Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.68 Billion |

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

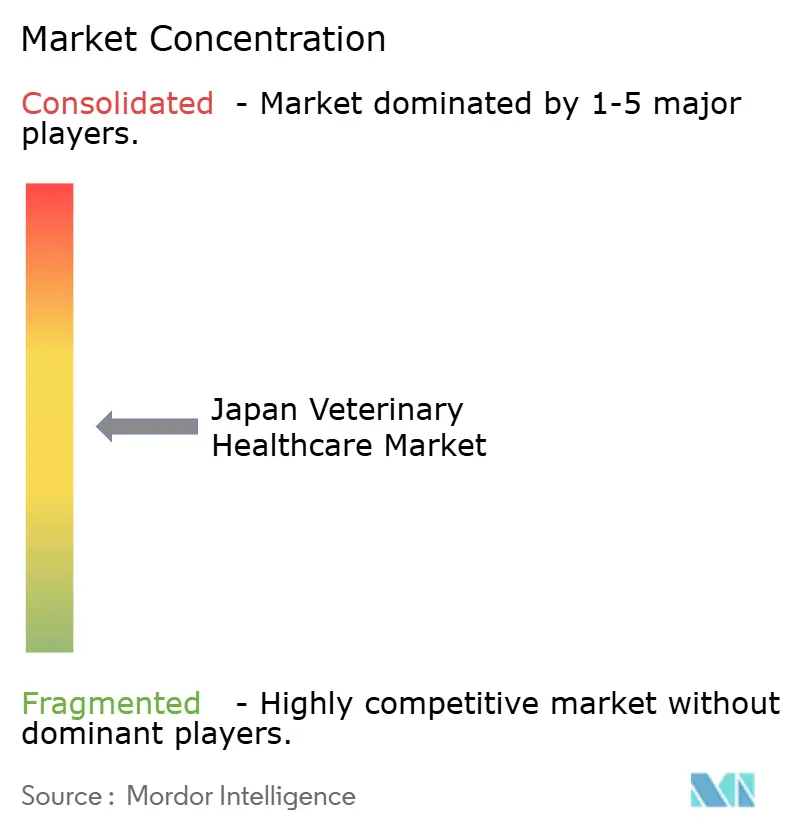

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Veterinary Healthcare Market Analysis by Mordor Intelligence

The Japan Veterinary Healthcare Market size is projected to be USD 2.68 billion in 2025, USD 2.85 billion in 2026, and reach USD 3.87 billion by 2031, growing at a CAGR of 6.34% from 2026 to 2031.

Multiple forces underpin this trajectory. Urban households are spending more on chronic-disease management for aging pets, while government vaccination mandates sustain baseline demand even as livestock herds contract. Diagnostic manufacturers are embedding AI in point-of-care analyzers, compressing turnaround times and reshaping referral patterns. Tele-veterinary platforms are starting to monetize prescription fulfillment in prefectures that face veterinarian shortages, and premium biologics are entering the companion-animal oncology pipeline despite a two-to-three-year MAFF approval lag. Counter-measures against counterfeit e-commerce drugs and regulatory harmonization under VICH further shape the competitive calculus.

Key Report Takeaways

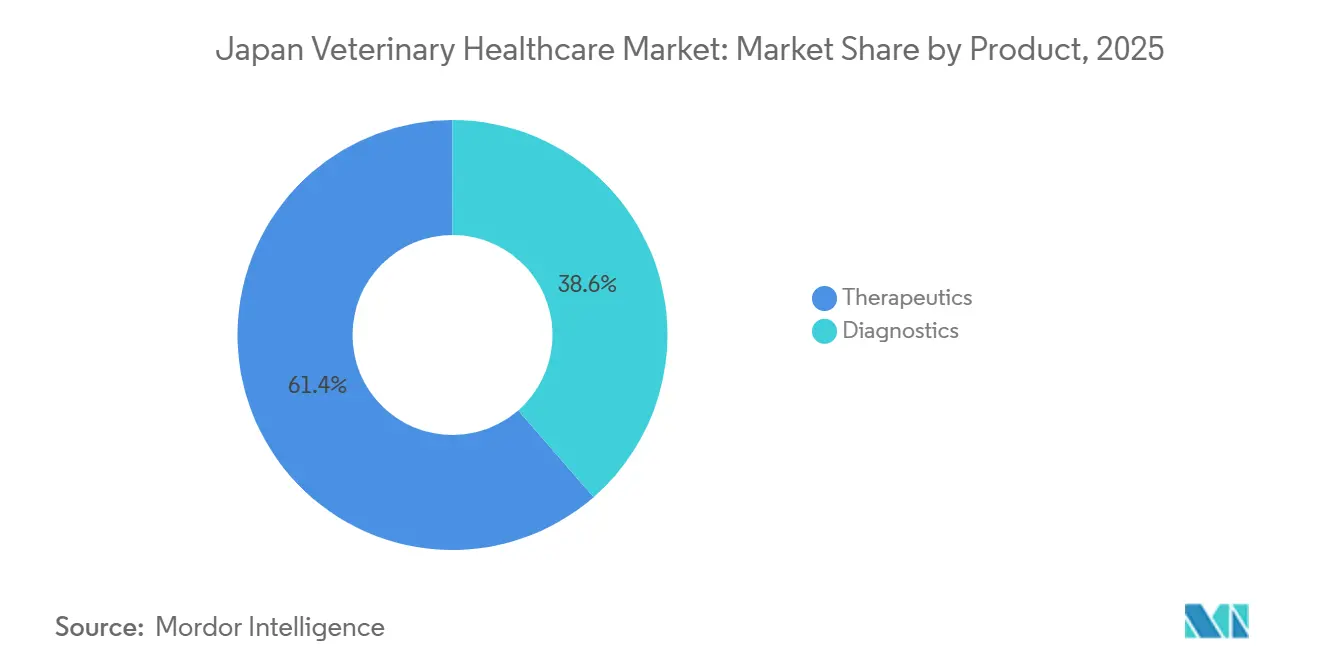

- By product category, therapeutics led with 61.4% of the Japan veterinary healthcare market share in 2025, while diagnostics is projected to expand at a 6.89% CAGR through 2031.

- By animal type, companion animals accounted for 54.1% share of the Japan veterinary healthcare market size in 2025, and livestock is forecast to grow at a 7.12% CAGR over 2026-2031.

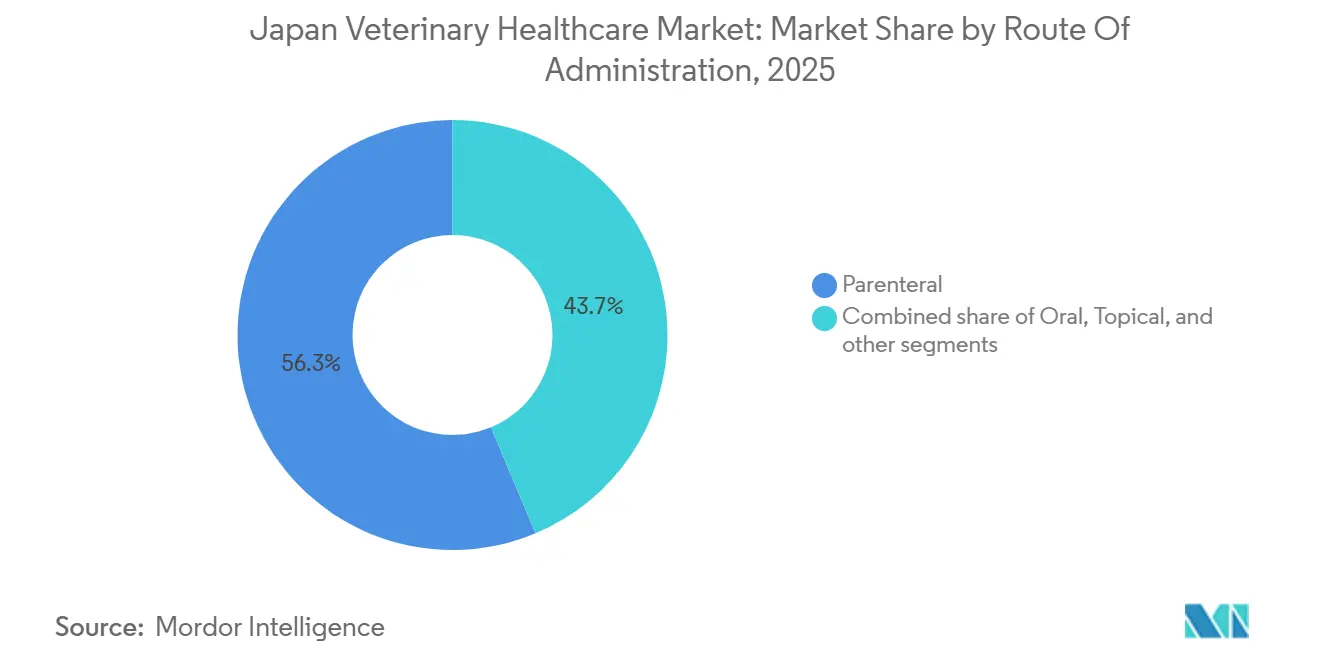

- By route of administration, parenteral formulations captured 56.3% revenue in 2025, whereas oral routes are advancing at a 7.33% CAGR to 2031.

- By end user, veterinary hospitals and clinics held 55.7% revenue share in 2025, while point-of-care and in-house diagnostic settings are set to rise at a 7.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Veterinary Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Companion-Animal Medical Spending | +1.2% | Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Government-Funded Livestock Vaccination Drives | +0.9% | Kyushu and Tohoku livestock regions | Short term (≤ 2 years) |

| Rapid Adoption of AI-Enabled Diagnostic Imaging Workflows | +0.8% | Urban multi-site veterinary chains | Medium term (2-4 years) |

| Growth of Tele-Veterinary Prescription Fulfillment Services | +0.6% | Rural prefectures with veterinarian shortages | Medium term (2-4 years) |

| Hospital Chains’ Shift to Subscription Wellness Plans | +0.5% | Tokyo, Kanagawa, Saitama | Long term (≥ 4 years) |

| Surging Demand for CBD-Based Nutraceuticals in Pets | +0.1% | Limited, Cannabis Control Act constraints | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Companion-Animal Medical Spending

Japanese owners now prioritize oncology, orthopedic, and advanced imaging services for pets, reflecting a steady rise in willingness to pay for specialized care. Anicom Holdings logged an 18% year-over-year jump in claims for cancer treatments and imaging in 2025, indicating elasticity despite overall household budget pressure [1]Anicom Holdings, “Annual Report 2024,” anicom-sompo.co.jp. The median age of pets surpasses eight years for dogs and seven for cats, inflating demand for chronic-disease pharmaceuticals. While premium procedures flourish in urban clinics, rural proprietors with low insurance penetration often defer costly interventions, creating a bifurcated spend profile that suppliers must navigate.

Government-Funded Livestock Vaccination Drives

Classical swine fever and highly pathogenic avian influenza outbreaks prompted MAFF to mandate vaccination through 170 Livestock Hygiene Service Centers, ensuring predictable vaccine uptake for local producers [2]Foreign Agricultural Service, “Japan Poultry and Products Annual 2024,” USDA, usda.gov. Although beef cattle inventories fell to 2.48 million head in 2024, per-animal vaccine spending is rising as multivalent protocols gain approval. Manufacturers with MAFF-accredited facilities maintain a defensible moat, whereas newcomers struggle to clear biological-assay hurdles within the required timelines.

Rapid Adoption of AI-Enabled Diagnostic Imaging Workflows

IDEXX and FUJIFILM embed machine-learning algorithms in digital radiography and ultrasound systems that flag anomalies seconds after exposure, freeing clinicians for consultative work and improving throughput [3]Foreign Agricultural Service, “Japan Poultry and Products Annual 2024,” USDA, usda.gov. Protein-level analyzers such as IDEXX’s SediVue Dx now complete urine sediment reviews 70% faster than manual microscopy, allowing same-day treatment starts. The top ten veterinary hospital chains operate more than 1,200 sites, and AI standardization helps them centralize radiology readings, creating switching costs that independent clinics struggle to match.

Growth of Tele-Veterinary Prescription Fulfillment Services

Anicom’s video-consultation platform dispenses prescriptions within 24 hours through regional pharmacies, addressing shortages in 47 prefectures where veterinarian-to-pet ratios are critically low. Consultation data feed actuarial models that flag high-risk pets, aligning insurer and owner incentives. However, MAFF rules require in-person exams for first diagnoses and restrict controlled-substance e-scripts, limiting telemedicine to chronic-care follow-ups and tempering near-term growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Veterinary Service Tariffs | -0.7% | Large metropolitan areas | Short term (≤ 2 years) |

| Proliferation of Counterfeit Pharmaceuticals | -0.5% | Online retail channels nationwide | Medium term (2-4 years) |

| Regulatory Lag for Novel Biologics Approvals | -0.4% | National | Long term (≥ 4 years) |

| Declining Domestic Cattle & Swine Inventory | -0.6% | Kyushu and Tohoku livestock regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Veterinary Service Tariffs

Average clinic visit fees rose 12% between 2024 and 2025 as labor scarcity and metropolitan real-estate costs inflated operating expenses. Insurance covers only about 10% of pets, forcing many owners to pay out-of-pocket. One fifth of policyholders postponed recommended procedures in 2025 due to cost, and the deferral rate exceeds one third among uninsured households. This price sensitivity compresses demand for routine vaccinations and diagnostics in the mass segment, even as premium clients continue to fund complex surgeries.

Proliferation of Counterfeit Pharmaceuticals

Interpol’s Operation Thunder seized hundreds of illicit veterinary shipments in 2024, exposing gaps in e-commerce gatekeeping. Substandard products erode brand trust when treatments fail, driving veterinarians to stock only proven lines and increasing compliance risk for smaller suppliers. MAFF and Customs intensified port inspections, but counterfeit listings reappear quickly online, sustaining the drag on legitimate revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostics Outpace Therapeutics on Technology Pivot

Therapeutics controlled 61.4% of 2025 revenue, yet diagnostics is advancing at a 6.89% CAGR, the fastest clip within the Japanese veterinary healthcare market. IDEXX real-time PCR panels detect 12 pathogens in under 90 minutes, enabling same-day therapy decisions that compress hospital stays. Immunodiagnostic ELISA kits still ship the highest volumes, but molecular platforms and digital pathology siphon incremental spend as clinics chase sensitivity gains. Monoclonal antibodies occupy the premium tier of therapeutics, but their roll-out lags global markets due to MAFF approval cycles. Meanwhile, feed-additive suppliers confront shrinking livestock herds and are repurposing probiotic lines for aquaculture.

Whole-slide scanners coupled with AI pattern recognition blur the boundary between diagnostics and therapeutics, supporting precision medicine that aligns drug choice with tumor histology. Manufacturers that bundle reagents, imaging software, and cloud analytics into subscription models lock clinics into proprietary ecosystems. Smaller laboratories may struggle to justify capital outlays, but group practices exploit volume discounts to reach breakeven faster. The interplay between comprehensive test menus and AI workflows explains why diagnostics will keep eroding the therapeutics share of Japan veterinary healthcare market size over the forecast window.

By Animal Type: Livestock Growth Defies Herd Contraction

Companion animals delivered 54.1% of 2025 spending, a lead driven by 8.76 million cats and 6.89 million dogs, yet livestock pharmaceuticals are on track for a 7.12% CAGR that outstrips feline and canine growth. Vaccination mandates following classical swine fever outbreaks assure steady volume even as bird culls climbed to 17.71 million during 2022-2023. MAFF-backed centers now deliver trivalent shots against CSF, PRRS, and circovirus, tripling per-animal costs relative to monovalent formulations.

Dog ownership is slipping as urban apartments favor smaller pets, which boosts demand for feline leukemia and FIV vaccines. Orthopedic and dental services, once mainstays of dog care, face deceleration, prompting clinics to diversify into geriatric feline medicine. Equine health remains niche, and aquaculture, while not charted as a formal segment, presents an emergent frontier as fish farms seek immunity against viral hemorrhagic septicemia.

By Route of Administration: Oral Gains on Compliance Innovation

Parenteral delivery captured 56.3% of 2025 revenue, reflecting clinician confidence in injectable bioavailability. Oral products, however, are growing at 7.33% and threaten to rebalance the Japanese veterinary healthcare market size in chronic segments. Zoetis’ Simparica Trio grabbed an 18% slice of the flea-and-tick market within a year of its 2024 launch, validating palatable chewables that bundle multiple actives. Sustained-release matrices and flavor enhancers push owners toward at-home administration, which frees clinic time for high-value procedures.

Topicals are shedding share amid concerns over residue transfer to children, while niche routes such as subcutaneous implants find footing in heartworm prevention. Regulatory requirements to prove bioequivalence when shifting routes extend development by up to two years, deterring smaller firms from reformatting legacy injectables.

By End User: Point-of-Care Disrupts Hospital Referrals

Hospitals and clinics generated 55.7% of 2025 spending, but point-of-care analyzers are climbing at 7.09% CAGR, reflecting veterinarians’ desire to control diagnostic revenue inside the practice. IDEXX Catalyst units deliver blood-chemistry panels in ten minutes, eliminating external-lab courier delays and capturing margin that once went elsewhere. Claims data show that in-clinic tests rose from 24% of total diagnostics in 2023 to 31% in 2025, a trend projected to continue.

Academic institutes has lower share of the budget yet set influential practice guidelines. As point-of-care sophistication rises, hospital chains justify premium pricing by offering oncology, cardiology, and neurology services that telemedicine and small clinics cannot match. Vendors must supply integrated software that feeds results into electronic records in real time, cementing brand stickiness across decentralized networks.

Geography Analysis

Metropolitan prefectures Tokyo, Kanagawa, Osaka, and Aichi accounted for the majority of companion-animal expenditure in 2025, powered by dense ownership, higher income, and an abundance of multi-site hospital chains. These regions host most specialty referral centers, allowing clinicians to command premium fees for orthopedic, cardiology, and oncology services. The clustering effect draws pet owners from adjacent prefectures, amplifying spending far beyond local populations.

Rural areas such as Hokkaido and Shimane endure veterinarian shortages, with fewer than one doctor per 5,000 pets. Tele-consultation tools fill part of the gap, yet the MAFF prescribing rules keep the penetration low of all consultations in 2026. Meanwhile, livestock-heavy prefectures in Kyushu and Tohoku command robust vaccine volumes even as producer demographics age. Kagoshima alone houses a notable share of Japan’s swine inventory and broilers, anchoring local production hubs for Nisseiken and Nippon Zenyaku Kogyo.

Second-tier cities such as Fukuoka, Sapporo, and Sendai show rising pet uptake among households aged 25-40 but lack sophisticated veterinary infrastructure. Hospital groups eye these markets for expansion, leveraging centralized cloud diagnostics to sidestep local expertise deficits. VICH harmonization now allows products licensed in the European Union or United States to secure accelerated approvals, compressing time-to-market for global suppliers and pressuring domestic incumbents who previously exploited regulatory barriers.

Regulatory Landscape

Japan regulates veterinary medicinal products and related biologics through the Ministry of Agriculture, Forestry and Fisheries (MAFF), with the National Veterinary Assay Laboratory (NVAL) conducting technical examinations, setting assay standards, and supporting approvals and compliance. Marketing approval requires robust quality, efficacy, and safety documentation aligned to Japanese requirements, including usage limitations such as withdrawal periods for food-producing animals, and conformity with GLP, GCP, and GVP expectations as assessed through the review framework that includes the Pharmaceutical Affairs and Food Sanitation Council (PAFSC).

In 2026, MAFF activity underscored continuing tightening and clarification of use standards for specific actives and biologicals. In March 2026, MAFF issued notifications amending standards for veterinary biological products and specific usage criteria for veterinary drugs containing ketoprofen (effective May 1, 2026), while June 2026 public-comment activity covered revisions to the Ministerial Ordinance on the Regulation of Veterinary Drugs (including consultation around tylosin tartrate feed-additive use for bees). These updates reinforce the need for Japan-ready dossiers and post-market compliance processes, particularly for products where residue control, food safety, and species-specific labeling constraints intersect.

Competitive Landscape

The top five multinationals hold a majority share, while domestic firms claim notable signaling moderate concentration within the Japanese veterinary healthcare industry. Global leaders focus on companion-animal biologics and AI-linked diagnostics, exploiting R&D scale and digital capabilities. Local companies defend livestock vaccine niches through intimate MAFF relationships, cold-chain logistics, and rapid outbreak response.

Vertical integration is reshaping boundaries as insurers like Anicom employ telemedicine to bypass traditional referrals and bundle preventive-care subscriptions. AI standardization also spurs consolidation: IDEXX filed 14 AI-diagnostic patents from 2024-2025, while Zoetis logged eight oral sustained-release patent applications. E-commerce entrants exacerbate price transparency for routine parasiticides, pressuring clinic margins.

Strategic alliances accelerate vaccine innovation. Boehringer Ingelheim teamed with Nippon Zenyaku to marry an mRNA platform with domestic regulatory know-how, pursuing a swine bivalent vaccine with 2027 approval targets. Elanco bought Kyorin’s dermatology portfolio to bolster its standing in a segment that accounts for 14% of consultations. Local manufacturing upgrades, like Kyoritsu Seiyaku’s aseptic line, underscore the need for GMP compliance as biologics volumes scale.

Japan Veterinary Healthcare Industry Leaders

Zoetis Inc.

Kyoritsu Seiyaku Corp.

Boehringer Ingelheim GmbH

Elanco Animal Health Incorporated

FUJIFILM Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A practical opportunity area centers on speeding development-to-approval execution for novel therapeutics and advanced diagnostics by working within MAFF's centralized review framework, including use of MAFF's Pre-Application Team Consultation for high-novelty or high-social-need products. For companies building companion-animal oncology, chronic-disease, or advanced in-clinic diagnostic propositions, early alignment to NVAL test expectations and MAFF review pathways can reduce rework on study design and CMC packages, which becomes more consequential in a market already flagged for multi-year approval lags for novel biologics.

Government disease-control architecture also creates structured demand touchpoints that vendors can align to: MAFF policy flows through prefectural Livestock Hygiene Service Centers that execute surveillance and vaccination programs under the Act on Domestic Animal Infectious Diseases Control. This supports whitespace for suppliers that can deliver compliant vaccines, testing reagents, and monitoring workflows into these programs, including products that align with multivalent vaccination protocols referenced in market dynamics. On the companion side, insurer-linked tele-veterinary prescription fulfillment and the rise of AI-enabled point-of-care diagnostics inside clinics create room for integrated offerings that connect testing, prescribing, and follow-up care within MAFF prescribing constraints, including limits around first diagnoses and controlled substances.

Recent Industry Developments

- March 2026: Kyoritsu Seiyaku and bitBiome announced a joint development and collaboration agreement to apply advanced biotechnology to animal health and nutrition products. The partnership expands Kyoritsu's platform options for next-generation R&D, supporting differentiation beyond traditional pharmaceuticals in segments tied to pet chronic disease management and preventive nutrition.

- March 2025: A Japanese research team led by Dr. Toru Miyazaki disclosed an AIM (apoptosis inhibitor of macrophage) protein injection concept aimed at feline chronic kidney disease, with stated intent to move the therapy toward veterinary use. The work highlights active innovation in high-burden companion-animal chronic conditions, an area where new modalities can reshape premium-care demand and clinic treatment pathways.

- August 2024: Zoetis received regulatory approval in Japan for Draxxin KP (tulathromycin and ketoprofen) for treatment of bacterial pneumonia in cattle. The approval strengthens Zoetis' presence in food-animal therapeutics where MAFF review and label conditions are decisive, and it raises the competitive bar for combination products that must satisfy efficacy and use-criteria requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Japan veterinary healthcare market is counted as the value of products and services used to prevent, diagnose, and treat animal diseases in Japan, as purchased through veterinary care settings and channels.

Scope exclusions: We exclude human healthcare products, pet food and accessories, and non-medical grooming and boarding services.

Segmentation Overview

- By Product

- Therapeutics

- Vaccines

- Parasiticides

- Anti-infectives

- Medical Feed Additives

- Monoclonal Antibodies & Biologics

- Diagnostics

- Immunodiagnostic Tests

- Molecular Diagnostics (PCR, qPCR, NGS)

- Diagnostic Imaging

- Clinical Chemistry & Hematology

- Digital Pathology & AI Platforms

- Therapeutics

- By Animal Type

- Companion Animals

- Equine

- Livestock

- By Route of Administration

- Oral

- Parenteral

- Topical

- Other Routes

- By End User

- Veterinary Hospitals & Clinics

- Academic & Research Institutes

- Point-of-Care / In-House Settings

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the market boundaries, build the timeline, and collect measurable signals that reflect demand in Japan. We mainly relied on public and official sources such as the Ministry of Agriculture, Forestry and Fisheries (MAFF) statistics and animal health updates, the Statistics Bureau of Japan, Japan Customs trade data, and guidance from the World Organisation for Animal Health (WOAH) and peer reviewed veterinary journals.

To convert these signals into a usable market model, we also reviewed company annual reports and investor presentations, association websites, and reputable press to understand product uptake, pricing direction, and policy impacts. In a few places, paid subscriptions were used for company financials and patent landscaping to check innovation pipelines and product momentum. The desk research sources listed here are illustrative only, and many other references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary conversations and structured surveys were used to pressure test assumptions that desk sources do not fully explain, especially around clinic purchasing behavior and pricing changes. We spoke with veterinary hospital and clinic stakeholders, reference lab and in house testing users, distributors, and industry specialists across Japan so the final inputs reflect real buying and usage patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | |

| Mid tier: 51% | Functional/Unit leaders: 27% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where Japan animal healthcare demand is reconstructed from treated animal pools and care intensity, and then translated into spend by applying typical therapy and diagnostic use rates. We anchor the model on a few practical inputs, including estimated companion animal and livestock populations, visit frequency at veterinary hospitals and clinics, testing adoption in point of care settings, vaccination and parasiticide compliance patterns, and average selling price movement for key therapy and diagnostic baskets.

Those totals are then checked using selective bottom-up approximations, such as sample supplier revenue splits, channel checks from distributors, and sampled volume times ASP for fast moving categories, which helps us adjust for gaps where public data is thin. For forecasting, scenario analysis is used because policy shifts, disease outbreaks, and insurance uptake can quickly change demand, and then key variables are stress tested with expert feedback to keep the trajectory realistic.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and large variances are flagged for re-check before sign off. We compare the implied spend per visit and per treated case against clinic workflows, trade movement, and product mix expectations, and then outliers are reviewed in a second analyst pass.

The report is refreshed annually, and interim checks are triggered when material events occur, such as regulatory changes, supply disruptions, or unusual disease activity. Before delivery, a final review pass is completed so clients receive the latest consistent view based on the most recent data available.

Mordor Intelligence's Japan Veterinary Healthcare Market Market Size Measured Against Other Published Estimates

Published market values for Japan veterinary healthcare can look different across sources because the scope boundary is not always the same, and the timing of price updates can shift the reported USD value in a meaningful way. Differences also show up when diagnostics are treated as a smaller add on versus being counted as a full value stream alongside therapeutics.

Refresh cadence and currency timing matter in this market because many products are priced with periodic list updates, while the reported value is still expressed in USD, which can change year to year even if local demand is steady. By updating ASP logic using current product mix signals and re-checking outputs against clinic utilization and testing adoption, Mordor Intelligence reduces drift caused by stale pricing assumptions and older conversion rates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.68 B (2025) | |

| Industry Publisher A | USD 2.30 B (2025) | This estimate appears to align more tightly to veterinary medicines, with a lighter treatment of diagnostics and service-adjacent testing spend, which can pull the total down in Japan. |

| Global Publisher B | USD 2.68 B (2024) | The year is earlier and the conversion timing can shift the USD figure, and the longer forecast window suggests assumptions may be carried forward without frequent re-validation of clinic pricing and test adoption. |

The table shows that the biggest spread is usually explained by what gets counted as veterinary healthcare in practice, and whether pricing and USD conversion are updated close to the base year. When the scope is clearly bounded and the inputs are repeatedly checked against real care and testing behavior, the final market size becomes easier to trace and reuse in planning.

Key Questions Answered in the Report

How fast is companion-animal spending growing in Japan?

Claims data show an 18% rise in oncology and imaging reimbursements during 2025, reflecting robust demand even with low insurance coverage.

Which product class is expanding the quickest?

Diagnostics lead with a 6.89% CAGR to 2031 as AI-enabled molecular and imaging tools displace manual assays.

Why do oral formulations matter now?

Palatable chewables like Simparica Trio gained 18% flea-and-tick share within a year by improving owner compliance.

How significant are livestock vaccines despite herd decline?

Multivalent CSF-PRRS-circovirus protocols boost per-animal spend, pushing livestock pharmaceuticals toward a 7.12% CAGR through 2031.

What role does telemedicine play in rural prefectures?

Video consultations mitigate veterinarian shortages, yet MAFF rules on controlled drugs limit remote care to chronic-disease follow-ups.

Page last updated on: