Finished Steel Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

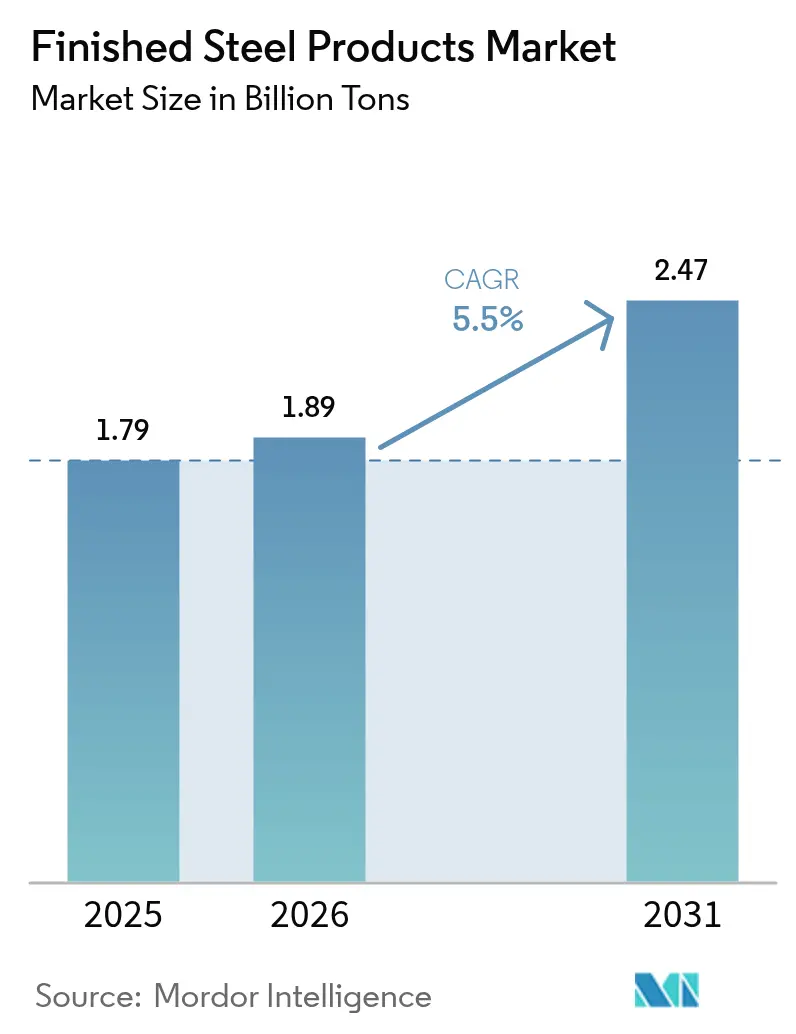

| Market Volume (2026) | 1.89 Billion tons |

| Market Volume (2031) | 2.47 Billion tons |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finished Steel Products Market Analysis by Mordor Intelligence

Finished Steel Products market size in 2026 is estimated at 1.89 billion tons, growing from 2025 value of 1.79 billion tons with 2031 projections showing 2.47 billion tons, growing at 5.50% CAGR over 2026-2031. Robust infrastructure pipelines in Asia and Africa, rising electric-vehicle (EV) penetration, and renewable-energy build-outs continue to anchor volume growth in the finished steel products market. Expanded electric-arc-furnace (EAF) capacity, supported by abundant metallic scrap, is improving regional cost competitiveness, while additive-manufacturing breakthroughs are opening new precision-engineering opportunities. Price volatility in iron ore and coking coal, coupled with trade-policy shifts, is reshaping sourcing strategies, yet sustained government spending on transport, energy, and housing projects buffers cyclical demand swings. The finished steel products market continues to benefit from defense re-armament, which drives premium demand for quenched-and-tempered (Q&T) grades, while rising carbon-pricing regimes accelerate capacity upgrades toward low-carbon production routes.

Key Report Takeaways

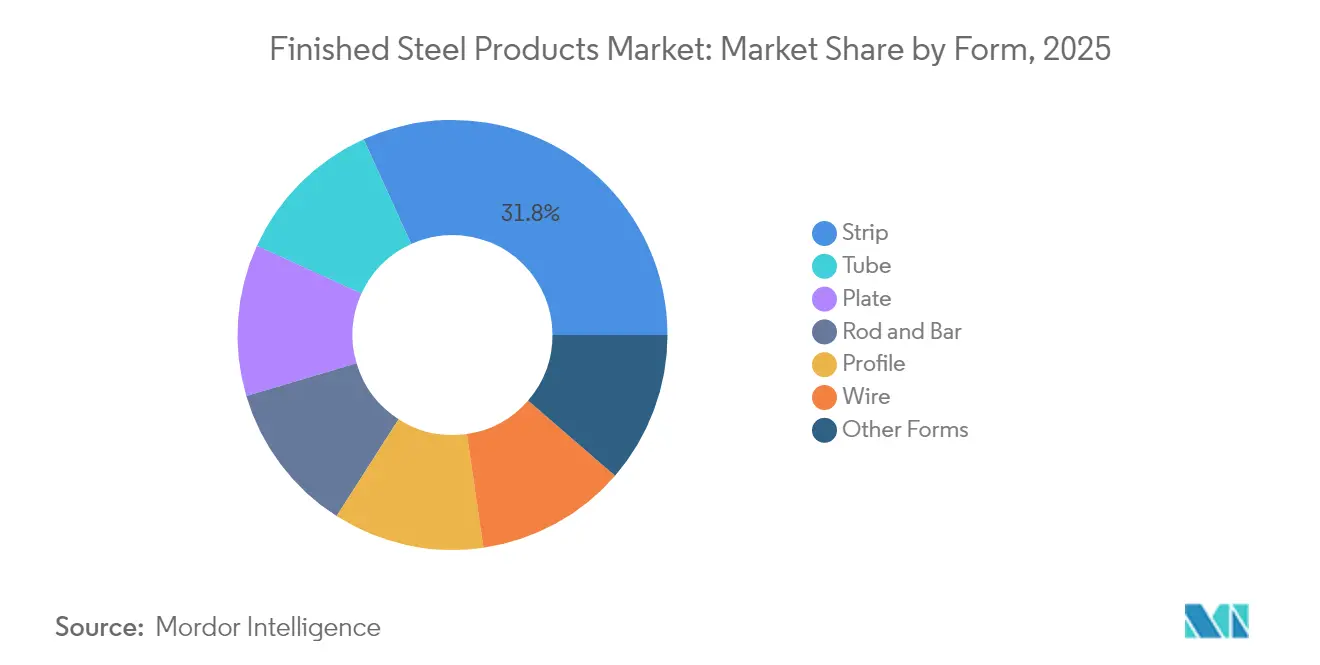

- By form, strip products led with a 31.78% revenue share in 2025, whereas tube products are forecast to expand at a 6.24% CAGR through 2031.

- By process, hot-rolling accounted for a 47.05% share of the finished steel products market size in 2025, while additive manufacturing is projected to grow at a 7.66% CAGR to 2031.

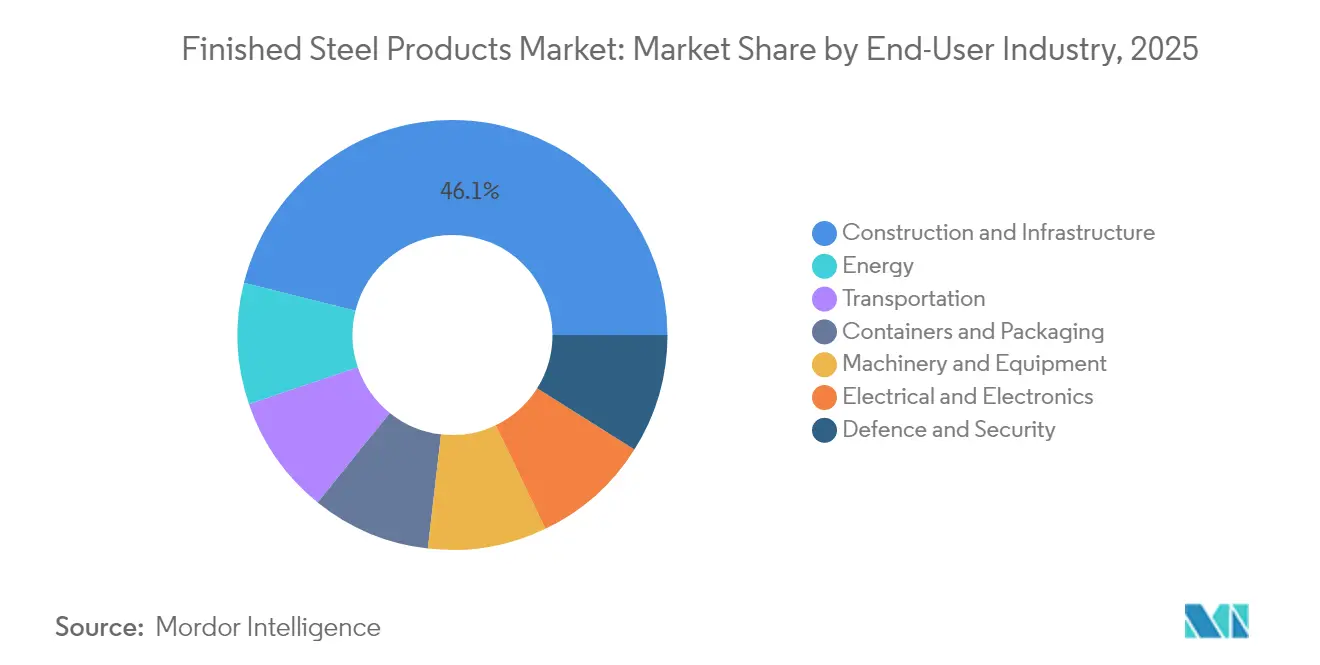

- By end-user industry, construction and infrastructure captured 46.10% of the finished steel products market share in 2025; energy applications represent the fastest-growing segment, advancing at a 5.95% CAGR during the forecast period.

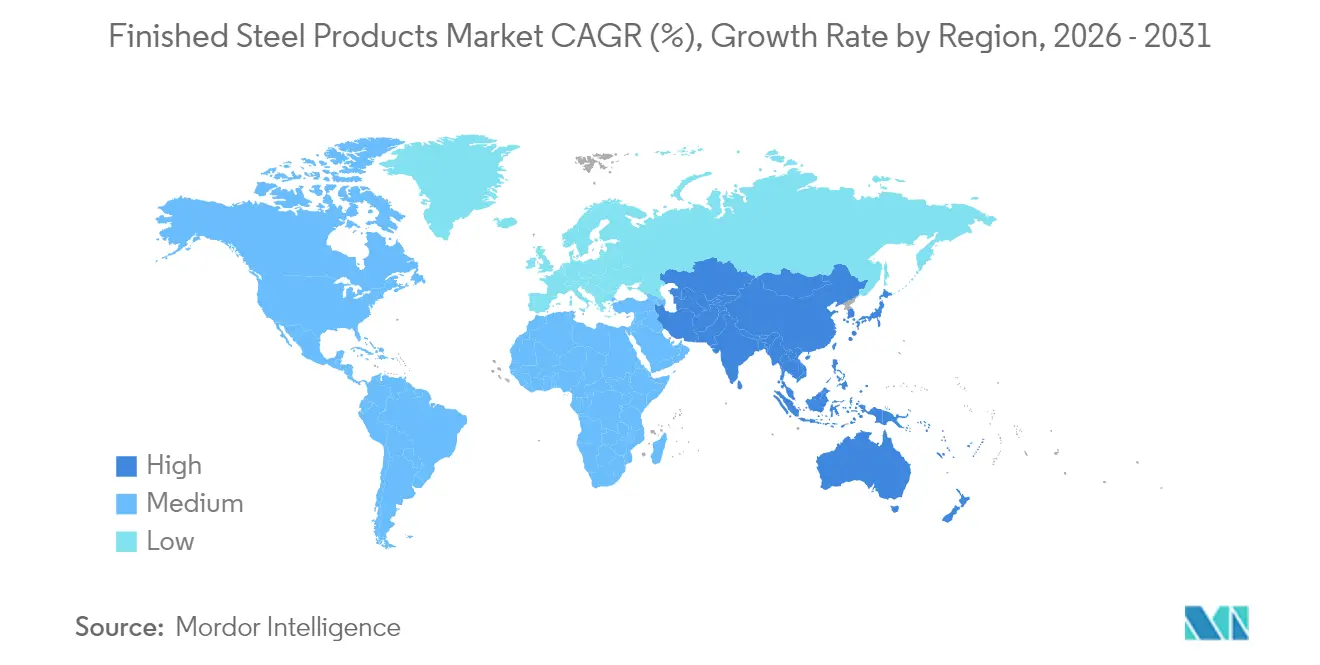

- By geography, Asia-Pacific dominated with a 60.88% share of the finished steel products market in 2025 and is poised to record the highest regional CAGR of 6.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Finished Steel Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure boom in Asia and Africa | +1.80% | Asia-Pacific core; Africa emerging | Medium term (2-4 years) |

| EV-driven demand for AHSS and electrical steels | +1.20% | Global; strongest in China, Europe, North America | Long term (≥ 4 years) |

| Renewable-energy build-out | +0.90% | Global | Long term (≥ 4 years) |

| Scrap-availability surge enabling EAF capacity growth | +0.70% | North America, Europe | Medium term (2-4 years) |

| Defense re-armament boosting Q&T armor plate | +0.40% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure boom in Asia and Africa

Annual infrastructure needs of USD 1.7 trillion in Asia and USD 67.6–107.5 billion in Africa are expanding demand for structural bars, beams, and rebar[1]Asian Development Bank, “Meeting Asia’s Infrastructure Needs,” adb.org . China’s Belt and Road Initiative spans 140 countries, funneling large tonnage orders to regional mills. India’s National Infrastructure Pipeline, valued at USD 1.4 trillion through 2025, continues to stimulate domestic capacity additions. Major producers are therefore establishing downstream finishing hubs nearer to project locations, shortening lead times and strengthening the finished steel products market. Intensified localization is also helping reduce CO₂ emissions tied to long-haul shipping.

EV-driven demand for AHSS and electrical steels

Advanced high-strength steel (AHSS) presently constitutes 35–40% of a typical EV body, up from 20% in conventional models. Tesla’s 2 million-unit capacity and BYD’s aggressive scaling point toward automotive steel consumption reaching 25–30 million tons by 2030. Grain-oriented electrical steels required for 800-volt traction motors are growing 15–20% annually, fetching premium price differentials. Suppliers are responding with rapid alloy-development cycles, hot-stamping expansions, and coating upgrades to safeguard market share against aluminum and composite alternatives. These investments enhance the finished steel products market as automakers recalibrate material balances for weight, safety, and cost.

Renewable-energy build-out driving steel intensity

Wind turbines consume 120–180 tons of steel per MW, while solar installations require 35–45 tons per MW. Global renewable additions exceeding 300 GW each year translate into more than 30 million tons of incremental annual demand, favoring plate, tower, and tubular products. Offshore wind development further boosts demand for corrosion-resistant and high-strength grades. Grid-modernization initiatives add sustained growth for transformer and power-transmission steels, reinforcing the finished steel products market outlook.

Scrap-availability surge enabling EAF capacity growth

Global scrap availability is projected to reach 800–900 million tons by 2030, lifting the EAF share of crude-steel production from 30% to 40%. Hyundai Steel’s USD 5.8 billion Louisiana plant, slated for 2029, exemplifies this drift toward flexible mini-mills. Greater scrap pools reduce dependence on iron ore and coking coal, lower operating emissions, and enable regional supply resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost volatility | -0.80% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Lightweight substitutes (Al, CFRP) in transport | -0.60% | North America, Europe, premium automotive segments | Long term (≥ 4 years) |

| EU-CBAM and green-premium cost divergence | -0.50% | Europe core, spillover to export-dependent producers | Medium term (2-4 years) |

| Structural over-capacity in China and GCC | -0.40% | Global, acute in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-material cost volatility pressuring margins

Iron ore and coking coal prices fluctuated sharply during 2024 and 2025 as supply disruptions and currency changes intersected with uneven demand recovery. Vale, Rio Tinto, and BHP collectively control a significant share of seaborne ore, magnifying price swings during outages or weather events. Elevated power prices in Europe—often two to three times those in Asia or the United States—erode local mill competitiveness. These dynamics compel steelmakers to pursue long-term supply contracts, hedging programs, and vertical integration to shield EBITDA margins in the finished steel products market.

Lightweight substitutes challenging traditional applications

Aluminum content in premium passenger vehicles has risen to 180–200 kg per car, while carbon-fiber-reinforced plastics (CFRP) are displacing steel in aerospace fuselages and select automotive panels[2]Massachusetts Institute of Technology Technology Review, “The World’s First Industrial-Scale Plant for Green Steel,” technologyreview.com . Lightweighting initiatives, driven by fuel-efficiency standards and EV range priorities, threaten steel penetration in transportation. Steelmakers counter with third-generation AHSS grades delivering comparable weight savings at lower cost, supported by established recycling loops and supply-chain familiarity. Continuous innovation remains essential to sustain competitiveness within the finished steel products market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Strip Products Sustain Leadership While Tubes Accelerate

Strip products generated the highest volume, capturing a 31.78% share in 2025 on the strength of automotive panels, appliance casings, and construction cladding. Robust demand from unibody vehicle platforms and standardized building components keeps mill utilization high. The finished steel products market size for strip products is forecast to maintain steady growth as surface-quality requirements rise. Tube products, although smaller in volume, are projected to achieve the fastest 6.24% CAGR through 2031, supported by pipeline expansions, renewable-energy towers, and HVAC installations. Precision tubes for automotive fuel lines and aerospace hydraulics command premium margins, encouraging investment in advanced welding and inspection systems.

Ongoing infrastructure spending in emerging markets supports heavy-section plate sales, whereas rod and bar benefit from reinforced-concrete demand. Profile and wire forms secure niche positions in engineered structures and electronic applications. Producers continue to optimize line flexibility to shift between strip and tube output as end-market signals evolve, preserving competitiveness within the finished steel products market.

By Process: Hot-Rolling Dominates, Additive Manufacturing Gains Momentum

Hot-rolling retained a commanding 47.05% revenue share in 2025, fueled by its cost efficiency and suitability for bulk applications in automotive, construction, and heavy equipment. Modern continuous-casting and thin-slab technologies improve yield and reduce energy use, sustaining hot-rolling relevance even as decarbonization pressures mount. Additive-manufacturing output, though less than 1% of tonnage, is forecast to soar at a 7.66% CAGR. Aerospace engine brackets, medical implants, and tooling inserts lead early adoption, demonstrating the technology’s value in near-net-shape fabrication and rapid prototyping.

Hertha Metals’ single-step pyrometallurgical process, validated at its Texas pilot plant, underscores the disruptive potential of small-scale molten-metal printing, promising 30% energy savings and 98% emission cuts when powered by clean hydrogen. Cold-rolling, forging, casting, extrusion, and drawing remain integral, especially for high-precision or high-strength applications, yet capital allocation is gradually migrating toward hybrid lines capable of additive finishing. These shifts keep the finished steel products market adaptive to emerging technology platforms.

By End-user Industry: Construction Leads; Energy Surges

Construction and infrastructure consumed 46.10% of total volume in 2025, reflecting sustained urbanization and large-scale transport projects. Rapid residential development in emerging economies continues to underpin reinforcing bar sales, while commercial real-estate renovations drive beams and structural sections. The finished steel products market size linked to construction is expected to grow steadily as governments prioritize housing affordability and climate-resilient public works.

Energy applications represent the fastest-growing end-use, with a 5.95% CAGR forecast through 2031. Each MW of installed wind capacity requires up to 180 tons of steel, and over 300 GW of annual renewable additions translate into significant plate and tubular demand. Transmission-line upgrades and battery-storage projects further enhance electrical-steel consumption. Transportation, machinery, packaging, electronics, and defense add diversified volume streams, mitigating sector-specific volatility and reinforcing the robustness of the finished steel products market.

Geography Analysis

Asia-Pacific generated the largest share at 60.88% in 2025 and is forecast to expand at a 6.12% CAGR, combining massive domestic consumption with export capability. China’s crude-steel output exceeded 1 billion tons in 2024, though carbon-pricing trials and capacity-swap regulations are nudging mills toward high-quality finishing and green-steel projects. India’s USD 1.4 trillion National Infrastructure Pipeline accelerates domestic demand, while Southeast Asia benefits from rising electronics and appliance manufacturing. Policy incentives for hydrogen-based direct-reduced-iron (DRI) and scrap-based EAFs aim to balance growth with emission commitments, thereby sustaining the finished steel products market.

North America is reorganizing around supply-chain security after the March 2025 imposition of 25% import tariffs. EAF expansions, such as Hyundai Steel’s Louisiana project, exploit abundant scrap and inexpensive energy. Regional OEMs increasingly favor local sourcing to mitigate tariff costs and geopolitical risk, supporting the finished steel products market despite cyclical construction softness.

Europe faces decarbonization and import-safeguard challenges under its Steel Action Plan, targeting a 15% reduction in non-EU inflows by 2026. Power-price differentials and carbon taxes pressure margins, yet hydrogen-driven DRI pilots and circular-economy scrap programs are positioning European mills as early movers in low-carbon premium grades. South America leverages abundant iron-ore reserves and renewable power to court green-steel investments, while Middle East and Africa, responsible for 45% of global DRI, aim to serve emerging green-iron corridors linking resource-rich regions with demand centers in Europe and Asia. These regional strategies collectively support long-term resilience in the finished steel products market.

Competitive Landscape

The finished steel products market exhibits highly fragmented concentration. China Baowu Steel Group leads global output, followed by ArcelorMittal, POSCO, HBIS, and Nippon Steel, yet specialized grades and regional proximity grant smaller mills competitive pockets.

Strategic moves center on vertical integration, decarbonization, and digitalization. U.S. Steel entered an AI-enabled maintenance partnership with Gecko Robotics in 2025 to boost asset uptime and reduce inspection costs. Nucor invested in Electra’s zero-carbon iron technology to secure low-emission feedstock for its EAF network. ArcelorMittal and BHP jointly advanced green-steel pilot trials featuring hydrogen injection into blast furnaces, targeting 30% emission cuts by 2030.

Trade policy shifts also reshape competitive dynamics. The Biden administration blocked Nippon Steel’s proposed USD 14.9 billion acquisition of U.S. Steel on national-security grounds in 2025, signaling heightened scrutiny of cross-border consolidation. Meanwhile, European safeguard measures deter low-priced imports, accelerating regional mini-mill capacity additions. Breakthroughs such as Hertha Metals’ fast-cycle pyrometallurgical technology threaten to disrupt legacy scale economics by enabling profitable 500,000-ton micro-mills. These developments keep the finished steel products market dynamic and innovation-driven.

Finished Steel Products Industry Leaders

ArcelorMittal

Baosteel Group

Nippon Steel Corporation

HBIS Group

POSCO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: BMW Industries Ltd. (BMWIL) has announced an investment of INR 803 crore (~USD 90.49 million) to establish a 0.5 million tonne cold rolling unit in Jharkhand, India. Supported by the government's PLI Scheme for Speciality Steel, this expansion will increase the company's manufacturing capacity to 2.5 million tons.

- May 2025: Tata Steel has initiated the Phase II expansion of its Kalinganagar facility in India, with the objective of enhancing its integrated steel production capacity. This development is expected to strengthen the company's position in the finished steel products market by meeting growing demand and improving supply capabilities.

Global Finished Steel Products Market Report Scope

Finished steel refers to products that are ready for the market just after completing the process of hot rolling or forging semi-finished steel products such as blooms, billets, or slabs. When compared to other materials, finished steel products offer excellent strength, safety, and comparatively low costs. The two broad categories of products include "long" products and "flat" products. The finished steel products market is segmented by form, process, end-user industry, and geography. By form, the market is segmented into plate, strip, rod, profile, tube, wire, and other forms. By process, the market is segmented into hot-rolling, cold-rolling, forging, and other processes. By end-user industry, the market is segmented into transportation, construction, energy, containers and packaging, electrical and electronics, and other end-user industries. The report also covers the market size and forecasts for the market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

| Plate |

| Strip |

| Rod and Bar |

| Profile |

| Tube |

| Wire |

| Other Forms |

| Hot-Rolling |

| Cold-Rolling |

| Forging |

| Casting |

| Extrusion and Drawing |

| Additive Manufacturing of Steel |

| Construction and Infrastructure |

| Transportation |

| Energy |

| Containers and Packaging |

| Electrical and Electronics |

| Machinery and Equipment |

| Defence and Security |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Turkey | |

| Rest of Middle-East and Africa |

| By Form | Plate | |

| Strip | ||

| Rod and Bar | ||

| Profile | ||

| Tube | ||

| Wire | ||

| Other Forms | ||

| By Process | Hot-Rolling | |

| Cold-Rolling | ||

| Forging | ||

| Casting | ||

| Extrusion and Drawing | ||

| Additive Manufacturing of Steel | ||

| By End-user Industry | Construction and Infrastructure | |

| Transportation | ||

| Energy | ||

| Containers and Packaging | ||

| Electrical and Electronics | ||

| Machinery and Equipment | ||

| Defence and Security | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Turkey | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand be for finished steel products by 2031?

Volume is projected to reach 2.47 billion tons by 2031, reflecting a 5.50% CAGR from 2026 levels.

Which region contributes most to finished steel growth?

Asia-Pacific dominates with 60.88% of 2025 volume and is forecast to grow at 6.12% CAGR through 2031, driven by China, India, and Southeast Asia.

What segment of finished steel is expanding fastest?

Tube products, supported by energy-infrastructure projects and precision industrial uses, are forecast to post a 6.24% CAGR to 2031.

How is decarbonization influencing steelmaking processes?

Investment is shifting toward EAF capacity and hydrogen-based direct-reduction, while additive manufacturing offers energy-efficient near-net-shape fabrication.

What are the key risks facing producers?

Raw-material cost volatility, trade-policy uncertainty, and competition from lightweight substitutes such as aluminum and CFRP present headwinds.

Page last updated on: