Special Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

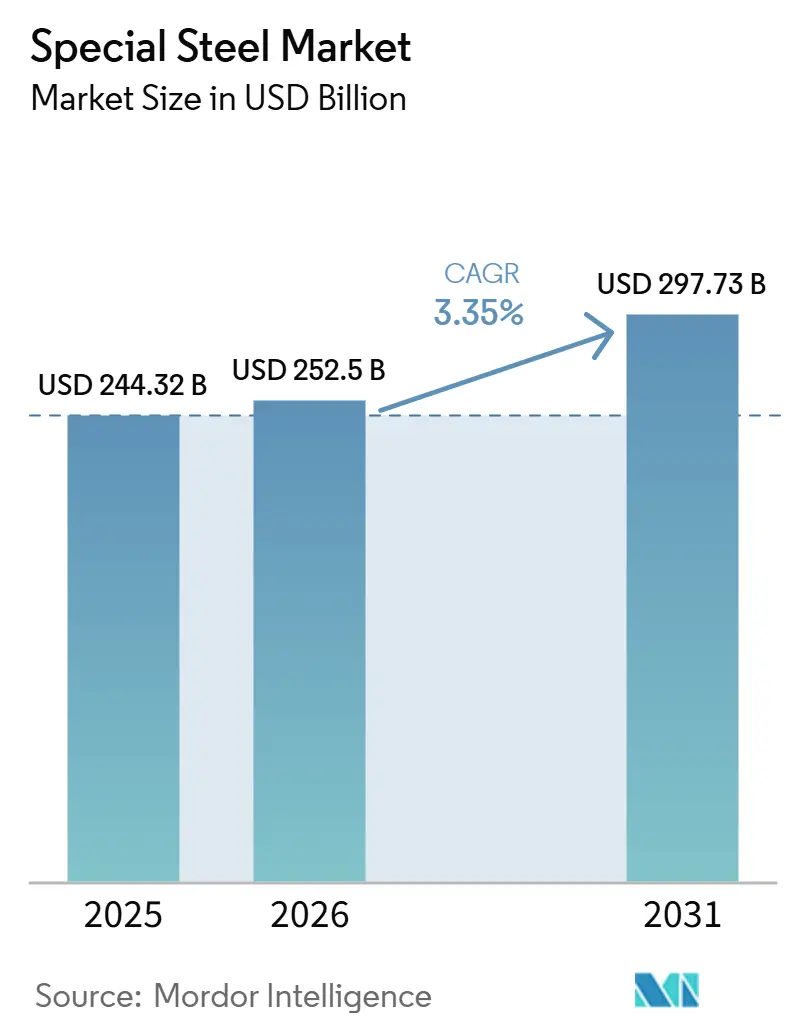

| Market Size (2026) | USD 252.5 Billion |

| Market Size (2031) | USD 297.73 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Special Steel Market Analysis by Mordor Intelligence

The Special Steel Market size is expected to grow from USD 244.32 billion in 2025 to USD 252.5 billion in 2026 and is forecast to reach USD 297.73 billion by 2031 at 3.35% CAGR over 2026-2031. Stainless grades, hydrogen-ready alloy development, and offshore-wind tower demand anchor this growth trajectory. Accelerated adoption of electric-arc-furnace (EAF) and hydrogen-direct-reduced-iron (H₂-DRI) routes is lowering carbon footprints and rewriting cost curves, while policy-backed infrastructure programs across India and ASEAN amplify base-metal volumes. Raw-material volatility in nickel and chromium continues to pressure producer margins, yet mills with captive feedstocks or integrated ferrochrome capacity defend profitability. The competitive landscape is shifting toward joint ventures that spread decarbonization capex, most notably JSW-JFE and POSCO-Nippon Steel tie-ups, even as mini-mills expand low-carbon sheet capacity for automotive and renewable-energy customers.

Key Report Takeaways

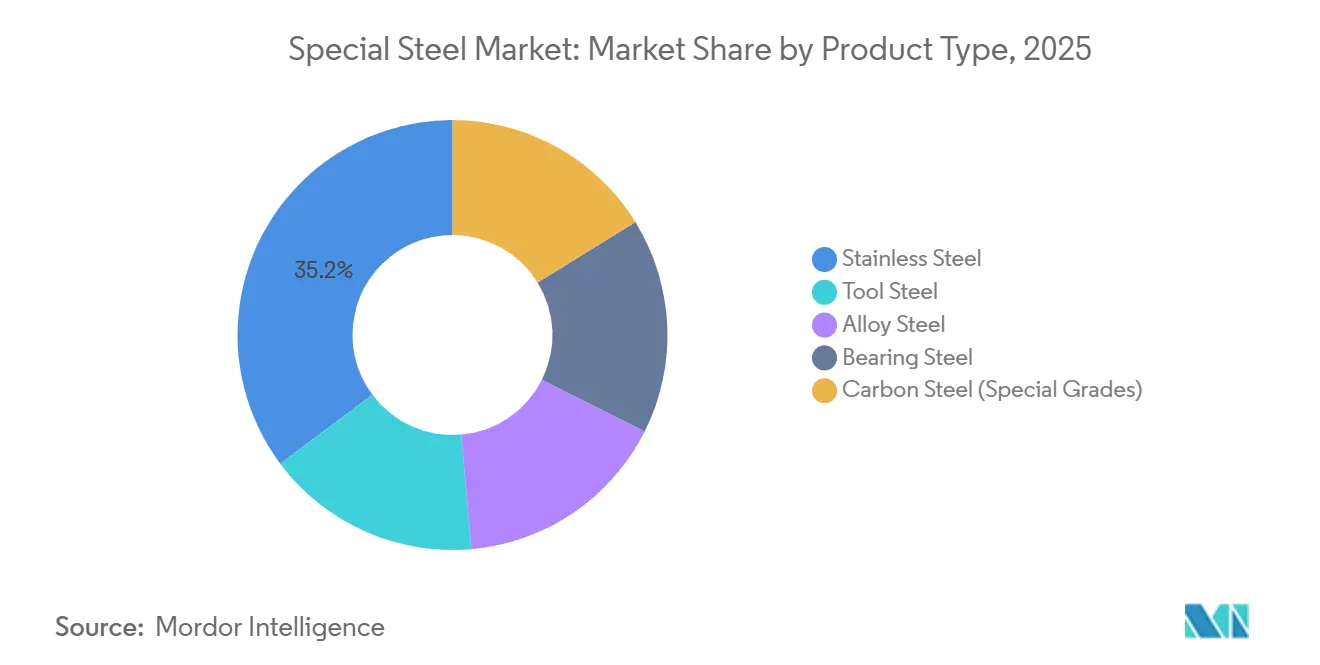

- By product type, stainless steel led with a 35.22% revenue share in 2025, and its segment is projected to advance at a 3.67% CAGR through 2031.

- By form, sheets and plates accounted for a 40.56% share of the special steel market size in 2025 and are set to register a 3.51% CAGR through 2031.

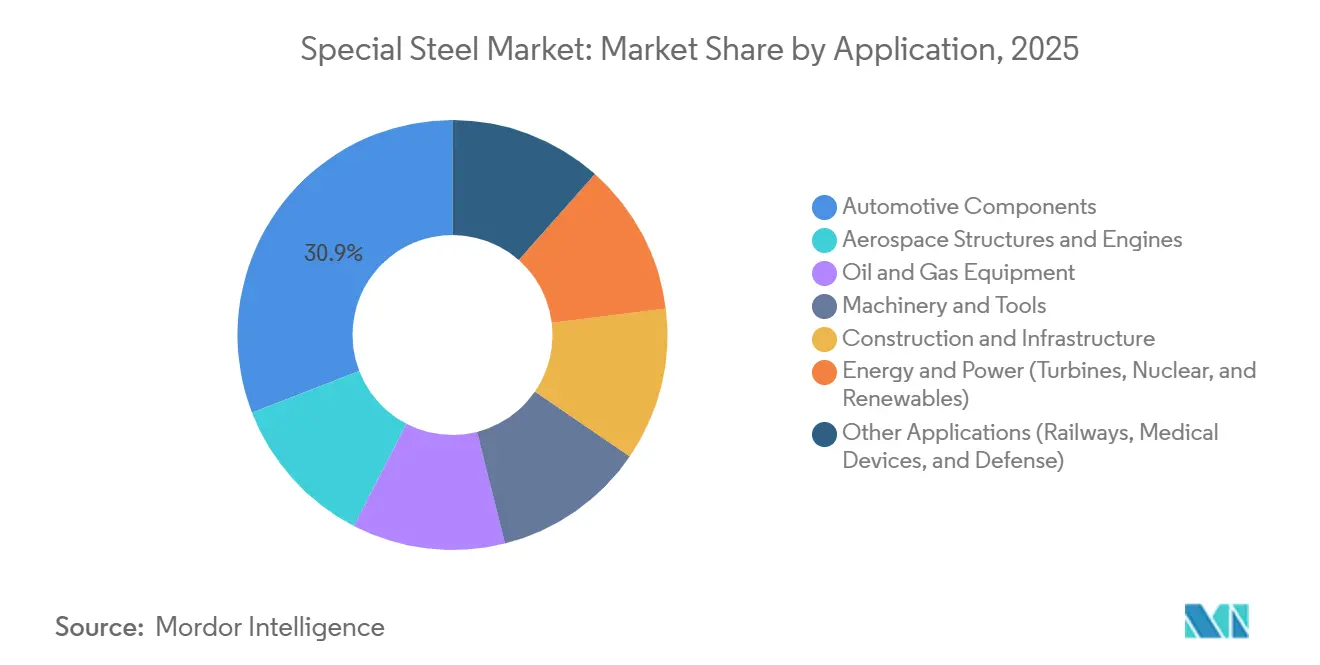

- By application, automotive components captured 30.88% of the special steel market share in 2025, while the energy and power segment exhibits the highest 4.65% CAGR through 2031.

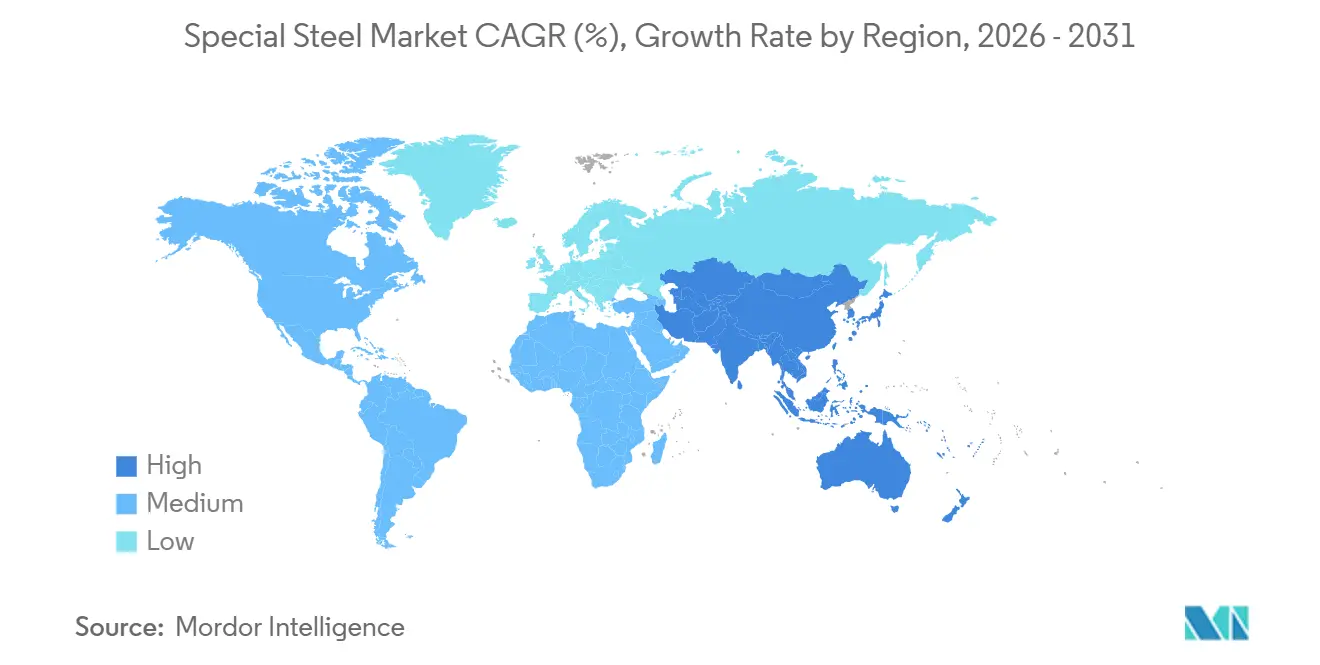

- By geography, Asia-Pacific led with a 43.35% revenue share in 2025, and its segment is projected to advance at a 3.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Special Steel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization-driven switch to EAF and H₂-DRI routes | +0.8% | EU, North America, Asia-Pacific | Medium term (2-4 years) |

| Expansion of renewable-energy hardware | +0.9% | North America, EU, coastal Asia-Pacific | Medium term (2-4 years) |

| Digitally enabled alloy-design platforms shortening grade-development cycles | +0.3% | Global R&D hubs | Short term (≤ 2 years) |

| Infrastructure stimulus in emerging economies | +0.7% | Asia-Pacific, South America, Middle East | Long term (≥ 4 years) |

| Surge in green-hydrogen-ready steels | +0.5% | EU, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Decarbonization Driven Switch To EAF And H₂-DRI Routes

EAF and H₂-DRI projects trim as much as 70% of site-level CO₂ emissions compared with blast furnaces. SSAB expects fossil-free output from Oxelösund by 2026, while H₂ Green Steel targets 5 million tons of green steel in Sweden by 2030[1]World Nuclear News, “Global Steelmakers Fast-Track Hydrogen-DRI Projects,” worldnuclearnews.com. Capital intensity remains high at USD 1,200-1,500 per tonne of annual capacity, yet European Union (EU) carbon prices above EUR 90 per ton are accelerating payback periods. North American conversions, such as Algoma Steel’s CAD 700 million program, align with automaker low-carbon sourcing mandates. Execution risk persists when hydrogen supply and renewable power lag project timelines, evidenced by Thyssenkrupp’s delayed Duisburg transition.

Expansion Of Renewable-Energy Hardware

Offshore-wind, electrolyzer, and hydrogen-pipeline projects are widening end-use diversity for special steel market grades. The United States earmarked USD 42 billion for offshore-wind infrastructure, aiming for 30 GW by 2030, equating to 1.5-2.0 million tons of plate demand per year. EU’s REPowerEU targets 300 GW of offshore wind by 2050, pulling 15-20 million tons of monopile and tower steel. Electrolyzer installations could reach 8 GW in 2026, with each gigawatt consuming around 4,000 tons of specialty stainless. API 5L X70/X80 pipe grades dominate hydrogen-transmission frameworks, and the European Hydrogen Backbone foresees 81,000 km of infrastructure by 2040.

Digitally Enabled Alloy-Design Platforms Shortening Grade-Development Cycles

Platforms such as DENS integrate CALPHAD with machine learning to model microstructure evolution, cutting qualification times below 12 months. Rosatom’s BR-1200 alloy development showcases 600°C stability within a year of computational screening, while additive tooling grades H13 and D2 now reach wrought-equivalent hardness with 80% less waste. Faster cycles allow mills to tailor chemistries for electrolyzer and offshore specifications, securing price premiums and first-mover certification.

Infrastructure Stimulus In Emerging Economies

India’s 2024-25 Union Budget raised infrastructure outlays to INR 11.11 lakh crore (USD 133 billion), pushing finished-steel consumption to 136.09 million tons in FY25. Production-linked incentives foster import substitution in automotive and defense grades, while ASEAN pipeline and rail expansions improve regional demand visibility. Brazilian anti-dumping measures aim to protect margins, though capex is tapering as Gerdau prioritizes free cash flow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-intensive processes and tightening carbon-pricing regimes | -0.6% | EU, North America, China | Short term (≤ 2 years) |

| Competition from additive-manufactured lightweight metals | -0.4% | North America, EU, Japan | Medium term (2-4 years) |

| Supply-chain volatility in critical minerals | -0.5% | Global, high Asia-Pacific exposure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-Intensive Processes and Carbon Pricing

Blast-furnace steelmaking consumes 18-22 gigajoules per tonne of crude steel, and carbon-pricing mechanisms are escalating operating costs faster than mills can pass through to customers. European Union (EU) allowance prices over EUR 90 (USD 103) add around EUR 18-20 (USD 20-23) per tonne to integrated costs, while CBAM removes the low-cost import avenue by 2026. China’s expanding carbon market and India’s fear of border adjustments are pushing domestic producers toward EAF (Electric Arc Furnace) investment despite higher initial costs.

Competition From Additive-Manufactured Lightweight Metals

Laser-powder-bed-fusion and directed-energy-deposition processes enable near-net-shape fabrication of aluminum, titanium, and nickel-based superalloys, eroding demand for forged and machined special-steel components in aerospace and defense. Additive routes deliver 30-50% lead-time savings for H13 dies and enable titanium-aluminide blades that trim turbine weight 20-30%. Tool steel’s share of aerospace forgings is already slipping, and certification hurdles remain the final moat. Certification timelines for additively manufactured flight-critical parts extend 3-5 years, and qualification costs can exceed USD 5 million per part number, creating a barrier to widespread substitution in legacy platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stainless Dominates, Tool Faces Additive Headwinds

Stainless steel’s 35.22% share in 2025 underscores its corrosion-critical role in electrolyzer stacks and offshore structures. Indonesia’s nickel-pig-iron surge and India’s capacity expansion underpin a 3.67% CAGR to 2031. Tool steel demand is flattening as the additive share in tooling production hit 11% in 2023, pressuring traditional supplies.

Alloy steel maintains relevance for drivetrain and heavy-equipment parts, but electric-vehicle shifts favor lighter metals. Bearing steel innovation, such as NSK’s high-speed EV axle unit, is pushing electroslag-remelted chemistries into mainstream auto supply. Nuclear programs, exemplified by Rosatom’s BR-1200 grade, pull austenitic alloys into high-temperature service.

By Form: Sheets And Plates Lead, Coils Accelerate

Sheets and Plates commanded 40.56% of 2025 revenue and are projected to expand at a CAGR of 3.51% during the forecast period (2026-2031), propelled by offshore-wind-tower fabrication, automotive body panels, and pressure-vessel applications that require wide-width rolling and tight thickness tolerances. The United States will require up to 2 million tons of plate annually once its 30 GW offshore-wind goal matures.

Coils, benefiting from automotive light-weighting and appliance production, exhibit the fastest trajectory, with Nucor’s West Virginia mill positioned for 2027 start-up. Bars and rods remain linked to machining hubs and wire-drawing operations, although EV penetration is trimming long shaft volumes. Others, including forgings and billets, serve turbine discs, rail wheels, and reroll feedstock, where certification and traceability fetch premiums.

By Application: Energy And Power Surges, Automotive Adjusts

Automotive components held 30.88% of 2025 revenue, yet drivetrain electrification shifts the mix toward high-strength, thinner cross-sections rather than heavy transmission gears. Energy and power lead segment growth at 4.65% CAGR through 2031 as Generation IV reactors, gas-turbine upgrades, and sizable offshore-wind projects escalate material complexity.

Aerospace structures employ special steel dies for superplastic-formed titanium parts, yet additive metals are eroding demand for large forgings. Oil and gas, machinery, construction, and rail each sustain niche, specification-driven demand profiles, protected by long certification cycles and safety codes.

Geography Analysis

Asia-Pacific’s 43.35% 2025 share stems from Chinese scale, Indian stimulus, and Indonesian nickel integration. China Baowu produced 131.85 million tons of crude steel in 2024 and pursues carbon-neutrality by 2050 through hydrogen metallurgy. India targets 300 million tons of capacity by 2030-31, supported by production-linked incentives that lower specialty-grade import reliance. ASEAN mills expand, though land and financing delays temper realization.

North America leverages scrap abundance and reshoring tailwinds. Nucor’s USD 3.1 billion sheet mill and ArcelorMittal’s USD 1 billion Calvert upgrade align with OEM (original equipment manufacturer) light-weighting programs. A pending Nippon Steel-US Steel tie-up would create a trans-Pacific specialty platform, while Gerdau’s EBITDA now skews 62% to its U.S. network.

Europe faces the steepest decarbonization costs. SSAB will deliver fossil-free steel by 2026, and Outokumpu’s ferrochrome integration buffers chromium volatility. Thyssenkrupp seeks partners as ETS prices pressure blast-furnace economics, and the UK’s Port Talbot conversion demonstrates political support framed by job cuts.

South America hinges on Brazilian trade defenses and sustainable mining improvements[2]Gerdau, “2025 Annual Report,” gerdau.com.br . Anti-dumping rulings due 2026 may stabilize domestic pricing. Argentina’s austerity curbs demand, though regional export channels open pockets of opportunity.

Middle East and Africa combine Saudi construction demand with South African ferrochrome supply dominance. Energy costs threaten smelter output, yet Vision 2030 megaprojects anchor long-product demand.

Competitive Landscape

The special steel market is highly fragmented. Nucor and SSAB emphasize scrap-based low-carbon sheet, while Rosatom’s TsNIITMASH illustrates R&D-led alloy differentiation. Digital alloy platforms shrink time-to-market, tightening the loop between customer specification and mill output. Additive bureaus act as disruptors in tool and prototype volumes, balancing the field.

Special Steel Industry Leaders

ArcelorMittal

Nippon Steel Corporation

POSCO

JFE Steel Corporation

China Baowu Steel Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AM/NS India, a joint venture of ArcelorMittal and Nippon Steel, began constructing an integrated steel plant in Andhra Pradesh, India. With an investment of USD 7.5 to USD 8 billion, the facility will have an annual capacity of 8.2 million tons. Production is expected to start in Q1 2029, focusing on a diverse range of steel products.

- June 2025: Thyssenkrupp introduced Bluemint Powercore grain-oriented electrical steel at CWIEME 2025. This special steel enhances energy efficiency in electric motors and generators, specifically for mobility applications. The product features reduced CO2 emissions, supporting environmental initiatives in the energy and mobility sectors.

Global Special Steel Market Report Scope

Special steel includes various kinds of steel with improved mechanical properties and better workability, which are essential for special applications in aerospace, power generation, nuclear, defense, cryogenic, and other general engineering industries.

The special steel market is segmented by product type, form, application, and geography. By product type, the market is segmented into stainless steel, tool steel, alloy steel, bearing steel, and carbon steel (special grades). By form, the market is segmented into sheets and plates, bars, rods, coils, and others (forgings, wires, and billets). By application, the market is segmented into automotive components, aerospace structures and engines, oil and gas equipment, machinery and tools, construction and infrastructure, energy and power (turbines, nuclear, and renewables), and other applications (railways, medical devices, and defense). The report also covers the market size and forecasts for special steel in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Stainless Steel |

| Tool Steel |

| Alloy Steel |

| Bearing Steel |

| Carbon Steel (Special Grades) |

| Sheets and Plates |

| Bars |

| Rods |

| Coils |

| Others (Forgings, Wires, and Billets) |

| Automotive Components |

| Aerospace Structures and Engines |

| Oil and Gas Equipment |

| Machinery and Tools |

| Construction and Infrastructure |

| Energy and Power (Turbines, Nuclear, and Renewables) |

| Other Applications (Railways, Medical Devices, and Defense) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Stainless Steel | |

| Tool Steel | ||

| Alloy Steel | ||

| Bearing Steel | ||

| Carbon Steel (Special Grades) | ||

| By Form | Sheets and Plates | |

| Bars | ||

| Rods | ||

| Coils | ||

| Others (Forgings, Wires, and Billets) | ||

| By Application | Automotive Components | |

| Aerospace Structures and Engines | ||

| Oil and Gas Equipment | ||

| Machinery and Tools | ||

| Construction and Infrastructure | ||

| Energy and Power (Turbines, Nuclear, and Renewables) | ||

| Other Applications (Railways, Medical Devices, and Defense) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big will special steel market size be by 2031?

The Special Steel Market size is expected to grow from USD 244.32 billion in 2025 to USD 252.5 billion in 2026 and is forecast to reach USD 297.73 billion by 2031 at 3.35% CAGR over 2026-2031.

What is the expected CAGR for special steels between 2026 and 2031?

The market is projected to grow at a 3.35% CAGR over 2026-2031.

Which product type leads revenue in special steels?

Stainless steel commanded 35.22% of 2025 revenue and continues to lead through the forecast period.

Why is energy and power the fastest-growing application?

Offshore-wind towers, Generation IV nuclear vessels, and hydrogen infrastructure demand corrosion-resistant, high-strength grades, driving a 4.65% CAGR.

Page last updated on: