Coated Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

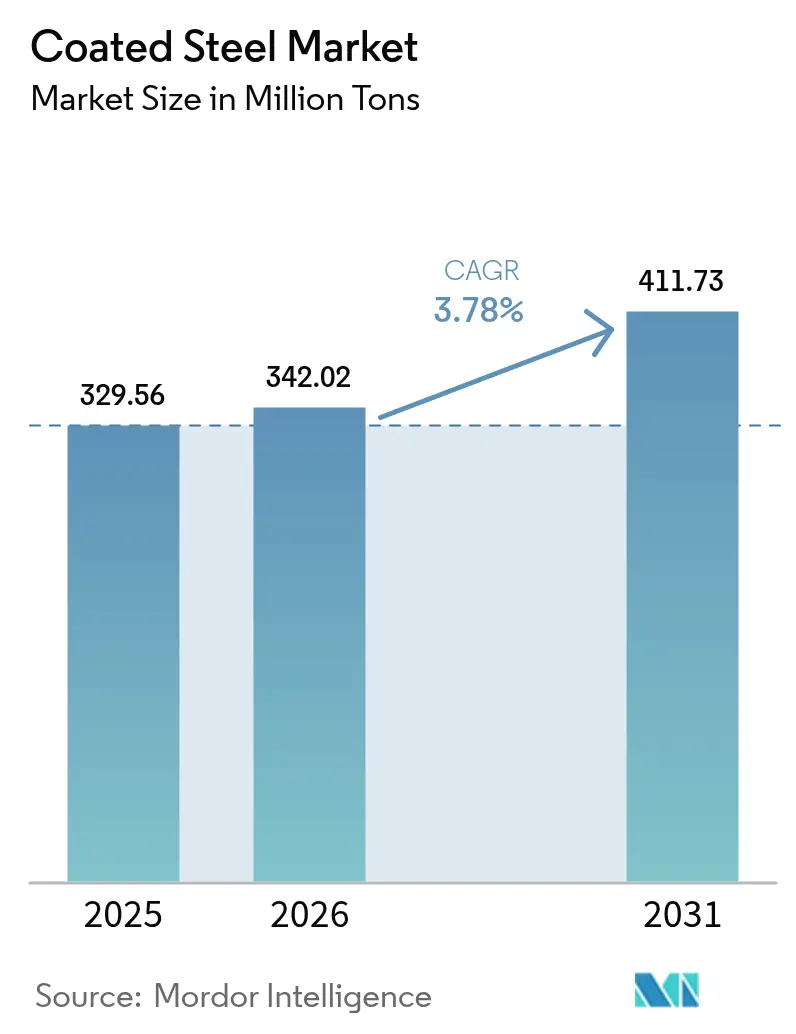

| Market Volume (2026) | 342.02 Million tons |

| Market Volume (2031) | 411.73 Million tons |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

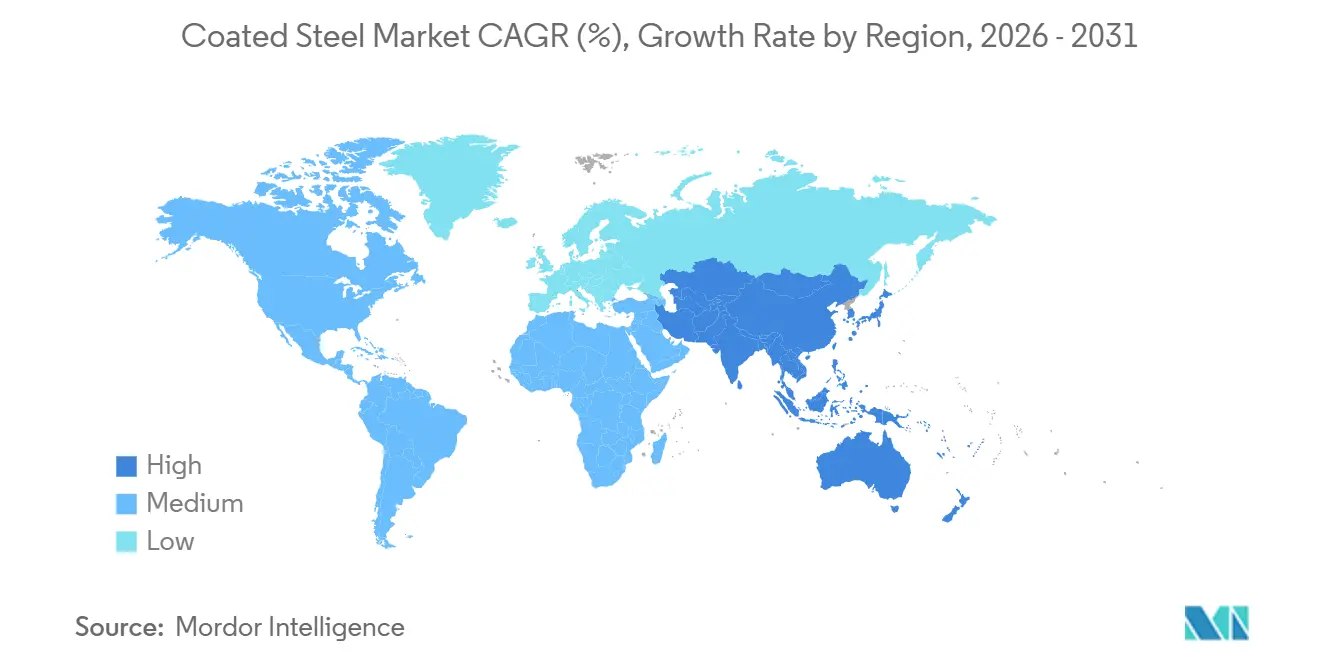

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coated Steel Market Analysis by Mordor Intelligence

The Coated Steel Market size is projected to expand from 329.56 Million tons in 2025 and 342.02 Million tons in 2026 to 411.73 Million tons by 2031, registering a CAGR of 3.78% between 2026 to 2031. Robust adoption of zinc-aluminum-magnesium (Zn-Al-Mg) alloy lines across Asia-Pacific, energy-efficient building-envelope codes in North America and Europe, and appliance-replacement incentives in both regions are jointly lifting demand for value-added coated substrates. Offshore-wind monopile specifications that require 25-year corrosion protection, together with agrivoltaic mounting structures in arid farming regions, are expanding the application range beyond cyclical construction activity. Tax credits such as the US Energy Efficient Home Improvement Credit and parallel European rebate programs are accelerating white-goods replacement, tightening supply of galvannealed sheet optimized for powder-coat adhesion. Meanwhile, trade actions that curb low-priced imports are encouraging new capacity closer to end-use hubs and reinforcing a moderate-concentration competitive landscape.

Key Report Takeaways

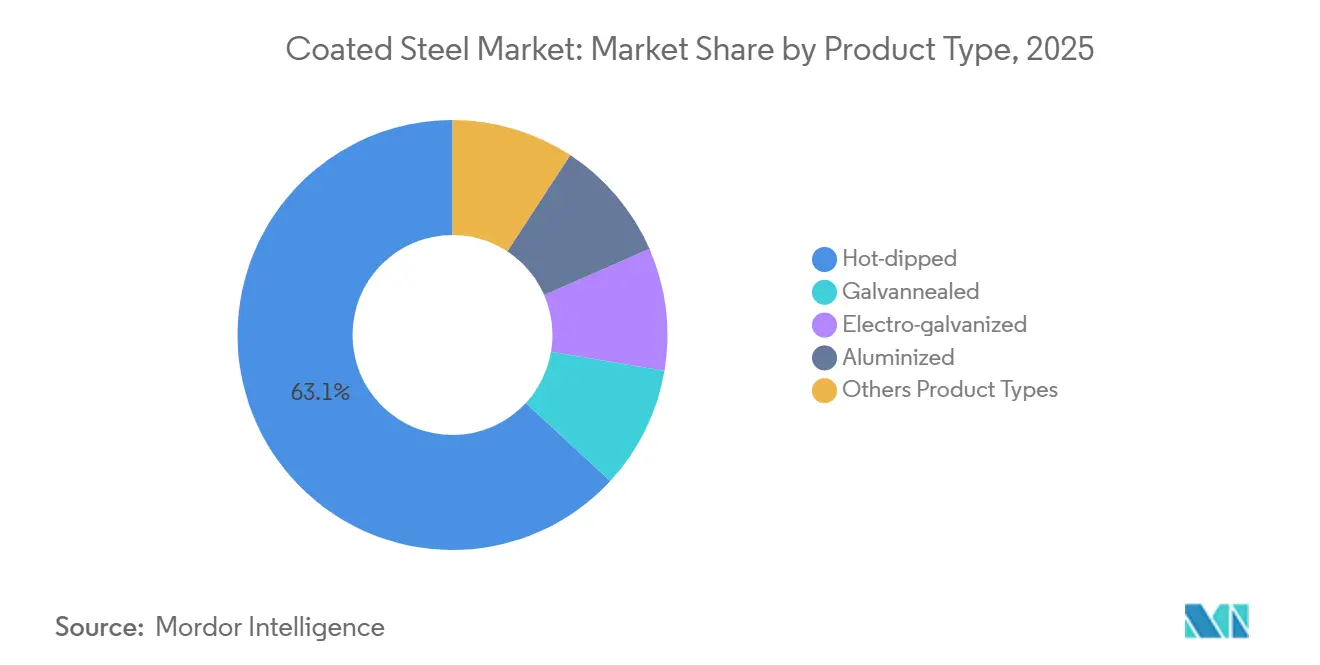

- By product type, hot-dipped coated steel captured 63.12% of the Coated Steel market share in 2025 and is advancing at a 3.94% CAGR to 2031.

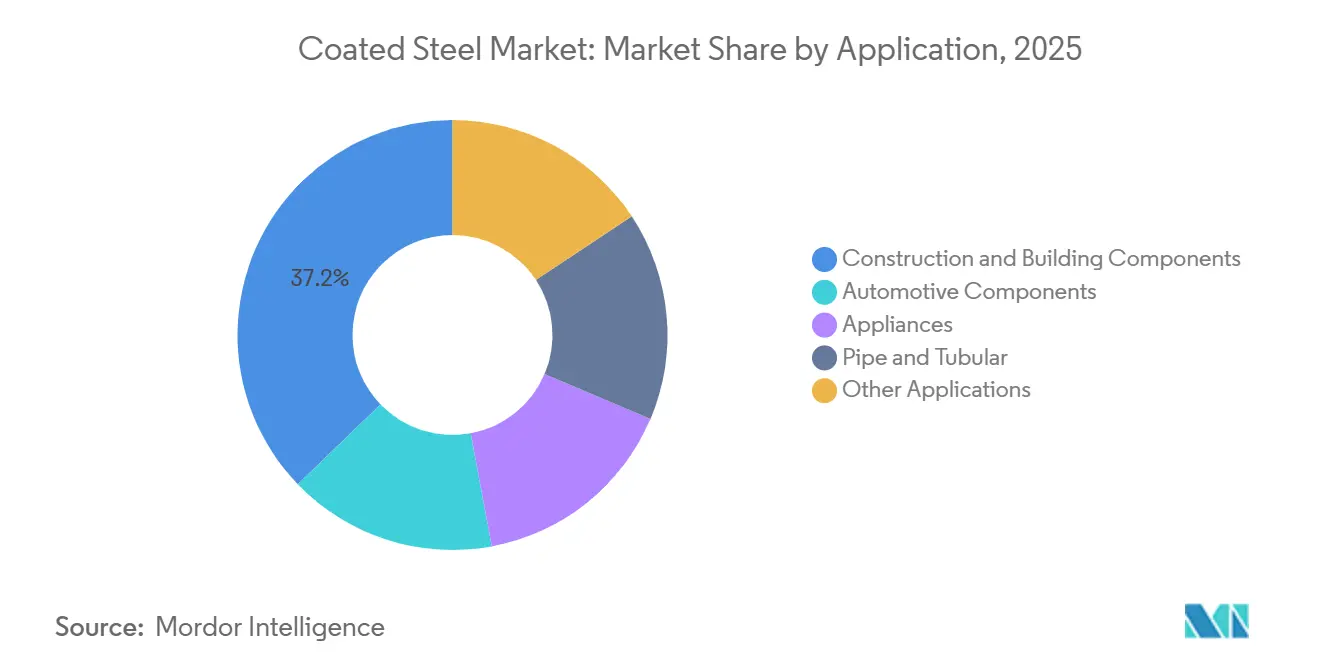

- By application, construction and building components accounted for 37.22% of the Coated Steel market size in 2025 and are projected to expand at a 4.46% CAGR through 2031.

- By geography, Asia-Pacific held 61.24% of the Coated Steel market share in 2025 and is moving at a 4.52% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coated Steel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficient building-envelope uptake of pre-painted coil | +0.9% | North America, EU, APAC (China, India) | Medium term (2–4 years) |

| Rapid rollout of Zn-Al-Mg alloy coating lines in Asia | +1.2% | APAC core (China, South Korea, Japan), spill-over to ASEAN | Short term (≤ 2 years) |

| Tax-driven appliance-replacement programs (EU and US) | +0.6% | North America, EU | Medium term (2–4 years) |

| Offshore-wind monopile corrosion-protected coil demand | +0.5% | EU (North Sea), APAC (Taiwan, Japan), North America (East Coast) | Long term (≥ 4 years) |

| Agrivoltaic structural steel coatings | +0.2% | APAC (India), EU (Spain), South America (Chile) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficient Building-Envelope Uptake of Pre-Painted Coil

Revised building codes in Europe and North America require lower thermal-transmittance values that insulated metal panels meet more economically than masonry or wood framing, directly boosting orders for factory-finished galvanized sheet[1]European Commission, “Energy Performance of Buildings Directive Recast,” europa.eu. The 2024 recast of the EU Energy Performance of Buildings Directive mandates near-zero energy use for new non-residential structures by 2028, while 18 US states had adopted the 2021 International Energy Conservation Code or stricter variants by mid-2025. Pre-painted products like Tata Steel’s Colorcoat HPS200 Ultra reflect up to 70% of solar radiation, cutting cooling loads by 15-18% in hot climates. Insurers now discount premiums for metal-clad buildings in wildfire zones by 10-15%, widening the economic gap versus vinyl or wood siding III.ORG. Procurement frameworks referencing ASTM D7897 and ISO 12944 have raised technical barriers for mills without in-house testing capabilities.

Rapid Rollout of Zn-Al-Mg Alloy Coating Lines in Asia

Twelve Zn-Al-Mg lines commissioned across China, South Korea, and Japan between 2024 and 2025 have added 8.5 million tons of annual capacity, positioning Asian mills to supply automakers and appliance OEMs demanding superior edge-corrosion resistance[2]Baowu Steel Group, “Meishan Zn-Al-Mg Line Announcement,” baosteel.com. Baowu’s 2 million t/a Meishan line delivers 1,500-hour neutral-salt-spray performance, triple that of standard galvanized sheet, by using an 11% Al, 3% Mg bath composition. POSCO’s 1.5 million t/a Gwangyang line targets electric-vehicle battery enclosures that require high formability at reduced gauge, achieving 8% mass savings. JFE Steel’s J-Star coating suppresses white rust during seaborne export, addressing a chronic issue in humid transit routes. The technology is diffusing into ASEAN, where NS BlueScope is investing THB 5 billion to retrofit its Bang Phra plant by 2027.

Tax-Driven Appliance-Replacement Programs (EU and US)

The US Energy Efficient Home Improvement Credit provides a 30% tax credit up to USD 2,000 for ENERGY STAR appliances, accelerating replacement of units built before 2015 and increasing coated-steel demand in refrigerator cabinets and washer drums. Parallel German and French grants offer EUR 100-500 per appliance, provided the retired unit is recycled through certified e-waste channels. Whirlpool reported a 7% year-over-year rise in North American shipments in Q4 2024, with galvannealed sheet making up 62% of cabinet weight. Nucor converted an electro-galvanized line at Crawfordsville, Indiana, to galvannealing in November 2024 to meet surging powder-coat substrate demand. The EU’s Ecodesign for Sustainable Products Regulation, effective January 2026, obliges OEMs to disclose recyclability indices, advantaging steel vs. plastic composites.

Offshore-Wind Monopile Corrosion-Protected Coil Demand

A 380 GW global offshore-wind pipeline as of December 2025, with monopiles for 75% of planned capacity, specifies zinc-rich primer plus epoxy-polyurethane topcoats that extend service life to 25 years. Each monopile consumes up to 1,200 tons of steel plate, driving total coated-steel needs of roughly 24 million tons for US Atlantic projects alone between 2027 and 2035. Hempel’s Hempadur Multi-Strength system recorded zero failures after 18 months of immersion testing on the UK’s Sofia wind farm. Jotun’s glass-flake reinforced Steelmaster 1200 WF extends maintenance intervals from 15 to 25 years by cutting moisture permeability by 40%. Mills are investing in 5-meter hot-strip capacity to fabricate extra-wide plate, a niche served by only six global producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminium-composite façade substitution | -0.4% | Middle East, Asia-Pacific | Medium term (2-4 years) |

| AD/CVD trade actions on coated sheet | -0.7% | North America, Mexico, Canada | Short term (≤ 2 years) |

| Supply tightness of low-carbon zinc feedstock | -0.3% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aluminum-Composite Façade Substitution

ACPs weigh 6-8 kg/m² versus 12-15 kg for steel panels, enabling lighter curtain-wall framing and 8-12% construction-cost savings in high-rise projects. Post-Grenfell fire-safety revisions accelerated the adoption of mineral-filled ACP cores above 18 meters, especially in Gulf megaprojects like NEOM and the Red Sea Development. The global ACP market grew 9.2% in 2024, eclipsing coated-steel cladding by 5.4 percentage points. However, aluminium’s lower galvanic potential accelerates pitting in coastal atmospheres, prompting premature failures after 7-10 years, whereas Zn-Al-Mg coated steel offers better edge protection. Producers are counteracting by offering hybrid steel panels with ceramic-frit or stone-veneer finishes that meet aesthetic demands without ceding performance.

AD/CVD Trade Actions on Coated Sheet

US combined AD/CVD duties of up to 456.23% on Vietnamese corrosion-resistant steel slashed imports 68% year-over-year in the first nine months of 2025. Diversion to Mexico raised its coated-sheet shipments to the US by 112%, triggering a new investigation in January 2025. European extensions of duties on Chinese cold-rolled feedstock in March 2025 further fragmented trade flows and inflated EU coil prices. US hot-dipped galvanized averaged USD 1,120 per ton in Q4 2025 versus USD 890 for duty-free alternatives, squeezing downstream HVAC and conduit fabricators. Mexican mills face inland logistics bottlenecks, delaying Midwest deliveries by up to four weeks and forcing OEMs to raise buffer inventories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hot-Dipped Dominance Anchored by Marine and Infrastructure Specifications

Hot-dipped coated steel commanded 63.12% of the coated steel market share in 2025 and is forecast to grow at a 3.94% CAGR to 2031, underpinned by Z275–Z450 coating-weight mandates in offshore wind monopiles and highway-infrastructure components. The coated steel market size for hot-dipped grades is projected to expand by nearly 52 million tons between 2026 and 2031 as developers standardize thicker zinc layers to assure 25-year durability. Electro-galvanized variants, favored for exposed auto panels, face cost headwinds from elevated European power prices and will decelerate to 2.5% CAGR, while galvannealed sheet remains supply-tight but niche at 18% share, held back by automaker migration to advanced high-strength Zn-Al-Mg solutions. Aluminized steel maintains relevance in high-temperature exhaust and oven liners but contributes less than 5% of incremental volume. Emerging micro-alloyed Zn-Al-Mg coatings, such as ArcelorMittal’s Magnelis, deliver 10-fold edge-corrosion improvement, positioning them for double-digit growth, albeit from a 2% base.

Demand for hot-dipped coil is also reinforced by the U.S. Infrastructure Investment and Jobs Act, which specifies galvanized guardrails and bridge decks in state DOT manuals, locking in multi-year volume commitments. Mini-mills are exploiting shorter campaign cycles to produce customized one-side galvanized sheet for appliance backs, capturing share from integrated giants resistant to frequent changeovers. Investment in inline laser-spectroscopy at POSCO’s Gwangyang works trims coating-weight variance to ±2 g/m², reducing scrap and sharpening cost competitiveness. Over the forecast horizon, capacity adds in India and ASEAN will meet surging regional construction demand, but environmental compliance costs in Europe could rationalize older electrolytic lines, nudging global supply toward modern hot-dip assets.

By Application: Construction Leads on Envelope Mandates and Pre-Engineered Building Adoption

Construction and building components represented 37.22% of 2025 volume and will post a 4.46% CAGR to 2031, the fastest among major applications, as retrofit mandates and wildfire-resilience criteria encourage metal-panel uptake. The coated steel market size linked to construction is set to grow by 46 million tons, fueled by 3% annual renovation targets for public buildings in Europe and cool-roof requirements such as California’s Title 24 reflectance threshold of 0.70. Pre-engineered buildings for e-commerce logistics drive another wave; Amazon reported 82% of fulfillment centers opened in 2024–2025 utilized metal roofs and walls, accelerating coil off-take.

Automotive, with a decent share in 2025, expands at a more modest CAGR as aluminium-intensive electric-vehicle platforms trim steel use per unit, though battery enclosures and crash-management systems still rely on advanced Zn-Al-Mg sheet for formability and corrosion resistance. Pipe and tubular applications capture oil-and-gas pipeline specifications under API 5L for sour environments, while “other” uses, such as data-center racking, expand on the back of hyperscaler capex. Modular construction’s 30-40% labor-saving advantage in markets like Germany and Japan is projected to lock in recurring orders for factory-finished coil.

Geography Analysis

Asia-Pacific dominated the coated steel market with 61.24% volume share in 2025 and is on track for a 4.52% CAGR to 2031. China, supported by its 14th Five-Year Plan, produced about 210 million tons in 2025, and integrated mills such as Baowu are pivoting toward Zn-Al-Mg lines to serve electric-vehicle and solar-frame customers. India’s Production Linked Incentive scheme spurred 11.3% demand growth in fiscal 2024–2025, with Tata Steel and JSW collectively adding 3.2 million tons of capacity.

In North America, the US coated steel market benefited from the Infrastructure Investment and Jobs Act and the reshoring of appliance production; domestic mills supplied 72% of the total consumed steel, with Nucor’s Brandenburg project adding 1.2 million tons of new capacity by Q3 2026. Canadian growth is steadier. pivoting on mining-sector conveyors, while Mexico’s surge risks reversal if AD/CVD tariffs emerge in late 2026.

In Europe, Germany consumed most, with thyssenkrupp and Salzgitter supplying Zn-Al-Mg sheet to automakers. The UK market grows modestly on social-housing grants requiring insulated metal panels, while France and Italy see upside from battery gigafactory and data-center projects. South America and Middle East and Africa’s growth in the market is fueled by Brazil’s agribusiness structures and Saudi Arabia’s NEOM megaproject.

Competitive Landscape

The Coated Steel market is fragmented. Mini-mill challengers leverage electric-arc furnaces for flexible short-run specialties, grabbing 8-10% share in niches like one-sided galvanized sheet for appliance backs. Emergent demand pockets include agrivoltaic structures requiring 40-year warranties and modular data-center enclosures where hyperscalers prioritize pre-painted steel for speed. ArcelorMittal’s 2025 purchase of Vallourec’s Brazilian assets seized a 0.9 million t/a color-coil line primed for Latin American pre-engineered building growth.

Coated Steel Industry Leaders

ArcelorMittal

China Baowu Steel Group Corp., Ltd

POSCO Coated Steel(Thailand) Co.,Ltd.

Nippon Steel Coated Sheet Corporation

JFE Steel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Jindal (India) Limited (JIL) initiated a metal coating production line at its Ranihati facility in West Bengal, India. Owing to this new line, JIL anticipates a boost in coated steel output by around 60%, bringing the total to nearly 300,000 tons.

- September 2025: AM/NS INDIA introduced Optigal Prime, a color-coated steel product manufactured to European standards, in Jammu & Kashmir. The product addresses the region's severe weather challenges and serves residential mountain construction and infrastructure projects.

Global Coated Steel Market Report Scope

When a coating of organic or metallic compounds is applied to the steel surface to prevent corrosion, it is called coated steel. Coated steel is considered an ideal and effective method for protecting steel from corrosive environments.

The Coated Steel market is segmented by product type, application, and geography. By product type, the market is segmented into hot-dipped, electro-galvanized, aluminized, galvannealed, and other product types. By application, the market is segmented into automotive components, appliances, construction and building components, pipe and tubular, and other applications. The report also covers the size and forecasts for the coated steel market in 16 countries across major regions. For each segment, the market sizing and forecasts are based on volume (tons).

| Hot-dipped |

| Galvannealed |

| Electro-galvanized |

| Aluminized |

| Others Product Types |

| Construction and Building Components |

| Automotive Components |

| Appliances |

| Pipe and Tubular |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Hot-dipped | |

| Galvannealed | ||

| Electro-galvanized | ||

| Aluminized | ||

| Others Product Types | ||

| By Application | Construction and Building Components | |

| Automotive Components | ||

| Appliances | ||

| Pipe and Tubular | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the coated steel market in 2031?

The sector is expected to reach 411.73 million tons by 2031, advancing at a 3.78% CAGR from 2026.

Which product type holds the largest share of coated steel demand?

Hot-dipped coated steel led with 63.12% market share in 2025, driven by marine and infrastructure specifications.

Why are Zn-Al-Mg coatings gaining momentum in Asia?

Asian mills added 8.5 million t/a of Zn-Al-Mg capacity through 2025 to supply automakers and appliance OEMs requiring superior edge-corrosion resistance.

How do appliance-replacement incentives affect coated steel consumption?

US and EU tax credits are accelerating replacement of pre-2015 units, adding an estimated 1.8 million tons of coated-steel demand between 2024 and 2027.

Which geographic region is growing fastest in coated steel demand?

Asia-Pacific is expanding at 4.52% CAGR to 2031, supported by Chinese infrastructure, India’s incentive schemes, and ASEAN housing programs.

Page last updated on: