Veterinary Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

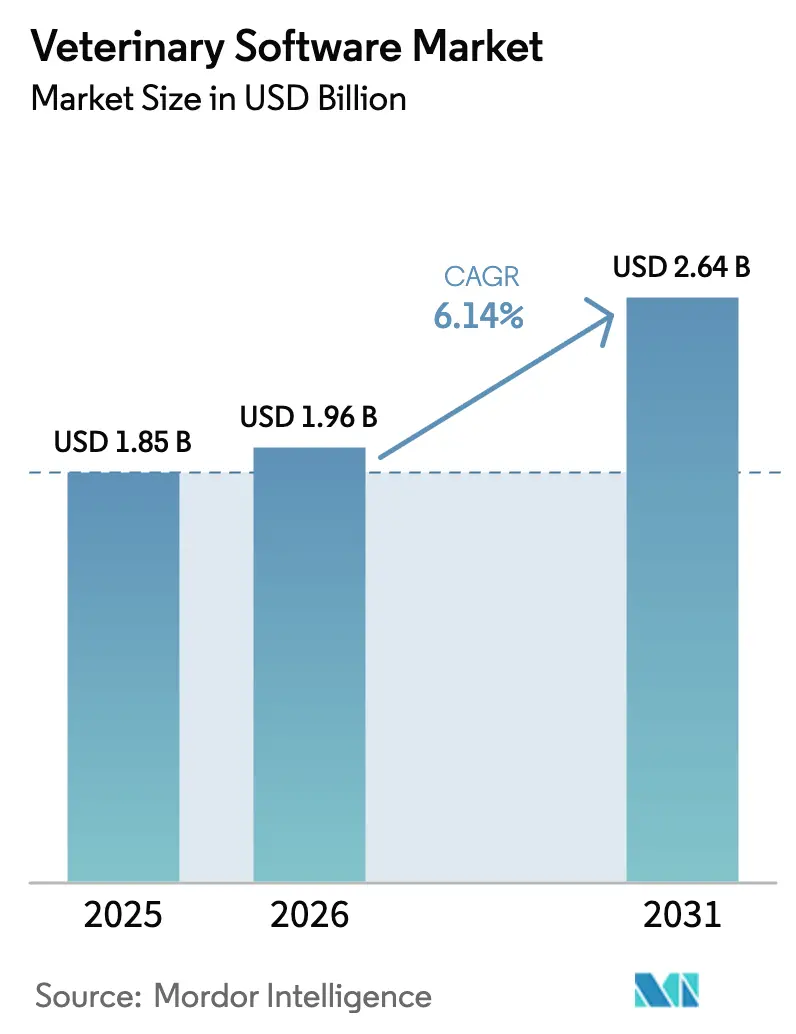

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 2.64 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Software Market Analysis by Mordor Intelligence

The Veterinary Software Market size is expected to increase from USD 1.85 billion in 2025 to USD 1.96 billion in 2026 and reach USD 2.64 billion by 2031, growing at a CAGR of 6.14% over 2026-2031.

The measured headline growth conceals a decisive inflection: consolidation among clinic chains is driving enterprise-level buying criteria, while new data-reporting rules in Europe and North America are turning optional digitization into a compliance necessity. Practice-management platforms remain the leader because they automate billing, inventory, scheduling, and clinical charting; however, telehealth engines are scaling quickly as owners seek always-on care and insurers reimburse virtual visits. Clinic consolidators are standardizing on cloud systems to harvest benchmarking data across hundreds of locations. In contrast, independents still cling to on-premises installs that shield them from bandwidth interruptions but expose them to higher maintenance risk. Vendors that combine analytics, diagnostics, and secure data exchange now win the majority of new contracts, underscoring an industry shift from license revenue to recurring cloud subscriptions.

Key Report Takeaways

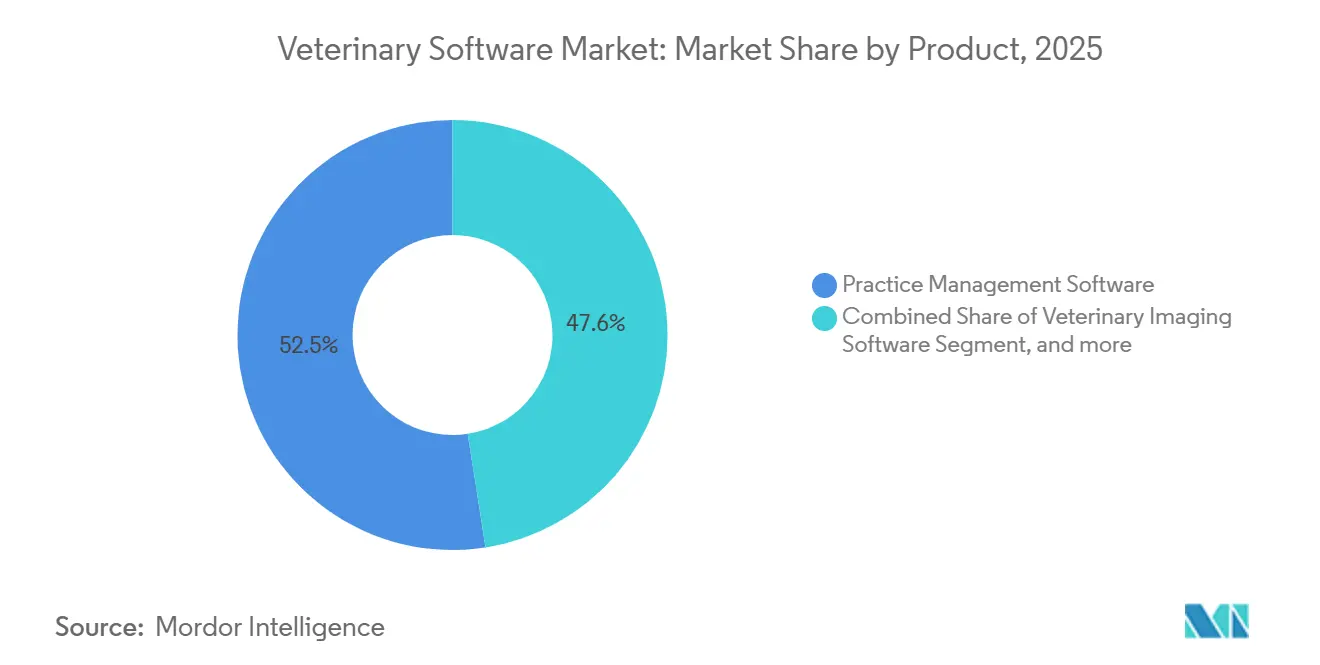

- By product category, practice-management software led with a 52.45% veterinary software market share in 2025, while telehealth platforms are forecast to expand at an 8.54% CAGR through 2031.

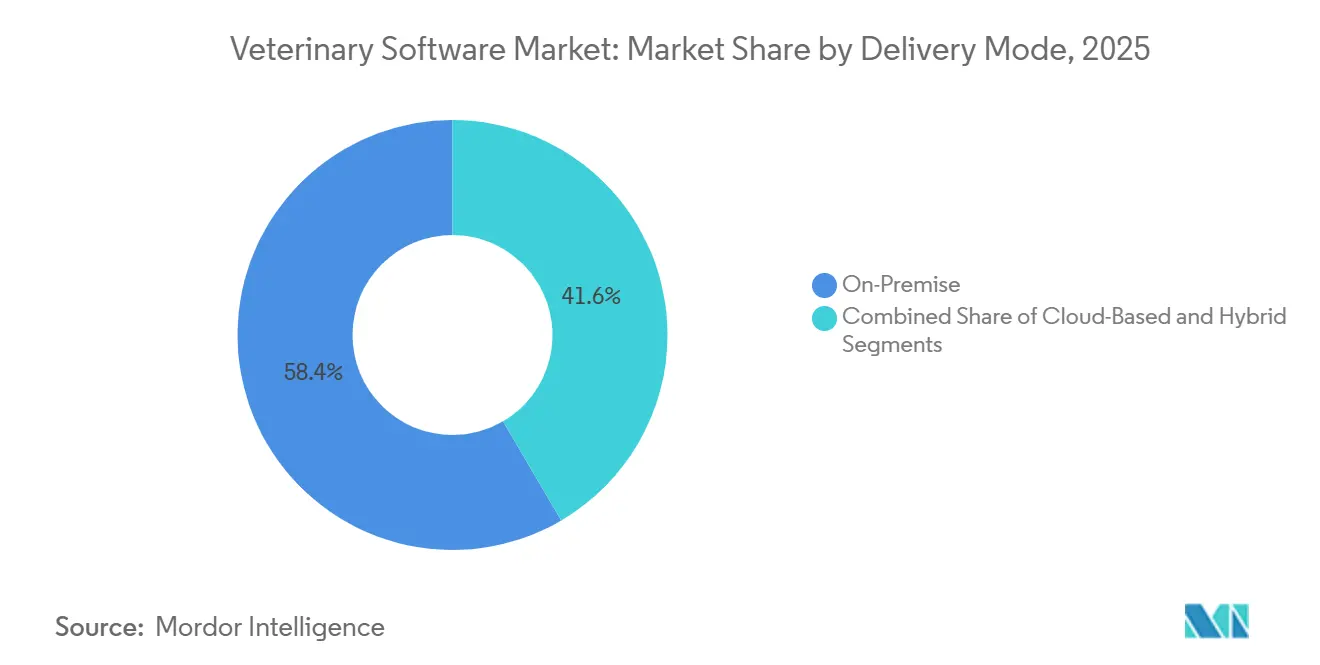

- By delivery model, on-premise deployments held 58.43% share of the veterinary software market size in 2025, whereas cloud solutions are advancing at an 8.01% CAGR through 2031.

- By animal type, companion-animal platforms accounted for 55.67% of 2025 revenue, and equine-specific software is rising at an 8.78% CAGR through 2031.

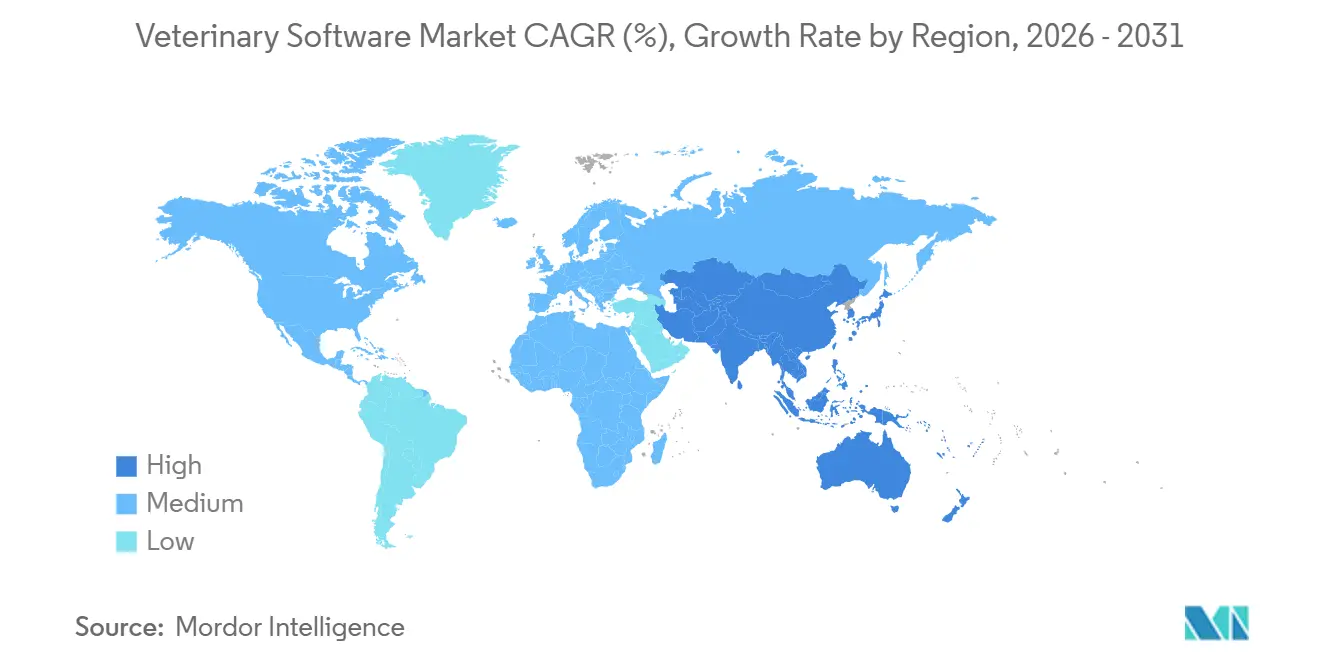

- By geography, North America captured 45.32% of 2025 revenue, while Asia-Pacific is projected to record a 7.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Veterinary Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Companion Animal Ownership and Healthcare Expenditure | +1.80% | Global, concentrated in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing Adoption of Cloud-Based Practice-Management Systems | +1.50% | North America and EU lead, Asia-Pacific core following | Medium term (2-4 years) |

| Integration of Diagnostic Imaging and Laboratory Workflows with PIMS | +1.20% | North America, Europe, Australia | Short term (≤ 2 years) |

| Expansion of Telehealth and Remote Consultation Services | +1.00% | Global, accelerated in North America post-2024 | Short term (≤ 2 years) |

| Consolidation of Veterinary Clinic Chains Driving Enterprise Software Demand | +0.90% | North America, United Kingdom, Australia | Long term (≥ 4 years) |

| Emergence of Data Analytics and Business Intelligence for Practice Optimization | +0.70% | North America, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Companion Animal Ownership and Healthcare Expenditure

Pet ownership climbed to record levels in 2024, with U.S. households spending USD 147 billion on pets, including USD 38.3 billion on veterinary care. Clinics that once relied on paper files now need longitudinal records, automated recalls, and mobile payment tools to keep pace with preventive and specialty care. Vendors have responded by embedding client-communication portals that trim no-show rates by up to 30%, directly lifting revenue per visit. Higher case complexity creates a virtuous cycle: sophisticated software enables data-driven treatment plans, and successful outcomes justify premium pricing. The United Kingdom offers a parallel example: CVS Group standardized 500-plus clinics on Provet Cloud in 2024 to unlock chain-wide benchmarking and compliance reporting, transforming software from a cost center into a profit lever.

Growing Adoption of Cloud-Based Practice-Management Systems

Cloud practice-management suites eliminate server purchases, shorten deployment windows, and provide instant access to patient files across sites. IDEXX launched the Vello platform in February 2024, allowing clinics to add new locations in days while pulling diagnostic data straight into the medical chart. Compliance is another catalyst: the European Union’s Regulation 2019/6 demands electronic antimicrobial reporting, a task cloud systems handle with automated uploads, whereas legacy platforms need manual exports [1]European Medicines Agency, “Veterinary Regulation 2019/6,” ema.europa.eu. Subscription fees ranging from USD 200–800 per veterinarian per month convert large capital outlays into predictable operating expenses that align vendor incentives with clinic success. Rural practices still worry about bandwidth and sovereignty, but hybrid models that keep local data for daily workflow while syncing to the cloud for analytics are easing that concern.

Integration of Diagnostic Imaging and Laboratory Workflows with PIMS

Diagnostic imaging and laboratory results now flow directly into patient records through DICOM and HL7-style interfaces. IDEXX’s Web PACS pipes radiographs into the Neo platform so specialists can review images remotely within hours rather than days. In emergency settings, that speed shortens triage, reducing morbidity and raising client satisfaction. Laboratory data follow an identical path: in-house analyzers from IDEXX, Zoetis, and Heska push values straight to the chart, eliminating transcription errors. The European Medicines Agency’s Big Data Strategy prioritizes open APIs to support pharmacovigilance, providing regulatory lift for vendors that invest in interoperability.

Expansion of Telehealth and Remote Consultation Services

Telehealth platforms matured quickly after regulators clarified prescribing rules in 2024. FirstVet raised EUR 20 million in June 2024 and now connects 400 veterinarians with 5 million insured pets across two continents[2]FirstVet, “Series C Funding Announcement,” firstvet.com. TeleVet followed with USD 2 million in March 2025 to grow its asynchronous consultation tool that slashes unnecessary emergency visits by 25%. The U.S. Drug Enforcement Administration now allows controlled-substance prescriptions after telehealth visits under specific safeguards, removing a major adoption hurdle. Aggregated consultation data also feed public-health dashboards, aligning with the European Health Data Space regulation implemented in March 2025.

Restraints Impact Analysis of Veterinary Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Acquisition and Implementation Costs | -1.30% | Global, acute in emerging markets and independent practices | Short term (≤ 2 years) |

| Data Security, Privacy, and Cyber-Threat Concerns | -0.90% | North America, EU (GDPR-driven), Australia | Medium term (2-4 years) |

| Limited Digital Infrastructure in Emerging Markets | -0.60% | Asia-Pacific (excluding Japan, Australia), Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Fragmented Regulatory and Interoperability Standards | -0.50% | Global, most acute in United States (state-level variance) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Acquisition and Implementation Costs

Complete migration can exceed USD 50,000 for a mid-sized clinic once hardware, data conversion, and staff training costs are factored in. A 2024 American Veterinary Medical Association survey found that 42% of respondents cited cost as the chief barrier[2]FirstVet, “Series C Funding Announcement,” firstvet.com. Productivity often dips for three to six months after the go-live date as teams adjust to the new workflows. While cloud models lower capital outlay, annual subscription fees of USD 10,000 or more per veterinarian can strain practices that are already thinly capitalized. Tiered pricing helps but risks fragmenting feature sets, slowing the network effects that anchor platform value.

Data Security, Privacy, and Cyber-Threat Concerns

Ransomware attacks against veterinary clinics increased in 2024, leading to a steady rise in cyber-insurance premiums. Penalties under GDPR reach 4% of annual revenue, so smaller European practices hesitate to move sensitive data online without assurances such as ISO 27001 audits[3]European Commission, “General Data Protection Regulation,” europa.eu. In the United States, the patchwork of state privacy laws forces vendors to juggle jurisdiction-specific settings, inflating development expense. The absence of a federal veterinary-privacy statute leaves clinics vulnerable to multi-state litigation when breaches occur, thereby intensifying the perceived risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Veterinary Software Market Segment Analysis

By Product:

Practice-Management Platforms Anchor Revenue, Telehealth AcceleratesPractice-management suites booked 52.45% of 2025 revenue, validating their role as the digital spine for scheduling, billing, medical records, and stock control. IDEXX Neo and Covetrus Ascend bundle integrated payments, diagnostics connectivity, and automated recalls, locking in users through workflow depth. Telehealth engines hold a smaller denominator but are scaling at an 8.54% CAGR to 2031. The investment signals are clear: FirstVet raised EUR 20 million in 2024, and TeleVet added USD 2 million in 2025 to extend asynchronous triage. Beyond pure remote care, imaging platforms such as Web PACS offer DICOM-compliant storage for referral traffic, while IDEXX inVue Dx marries on-site diagnostic hardware with cloud decision support.

Competition now pivots toward convergence. Vendors design single dashboards that surface lab flags, imaging thumbnails, and teleconsult transcripts inside the standard chart. The approach raises switching costs and underpins a durable subscription stream. Compliance modules have become mandatory; for instance, European clinics cannot submit antimicrobial data without in-app reporting. As a result, investors reward platforms that own end-to-end data pipelines rather than point solutions.

By Delivery Model:

On-Premise Still Dominant, Cloud Makes Rapid InroadsOn-premise setups accounted for 58.43% of 2025 installations, reflecting sunk server costs and long-standing fears over cloud latency in rural areas. Nevertheless, cloud deployments are growing at an 8.01% CAGR, propelled by subscription economics and automatic updates that slash IT overhead. IDEXX Vello targets greenfield clinics with multi-location reporting straight out of the box, whereas Provet Cloud’s 2025 U.S. pilot shows that European vendors can win deals by pairing data-privacy pedigree with modern UX.

Hybrid models balance both worlds: clinics keep a lightweight local server for uptime assurance, while daily backups and analytics flow to a cloud vault. This framework aligns nicely with Regulation 2019/6, which favors seamless antimicrobial uploads, and permits chain headquarters to run groupwide dashboards without burdening local bandwidth. Certification has moved from marketing line-item to procurement checkbox; SOC 2 Type II has become the baseline for North American corporate buyers, while ISO 27001 remains the gold standard in Europe.

By Animal Type:

Companion Leads, Equine Gains TractionCompanion-animal platforms delivered 55.67% of 2025 demand. Their feature set prioritizes two-way messaging, smartphone payments, and preventive-care reminders tailored to cats and dogs. North American and Western European clinics cite client communication as their biggest differentiator, reinforcing the segment’s software spend. Equine platforms, though niche, exhibit an 8.78% CAGR thanks to racing and breeding operators that need pedigree tracking, sensor integrations, and complex medication logs. Products such as ezyVet’s equine module and Shepherd’s dedicated workflow tools parse competition results and sync with national registries.

Livestock and mixed-practice solutions remain underdeveloped. Farm-management systems track herd nutrition, yet often sit outside clinical recordkeeping, hobbling disease traceability. As one-health frameworks expand, regulators may soon require integrated dashboards that connect prescription data with farm outcomes. Vendors capable of folding herd metrics into their core PIMS therefore stand to capture untapped white space.

Geography Analysis

North America Veterinary Software Market

North America maintained 45.32% of 2025 revenue, underpinned by high per-pet healthcare spend and aggressive clinic roll-up strategies. Mars Veterinary Health, National Veterinary Associates, and Thrive Pet Healthcare now manage thousands of outlets, each demanding unified platforms for billing, inventory, and teleconsults. The region’s maturity means nearly every clinic uses basic software, so growth comes from layering predictive analytics, AI diagnostics, and real-time supply chain dashboards on top of existing records. Canada mirrors U.S. adoption but adds provincial privacy nuances that oblige configurable user-consent workflows. Private-equity appetite confirms the thesis: Patient Square Capital’s USD 4.1 billion acquisition of Patterson Companies in December 2024 hinged partly on cross-selling software to the distributor’s installed base.

APAC Veterinary Software Market

Asia-Pacific is the fastest-growing arena, posting a 7.43% CAGR through 2031. China represents roughly 40% of regional spend, but software uptake is fragmented across local vendors that tailor interfaces to Mandarin and integrate with domestic payment rails. India’s public investment in digital livestock monitoring aims to lift productivity and disease surveillance, yet patchy rural connectivity still limits cloud migrations. In contrast, Japan and Australia approach North American penetration levels, favoring premium analytics and full diagnostics integration. Multilingual support, local cloud hosting, and currency-specific billing are non-negotiable, forcing Western incumbents to partner with regional integrators or risk losing to homegrown competitors.

EMEA and LATAM Veterinary Software Market

Europe occupies the middle ground in share but leads in policy innovation. Regulation 2019/6 has already shifted antimicrobial tracking online, and the Big Data Strategy outlines a centralized EU Veterinary Data Hub. The European Health Data Space, effective March 2025, adds zoonotic-disease surveillance, pushing clinics toward cloud or hybrid deployments capable of secure data exchange. Nordhealth’s partnerships with CVS Group and Vets for Pets prove that platforms built around GDPR resilience can pull business from domestic rivals. Latin America and the Middle East & Africa trail in infrastructure. Urban pockets such as São Paulo, Mexico City, and Dubai are early adopters, using cloud suites to circumvent local IT shortages, but rural areas remain largely paper-based.

Regulatory Landscape

Regulation is tightening around both clinical data exchange and the conditions under which remote care can be delivered. In the European Union, Regulation (EU) 2019/6 has made electronic antimicrobial reporting a practical requirement for many clinics, which is raising demand for compliant reporting workflows inside practice information management systems (PIMS). Separately, the Veterinary International Conference on Harmonisation (VICH) provides a cross-region anchor for electronic regulatory documentation through GL53, which standardizes electronic exchange and file formats across the EU, United States, and Japan.

In the United States, software governance spans clinical decision support and telehealth. The FDA updated its Clinical Decision Support (CDS) guidance in January 2026, clarifying which software functions fall outside the medical device definition, and followed with Computer Software Assurance (CSA) guidance in February 2026 for production and quality management system software. Telehealth is still governed primarily through state-level rules tied to the Veterinary-Client-Patient Relationship (VCPR); the American Association of Veterinary State Boards (AAVSB) released updated Model Regulations for Telehealth and Virtual Practice in March 2026 that maintain a VCPR cannot be established solely through virtual means, reinforcing the need for configurable, jurisdiction-aware telehealth and documentation features.

Value Chain Analysis

The veterinary software value chain starts with platform development, including PIMS, imaging, telehealth, analytics, and client engagement modules. It then shifts to implementation partners and integrations, such as diagnostic instruments, laboratory systems, payments, and communications, before reaching clinic users where chains and independents face different procurement and deployment requirements. Large vendors and distributors, including IDEXX (Neo, Cornerstone, ezyVet), Covetrus (AVImark, Impromed, Pulse), and Patterson (NaVetor), influence buying decisions by bundling software with diagnostics, pharmaceuticals, and practice supplies. For multi-site operators, cloud deployment and API connectivity have become core selection criteria.

In day-to-day practice operations, workflow integrations and inventory connectivity increasingly function as control points. Marketplace and ordering layers such as Vetcove reduce manual reordering and pricing friction across fragmented distributor networks, building a data-rich loop between demand signals and clinic purchasing. Rollouts remain bottlenecked by data conversion, training, and cybersecurity controls, while volatility in veterinary inputs increases the value of automated inventory tools and analytics. Policy-driven resilience efforts also feed into system requirements, including the UK Veterinary Medicines Directorate (VMD) September 2025 Statement of Intent encouraging a shift toward more resilient vaccine supply models, which supports demand for stronger traceability, inventory visibility, and compliance reporting inside clinic software stacks.

Competitive Landscape

The veterinary software industry displays moderate concentration. IDEXX, Covetrus, Henry Schein, and Patterson command substantial revenue via bundled diagnostics, pharmaceuticals, and software. IDEXX alone recorded USD 312.6 million in software revenue in fiscal 2024, an 11.9% year-over-year climb. Private-equity groups intensify consolidation by buying both chains and vendors, creating closed ecosystems where software controls consumables, equipment, and diagnostic data.

Competitive vectors are shifting from module breadth to data ownership. IDEXX’s inVue Dx Analyzer, launched late 2024, couples point-of-care testing with AI triage and seamless cloud upload, cementing user dependence on its stack. Nordhealth and Covetrus fight back by integrating third-party hardware and offering open APIs to capture clinics wary of single-supplier lock-in. Telehealth disruptors FirstVet and TeleVet pursue a different angle—owning the first client touch and routing cases to partner clinics on favorable terms.

White space remains in livestock and mixed-practice segments where current suites lack herd analytics and regulatory traceability. Startups like CoVet raised expansion capital in 2025 to close that gap with farm-ready dashboards that sync with standard PIMS. Interoperability standards mandated by European regulators may accelerate cross-vendor data sharing, but for now, proprietary integrations remain a key source of competitive edge.

Veterinary Software Industry Leaders

Carestream Health

IDEXX Laboratories Inc.

Patterson Companies, Inc.

Animal Intelligence Software, Inc.

Covetrus Inc.

- *Disclaimer: Major Players sorted in no particular order

Veterinary Software Market Companies Covered in this Report

- 2i Nova

- Airvet

- Animal Intelligence Software

- Business Infusions

- Carestream Health

- Covetrus

- DaySmart Vet

- Digitail

- ezyVet

- FirmCloud

- FirstVet

- Henry Schein (NaVetor)

- Hippo Manager Software

- IDEXX

- Nordhealth (Provet Cloud)

- Patterson Companies

- Shepherd Veterinary Software

- TeleVet

- Timeless Veterinary Systems

- Vetport

- Vetspire Inc.

- Vetter Software

Market Opportunities and Future Outlook

One key opportunity is an AI-enabled clinical intelligence layer that sits above core PIMS and aggregates diagnostics, imaging, teleconsult narratives, and longitudinal outcomes into operational and clinical decision support. Evidence of technical feasibility is visible in 2026 academic work on fine-tuning large language models for automated clinical coding across SNOMED-CT diagnosis codes, along with large-scale veterinary EHR analytics (including studies using records from one million dogs) that support population-level phenotyping and automated classification. Product direction also aligns with this architecture: Marley Health launched a clinical intelligence platform in June 2026, developed with support from the Royal Veterinary College and the University of Oxford, pointing to continued formation around analytics-first care workflows rather than administrative automation alone.

A second whitespace area involves extending software depth beyond companion animals into livestock and mixed-practice environments, where traceability, sensor inputs, and remote service models are less standardized. In 2026, researchers demonstrated a prototype telemedicine and teletriage architecture for livestock using standardized IT services and a sensor network, outlining a pathway for vendors to connect on-farm data streams with clinical records and referral networks. In parallel, compliance-led data exchange, such as EU antimicrobial reporting under Regulation 2019/6 and VICH GL53 documentation standards, keeps interoperability and structured coding central to product roadmaps, creating openings for vendors that offer open APIs, hybrid deployments for low-connectivity regions, and privacy-by-design tooling for multi-jurisdiction operations.

Recent Industry Developments in Veterinary Software Market

- May 2026: IDEXX Laboratories expanded the Fecal Dx antigen testing platform to include taeniid tapeworm detection, with automated inclusion for IDEXX Reference Laboratories customers in the United States and Canada. Broadening the test menu inside an existing platform reinforces IDEXXs integrated diagnostics plus software workflow and deepens data flow into practice systems without requiring clinics to change hardware or vendors.

- January 2026: Patterson Veterinary relaunched its NaVetor cloud-based veterinary practice management software after acquiring full rights to the platform. Full ownership supports tighter roadmap control and bundling across Pattersons distribution footprint, strengthening its position in enterprise and multi-site clinic deployments that prioritize standardized cloud operations.

- September 2024: Patterson Veterinary added pute.us, a veterinary-specific managed IT services provider, to its product portfolio. The move expands Pattersons role beyond software licensing into implementation and security operations, addressing a persistent barrier for practices that lack internal IT capacity and need ongoing support for cloud and hybrid environments.

Veterinary Software Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers paid software used by veterinary providers to manage clinical workflows and day-to-day operations, including patient records, scheduling, billing, imaging-related workflows, and telehealth modules, whether delivered as cloud, on-premise, or hybrid deployments.

Scope exclusions: Excludes hardware devices, general IT services, and revenue from veterinary care delivery that is not directly tied to software subscriptions, licenses, or support.

Segments Covered in This Report

- By Product

- Practice Management Software

- Veterinary Imaging Software

- Tele-Health Platforms

- Other Products

- By Delivery Model

- On-Premise

- Cloud-Based

- Hybrid

- By Animal Type

- Companion Animals

- Farm/Livestock Animals

- Equine

- Mixed Practices

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand map and to set realistic outer limits for the model before interviews refined the numbers. We leaned on public sources such as the American Veterinary Medical Association (AVMA) for clinic and veterinarian counts, the US Bureau of Labor Statistics for employment trends, and the US Census Bureau for business patterns that help approximate addressable sites.

To make the assumptions more practical, we also reviewed regulatory and standards context and adoption signals from sources such as the US Food and Drug Administration (FDA) for adjacent veterinary digital health context, peer-reviewed veterinary informatics literature, and trade association publications that discuss digitization in animal health. Company filings, investor presentations, and reputable press were used to understand pricing models (subscription versus perpetual) and feature bundling. In a few places, we supplemented this with paid database access for company financials and intelligence and patent databases to confirm product focus shifts. These examples are illustrative, and many other public and commercial sources were also referenced for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what clinics and hospitals actually buy, how pricing scales with seats, locations, and modules, and then aligning that with supplier side views on renewal and upsell behavior. We spoke with a spread of software providers, channel partners, and veterinary practice stakeholders across APAC, EMEA, and the Americas, so gaps from desk research could be closed and the final assumptions could be stress tested.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 51% |

| Mid tier: 46% | Functional/Unit leaders: 34% | EMEA: 31% |

| Smaller Players: 15% | Managers: 51% | Americas: 18% |

Market-Sizing & Forecasting

Sizing started with a top-down build where the demand pool was reconstructed from the number of veterinary practice sites and the share of sites using paid digital systems, and then converted into revenue using typical subscription price bands. To keep it grounded, the totals were then checked using selective bottom-up approximations such as supplier revenue roll-ups for a sampled set of visible players, channel feedback on average contract values, and a simple ASP times estimated user seat volume check.

Inputs that mattered most were the count of companion animal and mixed animal practices, the pace of cloud migration, typical module attachment rates (for example, practice management plus imaging workflow or telehealth), average seats per site, and renewal versus new logo mix. Since clinic throughput influences software utilization, signals like appointment volume trends and staffing levels were also used as directional indicators. Where bottom-up visibility was weak for smaller vendors, we filled gaps by applying conservative pricing bands and adoption shares validated through interviews, and we only scaled when the indicators moved together.

Forecasts used scenario analysis supported by expert views on price progression, feature bundling, and adoption speed, followed by a light regression check against clinic counts and digitization indicators to avoid unrealistic jumps. Growth rates were kept consistent with observable drivers like subscription penetration, telehealth normalization, and regional practice expansion, and then reviewed for plausibility at the regional roll-up level.

Data Validation & Update Cycle

Validation was done through multiple checks so the value stays traceable to clear inputs. We compared the modeled outcome against independent signals such as clinic counts, software penetration ranges discussed in interviews, and observed subscription pricing norms, and then reviewed any large variances before sign-off.

If a variance could not be explained by a known factor like a module mix shift or a regional weighting change, respondents were re-contacted and the assumption was adjusted with notes kept in the model. The report is refreshed annually, and interim updates are triggered when there are material events such as major product bundling changes, meaningful pricing resets, or policy shifts affecting telehealth use. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Veterinary Software Market Market Size Versus Other Published Estimates

Published values for veterinary software can look far apart, even when the topic sounds identical, because the counted revenue streams and year anchors do not always match. Differences also come from how firms treat cloud subscriptions versus perpetual licenses, whether telehealth modules are bundled into the total, and how currency timing is handled for non-US revenue.

Hardware-enabled imaging systems sit outside Mordor Intelligence's scope here, which reduces totals versus estimates that blend software with device and installation revenue, and the spread also widens when aggressive adoption curves or steep ASP escalation are used without matching clinic count and seat-based checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.96 B (2026) | |

| Global Research Publisher A | USD 1.43 B (2024) | Uses an earlier base year and often reports a narrower monetization view centered on core practice management revenue, which can undercount imaging workflow and telehealth modules when sold as add-ons. |

| Online Research Publisher B | USD 1.38 B (2024) | Applies broad category definitions and long-range CAGR assumptions, and the method description is usually less specific on adoption rates by clinic type and how pricing bands are converted across regions. |

The table shows that timing and scope are doing most of the work behind the gap, not just math. When the year is aligned and the included software modules are made explicit, the market total becomes easier to reconcile against clinic site counts, seats, and subscription price bands, which makes the output more repeatable for planning.

Key Questions Answered in the Report

What is the current size and projected value of global veterinary software sales?

Revenue stands at USD 1.96 billion in 2026 and is forecast to reach USD 2.64 billion by 2031, reflecting a 6.14% CAGR.

Which application area is growing the fastest?

Telehealth platforms are on an 8.54% CAGR trajectory through 2031 as clinics add virtual consults and insurers expand reimbursement.

How quickly are clinics shifting from on-premise to cloud deployments?

Cloud solutions are rising at an 8.01% CAGR, yet on-premise still accounts for 58.43% of installed systems in 2025, showing steady but gradual migration.

What role does clinic consolidation play in software purchases?

Private-equity backed chains demand enterprise-grade platforms to unify reporting across hundreds of sites, accelerating large-scale contracts and open-API requirements.

Which animal segments drive the bulk of spending?

Companion-animal practices hold 55.67% of 2025 revenue, while equine-focused software shows the fastest uplift at an 8.78% CAGR thanks to racing and breeding analytics.

What are the biggest obstacles to wider adoption?

Upfront implementation costs that can exceed USD 50,000 and rising cybersecurity threats remain the chief hurdles for independent practices.

Page last updated on: