High Strength Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

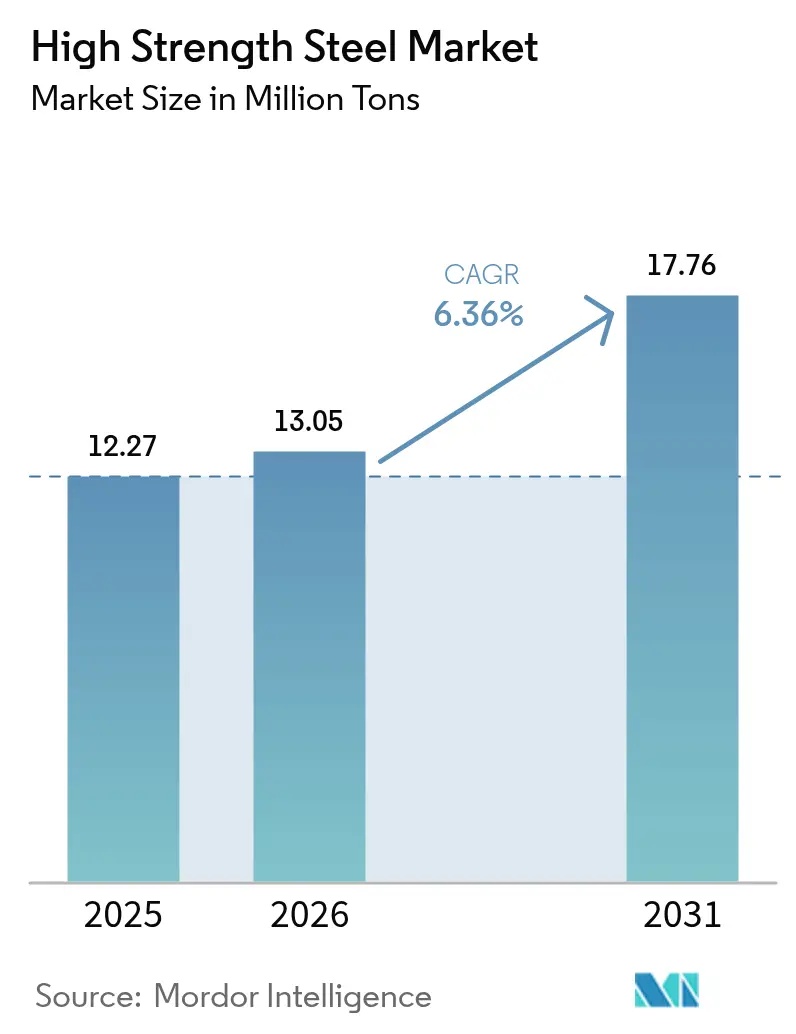

| Market Volume (2026) | 13.05 Million tons |

| Market Volume (2031) | 17.76 Million tons |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Strength Steel Market Analysis by Mordor Intelligence

The High Strength Steel Market size is expected to grow from 12.27 Million tons in 2025 to 13.05 Million tons in 2026 and is forecast to reach 17.76 Million tons by 2031 at 6.36% CAGR over 2026-2031. Automotive lightweighting mandates, modular high-rise construction, and offshore-wind tower build-outs are translating directly into larger order books for grades that couple tensile strengths above 600 MPa with high crash energy absorption. Dual-phase steel commands price premiums because its ferrite-martensite matrix preserves elongation during complex forming, a property automakers exploit for door inners and wheel-housing stampings. Hot-formed steel is scaling quickly in battery-electric chassis frames that must withstand side-impact tests while shielding lithium-ion modules from thermal runaway. At the same time, micro-alloyed ferritic-bainitic plate has emerged as the material of choice for hydrogen-ready pipelines, signalling a future growth node once large-diameter trunk lines move from pilot to commercial scale.

Key Report Takeaways

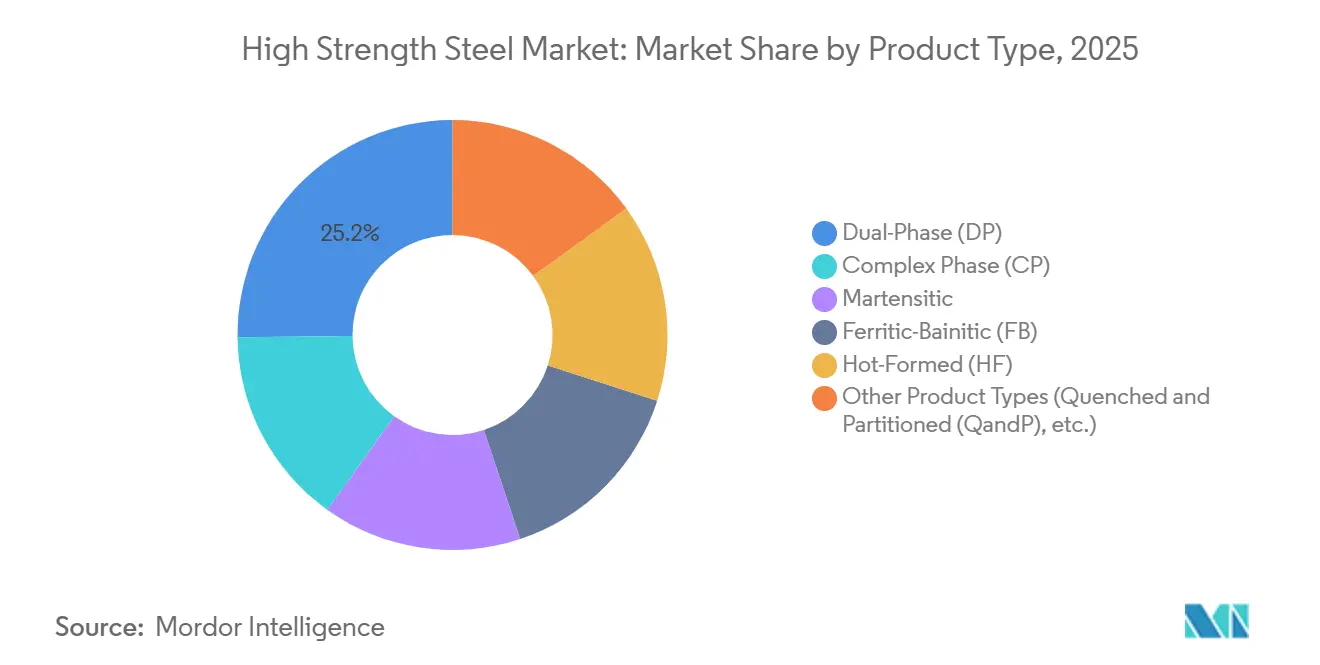

- By product type, dual-phase (DP) held 25.16% of the high strength steel market share in 2025 and is projected to grow at a 6.72% CAGR through 2031.

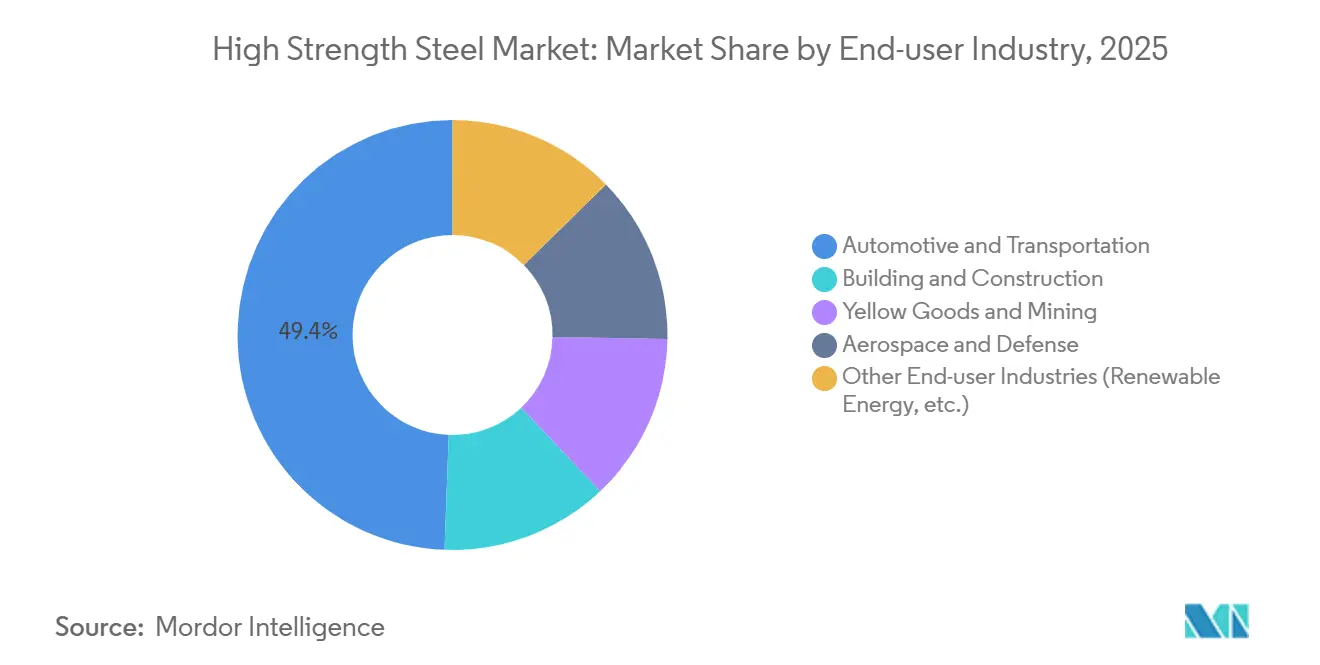

- By end-user industry, automotive and transportation led with 49.40% share of the high strength steel market size in 2025, while other end-user industries that include renewable energy are advancing at a 6.85% CAGR to 2031.

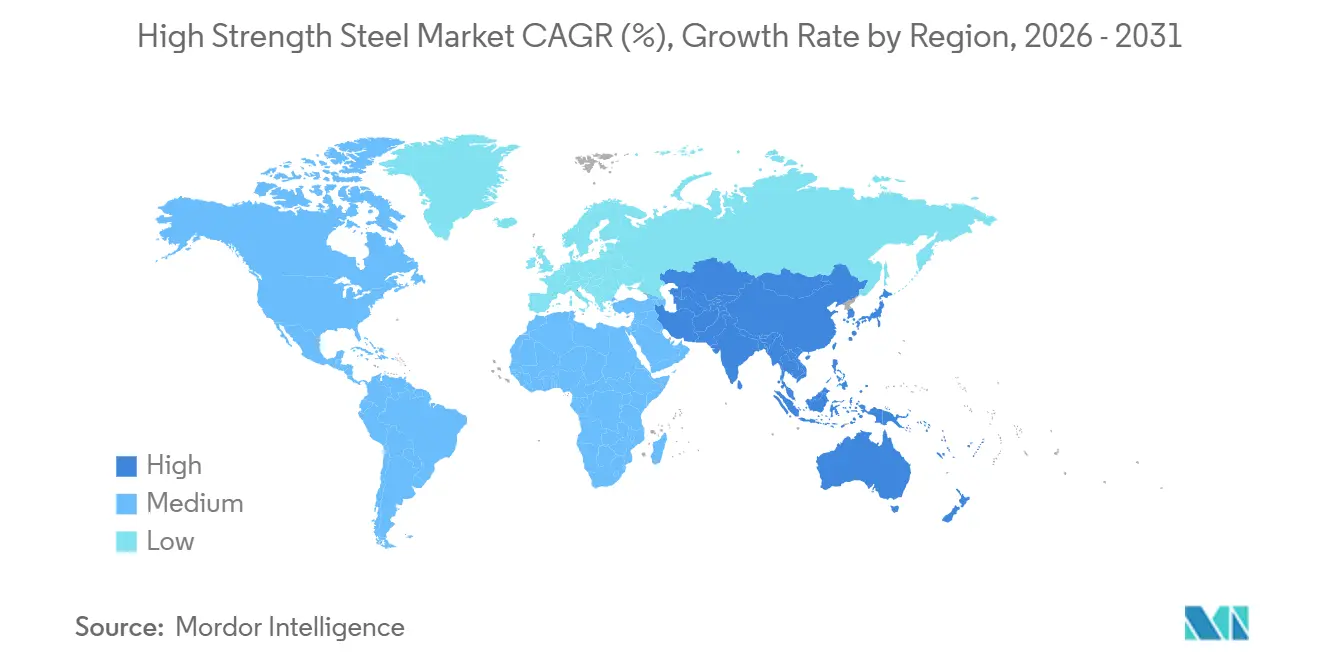

- By geography, Asia-Pacific accounted for 63.69% volume in 2025 and is forecast to expand at a 6.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Strength Steel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting and crash-safety mandates | +1.8% | Global, with peak adoption in EU, North America, and China | Medium term (2-4 years) |

| Rapid growth of modular high-rise construction | +1.3% | APAC core (China, India, ASEAN), spill-over to Middle-East | Medium term (2-4 years) |

| Offshore-wind tower build-out accelerates demand | +1.1% | North America and EU, emerging in APAC (Taiwan, South Korea) | Long term (≥ 4 years) |

| Hydrogen-ready pipeline specifications for micro-alloyed HSS | +0.6% | North America, EU, Australia | Long term (≥ 4 years) |

| Battery-electric skateboard chassis adoption | +1.2% | Global, led by China, EU, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automotive Lightweighting and Crash-Safety Mandates

Fleet CO₂ caps of 95 g/km in the European Union and a 54.5 miles-per-gallon target in the United States oblige automakers to swap mild steel for grades that remove 20-30% body-in-white mass while passing ever tougher small-overlap and side-impact tests. Updates to the Insurance Institute for Highway Safety protocol raised the bar for occupant survival space, which in turn lifted demand for 1,500 MPa B-pillars formed by hot stamping. General Motors reports that Ultium-based trucks now use dual-phase 980 MPa sheet in cab structures, trimming 180 kg from curb weight and raising torsional rigidity 15%. China’s GB 38900-2020 test regimen couples side-pole impacts with roof-crush metrics, a combination that rewards martensitic and complex-phase steels in A- and B-pillar designs[1]Ministry of Industry and Information Technology, “GB 38900-2020,” miit.gov.cn . Ford confirms that press-hardened steel battery enclosures satisfy Federal Motor Vehicle Safety Standard 305 without adding aluminum extrusions, simplifying under-body assembly.

Rapid Growth of Modular High-Rise Construction

Prefabricated steel modules allow contractors to cut inner-city build schedules by 30% because columns of S460-S690 grade carry identical loads at thinner wall thicknesses, freeing rentable floor space. Singapore’s Building and Construction Authority states that modular starts rose to 22% of residential projects in 2025, and most developers specify high strength hollow sections to comply with productivity metrics. Baosteel supplied 85,000 tons of Q460/Q550 plate for Shenzhen towers that shaved six months off traditional timelines. The 2024 International Building Code permits higher stress limits for ASTM A913 Grade 65 in seismic zones, widening usage in California and Japan. Tata Steel’s S700MC launch in 2024 targets Scandinavian modular firms that require weldable sections with Charpy toughness below –40 °C.

Offshore-Wind Tower Build-Out Accelerates Demand

More than 120 GW of offshore-wind capacity was under construction or late-stage permitting at end-2025, and hub heights above 150 m are driving a switch from S355 to S420-S460 for lower tower sections to curb wall thickness and logistics cost. Ørsted specified S460ML for the 704 MW Revolution Wind project where monopiles weigh 2,200 tons each. The U.S. Gulf of Mexico lease sale added 3.7 GW potential and an estimated 450,000 tons of plate demand this decade. Thyssenkrupp Steel qualified S500 plate with enhanced through-thickness ductility for floating foundations that experience multi-directional fatigue. Rotor diameters that exceed 240 m expose tower bases to amplified bending moments, reinforcing demand for micro-alloyed grades with guaranteed low-temperature toughness.

Hydrogen-Ready Pipeline Specifications for Micro-Alloyed HSS

API 5L X70HIC published in 2024 caps sulfur below 0.002% and calls for calcium-treated inclusions to cut hydrogen traps, a milestone that lifted procurement of ferritic-bainitic micro-alloyed coil. Germany’s 5,900 km hydrogen core network will require X80 pipelines that show a hydrogen embrittlement index below 0.15 in slow-strain-rate tests. POSCO demonstrated a 690 MPa plate passing NACE TM0284 at 10 bar hydrogen pressure, aligning with South Korea’s energy roadmap. The U.S. Department of Energy’s Hydrogen Shot aims for USD 1 per kg hydrogen by 2030 and expects incremental annual steel demand of 120,000-150,000 tons for new pipelines. Australian operators have launched design studies for 1,500 km of blend-ready transmission lines, embedding an early export market for API X70HIC plate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and alloying-element cost inflation | -0.9% | Global, acute in regions dependent on nickel and chromium imports | Short term (≤ 2 years) |

| Raw-material price volatility (iron ore, alloys) | -0.7% | Global, with pronounced effects in Asia-Pacific and Europe | Medium term (2-4 years) |

| Joining and welding challenges for high-strength grades | -0.5% | Global, particularly in automotive and construction sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production and Alloying-Element Cost Inflation

Nickel averaged USD 18,500 per ton in 2025, 22% above 2024, after Indonesia tightened matte exports and battery demand surged. Chromium spot prices rose to USD 11,200 per ton when South African labor strikes disrupted supply, lifting stainless and high strength production costs 10-15%. Molybdenum reached USD 45 per kg as Chilean mines curtailed output amid water scarcity. ArcelorMittal disclosed a 180-basis-point margin squeeze in its automotive steel business due to alloy inflation, prompting quarterly price renegotiations with automakers. Southeast Asian mini-mills have postponed martensitic line start-ups until alloy markets stabilize, delaying incremental volume.

Joining and Welding Challenges for High-Strength Grades

Resistance spot welding of more than 1,000 MPa sheet demands heat input below 1.0 kJ/mm and post-weld tempering near 230 °C; deviations induce brittle martensite in heat-affected zones and delayed cracking. Laser-arc hybrid welding yields joints that retain 95% base-metal strength but equipment capital exceeds USD 500,000 per station, limiting adoption. Nippon Steel tests reveal conventional spot welds on 1,500 MPa sheet lose 25% joint strength, whereas laser seams meet design loads at the cost of 40% slower throughput. Adhesive bonding spreads stress but requires surface prep and cure cycles incompatible with high-volume stamping lines. A new International Institute of Welding task force is drafting friction-stir protocols that may unlock continuous joining of ultra-high-strength grades without melting, though commercialization remains three years away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dual-Phase Dominance Anchors Volume Growth

Dual-phase (DP) captured a 25.16% share of the high strength steel market size in 2025 and is forecast to advance at a 6.72% CAGR through 2031, benefiting from an attractive mix of formability and 600-1,200 MPa tensile strength that meets most crash-safety targets. Volkswagen’s MEB platform uses DP 980 in side sills and rear floor cross-members, trimming vehicle mass 12% while satisfying latest Euro NCAP side-impact norms.

Martensitic and hot-formed grades above 1,200 MPa are expanding in door-intrusion beams and battery enclosures but incur higher processing costs and limited formability, issues mitigated by localized laser trimming. Complex-phase sheet with superior hole-expansion ratio wins suspension arms that experience multi-axial loads, while ferritic-bainitic plate secures chassis rails in heavy trucks that prioritize weldability. Quenched-and-partitioned steel remains pilot scale, yet its 2,000 MPa tensile strength plus 10% elongation profile signals future penetration in one-piece door rings once scaling challenges resolve.

By End-user Industry: Automotive Leads, Renewables Surge

Automotive and transportation accounted for 49.40% of high strength steel market share in 2025, because electric vehicles embed 15-20% more advanced grades to safeguard large battery packs and compensate for engine block removal. General Motors confirmed 420 kg of advanced high strength steel per Ultium SUV, up from 310 kg on similar gasoline models, enabling a 400 km driving range under U.S. test cycles.

Building and construction uses hollow sections above 460 MPa yield to shrink column footprints, and mining equipment requires 400-500 HBW plate to extend bucket life in abrasive conditions. Aerospace and defense turn to more than 1,800 MPa bar for landing gear and armored hulls where performance outweighs cost. Other end-user industries, including renewable energy, such as offshore-wind towers and hydrogen pipelines, are projected to grow 6.85% annually, making them the fastest rising consumer group as developers mandate fatigue and embrittlement resistance far above conventional S355 benchmarks.

Geography Analysis

Asia-Pacific dominated the high strength steel market with 63.69% volume in 2025; rising battery-electric output and infrastructure spending will sustain a 6.81% CAGR to 2031. China built 9.4 million plug-in vehicles in 2025 and enforces GB 38900-2020 test norms that steer automakers toward dual-phase and hot-formed solutions. India’s Bharatmala Phase II adds 12,000 km of highways. Japan and South Korea are introducing 1,800 MPa press-hardened door rings that cut mass by 20% in hybrid sedans, while ASEAN governments court Chinese and Japanese carmakers, pushing regional coil centers to commission continuous-annealing lines.

In North America, the U.S. Inflation Reduction Act incentivizes domestic sourcing, prompting Nucor and Cleveland-Cliffs to add continuous-annealing capacity to supply skateboard chassis blanks[2]U.S. Department of the Treasury, “Inflation Reduction Act Guidance,” treasury.gov . Canada committed CAD 13 billion (USD 9.6 billion) to battery manufacturing that will absorb a large amount of high strength beams and plates during plant builds. Mexico produced 3.8 million vehicles in 2025, with per-unit advanced steel content up to 280 kg as cross-border supply chains pivot to electric pickups.

In Europe, Carbon Border Adjustment fees accelerate the switch to scrap-based electric-arc furnaces for lower embedded emissions, a value proposition German automakers embrace to meet scope-3 targets. Offshore-wind capacity in the United Kingdom reached 16 GW, consuming S460/S500 monopile plate, while France adopted S690 for nuclear containment shells, opening a high-grade opportunity in reactor builds. South America and the Middle-East and Africa clock smaller volumes yet post double-digit growth, anchored by Brazilian mining trucks and Saudi Arabian hydrogen pipelines.

Competitive Landscape

The high strength steel market is moderately concentrated: the top five producers hold roughly 37% capacity but face regional erosion as mini-mills co-locate near assembly hubs and promise shorter lead times. ArcelorMittal’s new dual-phase patent blends niobium and titanium to reach 1,200 MPa tensile and 22% elongation, enabling single-piece door rings without inter-anneal, a step that trims energy use 12% versus multi-step stamping. Nucor and Steel Dynamics exploit electric-arc furnace routes with 45% lower carbon intensity, a differentiator for automakers chasing net-zero goals. POSCO’s PosMAC coating supplies battery enclosures with tenfold corrosion resistance, meeting the 15-year durability benchmarks demanded for electric platforms

Strategic moves center on alloying-element security; Nippon Steel bought 30% of a lithium-ion recycling plant to back-integrate nickel and cobalt streams, cutting cost volatility 5-7%. Capacity expansions track electric-vehicle hot spots: ArcelorMittal Gent adds 200,000 tons hot-stamping line, Cleveland-Cliffs upgrades Butler to supply 150,000 tons skateboard coil, and Tata Steel Europe ramps S700MC sections for U.K. modular towers. White-space opportunities include hydrogen pipeline plate and quenched-and-partitioned sheet that match hot-formed strength without the energy-intensive furnace step. Digital twins now optimize cooling curves and predict tensile properties within ±20 MPa, raising line yield and reinforcing margin defense.

High Strength Steel Industry Leaders

ArcelorMittal

NIPPON STEEL CORPORATION

POSCO

China Baowu Steel Group Corp., Ltd.

SSAB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AM/NS India commissioned a Continuous Galvanising Line (CGL), the first in India designed to produce high strength steel for the automotive industry. The facility was engineered to manufacture specialized, high-grade steel with strength levels up to 1180 MPa, aiming to replace imports.

- July 2025: thyssenkrupp Steel Europe invested over EUR 800 million to upgrade its production facilities in Duisburg, Germany. The modernization aimed to produce high strength steel to meet the increasing demand in the European market and included replacing outdated equipment with new casting-rolling lines to improve efficiency and support the automotive industry.

Global High Strength Steel Market Report Scope

High strength steel is a new generation with exceptional strength and flexibility. Unlike conventional carbon steel, this steel is more resistant to corrosion and other chemicals. High strength steel is typically alloyed with copper, vanadium, and titanium to increase strength. It is widely used in automobile applications due to their diverse range of properties, including lightweight characteristics and other mechanical advantages such as improved weldability, high toughness, and excellent formability.

The high strength steel market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into dual-phase (DP), complex phase (CP), martensitic, ferritic-bainitic (FB), hot-formed (HF), and other product types (e.g., quenched and partitioned (Q&P)). By end-user industry, the market is segmented into automotive and transportation, building and construction, yellow goods and mining, aerospace and defense, and other end-user industries (e.g., renewable energy). The report also covers the market size and forecasts for high strength steel in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Dual-Phase (DP) |

| Complex Phase (CP) |

| Martensitic |

| Ferritic-Bainitic (FB) |

| Hot-Formed (HF) |

| Other Product Types (Quenched and Partitioned (QandP), etc.) |

| Automotive and Transportation |

| Building and Construction |

| Yellow Goods and Mining |

| Aerospace and Defense |

| Other End-user Industries (Renewable Energy, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacifc | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Middle-East and Africa |

| By Product Type | Dual-Phase (DP) | |

| Complex Phase (CP) | ||

| Martensitic | ||

| Ferritic-Bainitic (FB) | ||

| Hot-Formed (HF) | ||

| Other Product Types (Quenched and Partitioned (QandP), etc.) | ||

| By End-user Industry | Automotive and Transportation | |

| Building and Construction | ||

| Yellow Goods and Mining | ||

| Aerospace and Defense | ||

| Other End-user Industries (Renewable Energy, etc.) | ||

| By Geography (Volume) | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacifc | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the high strength steel market?

The high strength steel market size stands at 13.05 million tons in 2026 and is forecast to reach 17.76 million tons by 2031, reflecting a 6.36% CAGR over 2026-2031.

Which product type leads demand today?

Dual-phase steel leads with 25.16% share in 2025 due to its balance of formability and 600-1,200 MPa strength.

How dominant is automotive demand for high strength grades?

Automotive and transportation absorbed 49.40% of 2025 as electric vehicles expand.

Why is Asia-Pacific critical for suppliers?

Asia-Pacific holds 63.69% volume and is growing at 6.81% annually because China and India are scaling electric-vehicle and infrastructure programs.

Page last updated on: