Fruit Fillings Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

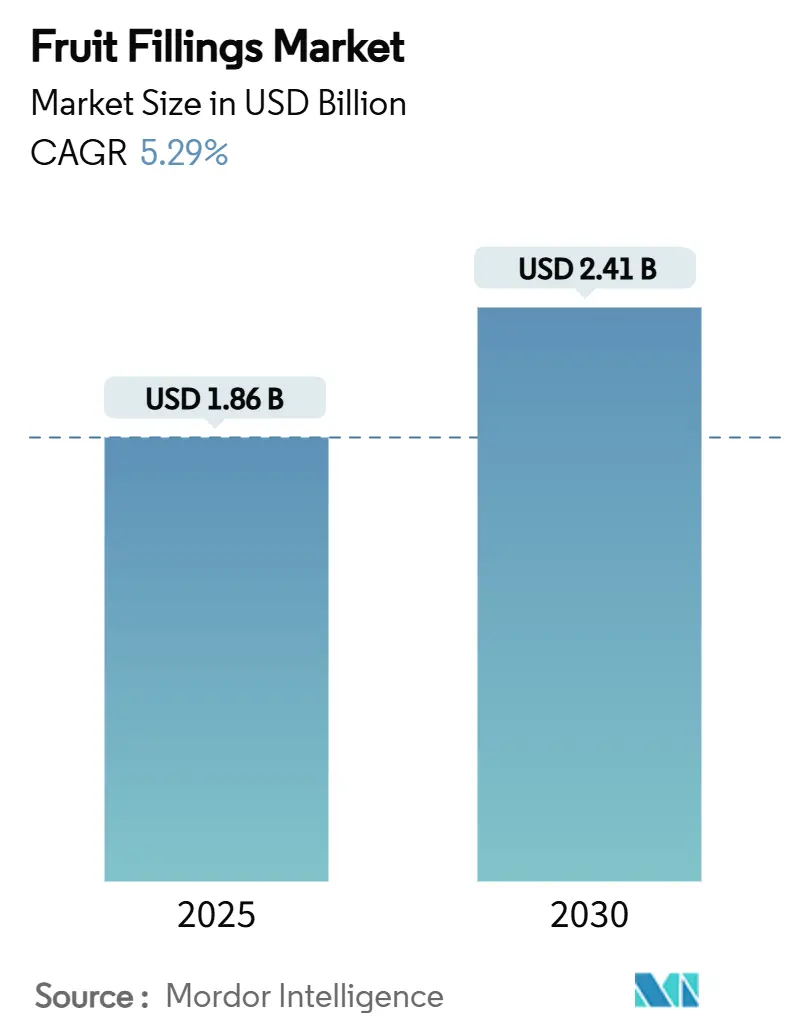

| Market Size (2025) | USD 1.86 Billion |

| Market Size (2030) | USD 2.41 Billion |

| Growth Rate (2025 - 2030) | 5.29% CAGR |

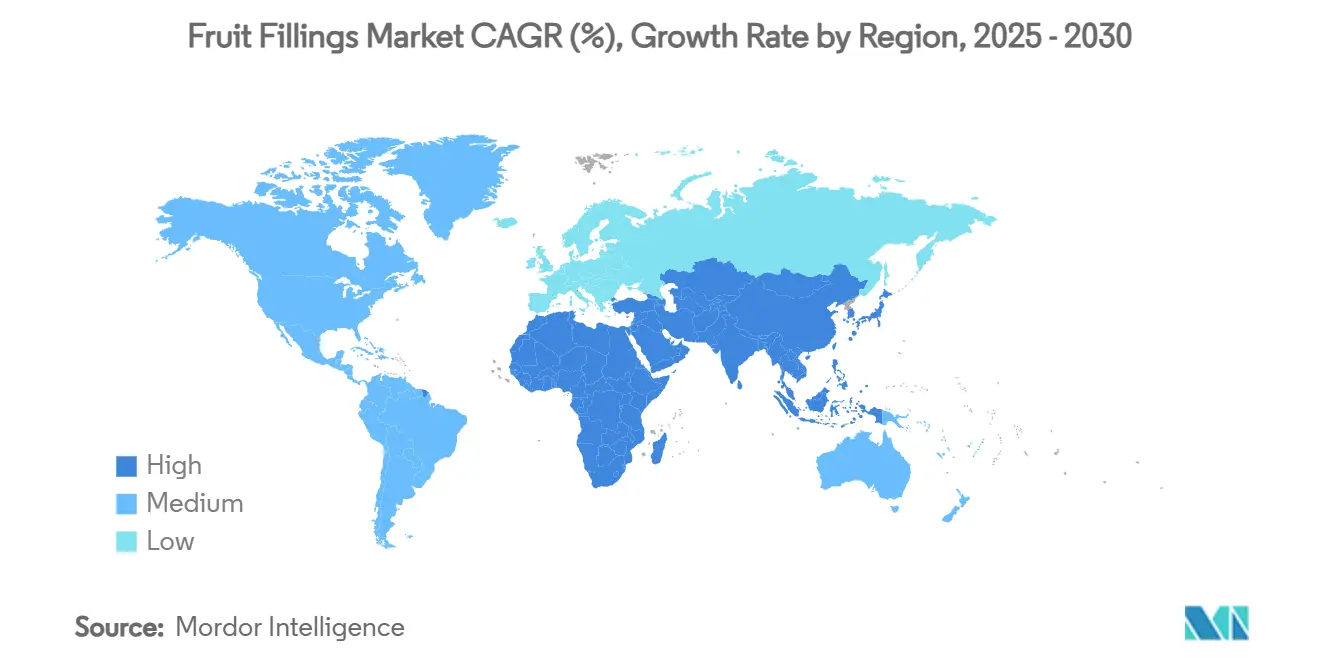

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

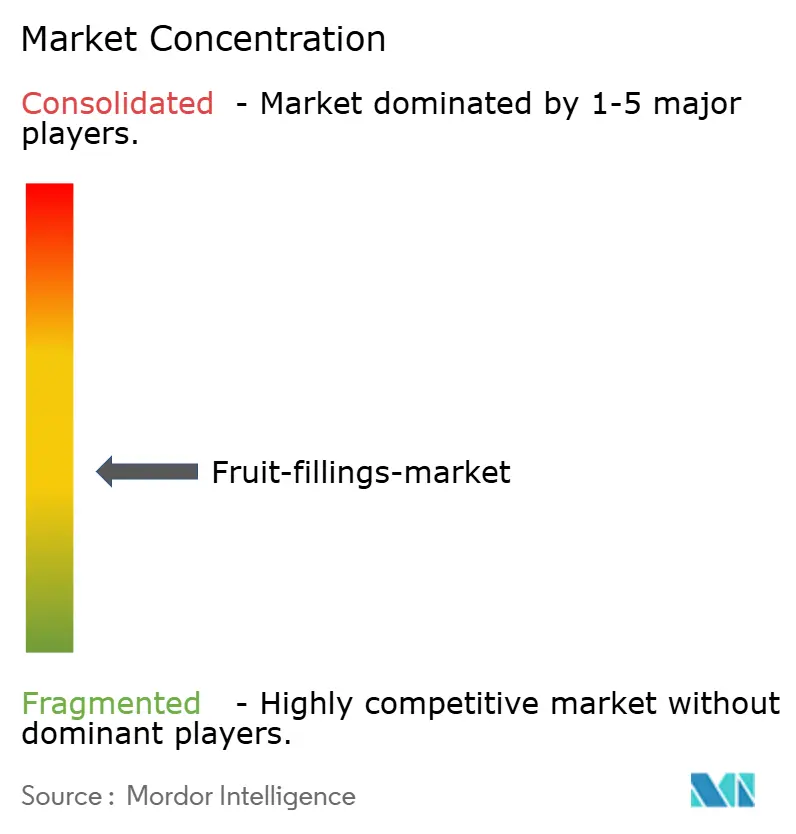

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fruit Fillings Market Analysis by Mordor Intelligence

The global fruit fillings market demonstrated robust performance by reaching USD 1.86 billion in 2025 and is expected to achieve a market size of USD 2.41 billion by 2030, maintaining a steady compound annual growth rate (CAGR) of 5.29%. The market's resilience stems from its integral role in food processing operations, particularly as consumer preferences shift toward convenient food options and products with clean-label ingredients. However, the industry faces significant operational challenges across its supply chain network. Orange juice futures have escalated to unprecedented levels, primarily due to the widespread impact of citrus greening disease and unpredictable weather patterns affecting crop yields [1]Source: American Farm Bureau Federation, “Orange Prices,” fb.org. The situation is further complicated in the European and Turkish markets, where cherry producers have reported substantial losses ranging from 70-80% of their harvests, attributed to devastating spring frost conditions that have severely impacted production capabilities.

Key Report Takeaways

- By type, Without Pieces commanded 55.83% of fruit fillings market share in 2024, whereas With Pieces is projected to log a 5.78% CAGR through 2030.

- By fruit category, Berries led with 51.05% share in 2024; Tropical Fruits are set to expand at a 5.98% CAGR between 2025-2030.

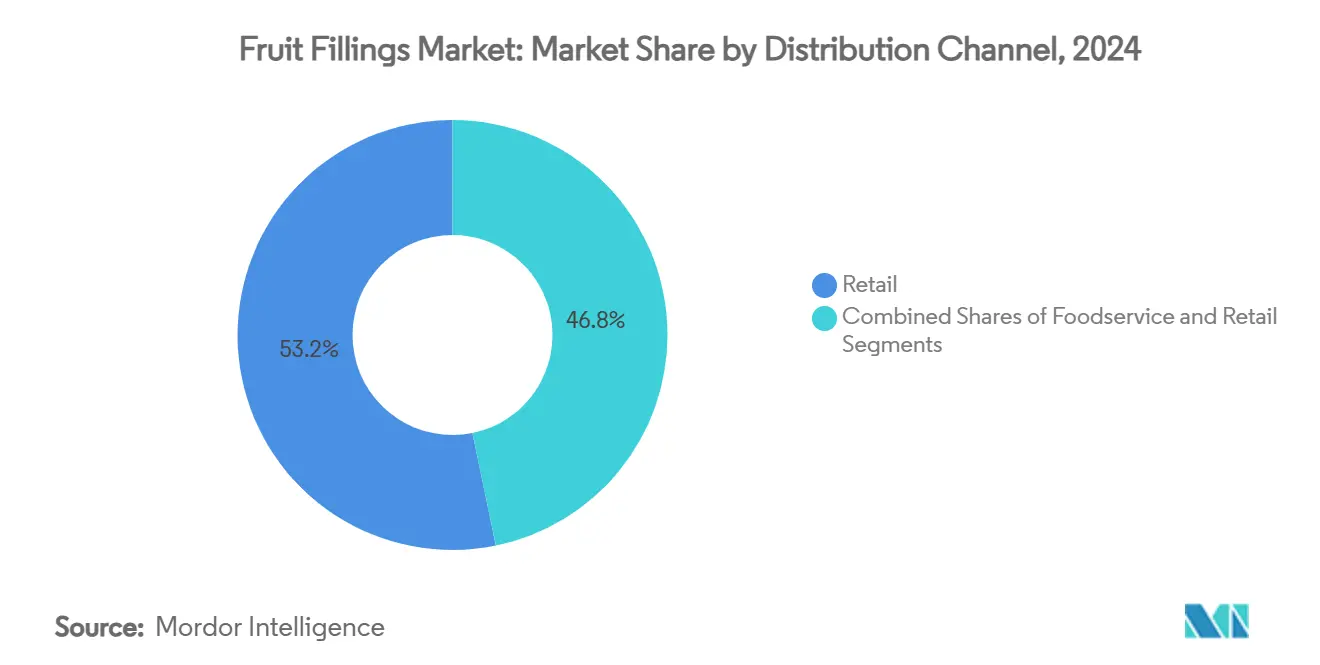

- By distribution channel, Retail accounted for 53.22% of the fruit fillings market size in 2024, while Foodservice is advancing at a 6.01% CAGR to 2030.

- By geography, North America held 37.19% share in 2024; Asia-Pacific registers the highest 6.14% CAGR through 2030

Global Fruit Fillings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenient, ready-to-eat and ready-to-bake food products | +1.2% | North America, Europe | Medium term (2-4 years) |

| Driving demand for low-sugar, natural, and organic fruit fillings | +0.9% | North America, Europe, APAC | Long term (≥ 4 years) |

| Expansion of bakery, confectionery, and dairy industries | +1.1% | APAC core, MEA & South America spill-over | Medium term (2-4 years) |

| Product innovation with new flavors, textures, and functional ingredients | +0.8% | Global | Short term (≤ 2 years) |

| Rising preference for natural colors and sweeteners | +0.7% | North America & EU | Long term (≥ 4 years) |

| Increasing popularity of artisanal and gourmet bakery products | +0.6% | Europe & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for convenient, ready-to-eat and ready-to-bake food products

Quick-service restaurants have strategically incorporated fruit ingredients into their menu offerings, with major players like McDonald's and Wendy's actively including fresh fruit portions in their value meals, demonstrating a significant shift toward fast and nutritious food options. The market has witnessed growing consumer demand for single-serve snacks featuring citrus and berry flavors, particularly resonating with health-conscious Millennial parents seeking convenient yet wholesome treats for their families. Industrial bakeries have adapted to market demands by utilizing advanced shelf-stable fillings that effectively maintain product quality throughout complex distribution networks. The implementation of Individually Quick Frozen (IQF) technology has revolutionized the preservation of color and texture in fruit fillings, enabling their versatile application across various baked goods, from traditional doughnuts to convenient hand-held pies. These market developments have firmly established the fruit fillings segment as an essential component of the global convenience food supply chain, fostering sustained demand across retail outlets, foodservice establishments, and industrial manufacturing sectors.

Driving demand for low-sugar, natural, and organic fruit fillings

Growing consumer concerns about artificial ingredients are driving increased demand for clean-label fruit fillings, with a significant portion of the consumer base expressing apprehension about the safety of artificial preservatives. This market shift has encouraged advancements in natural preservation methods, as demonstrated by Kemin Industries' introduction of Shield V, which combines buffered vinegar and botanical extracts to prevent mold growth while preserving product quality. The FDA's recent approval of natural color additives, including butterfly pea flower extract and Galdieria blue, provides manufacturers with natural alternatives to synthetic dyes. These natural colors play an essential role in fruit fillings, where color consistency influences consumer acceptance. The regulatory approvals facilitate the industry's transition toward natural ingredients while addressing preservation and stability requirements.

Expansion of bakery, confectionery, and dairy industries

The global bakery industry's substantial valuation in North America demonstrates strong demand that benefits fruit fillings suppliers, particularly as manufacturers focus on premium and health-conscious products. Puratos's Taste Tomorrow research identifies three key trends for 2025: significant growth in sourdough interest, expansion in culinary fusion, and increased consumer preference for nutritionally balanced chocolate products. The dairy segment shows considerable potential, with a majority of US consumers experimenting with exotic fruit flavors such as mango and guava. Strawberry, blueberry, and raspberry remain the primary fruit ingredients in dairy applications. Industry consolidation, exemplified by Emmi Group's substantial acquisition of Mademoiselle Desserts, aims to strengthen their premium desserts market position, necessitating enhanced fruit filling production capabilities to support French-inspired product innovations.

Product innovation with new flavors, textures, and functional ingredients

The fruit fillings market is experiencing rapid innovation as manufacturers adapt to emerging social media flavor trends and increasing consumer health awareness. White peach has established itself as a prominent flavor choice in the market, with substantial product launches recorded globally during the first half of the year, predominantly in beverages, yogurts, desserts, and ice creams. This flavor offers a naturally sweet and floral profile that meets consumer preferences for indulgence without additional sugar. Manufacturers are also developing functional ingredients, such as CherryShield, a maltodextrin-free, high-fiber fruit powder produced from Danish Stevnsbaer cherries. This ingredient provides enhanced health benefits, including polyphenols that support disease prevention and gut health. New processing technologies are enabling texture innovations in the market. For instance, Provisur Technologies has developed modular systems for fruit compote production that maintain product quality while achieving industrial-scale production. These technological improvements enable manufacturers to produce fruit fillings with enhanced textures and functional attributes at commercial scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and labeling regulations | -0.8% | Global, with highest compliance costs in North America and EU | Long term (≥ 4 years) |

| Challenges in maintaining product quality and consistency | -0.6% | Global, particularly affecting smaller manufacturers | Medium term (2-4 years) |

| Perishability of raw fruits leading to waste and cost inefficiencies in production | -0.5% | Global, with acute impact in regions with limited cold chain infrastructure | Short term (≤ 2 years) |

| Technological barriers in developing clean-label yet stable fruit fillings | -0.4% | Global, with higher barriers in developing markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety and labeling regulations

Food safety regulations are becoming more stringent across major markets, with governments implementing strict standards and labeling requirements that increase compliance costs and market entry barriers. In the United States, the FDA's Current Good Manufacturing Practice regulations (21 CFR Part 110) establish specific requirements for fruit fillings manufacturing, covering personnel hygiene, plant maintenance, equipment sanitation, and production controls[2]Source: U.S. FDA, “21 CFR Part 120—HACCP Systems,” ecfr.gov. The Safe Food for Canadians Act mandates detailed labeling requirements for processed fruit products, including standards of fill, nutritional information, and country of origin declarations, along with specific grading systems such as Canada Fancy and Canada Choice [3]Source: Government of Canada, “Labelling Requirements for Processed Fruit,” inspection.canada.ca. The Hazard Analysis and Critical Control Point (HACCP) systems under 21 CFR Part 120 require processors to identify food hazards, implement control measures, and maintain detailed records, including pathogen reduction processes that must achieve a 5-log reduction. These comprehensive regulatory requirements create entry barriers for smaller manufacturers while favoring established companies with existing compliance systems, which may lead to market consolidation.

Challenges in maintaining product quality and consistency

Quality consistency in fruit fillings faces challenges due to variations in agricultural raw materials and the complexity of maintaining natural fruit properties during processing. The high sugar content and moisture levels in fruit fillings make them susceptible to fungal contamination, necessitating robust preservation methods that align with clean-label requirements. Consumer preferences are shifting away from traditional preservatives like potassium sorbate and sodium benzoate, compelling manufacturers to adopt advanced technologies such as high-pressure processing, pulsed electric fields, and plant-based preservation systems. These technological implementations require substantial capital investments and specialized technical expertise. Raw material price volatility continues to impact production costs and operational planning, as demonstrated by the significant increase in global cocoa prices affecting Barry Callebaut's business operations. The perishable nature of fruits creates additional operational complexities, requiring efficient inventory management systems and temperature-controlled logistics infrastructure, which poses particular challenges for smaller manufacturers with limited resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Texture Preferences Drive Market Evolution

The Without Pieces segment dominated the market with a 55.83% share in 2024, demonstrating strong consumer acceptance across mainstream food applications. This preference for smooth, consistent textures particularly manifests in everyday products such as yogurt, ice cream, and mass-market baked goods, where manufacturing standardization and cost efficiency remain crucial factors.

In contrast, the With Pieces segment is experiencing robust growth at a 5.78% CAGR through 2030, capitalizing on evolving consumer preferences for premium food experiences. This growth is primarily fueled by artisanal positioning strategies that emphasize authentic fruit content and natural ingredients. The distinct textural characteristics create clear market differentiation, where smooth fillings optimize production efficiency and cost control, while fruit pieces enable manufacturers to implement premium pricing strategies based on perceived quality and natural product attributes.

By Fruit Category: Tropical Surge Challenges Berry Dominance

Berries continue to dominate the market landscape with a substantial 51.05% market share in 2024. This strong position stems from well-established supply chain networks and deep-rooted consumer familiarity with berry products. Meanwhile, the tropical fruits segment demonstrates remarkable momentum, advancing at a CAGR of 5.98% through 2030, as consumers increasingly embrace diverse flavor profiles and international taste experiences.

Stone fruits and citrus segments maintain their intermediate market positions, though citrus faces notable supply chain challenges due to the Mediterranean region's outsized influence on global production and trade flows. The tropical fruits category's acceleration reflects calculated moves by processors to capitalize on the Asia-Pacific region's emergence as the primary driver of global fruit import demand. However, the pineapple supply chain encounters significant challenges as El Niño weather patterns impact major producing nations, including Indonesia, Thailand, Vietnam, and the Philippines, affecting overall market dynamics.

By Distribution Channel: Foodservice Momentum Accelerates

Retail distribution maintained its dominant position with a 53.22% market share in 2024, building on well-established consumer purchasing behaviors and robust supply chain infrastructure. The foodservice segment demonstrates strong growth potential, with projections indicating a 6.01% CAGR through 2030, primarily influenced by the ongoing recovery in the restaurant industry and continuous innovations in menu offerings.

Industrial applications, encompassing diverse segments such as bakery and pastry, dairy and frozen desserts, confectionery, and beverages, represent the most substantial volume opportunity in the market, despite commanding lower per-unit prices. This preference stems from manufacturers' emphasis on maintaining consistent quality and functional performance rather than premium positioning. The notable growth in the foodservice segment reflects fundamental changes in consumer dining preferences, particularly evident in quick-service restaurants expanding their fresh fruit selections. Additionally, operators are increasingly implementing convenience solutions designed to preserve product quality during extended holding periods, addressing the practical challenges of food service operations.

Geography Analysis

North America commands a substantial 37.19% market share in 2024, demonstrating its dominance in the global market. This leadership position stems from the region's sophisticated food processing infrastructure and well-established consumer preferences for convenience foods. The market's strength is underscored by significant industrial investments, with over USD 700 million allocated to new food and beverage projects planned for January 2025. Major developments include Agristo's USD 450 million processing facility in Grand Forks, North Dakota, and a USD 410 million bakery manufacturing facility in Lancaster, Texas. However, the region faces notable challenges, including declining US orange production due to citrus greening disease and extreme weather impacts. Michigan's tart cherry market continues to navigate competition from Turkish imports while managing weather volatility and pest pressures. The USDA has responded proactively by implementing initiatives to strengthen food systems through enhanced local production and climate-smart agricultural practices.

Asia-Pacific has emerged as the fastest-growing region, projecting a robust 6.14% CAGR through 2030. This exceptional growth rate positions the region as the primary engine of market expansion, driven by its increasing role as the global hub for fruit and vegetable imports. The region's development is further accelerated by substantial investments in processing technology, exemplified by strategic partnerships such as OctoFrost's collaboration with Mekong Delta Gourmet in Vietnam for advanced IQF processing capabilities. Additionally, leading Indian processors are making significant investments in freezing technology, particularly for products like mangoes, demonstrating the region's commitment to technological advancement in food processing.

Europe has successfully navigated through price inflation challenges in its processed fruit and vegetable market, securing 47% of global imports by value in 2023. The region's market is led by key importers including Germany, the Netherlands, and the UK. Europe's market strength is reinforced by its focus on sustainability and organic products, with Germany establishing itself as the largest market for organic processed fruit. Consumer preferences for locally-sourced ingredients continue to drive premium positioning strategies across the region. The Mediterranean citrus industry maintains its significance as a leading exporter of easy-peeler fruits, contributing approximately 20% of world citrus production, despite ongoing challenges from diseases such as Citrus tristeza virus and Huanglongbing.

Competitive Landscape

The fruit fillings market demonstrates moderate concentration with a fragmented structure, creating diverse opportunities within the industry. This market environment enables established companies to pursue strategic consolidation while allowing niche players to carve out specialized market segments. The fragmented nature of the market provides flexibility for various business models and operational approaches to coexist and succeed.

Major companies are actively pursuing vertical integration strategies to strengthen their supply chain control and enhance their market position. A notable example is Dawn Foods' strategic acquisition of Royal Steensma's operations, which included four manufacturing facilities in the Netherlands and one in Thailand. This expansion has significantly enhanced Dawn Foods' production capabilities and international presence. In parallel, companies are investing in technological advancement as a key differentiator, implementing automation systems and AI-driven analytics to optimize their operations. Barry Callebaut's implementation of the BC Next Level program illustrates how companies are adapting to market challenges, maintaining operational excellence even during periods of commodity price volatility.

The market presents several untapped opportunities, particularly in developing clean-label preservation technologies and creating innovative exotic fruit flavor profiles. The expansion potential in emerging markets remains significant, offering new growth avenues for industry participants. Recent regulatory developments, such as the FDA's approval of natural color additives, have opened new possibilities for product formulation. These regulatory changes have created an environment where smaller, innovative companies can develop unique products and effectively challenge established market positions, contributing to the dynamic nature of the industry.

Fruit Fillings Industry Leaders

Puratos Group

Agrana Beteiligungs-AG

Dawn Food Products

Tate & Lyle PLC

Cargill Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Tate & Lyle completed the USD 1.8 billion acquisition of CP Kelco, creating a leading global specialty food and beverage solutions business with enhanced capabilities in sweetening, mouthfeel, and fortification, particularly strengthening pectin and nature-based ingredients portfolio.

- October 2024: Emmi Group completed the acquisition of Mademoiselle Desserts for approximately USD 973 million, doubling its sales share in the premium desserts market from 9% to 17% and establishing a leading global position in French-inspired dessert products.

- June 2024: Dawn Foods acquired Royal Steensma, a Dutch bakery ingredients manufacturer specializing in fruit fillings, including four manufacturing plants in the Netherlands and a facility in Thailand, significantly expanding Dawn's global manufacturing capabilities.

Global Fruit Fillings Market Report Scope

| With Pieces |

| Without Pieces |

| Berries |

| Citrus |

| Stone Fruits |

| Tropical Fruits |

| Others |

| Industrial | Bakery and Pastry |

| Dairy and Frozen Desserts | |

| Confectionery | |

| Beverages and Smoothies | |

| Others | |

| Foodservice | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | With Pieces | |

| Without Pieces | ||

| By Fruit Category | Berries | |

| Citrus | ||

| Stone Fruits | ||

| Tropical Fruits | ||

| Others | ||

| By Distribution Channel | Industrial | Bakery and Pastry |

| Dairy and Frozen Desserts | ||

| Confectionery | ||

| Beverages and Smoothies | ||

| Others | ||

| Foodservice | ||

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the global value of the fruit fillings market in 2025?

It reached USD 1.86 billion, with projections indicating USD 2.41 billion by 2030 at a 5.29% CAGR.

Which segment leads by fruit type?

Without Pieces variants held 55.83% share in 2024, appealing to manufacturers seeking smooth textures and processing efficiency.

Which geography is expanding fastest?

Asia-Pacific is forecast to post the highest 6.14% CAGR through 2030, propelled by urbanization and growing cold-chain capacity.

How are clean-label demands shaping formulations?

Producers are replacing synthetic preservatives and colors with natural antimicrobials, pectins, and plant-based pigments, driving low-sugar and organic options.

What growth opportunity exists for tropical fruit processors?

Rising consumer interest in mango, guava, and passion fruit fillings is pushing tropical fruit CAGR to 5.98%, creating export opportunities into Europe, North America, and the Middle East.

Page last updated on: