Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

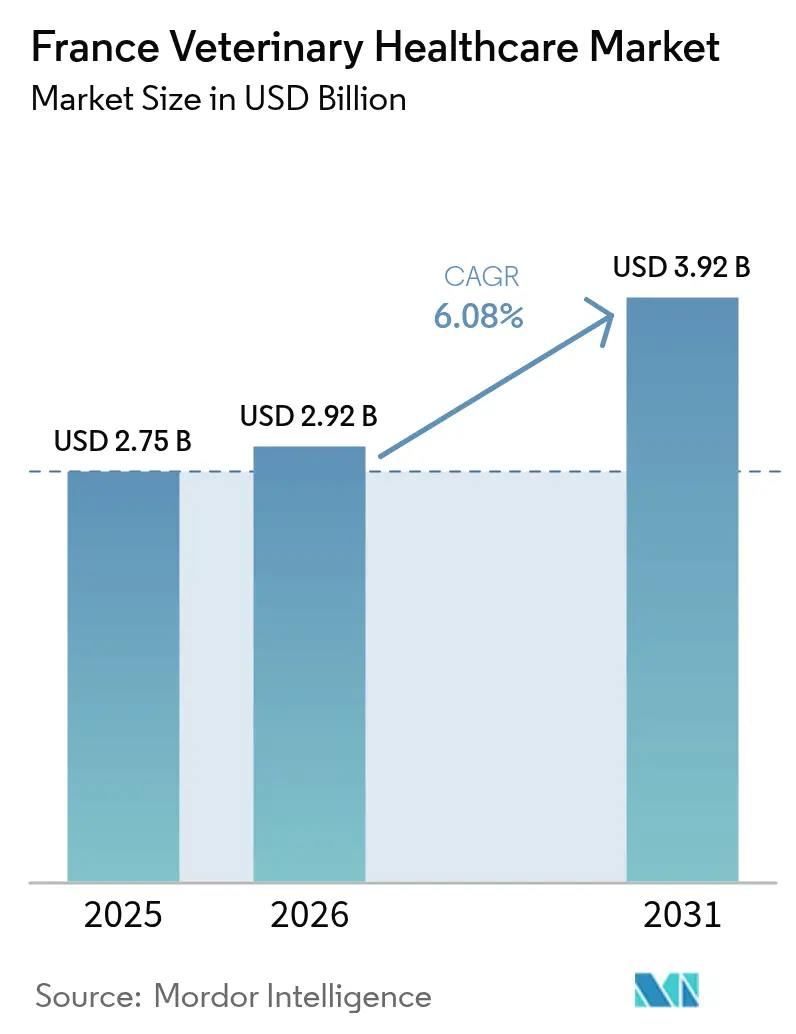

| Base Year Market Size (2025) | USD 2.75 Billion |

| Market Size (2026) | USD 2.92 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Veterinary Healthcare Market Analysis by Mordor Intelligence

The France veterinary healthcare market size was valued at USD 2.75 billion in 2025 and estimated to grow from USD 2.92 billion in 2026 to reach USD 3.92 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031). The market benefits from rising pet ownership, proactive livestock disease control, and rapid technology uptake across diagnostics and therapeutics. Growth concentrates in urban areas where companion animal spending climbs, while poultry health investments accelerate in rural regions. Digital tools such as AI-powered point-of-care analyzers shorten diagnosis times, and insurance uptake encourages owners to authorize advanced treatments. At the same time, veterinarian shortages outside major cities constrain service availability, prompting policy makers to subsidize rural practice and telemedicine expansion.

Key Report Takeaways

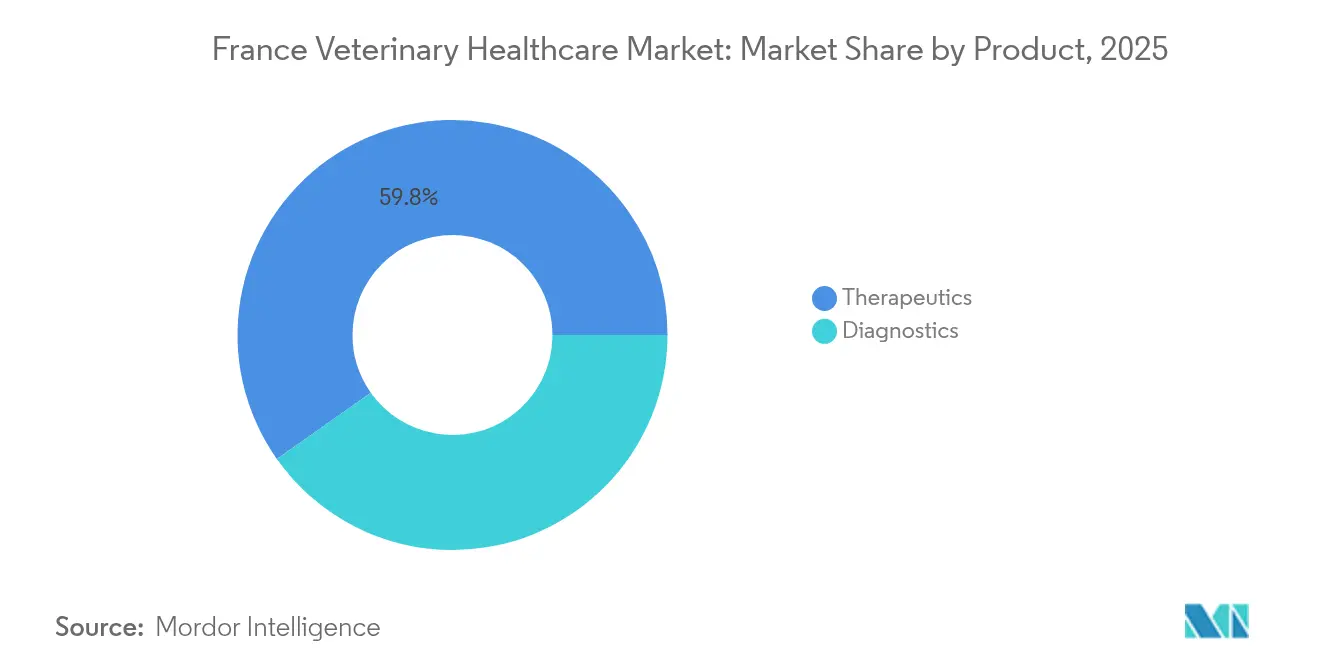

- By product type, therapeutics led with 59.78% of the France veterinary healthcare market share in 2025. Diagnostics is advancing at a 7.32% CAGR through 2031.

- By animal type, companion animals held 45.05% of the France veterinary healthcare market size in 2025. Poultry is registering the fastest 6.55% CAGR to 2031.

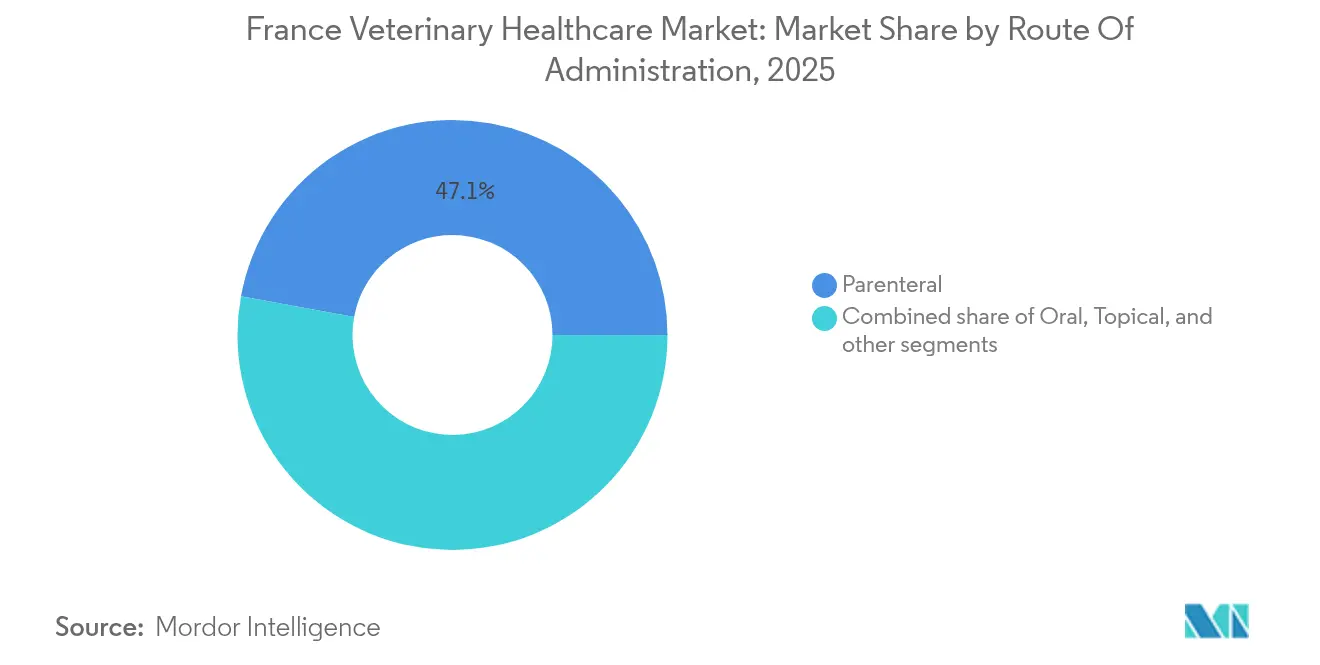

- By route of administration, parenteral products commanded 47.12% share of the France veterinary healthcare market size in 2025. Oral products are projected to expand at a 6.34% CAGR through 2031.

- By end user, veterinary hospitals and clinics retained 55.84% revenue share in 2025, whereas point-of-care settings are growing at 7.11% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Veterinary Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in veterinary diagnostics and therapeutics | +1.8% | National focus with global inputs | Medium term (2–4 years) |

| Rising pet insurance coverage and companion animal expenditure | +1.5% | Urban France | Short term (≤ 2 years) |

| Government-led livestock disease control programs | +1.2% | Rural France | Long term (≥ 4 years) |

| Expansion of e-commerce distribution channels for veterinary products | +0.9% | Urban France | Short term (≤ 2 years) |

| Corporate consolidation of veterinary clinic networks | +0.7% | National | Medium term (2–4 years) |

| Digital health and remote care adoption in veterinary services | +0.6% | Rural gaps | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Veterinary Diagnostics and Therapeutics

AI tools permeate French clinics, with 69.5% of professionals using machine-learning systems for cytology and imaging. Zoetis expanded its Vetscan Imagyst platform in 2025, enabling automated lymph-node and skin-mass review, which lifts diagnostic accuracy and cuts result turnaround to minutes. Virbac’s “Day 1” mobile application allows farmers to score colostrum quality on-site, supporting neonatal immunity tracking. Large reference laboratories enhance these digital gains; Mars Petcare completed the acquisition of Cerba Vet and ANTAGENE in January 2025, adding six labs and a genetics hub to its French network. Collectively, these tools shorten treatment initiation, reduce follow-up visits, and ease the workload on an overstretched veterinarian labor force.

Rising Pet Insurance Coverage and Companion Animal Expenditure

Pet insurance penetration climbed across metropolitan France after 2024 tariff liberalization. SantéVet, Lassie, and Pety each offer plans with annual limits up to EUR 5,000 (USD 5,400), cutting out-of-pocket bills for surgeries and imaging. The share of insured dogs rose from 25% in 2024 to 32% in 2025, while cats posted a 4-percentage-point jump. Higher coverage propelled service uptake: MRI utilization grew 12% year over year, and preventive dental cleanings rose 9%. Spending aligns with a wider consumer shift toward premium veterinary nutrition, grooming, and wellness visits that keeps the France veterinary healthcare market on its growth path.

Government-Led Livestock Disease Control Programs

Public programs remain a cornerstone for herd health. The 2023–2025 avian influenza vaccination drive protected 26 million ducks, trimming outbreaks from 315 cases to just 10 by early 2025[1]Ministère de l’Agriculture et de la Souveraineté Alimentaire, “Bilan Campagne Vaccination Influenza Aviaire 2025,” agriculture.gouv.fr. The Ministry of Agriculture covered 85% of vaccine costs, easing producer adoption and creating demand for cold-chain logistics and biologics. A new 2024–2029 roadmap targets bovine tuberculosis by widening compulsory testing and funding herd depopulation compensation. Continuous surveillance through the National Animal Health Surveillance Platform blends One-Health data to flag emerging threats swiftly.

Expansion Of E-Commerce Distribution Channels for Veterinary Products

French pet owners shifted further online after pandemic-era lockdowns. Zooplus and Amazon.fr now list prescription diets and parasite preventives that ship overnight, though antimicrobials stay under strict prescription control. Centravet and other wholesalers have introduced click-and-collect portals for clinics, posting 18% e-commerce revenue growth in 2024. Suppliers who optimize omnichannel logistics are capturing price-sensitive consumers, especially millennials who favor home delivery. Yet regulatory audits ensure that product authenticity and pharmacist oversight remain intact.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cost of veterinary services and pharmaceuticals | -1.4% | Nation-wide | Short term (≤ 2 years) |

| Limited veterinary infrastructure in rural areas | -1.1% | Livestock production zones | Long term (≥ 4 years) |

| Prevalence of counterfeit and substandard medications | -0.9% | Select online and informal channels | Medium term (2–4 years) |

| Declining companion animal population growth | -0.7% | Mature urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cost of Veterinary Services and Pharmaceuticals

Base consultation fees at primary-care clinics rose from EUR 26.50 to EUR 30 (USD 32.60) in January 2025[2]Ministère du Travail, de la Santé et des Solidarités, “Revalorisation des Honoraires de Consultation 2025,” sante.gouv.fr. Simultaneously, new prescription regulations moved opioids and codeine to secure pads, raising compliance overhead for practices[3]ANSM, “Renforcement de la Sécurisation des Ordonnances 2025,” ansm.sante.fr. Consolidation contributes to tariff creep: after Mars Petcare’s expansion, U.S. lawmakers cited up-charging concerns, mirroring anecdotal price increases in French urban hospitals. Livestock producers on thin margins often postpone treatments, eroding routine disease-prevention benefits.

Limited Veterinary Infrastructure in Rural Areas

Survey data show 78.5% of rural districts report open vacancies for food-animal veterinarians. Younger graduates lean toward small-animal practice in cities where incomes are higher and emergency rosters lighter. The average rural veterinarian age now exceeds 54 years. Workforce gaps result in longer travel distances, delayed emergency response, and heavier dependence on government field services. Grants covering student debt and mobile-clinic subsidies are being piloted but will take several years to rebalance supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutics Dominance Drives Market Foundation

Therapeutics generated 59.78% of 2025 revenue, anchoring the France veterinary healthcare market. Parasiticides and vaccines sold briskly as poultry and swine producers responded to stringent biosecurity rules, and companion-animal owners demanded broad-spectrum flea and tick solutions. Virbac’s launches, including a neonatal piglet diarrhea vaccine, highlight the pace of biologic innovation. Anti-infectives face stricter antimicrobial resistance rules, yet targeted molecules still see demand during outbreaks, sustaining double-digit product turnover.

Diagnostics, while smaller, is the fastest-growing line at 7.32% CAGR. Mars Petcare’s Cerba Vet acquisition multiplied laboratory throughput, and IDEXX bundled hematology and chemistry analyzers into subscription kits, lifting placement rates in independent clinics. AI algorithms embedded in handheld ultrasound and cytology readers reduce sample referrals and foster in-house revenues. The France veterinary healthcare market size for diagnostics is projected to top USD 1,650 million by 2031, reflecting this adoption wave.

By Animal Type: Companion Animals Lead While Livestock Shows Promise

Dogs and cats account for 45.05% of 2025 turnover, mirroring French urban demographics that support wellness plans, orthopedic surgery, and advanced imaging. Orthopedic supplement maker Vetoquinol broadened its Flexadin range in July 2025, underlining lucrative niche expansion.

Poultry, however, records the swiftest ascent with a 6.55% CAGR. Massive duck vaccination campaigns and export-oriented breeders require continuous immunization, diagnostics, and biosafety audits. The France veterinary healthcare market share for poultry health inputs is expected to pass 15.42% by 2031 as farmers invest in resilient production systems.

By Route Of Administration: Parenteral Leads with Oral Growth Accelerating

Parenteral formats, at 47.12% share, dominate high-potency vaccines and emergency therapeutics because they ensure rapid bioavailability. Ceva Santé Animale’s injectable avian influenza vaccine formed the backbone of France’s 2024 campaign.

Oral products are expanding fastest at 6.34% CAGR. Chewable NSAIDs, probiotic supplements, and prescription diets meet owner preference for ease of dosing. The France veterinary healthcare market size tied to oral formats is set to rise by USD 232.5 million between 2026 and 2031.

By End User: Hospitals Dominate While Point-of-Care Testing Accelerates

Hospitals and clinics contributed 55.84% of 2025 sales owing to their broad service menus and surgical capacity. Ownership rules that mandate licensed veterinarians as majority shareholders keep practice roll-ups moderate, preserving a diversified field of independents.

Point-of-care sites, including mobile clinics and on-farm labs, post the highest 7.11% CAGR. New analyzers such as Vetscan OptiCell provide a differential in under 3 minutes, trimming sample shipping costs and attracting time-pressed livestock producers.

Geography Analysis

France’s diverse topography creates uneven veterinary service access. Île-de-France, Auvergne-Rhône-Alpes, and Nouvelle-Aquitaine collectively house 42% of licensed veterinarians and generate over half of the France veterinary healthcare market. These urbanized hubs offer 24-hour hospitals, CT scanners, and referral specialties that capture complex surgical cases. The France veterinary healthcare market size in these three regions is forecast to approach USD 2.06 billion by 2031.

In contrast, Occitanie and Bourgogne-Franche-Comté contain dense livestock populations but fewer clinics per square kilometer. Government subsidies fund mobile bovine tuberculosis testing units and tele-consult portals to bridge gaps. Digital triage reduces travel miles for minor ailments, but emergencies still rely on on-call rosters that strain the limited workforce.

Border proximity to Spain, Germany, and Italy supports cross-border pharmaceutical distribution and referral collaborations. French firms like Virbac export 42% of their output, while foreign multinationals site research centers near Lyon’s advanced bio-cluster. Tight EU pharmacovigilance alignment through ANSES speeds authorization of new molecules, allowing local producers to innovate while meeting common quality benchmarks.

Regulatory Landscape

Veterinary medicinal products in France are regulated under EU Regulation 2019/6 and national rules in the French Public Health Code. ANSES, acting through the French Agency for Veterinary Medicinal Products (ANMV), is the competent authority for marketing authorizations (MAs), pharmacovigilance, and inspections. Companies typically enter the market via an ANMV MA or the European Commission centralized procedure, and dossiers are submitted electronically. Technical compliance checks are supported by tools such as the VNeeS Checker, used in cooperation with Belgian and French agencies.

On the animal health side, surveillance and control measures for transmissible diseases were reinforced through Décret 2025-987 (adopted October 22, 2025), with key provisions effective January 1, 2026. The change signals tighter expectations for prevention, reporting, and movement controls. France also updates disease-specific controls through orders published in the Journal officiel, including the February 5, 2026 Arrêté modifying surveillance, prevention, and control measures for contagious nodular dermatitis (lumpy skin disease) in metropolitan France, including movement restrictions for non-vaccinated animals in designated vaccination zones. ANMV can also grant one-year Temporary Use Authorizations when no authorized product is available in France.

Competitive Landscape

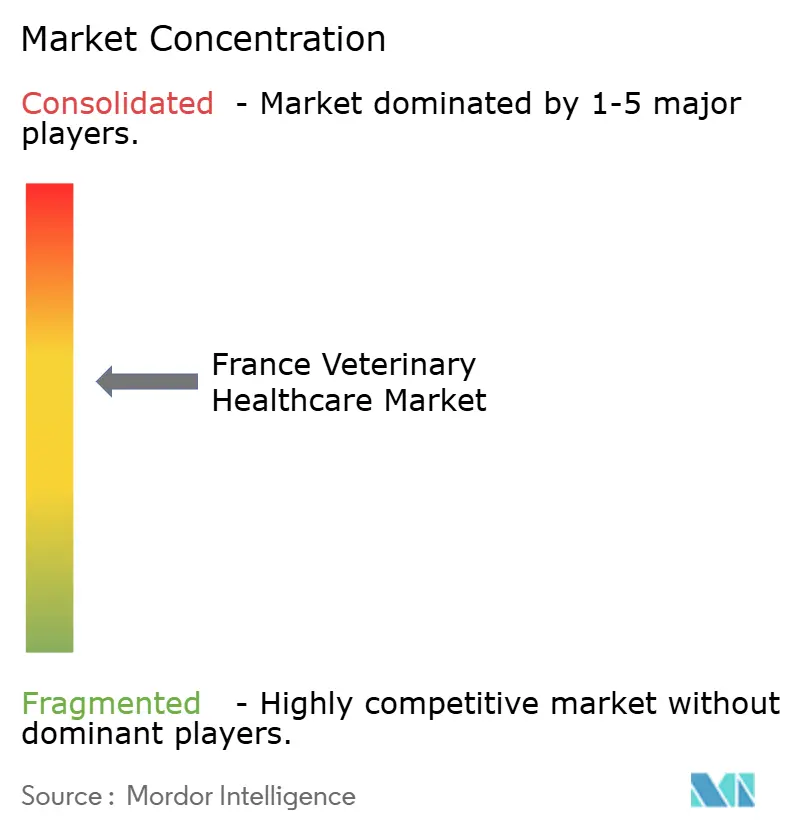

The market presents moderate concentration. The five largest suppliers hold roughly 55% combined revenue, implying a competitive landscape that encourages product differentiation and service upgrades. Zoetis registered 10% French revenue growth in Q4 2024 through portfolio breadth and bundled service contracts. Virbac climbed 13.6% in 2024 on the back of both acquisitions and core portfolio boosts. Ceva Santé Animale’s valuation topped USD 10 billion in March 2025 as it signaled a potential IPO.

Diagnostic capability is the new battleground. Mars Petcare’s January 2025 takeover of Cerba Vet granted it an expanded test menu, while IDEXX seeds clinics with rental analyzers linked to a consumables annuity model. Telehealth start-ups Digitail and Televet target independent practices that seek to keep triage in-house and lighten after-hours loads. Rural workforce gaps spur collaborations between corporate groups and veterinary schools to fund mixed-practice internships, preserving service continuity in remote communes.

France Veterinary Healthcare Industry Leaders

Ceva Animal Health, Inc

Zoetis Inc.

Boehringer Ingelheim International GmbH

Elanco Animal Health

Vetoquinol SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Diagnostics-led workflow digitization and clinic productivity tools are becoming a more visible area of whitespace as practices navigate staff constraints and rising case complexity. Adoption of online booking and practice-management platforms such as MonRendezVousVeto and CaptainVet, along with AI-driven reception and triage agents including VetoCall and Districall, points to front-office and care-coordination automation in hospitals, clinics, and point-of-care settings. At the same time, the teleconsultation framework remains in transition after earlier trial phases ended in 2021, which keeps focus on solutions that combine compliant remote triage, in-clinic diagnostics, and referral pathways. Suppliers and clinic networks can differentiate through offerings that translate into measurable time savings and faster treatment initiation.

Vaccine and biologics localization is another opportunity track tied to French and EU disease-prevention priorities. Boehringer Ingelheim confirmed a EUR 500 million investment plan for its French animal health operations through 2030 across sites in the Lyon area and Toulouse, while Ceva strengthened biologics capabilities through its June 2026 acquisition of Aquilon CyL S.L. (swine enteric vaccine). On the regulatory side, ANSES/ANMV oversight of establishment authorizations and marketing authorizations, paired with outbreak-control measures effective from January 1, 2026, supports demand for compliant manufacturing, cold-chain logistics, and pharmacovigilance-ready product launches across poultry, swine, and ruminant segments.

Recent Industry Developments

- July 2026: Zoetis received European Commission marketing authorization for its Poulvac Procerta HVT-ND poultry vaccine. The approval expands addressable EU-aligned demand for preventive vaccination protocols and supports broader adoption of combined poultry disease-prevention programs in France.

- June 2026: Boehringer Ingelheim confirmed a EUR 500 million investment plan through 2030 for its French animal health operations, including major spending at the Toulouse site and expanded oral/tablet production volumes. This commitment strengthens local supply capacity for vaccines and medicines and increases competitive pressure on manufacturing footprint and service levels in France.

- March 2026: Zoetis launched Equip WNV, a West Nile virus vaccine for horses, in France. The launch adds a prevention option for equine practitioners and enables the company to capture seasonal, outbreak-linked vaccination demand alongside its broader biologics portfolio.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the France veterinary healthcare market is defined as the value of veterinary therapeutics and diagnostic solutions used to prevent, detect, and treat animal diseases within France, across both companion and food-producing animals.

Scope exclusions: This sizing does not include general pet services such as grooming, boarding, and training, and it also excludes human healthcare products.

Segmentation Overview

- By Product

- Therapeutics

- Vaccines

- Parasiticides

- Anti-Infectives

- Medical Feed Additives

- Other Therapeutics

- Diagnostics

- Immunodiagnostic Tests

- Molecular Diagnostics

- Diagnostic Imaging

- Clinical Chemistry

- Other Diagnostics

- Therapeutics

- By Animal Type

- Dogs & Cats

- Horses

- Ruminants

- Swine

- Poultry

- Other Animal Types

- By Route Of Administration

- Oral

- Parenteral

- Topical

- Other Route of Administrations

- By End User

- Veterinary Hospitals & Clinics

- Reference Laboratories

- Point-Of-Care / In-House Testing Settings

- Academic & Research Institutes

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to build the baseline demand context for France, and then to anchor a few inputs that do not move quickly in the model, such as pet ownership trends and livestock populations. For this, we referred to public sources such as the French Ministry of Agriculture and Food Sovereignty statistics, Eurostat animal population datasets, the World Organisation for Animal Health disease and surveillance releases, and peer-reviewed veterinary journals that describe treatment practices and diagnostics adoption.

Next, we reviewed non-paywalled materials such as company annual reports, investor presentations, and reputable press coverage to understand how product mix shifted between therapeutics and diagnostics, and how spending moves across clinics and laboratories. In parallel, subscriptions that aggregate company financials, news, and patent activity were used to cross-check revenue direction and innovation focus without relying on a single disclosure. The sources listed here are illustrative only, and many other references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating what is purchased and used in France, and how spending shifts between therapeutics and diagnostics as disease patterns and clinic capabilities change. We spoke with veterinary clinics and hospitals, reference laboratories, distributors, and industry experts, and then used their input to confirm utilization rates, pricing movement, and how demand differs between companion animals and production animals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | |

| Mid tier: 47% | Functional/Unit leaders: 27% | |

| Smaller Players: 20% | Managers: 57% |

Market-Sizing & Forecasting

Our core build used a top-down approach where the animal population pool in France was translated into an addressable treated demand base, and then mapped to typical care pathways that drive therapeutics and diagnostics usage. Once the demand pool was shaped, it was converted to value using observed price bands and mix splits reported by respondents, and we then checked results with selective bottom-up approximations such as sampled clinic and lab revenue patterns, distributor channel checks, and volume times average selling price sanity tests.

A few practical inputs carried most weight in the model, including companion animal and livestock population trends, veterinary visit frequency, test utilization per visit for in-clinic and reference lab settings, treatment rates for common infectious and parasitic conditions, and price progression for key product classes as generics and premium products shift the mix. Where bottom-up signals were incomplete, gaps were handled through conservative penetration assumptions that were confirmed in interviews, and then stress-tested against observable clinic throughput and lab workload indicators.

For forecasting, we used scenario analysis so that adoption of advanced diagnostics, insurance penetration effects on clinic spend, and disease incidence swings could be expressed as a range before selecting a base case. Each forward assumption stayed simple and was kept only if it could be tied to a clear demand driver and supported by repeated expert feedback.

Data Validation & Update Cycle

Outputs were validated through several checks, where totals were compared against independent signals such as animal population direction, clinic capacity expansion, and diagnostics uptake patterns that appeared repeatedly in interviews. If any segment moved too far from these signals, the assumptions were revisited, and respondents were re-contacted when a variance could not be explained through mix or pricing.

Before sign-off, the full model goes through multi-step analyst reviews, including unit consistency checks, currency and year alignment, and cross-verification of growth rates against real-world drivers discussed by practitioners. Reports are refreshed annually, and interim updates are done when material events occur that could change demand, pricing, or access. Right before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's France Veterinary Healthcare Market Market Size Measured Against Other Published Estimates

Published estimates for France often differ because not every study counts the same spend streams, and the timing of the base year can vary by one or more years. Differences also come from how diagnostics is treated (in-clinic versus reference labs), how animal types are grouped, and whether value is measured at the manufacturer level or closer to the clinic invoice level.

The gaps usually get larger when a study folds in veterinary services revenue, uses aggressive price escalation, or applies untested penetration rates for diagnostics and specialty therapeutics. We kept the model tied to observable demand drivers in France, and then rechecked totals with interview-based reality checks on visit volumes, test utilization, and treatment patterns before finalizing the current-year value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.75 B (2025) | |

| Global Consultancy A | USD 4.12 B (2021) | Uses a veterinary care framing that can include clinic service revenue and procedure fees, and it is anchored on a 2021 base year, which shifts the price and volume context versus product-only tracking. |

| Industry Publisher B | USD 0.85 B (2024) | Appears to use a narrower counted basket and a different base-year construction, which can understate diagnostics value if reference lab activity and higher-complexity tests are not fully captured. |

The table shows a wide spread driven mainly by what is counted as healthcare spend, and in Mordor Intelligence's model the total reflects therapeutics and diagnostics product value rather than adding broad clinic service revenue. That is why it sits below care-inclusive figures, but above very narrow product baskets. When scope and base-year differences are made explicit, the remaining variance becomes easier to reconcile through repeatable checks on utilization, pricing, and mix.

Key Questions Answered in the Report

How large is the France veterinary healthcare market in 2026?

It stands at USD 2.92 billion and is forecast to reach USD 3.92 billion by 2031 at a 6.08% CAGR during 2026-2031.

Which product category holds the biggest share?

Therapeutics lead with 59.78% of 2025 revenue, driven by vaccines and parasiticides.

What is the fastest-growing segment of the market?

Diagnostics, supported by AI-enhanced point-of-care tools, is expanding at a 7.32% CAGR through 2031.

Why is poultry health spending rising?

Nationwide avian influenza vaccination success and export-oriented producers push poultry care to a 6.55% CAGR.

How does insurance influence veterinary spending?

Broader pet insurance coverage reduces cost barriers, increasing uptake of advanced treatments and diagnostics.

What challenges limit rural veterinary care?

An aging workforce and fewer new graduates in food-animal practice create service gaps in remote livestock regions.

Page last updated on: