Mango Puree Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

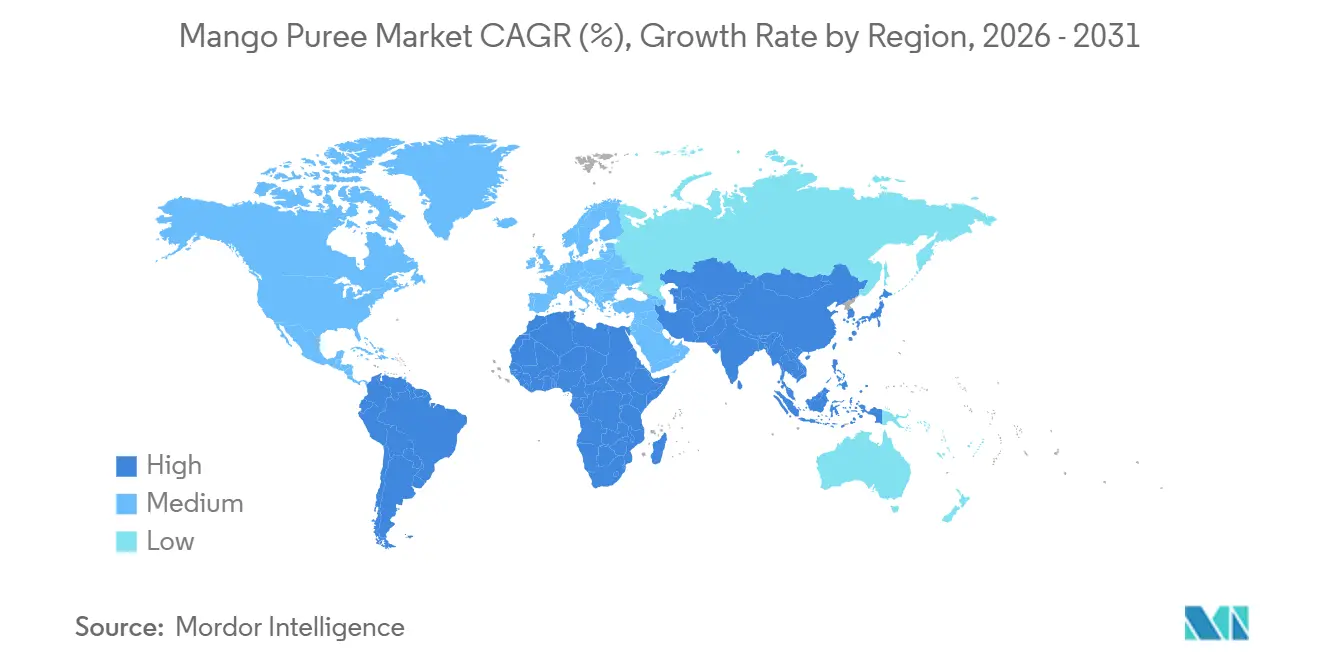

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

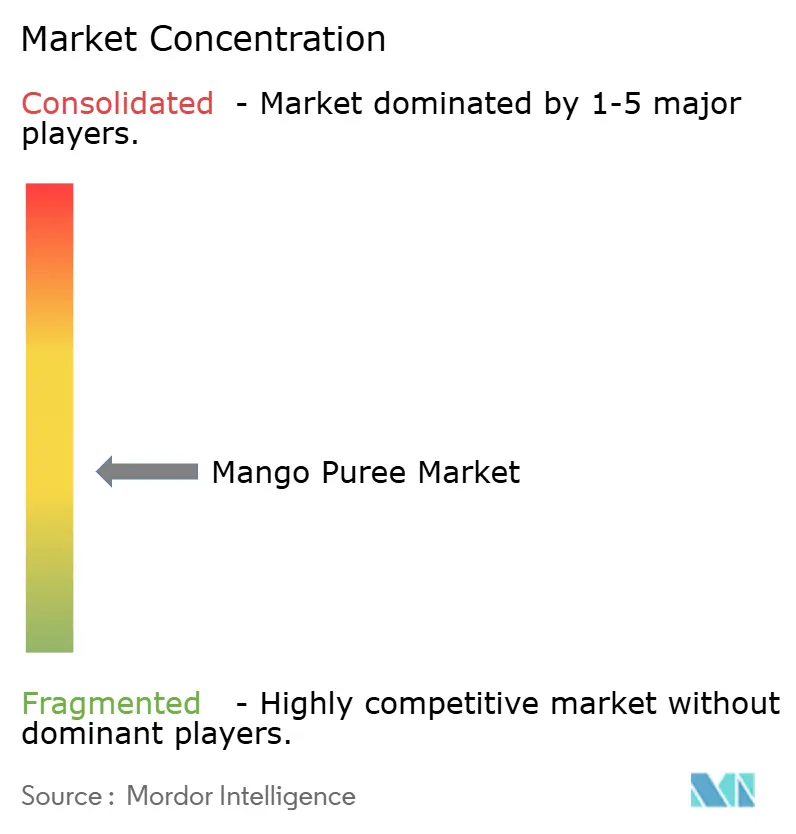

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mango Puree Market Analysis by Mordor Intelligence

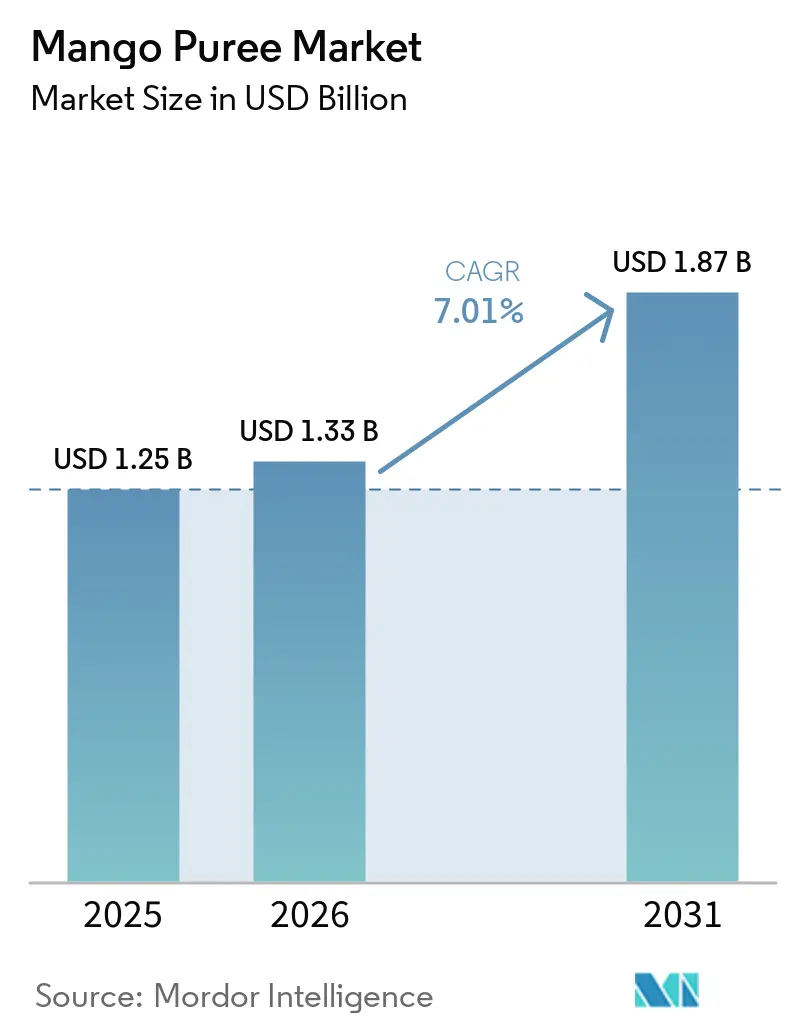

The mango puree market size was valued at USD 1.25 billion in 2025 and is estimated to grow from USD 1.33 billion in 2026 to reach USD 1.87 billion by 2031, at a CAGR of 7.01% during the forecast period (2026-2031). Growth is driven by the adoption of aseptic processing, increasing use in industrial beverage formulations, and rising demand for clean-label ingredients. Investments in quick-freezing and ozonated-water treatments are reducing waste and improving product quality. Expanding applications in baby food, functional beverages, and plant-based desserts are diversifying revenue streams. Producers are enhancing resilience by converting surplus harvests into long-shelf-life purées through regional processing hubs. Competitive dynamics are shaped by advancements in technology and organic certifications, which are critical for premium shelf positioning and export compliance.

Key Report Takeaways

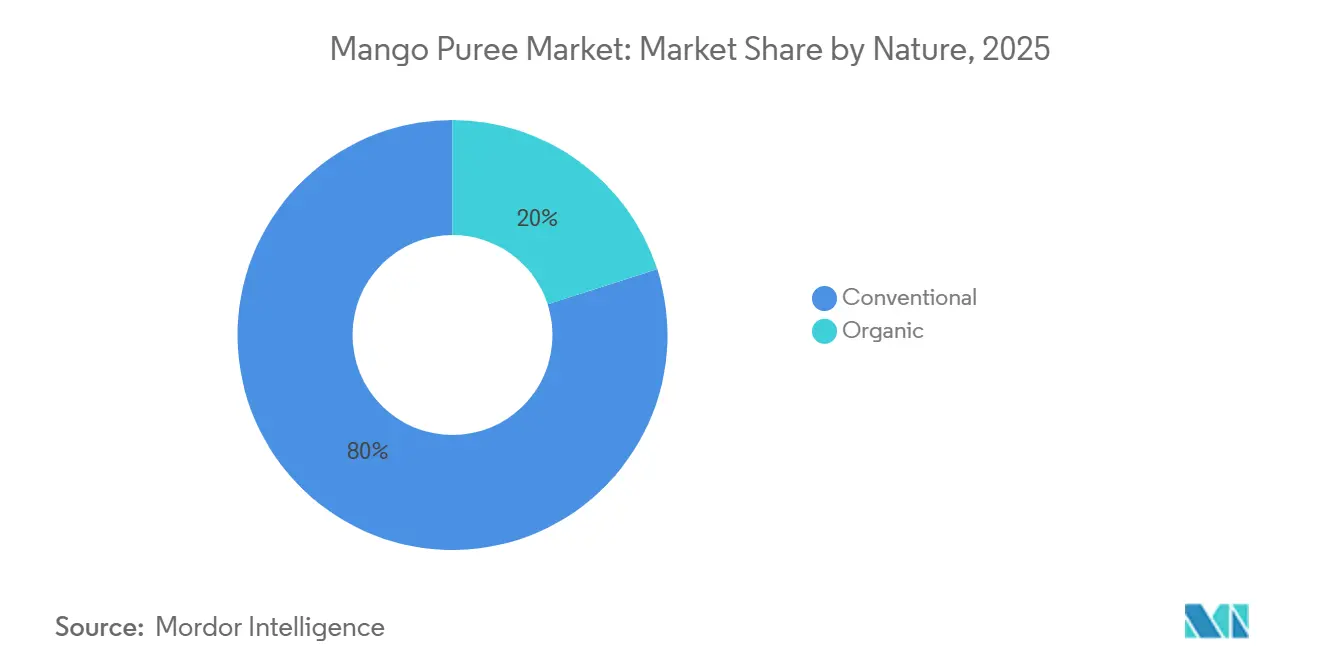

- By nature, conventional purée secured 79.96% of the mango puree market share in 2025, whereas the organic segment is poised to record the fastest 8.93% CAGR through 2031.

- By packaging, cans led the mango puree market size with a 52.33% revenue contribution in 2025, yet bottles are projected to advance at a 7.45% CAGR over 2025-2031.

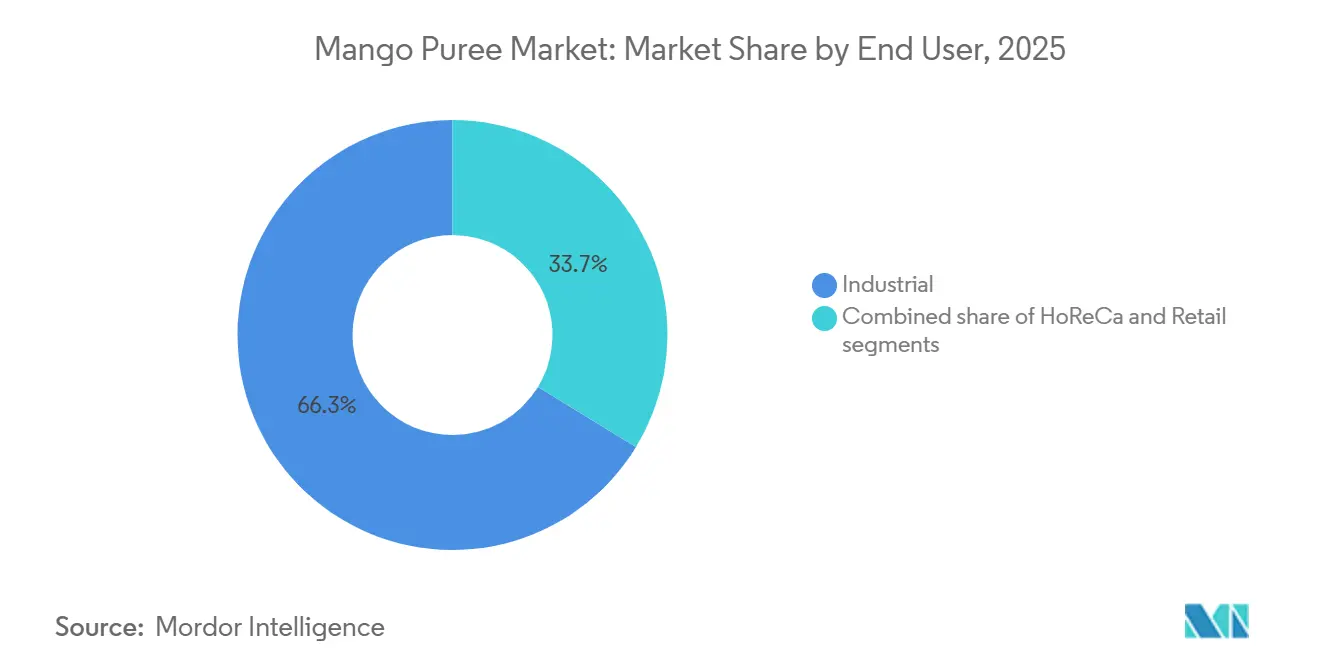

- By end user, industrial applications captured 66.29% of the mango puree market in 2025, while retail channels are on track for the highest 9.32% CAGR to 2031.

- By geography, Asia-Pacific commanded 38.45% of the mango puree market in 2025; the Middle East and Africa region is set to expand at an 8.23% CAGR during the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mango Puree Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer interest in exotic and tropical flavors | +1.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Increased use in baby and health foods | +1.2% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Product innovation and diversification | +1.5% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Technological advancements in processing and packaging | +0.8% | APAC core, spill-over to other regions | Medium term (2-4 years) |

| Rising consumer demand for natural and minimally processed foods | +0.6% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Regulatory push for natural ingredients | +0.4% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer interest in exotic and tropical flavors

The growing preference for exotic flavors is significantly influencing product development in the food and beverage sectors, with mango emerging as a standout ingredient for manufacturers aiming to differentiate their offerings. Golden mango, in particular, is anticipated to dominate flavor trends in 2025, especially within the functional beverage category. Its tropical profile enhances the appeal of hydration drinks and smoothies, making it a preferred choice for health-focused innovations. This trend is not limited to traditional applications; for example, Pure Finest Inc. has introduced a premium beverage line, "Tropical Bliss," that prominently features mango to appeal to health-conscious consumers in the United Kingdom and across European markets. The versatility of mango flavor allows manufacturers to explore both sweet and savory applications, unlocking opportunities in unconventional categories. Products such as chili-lime mango snacks are gaining traction among adventurous consumers seeking unique taste experiences. European markets, including the Netherlands, the United Kingdom, and Germany, are witnessing a rise in mango puree imports, driven by its growing use in beverage formulations. This shift in consumer preferences is encouraging manufacturers to adopt premium positioning strategies, as mango puree commands higher profit margins compared to traditional fruit ingredients, further solidifying its role as a valuable component in product innovation.

Increased use in baby and health foods

The integration of mango puree into infant nutrition is emerging as a significant growth driver, supported by its robust nutritional profile and compliance with stringent safety regulations. Several studies indicate that mango consumption increases nutrient intake and improves diet quality, particularly among women of childbearing age and older adults, reinforcing its potential for use in health-oriented products. The USDA's Commercial Item Description for frozen fruit purees ensures consistent quality by mandating specific °Brix levels (13.5 for single strength and 28.5 for concentrated) and pH ranges (3.9-4.2) for mango puree, making it a reliable ingredient for baby food applications. European markets are experiencing a notable rise in demand, as baby food manufacturers capitalize on mango puree's natural sweetness to reduce added sugars while maintaining an appealing taste profile. The puree's high carotene and vitamin C content aligns with global health initiatives promoting natural and nutrient-rich food sources, creating opportunities for manufacturers to develop premium infant nutrition products. Additionally, the growing recognition of mango's polyphenol content and antioxidant properties is driving its adoption in functional foods. These products, particularly those targeting digestive health and immune system support, are gaining traction in the adult health segment, further expanding the market potential for mango puree.

Product innovation and diversification

Advanced processing technologies are driving a surge in manufacturing innovation, boosting product quality and broadening application horizons. Companies are harnessing heat pump drying technology to craft mango powders, successfully retaining bioactive compounds and slashing defect rates by over 90% through enhanced colloid mill and homogenizer techniques. The infusion of probiotics, notably Lactobacillus casei, into mango puree is carving out fresh market niches, with ideal processing parameters set at a 40°C drying temperature and a 10% probiotic concentration. Thanks to aseptic processing, manufacturers can now produce shelf-stable items that don't need refrigeration, broadening distribution avenues and cutting logistics expenses. SIG is pioneering packaging solutions for juice drinks, rolling out specialized aseptic cartons and spouted pouches tailored for mango puree, catering to both on-the-go and home consumers. Meanwhile, Provisur Technologies is revolutionizing the game, unveiling advanced systems for premium fruit compotes and purees, with their STS series boosting both throughput and quality oversight.

Technological advancements in processing and packaging

The evolution of processing technology is transforming the mango puree value chain by optimizing production economics and raising product quality standards. Companies such as OctoFrost are leveraging advanced IQF (Individually Quick Frozen) systems through strategic partnerships in Vietnam, enabling cost-efficient operations while ensuring consistent product quality for tropical fruit processing. Ozonated water treatment has emerged as a significant innovation, extending mango storage life by up to 2 weeks and reducing chilling injuries by 40%, thereby addressing critical vulnerabilities in the supply chain [1]Source: Edith Cowan University, "From orchard to fridge: Helping mangoes stay sweet for longer", ecu.edu.au. In addition, the integration of vacuum deaerators in puree production lines is improving product quality by effectively removing air bubbles, while high-capacity processing equipment, capable of handling 3,000 kg/h, is driving large-scale production efficiency. Automated mango peeling and destoning machines, with the ability to process up to 20 fruits per minute, are significantly reducing labor dependency while maintaining uniform quality standards. These advancements are not only establishing new benchmarks for processing efficiency and product quality but are also providing a competitive edge to early adopters, positioning them as leaders in the evolving industry landscape.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal and limited mango supply | -0.9% | Global, particularly acute in APAC and Latin America | Short term (≤ 2 years) |

| Short shelf life of certain puree formats | -0.7% | Global, with higher impact in regions with limited cold chain | Medium term (2-4 years) |

| Quality variation in raw mangoes | -0.5% | Global, with highest impact in emerging production regions | Medium term (2-4 years) |

| Competition from substitute ingredients | -0.4% | Global, particularly in cost-sensitive applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seasonal and limited mango supply

Supply seasonality leads to persistent volatility, hindering market expansion and complicating production planning for manufacturers reliant on steady raw material availability. Industry representatives have dubbed Peru's 2024-2025 mango season as the "worst in history." Extreme weather events slashed export volumes by 65-80% and propelled prices to record highs. In China, domestic mango supply constraints, with Hainan accounting for the bulk of the 20,000 metric tons produced, pushed prices up to 11.5 yuan (USD 1.58) per kilogram in November 2024. This marked a 12.3% year-over-year increase. The global concentration of mango production poses systemic risks. With India holding a 50% share of global production, the entire supply chain becomes susceptible to monsoon patterns and climate fluctuations. To navigate these challenges, processing facilities are adopting strategic inventory management. Aseptic processing, which allows for extended storage, is bridging seasonal gaps. However, this method demands hefty investments in specialized equipment and storage infrastructure. Furthermore, developing counter-seasonal sourcing strategies across different hemispheres is becoming essential for ensuring a consistent year-round supply. This necessity is fostering collaborations between processors and growers situated in complementary growing regions.

Short shelf life of certain puree formats

Product degradation timelines significantly impact distribution strategies and inventory management, particularly in regions with inadequate cold chain infrastructure, thereby hindering market penetration. Canned mango products exhibit excellent shelf stability, retaining quality for 1-2 years beyond their expiration dates when stored at optimal temperatures of 50-70°F (10-21°C). However, once opened, these products must be consumed within a week to avoid spoilage. In contrast, fresh and minimally processed mango formats face greater challenges, with postharvest losses reaching up to 50% due to rapid ripening and vulnerability to diseases during handling and storage. These formats require continuous cold chain maintenance, which introduces logistical complexities and escalates costs, further limiting market accessibility in developing regions. To address these issues, advancements in processing technologies, such as polysaccharide edible coatings and leaf extracts, are being implemented to extend shelf life while maintaining the natural appeal of the products. The economic implications extend beyond direct product losses, as supply constraints often lead to stagnant retail sales. For example, during periods of shortages, organic mango prices can rise significantly, reaching USD 17-18 per carton, reflecting the strain on supply chains and the broader market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Conventional Infrastructure Advantage

In 2025, conventional mango puree holds a dominant 79.96% market share, driven by a strong processing infrastructure and cost-efficient strategies that ensure a stable supply for industrial applications. Mature agricultural practices and standardized systems further support this segment. For instance, Villa Puree in Brazil utilizes its production networks in São Paulo and Minas Gerais to deliver consistent yellow mango pulp through processes like classification, sorting, pasteurization, and aseptic packaging. India, producing 50% of the world's mangoes, provides conventional processors with a steady raw material supply and economies of scale, enabling competitive pricing. The segment effectively manages seasonal supply fluctuations through diversified sourcing and strong grower partnerships. Companies are improving profitability by adopting multi-fruit processing lines, optimizing utilization rates, and maintaining high-quality standards for industrial clients.

Organic mango puree is experiencing significant growth, with an 8.93% CAGR projected from 2026 to 2031. This growth is fueled by premium positioning and regulatory support for natural ingredients in key markets. The USDA's National Organic Program requires a three-year transition free from prohibited substances, creating supply constraints that drive premium pricing but also demand substantial certification investments. Companies like Pure Indian Foods are leveraging this trend by promoting organic Alphonso mango puree, emphasizing traditional cultivation and superior flavor to position it as a high-margin premium product. Tradin Organic's initiative in Burkina Faso highlights the shift toward value-added processing, creating 400 jobs and reducing food waste by utilizing lower-grade mangoes. Additionally, the USDA reports a robust infrastructure with over 14,000 certified organic flavor products, reinforcing organic mango puree's potential in premium food and beverage markets[2]Source: United States Department of Agriculture, National Organic Program Document Cover Sheet, ams.usda.gov.

By Packaging: Can Dominance Through Industrial Efficiency

In 2025, canned packaging dominates with a 52.33% market share, driven by its shelf stability and cost efficiency, which meet industrial application demands. Its ability to preserve product quality for 1-2 years beyond expiration at optimal storage temperatures (50-70°F or 10-21°C) ensures supply chain flexibility and reduces inventory risks. Industrial sectors, particularly beverage manufacturing, prefer canned formats for their bulk packaging and processing efficiency, essential for managing large volumes and cost optimization. Compliance with USDA standards for aseptic fruit purees, including minimum °Brix levels (13.5 for single strength, 28.5 for concentrated forms) and pH ranges (3.9-4.2), further supports the adoption of canned systems. Additionally, established supply chains and standardized production processes enable economies of scale, offering manufacturers cost advantages and efficient bulk distribution.

Bottle packaging is set to grow at a 7.45% CAGR from 2026 to 2031, fueled by consumer demand for portion control and premium product positioning in retail. Innovations like SIG's specialized bottle solutions for juice-based drinks cater to on-the-go and at-home consumption, aligning with lifestyle trends emphasizing convenience and aesthetics. Sustainability trends also drive growth, with manufacturers introducing recyclable packaging and plant-based films to attract eco-conscious consumers. Aseptic processing extends shelf life without refrigeration, enhancing distribution flexibility and supporting premium pricing strategies. Retail expansion further boosts the segment, as visual merchandising and portion control appeal to consumers, particularly in health-focused categories like smoothies and functional beverages, where presentation influences brand perception.

By End User: Industrial Foundation Stability

In 2025, industrial applications dominate the market, holding a 66.29% share, due to established supply relationships and economies of scale that ensure revenue predictability for processors. This segment's prominence underscores the vital role of mango puree in beverage manufacturing, food production, and ingredient supply, where consistent quality and competitive pricing are essential. In regions like South Gujarat, caterers, eyeing price and taste, show a marked preference for bulk purchases directly from processors, highlighting the region's potential for mango pulp marketing. Industrial clients enjoy tailored formulations and unwavering quality standards, with processors bolstering these relationships through technical support and bespoke solutions. This stability allows for strategic long-term capacity planning and investment choices. Companies are now adopting multi-fruit processing lines, optimizing utilization rates, and ensuring a steady supply to industrial clients, even amidst seasonal fluctuations.

From 2026 to 2031, retail applications are set to surge at a 9.32% CAGR, fueled by a growing consumer appetite for convenient products in smoothies, desserts, and health-centric uses. The European market, particularly the Netherlands as a redistribution hub and the UK's penchant for baking and smoothies, according to the Government of Netherlands CBI report 2024, showcases the retail segment's strength [3]Source: Government of the Netherlands, "The European market potential for mango puree", cbi.eu. This segment spans beverages, infant food, bakery items, dairy, frozen desserts, and extends to sauces, dressings, snacks, and nutraceuticals, offering processors a rich tapestry of revenue streams. Retail's growth trajectory is bolstered by premium positioning, where portion-controlled packaging and unique formulations promise fatter margins than their industrial counterparts, incentivizing processors to pivot towards retail-centric product lines.

Geography Analysis

In 2025, Asia-Pacific commands a dominant 38.45% share of the global mango market, leveraging its status as the top mango producer and a burgeoning processing center. With India accounting for half of the world's mango output, the nation is not only bolstering its processing capabilities but also adopting cutting-edge agricultural methods and precision farming to boost yields. Meanwhile, Vietnam is carving a niche as a premium mango exporter. Tien Giang province, for instance, spans over 3,300 hectares, producing upwards of 50,000 tonnes annually for both local and global markets. Partnerships, such as OctoFrost teaming up with Vietnamese processors, underscore the region's commitment to elevating its processing standards, particularly in IQF capabilities for tropical fruits.

West Africa's production growth and infrastructure advancements are propelling the Middle East and Africa to the forefront, boasting an 8.23% CAGR from 2026 to 2031. Côte d'Ivoire is eyeing a 30,000-tonne output for the 2025 season, bolstered by enhanced phytosanitary measures to align with EU standards, signaling a strategic push towards export markets. Meanwhile, North America and Europe, reliant on imports, face challenges: the U.S. grappled with a 22% drop in import volumes in 2024, underscoring its sensitivity to fluctuations in source countries. South America, with Peru navigating seasonal hurdles and Brazil's robust processing framework backing firms like Villa Puree, showcases its prowess in the global mango landscape.

In North America, the mango puree market is driven by the growing demand for tropical fruit-based beverages, baby food, and clean-label ingredients. South America benefits from abundant mango cultivation, supporting both domestic consumption and export-oriented processing industries. The region's favorable climate and low-cost production enhance its competitiveness in the global supply chain. In Europe, increasing interest in exotic flavors and natural fruit products is fueling the use of mango puree across beverages, dairy, and dessert applications. Regulatory focus on organic and sustainable sourcing is also shaping procurement and product innovation in the region.

Competitive Landscape

Several regional and international players compete in the mango puree market, focusing on product quality, pricing, and supply chain efficiency. The market remains moderately fragmented, with no single player dominating, allowing multiple companies to wield comparable influence. Key players include Kiril Mischeff Ltd., Ingredion Inc., SVZ International B.V., Rani Brand Factory Store, and Kerry Group. These companies are bolstering their positions by expanding processing capacities, securing high-quality raw mangoes, and forging strategic export partnerships. Moreover, innovations in packaging and aseptic processing technologies have empowered smaller players to cater to global demand.

As consumer willingness to pay premium prices for quality and sustainability credentials rises, there's a notable opportunity in organic processing and premium positioning strategies. Emerging disruptors are addressing supply chain vulnerabilities by employing advanced preservation technologies, such as ozonated water treatment, which extends storage life by two weeks and reduces chilling injury by 40%.

Companies are differentiating themselves through aseptic processing capabilities, investing in specialized equipment to produce shelf-stable products without refrigeration. The USDA's Commercial Item Description specifications for aseptic fruit purees set stringent quality standards, such as minimum °Brix levels and pH ranges, favoring technologically advanced processors. Furthermore, strategic partnerships between equipment manufacturers and processors are reshaping the competitive landscape. For instance, companies like OctoFrost are forming technology transfer relationships, enhancing processing capabilities and providing market access advantages.

Mango Puree Industry Leaders

-

Kiril Mischeff Ltd.

-

SVZ International B.V.

-

Ingredion Inc.

-

Rani Brand Factory Store

-

Kerry Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SKOT INDIA has commenced production of its 2025 season Aseptic Alphonso Mango Puree, using the finest Alphonso mangoes known for their flavor and consistent quality. According to the company, the puree is 100% natural, free from added sugar, preservatives, or artificial flavors, and comes in both 215 kg aseptic drums and 3.1 kg cans to serve diverse market needs.

- January 2025: Sahyadri Farms partnered with the Centre of Excellence for FPOs (CoE-FPO) to strengthen over 1,460 Farmer-Producer Organizations in Karnataka, India. This cooperation focuses on boosting the quality and consistency of mango supply for the pulp and puree processing industry through value chain development and modern post-harvest management.

- January 2025: Lat Eko Food Ltd has expanded its product line with the launch of its new Organic Mango‑Banana‑Quince Puree at Gulfood 2025. According to the brand, it is a certified organic blend suitable for infants from 4+ months with an 18‑month shelf life.

- July 2024: Coca-Cola India, through its foundation Anandana, collaborated with Gram Unnati in Karnataka to launch Project Unnati Mango. The initiative aims to support the sustainable cultivation of Alphonso and Totapuri mango varieties, improving supply chain reliability for mango pulp and puree production while enhancing local farmer livelihoods.

Global Mango Puree Market Report Scope

The Mango Puree Market Report is Segmented by Nature (Conventional, Organic), Packaging (Cans, Pouches, Jars, Bottles, Others), End User (Industrial, Horeca, Retail), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional |

| Organic |

| Cans |

| Pouches |

| Jars |

| Bottles |

| Others |

| Industrial | |

| HoReCa | |

| Retail | Beverages |

| Infant Food | |

| Bakery and Confectionery | |

| Dairy and Frozen Desserts | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Nature | Conventional | |

| Organic | ||

| By Packaging | Cans | |

| Pouches | ||

| Jars | ||

| Bottles | ||

| Others | ||

| By End User | Industrial | |

| HoReCa | ||

| Retail | Beverages | |

| Infant Food | ||

| Bakery and Confectionery | ||

| Dairy and Frozen Desserts | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the mango puree market?

The mango puree market size is USD 1.25 billion in 2025 and is forecast to reach USD 1.87 billion by 2031.

Which region leads global demand?

Asia-Pacific holds 38.45% of revenue, benefiting from abundant raw-mango supply and expanding processing capacity.

Which segment is growing fastest?

Retail applications are projected to post a 9.32% CAGR through 2031 as consumer demand rises for smoothie-ready and baby-food purées.

How do technology upgrades influence competitiveness?

Investments in IQF freezing, aseptic bottling and automated peeling reduce waste, extend shelf life and deliver cost savings that strengthen processor margins.

Page last updated on: