Infused Fruit Jellies Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

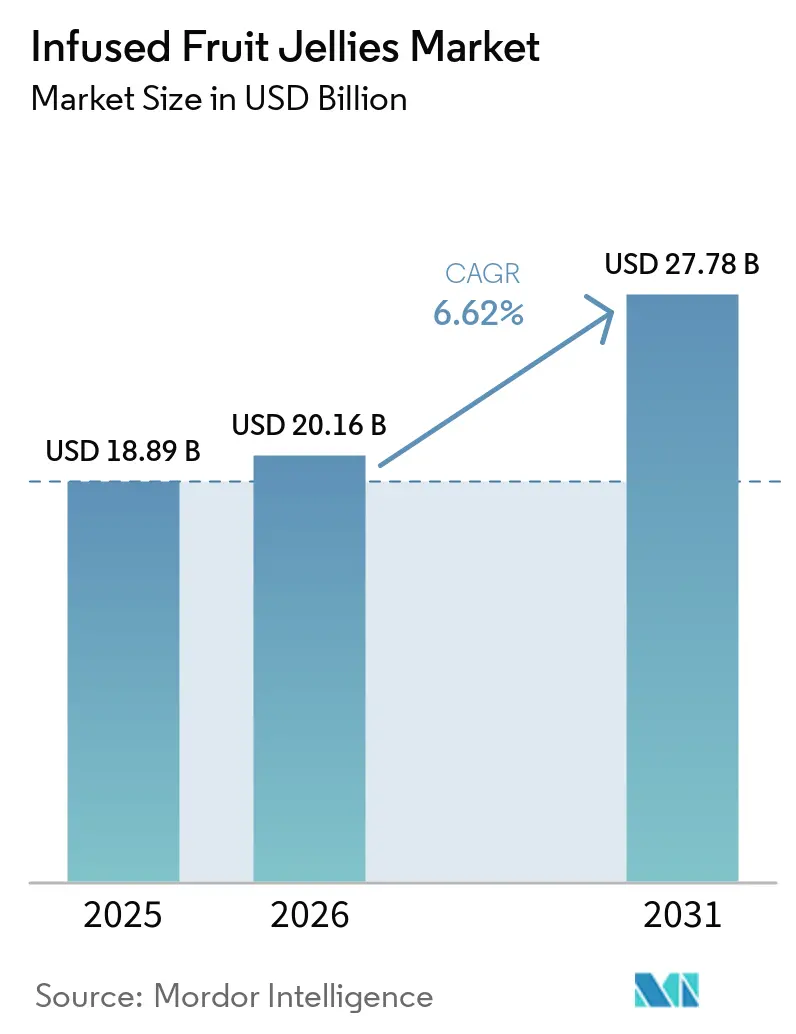

| Market Size (2026) | USD 20.16 Billion |

| Market Size (2031) | USD 27.78 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

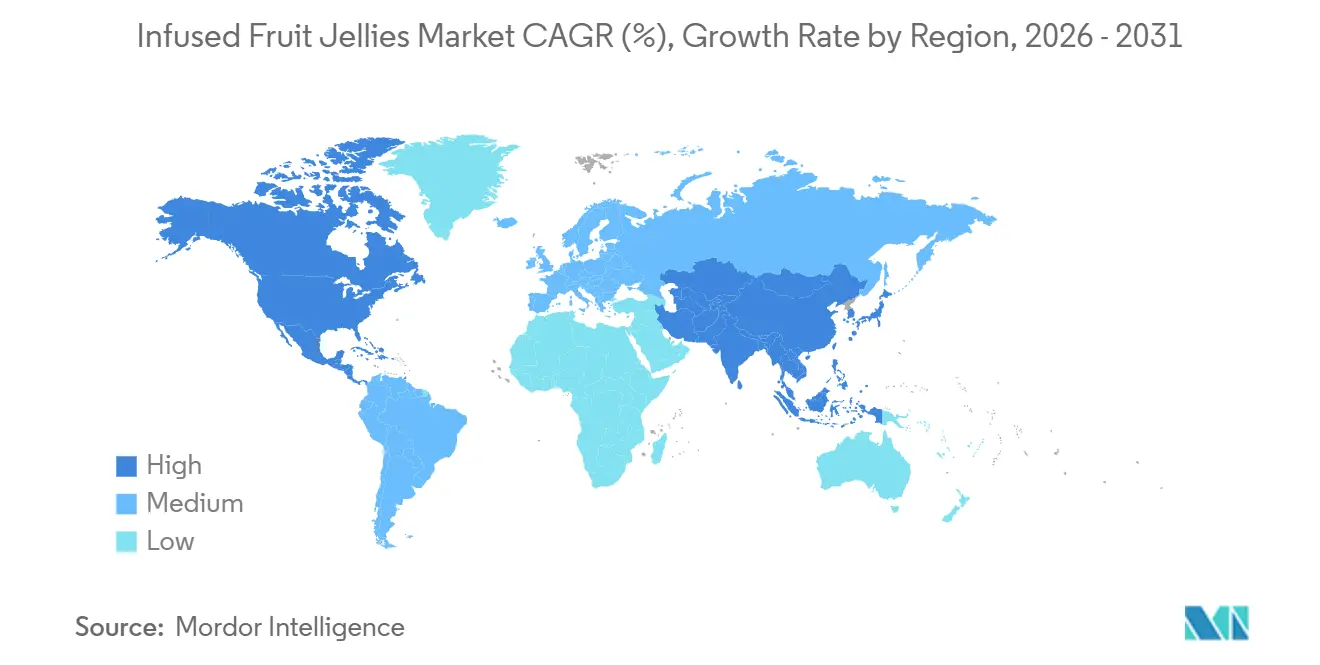

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Infused Fruit Jellies Market Analysis by Mordor Intelligence

The infused fruit jellies market is projected to grow from USD 18.89 billion in 2025 to USD 20.16 billion in 2026, reaching USD 27.78 billion by 2031, with a CAGR of 6.62% during 2026-2031. The increasing demand for confectionery that combines indulgence with wellness, a shift toward clean labels, and the growing acceptance of functional ingredients are driving value creation in this category. While tropical flavors remain central to sales, the market is witnessing growth in citrus-based products, innovations in CBD/THC-infused candies in regions with permissive regulations, and premium jar formats designed for gifting, which are broadening the consumer base. Regulatory changes are also influencing the market. The FDA's approval of Gardenia Blue as a natural color additive in July 2024 and the phase-out of Red No. 3 reflect a shift toward plant-based ingredients, aligning with consumer preferences for cleaner labels[1]Source: U.S Food & Drug Administration, " FDA Approves Gardenia (Genipin) Blue Color Additive While Encouraging Faster Phase", fda.gov. Similarly, the European Food Safety Authority's (EFSA) authorization of glucosyl hesperidin as a novel food in 2024, with a maximum intake of 5 mg/kg body weight per day, highlights regulatory support for citrus-derived functional compounds that enhance the nutritional value of confectionery products [2]Source: European Food Safety Authority, "Safety of glucosyl hesperidin as a Novel food pursuant to Regulation (EU) 2015/2283", efsa.onlinelibrary.wiley. These developments are paving the way for innovation in infused jellies, particularly those incorporating botanical extracts and bioactive compounds.

Key Report Takeaways

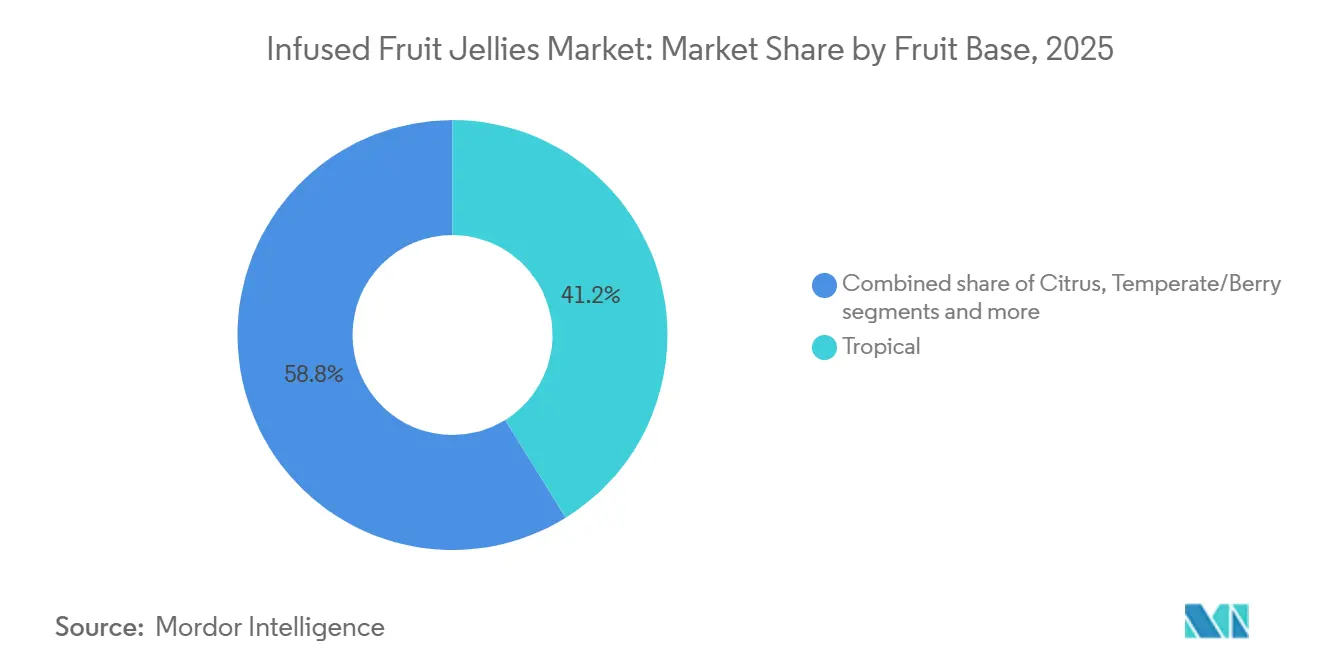

- By fruit base, tropical variants led with 41.16% revenue share in 2025, while citrus formulations are projected to advance at a 6.88% CAGR through 2031.

- By infusion ingredient, vitamins accounted for 56.29% of the infused fruit jellies market share in 2025; CBD/THC-infused lines are set to grow the fastest at 7.45% CAGR to 2031.

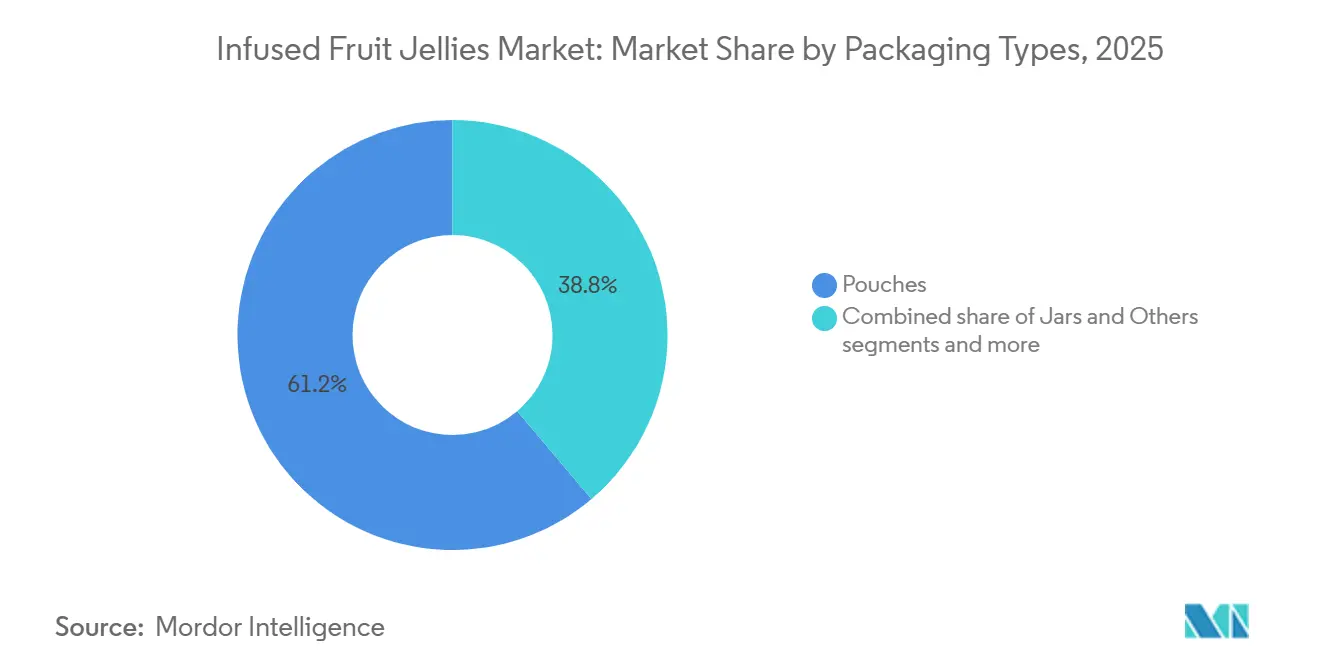

- By packaging type, pouches captured 61.19% of the infused fruit jellies market size in 2025, and jars are expected to expand at 7.08% CAGR between 2026 and 2031.

- By distribution channel, supermarkets/hypermarkets held 53.20% of revenue in 2025, whereas online retail is forecast to post a 7.89% CAGR to 2031.

- By geography, North America commanded a 35.18% share in 2025, and Asia-Pacific is positioned for the highest regional CAGR at 6.81% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Infused Fruit Jellies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenient, on-the-go fruit snacks | +1.5% | Global, with the strongest impact in North America and Europe | Long term (≥ 4 years) |

| Health-and-Wellness shift toward clean‐label confectionery | +0.8% | Global, with premium segments in developed markets | Medium term (2-4 years) |

| Increasing demand for functional confectionery products | +1.2% | Europe & North America core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Continuous flavor innovation and exotic fruit combinations | +0.9% | Global, with urban centers leading adoption | Short term (≤ 2 years) |

| Advancements in innovative and sustainable packaging formats | +0.7% | Developed markets initially, scaling globally | Medium term (2-4 years) |

| Expansion of plant-based and vegan product offerings | +0.6% | Global, with highest impact in Asia-Pacific & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for convenient, on-the-go fruit snacks

The global demand for convenient, on-the-go fruit snacks is a significant driver of growth in the infused fruit jellies market, closely aligned with modern consumption patterns shaped by fast-paced urban lifestyles. As consumers increasingly value portability, ease of consumption, and minimal preparation, infused fruit jellies have gained popularity as a preferred snack option due to their ready-to-eat format, compact packaging, and mess-free consumption. This trend is further supported by the growing need for quick snack solutions during commuting, work breaks, travel, and leisure activities, where traditional fruit or dairy-based snacks may be less practical. Infused fruit jellies meet this demand by offering single-serve, shelf-stable, and easy-to-carry options, making them suitable for consumption in various settings such as offices, schools, gyms, and outdoor activities. Overall, the combination of busy lifestyles, urbanization, and increasing snacking frequency is driving the adoption of infused fruit jellies as a portable, indulgent, yet functional fruit-based snack, reinforcing their position in the global convenience snacking market.

Continuous flavor innovation and exotic fruit combinations

Continuous flavor innovation and the introduction of exotic fruit combinations are driving demand in the global infused fruit jellies market by enhancing product appeal, differentiation, and encouraging repeat purchases. Younger demographics, in particular, are seeking unique taste experiences beyond traditional fruit flavors, prompting manufacturers to develop unconventional blends such as mango-passionfruit, yuzu-berry, dragon fruit-lychee, and tropical chili-infused variants. This focus on innovation helps brands sustain consumer interest in a competitive confectionery market where taste novelty significantly influences purchasing decisions. Exotic and cross-cultural flavor pairings are further supported by the globalization of food preferences, the influence of social media, and increased exposure to international cuisines. These trends are motivating consumers to explore premium and adventurous flavor profiles, positioning infused fruit jellies as a "discovery-driven" snack category rather than a conventional confectionery product. Additionally, ongoing investments in research and development for natural flavor extraction and fruit infusion technologies are enabling more authentic and intense taste experiences, enhancing consumer perceptions of quality and indulgence.

Health-and-Wellness shift toward clean‐label confectionery

The ongoing health-and-wellness movement is a major driver reshaping demand toward clean-label confectionery products. Consumers are increasingly prioritizing nutritional value, ingredient transparency, and overall well-being when selecting food and beverage options, with around 45% of global shoppers placing nutrition and wellness above price considerations in their purchasing decisions. This shift is particularly strong in the confectionery space, where traditional indulgence is being redefined through healthier positioning, including reduced sugar, natural flavors, and functional ingredient additions. At the same time, a clear, clean-label premium effect is emerging, especially among Gen Z and Millennials, who demonstrate a willingness to pay approximately 20–30% higher prices for products carrying claims such as organic, natural, high-protein, and free from artificial additives[3]Source: Ingredion, "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com. This willingness to trade up is encouraging manufacturers to reformulate confectionery offerings, including infused fruit jellies, with simpler ingredient lists and better-for-you positioning. As a result, health-driven consumption behavior is not only expanding the addressable market but also supporting value growth through premiumization.

Increasing demand for functional confectionery products

Vitamin-infused jellies account for more than half of segment sales, supported by claims related to immunity, energy, and beauty, which contribute to gross margins of 40-50%. These claims resonate strongly with health-conscious consumers seeking convenient and enjoyable ways to meet their nutritional needs. Albanese Confectionery’s omega-3 gummies demonstrate that sensitive bioactives, such as omega-3 fatty acids, can endure confectionery manufacturing processes without losing their efficacy, thereby broadening the wellness market by integrating functional benefits into traditional jellies formats. Variability in CBD/THC products continues as the FDA prohibits cannabinoids in conventional foods; however, state-level dispensaries maintain double-digit growth in compliant niches, driven by consumer demand for alternative wellness solutions. As consumers increasingly combine indulgence with supplementation, gummies are transitioning from supplement aisles to mainstream confectionery, offering a dual-purpose product that satisfies both taste and health needs. This trend is driving sustained growth in the functional infused fruit jellies market, as manufacturers innovate to meet evolving consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar content and regulatory scrutiny | -1.1% | Global, with heightened impact in regions with weak regulatory oversight | Short term (≤ 2 years) |

| Competition from gummies and alternative functional candies | -0.6% | Global, acute in import-reliant regions | Medium term (2-4 years) |

| Seasonal variability and inconsistent quality of fruit raw materials | -0.8% | Global, particularly in premium segments | Medium term (2-4 years) |

| Shelf-life challenges from low-preservative clean-label formulas | -0.7% | Global warm/humid supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adulteration/Safety Incidents

Safety incidents and concerns about adulteration significantly impact market confidence, especially as functional ingredients face heightened regulatory scrutiny and growing consumer skepticism regarding product claims. The joint enforcement action by the FDA and FTC in July 2024 against companies selling imitation delta-8 THC food products, which led to warning letters issued to five companies, illustrates how safety violations can prompt regulatory actions affecting entire product categories. Reports of over 300 adverse events linked to delta-8 THC products, many requiring hospitalization, underscore how safety issues in one segment can negatively influence perceptions of all infused confectionery products. A review by the German Research Foundation on CBD in foods concluded that CBD-containing products may lack substantiated health benefits and could pose risks, including liver enzyme increases observed at a daily intake of 4.3 mg CBD per kilogram of body weight. Manufacturing quality control is critical, as functional ingredients often necessitate specialized handling and testing protocols. Traditional confectionery manufacturers may lack these capabilities, increasing the risk of contamination or mislabeling incidents.

Competition from Alternatives Like Fruit-Infused Gummies

The competitive pressure from fruit-infused gummies is increasing as manufacturers in related categories adopt functional ingredient strategies while utilizing established consumer preferences and distribution networks. Gummy formulations that replace glucose syrup with fruit juice concentrates illustrate how traditional gummy producers can improve nutritional profiles while preserving the textures and flavors familiar to consumers. The introduction of functional gummy candies containing natural antioxidants and stevia highlights how established gummy manufacturers can integrate health-focused ingredients without significantly altering production processes. Patent activity related to anthocyanin applications in confectionery, including patents for anthocyanin-rich jellies, reflects substantial research and development investment in natural colorants that enhance visual appeal and provide antioxidant benefits. The primary challenge for infused fruit jellies is distinguishing themselves from gummy alternatives that may deliver similar functional benefits, superior texture, and broader appeal, particularly among younger consumers who are key drivers of confectionery demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fruit Base: Tropical Dominance Drives Premium Positioning

Tropical flavors accounted for 41.16% of the infused fruit jellies market share in 2025, driven by the popularity of mango and pineapple flavors in mainstream product lines. The infused fruit jellies market size for tropical flavors is expected to grow steadily due to broad consumer acceptance, a stable supply of concentrates, and vibrant color attributes. However, premium consumers are increasingly drawn to global citrus flavors such as yuzu and calamansi, which are associated with sophistication and refreshment.

Flavor manufacturers are combining citrus acids with berry sweetness to create layered taste profiles that reduce palate fatigue. Suppliers are also introducing freeze-dried pineapple pieces and yuzu zest to enhance texture and visual appeal. Additionally, social media "flavor challenge" trends are driving product trials, with citrus-based products projected to achieve the segment's highest CAGR of 6.88%, contributing incremental value to the infused fruit jellies market.

By Infusion Ingredient: Vitamins Lead While CBD Shows Promise

Vitamin-infused formats accounted for 56.29% of the infused fruit jellies market share in 2025, driven by the growing demand for functional confectionery products. Immune-support gummies, produced in CFR 111-certified facilities, have been a key contributor to this growth, offering consumers added health benefits alongside traditional candy enjoyment. Premium blends, such as C-plus-zinc combinations and collagen-enhanced jellies, not only cater to health-conscious consumers but also enable brands to achieve gross margins of 40-50%, which are reinvested into ongoing research and development efforts to innovate and expand product offerings. CBD/THC-infused products, while currently a niche segment, are projected to grow at a CAGR of 7.45% as regulatory frameworks expand in Canada, select U.S. states, and parts of Europe.

These products are gaining traction due to their potential wellness benefits, such as relaxation and stress relief. However, tightly regulated dispensary channels currently limit their broader market access. Despite these challenges, the high-margin nature of edibles has encouraged manufacturers to invest in advanced technologies like nano-emulsification for improved bioavailability and flavor-masking techniques to enhance consumer appeal. Additionally, probiotic and adaptogen inclusions are gaining prominence within the "others" category, allowing brands to address emerging consumer demands for gut health and stress management solutions. These inclusions align with the preferences of wellness-focused confectionery consumers, who are increasingly seeking products that combine indulgence with functional health benefits. This trend provides brands with opportunities to differentiate their offerings and capture a larger share of the wellness-driven confectionery market.

By Packaging Types: Pouches Dominate Convenience Trends

Pouches accounted for 61.19% of the projected 2025 revenue, driven by their lightweight nature, resealability, and enhanced shelf life achieved through metallized barriers. These features make pouches a preferred choice for both manufacturers and consumers, as they offer convenience and cost-effectiveness while maintaining product freshness. Additionally, sustainability objectives are encouraging converters to adopt recyclable polyethylene (PE) monolayers, enabling brands to meet circularity goals without compromising product quality. This shift aligns with growing consumer demand for environmentally friendly packaging solutions, further solidifying the dominance of pouches in the market.

Jars, although representing a smaller market share, are expected to grow at a compound annual growth rate (CAGR) of 7.08%. Transparent PET and premium glass formats are positioning fruit candies as suitable options for shareable gifts and pantry displays, appealing to consumers seeking visually appealing and reusable packaging. Features such as in-mold labeling and custom embossing enhance shelf appeal, particularly in premium seasonal product ranges, where differentiation and aesthetic value play a critical role. Flow-wraps and tins continue to serve impulse purchases and travel retail segments, ensuring a diverse range of packaging formats within the infused fruit jellies market. These formats cater to on-the-go consumers and those looking for compact, portable options, maintaining their relevance in niche applications.

By Distribution Channel: Traditional Retail Leads Digital Growth

Supermarkets and hypermarkets accounted for 53.20% of the projected 2025 turnover, highlighting their continued dominance in the distribution of core SKUs. These outlets remain a primary choice for consumers due to their extensive product availability and convenience. However, the infused fruit jellies market is increasingly shifting towards digital channels, with e-commerce expected to grow at a CAGR of 7.89%. This growth is driven by the rising preference for online shopping, supported by advancements in technology and logistics. Retailers are adopting click-and-collect and same-day delivery services to reduce delivery-related challenges, enhancing customer satisfaction and convenience.

Direct-to-consumer websites enable mid-tier competitors to test flavors through A/B testing, allowing them to refine their offerings based on consumer preferences. These platforms also facilitate the bundling of functional assortments, catering to specific consumer needs, and provide access to zero-party data, which helps in making informed decisions for rapid product iteration. Convenience stores maintain their relevance by offering single-serve trial options, appealing to on-the-go consumers. Meanwhile, specialty organic outlets focus on curating premium vegan or low-sugar collections, targeting ingredient-conscious demographics who prioritize health and wellness in their purchasing decisions.

Geography Analysis

North America is projected to maintain a 35.18% revenue share in 2025, driven by high per-capita confectionery spending and significant domestic capacity investments, such as Ferrara’s USD 675 million facility in South Carolina, scheduled for completion in 2029. The region’s regulatory environment is becoming increasingly stringent, particularly concerning sugar and cannabinoid labeling. However, high disposable income levels continue to support the introduction and success of premium functional products, which cater to evolving consumer preferences. Furthermore, the growing adoption of digital grocery platforms is accelerating the implementation of omnichannel loyalty programs. These programs are enhancing customer retention and deepening market penetration for both well-established heritage brands and newer challenger labels, ensuring sustained growth in the competitive landscape. The combination of regulatory adjustments, consumer spending power, and digital transformation is shaping North America into a dynamic market for confectionery products, with opportunities for innovation and expansion.

The Asia-Pacific region is expected to achieve the highest compound annual growth rate (CAGR) of 6.81% through 2031, driven by urban consumers increasingly adopting snackification trends and showing a preference for unique fruit flavors such as lychee and calamansi. The region’s rapidly expanding online marketplaces, particularly in China and India, provide low-barrier entry points for niche stock-keeping units (SKUs), enabling smaller players to compete effectively. Local producers are leveraging abundant domestic fruit harvests to reduce dependency on imports and buffer against volatility in global supply chains. While regulatory diversity across the region necessitates nuanced and tailored compliance strategies, the rising affluence of the middle class is creating a favorable environment for growth. This demographic shift is positioning Asia-Pacific as a critical frontier for the infused fruit jellies market with significant opportunities for both local and international players. The interplay of urbanization, digital commerce, and evolving consumer tastes is driving the region’s rapid growth and making it a focal point for market expansion.

Europe faces a complex regulatory landscape, with measures such as France’s sugar tax and the UK’s High Fat, Sugar, and Salt (HFSS) regulations prompting manufacturers to reformulate their products. Despite these challenges, the region benefits from deeply entrenched brand loyalty, which continues to drive consumer demand for established products. HARIBO’s GBP 35 million UK expansion and its 22.6% market share exemplify the resilience of legacy brands in maintaining their market position. This balance between regulatory pressures and consumer loyalty underscores the importance of innovation and adaptation in sustaining growth within the European market. Meanwhile, South America and the Middle East & Africa present significant long-term growth opportunities, primarily driven by the expansion of modern retail formats, the introduction of smaller packaging sizes tailored to local purchasing power, and rising income levels across these regions.

Competitive Landscape

The infused fruit jellies market demonstrates moderate concentration, characterized by competition between established confectionery companies and specialized functional food manufacturers. Prominent players such as Human Beanz, YumVs, Jelly Belly Candy Company, VitaWorksHealth, and Tastelli Konjac Jelly utilize extensive distribution networks and strong brand recognition. These companies are also investing in functional ingredient capabilities but face competition from agile startups focused on health-oriented products.

These companies benefit from increasing consumer awareness of the health advantages associated with ingredients like vitamins, CBD, and collagen. They differentiate their products through clean-label formulations, natural fruit bases, and premium positioning. Many leading brands are actively engaged in new product development and targeted marketing strategies to retain their market share across both mass-market and specialty channels. Additionally, they are exploring regulatory-compliant formulations for CBD-infused products in key markets.

In addition to established players, niche and emerging companies are capitalizing on opportunities in specific subcategories, such as collagen-infused and specialty wellness jellies. Innovation is particularly dynamic in the CBD-infused segment, where evolving regulations and changing consumer preferences enable rapid growth for boutique brands. Competition in this segment is driven by factors such as ingredient infusion, sugar reduction, organic certification, and plant-based claims. Strategic partnerships, private labeling for wellness retailers, and online-first distribution models further intensify competition. To maintain a competitive edge, companies must prioritize continuous innovation, regulatory compliance, and effective health-focused branding.

Infused Fruit Jellies Industry Leaders

-

YumVs

-

Human Beanz

-

VitaWorksHealth

-

Jelly Belly Candy Company

-

Tastelli Konjac Jelly

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Gelly Jelly, a new entrant in the collagen jelly market, launched five delectable flavors and swiftly gained traction among consumers. Tailored to promote skin health and wellness, this novel product has a distinctive texture and premium collagen. With five unique flavors, Gelly Jelly broadened its allure in the competitive health and beauty landscape.

- May 2023: NOW introduced its latest beauty-from-within offering, the Collagen Jelly Beauty Complex, presented in a convenient jelly stick pack format. These jelly sticks, offered in sweet orange and sweet plum flavors, are infused with Verisol Bioactive Collagen Peptides.

Global Infused Fruit Jellies Market Report Scope

| Citrus |

| Tropical |

| Temperate/Berry |

| Others |

| Vitamins-Infused |

| CBD/THC-Infused |

| Others |

| Pouches |

| Jars |

| Others |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Specialty Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Fruit Base | Citrus | |

| Tropical | ||

| Temperate/Berry | ||

| Others | ||

| By Infusion Ingredient | Vitamins-Infused | |

| CBD/THC-Infused | ||

| Others | ||

| By Packaging Types | Pouches | |

| Jars | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Specialty Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will global sales of infused fruit jellies market reach by 2031?

The infused fruit jellies market size is projected to reach USD 27.78 billion by 2031, reflecting a 6.62% CAGR over 2026-2031.

Which flavor base is growing fastest in premium candy launches?

Citrus-driven profiles featuring yuzu, calamansi, and blood orange are on track for a 6.88% CAGR through 2031, outpacing tropical and berry rivals.

What share do vitamins-infused candies currently command?

Vitamins-fortified SKUs led with 56.29% of the infused fruit jellies market share in 2025 and continue to benefit from high-margin immunity and beauty claims.

Which sales channel will add the most incremental revenue?

Online retail is forecast to post a 7.89% CAGR through 2031, driven by subscription models and direct-to-consumer launches that shorten shelf-space barriers.

Page last updated on: