Weathering Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

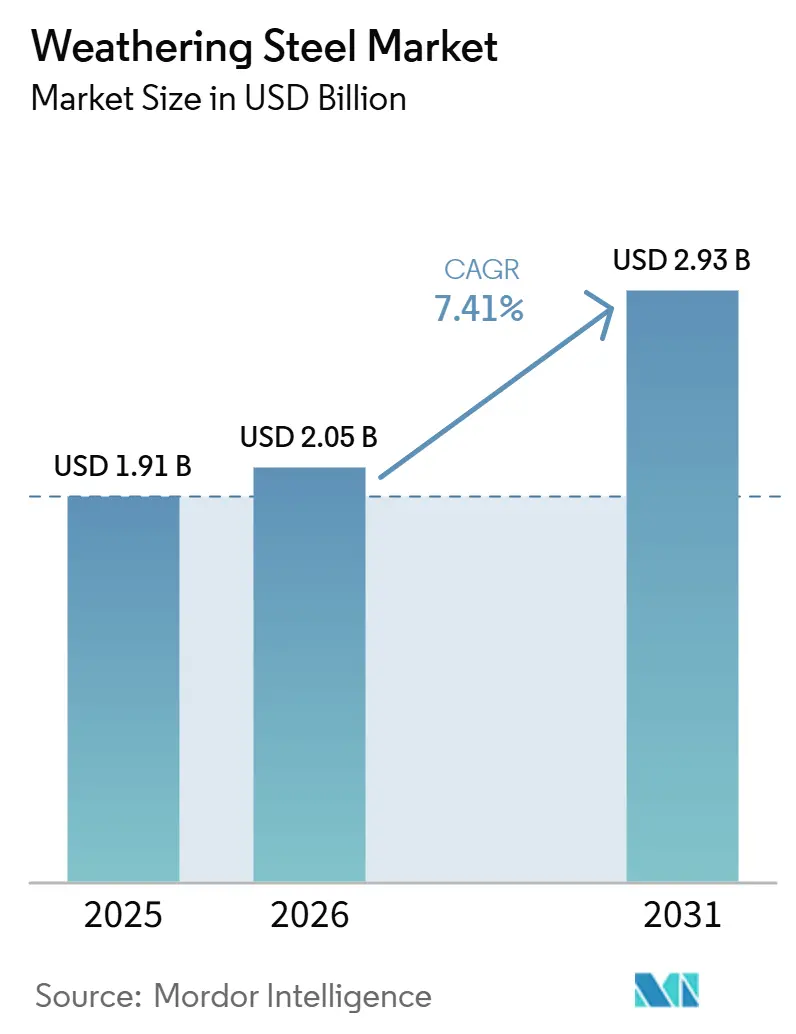

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 2.93 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

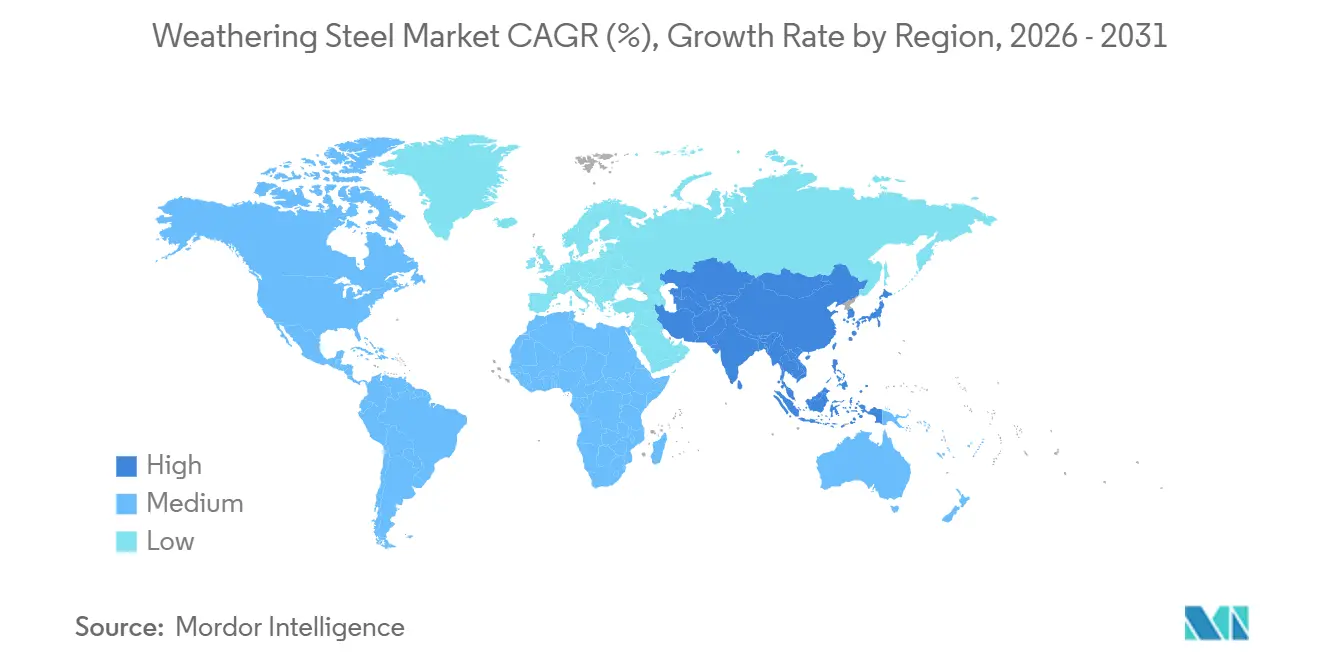

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

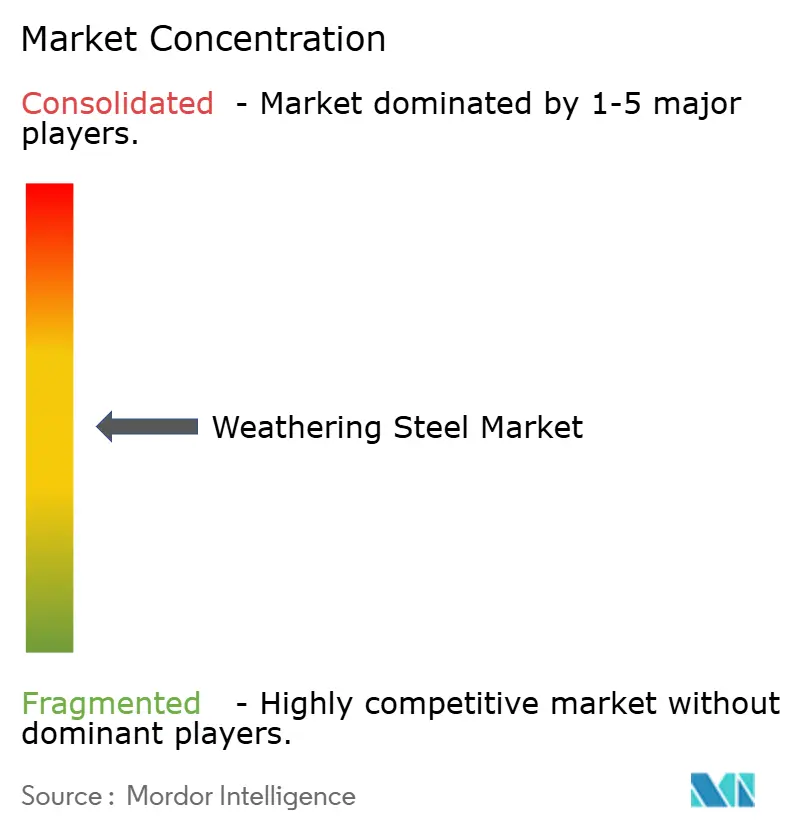

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Weathering Steel Market Analysis by Mordor Intelligence

The Weathering Steel Market size was valued at USD 1.91 billion in 2025 and is estimated to grow from USD 2.05 billion in 2026 to reach USD 2.93 billion by 2031, at a CAGR of 7.41% during the forecast period (2026-2031). As governments impose stricter lifecycle-cost and carbon-reporting mandates, there is a notable shift from painted carbon steel to corrosion-resistant alloys. This trend is particularly evident in applications like bridges, renewable-energy foundations, and modular data-center enclosures. Integrated mills are now introducing electric arc furnace (EAF) weathering grades, boasting over 75% scrap content and powered entirely by renewable energy. This innovation enables asset owners to achieve both corrosion resistance and a reduced carbon footprint. Demand in the Asia-Pacific region is buoyed by mega-bridge projects in China and capacity expansions in India. Simultaneously, North America's surge in grid reinforcement is driving demand for plates, pipes, and piles in transmission corridors. While a select few blast furnace giants dominate the supply of heavy plates, regional EAF mini-mills are carving out a niche. By situating themselves close to fabricators and ensuring shorter lead times, they are securing a steady stream of long-product orders.

Key Report Takeaways

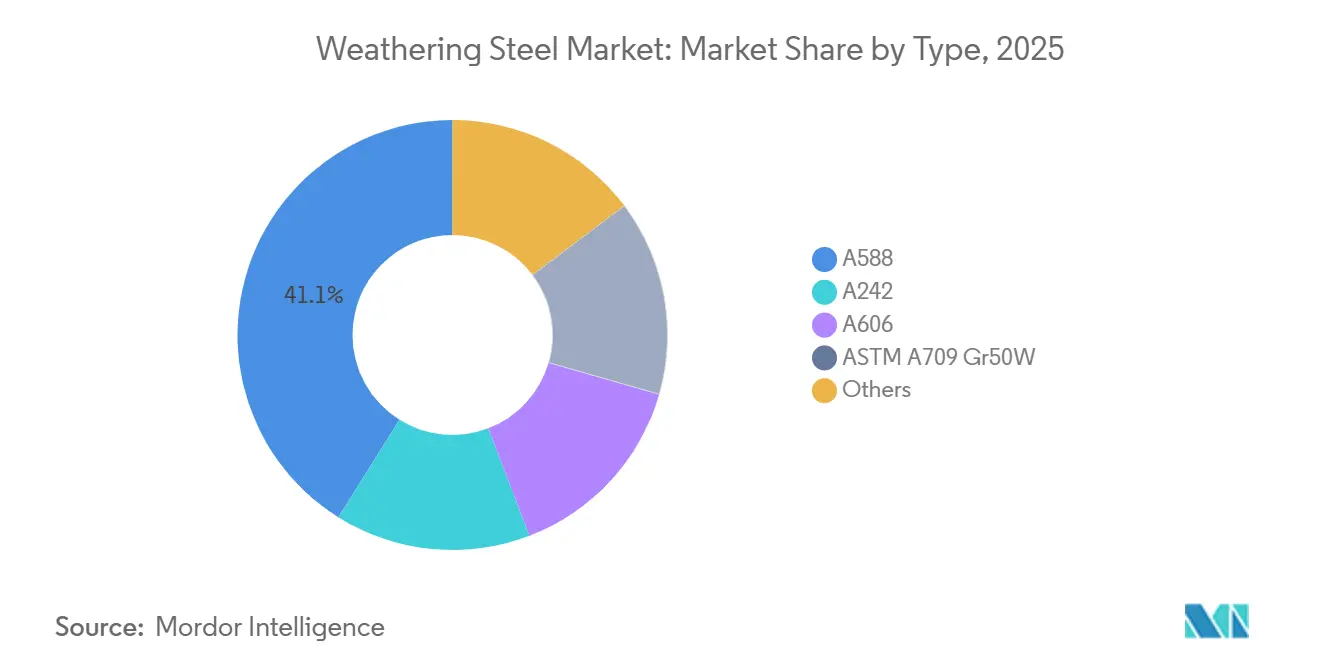

- By type, A588 led with 41.11% of the weathering steel market share in 2025, while ASTM A709 Gr50W posted the highest 7.88% CAGR from 2026 to 2031.

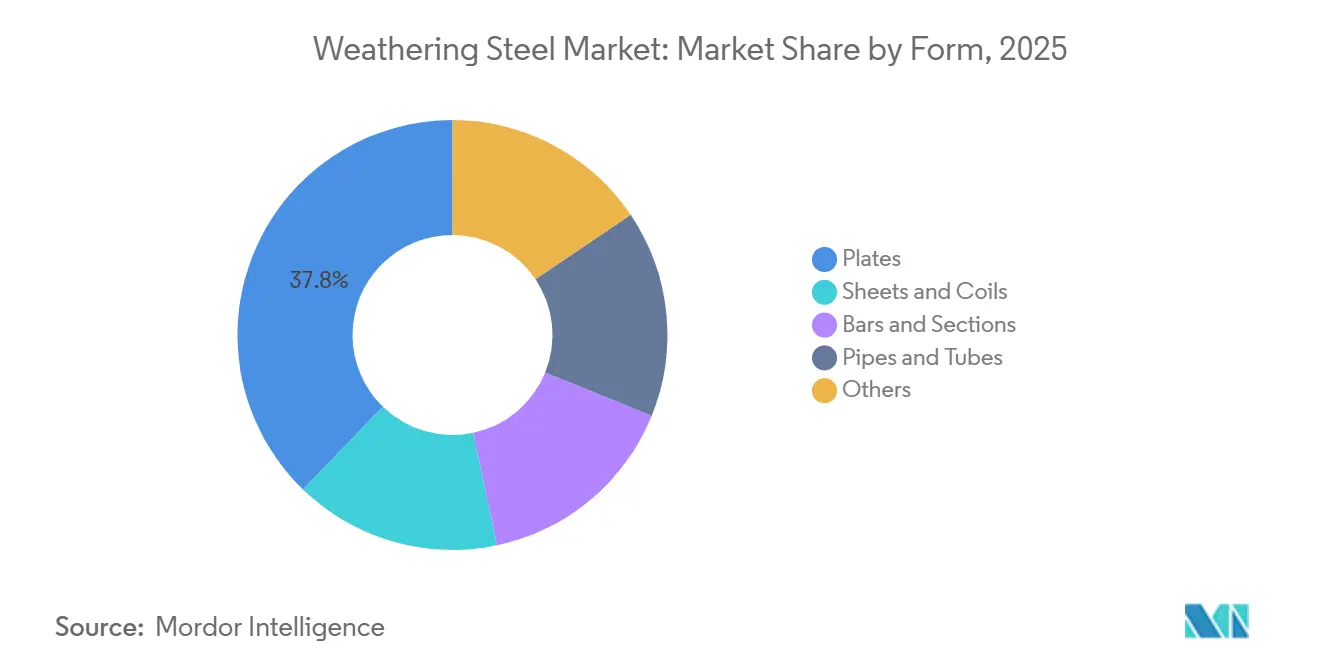

- By form, plates commanded 37.76% share of the weathering steel market size in 2025; pipes and tubes are projected to expand at 7.78% CAGR from 2026 to 2031.

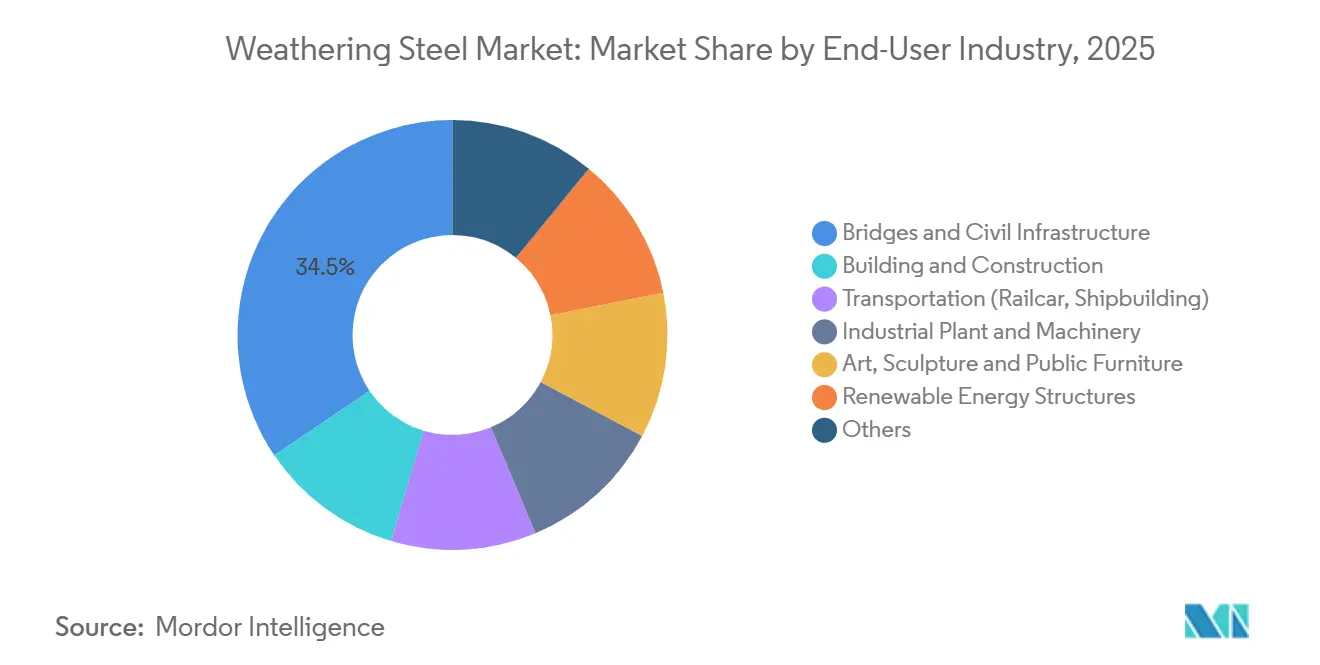

- By end-user, bridges and civil infrastructure accounted for 34.45% of the weathering steel market size in 2025, and renewable-energy structures are advancing at an 8.23% CAGR from 2026 to 2031.

- By geography, Asia-Pacific held 46.13% of the weathering steel market share in 2024 and is pacing an 8.02% regional CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Weathering Steel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization push favoring low-maintenance steels | +1.8% | Global, with early adoption in EU & North America | Medium term (2-4 years) |

| Aesthetic weather-tone appeal in urban architecture | +1.2% | North America, Europe, APAC urban cores | Short term (≤ 2 years) |

| Lifecycle-cost edge over galvanized and coated steels | +2.1% | Global | Long term (≥ 4 years) |

| Growing use in containerized data-center skids | +0.9% | North America, APAC (China, India, Singapore) | Short term (≤ 2 years) |

| Adoption in high-altitude solar tracker columns | +1.4% | APAC, North America, Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Decarbonization Push Favoring Low-Maintenance Steels

Steelmakers are now embedding lifecycle-carbon accounting into their product offerings. This shift is particularly advantageous for weathering grades, as the removal of paint systems not only eliminates volatile organic compounds but also reduces emissions from recurring maintenance. ArcelorMittal’s XCarb heavy plates, crafted in electric arc furnaces (EAFs) using over 75% scrap and powered entirely by renewable electricity, have achieved a 36% reduction in carbon intensity for Vestas’ Nordlicht 1 offshore wind project when compared to traditional blast-furnace steel. Starting January 2026, the EU's Carbon Border Adjustment Mechanism will impose tariffs on imports with high carbon footprints. This move is nudging buyers towards certified low-carbon weathering grades. In a strategic move, Tata Steel is channeling USD 3.2 billion into its Kalinganagar expansion, introducing dedicated lines for high-strength weathering plates. This positions Tata to cater to both the domestic infrastructure boom and the export markets that align with CBAM standards. Currently, Europe and North America lead in demand, but as global carbon pricing tightens, a peak is anticipated in the medium term.

Aesthetic Weather-Tone Appeal in Urban Architecture

In 2025, design portal Dezeen spotlighted 10 signature projects, showcasing architects' growing admiration for the evolving rust-brown patina, valued for its unique texture and depth. Municipalities in Singapore and Toronto have updated their guidelines, detailing drainage solutions to prevent staining on nearby façades. This move has expedited approvals for the use of exposed weathering steel. Meanwhile, JFE Steel introduced its FLExB weld bead on the Miyuki Bridge in March 2026. This innovation promises smoother surfaces, significantly reducing runoff marks and addressing a primary concern in pedestrian areas. As flagship buildings emerge, setting material precedents, this architectural trend is expected to influence dense urban centers in the short term.

Lifecycle-Cost Edge Over Galvanized and Coated Steels

According to an SSAB lifecycle study, weathering steel can reduce the total ownership cost of a bridge by 25% over an 80-year period compared to painted carbon steel[1]SSAB, “Lifecycle Cost of Weathering Steel Bridges,” ssab.com. This cost-saving primarily stems from sidestepping repainting expenses, which range from USD 150-300/m² and typically occur every 15-20 years. Utilities are witnessing similar financial benefits. For instance, Bull Moose Tube highlights a 10-15% lower initial cost and a 30% savings over the lifecycle for ASTM A847 transmission poles, in contrast to their hot-dip-galvanized counterparts. In 2025, six U.S. state DOTs broadened the application of weathering specifications, extending them from interstate bridges to secondary structures. This move underscores a heightened discipline in managing maintenance budgets. As asset owners continue to gather field data and inflation drives up coating prices, the economic benefits of using weathering steel become even more pronounced over time.

Growing Use in Containerized Data-Center Skids

In 2025, hyperscale cloud operators rolled out a substantial 23 GW of IT capacity. Meanwhile, modular container skids, crafted from weathering-grade frames, not only speed up site activation but also withstand corrosion in outdoor lay-down yards. In a strategic move, Chinese fabricator Wuxi Huanawell has begun shipping Corten containers. These containers eliminate the need for temporary climate-controlled storage, leading to significant logistics cost reductions for edge data centers. Demand is notably concentrated in Virginia, Texas, and India, regions currently witnessing AI training clusters and 5G rollouts. As these hyperscale projects near completion, the demand is set to surge in the short term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patina breakdown in marine/high-chloride climates | -1.3% | Coastal regions globally, offshore wind zones | Medium term (2-4 years) |

| Emerging "green-steel" grades with superior ESG | -0.8% | Europe, North America, APAC urban cores | Long term (≥ 4 years) |

| Designer push-back over perceived color drift | -0.5% | North America, Europe, APAC high-visibility urban projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Patina Breakdown in Marine/High-Chloride Climates

In 2025, a study by Buildings journal highlighted premature section loss on bridges along the Gulf Coast. This finding led the DOTs of Louisiana, Oregon, and Washington to impose a ban on weathering steel within a 10-mile radius of saltwater[2]Alexandra Díaz, “Corrosion of Weathering Steel in Coastal Bridges,” Buildings, mdpi.com . Similarly, while offshore wind foundations are turning to hot-dip galvanizing or epoxy coatings, the five U.S. Atlantic projects, collectively valued at over USD 28 billion and under construction in 2025, have steered clear of conventional weathering grades. Nippon Steel's CORSPACE hybrid plate, which was trialed on a bridge in Vanuatu in 2024, boasts extended repainting intervals. However, it finds itself in direct competition with traditional weathering plates for inland projects. Due to salt-spray limitations, growth in market share near coastal areas is expected to be restrained in the medium term.

Emerging Green-Steel Grades with Superior ESG

ArcelorMittal's XCarb, JFE's JGreeX, and Boston Metal's zero-carbon MOE route are now competing on a new front: achieving mechanical parity with weathering steel while boasting significantly lower embedded emissions. Microsoft's 2026 stake in Stegra underscores a pivotal shift, indicating that major buyers will increasingly demand a 95% reduction in emissions, coupled with ASTM certifications. Furthermore, shipyards have shown their commitment to sustainability by opting for the JGreeX plate for bulk carriers in June 2025, even agreeing to pay a premium for ESG compliance. On another front, mills that haven't adopted Electric Arc Furnace (EAF) or Direct Reduced Iron (DRI) methods are bracing for shrinking margins, especially as green public procurement scoring gains traction in major tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Higher-Strength Grades Gain in Seismic and Long-Span Bridges

In 2025, A588 captured 41.11% of the market share, highlighting its long-standing leadership in highway girders and transmission towers. Meanwhile, ASTM A709 Gr50W is on the rise, with a 7.88% CAGR, due to its preferred toughness and weldability among bridge engineers in seismic zones. Additionally, Ansteel’s Q500qE plate, recognized for its 50% weight reduction, was pivotal in the 800 m Yichang Dongyan Yangtze span project, awarded in January 2026. As agencies increasingly prioritize performance-based specifications that emphasize seismic resilience, the market for A709-based bridge applications is expected to grow steadily.

While demand for the legacy A242 is declining due to inventory rationalization, new proprietary high-strength products like SSAB's Strenx Weathering 700 and 960, introduced in March 2025, are creating niches in mining and offshore equipment. Furthermore, the recently published ASTM A588-24 standard in October 2024, which tightens chemistry and impact-test protocols, is facilitating cross-market certifications. As a result, the weathering steel market is anticipated to see an increase in the share of premium plates, driven by these higher-grade substitutions.

By Form: Pipes and Tubes Surge on Transmission and Solar Demand

In 2025, plates accounted for 37.76% of revenue, driven by orders for bridges, wind towers, and industrial equipment. Meanwhile, pipes and tubes are witnessing a 7.78% acceleration. This surge follows utilities' shift from wood and galvanized poles to ASTM A847 weathering tubes. This transition has unlocked a remarkable 30% lifecycle savings, as evidenced by a 222-pole retrofit in Finland, which, after a decade, showcased zero corrosion defects. The weathering steel market, particularly in tubular products, is set for further growth, especially with the adoption of this material in solar-tracker columns.

Sheets, coils, and light sections find their niche in architectural cladding, where the aesthetics of patina are paramount. Specialty rolled rings, used for turbine gearboxes and mooring chains, are categorized under the “others” segment. Bull Moose Tube's capacity expansion in 2025 hints at a sustained demand for distribution poles and utility piles over the coming years. This diversification in form not only underscores market fragmentation but also amplifies the need for specialized suppliers.

By End-User Industry: Renewables Outpace Traditional Infrastructure

In 2025, bridges and civil infrastructure accounted for a significant 34.45% of demand, as evidenced by Shandong Steel's delivery of 15,000 tonnes to the hybrid tower of the Beijing-Taiwan Expressway, commissioned in December 2025. Meanwhile, structures for renewable energy emerged as the fastest-growing segment, boasting an impressive 8.23% CAGR. This surge was largely driven by the addition of 27 GW in utility-scale solar and 6 GW in wind energy in the U.S. in 2025. Consequently, the weathering steel market, closely tied to renewables, is poised to surpass highway spending additions post-2027.

From Wyoming to London, architectural projects are driving an uptick in cladding demand. Simultaneously, frames for modular data centers and skeletons for mining equipment are broadening the industrial appeal. Notably, a rising trend in edge-computing skids, especially those with green-steel certifications, is steering demand more towards technology than traditional transport.

Geography Analysis

Asia-Pacific, commanding 46.13% of 2025's revenue, is projected to grow at a rate of 8.02% through 2031. The region's dynamism is supported by China's ambitious bridge program, India's 8 metric tons per annum Kalinganagar expansion, and Japan's FLExB weld innovation. Additionally, ASEAN's highway corridors and South Korea's offshore wind yards contribute to the incremental tonnage.

Since June 2025, North America has reaped the benefits of 50% Section 232 tariffs, providing a shield for domestic mills. Gerdau, in response, boosted its 2025 shapes shipments by 8.5% to reach 2.59 metric tons and is on track to introduce an additional 150 kilotons of EAF capacity in Texas by late 2026. Meanwhile, U.S. grid operators invested a total of USD 115 billion into transmission in 2025, spurring a heightened demand for weathering piles and poles.

Europe is pivoting towards a low-carbon plate. For example, ArcelorMittal's XCarb deliveries to Vestas achieved a 36% reduction in tower emissions. Concurrently, ThyssenKrupp's USD 870 million revamp in Duisburg and Salzgitter's takeover of 6 metric tons HKM in June 2026 are reshaping the continent's capacity landscape. Furthermore, the enforcement of CBAM from 2026 is set to bolster domestic premiums for certified EAF weathering grades.

In South America, Gerdau has slashed its 2026 capex by 20% due to a surge in imports, as authorities struggled to curb subsidized inflows. Nevertheless, Brazil, Argentina, and Chile continue to prioritize weathering plates for their viaducts and solar farms. Meanwhile, the Middle East & Africa's demand is concentrated around Gulf bridges, desalination plants, and South African mining, with regional fabricators like Cleveland Bridge Steel stepping up to meet these needs.

Competitive Landscape

The Weathering Steel market exhibits partial consolidation. Integrated majors, including ArcelorMittal, Nippon Steel, POSCO, JFE Steel, and SSAB, account for the majority of the heavy-plate output. Meanwhile, regional EAF players like Gerdau, U.S. Steel, and Tata Steel have carved out dominance in long-product niches. ArcelorMittal's USD 36 million investment in Boston Metal's molten-oxide electrolysis, coupled with its XCarb plate supply to Nordlicht 1, underscores its commitment to decarbonization and defending its premium market share. SSAB's Strenx Weathering 960, tailored for mining and offshore clients requiring yields over 700 MPa, commands a 15-20% price premium.

Disruptors like Stegra and Boston Metal are on the verge of delivering near-zero-carbon slabs, potentially overshadowing traditional patina-based differentiation. Advances in fabrication, such as digital twin patina modeling and automated weld toe grinding, are elevating entry barriers. Commodity plate mills that shy away from EAF/DRI strategies face margin pressures due to CBAM and green procurement scoring. As a result, the market is splitting: one side favors premium certified grades for renewables and data centers, while the other leans towards price-driven A588 plates for inland bridges.

Weathering Steel Industry Leaders

NIPPON STEEL CORPORATION.

SSAB AB

ArcelorMittal

JFE Steel Corporation

POSCO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ansteel won the 800 m Yichang Dongyan Yangtze bridge contract with Q500qE plate, enabling 50% plate-thickness reduction.

- July 2025: ThyssenKrupp invested USD 870 million in Duisburg hot-strip mill revamp.

Global Weathering Steel Market Report Scope

Weathering steel is a group of steel alloys developed to form a stable, rust-like, protective patina when exposed to the elements. This specialized oxide layer eliminates the need for painting and acts as a barrier against further corrosion, offering significantly improved weather resistance over standard carbon steels.

The market is segmented by type, form, and end-user industry. By type, the market is segmented into A588, A242, A606, ASTM A709 Gr50W, and other types. By form, the market is segmented into plates, sheets and coils, bars and sections, pipes and tubes, and other forms. By end-user industry, the market is segmented into building and construction, bridges and civil infrastructure, transportation (including railcar and shipbuilding), industrial plant and machinery, art, sculpture and public furniture, renewable energy structures, and other end-user industries. The market for Weathering Steel also covers 19 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| A588 |

| A242 |

| A606 |

| ASTM A709 Gr50W |

| Others |

| Plates |

| Sheets and Coils |

| Bars and Sections |

| Pipes and Tubes |

| Others |

| Building and Construction |

| Bridges and Civil Infrastructure |

| Transportation (Railcar, Shipbuilding) |

| Industrial Plant and Machinery |

| Art, Sculpture and Public Furniture |

| Renewable Energy Structures |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | A588 | |

| A242 | ||

| A606 | ||

| ASTM A709 Gr50W | ||

| Others | ||

| By Form | Plates | |

| Sheets and Coils | ||

| Bars and Sections | ||

| Pipes and Tubes | ||

| Others | ||

| By End-user Industry | Building and Construction | |

| Bridges and Civil Infrastructure | ||

| Transportation (Railcar, Shipbuilding) | ||

| Industrial Plant and Machinery | ||

| Art, Sculpture and Public Furniture | ||

| Renewable Energy Structures | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will global demand for weathering steel grow through 2031?

Aggregate revenue is projected to rise from USD 2.05 billion in 2026 to USD 2.93 billion by 2031, reflecting a 7.41% CAGR tied to bridge upgrades, renewable-energy foundations, and data-center frames.

Which region contributes the most incremental volume?

Asia-Pacific adds the largest tonnage as China pursues mega-bridge programs and India expands EAF capacity dedicated to high-strength weathering plates.

Why are utilities replacing galvanized poles with weathering-grade tubes?

Eliminating galvanizing cuts 10-15% upfront cost and 30% lifecycle expense, while field inspections after 10 years report no corrosion failures in harsh freeze-thaw environments.

What limits weathering steel near coastlines?

Continuous salt spray prevents the protective patina from stabilizing, accelerating corrosion and steering engineers toward galvanized or epoxy-coated alternatives for marine or offshore structures.

How are mills addressing carbon-footprint requirements?

Producers such as ArcelorMittal and SSAB run EAFs with >75% scrap and renewable electricity, publish ISO 14067 product footprints, and supply XCarb or Strenx Weathering grades that embed both corrosion resistance and low embodied carbon.

Page last updated on: