North America Cold Pressed Juices Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

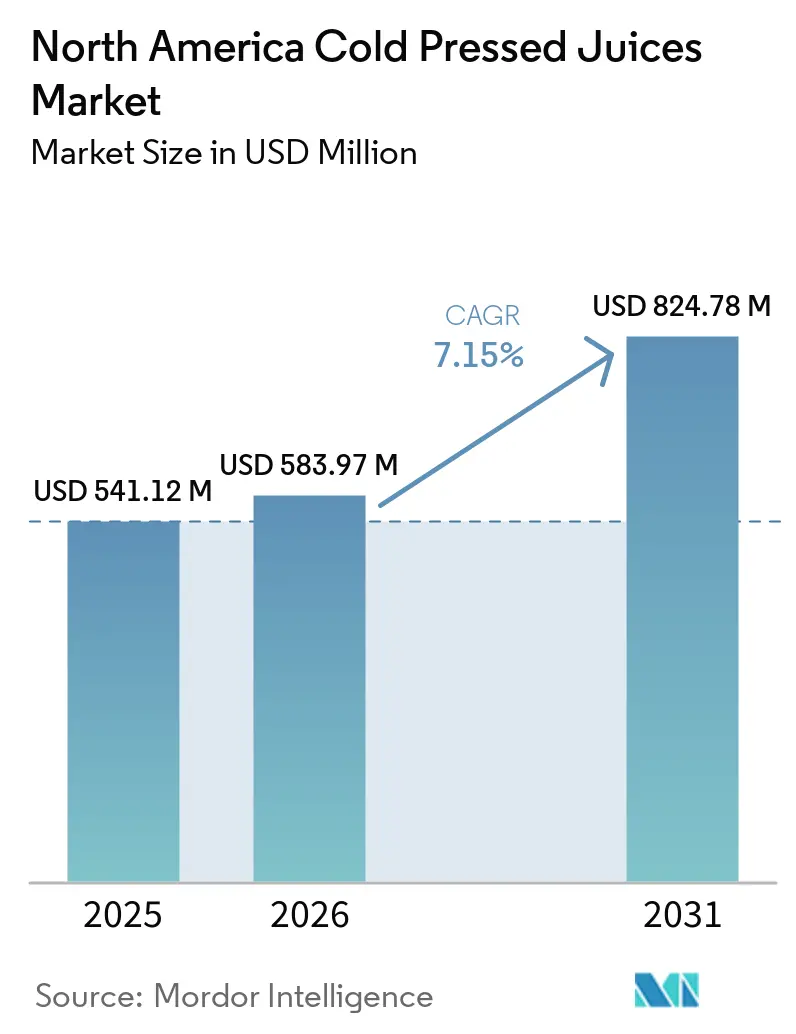

| Base Year Market Size (2025) | USD 541.12 Million |

| Market Size (2026) | USD 583.97 Million |

| Market Size (2031) | USD 824.78 Million |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Cold Pressed Juices Market Analysis by Mordor Intelligence

The North America cold pressed juice market size is expected to grow from USD 541.12 million in 2025 to USD 583.97 million in 2026 and is forecast to reach USD 824.78 million by 2031 at a 7.15% CAGR over 2026-2031. The North America cold-pressed juice market is driven by increasing consumer demand for clean-label, minimally processed beverages that preserve the natural nutrients, enzymes, and flavors of fresh fruits and vegetables. Growing awareness of preventive healthcare and functional nutrition has led consumers to replace carbonated soft drinks with nutrient-rich cold-pressed juices that promote immunity, digestion, hydration, and overall wellness. The rising preference for organic, plant-based, and preservative-free products is further boosting adoption, particularly among health-conscious millennials and urban professionals. Improved product accessibility through retail expansion in supermarkets, specialty health stores, and e-commerce platforms, along with advancements in high-pressure processing (HPP) technology, has extended shelf life without compromising nutritional quality, enabling broader distribution. Additionally, the popularity of juice cleanses, detox programs, and fitness-oriented lifestyles has increased demand for premium cold-pressed juices. Manufacturers are responding by introducing innovative blends with superfruits, vegetables, herbs, adaptogens, and functional ingredients to meet evolving consumer preferences. Efforts in sustainable packaging and transparent ingredient sourcing continue to build consumer trust and support sustained market growth.

Key Report Takeaways

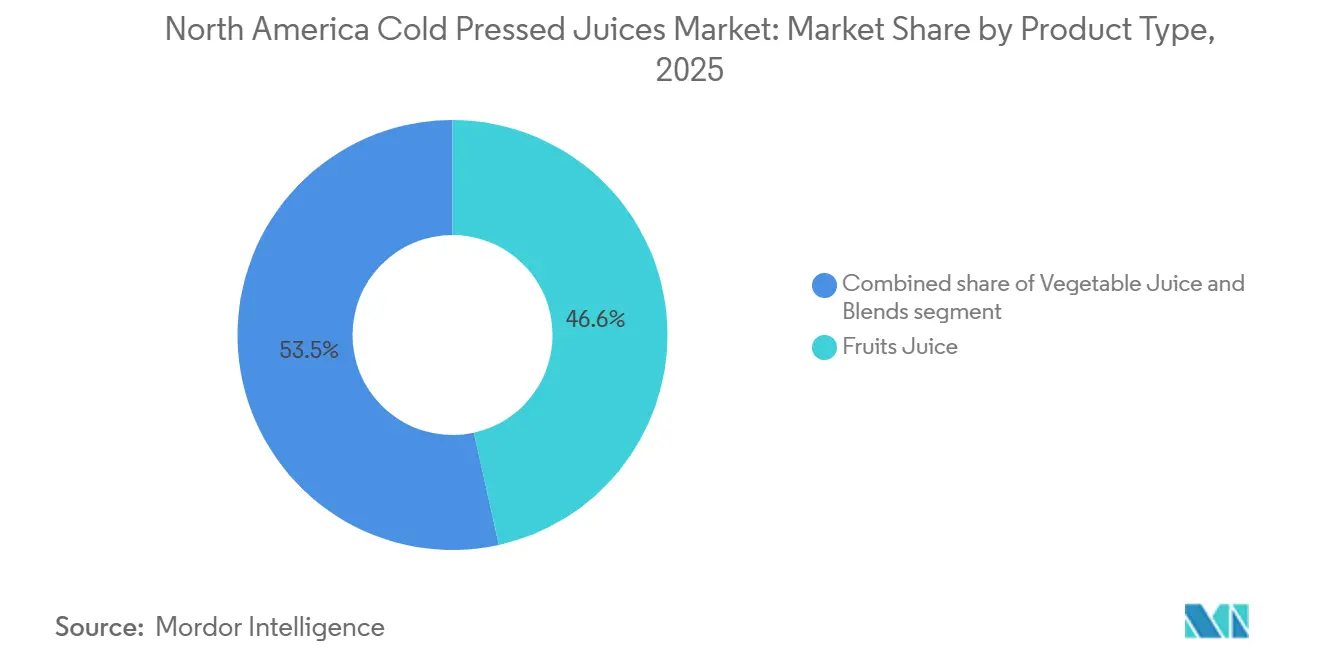

- By product type, fruit juice held 46.55% share of the North America cold-pressed juice market in 2025 across the region, while blends are forecast to record the fastest 8.13% CAGR during 2026-2031.

- By packaging type, PET bottles accounted for 45.77% of the 2025 regional value in the North America cold-pressed juice market, while recyclable-pouch/Tetra-Pak formats are projected to grow at the fastest 7.85% CAGR during 2026-2031.

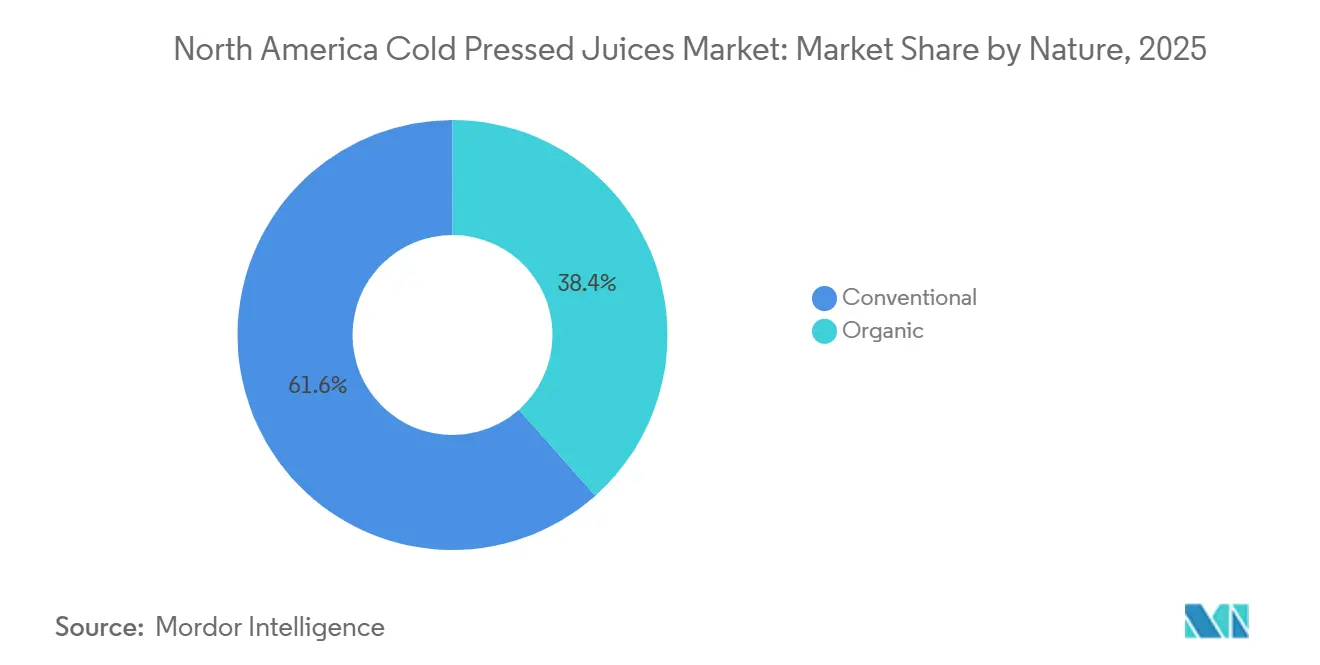

- By nature, conventional products represented 61.57% of 2025 demand across the North America cold-pressed juice market, while organic products are expected to post the highest 8.55% CAGR during 2026-2031.

- By distribution channel, off-trade held 62.45% of the 2025 North America cold-pressed juice market size and is forecast to expand at the fastest 8.73% CAGR during 2026-2031.

- By geography, the United States captured 88.46% of the North America cold-pressed juice market share in 2025, while Mexico is forecast to advance at the fastest 7.75% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Cold Pressed Juices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for clean-label and minimally processed beverages | +1.6% | North America, with highest concentration in United States coastal metros and Canadian urban centers | Medium term (2-4 years) |

| Increasing popularity of functional and immunity-boosting ingredients | +1.4% | United States, Canada | Short term (≤ 2 years) |

| Growing demand for organic and natural juice products | +1.1% | United States, Canada | Medium term (2-4 years) |

| Product innovation through unique ingredient blends and flavors | +0.9% | United States | Short term (≤ 2 years) |

| Growing popularity of plant-based and vegan diets | +0.6% | United States coastal cities, major Canadian metros | Long term (≥ 4 years) |

| Advancements in high-pressure processing (HPP) technology | +1.0% | United States, Canada, with spillover into Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer preference for clean-label and minimally processed beverages

The North America cold-pressed juice market is witnessing significant growth as consumers increasingly prioritize clean-label beverages made with simple, recognizable, and minimally processed ingredients. Health-conscious consumers are focusing on ingredient transparency and opting for products free from artificial preservatives, colors, flavors, and added sugars, positioning cold-pressed juices as a preferred alternative to conventional packaged drinks. In response, manufacturers are emphasizing natural ingredient lists, non-GMO sourcing, and minimal processing methods to build consumer trust and differentiate their products. According to data from Ingredion, in 2024, 56% of consumers expressed a willingness to pay a premium for products with recognizable ingredients, while 38% of new food and beverage launches in the United States and Canada included clean-label claims[1]Source: Ingredion, "Clean label ingredients: From buzzword to business driver," ingredion.com. These evolving consumer preferences are driving beverage companies to expand their clean-label cold-pressed juice offerings, thereby fueling market growth across North America.

Increasing popularity of functional and immunity-boosting ingredients

The North America cold-pressed juice market is driven by increasing demand for functional beverages containing ingredients that promote immunity, digestive health, energy, and overall wellness. Consumers are showing a growing preference for juices made with nutrient-rich fruits, vegetables, herbs, spices, probiotics, adaptogens, and superfoods such as ginger, turmeric, kale, spinach, elderberry, and citrus fruits to achieve health benefits beyond hydration. This trend is supported by heightened awareness of preventive healthcare and a shift toward obtaining vitamins, antioxidants, and bioactive compounds from natural food sources instead of synthetic supplements. In response, manufacturers are developing cold-pressed juice blends with specific health claims, such as immune support, gut health, detoxification, and stress management, while focusing on natural formulations free from artificial additives. The increasing adoption of these functional beverages by health-conscious consumers is driving product innovation and boosting demand for cold-pressed juices across North America.

Growing demand for organic and natural juice products

The North America cold-pressed juice market is experiencing growth due to rising consumer demand for organic and natural beverages free from synthetic pesticides, artificial additives, preservatives, and genetically modified ingredients. Health-conscious consumers are increasingly prioritizing ingredient quality, environmental sustainability, and transparent sourcing, driving a preference for organic cold-pressed juices over conventionally processed options. This shift is prompting manufacturers to expand certified organic product offerings, collaborate with organic fruit and vegetable growers, and emphasize clean agricultural practices as key differentiators. Supporting this trend, the 2025 IFIC Food & Health Survey indicates that 30% of Americans actively seek organic labels when purchasing food and beverages with production-related claims[2]Source: International Food Information Council, "2025 IFIC Food & Health Survey," ific.org. As interest in natural and organically sourced products continues to rise, the demand for premium organic cold-pressed juices is expected to remain a significant factor in market growth across North America.

Growing popularity of plant-based and vegan diets

The North America cold-pressed juice market is experiencing growth as plant-based and vegan lifestyles increasingly shape consumer beverage preferences. Individuals adhering to these dietary patterns favor beverages made entirely from fruits, vegetables, herbs, and botanicals, aligning with their nutritional and ethical values. Cold-pressed juices meet these criteria by providing a convenient source of vitamins, minerals, antioxidants, and phytonutrients, free from animal-derived ingredients or artificial additives. Additionally, flexitarian consumers are incorporating plant-based beverages into their diets to promote wellness, sustainability, and healthier eating habits. According to the 2025 IFIC Food & Health Survey, 3% of Americans follow a plant-based diet, while 1% identify as vegan[3]Source: International Food Information Council, "2025 IFIC Food & Health Survey," ific.org. Although these groups constitute a small portion of the population, their impact on product innovation and consumer preferences is driving manufacturers to expand plant-based cold-pressed juice offerings, fostering market growth across North America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited shelf life due to minimal processing | -1.1% | North America, with highest impact in lower cold-chain-density regions such as Mexico secondary cities and Rest of North America | Short term (≤ 2 years) |

| Competition from other healthy beverage categories | -0.9% | United States, Canada | Medium term (2-4 years) |

| Complex food safety and labeling compliance requirements | -0.7% | United States and Canada | Medium term (2-4 years) |

| Raw material fluctuations in fresh fruit and vegetable supply | -0.8% | United States, Canada, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from other healthy beverage categories

The North America cold-pressed juice market is experiencing heightened competition from various healthy beverage categories that deliver comparable wellness benefits, often at lower costs and with extended shelf lives. Alternatives such as kombucha, functional waters, ready-to-drink teas, probiotic beverages, protein shakes, plant-based milks, sparkling waters, and vitamin-enhanced drinks are gaining traction among health-conscious consumers seeking convenient and functional options. These beverages often offer specific benefits, including hydration, digestive health, energy, immune support, or high protein content, while requiring less refrigeration and enabling broader distribution compared to cold-pressed juices. Furthermore, ongoing product innovation, robust marketing efforts, and increased retail availability in these competing categories are expanding consumer choices and reducing the frequency of cold-pressed juice purchases. As consumers diversify their preferences for healthy beverages, the rising presence of substitute products is exerting pricing pressure and constraining the growth potential of the North America cold-pressed juice market.

Raw material fluctuations in fresh fruit and vegetable supply

The North America cold-pressed juice market faces challenges due to fluctuations in the availability and pricing of fresh fruits and vegetables, which significantly impact production costs and supply stability. The production of cold-pressed juices depends on high-quality, fresh produce to preserve their nutritional value, flavor, and premium positioning. This reliance makes manufacturers susceptible to seasonal variations, adverse weather conditions, droughts, floods, plant diseases, and shifts in agricultural yields. Additionally, supply chain disruptions, transportation issues, and labor shortages in the agricultural sector further limit the availability of essential ingredients and drive up procurement costs. Rising prices for organic and specialty produce add further strain on manufacturers' profit margins, as transferring these costs to consumers may reduce affordability in a price-sensitive market. These factors contribute to uncertainty in production planning, pricing strategies, and inventory management, hindering the consistent growth of the North America cold-pressed juice market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fruit Juice Leads, but Blends Capture Incremental Growth

Fruit juice holds the largest share of the product-type market, accounting for 46.55% of the projected 2025 market value. The demand for cold-pressed fruit juice in North America is primarily driven by consumers seeking natural, refreshing beverages that offer authentic fruit flavors without artificial additives or excessive processing. Growing awareness of the nutritional benefits of fruits, including their vitamin, mineral, and antioxidant content, has encouraged consumers to replace sugar-sweetened soft drinks with premium fruit-based juices. Additionally, the rising preference for clean-label, organic, and non-GMO products has enhanced the appeal of cold-pressed fruit juices, particularly among health-conscious millennials and families. Manufacturers are responding to evolving consumer preferences by expanding their offerings to include exotic fruits, single-origin varieties, seasonal flavors, and reduced-sugar formulations, all while maintaining a premium image. The widespread availability of these products through supermarkets, specialty health stores, cafés, and e-commerce platforms, coupled with advancements in high-pressure processing (HPP) technology that preserves freshness and nutritional quality, continues to drive the growth of the cold-pressed fruit juice segment across North America.

Blended fruit and vegetable juices represent the fastest-growing product segment, with a compound annual growth rate (CAGR) of 8.13% projected through 2031. The North American market for cold-pressed blended fruit and vegetable juices is fueled by increasing consumer interest in functional nutrition and convenient ways to enhance daily fruit and vegetable intake. These juices combine the natural sweetness of fruits with nutrient-rich vegetables such as kale, spinach, celery, beetroot, cucumber, and carrots, offering a balanced flavor profile while delivering essential vitamins, minerals, antioxidants, and dietary phytonutrients. The rising demand for beverages that support immunity, digestive health, detoxification, hydration, and overall wellness has encouraged consumers to incorporate blended juices into their daily health routines. Additionally, the growing adoption of plant-based lifestyles and preventive healthcare habits has further boosted demand for these nutrient-dense beverages. In response, manufacturers are introducing innovative combinations that include superfoods, herbs, adaptogens, and functional ingredients such as ginger, turmeric, and matcha. These efforts aim to differentiate product portfolios and cater to consumers seeking beverages with multiple health benefits, thereby accelerating growth in the blended fruit and vegetable juice segment.

By Packaging Type: PET Dominates, Sustainable Formats Accelerate

PET bottles accounted for 45.77% of the market value in 2025. The demand for cold-pressed juice packaged in PET bottles in North America is driven by factors such as convenience, product visibility, durability, and compatibility with refrigerated distribution systems. PET bottles are lightweight, shatter-resistant, and easy to transport, making them ideal for on-the-go consumption and retail merchandising in supermarkets, convenience stores, cafés, and fitness centers. Their transparency allows consumers to view the juice's natural color and freshness, reinforcing the premium and minimally processed image associated with cold-pressed beverages. Additionally, PET packaging is compatible with high-pressure processing (HPP), enabling manufacturers to extend shelf life while preserving nutritional quality and flavor without using preservatives. The increasing use of recyclable PET (rPET) and advancements in recycling infrastructure are helping brands meet consumer demand for sustainable packaging while maintaining cost efficiency, further supporting the dominance of PET bottles in the North American cold-pressed juice market.

Recyclable pouches/Tetra Pak formats are the fastest-growing packaging segment, with a CAGR of 7.85% through 2031. The adoption of these packaging formats for cold-pressed juice in North America is driven by a growing focus on sustainability, packaging innovation, and product convenience. Environmentally conscious consumers are increasingly seeking beverages packaged in formats that reduce plastic usage and minimize environmental impact, prompting manufacturers to introduce recyclable and responsibly sourced alternatives. Tetra Pak cartons offer excellent protection against light and oxygen, preserving product quality while reducing packaging weight and transportation-related emissions. Recyclable pouches provide flexibility, portability, and lower material usage, making them suitable for single-serve and family-sized products. Furthermore, beverage companies are aligning with corporate sustainability goals and retailer environmental requirements by expanding the use of recyclable, renewable, and low-carbon packaging materials. These factors, combined with increased investments in recycling technologies and circular packaging initiatives, are driving the adoption of recyclable pouches and Tetra Pak formats in the North American cold-pressed juice market.

By Nature: Organic Premium Accelerates While Conventional Anchors Volume

Conventional cold-pressed juice accounted for 61.57% of the 2025 market value, driven by strong consumer demand for fresh, minimally processed beverages at more affordable prices compared to certified organic alternatives. These juices provide the nutritional benefits, natural taste, and clean-label appeal associated with cold-pressed processing while remaining accessible to a wider consumer base. Their broad availability through supermarkets, warehouse clubs, convenience stores, cafés, and foodservice outlets has enhanced market penetration across various income groups. Manufacturers are utilizing high-pressure processing (HPP) technology to extend shelf life without preservatives, enabling efficient large-scale distribution while maintaining product quality. Ongoing innovation in fruit and vegetable blends, reduced-sugar formulations, and functional ingredients has further boosted consumer interest, positioning conventional cold-pressed juices as the preferred choice for shoppers seeking premium beverages that balance quality, convenience, and value.

The organic segment is projected to grow at a CAGR of 8.55% through 2031, driven by increasing consumer preference for beverages made from organically grown fruits and vegetables, free from synthetic pesticides, fertilizers, genetically modified ingredients, or artificial additives. Rising awareness of food safety, environmental sustainability, and clean agricultural practices has motivated consumers to opt for certified organic products that align with their health and lifestyle values. Premium shoppers are increasingly willing to pay higher prices for organic cold-pressed juices, associating organic certification with superior ingredient quality, transparency, and responsible sourcing. Expanded retail shelf space for organic beverages in supermarkets, natural food stores, and online platforms has improved accessibility. Beverage manufacturers are also introducing innovative organic blends featuring superfruits, botanicals, herbs, and functional ingredients. The combination of rising disposable incomes, growing clean-label preferences, and sustained interest in sustainable food production continues to drive demand for organic cold-pressed juices across North America.

By Distribution Channel: Off-Trade Anchors and Accelerates All Growth Vectors

Off-trade channels accounted for 62.45% of the 2025 market value and are projected to grow at a CAGR of 8.73% through 2031. This growth is driven by the widespread availability of products across supermarkets, hypermarkets, convenience stores, warehouse clubs, specialty health retailers, and e-commerce platforms. Consumers increasingly prefer purchasing cold-pressed juices during routine grocery shopping due to the convenience of comparing brands, flavors, nutritional claims, and pricing in a single location. Retailers have expanded refrigerated beverage sections and premium health food aisles, enhancing product visibility and encouraging impulse purchases. Additionally, the growth of online grocery services and direct-to-consumer subscriptions has improved accessibility by offering home delivery and recurring purchase options for health-conscious consumers. Promotional discounts, loyalty programs, multipack offerings, and a wide variety of conventional, organic, and functional juice options further strengthen off-trade sales, establishing this channel as the primary distribution route for cold-pressed juice in North America.

The growth of cold-pressed juice sales through on-trade channels in North America is supported by the increasing presence of cafés, juice bars, restaurants, hotels, fitness centers, corporate cafeterias, and wellness-focused foodservice establishments. Consumers are seeking freshly prepared or premium ready-to-drink beverages while dining out or maintaining active lifestyles, driving demand for cold-pressed juices as healthier alternatives to carbonated soft drinks and sugary beverages. Foodservice operators are integrating cold-pressed juices into breakfast menus, healthy meal combinations, smoothie offerings, and wellness programs to align with evolving consumer preferences for natural and functional beverages. Rising demand for convenient post-workout refreshments and nutrient-rich drinks in gyms and fitness clubs has also contributed to higher on-premise consumption. Furthermore, premium dining experiences, customized juice pairings, and the expansion of health-oriented menus are encouraging foodservice establishments to broaden their cold-pressed juice selections, supporting consistent growth in on-trade sales across North America.

Geography Analysis

In 2025, the United States accounted for 88.46% of the total North American cold-pressed juice market value, driven by heightened consumer awareness of health, wellness, and clean-label nutrition. The increasing preference for minimally processed beverages made with natural ingredients has led consumers to replace traditional soft drinks with cold-pressed juices, which provide vitamins, antioxidants, and functional health benefits. The country's advanced retail infrastructure ensures broad product availability. Additionally, the growing interest in organic products, plant-based diets, immunity-supporting beverages, and convenient on-the-go nutrition has further fueled demand. Continuous product innovation featuring superfruits, vegetables, botanicals, and functional ingredients, coupled with the widespread adoption of high-pressure processing (HPP) technology, allows manufacturers to offer premium juices with extended shelf life while maintaining nutritional quality, supporting sustained market growth in the United States.

Mexico is projected to be the fastest-growing geography in the North American cold-pressed juice market, with a CAGR of 7.75% through 2031. Rising urbanization, increasing disposable incomes, and growing health awareness are driving consumers to adopt healthier beverage alternatives. A gradual shift from sugar-sweetened carbonated drinks to natural fruit- and vegetable-based beverages is boosting demand for cold-pressed juices, particularly among younger consumers and middle-income households. Mexico's abundant domestic production of tropical fruits, including oranges, mangoes, pineapples, guavas, and limes, provides manufacturers with access to fresh raw materials, enabling the creation of diverse product offerings with authentic local flavors. The rapid expansion of modern retail formats, convenience stores, cafés, and premium grocery chains has improved the availability of refrigerated cold-pressed juices. Additionally, the growth of fitness centers, wellness trends, and foodservice establishments is creating new consumption opportunities, collectively driving the steady expansion of the cold-pressed juice market in Mexico.

The Canadian cold-pressed juice market is experiencing growth due to increasing consumer preference for natural, organic, and sustainably produced beverages that align with healthier lifestyles. Consumers are prioritizing ingredient transparency and actively seeking beverages free from artificial preservatives, added sugars, and synthetic colors. Rising awareness of preventive healthcare, along with the growing adoption of plant-based eating habits, has driven demand for nutrient-rich fruit and vegetable juices that support immunity and overall wellness. Furthermore, strong environmental awareness among Canadian consumers is encouraging manufacturers to use recyclable packaging and responsibly sourced ingredients, bolstering the appeal of premium cold-pressed juice brands across the country.

Competitive Landscape

The North America cold-pressed juice market exhibits a dual competitive structure, consisting of established premium brands and a diverse range of regional manufacturers, emerging wellness beverage companies, and retailer-owned private-label products. Premium brands distinguish themselves through the use of high-pressure processing (HPP) technology, vertically integrated production systems, organic certifications, functional formulations, and strong brand positioning. In contrast, regional producers focus on locally sourced ingredients, artisanal recipes, and unique flavor combinations. Private-label offerings are gaining momentum by delivering comparable quality at lower price points, leveraging retailer-controlled shelf placement and large-scale manufacturing partnerships. This competitive dynamic is driving price competition while enhancing product accessibility across the region.

The competitive landscape is undergoing significant changes due to industry consolidation and portfolio diversification. Beverage manufacturers are expanding their presence in the broader health and wellness category by introducing complementary products such as wellness shots, functional beverages, and other nutrient-enriched drink formats. These strategies allow companies to cater to various consumption occasions, diversify revenue streams, and meet evolving consumer preferences for beverages that promote immunity, hydration, digestive health, energy, and overall wellness. Investments in manufacturing capabilities, supply chain integration, and product innovation are emerging as critical factors for achieving long-term growth and maintaining a competitive edge.

Future competition in the market is expected to focus on functional beverage innovation, advancements in packaging, and geographic expansion rather than solely on traditional cold-pressed juice offerings. Wellness shots and other concentrated functional formats are experiencing faster growth compared to conventional bottled juices, driven by increasing consumer demand for convenient, health-oriented products with specific benefits. Additionally, manufacturers are exploring opportunities in shelf-stable functional beverages, direct-to-consumer subscription models, and personalized wellness programs to enhance consumer engagement beyond traditional retail channels. Significant growth potential exists in secondary cities across Canada and Mexico, where improvements in cold-chain infrastructure and the expansion of modern retail networks are increasing the availability of premium cold-pressed beverages. These developments provide opportunities for new market entrants and regional expansion.

North America Cold Pressed Juices Industry Leaders

-

Hain BluePrint, Inc.

-

Suja Life, LLC

-

Evolution Fresh, Inc.

-

Pressed Juicery, Inc.

-

Naked Juice Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AllWellO introduced of AllWellO Kids, a new line of USDA Organic, shelf-stable cold-pressed juice pouches made from fruits, vegetables, and water. These products are free from added sugar, preservatives, artificial ingredients, and concentrates, catering to the increasing demand for clean-label beverages for children. The product line is set to launch in HEB and Sprouts Farmers Market stores in May 2026, further expanding the company's family-oriented beverage portfolio.

- December 2024: Just Made enhanced its cold-pressed beverage production capabilities by implementing a high-pressure processing (HPP) system at its newly established 22,000-square-foot manufacturing facility in Houston, Texas. This investment boosts production capacity, minimizes reliance on third-party HPP services, enhances operational efficiency, and supports the company's ongoing expansion within the United States retail market.

- December 2023: Gopuff collaborated with Pure Green to introduce an exclusive line of cold-pressed juice Refreshers, incorporating functional ingredients such as matcha, turmeric, camu camu, and ashwagandha. These products are available exclusively through Gopuff's nationwide delivery platform. This partnership enhanced both companies' presence in the functional beverage market and bolstered Gopuff's private-label offerings.

North America Cold Pressed Juices Market Report Scope

| Fruit Juice |

| Vegetable Juice |

| Blends |

| PET Bottles |

| Glass Bottles |

| Recyclable-Pouch/Tetra-Pak |

| Others |

| Conventional |

| Organic |

| On-trade | |

| Off-trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Fruit Juice | |

| Vegetable Juice | ||

| Blends | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Recyclable-Pouch/Tetra-Pak | ||

| Others | ||

| By Nature | Conventional | |

| Organic | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the projected value of North America cold pressed juice by 2031?

The category is projected to reach USD 824.78 million by 2031, up from USD 583.97 million in 2026, at a 7.15% CAGR.

Which product type leads revenue in North America cold pressed juice?

Fruit juice led with 46.55% share in 2025, while blends are forecast to grow the fastest at 8.13% through 2031.

Why is off-trade the most important sales channel for cold pressed juice in North America?

Off-trade held 62.45% of 2025 value and is also expected to post the fastest 8.73% CAGR, supported by supermarkets, online subscriptions, and warehouse retail.

Which country contributes the most to regional demand for cold pressed juice?

The United States dominated with 88.46% of 2025 regional value because it has stronger HPP capacity, wider premium retail access, and deeper consumer adoption.

Page last updated on: