Wear Resistant Steel Plate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 3.40 Million tons |

| Market Volume (2031) | 4.06 Million tons |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wear Resistant Steel Plate Market Analysis by Mordor Intelligence

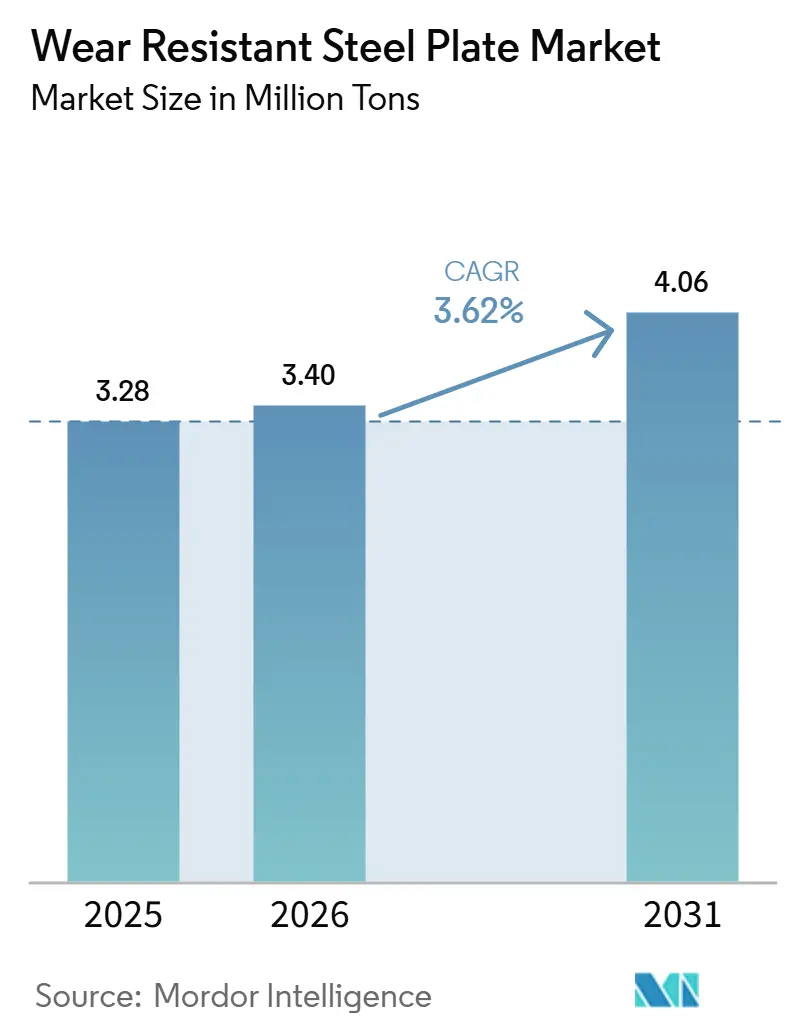

The Wear Resistant Steel Plate Market size is projected to be 3.28 Million tons in 2025, 3.40 Million tons in 2026, and reach 4.06 Million tons by 2031, growing at a CAGR of 3.62% from 2026 to 2031. As hydrogen-based direct-reduced-iron routes gain traction, mills are compelled to eliminate tramp elements, elevating qualification thresholds even as overall tonnage sees consistent growth. In the U.S., a significant USD 110 billion investment in roads and bridges, part of public-sector megaprojects, is shifting demand from thinner, low-hardness sheets to robust, thicker plates. These plates are better suited to endure abrasive soil and demolition debris. Meanwhile, ultra-class haul trucks are now demanding Brinell hardness specifications exceeding 400 HBW, steering mining consumption, and pushing alloy design into increasingly narrow chemistry windows. Concurrently, Europe's Carbon Border Adjustment Mechanism (CBAM) is reshaping competition, emphasizing decarbonization credentials over pricing.

Key Report Takeaways

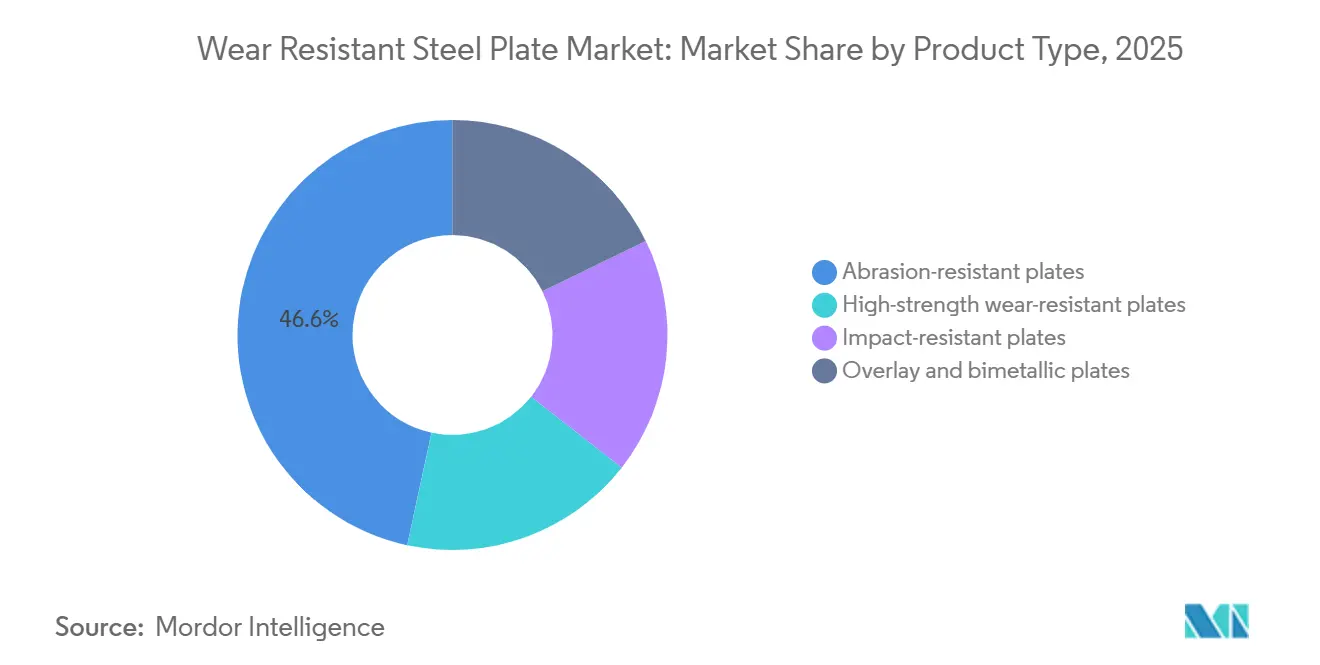

- By product type, the abrasion-resistant plate led with 46.61% of the wear-resistant steel plate market share in 2025. Impact-resistant plate is projected to expand at a 4.12% CAGR from 2026 to 2031, the fastest among all product categories.

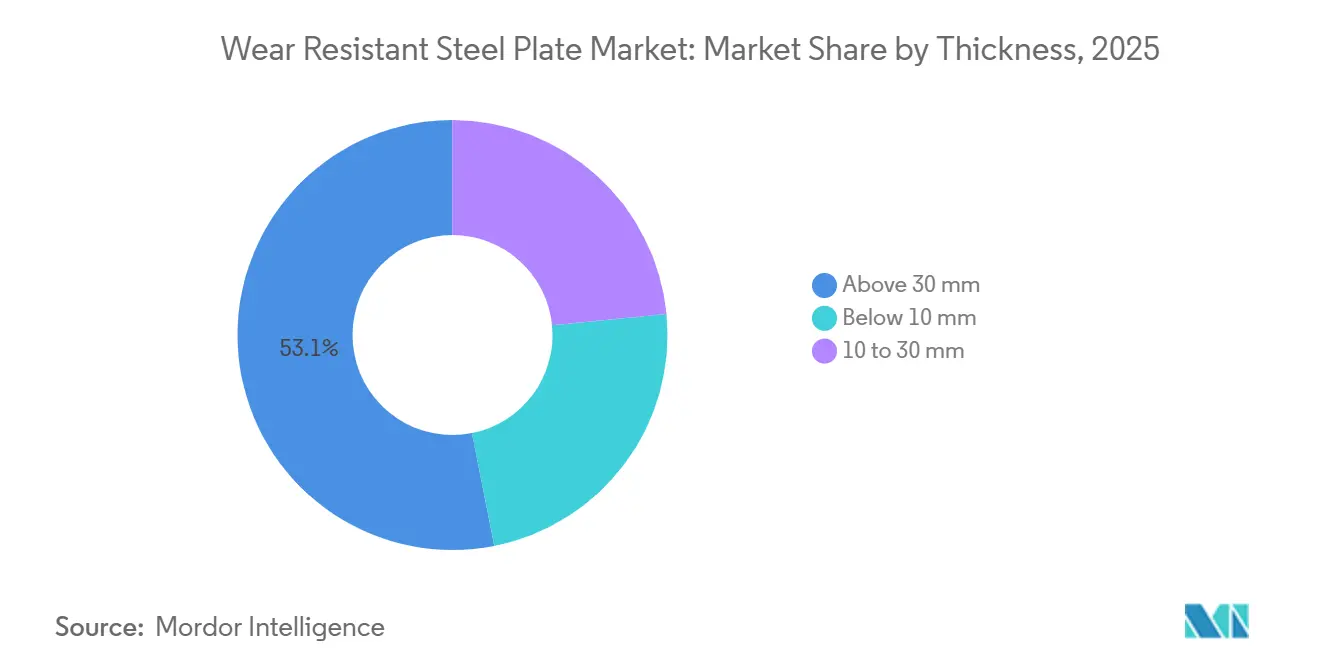

- By thickness, plates above 30 mm captured 53.11% of the 2025 volume and are advancing at a 3.96% CAGR from 2026 to 2031.

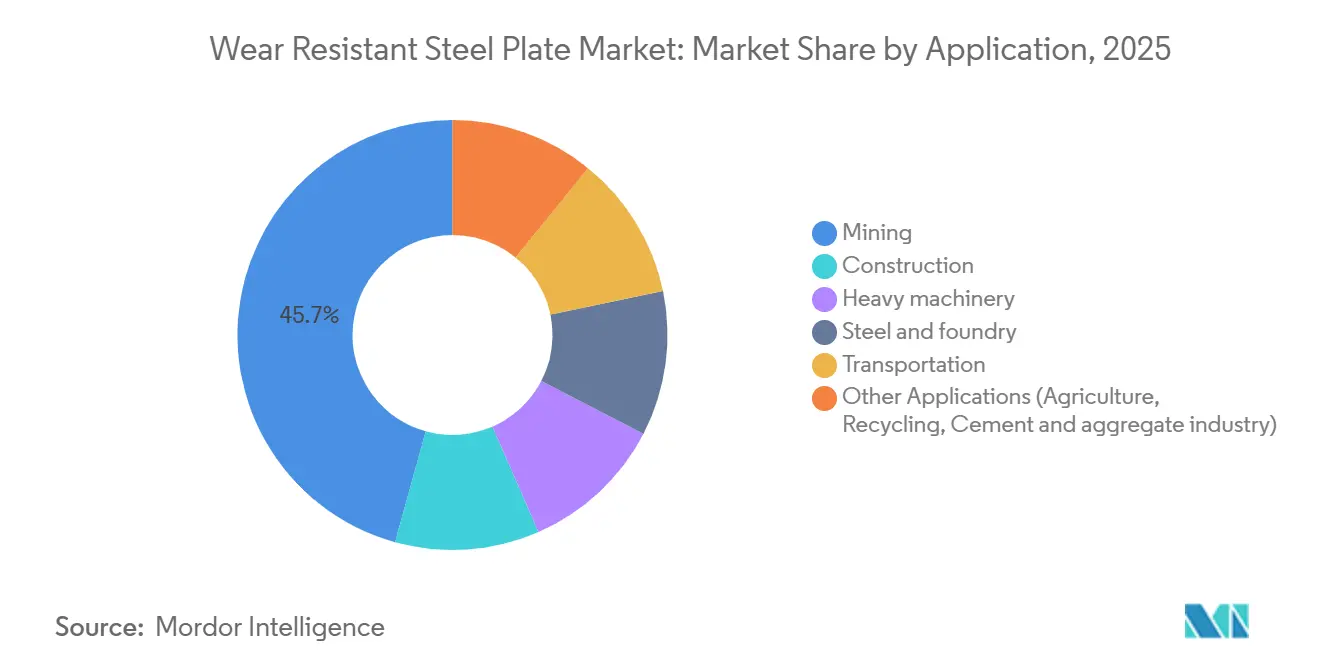

- By application, mining retained a 45.67% share in 2025, while construction is forecast to accelerate at a 4.72% CAGR from 2026 to 2031.

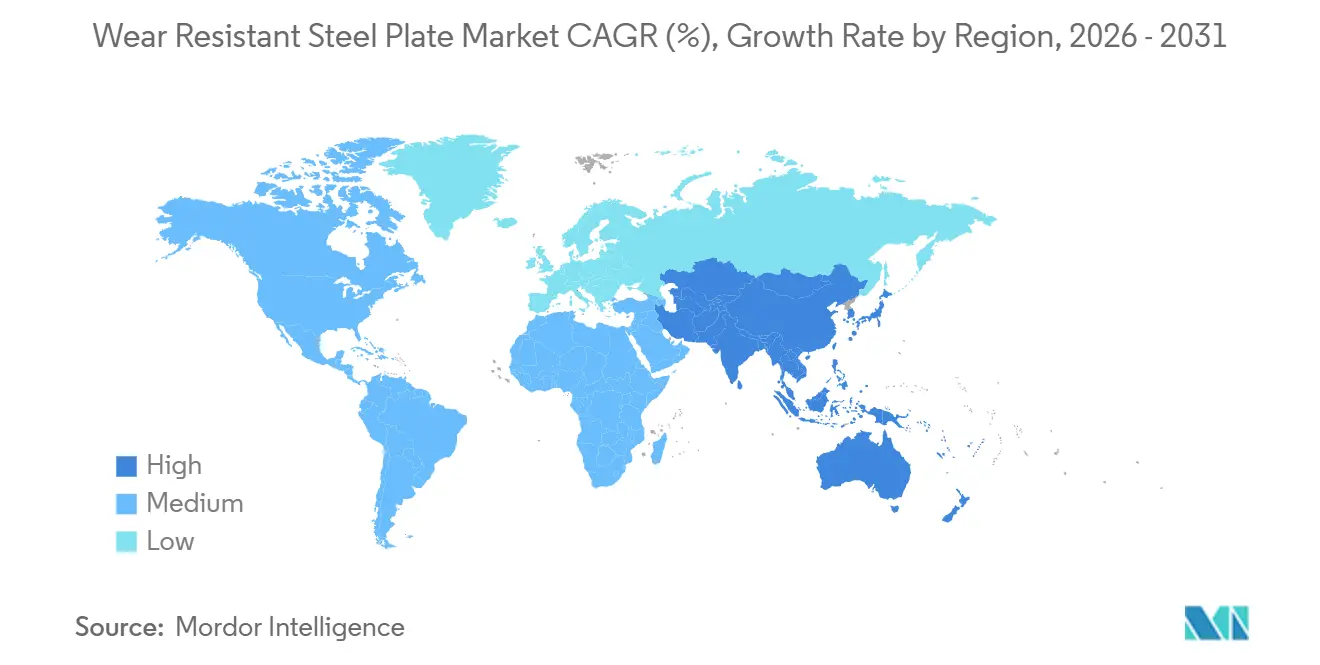

- By geography, Asia-Pacific commanded 47.72% volume in 2025 and is set to post a 4.66% CAGR, maintaining regional leadership.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wear Resistant Steel Plate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing infrastructure development and urbanization | +1.2% | Asia-Pacific core, spill-over to Middle East and South America | Medium term (2-4 years) |

| Growth in industrial machinery and heavy equipment sectors | +0.9% | Global, focus on North America and Europe replacement cycles | Long term (≥ 4 years) |

| Need for longer equipment life and lower maintenance costs | +0.7% | Global, mining-intensive regions | Long term (≥ 4 years) |

| Digital wear-monitoring and predictive-maintenance adoption | +0.5% | North America and EU early adopters | Medium term (2-4 years) |

| Hydrogen-ready green steel routes requiring ultra-clean wear grades | +0.4% | EU and Japan leading, China and India scaling | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Infrastructure Development and Urbanization

U.S. federal funding is driving demand for excavator buckets, loader edges, and demolition shears. These now use 500 HBW plates to improve uptime, increasing per-project tonnage while overall growth remains moderate. In India, the National Infrastructure Pipeline, with a cumulative capital outlay of USD 1.4 trillion, is supporting demand for crusher-liners and conveyor-chutes in the 400 to 500 HBW grade range[1]Government of India, “National Infrastructure Pipeline Dashboard,” india.gov.in. In Vietnam, Indonesia, and Thailand, investments in highways and ports are increasing the need for thick (> 40 mm) wear plates, particularly for piling shoes and dredge components. Contractors in tier-2 Asian cities are adopting ISO 6301-1 hardness tolerances, shifting sourcing from local soft steels to globally certified abrasion-resistant grades. These civil-works programs are influencing the specification baseline, requiring greater thickness and hardness for each tonne of concrete handled.

Growth in Industrial Machinery and Heavy Equipment Sectors

Body panels for the Komatsu 980E haul truck now require a hardness of over 400 HBW. This change eliminates conventional HSLA alternatives and highlights the demand for quenched-and-tempered plates. Crusher manufacturers targeting a throughput of 1,000 ton/hour are adopting overlay liners. These liners incorporate martensitic skins on a mild-steel backing, achieving a 25% reduction in weight while maintaining service life. Fleets in North America and Europe, acquired during the commodity boom from 2010 to 2015, have reached their end-of-life. This creates a predictable wave of replacements, largely unaffected by fluctuations in new mine activity. Service centers are responding to this trend by increasing their value-added share. They are supplying laser-profiled, kit-ready sets, which reduce on-site labor and minimize downtime. Consequently, the wear-resistant steel plate market is driven not only by raw tonnage but also by the demand for kit fabrication and field service efficiency.

Need for Longer Equipment Life and Lower Maintenance Costs

Miners in Australia and Chile are now structuring their procurement contracts around guaranteed operating hours instead of traditional grade designations. This shift is prompting mills to adjust their processes, ensuring sulfur levels drop below 0.003% and incorporating calcium treatments to enhance ductility. By extending a truck body's operational hours from 8,000 to 12,000, miners can realize a net-present-value gain of USD 300,000 per unit, based on current haulage rates. Predictive maintenance systems, which meld ultrasonic gauges with machine-vision cameras, facilitate timely replacements during scheduled downtimes, thereby maximizing the value of longer-lasting plates. These economic trends bolster the demand for thicker gauges and increased hardness in the wear-resistant steel plate market.

Digital Wear-Monitoring and Predictive-Maintenance Adoption

Edge-mounted IoT sensors in haul-truck beds transmit real-time thickness data, providing shift-based dashboards that identify remaining life with 24-hour accuracy. Field pilots in Western Australia demonstrated a 22% reduction in unscheduled liner change-outs, validating the effectiveness of condition-based strategies at copper and gold sites. Sensor analytics identified abrasion concentrated in leading edges, driving the adoption of hybrid layouts: 500 HBW in impact zones, 400 HBW in other areas, and structural steel where contact is minimal. This approach reduced material costs by 18% while maintaining uptime. SSAB’s Hardox In My Body program combines sensors with plates and a three-year analytics subscription, enabling predictive maintenance for mid-tier fleets. ISO 13374 data-format standards are increasingly adopted, allowing mines to avoid vendor lock-in and integrate wear data directly into enterprise asset-management platforms[2]ISO, “ISO 6301-1:2024 Structural Steels,” iso.org .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of substitutes (hard-facing, ceramics, polymers) | –0.6% | Global, higher penetration in chemical processing and slurry handling | Medium term (2-4 years) |

| Volatility in iron-ore and alloying-element prices | –0.4% | Global, acute in seaborne-dependent regions | Short term (≤ 2 years) |

| Supply-chain emissions caps tightening scrap-to-billet availability | –0.3% | EU and China, spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of substitutes (hard-facing, ceramics, polymers)

Flux-cored hard-facing deposits place chromium-carbide precisely where wear occurs, reducing steel usage by 70% and enabling in-situ refurbishments that eliminate the need for component removal. In some coal and grain installations, UHMW-PE liners reduce material build-up in low-impact chutes, leading to a complete replacement of steel. Ceramic tile packages in slurry pumps have now achieved a hardness of 1,000 HV, exceeding the 600 HBW plate life and affecting high-margin niches. SSAB’s Duroxite overlay welds carbide onto a structural backing, combining the wear life of ceramics with their weldability, creating a hybrid defense against market substitution. However, the lack of fracture toughness in both polymers and ceramics, particularly in impact zones, ensures the core of the wear-resistant steel plate market remains stable.

Supply-Chain Emissions Caps Tightening Scrap-to-Billet Availability

The EU's CBAM imposes an additional cost of EUR 50–80/ton on blast-furnace plate imports lacking proof of low-carbon intensity. This move is hastening the industry's shift towards electric-arc furnaces (EAFs). From 2020 to 2025, prime scrap generation in the EU saw a modest annual growth of 2.1%. In contrast, EAF capacity surged by 4.3%, leading to a widening deficit. Consequently, prime scrap prices soared to EUR 380/ton in early 2026. In 2025, China's scrap collection reached only 260 million tons, a fraction of its 1.03 billion tons of crude steel output. This shortfall resulted in a 75% dependency on iron ore, a situation made more expensive by policy-imposed caps. Meanwhile, U.S. EAF expansions, spurred by the Inflation Reduction Act, confront a similar challenge: a potential appetite for 90 million tons of scrap but only a 70 million tons domestic supply. This gap necessitates imports from Mexico, putting pressure on border rail capacity. Mills like SSAB and ArcelorMittal, with the flexibility to blend Direct Reduced Iron (DRI) or Hot Briquetted Iron (HBI), can sustain their wear-grade output. In contrast, scrap-dependent minimills are either downgrading to structural grades or exiting the market altogether. This shift is tightening the availability of wear-resistant steel plates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Impact Toughness Gains Traction

In 2025, abrasion-resistant plates accounted for 46.61% of the market share, supported by their use in continuous-wear environments such as haul-truck floors and conveyor skirts, which require a hardness of 400–500 HBW. The impact-resistant plate segment is anticipated to grow at a CAGR of 4.12% through 2031. This growth is driven by the adoption of plates with a Charpy toughness of 27 J or higher at –40 °C in demolition and recycling yards to mitigate brittle fractures. Overlay and bimetallic solutions, featuring 4–8 mm carbide layers on mild-steel backings, reduce weight by 30% compared to solid plates. This weight reduction appeals to cost-sensitive mid-tier mining budgets. High-strength wear-resistant grades with a 1,000 MPa yield are designed for mobile cranes and tele-handlers, where structural strength is prioritized over abrasion resistance.

The standard 400 and 500 HBW grades experience significant competition, with more than 20 active mills operating globally in the wear-resistant steel plate market. Hybrid overlays are increasing market accessibility by offering localized hardness at approximately 60% of the cost of full-thickness plates. This cost efficiency is encouraging quarry operators and aggregate producers to explore higher hardness classes. The segment is shifting from generic commodity sheets to application-specific kits, which are now integrated with digital wear tracking features.

By Thickness: Heavy Gauge Holds Majority Share

Plates exceeding 30 mm represented 53.11% of the 2025 volume. This reflects the requirements of ultra-class haul-truck bodies and 1,000 ton/hour crushers, which need 35–60 mm walls to withstand repeated 300 MPa load cycles. This sub-segment is anticipated to grow at a CAGR of 3.96%, driven by the adoption of thicker wear shims in larger mobile equipment and bridge-bearing pads. Plates in the 10–30 mm range are primarily used in dozers, loaders, and excavators. In this segment, while thickness is limited due to mass trade-offs, maintaining 450–500 HBW hardness is critical. Plates under 10 mm are applied in agricultural tillage tools and light-duty bins, although they face competition from in-situ hard-facing overlays.

Fabrication economics significantly influence demand. Laser and plasma cutting methods remain cost-effective for plates up to 30 mm. For thicker plates, oxy-fuel processes increase processing costs by 20%, leading some buyers to opt for overlays with a 6 mm hard layer on a 25 mm structural base. Although ceramic materials pose a substitution risk, they do not match the structural load-bearing capacity required for 50 mm truck floors. As a result, heavy gauge plates continue to play a central role in the wear-resistant steel plate market.

By Application: Mining Anchors While Construction Rises

Mining represented 45.67% of the 2025 tonnage, supported by the global fleet expansion for copper, lithium, and iron ore. Each haul-truck overhaul requires 8–12 tons of plate over its lifecycle. Construction is projected to grow at a 4.72% CAGR through 2031, driven by the U.S. Infrastructure Act and large-scale Asian projects. These initiatives are increasing the demand for 500 HBW bucket edges and shear blades to meet project timelines. In Southeast Asia, rising container traffic is driving the need for heavy machinery such as gantry cranes and reach stackers. In India and China, the addition of new EAF capacity in steel plants and foundries is increasing the demand for 450 HBW slag-pot and tundish liners.

The recycling segment is gaining traction as electric-arc furnace expansions increasingly depend on shredders and sorting lines equipped with impact-tough plates, transitioning the segment from a niche application to a broader market. The transportation segment, including railcars and bulk holds, remains stable due to the long lifecycle of assets. However, the adoption of predictive maintenance is extending wear life while simultaneously raising material cleanliness standards. This shift is favoring mills capable of meeting higher qualification requirements with ultra-clean chemistries.

Geography Analysis

In 2025, Asia-Pacific accounted for 47.72% of the global volume and is expected to grow at a 4.66% CAGR through 2031, surpassing all other regions. China, supported by Baowu and HBIS capacities each exceeding 7 million tons for wear grades, remains a key contributor to the region's volume. However, with dual-control output caps in place, mills are shifting focus toward value-added plates instead of bulk production. In India, the National Infrastructure Pipeline is driving demand for crusher-liners and conveyor-chute replacements, contributing to consistent growth for the 400–500 HBW grades. In Southeast Asia, public-investment completion rates exceeding 95% are directing thicker plates (> 40 mm) into piling shoes and dredge components, driven by investments in highways and ports.

In North America, the U.S. Infrastructure Investment and Jobs Act has prompted upgrades to 500 HBW bucket edges. This initiative reduces mid-project downtime fines and encourages OEMs to maintain inventories of thicker plates. Canada’s iron-ore and potash operations continue to generate steady demand for wear plates, while Mexico’s near-shoring of automotive supply chains is increasing the need for material-handling equipment liners. As replacement cycles align across mining and construction fleets, the wear-resistant steel plate market in North America is projected to grow at a 3.5% CAGR.

In Europe, western countries are focusing on green initiatives, while eastern countries face cost pressures. Germany and Scandinavia are transitioning to fossil-free supplies. SSAB’s hydrogen plate, which complies with CBAM tenders, has secured OEM contracts with premiums of approximately 7%. In contrast, eastern mills that rely on blast-furnace routes are dealing with EUR 50–80/ton CBAM levies, which are affecting their market share. The region primarily relies on replacement demand rather than new tonnage, but low-carbon procurement rules are helping qualified suppliers maintain margins.

In South America and the Middle East-Africa, Brazil’s Vale is utilizing plates for truck bodies and crushers. In Saudi Arabia, the Vision 2030 initiative is driving imports of thicker gauges for demolition shears. Although energy volatility and currency fluctuations are limiting growth in South Africa and Argentina, niche markets in phosphate and gold mining are sustaining demand.

Competitive Landscape

In 2025, the wear-resistant steel plate market reflected a moderately concentrated profile, with the top five producers being SSAB, ArcelorMittal, Nippon Steel, China Baowu Steel Group, and thyssenkrupp. Integrated mills leveraged captive iron ore and ferrochrome, while specialty suppliers such as Bisalloy and NLMK DanSteel focused on ultra-high-hardness offerings (600 HBW+) and expedited 48-hour delivery programs designed for mine shutdowns.

Decarbonization and digitalization remained key strategic priorities. SSAB, with its fossil-free plates, aimed to meet the demand from OEMs requiring products with verified emissions of less than 0.4 tons of CO₂ per ton. Nippon Steel's planned USD 14 billion upgrade of U.S. Steel assets aligned with Buy America content rules and targeted opportunities in North America's infrastructure spending. SSAB also introduced the Hardox In My Body ecosystem, which combines pre-cut kits, IoT thickness sensors, and a three-year analytics license, driving recurring subscription revenue and increasing switching costs for fleet operators.

Technological investments focused on in-line ultrasonic mapping to ensure uniformity in through-thickness hardness. This development reduced reject rates from 4% to 1%, supporting just-in-time deliveries. The patent race intensified in 2024–2025, with efforts centered on explosive-welded overlays and laser-clad chromium carbides. Both thyssenkrupp and voestalpine filed 8–10 patents each, aiming to improve layer adhesion under high-impact loads.

Wear Resistant Steel Plate Industry Leaders

ArcelorMittal

SSAB

thyssenkrupp AG

NIPPON STEEL CORPORATION

Shandong Baowu Steel Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: POSCO restarted the No. 4 blast furnace at its Pohang works following a KRW 500 billion (USD 375 million) upgrade that increased annual capacity by 1.2 million tons and integrated digital twin technology for real-time process optimization. The expansion positions POSCO to capture growing wear-plate demand from South Korea's shipbuilding and construction sectors, which are adopting thicker-gauge plates for LNG carrier insulation supports and high-rise foundation piles.

- April 2025: JFE Steel is currently building a 2-million-ton-per-year large-scale electric arc furnace (EAF) at its West Japan Works (Kurashiki district), with operations scheduled to start in the first half of fiscal year 2028 (Q1 FY2028).

Global Wear Resistant Steel Plate Market Report Scope

Wear resistant steel plates, often called abrasion resistant (AR) steel, are specialized high-hardness, high-toughness steel plates designed to withstand extreme surface abrasion, gouging, and impact. Used as "sacrificial" layers to protect structural equipment, they extend the life of parts in mining, construction, and manufacturing.

The market is segmented by product type, thickness, application, and geography. By product type, the market is segmented into abrasion-resistant plates, high-strength wear-resistant plates, impact-resistant plates, and overlay and bimetallic plates. By thickness, the market is segmented into below 10 mm, 10 to 30 mm, and above 30 mm. By application, the market is segmented into mining, construction, heavy machinery, steel and foundry, transportation, and other applications (including agriculture, recycling, and the cement and aggregate industry). The report also covers the market size and forecasts for Wear Resistant Steel Plate in 17 countries across the world. For each segemnt market sizing and forecasts are provided in terms of volume (tons).

| Abrasion-resistant plates |

| High-strength wear-resistant plates |

| Impact-resistant plates |

| Overlay and bimetallic plates |

| Below 10 mm |

| 10 to 30 mm |

| Above 30 mm |

| Mining |

| Construction |

| Heavy machinery |

| Steel and foundry |

| Transportation |

| Other Applications (Agriculture, Recycling, Cement and aggregate industry) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Abrasion-resistant plates | |

| High-strength wear-resistant plates | ||

| Impact-resistant plates | ||

| Overlay and bimetallic plates | ||

| By Thickness | Below 10 mm | |

| 10 to 30 mm | ||

| Above 30 mm | ||

| By Application | Mining | |

| Construction | ||

| Heavy machinery | ||

| Steel and foundry | ||

| Transportation | ||

| Other Applications (Agriculture, Recycling, Cement and aggregate industry) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the wear resistant steel plate market?

The Wear Resistant Steel Plate Market size is projected to be 3.28 Million tons in 2025, 3.40 Million tons in 2026, and reach 4.06 Million tons by 2031, growing at a CAGR of 3.62% from 2026 to 2031.

Which region accounts for the largest demand for wear plate?

Asia-Pacific led with 47.72% of global volume in 2025 and remains the fastest-growing region.

Which application segment is growing fastest?

Construction equipment is forecast to expand at a 4.72% CAGR through 2031 thanks to global infrastructure programs.

How does hydrogen DRI influence wear plate quality?

Hydrogen-based DRI eliminates tramp elements and lowers residual nitrogen, enabling cleaner, tougher 500 HBW grades suitable for ultra-demanding mining and construction uses.

Page last updated on: