Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

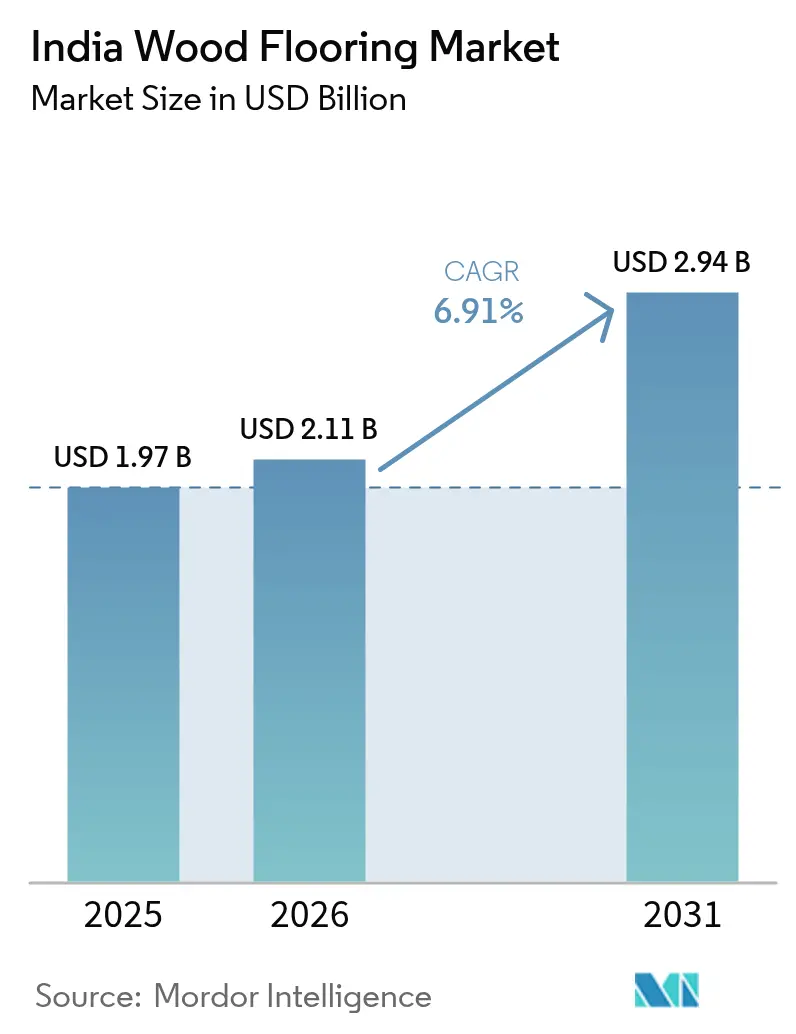

| Base Year Market Size (2025) | USD 1.97 Billion |

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 2.94 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

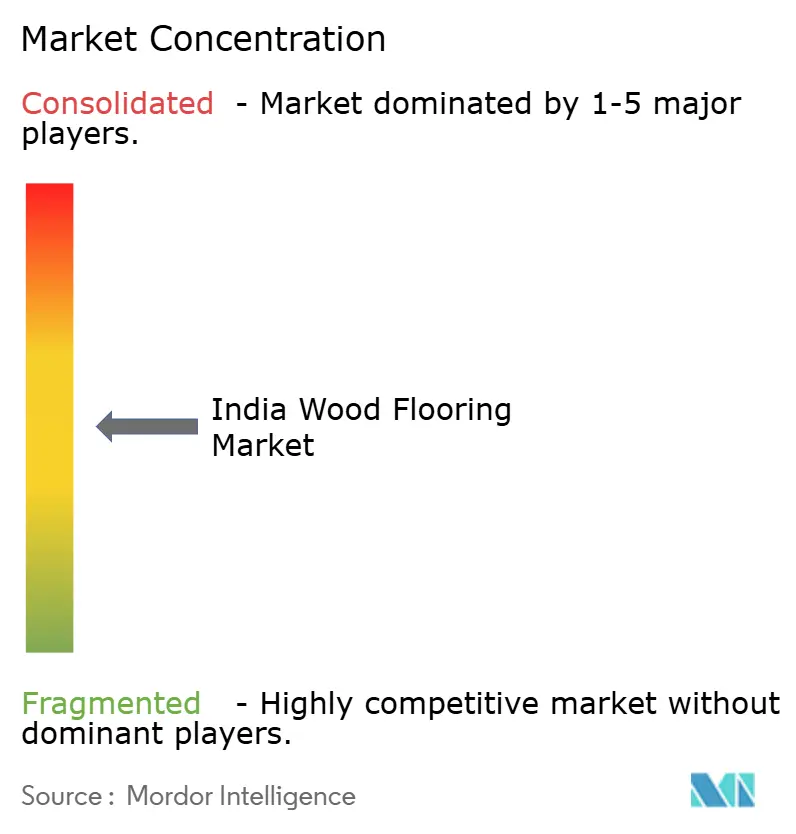

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Wood Flooring Market Analysis by Mordor Intelligence

The India wood flooring market size was valued at USD 1.97 billion in 2025 and estimated to grow from USD 2.11 billion in 2026 to reach USD 2.94 billion by 2031, at a CAGR of 6.91% during the forecast period (2026-2031). This trajectory reflects rapid urbanization, stronger household balance sheets, and rising preference for premium interior finishes. Large institutional real-estate inflows, resilient housing demand across Tier-1 and emerging Tier-2 cities, and a visible shift toward ESG-compliant construction underpin sustained demand for engineered and laminated solutions. Organized players expand capacity to capitalize on policy support for manufacturing, while global brands introduce waterproof and acoustic-enhanced ranges that suit India’s diverse climate. Competitive intensity remains moderate; regional specialists still command sizable local loyalty, yet integrated producers with sustainability credentials gain share through channel partnerships and digital outreach.

Key Report Takeaways

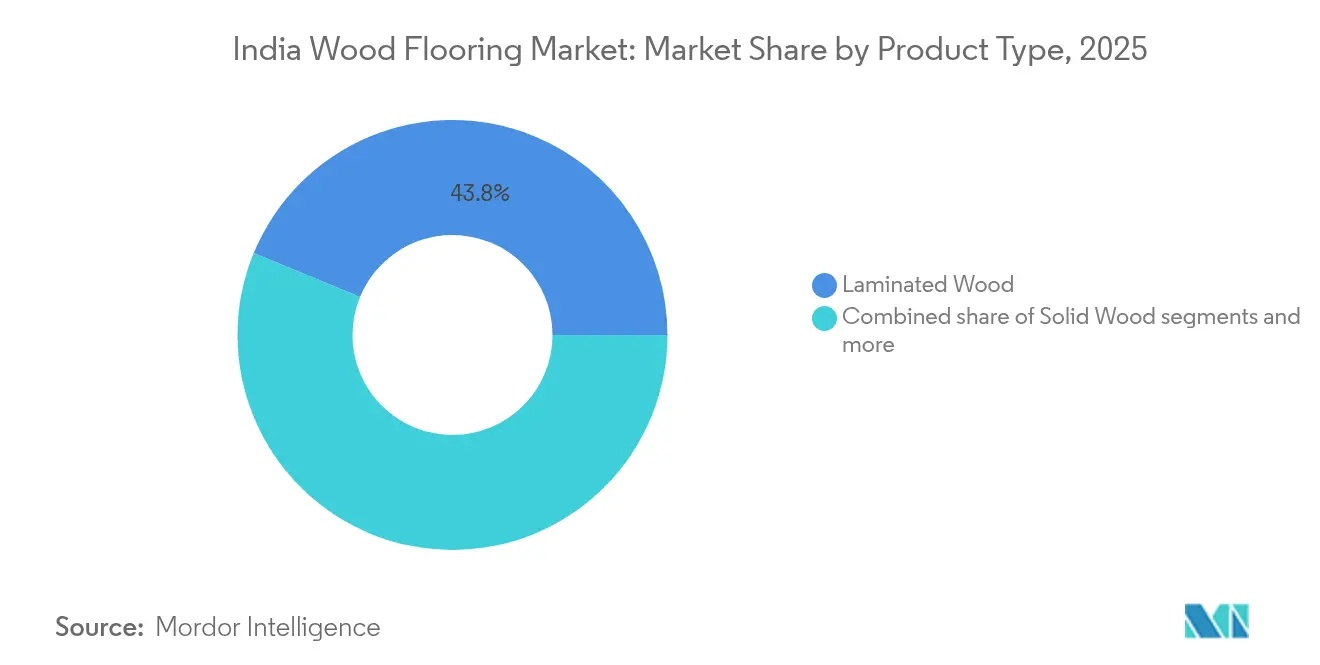

- By product type, laminated wood accounted for 43.78% of the India wood flooring market share in 2025, while the India wood flooring market size for engineered wood is forecast to expand fastest at a CAGR of 10.95% between 2026 and 2031.

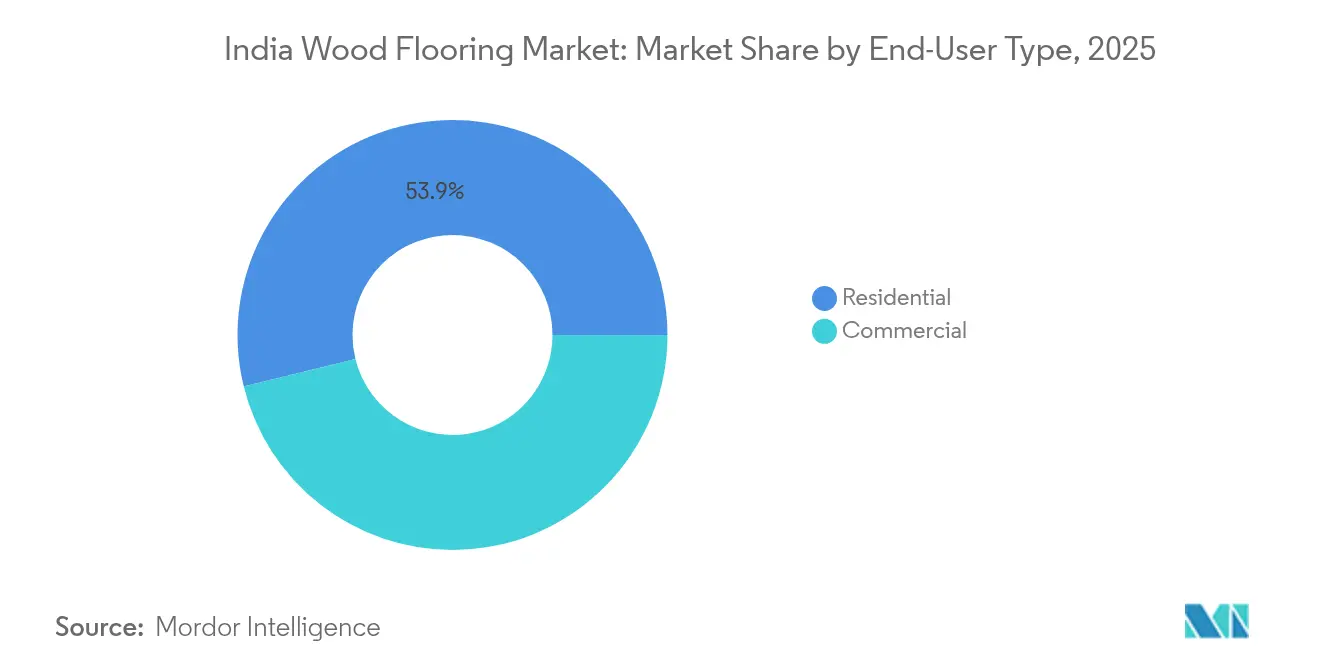

- By end-user type, residential applications captured 53.85% of the India wood flooring market share in 2025, with the India wood flooring market size for commercial end users projected to grow fastest at a CAGR of 9.22% during 2026-2031.

- By distribution channel, home centers represented 39.92% of the India wood flooring market share in 2025, while the India wood flooring market size for online channels is forecast to expand at the highest CAGR of 12.05% from 2026 to 2031.

- By geography, South India led with 32.75% of the India wood flooring market share in 2025, whereas the India wood flooring market size in West India is projected to grow fastest at a CAGR of 8.09% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Wood Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization-led housing boom | +1.8% | Nationwide, early gains in Mumbai, Bangalore, Chennai | Medium term (2-4 years) |

| Rising disposable incomes & premiumization | +1.5% | Urban centres, strongest in South & West India | Long term (≥4 years) |

| Commercial real-estate expansion & office retrofits | +1.2% | Tier-1 cities; spreading to Tier-2 markets | Medium term (2-4 years) |

| Cost-effective laminated/engineered options | +1.0% | National, deepening in Tier-2/3 cities | Short term (≤2 years) |

| Furniture QCOs favour certified wood flooring | +0.8% | Export hubs, premium residential projects | Long term (≥4 years) |

| E-commerce unlocking Tier-2/3 demand | +0.7% | Tier-2/3 cities countrywide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization-Led Housing Boom

India is adding 100 million new homes this decade, yet the annual supply of 600,000 units leaves a sizeable gap that keeps flooring demand robust[1]Economic Times, “India will need to build 100 million homes this decade amid rising household incomes,” economictimes.indiatimes.com . Residential floor space is set to surpass 50 billion m² by 2040, meaning most buildings that will exist in 2040 are still on the drawing board. The luxury housing market experienced significant growth, with its share increasing from 16% in 2018 to 43% in 2024. This expansion has driven demand for high-specification flooring solutions that offer enhanced acoustic properties and sustainability benefits. Developers targeting high-net-worth individuals are increasingly incorporating standardized engineered flooring ranges in their show apartments, a strategy that accelerates product awareness and adoption among potential buyers. Additionally, improved financing options, as banks extend mortgage accessibility to younger demographics, have facilitated the conversion of aspirational demand into finalized sales. This trend is evident across both metropolitan areas and emerging satellite towns, reflecting a broader shift in consumer preferences and purchasing power within the housing market.

Rising Disposable Incomes & Premiumization

In 2024, the high-value property market experienced a year-on-year growth, reflecting a sustained increase in purchasing power among affluent consumer segments. This trend highlights the resilience of demand within the premium real estate market, driven by the financial capacity and investment preferences of high-net-worth individuals. Shorter refurbishment cycles are driving repeat demand at a faster pace, particularly in urban apartment settings. Laminated planks, which can be replaced over a weekend without requiring extensive demolition, offer a cost-effective and time-efficient solution, making them a preferred choice for such environments. Retailers bundle extended warranties and post-installation care plans, reinforcing the value proposition of premium surfaces over low-end substitutes[2]Economic Times, “India will need to build 100 million homes this decade amid rising household incomes,” economictimes.indiatimes.com .

Commercial Real-Estate Expansion & Office Retrofits

Global capability centres and flex-space operators are increasingly modernizing older properties to meet Grade A specifications, focusing on sustainability and performance enhancements such as FSC-certified wood flooring, superior fire safety standards, and advanced acoustic solutions. The implementation of return-to-office policies has amplified the importance of employee-centric environments, driving demand for soft-touch, low-maintenance flooring options that contribute to achieving WELL or LEED certification. In central business districts (CBDs), rental growth is surpassing regional averages, motivating property owners to invest in upgrading high-traffic areas, including lobbies, circulation zones, and food courts, with durable engineered systems capable of withstanding significant footfall. The combination of retrofit activities and the development of greenfield IT parks is fuelling sustained demand for moisture-resistant, click-lock flooring products, which offer operational efficiency by reducing downtime during tenant turnover.

Cost-Effective Laminated & Engineered Options

Innovations such as edge-coating technologies now enable 24-hour spill resistance without raising the bill of materials, addressing India’s lengthy monsoon seasons. Finger-jointed plantation species have emerged as a cost-effective solution for reducing sourcing expenses. This innovation enables manufacturers to offer premium aesthetics at a more accessible price point, catering effectively to the mid-income consumer segment. Digital printing reproduces rustic or Scandinavian finishes with 4× resolution, narrowing the visual gap with solid hardwood. Engineered boards achieve transmission loss of 11 dB, satisfying new apartment acoustics codes in cities that regulate impact noise [3]Floor Covering Weekly, “Laminate gets an upgrade with Unicoat technology,” floorcoveringweekly.com . In Tier-2 markets like Indore and Lucknow, laminated price points as low as INR 120 per ft² broaden adoption among aspirational households while still providing better resale value than ceramic alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GST & import duties on processed wood | -1.2% | Nationwide, a higher impact on import-dependent areas | Short term (≤2 years) |

| Intense competition from ceramic & vinyl alternatives | -0.9% | Price-sensitive Tier-2/3 markets | Medium term (2-4 years) |

| Fragmented installer base & skills gap | -0.7% | National, acute in emerging towns | Long term (≥4 years) |

| Humidity-related durability concerns | -0.5% | Coastal belts of West & South India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High GST & Import Duties on Processed Wood

Wood flooring attracts 18% GST, while certain laminated and plywood categories incur 28%, eroding affordability compared with ceramic or SPC tiles taxed at lower slabs[4]ClearTax, “Impact of GST Rate on Furniture Manufacturers,” cleartax.in . Despite the expansion of 24-hour clearance ports, delays in customs clearance continue to immobilize working capital and disrupt the efficiency of just-in-time inventory systems. Medium-sized traders face significant inefficiencies in reclaiming Input Tax Credit, which drives them to source lower-cost domestic alternatives. However, these substitutes often fail to meet durability standards, potentially impacting product quality and customer satisfaction. Policymakers are actively assessing measures for tax rationalization; however, the lack of clarity regarding future tax relief creates an environment of uncertainty. This uncertainty discourages distributors from committing to long-term pricing strategies, thereby affecting market stability and planning.

Intense Competition From Ceramic & Vinyl Alternatives

Rigid-core SPC and high-definition porcelain planks replicate oak or teak visuals with higher moisture tolerance, particularly attractive in coastal or ground-floor settings. Agrifiber-based SPC produced at LEED-certified plants exploits rice-husk waste, positioning itself as an eco-friendly option at a lower cost. Installation speed favours click-fit vinyl, which requires fewer specialist tools than tongue-and-groove wood, tipping project managers toward non-wood surfaces for fast-track handovers. Digital marketing by tile giants saturates consumer feeds, narrowing perceived differentiation with genuine timber. The cost-of-ownership narrative leans toward ceramic and vinyl in rental markets where landlords prefer minimal maintenance between tenants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Innovation Shifts Demand Toward Engineered Solutions

Engineered boards anchor growth after recording an 10.95% CAGR outlook, thanks to multilayer constructions that stabilize against India’s humidity swings. They account for a rising share of the India wood flooring market size and command premium positioning in both housing and commercial retrofits. Laminated panels, still the volume leader at 43.78% share in 2025, gain fresh life through enhanced wear layers and registered emboss finishes that mirror sawn timber grain. The India wood flooring market share of solid wood narrows to niche luxury projects where end-customers prize natural patina and are willing to fund rigorous maintenance. Manufacturers channel R&D into waterproof treatments, acoustic membranes, and recycled-content cores that align with green-building mandates.

Engineered lines now feature transmission loss up to 11 dB, fulfilling new multi-dwelling rules for impact isolation. Waterproof iterations ensure 24-hour spill protection, permitting continuous installation across kitchens and living spaces without metal junction profiles. Digital printing technology significantly enhances knot details with a 4× resolution, creating a seamless integration with solid planks. This technological advancement, coupled with the segment's focus on delivering superior aesthetics, high performance, and sustainability, strengthens its position as a key driver of growth in India's wood flooring market. The segment's ability to align with evolving consumer preferences and industry demands further underscores its leadership in shaping market dynamics.

By End-User Type: Commercial Momentum Outpaces Residential Dominance

Residential demand anchored 53.85% of 2025 revenues as urban households invested in aesthetics reflecting aspirational lifestyles. First-time buyers accelerate decision cycles with mortgage approvals moving online, enabling flooring upgrades at the point of sale. The India wood flooring market size for residential renovations rises on shorter replacement intervals of 10-12 years versus the previous 15 years. Luxury condominium developers standardize FSC-certified engineered ranges to differentiate branding, widening consumer exposure, and bolstering long-term conversion.

Commercial installations, forecast at a 9.22% CAGR, pivot on return-to-office strategies and Grade A stock additions. Corporate leases often specify LEED or WELL targets, compelling fit-out contractors to choose low-VOC, recycled-content planks. Flex operators refresh interiors every 3-5 years, generating recurrent volumes for laminated and hybrid-core products. Logistics and light manufacturing parks expand auxiliary office space, extending commercial flooring opportunities into peripheral districts. The confluence of accelerated capex and sustainability compliance positions commercial buyers as catalysts for technological adoption within the India wood flooring market.

By Distribution Channel: Digital Ecosystems Reshape Access

Home centres maintain a 39.92% share through bundled installation, finance, and after-sales packages that resonate with time-pressed urban consumers. Their private-label volumes leverage scale to hold entry-level price points, anchoring the laminated category. Online platforms, growing at a 12.05% CAGR, unlock the India wood flooring market for Tier-2 and Tier-3 buyers previously dependent on limited local selections. Visualizer apps and AI-led consultations replicate showroom experiences, shrinking discovery friction. Specialty stores focus on design-led assortments, often collaborating with architects to supply bespoke finishes for boutique hospitality or luxury villas.

Marketplace algorithms are increasingly leveraging curated bundles, which include components such as planks, underlays, and adhesives. This approach not only drives higher basket sizes but also minimizes risks associated with product compatibility, thereby enhancing the overall customer experience. Additionally, the enforcement of consumer-protection regulations requiring warranty disclosures is strengthening the position of organized brands. These regulations are effectively redirecting uncertain consumers away from unbranded imports, fostering greater trust in established players. Consequently, the adoption of omnichannel strategies has emerged as a critical factor in establishing a competitive advantage within the Indian wood flooring market.

Geography Analysis

South India retained a 32.75% revenue share in 2025 on the back of tech-sector prosperity in Bangalore, Chennai, and Hyderabad. High disposable incomes and sophisticated tenant profiles normalize engineered or solid planks in premium housing, while Grade A offices specify acoustic-rated floors to lift employee comfort. Manufacturing clusters across Tamil Nadu and Karnataka shorten lead times, aiding aggressive project schedules. Although coastal microclimates in Chennai demand higher-spec installation protocols, inland cities like Hyderabad experience thriving demand for mid-priced laminates.

West India is anticipated to achieve the highest CAGR of 8.09% through 2031, driven by the exceptional sales performance in the Mumbai Metropolitan Region during 2024 and the implementation of extensive infrastructure projects under the PM GatiShakti initiative. The increasing property valuations in peripheral locations, including Panvel and Thane, are contributing to higher flooring budgets and larger plinth areas, reflecting a shift in consumer preferences and investment patterns in the region. Gujarat’s industrial corridors and Rajasthan’s tourism-led urban revival further diversify demand. Logistics advantages via JNPT and Mundra ports facilitate raw-material imports and outbound distribution. Developers capitalize on premium seaside addresses by specifying waterproof engineered planks with salt-spray-resistant coatings, reinforcing market footholds despite climatic hurdles.

North, East, Central, and Northeast India contribute the remaining opportunity pool at varying readiness levels. Delhi-NCR’s mixed-use mega-projects drive specification of FSC-certified flooring to meet green ratings, yet affordability pressures temper penetration in mass housing. Kolkata’s commercial revival and smart-city projects in Bhubaneswar nurture gradual uptake. Central India leverages highway and industrial corridor programs to accelerate urbanity around Bhopal and Indore. Improved connectivity in Assam and Meghalaya opens nascent niches for organized suppliers.

Competitive Landscape

The Indian wood flooring market exhibits a moderately concentrated structure, with the top five brands collectively accounting for nearly 50% of the market share. This leaves significant opportunities for regional players and import-driven traders to establish a foothold. Leading companies are adopting vertical integration strategies, expanding into medium-density fiberboard (MDF), laminate, and decorative surface value chains. This approach not only mitigates the impact of raw material price fluctuations but also enhances operational efficiency and profit margins, providing a competitive edge in a dynamic market environment.

Sustainability has become a critical factor influencing purchasing decisions in the market. Certifications such as FSC (Forest Stewardship Council), PEFC (Program for the Endorsement of Forest Certification), GreenPro, and IGBC (Indian Green Building Council) are increasingly shaping both corporate procurement processes and consumer preferences. These credentials are now integral to meeting the growing demand for environmentally responsible products, positioning companies with strong sustainability practices as preferred suppliers in both B2B and retail segments.

International entrants are driving innovation by introducing advanced technologies, including high-definition printing and waterproof flooring solutions. To achieve nationwide market penetration, these players are forming strategic partnerships with domestic distributors. Additionally, they are investing in collaborative training programs aimed at standardizing installation practices, which currently vary significantly across regions. By addressing inconsistencies in workmanship, these initiatives are expected to enhance customer satisfaction and support the long-term growth of the market.

India Wood Flooring Industry Leaders

Greenlam Industries Ltd.

Pergo (Mohawk Industries)

Greenpanel Industries Ltd.

SquareFoot Flooring Pvt. Ltd.

Action Tesa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: HIL Limited rebranded as BirlaNu and earmarked USD 150 million for capacity expansion while preparing to launch its global premium flooring brand Parador in the Indian market.

- March 2025: Mohawk Industries introduced 26 new products across its RevWood laminate and TecWood engineered lines, including 72-hour wet-resistance warranties and the first NALFA platinum carbon-negative certification for laminate flooring.

- January 2025: Kronospan debuted waterproof acoustic flooring and the PerfectPad recycled-wood underlay at BAU 2025 Munich, positioning the launches for near-term rollout through its Indian distribution partners.

- September 2024: Century Plyboards approved a 30% plywood-line expansion via an INR 140 crore investment and shortlisted new sites in Punjab, Uttar Pradesh, Odisha, and Andhra Pradesh to lift organized-segment share beyond 10%

India Wood Flooring Market Report Scope

Wood flooring is any product manufactured from timber that is designed for use as flooring, either structurally or aesthetically. Wood is a common choice as a flooring material and can come in various styles, colors, cuts, and species. Bamboo flooring is often considered a form of wood flooring, although it is made from grass (bamboo) rather than timber.

The India Wood Flooring Market Is Segmented By Product Type (Solid Wood Flooring, Laminated Wood Flooring, And Engineered Wood Flooring), By End-User (Residential And Commercial), And By Distribution Channel (Home Centers, Specialty Stores, Online Retailers, And Other Distribution Channels). The Report Offers Market Size And Forecasts For The Indian Wood Flooring Market In Terms Of Value (USD) For All The Above Segments.

By Product Type

| Solid Wood |

| Laminated Wood |

| Engineered Wood |

By End-User Type

| Residential |

| Commercial |

By Distribution Channel

| Home Centers |

| Specialty Stores |

| Online |

| Other Distribution Channels |

By Geography

| North India |

| South India |

| West India |

| East India |

| Central India |

| Northeast India |

| By Product Type | Solid Wood |

| Laminated Wood | |

| Engineered Wood | |

| By End-User Type | Residential |

| Commercial | |

| By Distribution Channel | Home Centers |

| Specialty Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | North India |

| South India | |

| West India | |

| East India | |

| Central India | |

| Northeast India |

Key Questions Answered in the Report

What is the projected size of the India wood flooring market by 2031?

It is forecast to reach USD 2.94 billion, reflecting a 6.91% CAGR between 2026-2031.

Which product category will grow fastest through 2031?

Engineered wood flooring is expected to record an 10.95% CAGR due to waterproof and acoustic enhancements.

How quickly are online channels expanding for wood flooring in India?

E-commerce sales are set to grow at a 12.05% CAGR as digital tools broaden access in Tier-2 and Tier-3 cities.

Which region will show the strongest growth momentum?

West India is projected to post an 8.09% CAGR through 2031 on the back of housing and infrastructure booms.

Why are certifications important when selecting wood flooring?

FSC and PEFC credentials assure legal, sustainable sourcing and help projects earn LEED points, leading many corporate buyers to favor certified products.

What hampers installation quality in emerging towns?

A fragmented installer base and limited formal training lead to inconsistent workmanship, restricting premium product adoption.

Page last updated on: