100% Juice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

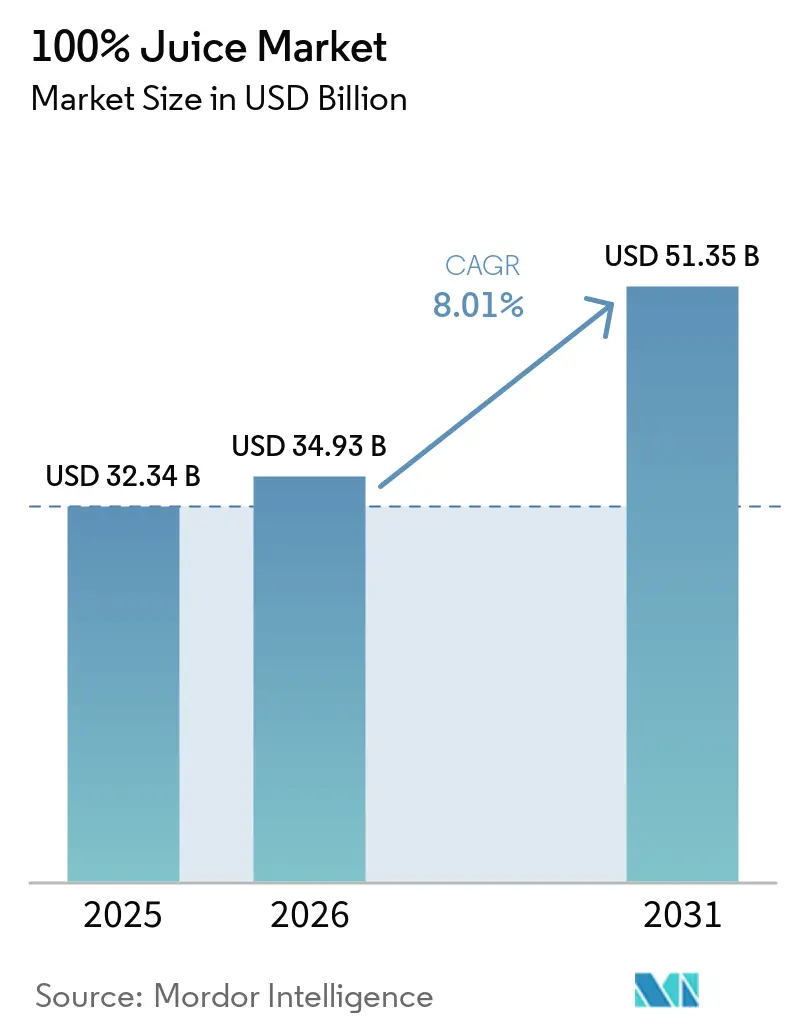

| Market Size (2026) | USD 34.93 Billion |

| Market Size (2031) | USD 51.35 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

100% Juice Market Analysis by Mordor Intelligence

The 100% juice market size was valued at USD 32.34 billion in 2025 and estimated to grow from USD 34.93 billion in 2026 to reach USD 51.35 billion by 2031, at a CAGR of 8.01% during the forecast period 2026-2031. The market is expanding as households increasingly prefer pure juice over carbonated and sweetened beverages. A 2025 Fruit Juice Science Centre survey revealed that a 150 ml serving of 100% orange juice provides over 90% of the daily recommended vitamin C intake, highlighting its nutritional value in both mature and emerging markets. Premiumization trends are evident, with rising demand for not-from-concentrate products, fruit and vegetable blends, and cold-chain offerings that meet clean-label expectations. Competition focuses on reformulation, improved packaging, and wider distribution. However, challenges like raw material volatility, sugar misconceptions, and compliance pressures in Europe persist, making growth dependent on supply, pricing, labeling clarity, and consumer education.

Key Report Takeaways

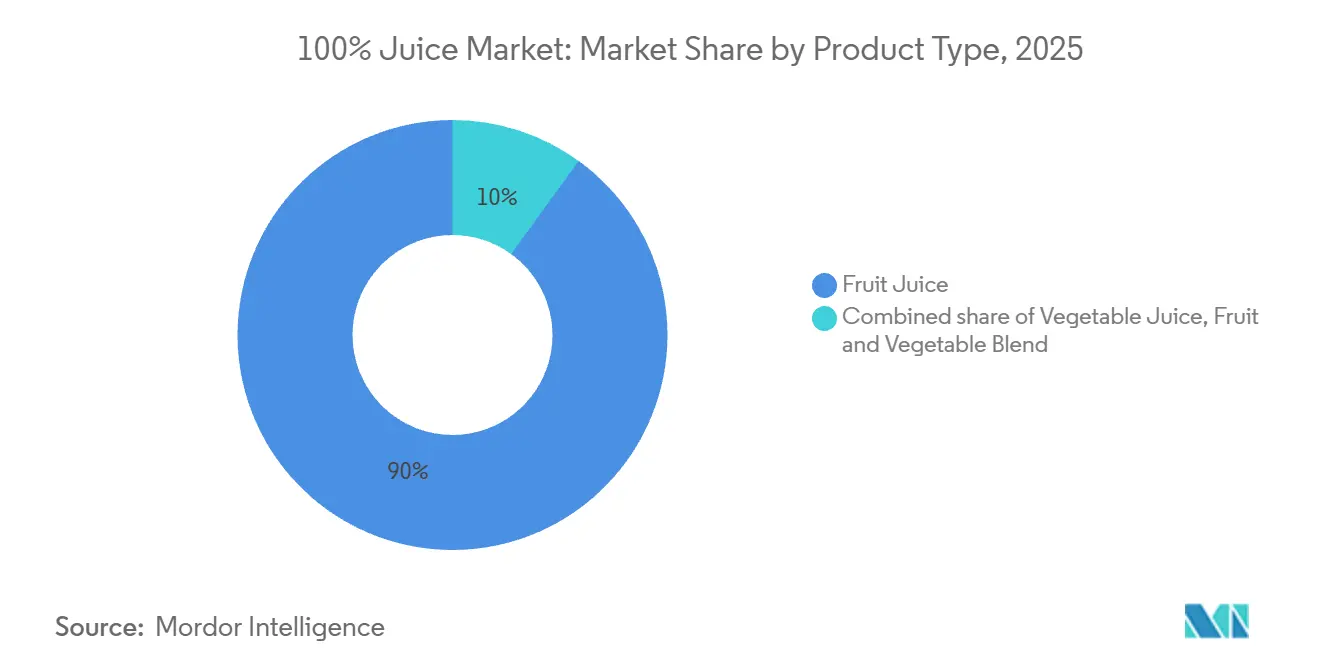

- By product type, fruit juice held 90.02% of the 100% juice market share in 2025, while fruit and vegetable blends are forecast to expand at a 9.32% CAGR through 2031.

- By category, not-from-concentrate juice accounted for 68.34% of the 100% juice market size in 2025, while from-concentrate juice is projected to grow at an 9.01% CAGR through 2031.

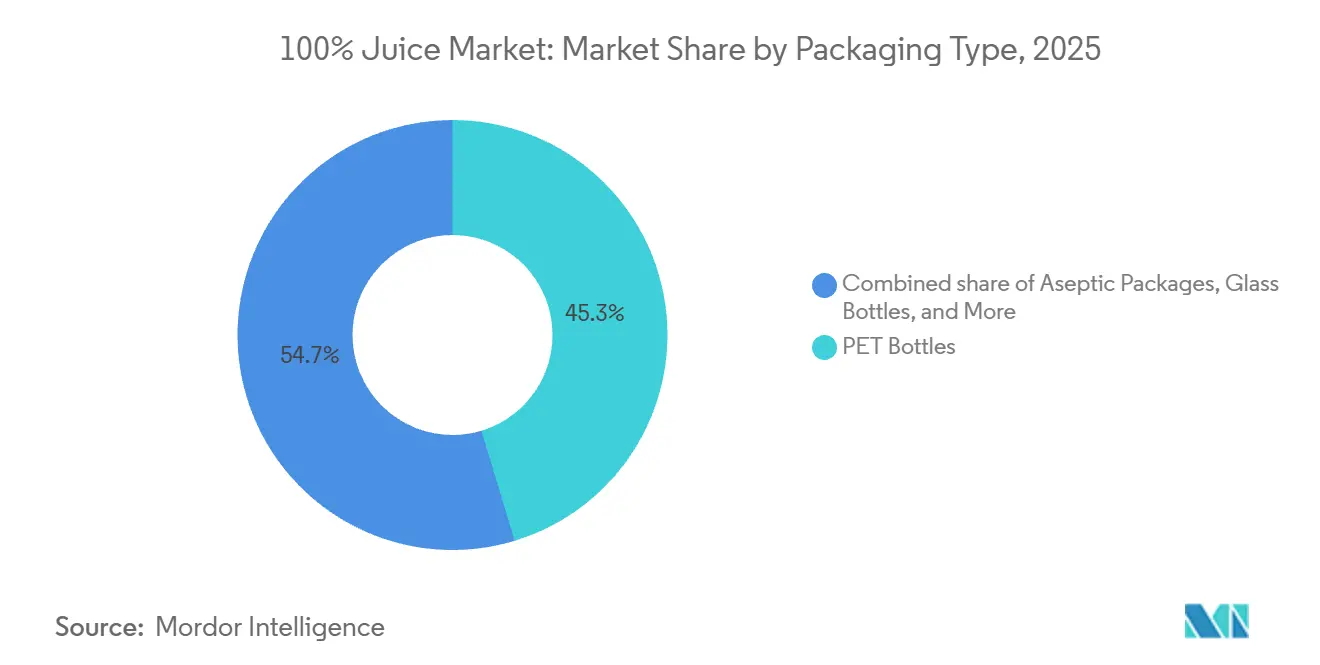

- By packaging type, PET bottles captured 45.33% of the 100% juice market size in 2025, while disposable cups and pouches are expected to advance at an 8.83% CAGR through 2031.

- By distribution channel, off-trade held 83.48% share in 2025, while on-trade recorded the fastest projected CAGR at 9.62% through 2031.

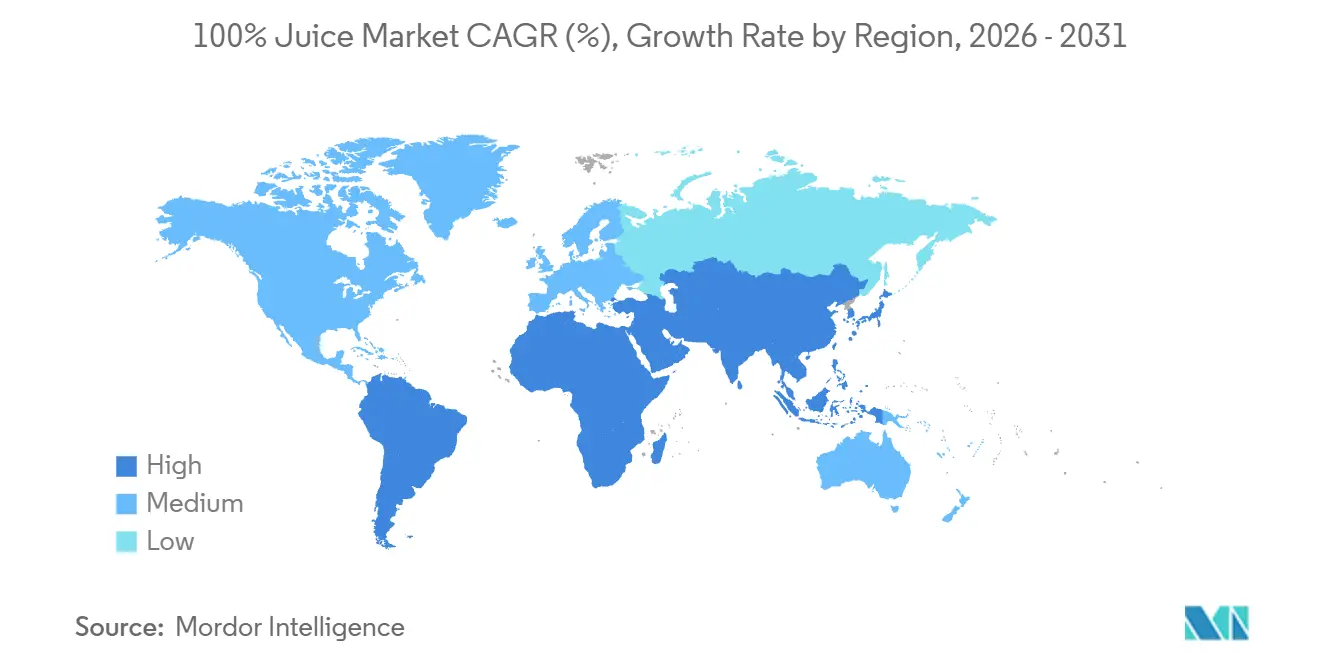

- By geography, North America held 37.18% of the 100% juice market share in 2025, while Asia-Pacific is forecast to grow at a 10.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 100% Juice Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and wellness trends | +2.5% | Global | Short term (≤ 2 years) |

| Preference for clean-label and minimally processed beverages | +1.8% | North America & Europe | Medium term (2–4 years) |

| Cold-pressed juice bar proliferation | +1.3% | North America, APAC core | Medium term (2–4 years) |

| Demand for natural and organic products | +1.5% | North America, Europe, APAC | Medium term (2–4 years) |

| Growing popularity of plant-based and vegan diets | +0.9% | North America, Europe | Medium term (2–4 years) |

| Increasing demand for convenience and ready-to-drink formats | +1.2% | Global, led by APAC and MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness and Wellness Trends

The 100% juice market continues to grow across different income and age groups, driven by health-conscious beverage choices. According to USDA data from China, 75% of consumers actively prefer products labeled as 100% pure juice, highlighting a strong inclination toward low-sugar, all-fruit options instead of diluted alternatives[1]Source: USDA Foreign Agricultural Service, “Unlocking Opportunities in China’s 170 Billion Dollar Beverage Market”, usda.gov . A similar pattern is observed in Europe, where the Fruit Juice Science Centre reports that many consumers associate 100% juice with essential vitamins and daily fruit intake. However, there is still limited awareness about sugar content and the importance of moderation. This trend is significant for the 100% juice market, as consumers who view juice as a functional food are less likely to leave the category, even during price increases. This behavior benefits premium juice formats more than standard ambient options, particularly when nutritional information is clearly displayed on the packaging. It also emphasizes the need for clinical messaging, transparent ingredient lists, and educational marketing strategies to help brands maintain customer loyalty and encourage repeat purchases.

Preference for Clean-Label and Minimally Processed Beverages

In North America and Europe, clean-label expectations have become fundamental in the 100% juice market. Tracking by Ingredion in 2025 highlighted a growing emphasis on claims like simple ingredients, concise ingredient lists, and traceable sourcing in purchase decisions. This trend underscores a broader resistance to ultra-processed foods. Consumers' preference for not-from-concentrate products aligns with their desire for minimal intervention and ingredient simplicity. In Europe, regulatory pressures, particularly sugar-reduction rules, are nudging producers and retailers towards cleaner juice formulations and product reformulations. Consequently, the demand for clean labels is influencing product design, shelf composition, and capital allocation within the 100% juice market. Producers adept at balancing minimal processing with robust taste retention are securing premium shelf placements.

Demand for Natural and Organic Products

The growing preference for natural and organic products is boosting the premium segment of the 100% juice market. Consumers are drawn to organic and purity-focused messaging, as it assures them of both nutritional quality and responsible sourcing. This trend is particularly evident in developed retail channels, where premium juice lines are gaining popularity. For example, the USDA reported that in China, Sam’s Club's private-label 100% pure fruit juice achieved an 11.7% sales increase in 2024. This indicates that the demand for purity credentials is no longer limited to niche health-conscious shoppers but is expanding into broader retail formats. As a result, both branded and private-label portfolios in the 100% juice market are experiencing growing demand for premium products. This shift is also driving the adoption of high-pressure processing and cold-chain formats, which help maintain a fresh and minimally processed product image. Brands that combine organic certifications with consistent taste and reliable availability are better positioned to build stronger customer loyalty compared to those competing solely on price.

Increasing Demand for Convenience and Ready-to-Drink Formats

Convenience is driving growth in the 100% juice market by increasing access points and promoting more frequent consumption. Ready-to-drink packs are particularly effective in modern retail, foodservice, travel, schools, and quick meal scenarios, making packaging and channel strategies more critical than ever. In China, the USDA reported a 14% CAGR for e-commerce beverage sales, highlighting how digital platforms are expanding the reach of premium juice products beyond traditional retail channels. Coca-Cola Europacific Partners demonstrated this approach by introducing Innocent's Kids Juicy Water in 549 Burger King restaurants across the UK before rolling it out to broader retail markets. This strategic use of channel sequencing helps the 100% juice market encourage product trials, especially for newer formats that rely on building brand recognition. It also benefits suppliers who can efficiently manage various pack sizes and adapt quickly to both retail and foodservice environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar content and natural sugar concerns | -0.7% | Global, acute in EU and North America | Short term (≤ 2 years) |

| Calorie density and weight management trends | -0.5% | North America, Europe | Medium term (2–4 years) |

| Short shelf life and cold-chain dependency | -0.3% | APAC developing markets, MEA, South America | Long term (≥ 4 years) |

| Fluctuating raw material prices and fruit availability | -0.3% | Global, acute in South America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Sugar Content and Natural Sugar Concerns

Perceptions about sugar significantly hinder the growth of the 100% juice market. Research from the Fruit Juice Science Centre revealed that close to 40% of European consumers mistakenly believe that 100% juice has added sugar, despite legal prohibitions against it. Furthermore, the study highlighted that nearly 30% of consumers shun the category due to these sugar-related concerns, indicating that the demand is influenced more by behavior than by nutritional facts. In Germany, VdF noted a dip in fruit juice and nectar consumption in 2025, primarily attributed to rising prices, but concerns over sugar also weighed heavily on the volumes. In the U.S., regulatory efforts are underway to modernize identity standards for pasteurized orange juice, underscoring the heightened compliance and communication challenges producers face in championing the juice's nutritional value. Consequently, for the 100% juice market, education, portion guidance, and transparent labeling have become as crucial as taste and price.

Calorie Density and Weight Management Trends

Weight management concerns are increasingly influencing the 100% juice market, as calorie-conscious consumers adjust their beverage choices. In France, UNIJUS reported a steady decline in national juice and nectar sales, with the 2024 drop reflecting a growing preference for lower-calorie alternatives. Although 100% juice provides essential vitamins, minerals, and plant compounds, its calorie content has become a concern for many consumers. Producers are addressing this challenge by adapting their offerings rather than compromising on nutritional value. They are introducing smaller portion sizes, developing lower-sugar blends, and creating juice-and-water combinations to reduce the perceived calorie barrier. For instance, Tropicana’s 'Fresh & Light' and Mott’s 'Zero Sugar Juice Drinks' demonstrate how major brands are catering to consumers seeking better control over sugar and calorie intake. These innovations, while not strictly within the 100% juice segment, reflect how weight management trends are driving product development across the broader beverage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fruit Juice Leads While Blended Formats Gain Speed

In 2025, fruit juice led the 100% juice market with a dominant 90.02% share, significantly ahead of vegetable juice and blends. Its success stems from strong household familiarity, extensive retail availability, and popular varieties like orange, apple, and grape. Consumers trust its taste and easily incorporate it into daily routines. In Germany, VdF reported easing orange juice prices after a 2025 peak, indicating improved supply conditions following high citrus costs. Despite volume challenges in mature markets, fruit juice remains the backbone of the 100% juice market due to its unmatched scale and distribution.

Vegetable juice, though smaller, showed potential to offset declines in traditional fruit lines. VdF noted a 10% rise in vegetable juice consumption in Germany in 2025, even as fruit juice volumes dropped, reflecting a shift toward lower-sugar, functional beverages[2]Source: Verband der deutschen Fruchtsaft-Industrie, “VdF Veröffentlicht Branchendaten, Verbrauch Von Fruchtsaft Sinkt, fluessiges-obst.de. Fruit and vegetable blends are the fastest-growing segment, with a 9.32% CAGR through 2031, driven by demand for healthier options with familiar flavors. USDA highlighted increasing interest in China for prunes, blueberries, pomegranates, and fruit-vegetable blends among health-conscious urban consumers. These blends help brands address sugar concerns while maintaining nutritional and premium appeal, offering relevance to vegan, flexitarian, and wellness-focused buyers seeking functional benefits in a single serving.

By Category: NFC Holds the Largest Position While FC Expands Through Practicality

In 2025, not-from-concentrate (NFC) juice led the 100% juice market with a 68.34% share, driven by minimal processing, fresh taste, and alignment with clean-label trends. Consumers associate NFC with better taste and a fresher experience, supporting its premium pricing. In Asia-Pacific, Mordor Intelligence noted NFC's premium positioning in China's tier-1 supermarkets, where natural and minimally processed claims are key in premium beverage choices. This makes NFC the most familiar and quality-aligned segment in the market.

From-concentrate (FC) juice is projected to grow at an 9.01% CAGR through 2031, making it the fastest-growing segment despite NFC's dominance. This growth is due to FC's practicality in areas with cold-chain challenges, foodservice demand for stable supply, and price-sensitive households. Industry insights from Spain show FC evolving with fortified products and smaller formats, maintaining its presence on shelves. FC plays a vital role in expanding distribution in hot climates and developing markets, enabling the 100% juice market to balance premium growth with practical volume expansion.

By Packaging Type: PET Bottles Stay on Top While Single-Serve Packs Grow Faster

In 2025, PET bottles accounted for 45.33% of the juice packaging market, making them the leading choice due to their volume relevance and versatility. Producers prefer PET bottles for their cost-efficiency, flexible sizes, and strong consumer acceptance. PET supports both mainstream and premium juice lines, allowing suppliers to manage diverse portfolios across price points. Plastipak's June 2026 certification for O2Blox recyclable PET barrier packaging highlighted advancements in combining oxygen protection with bottle-to-bottle recyclability for juice applications. These innovations strengthen PET's position in the 100% juice market as sustainability and shelf-life demands grow.

Aseptic packs, glass bottles, and metal cans serve niche roles. Aseptic cartons suit family-sized ambient consumption, glass bottles cater to premium and organic products, and metal cans target impulse and convenience purchases. Disposable cups and pouches are projected to grow at an 8.83% CAGR through 2031, making them the fastest-growing packaging format. Their growth is driven by on-the-go use, affordability, and rising foodservice demand, especially for single-serve options. Kraft Heinz's 2026 Capri-Sun Hydrate launch demonstrated how pouch-based systems with added functionality can boost consumer interest in portable formats. While Capri-Sun is not strictly 100% juice, its packaging innovation highlights how convenience-focused designs are shaping the 100% juice market, particularly for portability, trial, and family use.

By Distribution Channel: Off-Trade Dominates While On-Trade Builds Trial and Premium Reach

In 2025, off-trade channels captured an impressive 83.48% share of the 100% juice market, underscoring the dominance of supermarkets, hypermarkets, convenience stores, and online platforms. These outlets not only drive repeat purchases and larger basket sizes but also facilitate price comparisons between branded and private-label products. While supermarkets and hypermarkets lead the off-trade scene—especially in developed markets where chilled sections boost premium NFC sales—online retail is emerging as the fastest-growing segment. According to USDA, e-commerce beverage sales in China are surging at a 14% CAGR, buoyed by livestreaming and social commerce. This robust growth in the 100% juice market not only solidifies its foundation but also paves the way for targeted premium product launches.

Forecasted to expand at a 9.62% CAGR through 2031, on-trade channels are emerging as the fastest-growing distribution avenue. Juice bars, hotels, cafes, and fast-casual dining establishments are driving this growth, promoting higher-value purchases. The significance of this channel lies in its ability to introduce consumers to cold-pressed, blended, and premium-origin products, which they may subsequently seek in retail. Coca-Cola Europacific Partners capitalized on this trend, debuting Innocent's Kids Juicy Water at Burger King before a broader retail rollout. This strategy highlights the potential of foodservice as a brand trial platform for the 100% juice market, rather than merely a volume outlet. It also indicates that while off-trade channels dominate in scale, on-trade growth will continue to elevate the perception of premium products.

Geography Analysis

In 2025, North America led the 100% juice market with a 37.18% share. Its success stems from advanced retail systems, strong refrigeration infrastructure, and consumer familiarity with premium juices. Established brands, efficient distribution, and a product mix catering to both mass and premium tiers further strengthen its position. The U.S. drives regional value, while Canada maintains steady demand for premium formats. Mexico and other areas offer growth potential as modern retail expands and premium products become more accessible. North America sets benchmarks in product innovation, premium packaging, and channel execution.

Europe, the second-largest market, remains vital due to regulatory influence. In 2025, 100% juice accounted for 48.82% of Europe's fruit and vegetable juice market, supported by reformulation trends and retailer preference for cleaner products. Producers focus on reduced-sugar options, clearer labeling, and cleaner formulations to meet compliance standards. Germany exemplifies the region's shift, with VdF reporting lower fruit juice consumption but higher vegetable juice demand in 2025. This trend highlights Europe's move toward selective, value-driven demand rather than declining relevance.

Asia-Pacific is the fastest-growing region, with the 100% juice market projected to grow at a 10.02% CAGR through 2031. Urbanization, rising incomes, and changing diets drive demand in China, India, and Southeast Asia. USDA data shows premium NFC and HPP juices make up over 45% of China's domestic juice revenue, reflecting rapid adoption of premium products. The same report noted an 11.7% sales increase for Sam’s Club private-label 100% juice in 2024, signaling broader premium adoption. Southeast Asia benefits from modern retail growth and trust in certified products, while India expands through its young population and growing e-commerce. South America, the Middle East, and Africa are smaller markets, but Brazil's role in global orange juice supply significantly impacts sourcing and pricing in the 100% juice market.

Competitive Landscape

The 100% juice market is dominated by a few multinational companies, while regional and private-label producers hold a notable share. Key players like The Coca-Cola Company, PepsiCo, Tropicana Brands Group, Ocean Spray Cranberries, Inc, and Welch Foods Inc leverage strong brands and extensive distribution networks. This approach ensures shelf space in supermarkets and convenience stores while supporting product development and marketing.

Competition focuses on health-driven innovations, premium products, and clean labeling. Manufacturers are launching products without added sugars, with organic certifications, and fortified with functional ingredients to meet changing consumer preferences. Premium options, such as cold-pressed juices, exotic fruit blends, and sustainably sourced ingredients, help companies stand out and attract high-value customers.

Private-label and regional producers compete by offering affordable options and catering to local tastes. Meanwhile, established players invest in packaging innovations, sustainability, and supply chain improvements to boost brand loyalty and efficiency. As demand grows for healthier, natural beverages, companies with strong brands, innovative products, and wide distribution are expected to lead the 100% juice market.

100% Juice Industry Leaders

The Coca-Cola Company

PepsiCo, Inc.

Tropicana Products, Inc.

Ocean Spray Cranberries, Inc.

Welch Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Fresh Del Monte Produce completed the court-supervised acquisition of selected Del Monte Foods assets, including U.S. and Mexico rights to the Del Monte and S&W brands for the shelf-stable fruit business, after Pacific Coast Producers won a key portion in Del Monte Foods' Chapter 11 bankruptcy auction. This consolidation restructures the competitive landscape for canned and packaged fruit-and-juice-adjacent products in North America.

- September 2025: Rhodes Quality introduced its new Limited Edition Juice range, offering consumers a refreshing, 100% fruit and vegetable juice. The range features three distinctive flavors: Apple, Lemon & Ginger, and Pineapple, Carrot & Turmeric.

- August 2025: Tropicana Brands Group introduced Tropicana Essentials in the United States, a fortified orange juice blend at an accessible price point of USD 3.89 for 46 fl oz. The product addresses growing value-tier demand from cost-sensitive households while maintaining nutrient fortification, including vitamins C and E, calcium, and vitamin D.

Global 100% Juice Market Report Scope

| Fruit Juice |

| Vegetable Juice |

| Fruit and Vegetable Blend |

| Not From Concentrate |

| From Concentrate |

| Aseptic Packages |

| Glass Bottles |

| Metal Can |

| PET Bottles |

| Disposable Cups and Pouches |

| On-trade | |

| Off-trade | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fruit Juice | |

| Vegetable Juice | ||

| Fruit and Vegetable Blend | ||

| By Category | Not From Concentrate | |

| From Concentrate | ||

| By Packaging Type | Aseptic Packages | |

| Glass Bottles | ||

| Metal Can | ||

| PET Bottles | ||

| Disposable Cups and Pouches | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in 100% juice consumption worldwide?

Growth is being supported by the shift away from sugary soft drinks, stronger health awareness, clean-label demand, and premium interest in NFC and blended formats. The category is projected to grow at an 8.01% CAGR from 2026 to 2031.

Which region leads global demand for 100% juice?

North America held the largest share at 37.18% in 2025, supported by mature retail systems, strong refrigeration infrastructure, and wide premium product availability.

Which region is growing the fastest for packaged pure juice products?

Asia-Pacific is forecast to grow the fastest, at a 10.02% CAGR through 2031, driven by urbanization, income growth, and rising premium demand in China, India, and Southeast Asia.

Which product segment is growing fastest within juice categories?

Fruit and vegetable blend is the fastest-growing product type, with a 9.32% CAGR through 2031, because it combines taste familiarity with lower sugar perception and broader functional appeal.

Page last updated on: