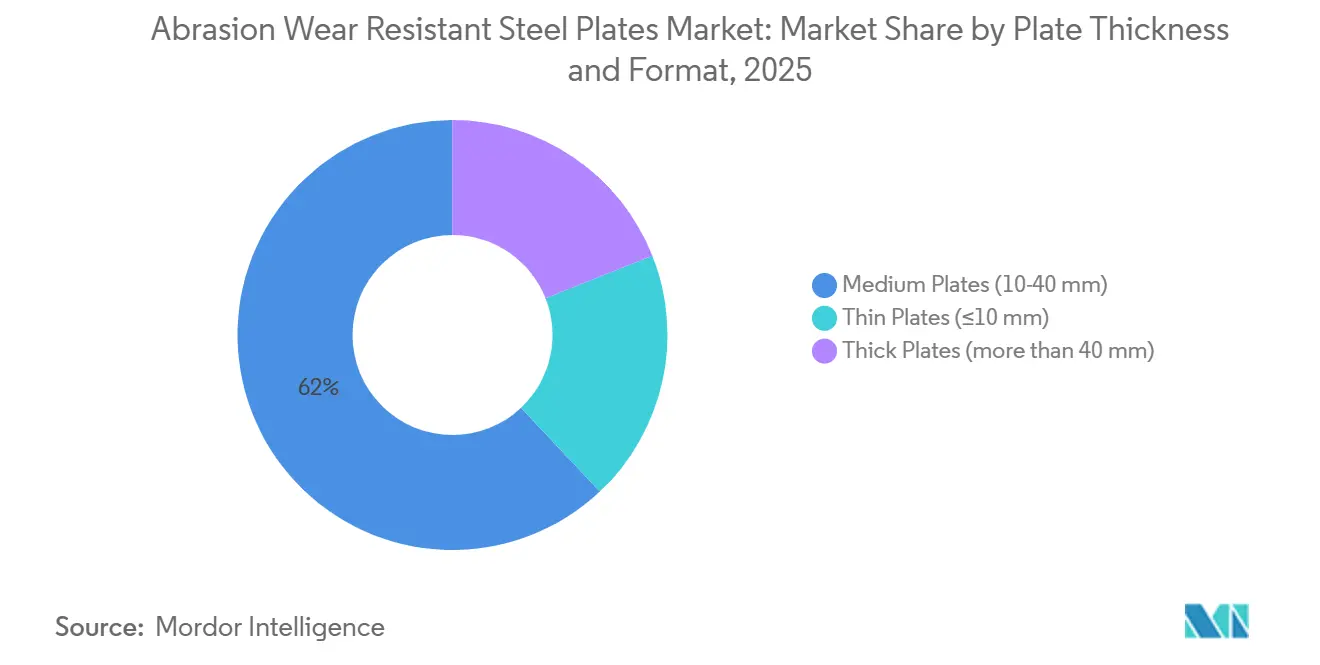

- By plate thickness, medium plates (10–40 mm) delivered 62.02% of 2025 revenue, whereas thin plates (≤10 mm) are on track for a 10.95% CAGR between 2026 and 2031.

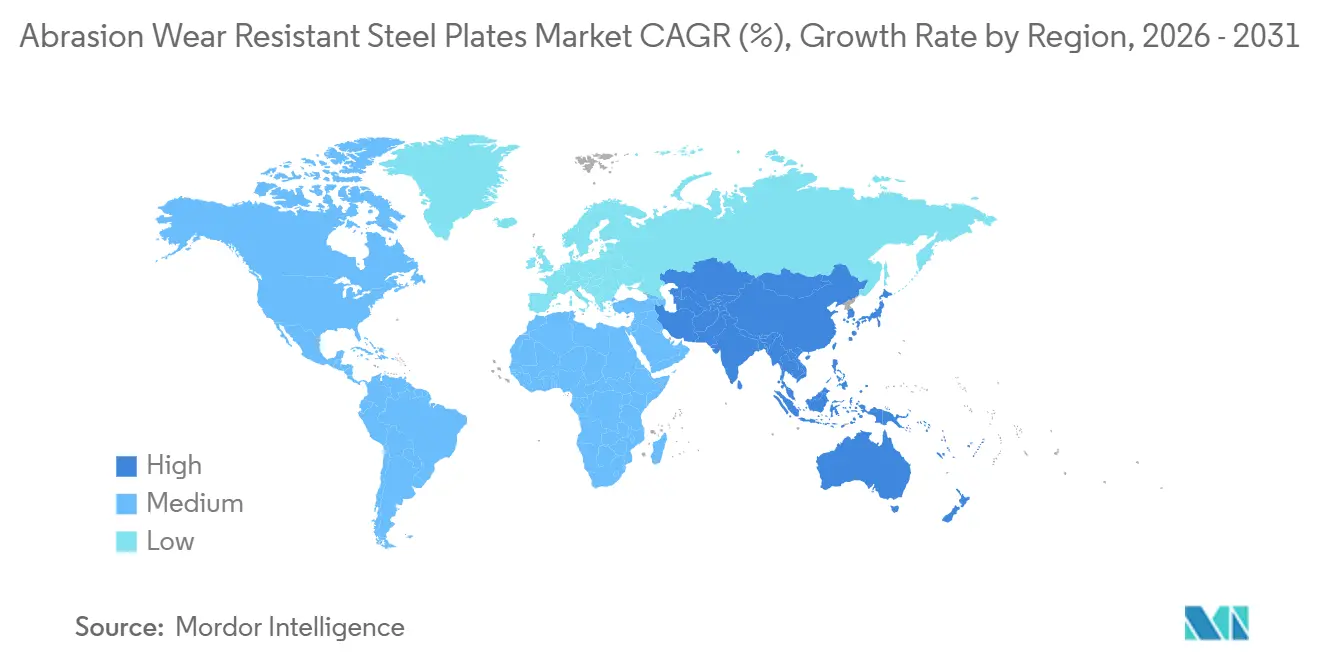

- By geography, Asia-Pacific commanded 58.53% of 2025 revenue and is forecast to grow at a 9.49% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Abrasion Wear Resistant Steel Plates Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from the mining and construction sectors | +2.8% | Global, with APAC core and spill-over to South America, MEA | Medium term (2–4 years) |

| Regulation-driven safety and wear standards expansion | +1.5% | North America, EU, India (IS 18809:2024), China (GB/T 24186-2022) | Long term (≥4 years) |

| Supply-chain localization incentives in heavy-equipment hubs | +1.2% | India, ASEAN, Mexico, Saudi Arabia | Medium term (2–4 years) |

| Circular-economy demand for recycled wear-plate feedstock | +0.9% | EU, North America, Japan | Long term (≥4 years) |

| Digital twins enabling predictive wear optimization | +0.7% | Global, early adoption in North America, EU mining fleets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Mining and Construction Sectors

New projects in the copper, lithium, and rare-earth sectors are driving up orders for dump-truck bodies, liners, and conveyor components. In the Asia-Pacific region, the production of excavators and loaders has surged to support transport and infrastructure initiatives. North-American OEMs are adopting higher-hardness plates to navigate regulatory weight constraints effectively. In a strategic move, ArcelorMittal Nippon Steel India has allocated funds to triple its capacity, aiming for faster domestic deliveries and reduced reliance on imports. Mining operators are increasingly favoring HB 500 and grades above 500. This preference enables them to extend operational intervals in remote sites, where downtime costs significantly exceed material premiums. As a result, this trend not only tightens the supply of ultra-hard grades but also reinforces price stability.

Regulation-Driven Safety and Wear Standards Expansion

IS 18809:2024 and GB/T 24186-2022 set new benchmarks by mandating hardness and impact-toughness criteria, tightening OEM bid specifications, and phasing out older mild-steel components. New regulations on traceability introduced heat-number stamping and certified test reports, which reduced counterfeiting risks and directed orders to rigorously audited high-capex plate mills[1]Convergence Steel, “IS 18809:2024 – Wear and Abrasion-Resistant Steel Standard,” convergencesteel.com. Safety agencies in the United States and the European Union updated equipment guidelines, designating HB 400 as the standard. As a result, heavy-duty applications increasingly favor HB 450 and harder variants.

Supply-Chain Localization Incentives in Heavy-Equipment Hubs

Governments are providing tax rebates and content-threshold credits for domestically melted plates. In a bid to reduce import reliance, Canada granted Titus Steel a subsidy in January 2026 for a new warehouse in Ontario[2]Titus Steel, “Government of Canada Invests to Help Strengthen Titus Steel's Edge,” titussteel.com. Meanwhile, POSCO's memorandum of understanding with Tata Daewoo aligns material design and logistics to expedite development cycles. This move serves as evidence of a broader trend where original equipment manufacturers increasingly favor partnerships with regional steel providers.

Circular-Economy Demand for Recycled Wear-Plate Feedstock

SSAB Zero, a green steel made from scrap and powered by fossil-free energy, is projected to achieve significant shipping volumes. This environmentally friendly steel has already been incorporated into Volvo Cars’ closed-loop program and Sandvik’s mining buckets. As original equipment manufacturers (OEMs) intensify their climate commitments, they are increasing premiums for near-zero-carbon plate grades. As a result, mills are focusing on higher-purity scrap flows and directing investments toward Electric Arc Furnace (EAF) technology.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs of ultra-hardness grades | -1.4% | Global, acute in regions with high energy costs (EU, Japan) | Short term (≤2 years) |

| Limited fabrication and welding flexibility at HB grades greater than 500 | -0.8% | Global, particularly affecting small fabricators in emerging markets | Medium term (2–4 years) |

| Scarcity of skilled welders for wear-resistant alloys | -0.6% | North America, EU, Australia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Production Costs of Ultra-Hardness Grades

The meticulous quench-and-temper protocols, the incorporation of chromium and molybdenum during alloying, and rigorous post-treatment inspections have driven up unit costs for certain products. In 2025, SSAB earmarked a substantial budget to upgrade its Oxelösund EAF with the aim of maintaining its premium capacity. At the same time, rising energy prices in the European Union have tightened mill margins, limiting the discounting flexibility for HB 550 and HB 600 plates.

Limited Fabrication and Welding Flexibility at HB grades greater than 500

Small job shops grapple with the intricacies of preheating and inter-pass welding, especially when dealing with ultra-hard grades. Peer-validated trials reveal that, although multi-pass overlay joints boast notably superior abrasion resistance over Hardox 400, they demand specialized fillers and rigorous hydrogen management. These technical hurdles stymie broader market acceptance, especially in emerging economies grappling with a shortage of qualified welders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ultra-Hard Grades Gain as Mines Target Longer Intervals

HB 450, which is projected to account for 34.39% of 2025's revenue, establishes its position as a key player in the mining and dump-body applications. The market for abrasion wear-resistant steel plates, particularly those with HB grades exceeding 500, is poised for robust growth at a 10.47% CAGR during the forecast period of 2026–2031. This growth is attributed to mines adopting harder, thinner liners that optimize truck payloads without compromising durability. In March 2026, SSAB unveiled Hardox HiAce, an innovation that combines the hardness of HB 450 with corrosion resistance up to 400 degrees Celsius. This advancement opens doors to wider applications, such as cement coolers and waste-handling bins.

Ultra-hard grades are benefiting from digital-twin analytics, which confirm that longer service intervals can offset the premium costs of these plates. However, challenges persist: complexities in welding and increased alloy surcharges lead to a notable price gap when compared to HB 400. Mills operating under IS 18809:2024 chemistry standards grapple with balancing boron and carbon-equivalent values to ensure toughness. This challenge necessitates investments in in-line quench equipment and automated inspection tools. Still, mining contractors are reaping the rewards. By switching to Hardox 500 Tuf, truck bodies have shed over 500 kilograms, translating to significant fuel savings. This not only strengthens the cost-of-ownership argument but also boosts confidence in the segment's growth.

By Customer Type: OEMs Accelerate as Co-Engineering Partnerships Deepen

In 2025, distributors accounted for 48.47% of global revenue, underscoring the fragmented nature of the aftermarket, where swift decisions are crucial. Meanwhile, the market share for OEM direct purchases of abrasion wear-resistant steel plates is increasing, with OEMs growing at a CAGR of 9.66% in the forecast period of 2026-2031. This growth is attributed to equipment builders increasingly factoring plate selection into their structural simulations and life-cycle carbon assessments. A testament to this shift is the agreement that secures a mill-to-line supply chain for all trucks debuting in 2027.

OEM influence is reinforced by mill-owned service networks. SSAB’s 550-member Hardox Wearparts chain delivers next-day kits, helping OEMs eliminate buffer inventory and simplifying warranty tracking. While distributors will continue to play a role in addressing repair emergencies and small-lot orders, their significance is waning. This decline is evident as mills and builders increasingly share ownership of development data, software interfaces, and performance diagnostics.

By End-User Industry: Recycling Surges as E-Waste Streams Harden

In 2025, mining, supported by approvals for copper and lithium projects, emerged as the dominant consumer, accounting for 41.65% of the market. Meanwhile, the recycling industry has surged ahead, with a robust 10.97% CAGR projected for the 2026-2031 period. This growth is attributed to facilities retrofitting shredders to handle compact battery casings and high-strength automotive alloys. Operators leveraging predictive wear analytics to synchronize maintenance with urban collection routes are now bypassing mid-cycle downtimes by transitioning directly to HB 500 or HB 550.

The quarrying and cement sectors, while stable, are in a mature phase, opting for replacement cycles of medium plates for crushers and clinker conveyors rather than pursuing expansion. In the construction equipment segment, excavators and skid steers have benefited from infrastructure investments in India and the Asia-Pacific region. However, weight regulations are compelling fabricators to shift their focus from HB 400 at 20 mm to HB 500 at 12 mm. This shift, while moderating growth, has proven to be advantageous in terms of value addition for mills.

By Plate Thickness and Format: Thin Plates Gain as Laser Cutting Enables Precision Designs

In 2025, medium plates, measuring between 10 mm and 40 mm, generated 62.02% of the total revenue, highlighting their prevalent use in truck bins and loader buckets. On the other hand, thin plates, with measurements up to 10 mm, are projected to witness a robust CAGR of 10.95% during the forecast period of 2026–2031. This anticipated growth is largely due to advancements in fiber-laser systems. These innovations enable fabricators to produce intricate gussets and wear strips for agricultural combines, eliminating the need for secondary machining. Moreover, the market for thin gauges of abrasion wear-resistant steel plates is on the rise. Original Equipment Manufacturers (OEMs) are now achieving an optimal blend of durability and reduced weight by combining HB 500 hardness with a thickness of 6–8 mm - a combination that was out of reach a decade ago.

Thick plates, those exceeding 40 mm, are tailored for specialized uses such as crusher jaws and mill liners. Here, the demand for maximum impact energy requires a substantial mass. Single-rolled plates have a cap set at 120 mm. This stipulation has resulted in a supply concentration among mills equipped with heavy-plate stands and multi-zone quench lines. Additionally, price premiums persist, driven by the limited availability of roll slots and the necessity for high-energy hydraulic presses during the fabrication process.

Geography Analysis

In 2025, the Asia-Pacific region commanded a dominant 58.53% share of global revenue and is set to outpace all other regions with a CAGR of 9.49% projected through the forecast period of 2026–2031. China's GB/T 24186-2022 standard has become the cornerstone for domestic OEM tenders, significantly reducing the nation's dependence on imports. Concurrently, India's IS 18809:2024 standard is harmonizing local production with international benchmarks, allowing "Make in India" procurement teams to shorten lead times. ArcelorMittal Nippon Steel India is on track to expand its capacity by 2030, ensuring a consistent supply of flat plates to meet the demands of both domestic and export markets, particularly for excavators and tippers.

North America, though not the dominant player, is capitalizing on mining investments, especially in battery-metal initiatives in Nevada and Ontario. Highlighting a policy-driven localization effort, the Canadian government has granted Titus Steel a subsidy, aiming to fortify supply chains against shipping disruptions. In the United States, equipment manufacturers are pivoting towards low-carbon plates, a shift influenced by state procurement rules adopting Scope 3 accounting. This transition paves the way for SSAB Zero deliveries, which are slated to be housed in a new yard in Iowa.

Europe's growth trajectory may be stabilizing at mid-single digits, yet it commands premium pricing, in part due to environmental surcharges. SSAB's forthcoming projects, such as the Oxelösund EAF start-up and the Luleå mini-mill, are poised to make significant cuts to Scope 1 emissions over the next decade. This positions European tonnage as a preferred choice for automotive and construction OEMs that prioritize verified low-carbon content. Moreover, NATO member states are ramping up their demand for specialty products, especially in defense retrofits like armored-vehicle floor plates.

While South America and the Middle-East and Africa maintain modest market shares, both regions are experiencing robust mid-single-digit growth rates. This expansion is primarily fueled by copper pit enlargements in Chile and Peru, coupled with ambitious infrastructure megaprojects along the Saudi Red Sea coast. Baosteel's state-of-the-art plate mill in Ras Al-Khair, utilizing cost-effective natural gas DRI, is set to become a key supplier of plates to MENA mines and shipyards. This localized production not only simplifies procurement for Gulf mining contractors but also alleviates freight challenges tied to transporting heavy plates.

Trade tensions remain a looming threat. In a proactive stance, POSCO is making substantial investments in downstream assets across the United States and India, strategically positioning itself to counter potential hefty import tariffs in North America. These strategic moves, combined with region-specific regulations and capacity investments, underscore the intricate dynamics shaping the abrasion wear-resistant steel plates market.

Competitive Landscape

The abrasion wear-resistant steel plates market is moderately consolidated. Breaking into the market proves to be a challenge; setting up a quench-line requires hefty investments, and metallurgical know-how is often shrouded in trade secrets. Nevertheless, China's Tier-2 mills are elevating their quality, crafting private-label NM-series plates in line with GB/T 24186-2022 standards. These competitively priced plates challenge imports in ASEAN and Africa. Consequently, the competitive landscape shifts from mere tonnage to a wider array of services and emissions credentials. Mills are unable to fund Electric Arc Furnace (EAF) transitions risk shrinking margins as buyers lean towards low-carbon alternatives.

Abrasion Wear Resistant Steel Plates Industry Leaders

SSAB

ArcelorMittal

NLMK Group

AG der Dillinger Hüttenwerke

JFE Steel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SSAB opened a steel service center in Mumbai to supply parts and advanced components made from Hardox and Strenx grades, reinforcing downstream capabilities in India.

- January 2026: Bisalloy Steel Group expanded its distribution network across Central and Eastern Europe to meet rising demand for steel plate in defense and mining projects.

Global Abrasion Wear Resistant Steel Plates Market Report Scope

Abrasion Wear Resistant Steel Plates are high-carbon alloy steel plates manufactured through quenching and tempering processes. These plates are designed to offer exceptional resistance to sliding wear, high surface pressure, and abrasive materials. Defined by their Brinell Hardness (HB/HBW), they are available in standard grades such as 400, 450, and 500, as well as ultra-high grades exceeding 500, making them suitable for extending the service life of machinery in demanding applications.

The market is segmented by product type, customer type, end-user industry, plate thickness and format, and geography. By product type, the market is segmented into HB 400, HB 450, HB 500, and HB grades exceeding 500. By customer type, the market is segmented into OEMs, distributors, maintenance contractors, and other customer types. By end-user industry, the market is segmented into mining, quarrying, cement industry, construction, recycling, and other industries. By plate thickness, the market is segmented into thin plates (≤10 mm), medium plates (10-40 mm), and thick plates (more than 40 mm). The report also covers the market size and forecasts for the market in 18 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| HB 400 |

| HB 450 |

| HB 500 |

| HB grades greater than 500 |

| OEMs |

| Distributors |

| Maintenance Contractors |

| Other Customer Types |

| Mining |

| Quarrying |

| Cement Industry |

| Construction |

| Recycling Industry |

| Other End-user Industries |

| Thin Plates (≤10 mm) |

| Medium Plates (10-40 mm) |

| Thick Plates (more than 40 mm) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Product Type | HB 400 | |

| HB 450 | ||

| HB 500 | ||

| HB grades greater than 500 | ||

| By Customer Type | OEMs | |

| Distributors | ||

| Maintenance Contractors | ||

| Other Customer Types | ||

| By End-User Industry | Mining | |

| Quarrying | ||

| Cement Industry | ||

| Construction | ||

| Recycling Industry | ||

| Other End-user Industries | ||

| By Plate Thickness | Thin Plates (≤10 mm) | |

| Medium Plates (10-40 mm) | ||

| Thick Plates (more than 40 mm) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the abrasion wear-resistant steel plates sector be in 2031?

It is projected to reach USD 7.62 billion by 2031, growing at an 8.82% CAGR from USD 5.00 billion in 2026.

Which hardness grade is expanding fastest?

Plates above HB 500 are set to post the quickest 10.47% CAGR from 2026 to 2031 as mines upgrade to ultra-hard liners.

Why are recycling plants moving to higher-hardness plate?

Tougher e-waste streams and battery casings speed up wear, so operators specify HB 500–550 to cut downtime, backing a 10.97% CAGR in the 2026 to 2031 period in recycling demand.

What role will OEMs play in future plate demand?

Equipment builders integrating plate choice in early design are expected to lift direct purchases at a 9.66% CAGR in the 2026 to 2031 period, gradually overtaking distributor-driven sales.

How do new safety standards affect sourcing decisions?

IS 18809:2024 and GB/T 24186-2022 raise hardness and traceability requirements, pushing buyers toward certified domestic mills in Asia-Pacific.

Page last updated on: