Coating Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 24.39 Billion |

| Market Size (2031) | USD 32.46 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

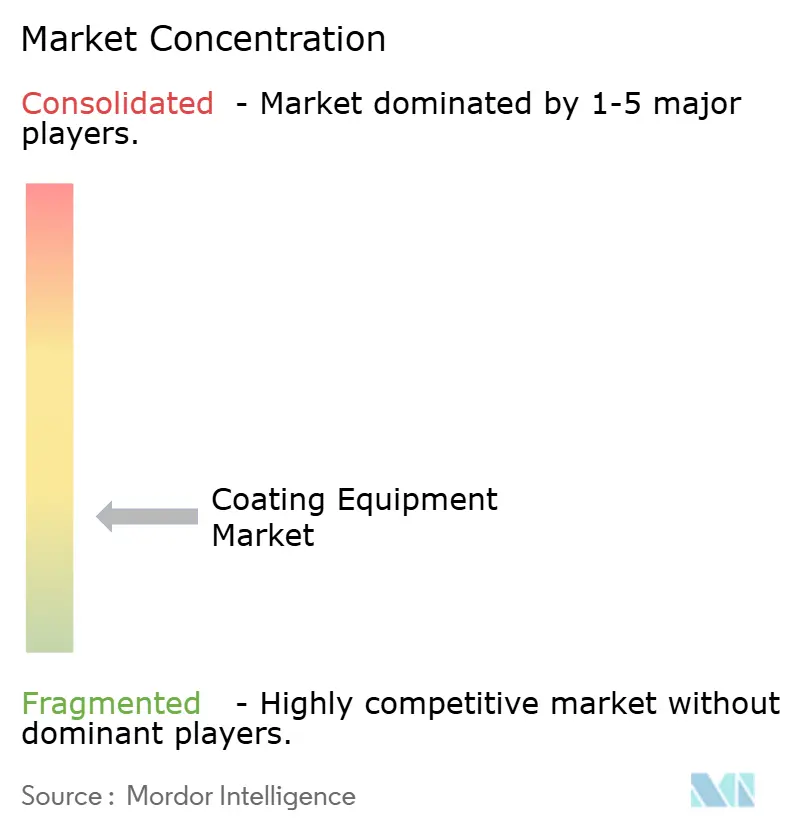

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coating Equipment Market Analysis by Mordor Intelligence

The Coating Equipment Market size is projected to expand from USD 23.20 billion in 2025 and USD 24.39 billion in 2026 to USD 32.46 billion by 2031, and is expected to register a CAGR of 5.88% between 2026 to 2031. Demand in the coating equipment market is being shaped by the shift toward EV production platforms, tighter regulations on solvent-heavy and chromium-based surface treatments, and faster adoption of robotic application systems that reduce dependence on manual lines. These changes are driving demand for new equipment and accelerating replacement decisions for aging assets. Suppliers are now serving two distinct customer groups: one focused on new EV paint shops and another focused on upgrading existing lines. This split is influencing product design, service requirements, and project timelines. Sustainability regulations are also shifting buying decisions toward powder, electrostatic, and electrified drying systems, raising the value of compliance-ready installations. Trade frictions and localization demands have slowed some order cycles, but the market's long-term direction remains tied to the EV ramp-up, compliance upgrades, and multi-region industrial investment.

Key Report Takeaways

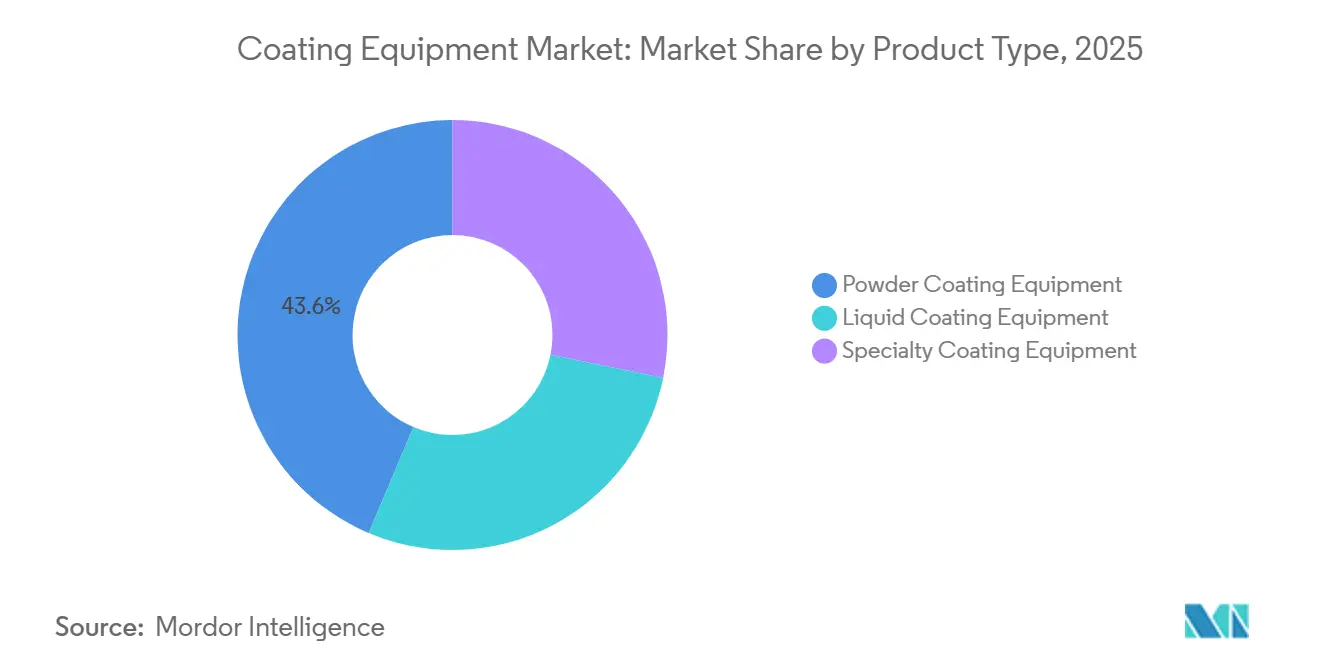

- By product type, Powder Coating Equipment held a 43.63% share in 2025, while Specialty Coating Equipment is projected to expand at 7.62% CAGR through 2031.

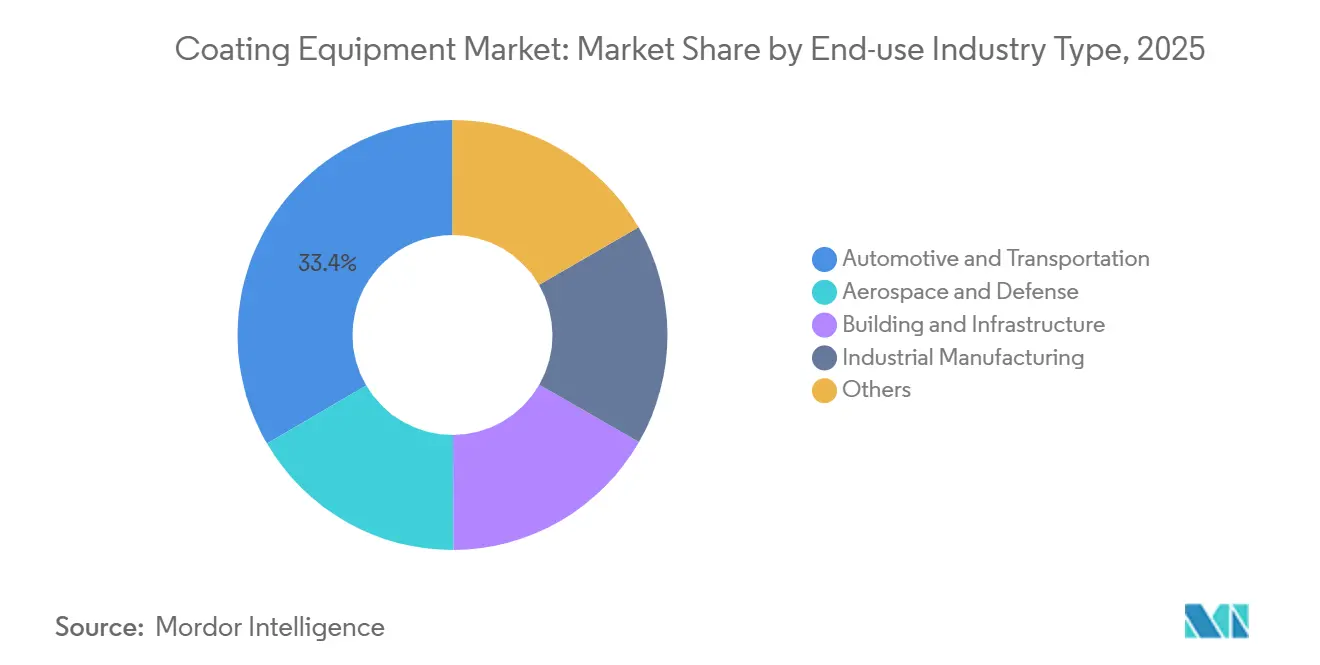

- By end-use industry, Automotive and Transportation held a 33.42% of the coating equipment market share in 2025 and is expected to be the fastest-growing segment with a 6.50% CAGR through 2031.

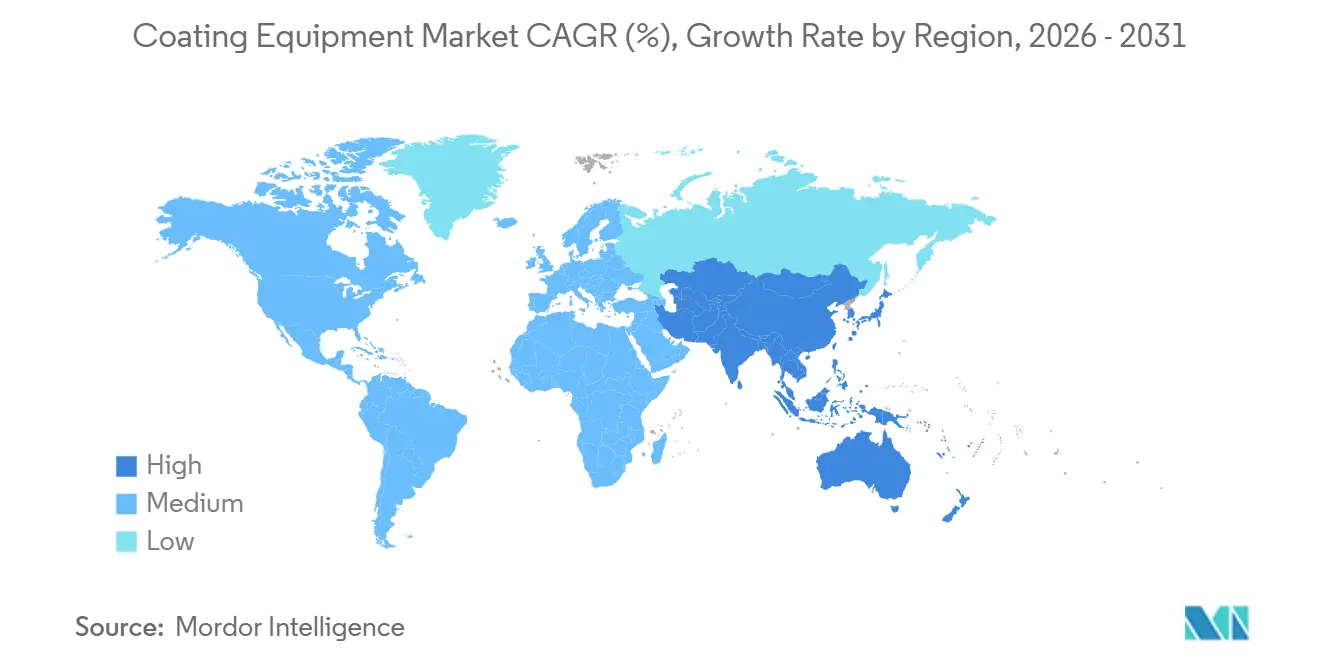

- By geography, Asia-Pacific accounted for 38.71% of the coating equipment market size in 2025 and is projected to record the highest regional CAGR of 6.35% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coating Equipment Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electric Vehicle (EV) and Automotive Coatings Demand | +1.9% | Global, with concentration in China, Germany, the United States, Mexico, and India | Short term (≤ 2 years) |

| Low-Volatile Organic Compound (VOC) Shift Toward Sustainable Coatings | +0.8% | Global, with regulatory acceleration in the EU, China, United States, and South Korea | Medium term (2-4 years) |

| Robotic and Smart-Factory Integration | +0.8% | Global, strongest in Germany, Japan, China, and South Korea | Medium term (2-4 years) |

| Infrastructure and Industrial Expansion | +0.7% | Asia-Pacific core, with spillover to the Middle East and South Asia | Medium term (2-4 years) |

| Paint-Shop Electrification | +0.6% | EU-led, expanding to North America and Gulf states | Medium term (2-4 years) |

| Hard-Chrome Replacement Regulations | +0.5% | EU and UK primary, with spillover to the United States and export-oriented markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV and Automotive Coatings Demand Reshapes Equipment Specifications

The ramp-up in EV production is changing the requirements for paint shops in the coating equipment market. Aluminum-heavy vehicle structures, battery enclosure protection needs, and the temperature sensitivity of high-voltage components are pushing automakers toward coating chemistries and application systems that differ from those used in internal combustion engine setups. New EV projects are generating equipment demand even when broader vehicle production cycles remain uneven. Dürr's January 2026 contract with CEER Motors for an advanced paint shop in King Abdullah Economic City shows that EV-led paint shop investment is expanding beyond traditional automotive manufacturing centers into newer locations[1]CEER Motors, “CEER and Dürr to Install One of the Most Advanced Paint Shops in the Automotive World,” CEER Motors, ceermotors.com. This shift is also widening demand beyond vehicle bodies, as battery-related coating steps and electrode processing are increasing the relevance of precision application systems in the coating equipment market.

Hard-Chrome Replacement Regulations Accelerate Specialty Equipment Demand

Regulatory pressure on hexavalent chromium is driving a substitution cycle in specialty systems within the coating equipment market. Aerospace, automotive, and industrial manufacturers that relied on hard chrome plating are being required to qualify alternatives such as physical vapor deposition (PVD), thermal spray, and related deposition methods. The resulting demand reflects a compliance-led shift toward higher-value systems rather than a standard volume upgrade cycle. Oerlikon has positioned non-hazardous PVD coatings as a viable alternative for aerospace applications facing tighter restrictions on hard-chrome processes. As export-oriented manufacturers align with European requirements, suppliers with installed capability in plasma spray, arc-PVD, and related processes are likely to capture a larger share of project qualification activity in the coating equipment market.

Robotic and Smart-Factory Integration Compresses Return-on-Investment Timelines

Automation is shifting from a premium feature to a standard requirement in the coating equipment market. Large OEM paint shops already rely on robotic application systems, but modular automation is becoming accessible to manufacturers that previously depended on manual spray setups. This broadens the addressable market for suppliers, as mid-sized users can now justify automated installations based on labor, consistency, and maintenance benefits. Dürr's May 2026 launch of the EcoRP4 painting robot, which features an arm geometry that improves access and reduces maintenance complexity, reflects this push toward broader deployment and more serviceable robot designs[2]Dürr AG, “EcoRP4 with Optimized Arm Geometry for All Painting Tasks,” Dürr, durr.com. As smart controls, process monitoring, and robot-compatible line architecture become more widespread, competition in the coating equipment market is shifting away from basic hardware and toward uptime, repeatability, and data-backed performance.

Low-VOC Shift Toward Sustainable Coatings Structurally Favors Powder and Electrostatic Systems

Volatile organic compound (VOC) regulations are steadily influencing equipment selection in the coating equipment market. As limits tighten, the economics of powder, electrostatic, and water-compatible systems improve because compliance is increasingly tied to line design rather than coating formulation alone. Powder systems continue to hold scale in the coating equipment market, particularly in applications where emission reduction and transfer efficiency carry direct operating value. The European Union reinforced this direction through its December 2025 decision to update the Ecolabel criteria for decorative paints, varnishes, and related products, which supports a preference for lower-emission application systems. Procurement is also moving toward systems that combine low emissions with reduced waste, supporting the long-term position of compliance-ready equipment suppliers in the coating equipment market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Retrofitting Costs | -0.8% | Global, most acute in emerging markets and small and medium-sized enterprise (SME)-heavy fabrication clusters in Southeast Asia, South Asia, and South America | Medium term (2-4 years) |

| Low-Cost Manual and Semi-Manual Alternatives | -0.5% | Developing economies in the Asia-Pacific, South America, and the Middle East and Africa | Short term (≤ 2 years) |

| Tariff and Localization Challenges | -0.6% | North America, Europe, and export-dependent markets in China and South Korea | Short term (≤ 2 years) |

| Qualification Bottlenecks | -0.3% | Aerospace and semiconductor end markets globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex and Retrofitting Costs Constrain Mid-Market Adoption

High upfront costs remain a significant barrier in the coating equipment market, particularly for small- and mid-sized manufacturers. A fully automated line requires investment in booths, conveyors, curing systems, controls, and compliance-related upgrades, and retrofit work often adds another layer of cost. This challenge is more pronounced when older facilities must be adapted for powder or waterborne processes, as those changes are harder to absorb in lower-volume production settings. This creates a divide in the coating equipment market, with larger OEMs and Tier-1 suppliers advancing compliance and automation programs, while smaller operators extend asset life and delay major upgrades. Newer service models and shared-use arrangements may ease this pressure over time, but the current capital expenditure hurdle continues to slow broader equipment replacement across the coating equipment market.

Tariffs and Localization Pressures Reshape Supply Chain Architecture

Trade and localization pressures are changing how projects are sourced in the coating equipment market. Customers are paying closer attention to local-content thresholds, lead times, and cost risks tied to imported machinery and parts. This is pushing suppliers to move beyond exports and toward regional assembly, service coverage, and local sourcing structures. Dürr's preliminary 2025 results pointed to a recovery in order intake, partly through localization-oriented painting technology projects in North America and Europe, indicating that local delivery capability is becoming a commercial advantage. The result is a supply chain model that is more complex and more capital-intensive, even when end-market demand in the coating equipment market remains stable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Powder Coating Holds Scale While Specialty Systems Lead Growth

Powder coating equipment held 43.63% of the coating equipment market share in 2025, maintaining its position across product categories. This reflects strong demand from automotive components, appliances, general metal fabrication, and architectural aluminum applications, where transfer efficiency and lower emission profiles are key considerations. The segment also benefits from a mature installed base, allowing vendors to grow through controls, software, and retrofit add-ons rather than relying solely on full-line replacements. Gema Switzerland's April 2026 launch of MagicControl MAX demonstrated how suppliers are improving automated powder lines through smarter control interfaces and tighter process visibility. Nordson's Encore HD dense-phase technology, with more than 1,000 installations globally, illustrates how performance gains in powder application continue to support productivity-driven replacement demand.

Specialty coating equipment is projected to expand at a 7.62% CAGR through 2031, making it the fastest-growing product segment. This category includes Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD), Atomic Layer Deposition (ALD), plasma spray, and thermal spray systems. Its growth is tied to semiconductor investment and hard-chrome substitution rather than mainstream vehicle production cycles. SEMI projected global semiconductor equipment sales of USD 125.5 billion in 2025 and USD 138.1 billion in 2026, supporting continued capital spending in deposition technologies. Liquid coating equipment remains relevant across mature applications but faces increasing pressure in areas where powder or specialty processes offer a clearer compliance or performance advantage.

By End-use Industry: Automotive Anchors Demand While Adjacent Industries Gain Momentum

Automotive and transportation accounted for 33.42% of the coating equipment market share in 2025 and is projected to grow at a 6.50% CAGR through 2031. This combination of scale and growth reflects concurrent investment in greenfield EV plants and upgrades to existing internal combustion engine paint shops. The coating equipment market is benefiting from two types of automotive spending simultaneously: one focused on building new production lines and another on modernizing existing assets. Dürr AG reported an 8.6% EBIT margin for its automotive division in 2025, with painting technology cited as a key earnings driver. BMW's Debrecen paint shop, the first in the group's network to operate without fossil fuels, demonstrated how future automotive facilities are combining surface-quality targets with energy-system redesign.

Aerospace and defense remains one of the most important adjacent segments in the coating equipment market, given high project values and long qualification cycles. Demand in this segment is driven by the transition away from hard-chrome processes toward PVD, thermal spray, and HVOF alternatives for critical components. Building and infrastructure provide steady demand for liquid and powder systems used on structural steel, aluminum extrusions, and prefabricated building components. Industrial manufacturing represents the broad volume base for mid-range powder and liquid equipment, while the others segment covers woodworking, electronics, and specialized applications with more fragmented purchasing patterns. This mix means the coating equipment market is not dependent on a single end-use cycle, even though automotive continues to anchor the largest project pipeline.

Geography Analysis

Asia-Pacific held a 38.71% share of the coating equipment market in 2025 and is projected to record the fastest regional CAGR of 6.35% through 2031. China remains the core demand center, combining large automotive output, ongoing EV capacity additions, and stricter environmental requirements around coating operations. This mix drives both volume demand and faster adoption of newer line configurations, while also supporting local supplier development, which is changing procurement behavior for domestic and export-focused manufacturers. India is gaining relevance as upstream coatings capacity expands and manufacturing investment creates a broader base for demand for application equipment.

North America and Europe together remain major sources of demand in the coating equipment market, driven by regulatory retrofits, EV facility investment, and higher-value aerospace programs. In North America, EV manufacturing buildouts in the United States and Mexico are increasing interest in automated and lower-emission paint shop systems. Dürr completed a turnkey CO2-efficient paint shop for Volkswagen's Puebla site in Mexico, combining electric drying and driverless transport systems within its Paint Shop of the Future approach. Europe's demand outlook is tied to decarbonization regulations, low-emission coating preferences, and continued hard-chrome substitution pressure. The EU's December 2025 Ecolabel update reinforced support for lower-emission coating pathways, while Germany remains the region's main center for automotive OEM production and coating equipment manufacturing.

South America and the Middle East and Africa remain smaller markets, but investment tends to be concentrated in specific industrial clusters. Brazil and Argentina support demand through automotive manufacturing and packaging-related coating applications. In the Middle East, CEER Motors' January 2026 agreement with Dürr for a Paint Shop of the Future in Saudi Arabia marked a step in regional development of local EV manufacturing capability. South Africa remains the main entry point in Sub-Saharan Africa, although infrastructure gaps and currency pressures continue to limit broader adoption across the wider region.

Competitive Landscape

The coating equipment market is fragmented across regional and mid-range categories. Dürr AG, Nordson Corporation, and Graco Inc. hold strong positions in segments where customers require full-system integration, high-throughput performance, and reliable service coverage. This gives larger players an advantage in OEM and industrial programs, where qualification cycles are long and switching costs are high. Dürr reported painting technology EBIT margins of 8.6% in 2025, up from 8.4% in 2024, and its 2026 order intake guidance reflected confidence in the recovery of the automotive market. However, the market still has room for specialized suppliers, as not every customer requires a full paint shop platform.

A competitive opportunity exists where collaborative robotics intersects with high-mix production. Mid-sized manufacturers seek automation that is easier to deploy and maintain, and less capital-intensive than full OEM-style installations. ANEST IWATA's 2026 exclusive European partnership with Asahi Sunac demonstrated how mid-tier firms are expanding access to electrostatic technology through alliances rather than lengthy internal development cycles. Carlisle Fluid Technologies' acquisition of Reinhardt Technik added sealants and adhesives capabilities, strengthening cross-selling potential in automotive sealing and bonding workflows. Graco's March 2026 launch of a wirelessly connected and automated fluid management system indicated that data-enabled control is becoming a stronger point of differentiation.

Specialists remain relevant as the market is increasingly defined by process quality, uptime, and application-specific expertise. Gema Switzerland is reinforcing its powder coating position through more automated platforms and expanded testing capabilities, supporting deeper customer integration at the line level. Oerlikon remains well positioned in specialty applications linked to aerospace substitution needs, where technical qualification is more important than broad installed volume. Overall, the market is likely to remain competitive on the basis of product depth, localization capabilities, digital controls, and service reach rather than price alone.

Coating Equipment Industry Leaders

Nordson Corporation

Graco Inc.

Dürr AG

ANEST IWATA Corporation

J. Wagner GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Dürr announced a turnkey paint shop contract with Volkswagen Autoeuropa for its Palmela, Portugal facility. The project integrates the EcoSmartCure oven for targeted, demand-based drying and DXQcontrol software, unifying three separate paint shops under one control environment. Completion is targeted by mid-2027. This project extends Dürr's European CO2-reduction paint shop reference portfolio following the Puebla inauguration, indicating Volkswagen Group's focus on electrified drying standards across its global manufacturing footprint.

- April 2026: Gema Switzerland GmbH launched MagicControl MAX (CM50) at PaintExpo 2026, a new-generation control platform for fully automated powder coating systems. The platform features intelligent networking, high-speed processing, and advanced process transparency. The launch follows Gema's relocation to a new 20,000-square-meter headquarters in Gossau, Switzerland, which expanded production capacity and introduced four advanced coating test lines in its customer application laboratory.

Global Coating Equipment Market Report Scope

Coating equipment refers to the machinery and tools used to apply a uniform layer of liquid, powder, or film onto a substrate. These systems incorporate spray nozzles, coating pans, and drying units to enhance, protect, or modify the properties of substrates, such as automotive parts, pharmaceutical tablets, and electronic components.

The coating equipment market is segmented by product type, end-use Industry, and geography. By product type, the market is segmented into Specialty Coating Equipment, Powder Coating Equipment, and Liquid Coating Equipment. By end-use Industry, the market is segmented into automotive and transportation, aerospace and defense, building and infrastructure, industrial manufacturing, and others. The report also covers market size and forecasts for coating equipment market across 18 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Specialty Coating Equipment | Physical Vapor Deposition Equipment |

| Chemical Vapor Deposition Equipment | |

| Thermal Spray Equipment | |

| Plasma Spray Equipment | |

| Atomic Layer Deposition and Other Specialty Systems | |

| Powder Coating Equipment | Powder Spray Guns and Applicators |

| Powder Booths and Recovery Systems | |

| Powder Feed Centers and Hoppers | |

| Conveyors and Material Handling Systems | |

| Curing Ovens and Complete Powder Lines | |

| Liquid Coating Equipment | Air Spray Systems |

| Airless Systems | |

| Air-Assisted Airless Systems | |

| Electrostatic Liquid Systems | |

| Dip, Flow, Curtain, and Roll Coating Systems |

| Automotive and Transportation |

| Aerospace and Defense |

| Building and Infrastructure |

| Industrial Manufacturing |

| Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Specialty Coating Equipment | Physical Vapor Deposition Equipment |

| Chemical Vapor Deposition Equipment | ||

| Thermal Spray Equipment | ||

| Plasma Spray Equipment | ||

| Atomic Layer Deposition and Other Specialty Systems | ||

| Powder Coating Equipment | Powder Spray Guns and Applicators | |

| Powder Booths and Recovery Systems | ||

| Powder Feed Centers and Hoppers | ||

| Conveyors and Material Handling Systems | ||

| Curing Ovens and Complete Powder Lines | ||

| Liquid Coating Equipment | Air Spray Systems | |

| Airless Systems | ||

| Air-Assisted Airless Systems | ||

| Electrostatic Liquid Systems | ||

| Dip, Flow, Curtain, and Roll Coating Systems | ||

| By End-use Industry | Automotive and Transportation | |

| Aerospace and Defense | ||

| Building and Infrastructure | ||

| Industrial Manufacturing | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is current market size of Coating Equipment Market?

The Coating Equipment Market size is projected to expand from USD 23.20 billion in 2025 and USD 24.39 billion in 2026 to USD 32.46 billion by 2031, and is expected to register a CAGR of 5.88% between 2026 to 2031.

Which product category leads to current revenue?

Powder Coating Equipment led in 2025 with 43.63% share, supported by broad use in automotive components, appliances, and metal fabrication.

Which product segment is growing the fastest through 2031?

Specialty Coating Equipment is projected to record the highest growth at 7.62% CAGR, supported by semiconductor deposition demand and hard-chrome replacement needs.

Why is automotive demand so important for suppliers?

Automotive and Transportation held a 33.42% share in 2025 and is also the fastest-growing end-use segment, with a 6.50% CAGR, driven by EV paint shop builds and retrofit programs.

Page last updated on: