Veterinary CRO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

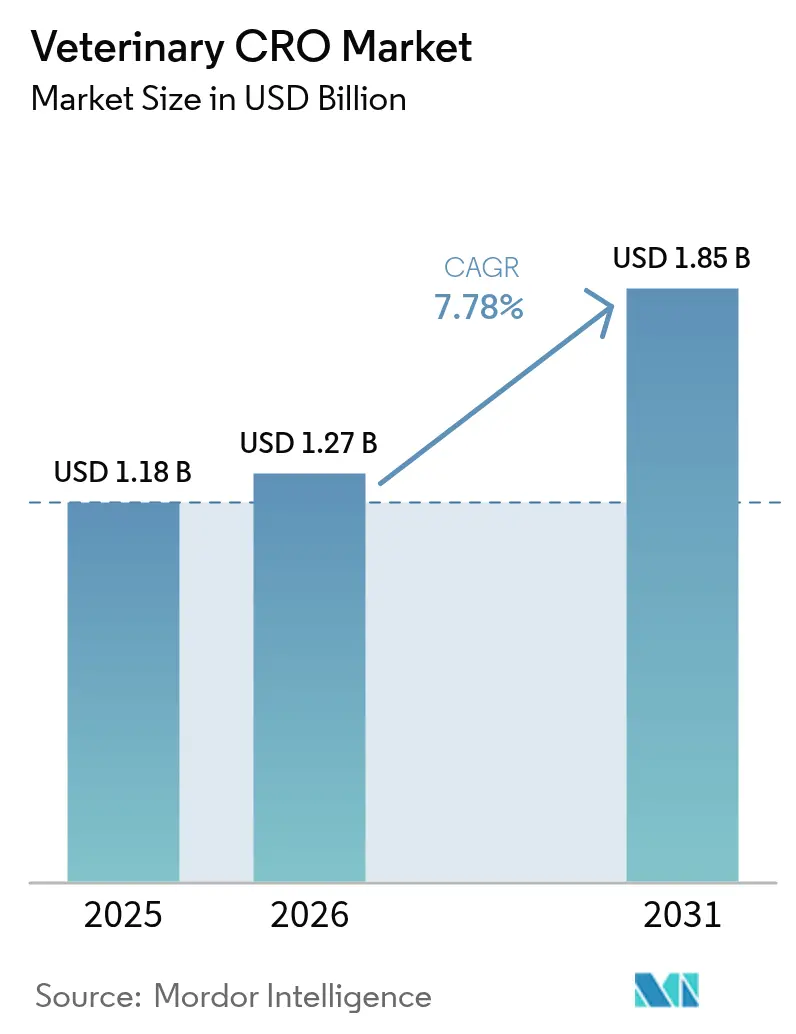

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary CRO Market Analysis by Mordor Intelligence

The Veterinary CRO Market size is projected to be USD 1.18 billion in 2025, USD 1.27 billion in 2026, and reach USD 1.85 billion by 2031, growing at a CAGR of 7.78% from 2026 to 2031.

Rapid outsourcing of discovery and development tasks, rising global spending on companion-animal and livestock health, and the rollout of streamlined regulatory pathways are together accelerating the flow of projects into contract research pipelines. Sponsors now favor external partners that can compress timelines, manage multi-jurisdiction dossiers, and provide specialized pathogen-handling capacity, especially for vaccine challenge studies. Asia-Pacific is emerging as the cost-advantaged growth engine, yet North America retains scale leadership thanks to its dense network of veterinary teaching hospitals and Good Laboratory Practice (GLP) sites. Meanwhile, digital monitoring tools are lowering per-patient costs in decentralized companion-animal trials, and biologics innovation—from monoclonal antibodies to gene therapies—is lengthening average study duration, which lifts overall CRO revenues.

Key Report Takeaways

- By service type, clinical trials held 33.12% of 2025 revenue, while regulatory and consulting services are projected to expand at a 9.43% CAGR through 2031.

- By animal type, companion animals led with a 57.45% revenue share in 2025; livestock studies are forecast to grow at a 9.66% CAGR through 2031.

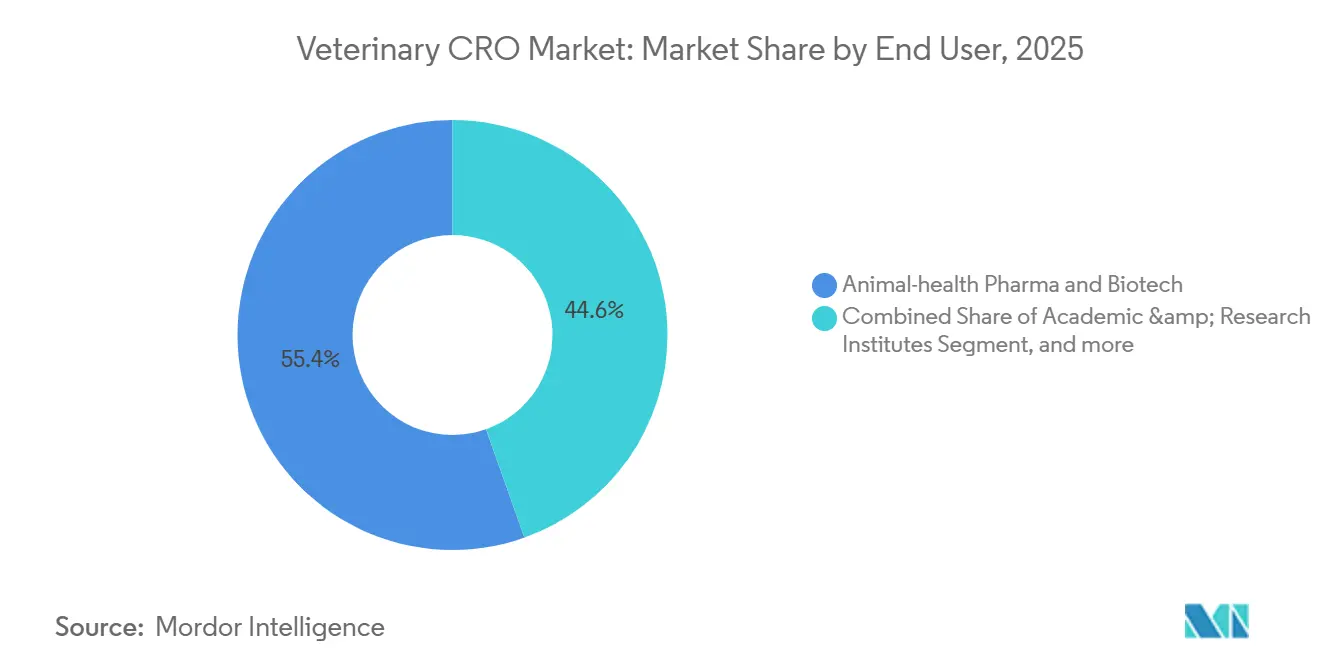

- By end user, pharmaceutical and biotech companies accounted for 55.43% of 2025 demand, whereas academic and research institutes are expected to grow at a 10.54% CAGR between 2026 and 2031.

- By indication, infectious-disease programs accounted for 35.76% of 2025 revenue, yet neurology trials are anticipated to register a 10.32% CAGR through 2031.

- By geography, North America commanded 41.75% of the veterinary contract research organization market in 2025, while Asia-Pacific is advancing at a market-leading 8.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary CRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in global animal health expenditure | +1.8% | Global, with highest intensity in North America and Western Europe | Medium term (2-4 years) |

| Favorable regulatory pathways for veterinary pharmaceuticals | +1.5% | North America and Europe, spill-over to Asia-Pacific | Long term (≥4 years) |

| Increasing outsourcing of R&D activities by animal-health companies | +2.1% | Global, led by North America and emerging in Asia-Pacific | Short term (≤2 years) |

| Intensifying focus on One Health and zoonotic disease preparedness | +1.3% | Global, priority in Asia-Pacific and Sub-Saharan Africa | Medium term (2-4 years) |

| Expansion of companion-animal biologics and specialty therapies | +1.6% | North America and Europe, early adoption in urban Asia-Pacific | Medium term (2-4 years) |

| Digitalization and data-driven approaches in veterinary research | +1.2% | North America and Europe, gradual uptake in Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growth in Global Animal Health Expenditure

Global veterinary pharmaceutical sales, including over-the-counter products and diagnostics, exceeded USD 50 billion in 2025, up sharply from pre-pandemic levels[1]HealthforAnimals, “Global Animal Health Report 2025,” healthforanimals.org. U.S. households now spend an average of USD 1,500 per pet each year, a 22% jump since 2020, which sustains demand for advanced trials in oncology, cardiology, and neurology. Livestock producers have likewise raised biosecurity budgets, allocating up to 12% of farm operating costs to veterinary services and vaccines. As spending expands on both the companion and production sides, the veterinary CRO market attracts projects that amortize fixed infrastructure across species. Heightened willingness to pay for specialty therapies underscores a durable revenue base for providers capable of serving multi-species portfolios.

Favorable Regulatory Pathways for Veterinary Pharmaceuticals

The U.S. Animal Drug User Fee Act V provides USD 35 million a year to expedite reviews and broaden conditional approvals for products targeting serious conditions. In Europe, the Platform Technology Master File enables a single dossier to support multiple vaccine candidates, reducing redundant studies by nearly 20%. VICH guideline GL52 now harmonizes pharmacokinetic protocols across key markets, eliminating region-specific bridging trials that once extended timelines. Although these tailwinds shorten time-to-market, they also elevate documentation standards, prompting sponsors to enlist CROs with proven regulatory track records. Post-approval efficacy commitments linked to conditional pathways further extend CRO engagement across the product life cycle.

Increasing Outsourcing of R&D Activities by Animal-Health Companies

Outsourcing penetration rose to 42% of preclinical and clinical workloads in 2025, up from 31% five years earlier. Industry leader Zoetis reported that external partnerships now cover 38% of its innovation pipeline. Venture-backed biotech entrants rely even more heavily on CRO capacity—often exceeding 90%—because they lack internal toxicology or clinical infrastructure. Complex biologics, from monoclonal antibodies to mRNA vaccines, require specialized analytics and manufacturing, pushing sponsors toward integrated service providers. As portfolios mature, companies streamline vendor rosters in favor of CROs that can deliver formulation, toxicology, clinical execution, and regulatory submission under a single quality system.

Intensifying Focus on One Health and Zoonotic-Disease Preparedness

The U.S. National One Health Framework allocates USD 1.2 billion through 2029 for integrated zoonotic-disease surveillance projects that heavily involve veterinary CROs. Emergency vaccine-challenge studies for avian influenza and African swine fever are being fast-tracked with public-sector funding in the United States and Southeast Asia alike. European guidance now mandates linking veterinary and human epidemiological data sets, boosting demand for dual-species study designs that CROs are uniquely positioned to manage. These multi-stakeholder initiatives broaden the veterinary CRO market beyond classic drug development into epidemiology, diagnostics validation, and public-health interventions, diversifying revenue and reducing exposure to cyclical pharmaceutical R&D budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development costs and lengthy approval timelines | -1.4% | Global, most acute in North America and Europe | Long term (≥4 years) |

| Limited availability of specialized animal research infrastructure | -0.9% | Asia-Pacific, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Shortage of skilled veterinary research professionals | -0.7% | Global, particularly severe in emerging markets | Long term (≥4 years) |

| Ethical concerns and regulatory scrutiny over animal testing | -0.6% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Development Costs and Lengthy Approval Timelines

Bringing a novel veterinary biologic to market can cost up to USD 150 million and take 7-9 years, versus 5-6 years a decade ago[2]Tufts University, “Economic Analysis of Veterinary Drug Development,” tufts.edu. Field trials for livestock vaccines may involve 10-15 commercial farms, with each site adding USD 200,000-400,000 to budgets. Companion-animal oncology studies are similarly expensive, sometimes exceeding USD 5 million for 100 dogs enrolled across specialty centers. The EMA’s five-year post-approval monitoring rule for food-animal products adds another USD 2-4 million to lifecycle costs. Escalating capital requirements deter smaller innovators and concentrate projects among well-funded sponsors, which could slow the overall expansion pace of the veterinary CRO market.

Limited Availability of Specialized Animal Research Infrastructure

Fewer than 30 GLP-certified sites worldwide can handle large-animal studies at biosafety-level-3, and just 12% of those are in Asia-Pacific[3]Association for Assessment and Accreditation of Laboratory Animal Care International, “Accredited Facilities Directory 2025,” aa¬alac.org. Sponsors often relocate livestock across continents, extending timelines by up to a year and inflating costs by more than 30%. Establishing a specific-pathogen-free swine herd can require USD 1.5-3 million annually, discouraging greenfield builds in emerging markets. Limited access to advanced imaging and oncology equipment further constrains enrollment capacity at veterinary teaching hospitals. Until new facilities come online, infrastructure scarcity will remain a headwind, particularly for regions that aspire to capture the fastest-growing share of outsourced studies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Regulatory Consulting Gains as Harmonization Cuts Redundancy

Clinical trials accounted for the largest share of 2025 revenue, yet the segment’s 7.2% growth lags the 9.43% CAGR projected for regulatory and consulting work as harmonized VICH guidelines streamline dossier strategies across regions. Toxicology and safety studies held nearly 28% share, buoyed by stringent residue-depletion rules for food-animal therapies. Integrated providers that pair GLP toxicology with real-time bioanalytical support are steadily increasing their market share in the veterinary CRO market.

Over the forecast horizon, the regulatory-consulting niche is poised to expand its contribution to the veterinary CRO market, as sponsors prize rapid, audit-ready submissions. ISO 13485 certification has emerged as a key differentiator, with compliant firms able to command double-digit price premiums. Service bundling increasingly places dossier preparation, study monitoring, and pharmacovigilance under single-provider contracts, simplifying oversight for resource-constrained sponsors.

By Animal Type: Livestock Vaccines Outpace Companion Dominance

Companion species accounted for 57.45% of 2025 revenue, led by canine and feline projects that mimic human medicine protocols. Oncology and dermatology remain the highest-value indications, often supported by owner-paid expenses that offset trial costs. Even so, accelerating vaccine development for African swine fever and avian influenza positions livestock programs to capture a larger share of the veterinary CRO market.

Livestock trials are forecast to post a 9.66% CAGR as governments inject funding to safeguard food security. Swine studies, propelled by new ASF vaccine candidates, are the fastest riser. Cattle respiratory-disease projects and poultry biosecurity mandates also add volume. The shift diversifies revenue streams away from consumer discretionary spending toward publicly financed disease-control budgets.

By End User: Academic Institutes Ride One Health Funding Wave

Pharmaceutical and biotech sponsors still dominate, accounting for 55.43% of the 2025 contract value, while universities and public institutions are scaling rapidly under One Health grant programs. These academic sites, once limited to exploratory work, now run pivotal trials under ISO 9001 quality systems, securing a larger share of the veterinary CRO market.

Growth at a 10.54% CAGR reflects both new government funding and the strategic monetization of teaching-hospital assets, such as the 400-dog oncology enrollment capacity at UC Davis. Non-profit agencies and agricultural cooperatives also fund data-rich studies aimed at addressing disease threats in developing countries, further broadening the customer mix.

By Indication: Neurology Emerges as Fastest-Growing Domain

Infectious-disease programs retained the top revenue spot in 2025, fueled by government-backed livestock vaccine efforts. Nonetheless, neurology projects—anchored by canine epilepsy gene therapy and feline cognitive diagnostics—are projected to log a 10.32% CAGR, the highest among all indications. This surge is drawing cross-over investment from human CNS specialists, enhancing the overall depth of the veterinary CRO market.

Oncology maintains a sizeable 22% share as comparative cancer models gain favor among translational researchers. Dermatology and gastrointestinal studies round out the pipeline diversity, ensuring that revenue is not overly dependent on any single disease class.

Geography Analysis

North America contributed 41.75% of 2025 revenue on the strength of its dense GLP infrastructure, 67 million pet-owning households, and the FDA’s conditional-approval pathway that rewards early data packages. Canada adds volume via harmonized reviews, while Mexico offers cost-effective sites for poultry and swine vaccine work. Although regional CAGR moderates to 6.5% through 2031, North America will remain the largest component of the veterinary CRO market thanks to entrenched capacity and owner willingness to fund premium therapies.

Europe accounted for roughly 32% of global revenue, supported by EMA pharmacovigilance mandates that generate recurring service streams. Germany’s large swine population, the UK’s fast-track antimicrobial process, and France’s expansive companion-animal base concentrate trial activity in Western Europe. Regional growth is projected at 7.0%, aided by the EU Animal Health Law’s surveillance requirements, which sustain demand for epidemiology and diagnostics validation services.

Asia-Pacific is set to outpace all regions with an 8.65% CAGR, led by China’s USD 8 billion domestic veterinary-drug market and India’s vast cattle population. Expanded AAALAC accreditation, local approval of monoclonal antibodies, and government vaccination programs drive trial volume. Australia and Japan add high-compliance capacity, though longer regulatory timelines temper immediate revenue gains. Middle East & Africa and South America jointly deliver 8% of 2025 sales, yet infrastructure gaps and fragmented rules keep their share below 10% through 2031.

Competitive Landscape

The top five providers—Charles River Laboratories, Eurofins Scientific, Labcorp Drug Development, IDEXX Laboratories, and Envigo—command about 38% of revenue, indicating a moderately concentrated field. Scale advantages revolve around multi-species GLP sites, biosafety-level-3 containment, and integrated regulatory consulting that smaller firms struggle to replicate. Still, niche specialists thrive by focusing on single species or regional livestock markets, such as South Africa’s Clinvet, which focuses on swine vaccines.

Technology remains a key battleground. Large CROs deploy AI-enabled image analytics, blockchain for data integrity, and wearable biosensors to cut monitoring costs, widening the capability gap. Strategic moves include Charles River’s exclusive partnership with the NIH Comparative Oncology Trials Consortium and Eurofins’ acquisition of a UK toxicology lab, both aimed at adding specialized capacity.

Vendor consolidation is gathering pace as sponsors demand fewer, more capable partners. Hourly fees for high-end regulatory consulting now reach USD 400, more than double routine clinical-monitoring rates, underscoring the premium attached to dossier expertise. Telemedicine-enabled, decentralized-trial platforms may further disrupt the competitive order by slashing site-coordination costs and widening geographic patient pools.

Veterinary CRO Industry Leaders

Charles Laboratories Inc.

IDEXX Laboratories, Inc.

knoell Germany GmbH

Argenta Limited

Eurofins Scientific SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Zoetis introduced AI Masses, an in-clinic cytology module for the Vetscan Imagyst platform that uses deep learning to detect neoplastic cells

- January 2025: Absci and Invetx launched a generative-AI antibody design collaboration for animal health, with milestone-based royalties

- January 2025: Argenta Limited, one of the leading animal health pharmaceutical services company announced a strategic realignment of its animal health CRO platform to strengthen its capabilities and better serve the entire R&D and product development process in the industry. This move aims to enhance customer value and integrate its services more seamlessly.

Global Veterinary CRO Market Report Scope

As per the scope of the report, a veterinary CRO (Contract Research Organization) specializes in providing outsourced research services for veterinary medicine. They conduct clinical trials, regulatory submissions, and data management for animal health products. Their goal is to support the development and approval of veterinary pharmaceuticals and diagnostics.

The Veterinary CRO Market is Segmented by Service Type (Clinical Trials, Toxicology & Safety Studies, Regulatory & Consulting Services, and Other Specialized Services), Animal Type (Companion Animals [Dogs, Cats, and Other Companion Species], and Livestock [Cattle, Swine, Poultry, and Other Livestocks]), End User (Animal-Health Pharma & Biotech Companies, Academic & Research Institutes, Government & Non-Profit Sponsors, and Other End Users), Indication (Oncology, Infectious Diseases, Dermatology, Gastrointestinal Disorders, Neurology, and Other Indications), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Clinical Trials |

| Toxicology & Safety Studies |

| Regulatory & Consulting Services |

| Other Specialized Services |

| Companion Animals | Dogs |

| Cats | |

| Other Companion Species | |

| Livestock | Cattle |

| Swine | |

| Poultry | |

| Other Livestocks |

| Animal-Health Pharma & Biotech Companies |

| Academic & Research Institutes |

| Government & Non-Profit Sponsors |

| Other End Users |

| Oncology |

| Infectious Diseases |

| Dermatology |

| Gastrointestinal Disorders |

| Neurology |

| Other Indications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Clinical Trials | |

| Toxicology & Safety Studies | ||

| Regulatory & Consulting Services | ||

| Other Specialized Services | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Other Companion Species | ||

| Livestock | Cattle | |

| Swine | ||

| Poultry | ||

| Other Livestocks | ||

| By End User | Animal-Health Pharma & Biotech Companies | |

| Academic & Research Institutes | ||

| Government & Non-Profit Sponsors | ||

| Other End Users | ||

| By Indication | Oncology | |

| Infectious Diseases | ||

| Dermatology | ||

| Gastrointestinal Disorders | ||

| Neurology | ||

| Other Indications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the veterinary CRO market expected to be by 2031?

It is projected to reach USD 1.85 billion by 2031, growing at a 7.8% CAGR over 2026-2031.

Which region is forecast to grow fastest in outsourced veterinary research?

Asia-Pacific, supported by lower trial costs and expanding biosecurity programs, is set for an 8.65% CAGR through 2031.

What service line within contract research is expanding most rapidly?

Regulatory and consulting services should pace the field with a 9.43% CAGR as harmonized guidelines cut dossier redundancy.

Which animal segment is projected to add the most incremental revenue?

Livestock studies, especially swine vaccine programs, are forecast to grow at 9.66% per year to 2031.

Why are neurology trials gaining momentum in veterinary R&D?

Advances in gene therapy for canine epilepsy and other CNS disorders are drawing new funding, producing a 10.32% CAGR for neurology studies.

How concentrated is competition among veterinary CROs?

The top five providers hold about 38% of revenue, signaling moderate concentration with room for niche specialists.

Page last updated on: