Veterinary CRO And CDMO Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

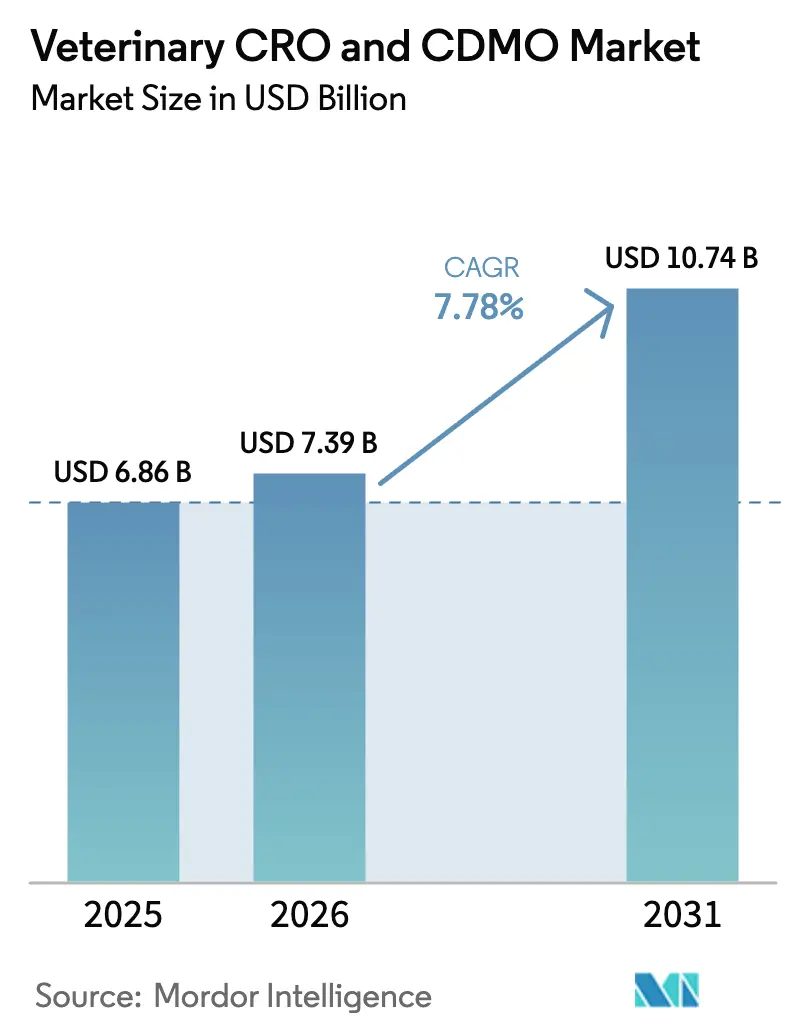

| Market Size (2026) | USD 7.39 Billion |

| Market Size (2031) | USD 10.74 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

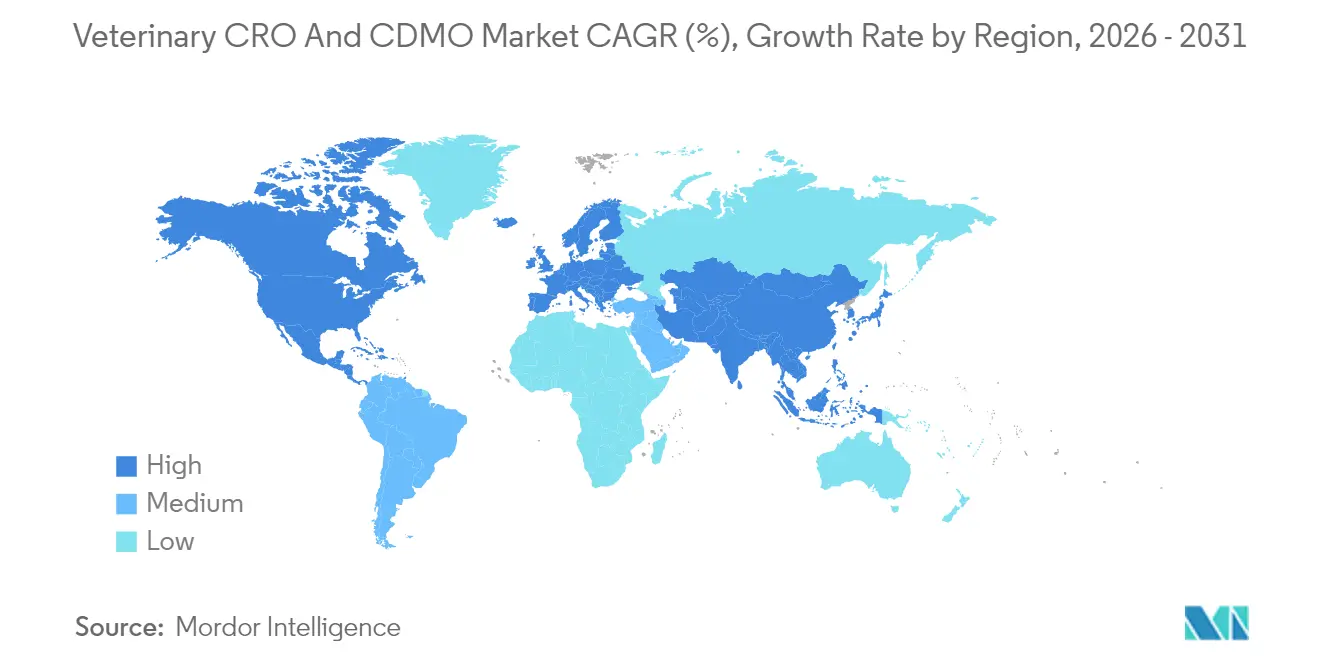

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

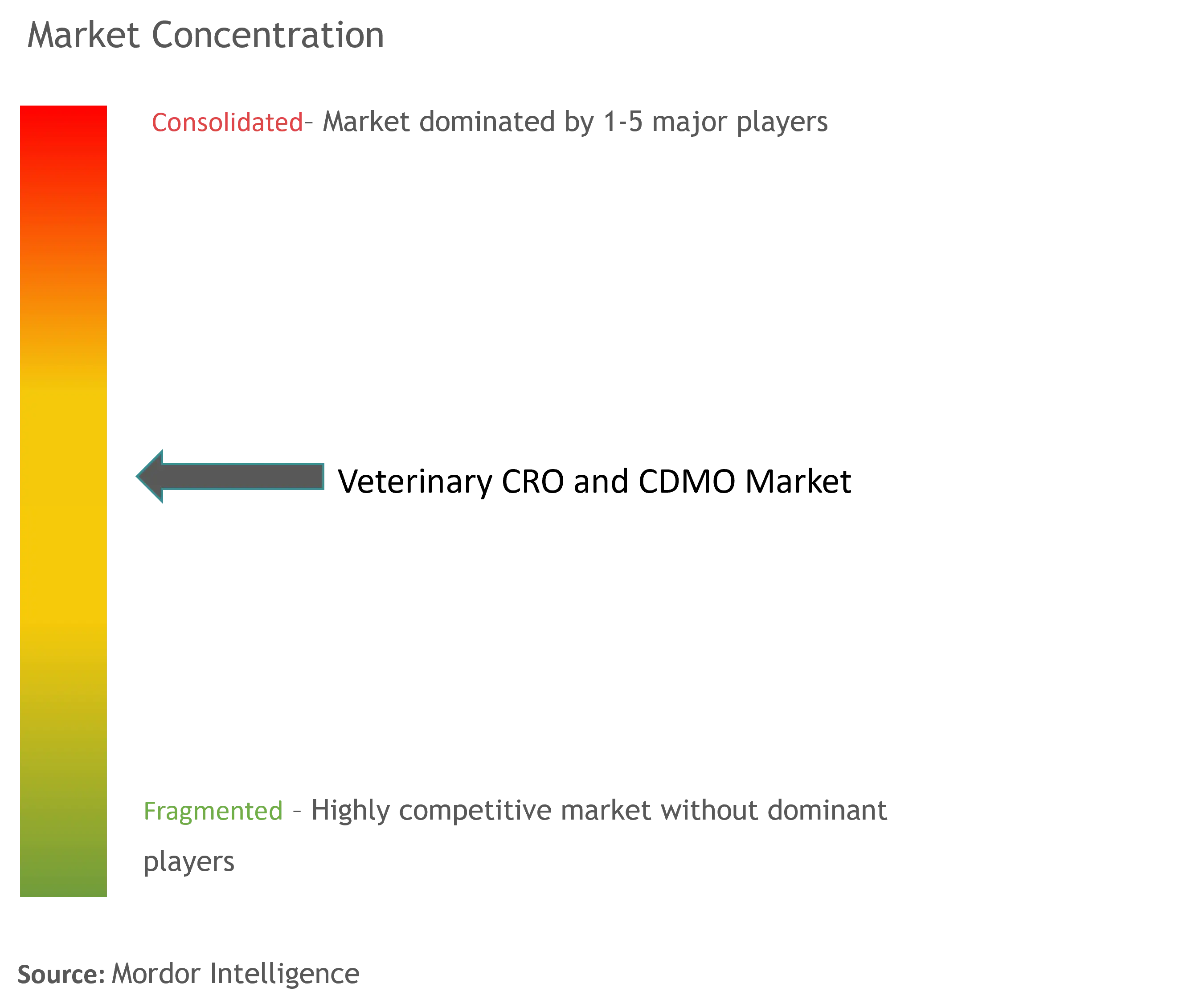

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary CRO And CDMO Market Analysis by Mordor Intelligence

The veterinary CRO and CDMO market size was valued at USD 6.86 billion in 2025 and estimated to grow from USD 7.39 billion in 2026 to reach USD 10.74 billion by 2031, at a CAGR of 7.78% during the forecast period (2026-2031). Rising outsourcing of complex biologics, persistent shortages of qualified GLP/GMP talent, and the widening adoption of asset-light strategies by animal health companies underpin this expansion. The market benefits from the mainstreaming of monoclonal antibodies, viral-vector vaccines, and gene therapies that require high-containment suites and advanced analytics that many sponsors prefer to subcontract. Capacity additions such as Merck Animal Health’s USD 895 million Kansas upgrade and Zoetis’ four-fold monoclonal antibody scale-up in Melbourne signal robust demand for external expertise. Meanwhile, specialized providers leverage integrated service platforms to shorten development timelines and facilitate global submissions, bolstering the overall attractiveness of the veterinary CRO and CDMO market.

Key Report Takeaways

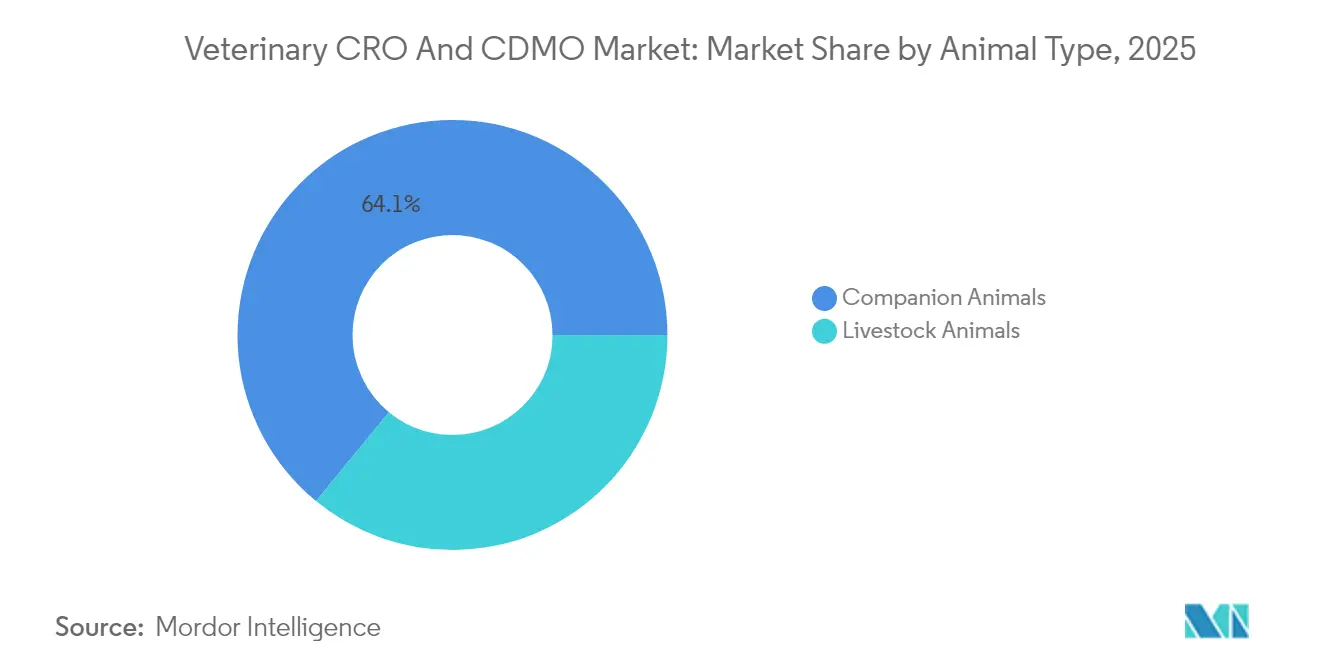

- By animal type, companion animals led with 64.05% revenue share in 2025, while livestock is forecast to expand at a 10.35% CAGR through 2031.

- By service type, development services held 40.85% of veterinary CRO and CDMO market share in 2025; manufacturing services are advancing at an 11.25% CAGR to 2031.

- By application, medicines accounted for 71.15% of the veterinary CRO and CDMO market size in 2025, whereas medical devices are set to grow at a 11.99% CAGR through 2031.

- By geography, North America captured 42.55% share in 2025, while Asia Pacific is poised for the fastest 9.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary CRO And CDMO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wide Adoption Of Veterinary Outsourcing Services | +1.80% | Global, with North America leading adoption | Medium term (2-4 years) |

| Growing Demand For Animal Health Products | +1.60% | Global, strongest in Asia Pacific emerging markets | Long term (≥ 4 years) |

| Rising R&D Spend Among Animal-Health Innovators | +1.20% | North America & Europe core markets | Medium term (2-4 years) |

| Mainstreaming Of Complex Biologics & Gene-Therapies For Animals | +0.90% | North America & Europe, expanding to Asia Pacific | Long term (≥ 4 years) |

| Acute Talent Shortage In GLP/GMP Animal Facilities | +0.70% | Global, most acute in North America | Short term (≤ 2 years) |

| Toxicology Model Shortages Driving Premium Pricing | +0.60% | Global, concentrated in specialized testing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Wide Adoption of Veterinary Outsourcing Services

Animal health companies are pivoting toward asset-light models, favoring specialized partners that deliver faster, more capital-efficient paths to market. Post-pandemic supply-chain disruptions reinforced the value of geographically diversified networks, prompting strategic moves such as Elanco’s USD 25 million purchase of the Speke biologics site to secure dedicated output while retaining flexibility. Outsourcing also de-risks entry into emerging markets because CRO/CDMOs contribute localized regulatory insight. Sponsors increasingly rely on end-to-end providers to manage complex technology transfers, enabling parallel development and manufacturing that compress launch timelines.

Growing Demand for Animal Health Products

Elevated pet adoption, expanding middle-class spending, and the One Health agenda drive steady consumption of premium veterinary therapeutics. Zoetis recorded 9% organic operational growth in Q1 2025 on strong uptake across companion and livestock portfolios. Protein producers simultaneously seek alternatives to antibiotic growth promoters, fueling investment in next-generation vaccines and microbiome-based solutions. Harmonized VICH guidelines reduce duplicative studies, further incentivizing product pipelines that enlarge the veterinary CRO and CDMO market.

Rising R&D Spend Among Animal-Health Innovators

Major sponsors now mirror human-pharma behaviors, channeling capital into platform technologies covering multiple species. Elanco allocated USD 344 million to R&D in 2024, signaling confidence in biologics and digital therapeutics. Partnerships such as Absci-Invetx apply generative AI to optimize antibody libraries, illustrating how computational biology reshapes discovery workflows. The sophistication of these projects heightens reliance on CROs with deep veterinary pharmacology expertise, strengthening demand for integrated study design, bioanalytics, and regulatory support.

Mainstreaming of Complex Biologics & Gene Therapies for Animals

Regulators approved 14 veterinary medicines in 2023, nine of which were biotechnology products, highlighting the growing acceptance of advanced modalities.[1]European Medicines Agency, “EMA Recommends 14 Veterinary Medicines for Authorization in 2023,” ema.europa.eu Successes like Librela and Solensia confirm that owners will pay premium prices for monthly monoclonal antibodies that address osteoarthritis pain. Manufacturing this class of products requires viral-vector suites and species-specific immunogenicity testing, seldom available in-house. Established CDMOs, therefore, enjoy significant entry barriers and pricing power, reinforcing growth in the veterinary CRO and CDMO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack Of Industry-Wide Quality Standards | -0.80% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Stringent Multi-Jurisdictional Regulatory Hurdles | -0.90% | Global, particularly complex for North America-Europe-Asia Pacific approvals | Long term (≥ 4 years) |

| Scarcity Of High-Containment (BSL-3/4) CRO Capacity | -0.70% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Rapid Cost Escalation For Viral-Vector Manufacturing Suites | -0.60% | Global, most acute in established manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Industry-Wide Quality Standards

Unlike human ICH frameworks, veterinary operations contend with fragmented guidelines that complicate batch release, tech transfer, and documentation. Biologics magnify the challenge because analytical methods vary across regions, prompting companies to invest heavily in duplicate validation runs. While the VICH program is narrowing gaps, adoption remains uneven, raising compliance risk and diluting some cost advantages that outsourcing is meant to deliver.

Stringent Multi-Jurisdictional Regulatory Hurdles

Animal health sponsors pursuing simultaneous approvals in the United States, Europe, and Asia must navigate diverging dossier formats and labeling rules. Recent FDA updates to animal drug labeling and evolving EMA expectations for novel vectors underscore a dynamic environment.[2]U.S. Food and Drug Administration, “FDA Updates Animal Drug Labeling Requirements,” fda.gov Smaller providers often lack in-house regulatory breadth, lengthening review cycles and inflating budgets. Larger CDMOs convert this complexity into a competitive edge by offering integrated, region-specific submission support, yet overall industry growth loses momentum to prolonged approval timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Companion Animals Drive Premium Growth

Companion animals accounted for 64.05% of 2025 revenue, establishing them as the largest slice of the veterinary CRO and CDMO market. Premium pricing tolerance stems from owners who treat pets as family members and willingly adopt high-value biologics. Zoetis’ monoclonal antibody duo illustrates this willingness to pay, sustaining robust demand for contract biologics capacity. Livestock projects trail in absolute size but advance at a 10.35% CAGR, buoyed by global protein demand and antibiotic-reduction mandates that favor novel vaccines. Aquaculture’s expanding share—reinforced by Merck Animal Health’s acquisition of Elanco’s fish health unit—adds fresh momentum to outsourcing needs in cold-chain vaccine fill-finish.

Livestock sponsors increasingly pursue precision agriculture tools, such as sensor-enabled monitoring and microbiome interventions, which require combined pharmacological and device expertise. CRO/CDMOs able to integrate formulation, toxicology, and digital hardware validation gain first-mover advantages. Although companion animals retain the lion’s share, accelerating livestock innovation diversifies revenue streams and anchors the veterinary CRO and CDMO market against consumer-spending volatility.

By Service Type: Manufacturing Services Accelerate

Development work delivered 40.85% of 2025 revenue, confirming its central role within the veterinary CRO and CDMO market. However, manufacturing is growing fastest at 11.25% CAGR as more late-stage assets enter commercial production. Sponsors elect to source fill-finish, lyophilization, and large-scale cell-culture runs from partners rather than expanding capital-intensive plants. This shift is magnified by the specialized containment needs of viral vectors and the regulatory overhead that accompanies GMP biologics. Integrated providers that combine development history with vertically aligned manufacturing streamline validation and release testing, offering a powerful value proposition.

Discovery services, while still the smallest contributor, are enjoying renewed focus because AI-driven target identification compresses early-stage timelines. Partners are proficient in computational biology, high-throughput screening, and in-silico toxicology differentiate their bids. Packaging and labeling tasks grow steadily too, driven by cold-chain biologics that demand specialized presentation to maintain stability. Collectively, these trends reinforce the progression from stand-alone task outsourcing to holistic, lifecycle-oriented partnerships that expand the addressable veterinary CRO and CDMO market.

By Application: Medical Devices Gain Momentum

Medicines retained 71.15% revenue share in 2025, dominating contractual workflows. Still, medical devices are projected to record a 11.99% CAGR as AI diagnostics, wearables, and smart injectors invade veterinary clinics. Zoetis’ AI Masses cytology module exemplifies how in-clinic analytics shorten diagnostic cycles and create incremental service opportunities. Device sponsors leverage CRO/CDMOs for design verification, biocompatibility testing, and software validation, complementing traditional pharmacological services.

Accelerated device evolution draws on shorter development loops and generally lighter regulatory burdens compared with pharmaceuticals. Hybrid “drug-device” products that pair long-acting injectables with smart applicators require integrated chemistry, engineering, and regulatory know-how. Providers capable of bridging these disciplines attract a widening slate of projects and further expand the veterinary CRO and CDMO market.

Geography Analysis

North America maintained leadership with 42.55% of global revenue in 2025. The region hosts the headquarters of major sponsors, deep venture capital pools, and a mature reimbursement environment that supports premium treatments. Predictable FDA pathways expedite commercialization, while sizeable expansions such as Zoetis’ Louisville diagnostics hub underscore confidence in long-term demand. Furthermore, a dense network of academic institutions supplies basic research that feeds the contract services pipeline.

Asia Pacific is forecast to grow at 9.35% CAGR through 2031, making it the fastest-advancing territory in the veterinary CRO and CDMO market. Rising disposable incomes, urban pet adoption, and government mandates on livestock disease control lift baseline consumption. China and India invest heavily in domestic biologics capacity yet still rely on external expertise for advanced analytics and regulatory guidance. Strategic moves by international sponsors, such as Virbac’s acquisitions in India and Japan, signal mounting interest in localized production that still leans on transnational technology transfers.

Europe offers a stable, innovation-friendly arena thanks to EMA’s supportive stance on veterinary biologics. The agency backed 14 new veterinary medicines in 2023, nine of which were biotech products. High animal welfare standards sustain demand for premium therapies and bolster uptake of evidence-based nutritional supplements. Although growth lags Asia Pacific, Europe’s sophisticated GMP ecosystem and cross-border logistics keep it integral to multinational launch strategies. Emerging regions such as South America and the Middle East & Africa contribute incremental growth by modernizing livestock value chains, though regulatory and economic volatility temper near-term expansion.

Competitive Landscape

The veterinary CRO and CDMO market remains moderately fragmented, yet consolidation is accelerating. Argenta Group positions itself as the only animal-health-exclusive, end-to-end provider, while diversified pharmaceutical CDMOs like Lonza and Vetter establish dedicated veterinary divisions. Technology adoption has become a primary differentiator. Absci’s partnership with Invetx brings generative AI into antibody design, potentially slashing discovery timelines and cost structures. Likewise, Merck Animal Health’s Kansas buildout installs next-generation single-use bioreactors that raise flexibility for small-batch viral vectors.

Competitive emphasis is shifting from pure capacity to integrated regulatory, digital, and analytical services. Companies that couple device engineering with biologics fill-finish now win mandates for combination products. White-space opportunities include aquaculture, exotic species therapeutics, and precision livestock diagnostics—areas where regulatory pathways are forming and experienced CDMOs are scarce. Strategic acquisitions, such as Lonza’s USD 1.2 billion purchase of Genentech’s Vacaville plant, aim to secure scale while adding high-containment suites ready for veterinary projects.

Talent scarcity shapes market power dynamics. Providers able to recruit and retain cross-trained veterinary pathologists, GMP bioprocess engineers, and digital validation specialists command premium pricing. Firms embed academic partnerships to fortify pipelines of qualified graduates and deploy global mobility programs to staff emerging-market facilities. Collectively, these factors foster a competitive environment where scale, specialization, and technology convergence dictate share gains within the veterinary CRO and CDMO market.

Veterinary CRO And CDMO Industry Leaders

OCR – Oncovet Clinical Research

Argenta Group (KLIFOVET GmbH)

Clinvet

VETSPIN

Knoell

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Elanco partnered with Medgene to commercialize a highly pathogenic avian influenza vaccine for dairy cattle.

- January 2025: rán BioScience secured a USD 200 million+ investment to construct a commercial-scale manufacturing site in Bend, Oregon.

- February 2025: Merck Animal Health closed its acquisition of Elanco’s aqua business, expanding its fish-health vaccine portfolio

Global Veterinary CRO And CDMO Market Report Scope

As per the report's scope, CRO and CDMO are specialized service providers in veterinary pharmaceutical and biotechnology research. These organizations work with pharmaceutical and biotechnology companies, offering expertise in formulation development, analytical testing, manufacturing process optimization, and large-scale production of veterinary drugs.

By animal type, the market is segmented into companion animals and livestock animals. By service, the market is segmented by discovery, development, manufacturing, packaging and labeling, and market approval and post-marketing. By market approval and post-marketing, the market is segmented by early phase/preclinical and late phase/clinical. By application, the market is segmented into medicines and medical devices. By geography, the market is segmented by North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Companion Animals |

| Livestock Animals |

| Discovery |

| Development |

| Manufacturing |

| Packaging & Labelling |

| Market Approval & Post-marketing |

| Medicines |

| Medical Devices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Animal Type | Companion Animals | |

| Livestock Animals | ||

| By Services | Discovery | |

| Development | ||

| Manufacturing | ||

| Packaging & Labelling | ||

| Market Approval & Post-marketing | ||

| By Application | Medicines | |

| Medical Devices | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the veterinary CRO and CDMO market?

The veterinary CRO and CDMO market size reached USD 7.39 billion in 2026 and is on track to hit USD 10.74 billion by 2031 at a 7.78% CAGR during 2026-2031.

Which region holds the largest share of the veterinary CRO and CDMO market?

North America leads with 42.55% of global revenue thanks to mature regulatory pathways and significant sponsor presence.

Which segment is growing fastest within the veterinary CRO and CDMO market?

Manufacturing services are expanding at an 11.25% CAGR as complex biologics move from development into commercial production.

Why are companion animals important to CRO/CDMO demand?

Companion animals account for 64.05% of 2025 revenue because owners accept premium prices for advanced therapeutics, boosting demand for outsourced development and manufacturing.

What technological trends are reshaping the veterinary CRO and CDMO industry?

AI-enabled drug design, advanced monoclonal antibody platforms, and digital diagnostics are accelerating discovery and broadening service scopes, compelling providers to integrate biology, engineering, and software expertise.

Page last updated on: