Steel Fabrication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

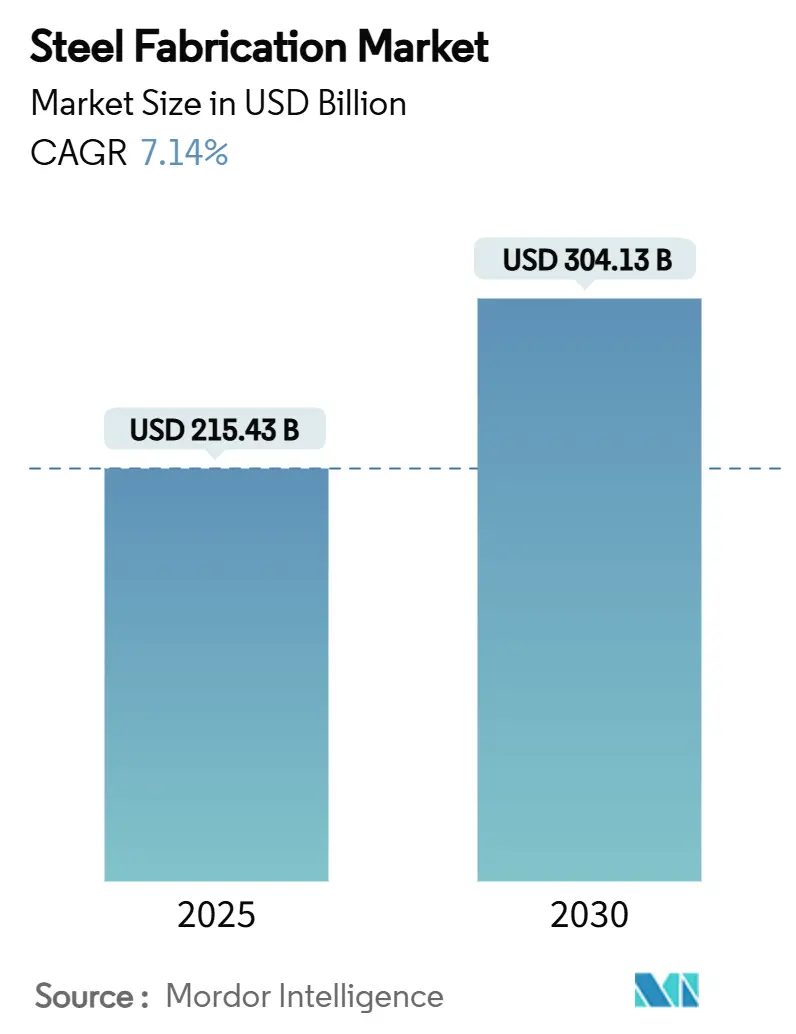

| Market Size (2025) | USD 215.43 Billion |

| Market Size (2030) | USD 304.13 Billion |

| Growth Rate (2025 - 2030) | 7.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Steel Fabrication Market Analysis by Mordor Intelligence

The Steel Fabrication Market size is estimated at USD 215.43 Billion in 2025, and is expected to reach USD 304.13 Billion by 2030, at a CAGR of 7.14% during the forecast period (2025-2030). Demand benefits from record infrastructure spending programs, renewed capital expenditure in oil-and-gas and power-generation assets, and rising investments in low-carbon production routes. Fabricators integrating automation, advanced materials processing, and sustainability credentials are securing longer-term contracts from end users seeking resilient, traceable supply chains. Price volatility for hot-rolled coil and alloying elements remains a margin headwind, yet forward-pricing agreements and hedging tools are widening adoption, particularly among mid-sized players. Regulation, notably the European Union’s Carbon Border Adjustment Mechanism (CBAM), is accelerating a shift toward certified low-CO₂ steel grades, creating competitive advantages for early movers able to demonstrate verifiable emissions reductions.

Key Report Takeaways

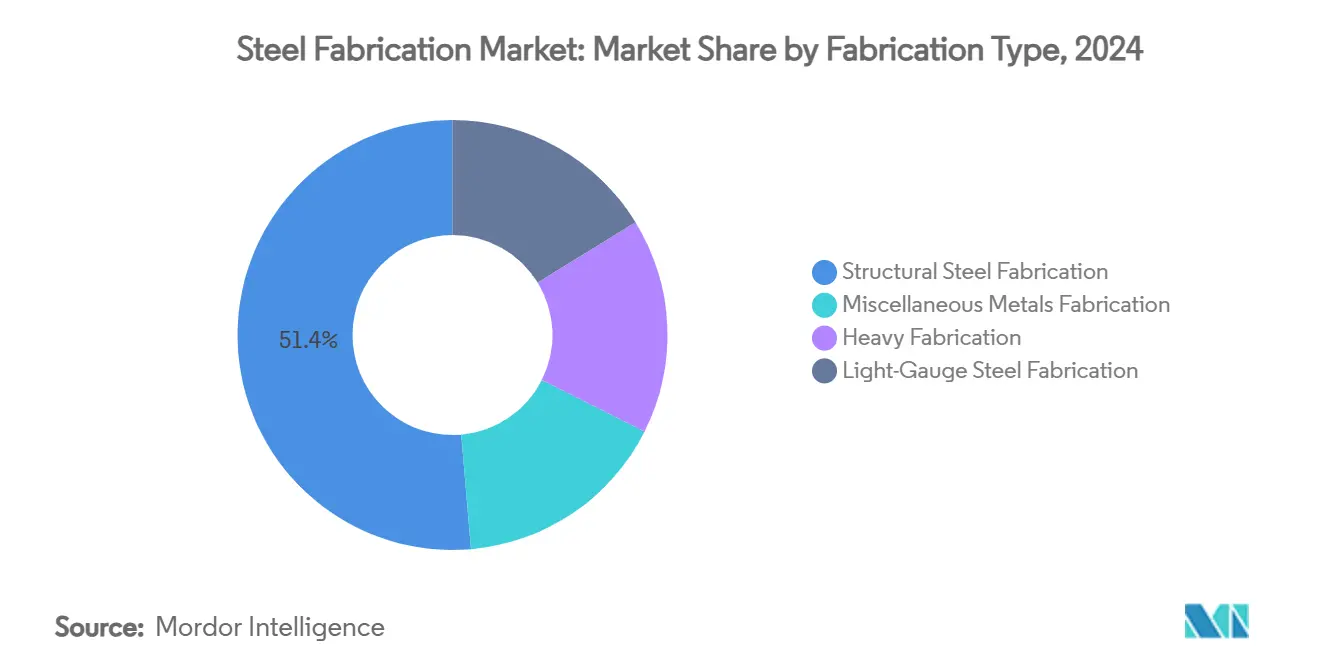

- By fabrication type, structural steel captured 51.38% of the Steel Fabrication market share in 2024, while light-gauge steel is forecast to expand at 7.56% CAGR through 2030.

- By service type, metal welding held 37.54% of the Steel Fabrication market size in 2024, whereas other services will post the highest 7.71% CAGR to 2030.

- By steel grade, carbon steel dominated with 54.67% share in 2024; alloy steel is poised for the fastest 7.65% CAGR through 2030.

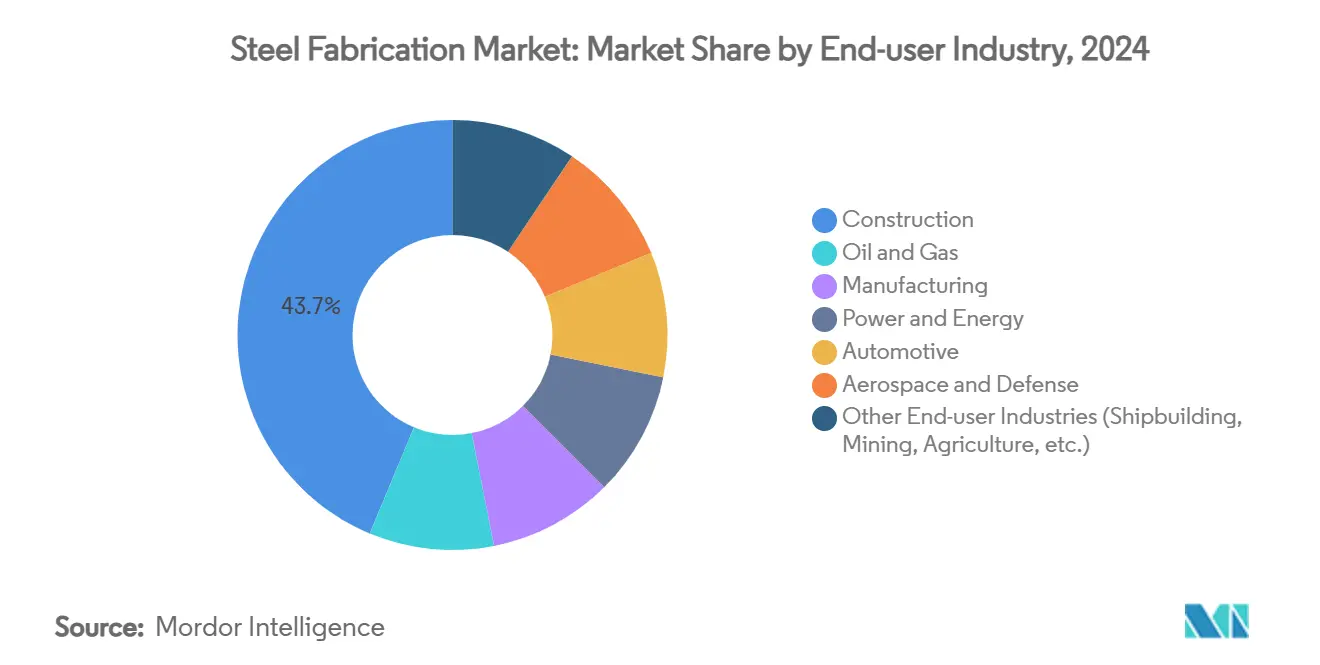

- By end user, construction accounted for 43.72% of the Steel Fabrication market size in 2024, while automotive applications will grow the quickest at 7.92% CAGR to 2030.

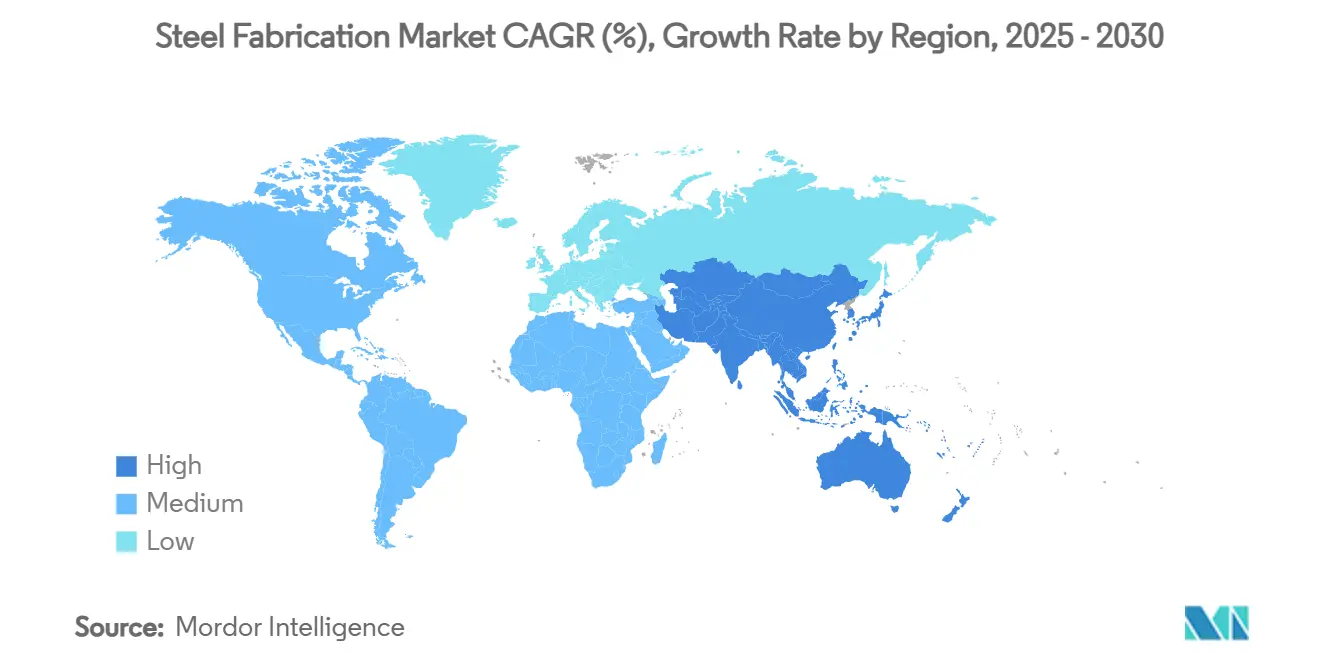

- By geography, Asia-Pacific commanded 45.51% of 2024 revenue and is projected to grow at a 7.84% CAGR, outpacing all other regions through 2030.

Global Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Global Construction and Infrastructure Spend | +1.8% | APAC, North America | Medium term (2-4 years) |

| Expansion of Oil and Gas Plus Power-generation Projects | +1.2% | Middle East, North America, APAC | Long term (≥ 4 years) |

| Rising Adoption of Pre-fabricated Steel Buildings | +1.5% | North America, EU, APAC | Medium term (2-4 years) |

| Shift toward High-strength, Low-carbon Steels for Decarbonisation | +1.1% | EU, North America, APAC | Long term (≥ 4 years) |

| Hydrogen-ready Renewable Projects Demanding Bespoke Modules | +0.8% | EU core, North America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Global Construction and Infrastructure Spend

Infrastructure stimulus packages lift demand for fabricated beams, columns, and rebar across transport, energy, and social housing programs. The United States Infrastructure Investment and Jobs Act supports a higher near-term baseline for steel pricing and encourages fabricators to lock in multi-year supply commitments with mills to secure margin visibility[1]ArcelorMittal, “2024 Integrated Annual Review,” arcelormittal.com. Urbanization in Indonesia, Vietnam, and India pushes public–private partnerships toward modular bridge decks and transit hubs that favor factory-finished structural modules. Design-build procurement models shorten bidding cycles, enabling fabricators with integrated engineering services to win turnkey packages. Digital tracking of project milestones improves payment certainty, further incentivizing automation investment.

Expansion of Oil and Gas Plus Power-generation Projects

The resumption of long-deferred LNG (liquefied natural gas) trains, refinery upgrades, and new-build gas-fired turbines is lifting orders for heavy plate, skids, and pressure vessels. Saudi-based complex revamps integrating hydrogen coproduction require metallurgy to resist sulfidation at 900°C, supporting higher-margin alloy fabrication. Renewable power, meanwhile, is steel-intensive; an offshore 12 MW wind turbine demands up to 900 tons of fabricated steel tower, nacelle frame, and transition piece, roughly 2-3 times more steel per MW than a combined-cycle unit. Fabricators that certify welders to ISO 3834 are winning frame supply contracts from turbine original equipment manufacturers (OEMs).

Rising Adoption of Pre-fabricated Steel Buildings

Modular hotels, student dormitories, and data centers built from cold-formed panels reduce site labor by about 50% and shorten schedules by nearly one-third compared with cast-in-place concrete, shifting value capture upstream to factory fabricators. U.S. developers have moved beyond warehouses to mid-rise offices, illustrated by an 8.4% CAGR for pre-engineered metal building shipments through 2030. Integrating BIM (Building Information Modeling) with CNC (Computer Numerical Control) punch-and-bend lines allows zero-scrap optimization, trimming plate usage by up to 12%. Cost predictability and speed combination drive repeat procurement from general contractors contending with skilled-labor scarcity.

Shift toward High-strength, Low-carbon Steels for Decarbonisation

Automakers have locked in offtake agreements for advanced high-strength steels that reduce body-in-white mass, offsetting battery weight in electric vehicles. ArcelorMittal supplied 11.5 Million tons of such grades to vehicle platforms in 2023, reflecting the rapid material transition underway. Fabricators upgrading press brakes and laser cutters to handle 1,700 MPa yield steels achieve tighter bend radii without cracking, enabling more compact crash structures. Green hydrogen-based direct-reduced iron feedstock lowers embedded CO₂ in the plate by up to 90%, commanding price premiums that offset ore beneficiation costs. Certification schemes such as ResponsibleSteel give early-adopter fabricators an edge in bids where scope 3 emissions are weighed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Steel Raw-material Prices | -1.4% | Global | Short term (≤ 2 years) |

| High Upfront Investment for CNC and Robotic Lines | -0.9% | Developed markets, emerging adopters | Medium term (2-4 years) |

| Carbon–border Taxes Increasing Compliance Costs | -0.6% | EU and exporters to EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Steel Raw-material Prices

Hot-rolled coil prices have swung from USD 650 to USD 900 per ton within six months on supply-chain disruptions and tariff reviews, compressing gross margins for spot-oriented fabricators unable to pass surcharges along mid-project. Contract clauses that peg finished-goods billing to Fastmarkets indexes now appear in over 60% of EPC (Engineering, Procurement, and Construction) frameworks; however, such hedging narrows discretionary pricing levers. Smaller workshops lacking working-capital facilities find it difficult to pre-buy inventory, risking production stoppages during spikes. The resultant consolidation trend favors vertically integrated processors that own scrap yards or direct-reduced iron modules.

High Upfront Investment for CNC and Robotic Lines

Robotic welding islands, fiber-laser cutters, and multi-axis machining centers can require capital outlays above USD 10 Million per plant. Payback often exceeds five years unless framework agreements with OEMs guarantee throughput. Skilled maintenance technicians able to program robot-hose seam tracking remain scarce, pushing hourly rates beyond USD 70 in the United States. Technology obsolescence risk rises as software iterations shorten; a five-year-old cutting table may lack real-time adaptive height control, reducing nesting efficiency compared with next-generation models. Financing solutions offered by equipment vendors are emerging, but stringent credit assessments still limit uptake among family-owned shops.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fabrication Type: Structural Steel’s Revenue Anchor with Light-Gauge Momentum

Structural steel accounted for 51.38% of 2024 revenue, underscoring its role in high-rise frames, bridges, and industrial platforms that underpin public works programs. Light-gauge output is projected to register a 7.56% CAGR, capturing demand from modular schools and data centers where panels arrive on site in flat-pack assemblies. The steel fabrication market size for light-gauge applications is forecast to reach USD 48 Billion by 2030, reflecting the steady penetration of cold-formed techniques.

Manufacturers capitalizing on this trend deploy roll-forming lines with inline punching and embossing, permitting batch-size-one production without die changes. Seismic testing indicates up to 79.5% lower inter-story drift for light-gauge walls than legacy masonry, accelerating code compliance in earthquake zones. Integrated supply packages that include insulated panels, stair cores, and roof trusses differentiate bidders and reduce total installed cost, positioning light-gauge specialists as enablers of ambitious housing targets in Asia-Pacific.

By Service Type: Welding Dominance Faces Automated Multiservice Emergence

Metal welding remained the largest service in 2024 with 37.54% share of the Steel Fabrication market. Automated gas-metal-arc stations combined with camera-guided seam tracking deliver up to 40% cycle-time reduction, preserving welding’s centrality even as punching, stamping, and machining collectively outpace at a 7.71% CAGR. The Steel Fabrication market share linked to integrated punching-and-tapping cells is expected to double by 2030 as OEMs seek one-stop production.

Multi-process platforms now punch louvers, countersink holes, and form offsets without material re-handling, compressing lead times from days to hours. Fabricators monetizing these capabilities through subscription-style capacity blocks create predictable cash flows that fund further automation. Meanwhile, robotic welding is overcoming fixture costs via adaptive tooling that self-adjusts for plate variance, enabling economical low-volume runs.

By Steel Grade: Carbon Steel Stability Meets Alloy Upside

Carbon steel retained a 54.67% share in 2024 due to its cost advantage and universality across construction. The alloy category will expand at 7.65% CAGR, driven by aerospace, energy, and defense specifications that mandate elevated tensile properties. The Steel Fabrication market size tied to alloy grades is forecast to add USD 19 Billion during 2025-2030, supported by investments in hydrogen pipelines and defense procurement programs.

Custom 465 stainless, for example, exceeds 250 ksi ultimate strength after aging, facilitating lighter drill-string components that travel deeper with less torque. Fabricators that secure AS9100 or NADCAP approvals capture outsized margins, as qualification cycles for competing suppliers extend past 18 months. Stainless plate cutting also gains from expanded chemical-processing capacity in South-east Asia, where corrosion resistance offsets lifecycle costs.

By End-user Industry: Construction Anchor Enables Automotive Upshift

Construction consumed 43.72% of the Steel Fabrication market size in 2024, furnishing predictable base-load that justifies capacity investments. Automotive volumes constitute a smaller slice but lead growth at 7.92% CAGR as battery-electric platforms multiply. The sector’s demand for gigafactory mezzanines, stamping-press bases, and lightweight crash boxes translates into high-precision fabrication slots booked two years ahead.

Global automakers have announced over USD 140 Billion in new EV-aligned steel demand since 2024, including Honda’s CAD 15 Billion Canadian EV hub and BMW’s doubling of Mexican body-shop capacity. Fabricators providing tolerance-verified subframes meet statistical-process-control thresholds demanded by just-in-sequence final assembly, reinforcing long-run contracts and smoothing commodity price transmission.

Geography Analysis

Asia-Pacific held 45.51% of 2024 revenue and will advance at a market-leading 7.84% CAGR toward 2030. China’s fabricated-steel component output exceeded CNY 600 Billion (USD 84 Billion) in 2024, and the country’s demand shift toward machinery and infrastructure applications signals higher value-added orders for precision fabricators. India’s National Green Steel Mission and AM/NS India’s 7 million t integrated mill reinforce domestic sourcing preferences, while Vietnam and Indonesia absorb capacity from supply-chain relocation. Government incentives for automated plants in Thailand and Malaysia further stimulate regional investment.

North America represents a mature yet technologically progressive arena. The U.S. Inflation Reduction Act encourages low-CO₂ procurement for federal projects, spawning preference premiums of up to USD 100 per ton for verified green plate. Capacity additions such as Hyundai Steel’s planned USD 5.8 Billion Louisiana slab mill and Pacific Steel’s Mojave micro-mill signal a pivot to shorter-haul domestic supply, bolstering resilience against maritime disruption[2]Louisiana Economic Development, “Hyundai Steel Chooses Louisiana for Slab Mill,” opportunitylouisiana.com. Fabricators that demonstrate Origin-of-Melt traceability secure buy-American carve-outs across bridge and substation contracts.

Europe is the frontrunner in decarbonised production, with more than 50 announced low-carbon steel projects targeting 172 Million t capacity by 2030. CBAM (Carbon Border Adjustment Mechanism) implementation elevates demand for hydrogen-based DRI (Direct Reduced Iron) plate, and fabricators with energy-efficient laser lines and digital material passports are positioned to win high-margin orders from automotive OEMs. Meanwhile, Middle East projects leverage surplus renewable electricity for green hydrogen, driving fabrication of large-diameter pipe and storage spheres. Africa’s urban population growth underpins long-term infrastructure steel needs, yet capital scarcity postpones near-term take-off.

Competitive Landscape

The Steel Fabrication market is moderately fragmented, due to the presence of a large number of players. Automation capability is the principal differentiator. Fabricators integrating vision-guided welding and IoT (Internet of Things) telemetry achieve first-time-right rates above 98%, cutting rework costs and unlocking premium pricing. Digital transformation extends to predictive maintenance software that maximises spindle and torch uptime. Sustainability credentials form the second axis of competition: plants certified to ISO 50001 and ResponsibleSteel win preferential access to green-incentive projects and often secure multi-year offtake agreements with OEMs seeking emissions transparency. Strategic alliances between design-engineering firms and fabricators are appearing to deliver turnkey modular solutions, particularly in data-center and battery-plant construction.

Steel Fabrication Industry Leaders

Schuff Steel

Zamil Steel Holding Company Limited

Tata Steel

Severfield plc

ArcelorMittal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Pacific Steel Group (PSG) commenced constructing a steel melting and rolling micro mill in California's Mojave Desert. PSG will transform scrap steel into an annual output of 380,000 tons of rebar and spooled coils.

- March 2025: ArcelorMittal Nippon Steel India Private Limited (AM/NS India), a key subsidiary of Nippon Steel Corporation, announced its land acquisition of 2,200 acres in Andhra Pradesh, southern India, to establish an integrated steel mill boasting an annual production capacity of 7 million tons of crude steel.

Global Steel Fabrication Market Report Scope

| Structural Steel Fabrication |

| Miscellaneous Metals Fabrication |

| Heavy Fabrication |

| Light-Gauge Steel Fabrication |

| Metal Welding |

| Metal Cutting |

| Metal Shearing |

| Metal Forming |

| Other Services (Punching, Stamping, Machining) |

| Carbon Steel |

| Alloy Steel |

| Stainless Steel |

| Construction |

| Oil and Gas |

| Manufacturing |

| Power and Energy |

| Automotive |

| Aerospace and Defense |

| Other End-user Industries (Shipbuilding, Mining, Agriculture, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Fabrication Type | Structural Steel Fabrication | |

| Miscellaneous Metals Fabrication | ||

| Heavy Fabrication | ||

| Light-Gauge Steel Fabrication | ||

| By Service Type | Metal Welding | |

| Metal Cutting | ||

| Metal Shearing | ||

| Metal Forming | ||

| Other Services (Punching, Stamping, Machining) | ||

| By Steel Grade | Carbon Steel | |

| Alloy Steel | ||

| Stainless Steel | ||

| By End-user Industry | Construction | |

| Oil and Gas | ||

| Manufacturing | ||

| Power and Energy | ||

| Automotive | ||

| Aerospace and Defense | ||

| Other End-user Industries (Shipbuilding, Mining, Agriculture, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Steel Fabrication market?

The market is valued at USD 215.43 Billion in 2025, with projections pointing to USD 304.13 Billion by 2030.

How fast is demand for prefabricated steel buildings growing?

Light-gauge fabrication tied to modular construction is expected to expand at a 7.56% CAGR through 2030, outpacing traditional heavy fabrication.

Which geographic region holds the largest share in fabricated-steel revenues?

Asia-Pacific leads with 45.51% of 2024 revenue and will maintain the fastest regional growth at 7.84% CAGR.

Why are automotive applications important to fabricators?

Electric-vehicle platforms require high-strength, lightweight steel components, driving a 7.92% CAGR for automotive fabrication demand through 2030.

How does the EU’s CBAM affect exporters?

CBAM imposes embedded-carbon reporting and eventual levies on imported fabricated steel, favoring low-CO₂ producers with verifiable emissions data.

Page last updated on: