Heat-treated Steel Plates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.91 Billion |

| Market Size (2031) | USD 9.71 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

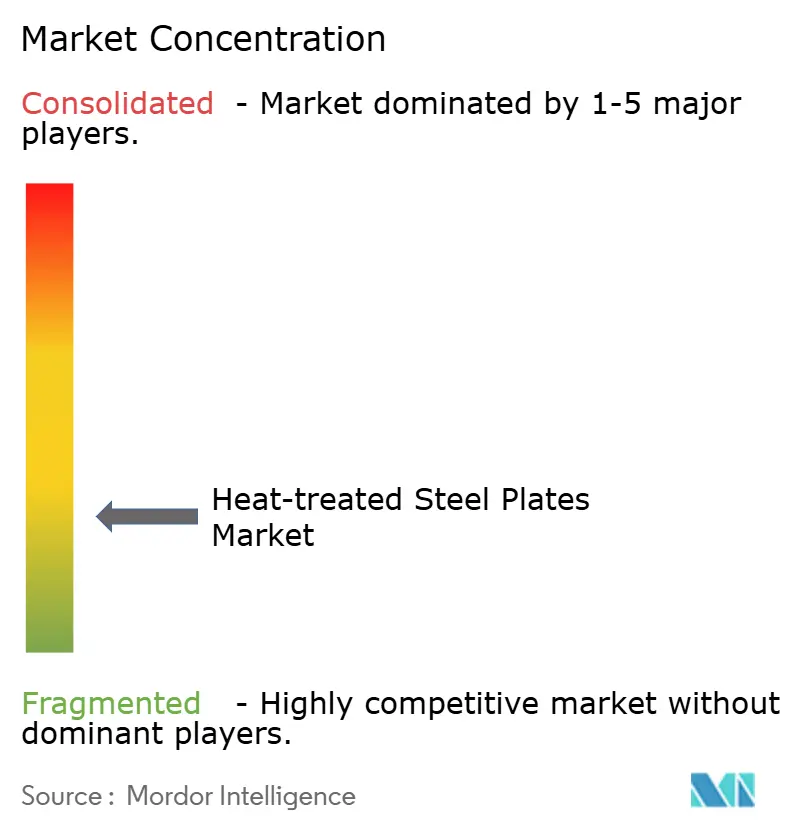

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heat-treated Steel Plates Market Analysis by Mordor Intelligence

The Heat-treated Steel Plates Market size is expected to grow from USD 7.59 billion in 2025 to USD 7.91 billion in 2026 and is forecast to reach USD 9.71 billion by 2031 at 4.18% CAGR over 2026-2031. Robust spending on offshore wind monopile foundations, autonomous mining fleets, and pressure vessels for green-hydrogen electrolyzers is lifting demand for ultra-high-strength, TMCP, and normalized plates, respectively. Fabricators value these routes because they lower post-weld heat-treatment cost, satisfy seismic codes, and extend wear life, even as composite liners and furnace-emission caps curb growth in traditional abrasion-resistant plate. Competitive intensity is moderate: the top five mills control about 38% of global capacity, yet regional specialists thrive in heavy offshore and abrasion-resistant niches. Rapid shifts in energy prices, carbon levies, and ship decarbonization rules continue to reshape procurement strategies across the heat-treated steel plates market.

Key Report Takeaways

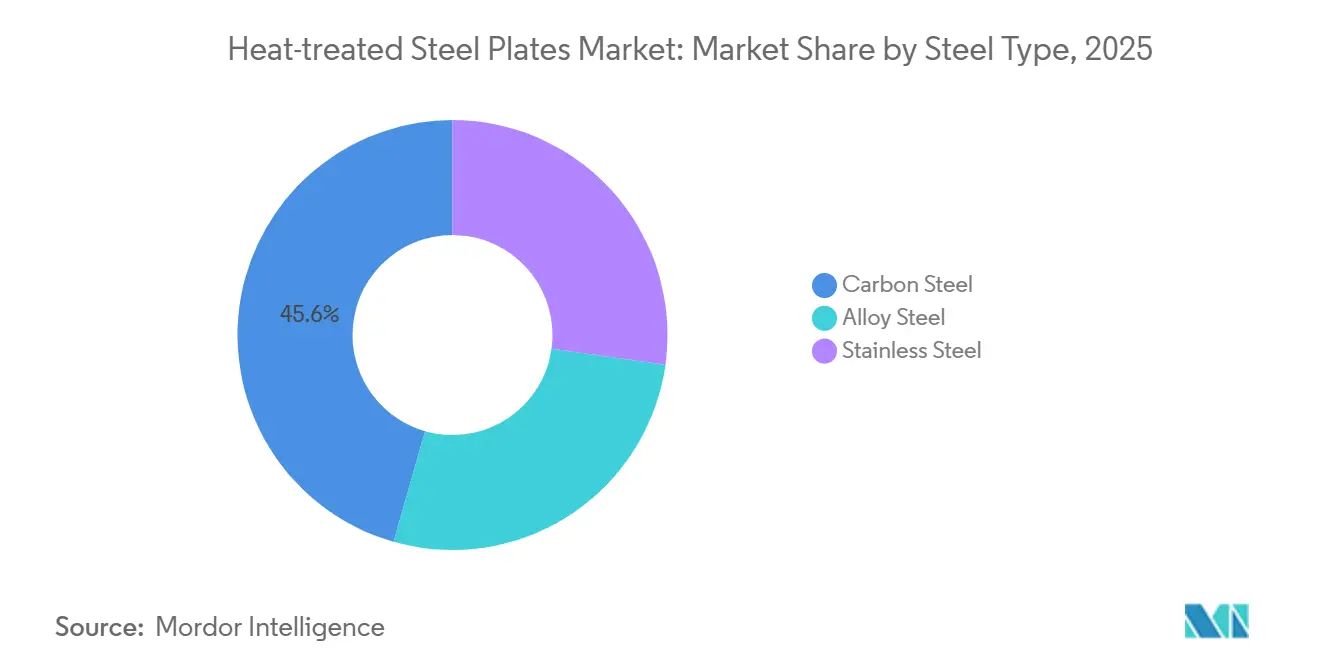

- By steel type, carbon steel led with a 45.58% share in 2025, whereas alloy steel is poised to grow at a 5.05% CAGR through 2031.

- By heat-treatment type, quenching held 40.75% of output in 2025, but TMCP is advancing at 5.42% through 2031.

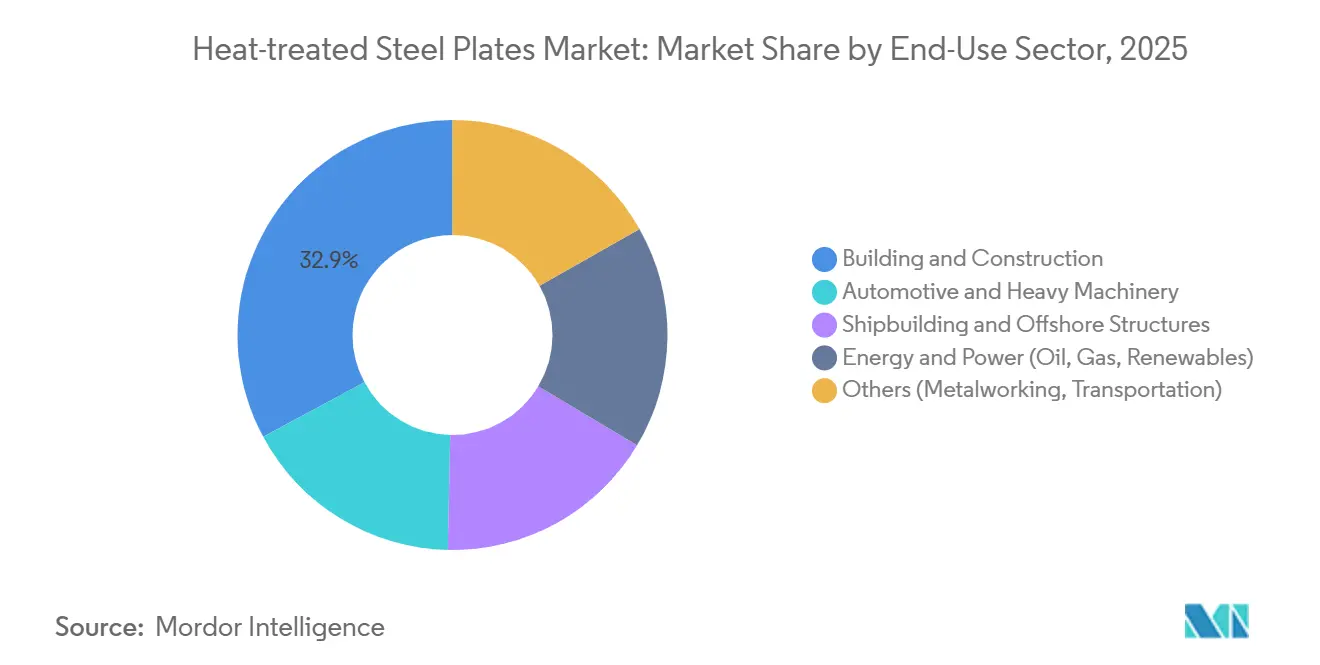

- By end-use sector, building and construction absorbed 32.86% of the 2025 volume, while energy and power are projected to expand at a 5.65% CAGR to 2031.

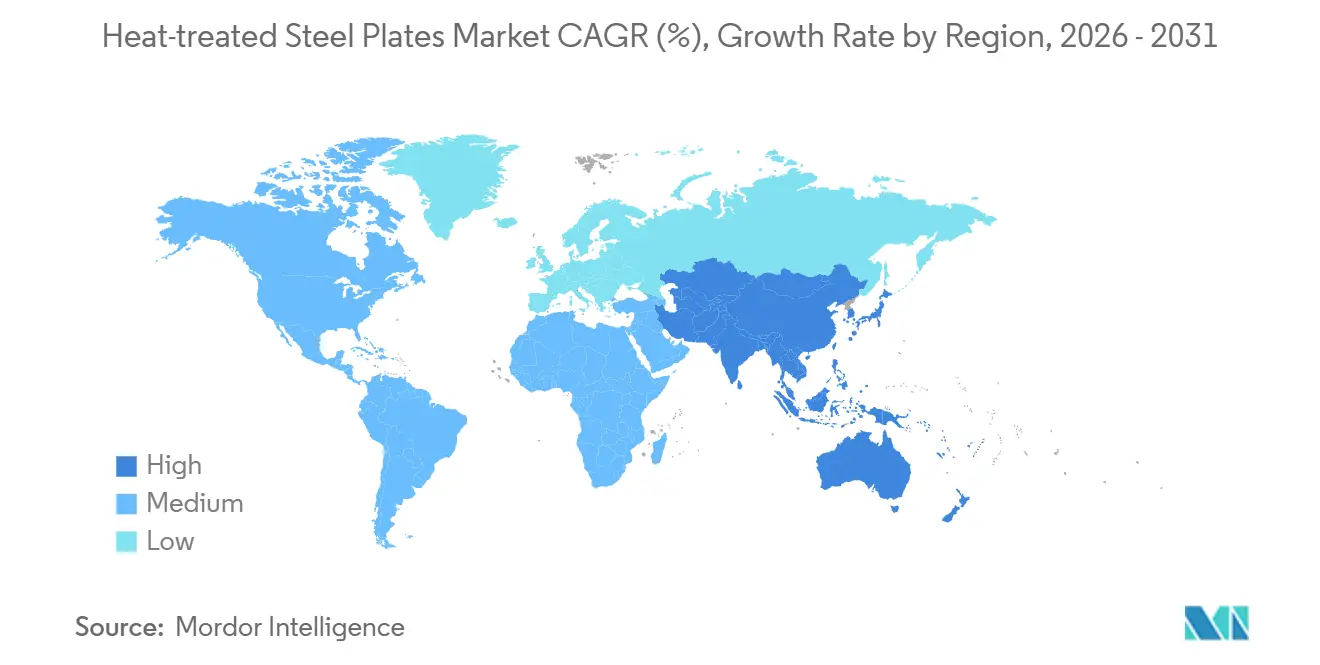

- By geography, Asia-Pacific commanded 52.95% of 2025 revenue and is expected to sustain a 5.74% growth trajectory through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heat-treated Steel Plates Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Offshore-wind monopile foundations driving demand | +1.2% | Europe, Asia-Pacific (Taiwan, Japan, South Korea), North America (US East Coast) | Medium term (2-4 years) |

| Abrasion-resistant plates adopted in autonomous mining truck bodies | +0.9% | Global, with concentration in APAC (Australia, Indonesia) and Americas (Chile, Canada) | Short term (≤ 2 years) |

| Seismic-resilient normalized plate mandated by new building codes | +0.8% | North America (California, Pacific Northwest), Asia-Pacific (Japan, Taiwan, Philippines) | Long term (≥ 4 years) |

| Duplex stainless plates for green-hydrogen electrolyzer pressure vessels in Europe | +1.0% | Europe (Germany, Spain, Netherlands), early adoption in Middle East and APAC | Medium term (2-4 years) |

| Lightweight cargo-ship designs utilizing heat-treated steel plate | +0.7% | Global, led by Asia-Pacific shipbuilding hubs (China, South Korea, Japan) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Offshore-Wind Monopile Foundations Driving Demand

Monopile diameters have climbed to 11 m and wall thicknesses to 150 mm for 15-MW turbines, pushing demand for normalized or TMCP plate that meets DNV fracture-toughness rules[1]DNV, “Offshore Standard D-101,” dnv.com. Taiwan’s China Steel Corporation secured a 5-year order for 180,000 tons of S355G10+N plate in 2025, specifying 100 J Charpy toughness at −20 °C to mitigate typhoon-induced brittle fracture. Dillinger and Ørsted agreed in 2024 to co-develop 12-m monopiles using quenched-and-tempered S690QL, reducing steel weight per MW by 18% and cutting installation costs. The Global Wind Energy Council foresees 110 GW of new offshore capacity by 2030, equal to about 8 million tons of plate if monopiles keep a 65% share[2]Global Wind Energy Council, “Global Offshore Wind Report 2025,” gwec.net. Each GW of offshore wind consumes an estimated 70,000 tons of heavy plate, underlining the sector’s pull on heat-treatment capacity.

Abrasion-Resistant Plates Adopted in Autonomous Mining Truck Bodies

Autonomous haul trucks run 24 h per day, intensifying liner wear and raising demand for 500-Brinell quenched plate that stretches replacement cycles from 8,000 h to 14,000 h. SSAB’s Hardox 500 Tuf, launched in 2025, delivers 45-J Charpy toughness, avoiding crack propagation when 220-t payloads strike the bed. JFE’s EVERHARD 450 debuted in 2024 with phosphorus micro-alloying that cuts quenching distortion and lets users laser-cut without preheating. Austin Engineering reported a 32% jump in autonomous-fleet orders in 2025, with abrasion-resistant plate making up 68% of material spend. Rio Tinto’s Pilbara fleet of 220 Komatsu 930E trucks switched to Hardox liners and reduced maintenance downtime by 22%.

Seismic-Resilient Normalized Plate Mandated by New Building Codes

The American Institute of Steel Construction’s 341-22 standard, effective 2024, requires normalized or TMCP plate in special moment frames for high seismic categories, removing as-rolled variants. California adopted the rule unchanged, compelling fabricators to source ASTM A572 Grade 50 with documented normalizing temperatures between 900 °C and 950 °C. The U.S. General Services Administration now demands Charpy tests at 0 °C for plates thicker than 38 mm in federal buildings. Japan’s Building Standard Law revisions in 2025 mandate a normalized plate for towers above 60 m within 30 km of active faults, affecting Tokyo redevelopment. Nucor responded by adding 300,000 tons of normalizing capacity at Hertford County in 2025.

Duplex Stainless Plates for Green-Hydrogen Electrolyzer Pressure Vessels

Proton-exchange-membrane and alkaline electrolyzers operate near 80 bar and chloride-rich loops, favoring duplex grades like EN 1.4462 that resist stress-corrosion cracking. H2 Green Steel’s Boden plant will consume roughly 12,000 tons of duplex plate annually when Phase 1 starts in 2026 to support EU taxonomy-aligned green bonds. Spain’s Cepsa intends to deploy 2 GW of electrolyzers by 2030, implying 18,000 tons of duplex plate demand. GrInHy2.0 trials in 2024 confirmed that solution-annealed duplex attains a balanced 50-50 microstructure and doubles pitting resistance over 316L. Salzgitter’s SALCOS project integrated a 720-MW electrolyzer in 2025, creating a captive need for 8,000 tons of duplex plate each year.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Composites replacing wear plate in next-generation earth-moving equipment | -0.8% | Global, concentrated in mining regions (Australia, Canada, Chile, South Africa) | Medium term (2-4 years) |

| Energy-price volatility reducing furnace utilization | -0.9% | Europe, energy-intensive markets in North America and Asia | Short term (≤ 2 years) |

| Stricter NOx/CO₂ furnace-emission caps raising compliance cost | -0.6% | Europe, North America, developed Asia-Pacific markets (Japan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Composites Replacing Wear Plate in Next-Generation Earth-Moving Equipment

Ultra-high-molecular-weight polyethylene liners bonded to basalt fiber captured 18% of haul-truck bed retrofits in 2025, lowering weight by 40% and eliminating weld spatter that seeds fatigue cracks. Caterpillar’s 794 AC truck, launched in 2024, offers composite beds rated to 400-Brinell equivalent abrasion resistance and extends life to 16,000 h. Komatsu introduced a carbon-fiber reinforced bucket edge in 2025 that trims tip weight by 35% and cuts fuel burn by 2.1%. Volvo Construction Equipment disclosed that composite wear parts climbed to 12% of its articulated-hauler material spend in 2025, up from 4% in 2023. Bruce Rock Engineering demonstrated a USD 31,000 three-year savings per truck when switching to UHMWPE liners, accelerating adoption in cost-focused mines.

Energy-Price Volatility Reducing Furnace Utilization

thyssenkrupp plans to idle its Duisburg normalizing furnace for six weeks and defer 40,000 tons of orders. Peak Spanish power prices above EUR 0.22/kWh in summer 2025 forced electric-arc operators to curtail output, slicing regional plate supply by 11% year on year. ArcelorMittal Fos-sur-Mer cut throughput by 14% in 2025, prioritizing high-margin wind plate and outsourcing commodity grades to India and Mexico. U.S. industrial gas prices in winter 2024-2025 averaged USD 7.80/MMBtu, hiking normalizing costs by USD 18/ton. JSW’s Dolvi mill faced a 23% power-tariff rise in 2025 and pivoted to higher-value quenched plate to protect margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Steel Type: Alloy Grades Gain as Hydrogen and Offshore Applications Multiply

The carbon steel accounted for 45.58% of the heat-treated steel plates market share in 2025, while alloy steel is forecast to expand at a 5.05% CAGR to 2031 as duplex stainless and martensitic grades penetrate electrolyzer vessels and subsea lines. Duplex stainless, notably EN 1.4462, covered about 8% of alloy tonnage in 2025, propelled by EU green-hydrogen projects. Stainless plate stays niche but essential in cryogenic and pharmaceutical uses, commanding price premiums that offset lower volume.

Cost differentials explain carbon steel’s resilience—S355 normalized sells near USD 650/ton, versus duplex plate at roughly USD 2,400/ton. Even so, alloy formulations gain ground through innovations such as ArcelorMittal’s Usibor 2000 press-hardening steel, which enables 2,000-MPa tensile strength for EV battery enclosures, and POSCO’s PosMAC, which offers tenfold marine corrosion resistance relative to galvanized alternatives. Nippon Steel’s NSGP1 normalized alloy meets -60 °C Charpy toughness for Arctic offshore rigs, further widening the addressable field for high-specification alloy plates.

By Heat-Treatment Type: TMCP Gains as Fabricators Prioritize Weldability and Energy Savings

Quenching controlled 40.75% of production in 2025, reflecting its dominance in abrasion-resistant grades, yet Thermo-Mechanical Controlled Process (TMCP) is expected to capture additional share at a 5.42% CAGR through 2031. TMCP eliminates separate normalizing, lowers residual stress, and improves weldability, helping shipyards and tower fabricators manage cycle time and cost. Normalizing held close to 22% in 2025, bolstered by seismic codes that demand predictable ductility.

The heat-treated steel plates market size for TMCP plates is projected to approach USD 3.6 billion by 2031 if current growth holds. JFE’s Super-OLAC and Dillinger’s new accelerated-cooling line underscore how mills now integrate controlled rolling and quenching to slash energy by up to 18% and hit offshore-grade toughness in a single pass. Voestalpine’s direct-quench line reduces cycle time from 72 h to 18 h, and China Baowu’s Zhanjiang expansion leverages inline quenching to address automotive press-hardening demand.

By End-Use Sector: Energy and Power Accelerates as Renewables and LNG Infrastructure Expand

Building and construction absorbed 32.86% of the 2025 market size, aided by seismic-code updates and public works in India and Southeast Asia. However, energy and power is forecast to be the fastest-growing customer, advancing at a 5.65% CAGR through 2031 as offshore wind, hydrogen, and LNG terminals proliferate. Automotive and heavy machinery are witnessing rising demand owing to autonomous fleets and EV lightweighting, while shipbuilding rebounded on container-ship and floating wind orders.

The International Energy Agency’s net-zero pathway calls for 850 GW of electrolyzers by 2050, equating to roughly 15 million tons of duplex and pressure-vessel plate. The heat-treated steel plates market size dedicated to offshore wind alone could exceed USD 2 billion by 2031, given that each gigawatt consumes around 70,000 tons of plate. The “others” bucket—rail, dies, defense—contributed 12% of demand in 2025 and should edge up as reshoring spurs tooling investment.

Geography Analysis

Asia-Pacific held 52.95% of global revenue in 2025 and is forecast to grow at 5.74% through 2031, driven by Chinese wind-turbine supply chains, India’s infrastructure pipeline, and Southeast Asian shipbuilding. China produced around 580 million tons of crude steel in 2025, with heat-treated variants accounting for close to 1.8%, indicating ample headroom for value-added migration. India’s National Infrastructure Pipeline, worth INR 111 trillion (USD 1.3 trillion), is triggering 2.2 million tons of fresh plate capacity from JSW and Tata.

Europe trails in share but leads on margin-rich duplex output. H2 Green Steel’s Boden mill, coming online in 2026, will supply 500,000 tons of fossil-free plate annually, aiming at users willing to pay EUR 50-80/ton green premiums. Germany’s thyssenkrupp is co-developing hydrogen DRI, and UK offshore wind projects such as Dogger Bank are set to consume 1.2 million tons of normalized and TMCP plate from 2026 to 2031.

North America combines seismic mandates and LNG growth. Nucor’s new normalizing line adds 300,000 tons of capacity for East Coast builders and Gulf Coast energy plants. The Middle East pivots on Saudi Arabia’s NEOM, desalination, and petrochemical projects, anticipating a 6.2% annual steel-consumption rise to 2031. South America, led by Brazil and Argentina, benefits from lithium mining and farm-equipment production, with POSCO building a lithium-hydroxide plant requiring duplex pressure vessels.

Competitive Landscape

The heat-treated steel plates market is highly fragmented. China Baowu, ArcelorMittal, Nippon Steel, POSCO, and JFE together hold considerable market share, while regional specialists such as Dillinger and SSAB dominate niches like heavy offshore monopile and abrasion-resistant plate. Decarbonization is the investment priority: Voestalpine will spend EUR 1.5 billion converting Linz to electric-arc furnaces by 2027, cutting CO₂ intensity by 30% and aligning greentec steel with automotive and wind buyers. SSAB’s HYBRIT venture is scaling to 1.3 million tons of green plate by 2030 on hydrogen DRI. Process innovation underpins differentiation. JFE’s Super-OLAC integrates accelerated cooling and microalloying to hit offshore toughness without separate normalizing, saving 18% energy. Nippon Steel filed 12 patents in 2024-2025 on inline quench control, reflecting a shift toward adaptive heat-treatment that tailors grain size per coil. ISO 3834 and DNV approvals become minimum entry tickets, shrinking the supplier pool and raising switching costs. Smaller mills leverage partnerships: Dillinger’s 2024 MOU with Ørsted secures long-term take-or-pay slots for 12-m monopile plates. SSAB formed a Hardox Wearparts network that offers lifecycle guarantees, tying miners to proprietary AR grades. New entrants face high capex for clean energy compliance and sophisticated cooling lines, reinforcing current hierarchies even as absolute supply grows.

Heat-treated Steel Plates Industry Leaders

ArcelorMittal

Baosteel Co.,Ltd.

Nippon Steel Corporation

POSCO

SSAB AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Jiangnan Shipyard completed the world’s first 400 m ore carrier using normalized EH36 produced by controlled rolling, achieving a 9% steel-weight saving and cutting lifetime CO₂ by 14,000 tons.

- November 2025: JSW Steel commissioned a 5-million-ton plate mill at Dolvi, integrating inline normalizing and accelerated cooling to serve infrastructure and energy customers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the heat-treated steel plates market as carbon, alloy, and stainless plates of at least three millimeters that have been quenched, tempered, normalized, annealed, or thermo-mechanically processed to boost strength, toughness, and weldability for use in construction, energy, shipbuilding, heavy machinery, and mobility applications.

Scope exclusion: coils, unprocessed slabs, long steel products, and clad composite plates are outside the study.

Segmentation Overview

- By Steel Type

- Carbon Steel

- Alloy Steel

- Stainless Steel

- By Heat-Treatment Type

- Annealing

- Tempering

- Normalizing

- Thermo-Mechanical Controlled Process (TMCP)

- Quenching

- By End-Use Sector

- Automotive and Heavy Machinery

- Building and Construction

- Shipbuilding and Offshore Structures

- Energy and Power (Oil, Gas, Renewables)

- Others (Metalworking, Transportation)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Russia

- Turkey

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- South Africa

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview mill technologists, shipyard buyers, construction engineers, and plate distributors across Asia-Pacific, North America, and Europe. These discussions confirm typical thickness mixes, live transaction prices, and emerging drivers, filling information gaps and letting us tighten assumptions.

Desk Research

We start by using public datasets from the World Steel Association, national statistics offices, and United Nations Comtrade to size crude plate output, trade flows, and end-use demand pools, which are then cross-checked with association briefings on offshore wind foundations and seismic-resistant building codes. Next, we mine company filings, mill capacity disclosures on D&B Hoovers, Questel patent trends, and regulatory documents to refine process splits and regional intensity of use. The sources cited are illustrative; many other publications supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A blended top-down approach begins with regional production, import-export reconciliations, and penetration-rate demand pools, while selective bottom-up checks, sampled average selling price multiplied by shipment volumes, test the totals. Key variables include offshore wind monopile installations, seismic-resistant building starts, heavy truck output, global ship completions, and construction steel intensity. We model revenue through 2030 using multivariate regression and scenario analysis, bridging any bottom-up gaps through focused triangulation.

Data Validation & Update Cycle

Mordor analysts run variance filters that flag swings beyond five percentage points; anomalies trigger re-contact with data providers before senior review sign-off. Reports refresh yearly, with interim updates after material events, and an analyst completes a fresh pass just before delivery.

Why Mordor's Heat-treated Steel Plates Baseline Inspires Reliability

Published numbers often diverge because providers choose different scopes, pricing inputs, and refresh speeds; we lay these factors bare so buyers know why totals differ.

Key gap drivers include whether plates under three millimeters are counted, how analysts translate mill-gate prices to market revenue, and whether TMCP volumes are separated. Mordor counts only commercial-grade plates >=3 mm, relies on live transactional pricing confirmed by interviews, and updates the model annually, while others may merge broader flat steel categories or lean on historical averages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.60 B (2025) | Mordor Intelligence | - |

| USD 6.86 B (2024) | Global Consultancy A | Narrower geography and stricter thickness cut-off |

| USD 6.91 B (2024) | Trade Journal B | Excludes TMCP plates; uses fixed ASP uplift |

| USD 121.77 B (2022) | Industry Association C | Combines untreated hot-rolled plate with heat-treated products |

The comparison shows that scope stretch or price shortcuts swing values widely. Mordor's disciplined variable tracking and yearly refresh give decision-makers a dependable midpoint anchored to transparent, repeatable steps.

Key Questions Answered in the Report

What is the projected value of the heat-treated steel plates market in 2031?

The market is forecast to reach USD 9.71 billion by 2031, reflecting a 4.18% CAGR from 2026.

Which steel type is expected to grow fastest through 2031?

Alloy steel, buoyed by duplex and martensitic grades for hydrogen and offshore uses, is projected to grow at a 5.05% CAGR.

Why is TMCP gaining share over quenching?

TMCP lowers post-weld heat-treatment cost, reduces distortion, and cuts energy use, prompting shipyards and wind-tower makers to favor it.

Which region leads demand for heat-treated steel plates?

Asia-Pacific held a 52.95% share in 2025 and is forecast to maintain leadership, expanding at 5.74% through 2031.

How will carbon regulations influence suppliers?

EU ETS Phase IV and other carbon caps push mills toward hydrogen DRI and electric-arc furnaces, raising capex but opening premium green-steel markets.

Page last updated on: