Veterinary Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

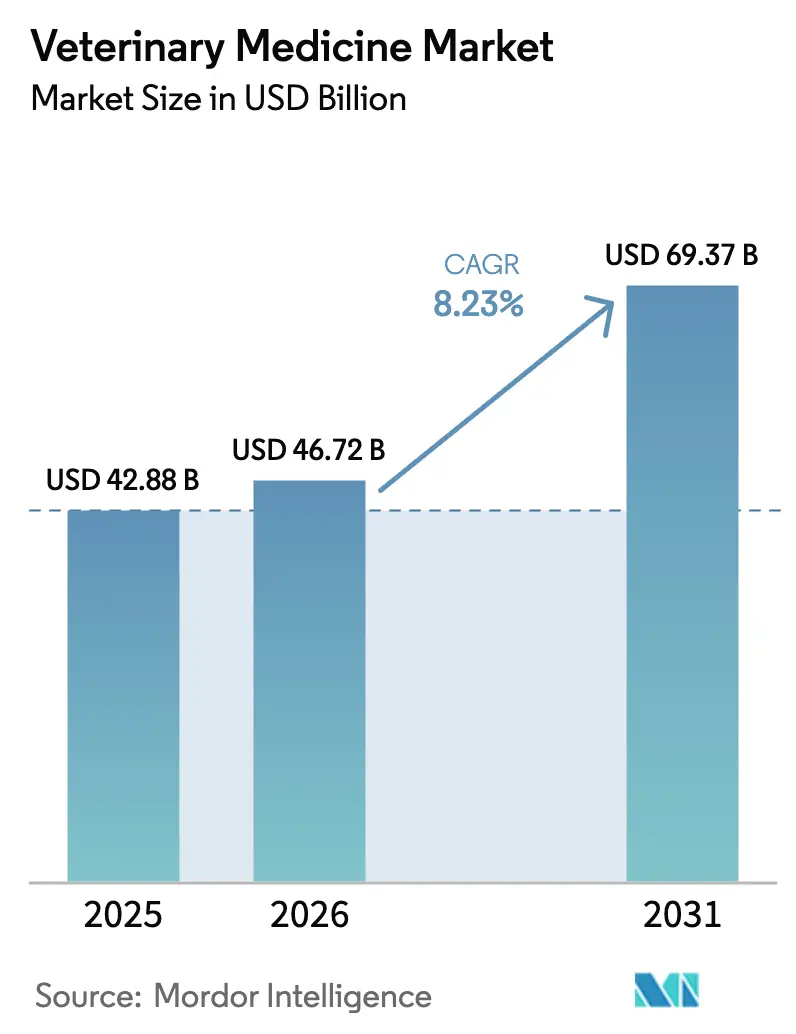

| Market Size (2026) | USD 46.72 Billion |

| Market Size (2031) | USD 69.37 Billion |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Medicine Market Analysis by Mordor Intelligence

The Veterinary Medicine Market size is expected to grow from USD 42.88 billion in 2025 to USD 46.72 billion in 2026 and is forecast to reach USD 69.37 billion by 2031 at 8.23% CAGR over 2026-2031.

Strong pet ownership growth in the Asia-Pacific region, industrialized poultry and swine operations in South America, and stringent antibiotic stewardship rules in North America and Europe continue to widen the demand for vaccines, recombinant platforms, and topical parasiticides. Competitive dynamics remain moderately consolidated, as the top four suppliers utilize vertically integrated R&D and multispecies portfolios to defend a combined significant share. Meanwhile, e-pharmacy penetration, although still below 15%, accelerates owner access to chronic-care prescriptions. Venture funding channels into monoclonal antibody (MAb) and gene-edited vaccine pipelines, indicating an innovation cycle that favors biologics, which have gross margins of 40-60%, compared with 20-30% for small-molecule generics.

Key Report Takeaways

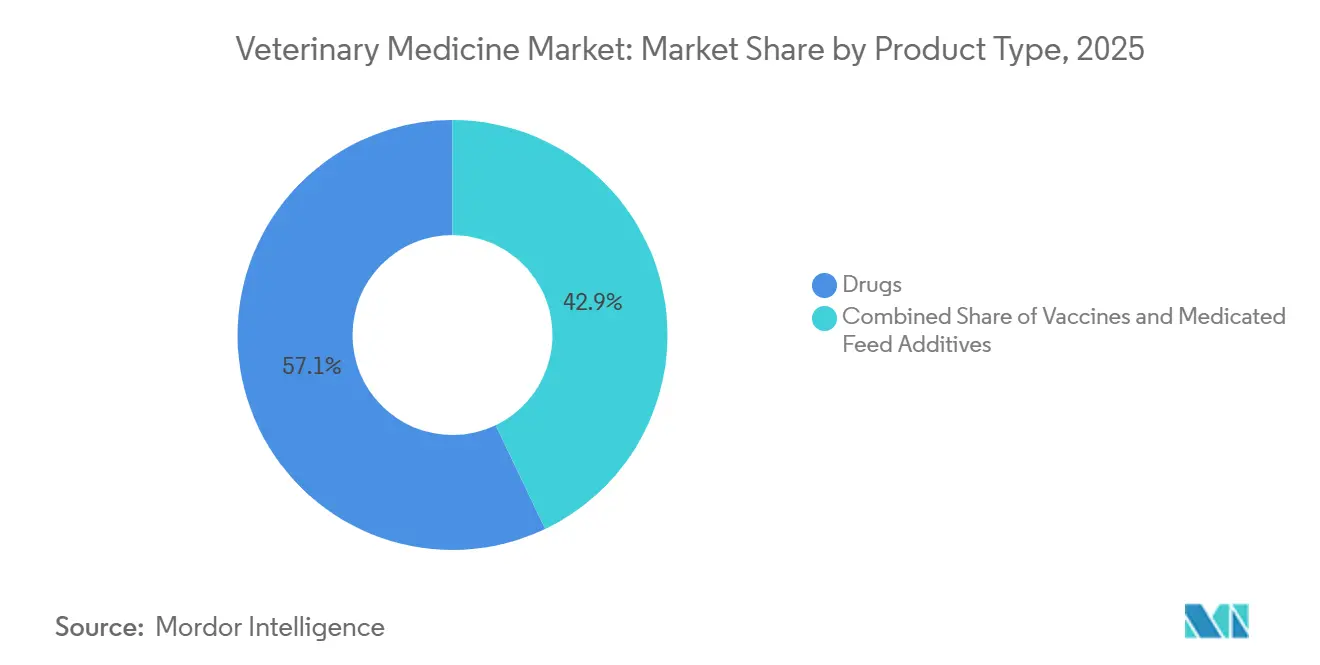

- By product type, drugs led with a 57.11% revenue share in 2025, while vaccines are projected to advance at a 10.62% CAGR through 2031.

- By animal type, companion animals accounted for 55.93% of the 2025 total, while livestock treatments are projected to grow at a 12.26% CAGR through 2031.

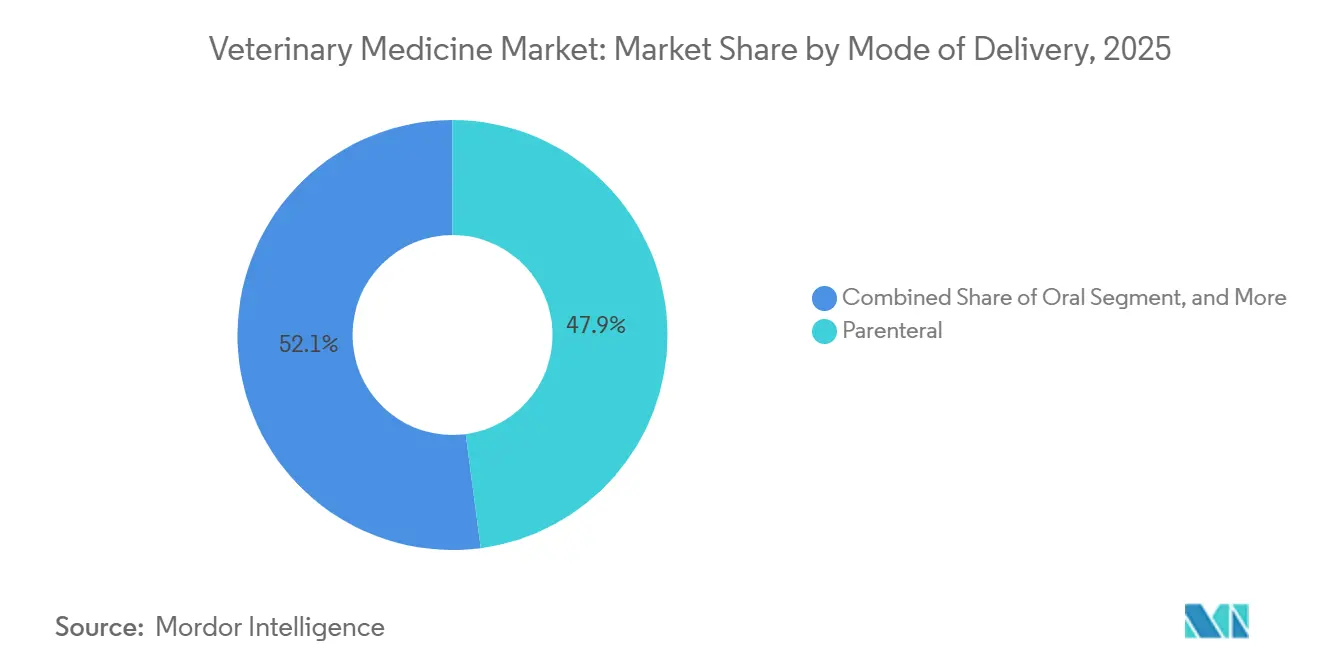

- By mode of delivery, parenteral formats accounted for 47.88% of sales in 2025; however, topical formulations are expanding at a 10.06% CAGR through 2031.

- By end user, veterinary hospitals represented 58.14% of 2025 spending, whereas clinics are poised for a 12.75% CAGR as telehealth routes prescriptions to lower-overhead settings.

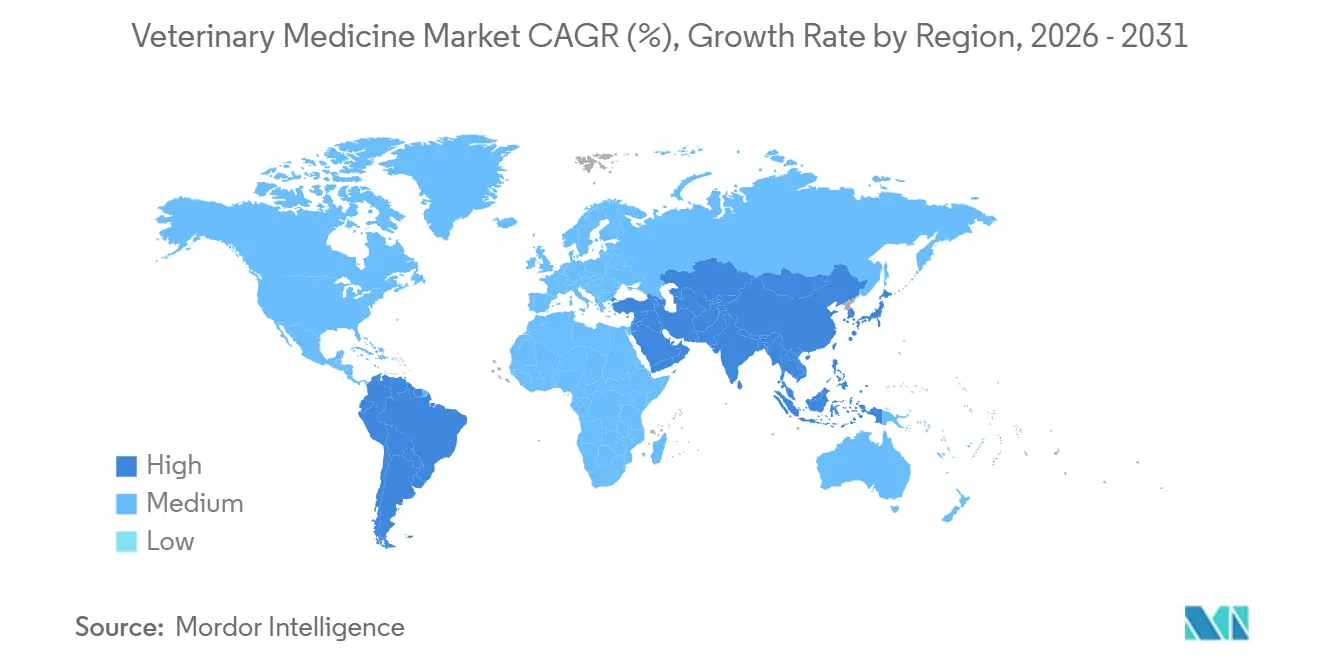

- By geography, North America accounted for 41.46% of 2025 revenue, and the Asia-Pacific region is projected to post an 11.86% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Medicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Animal Diseases & Pet Ownership | +1.8% | Global, concentrated in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Industrialised Livestock Expansion | +1.5% | Asia-Pacific core (China, India, Vietnam), spill-over to South America (Brazil, Argentina) | Long term (≥ 4 years) |

| Regulatory Antibiotic-Stewardship Push for Vaccines/Biologics | +1.3% | Europe (EU mandates), North America (FDA guidance), emerging in APAC | Medium term (2-4 years) |

| Break-Through MAbs & Gene-Based Therapies Approvals | +1.1% | North America & Europe (early adoption), premium segments in APAC | Long term (≥ 4 years) |

| Digital / E-Pharmacy Acceleration | +0.9% | North America, Western Europe, urban China and India | Short term (≤ 2 years) |

| Specialty Therapeutics for Ageing Pets | +0.7% | North America, Japan, Australia, affluent urban centers globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Animal Diseases & Pet Ownership

Pet-ownership levels climbed to 67% of U.S. households in 2024 and continue to rise, while chronic conditions now affect approximately 40% of dogs older than seven years.[1]American Veterinary Medical Association, “U.S. Pet Ownership Statistics,” avma.org The annual spend per companion animal reached USD 1,620 in 2025, a 12% year-over-year increase, as owners opt for long-term disease management over euthanasia. Four-point-four million pets carried insurance in North America by the end of 2025, shifting more out-of-pocket risk to insurers and enabling the uptake of premium biologics. China, with a population of over 200 million pets in 2025, mirrors these patterns as urban millennials allocate 15% of their disposable income to pet care. The resulting demand underscores a durable driver for the veterinary medicine market across both mature and emerging economies.

Industrialised Livestock Expansion

China rebuilt its swine herd to 450 million head by mid-2025 under biosecurity rules that require trivalent vaccines, triggering sustained demand for porcine biologics.[2]USDA Foreign Agricultural Service, “Livestock and Poultry: World Markets and Trade,” usda.gov India’s layer-hen capacity increased by 8% between 2024 and 2025, resulting in the production of 52 billion eggs, which subsequently raised demand for respiratory vaccines. Brazil’s 234 million-head cattle sector is trialing methane-reducing feed additives that also improve weight gain, thereby boosting therapeutic volumes. Vietnam’s aquaculture producers lowered antibiotic use by 22% in 2025 by adopting autogenous vaccines. Together, these developments serve as a long-term catalyst for the veterinary medicine market, as producers shift from growth-promoting antibiotics to preventive platforms.

Regulatory Antibiotic-Stewardship Push for Vaccines/Biologics

EU Regulation (EU) 2019/6, which prohibits the use of prophylactic antibiotics in livestock, came into full force in 2024.[3]European Medicines Agency, “Veterinary Medicinal Products Regulation,” ema.europa.eu In the United States, FDA Guidance 263 was issued in 2025, removing the remaining over-the-counter livestock antibiotics. China banned colistin feed additives and will mandate electronic prescriptions by 2026. Compliance costs averaged EUR 8,500 per EU farm in 2025, nudging smallholders toward consolidators. These policy moves divert investment to vaccines, probiotics, and organic acids, lifting the preventive-care contribution to the veterinary medicine market.

Break-Through MAbs & Gene-Based Therapies Approvals

The FDA granted conditional approval for Librela in cats in 2024, and the earlier canine version, which validated MAb pain control, was priced at USD 90-120 per month, compared to triple generic NSAIDs. Elanco’s Credelio Plus won EMA clearance in 2025, combining flea, tick, and heartworm protection in one dose. Boehringer Ingelheim’s gene-deleted African swine fever vaccine entered Phase III trials after proving 94% efficacy. Ceva’s recombinant fowlpox vector vaccine launched in Latin America in 2025, broadening DIVA-capable poultry immunization. These milestones highlight the increasing share of biologics in the veterinary medicine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Veterinary Care & Diagnostics | -0.8% | Global, acute in price-sensitive markets (South America, Southeast Asia, rural areas) | Short term (≤ 2 years) |

| Stringent Multi-Region Regulatory Pathways | -0.6% | Global, most complex in EU and North America, emerging in China and India | Medium term (2-4 years) |

| Consumer Backlash on Antibiotic Use in Food Animals | -0.4% | Europe, North America, urban Asia-Pacific | Medium term (2-4 years) |

| Fragile API & Biologics Cold-Chain Supply | -0.5% | Global, critical in tropical regions (Southeast Asia, Sub-Saharan Africa, South America) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Veterinary Care & Diagnostics

MRI scans cost USD 2,500-3,500 in the United States in 2025, discouraging 40% of uninsured owners from pursuing advanced imaging. Cytopoint therapy for a 30-kg dog costs USD 1,080-1,440 per year, while generic steroids total USD 180, creating adherence gaps. South American cattle operations earn margins below USD 50 per head, making USD 2 vaccines unviable unless mortality risk is severe. Small Indian dairy farmers spend under USD 12 annually per cow, relying on subsidized campaigns. High price points, therefore, constrain premium uptake, tempering expansion of the veterinary medicine market.

Stringent Multi-Region Regulatory Pathways

Veterinary approvals take an average of 7.2 years in the United States, longer than for human drugs, because safety trials span multiple species. EMA procedures can extend to 8.5 years when arbitration is involved. China’s 2024 biologics rules add domestic trials even for already-approved Western products, adding 18-24 months and USD 3-5 million in costs. Divergent residue limits require reformulation or market exit. Smaller companies struggle to navigate the complexity, dampening competitive diversity within the veterinary medicine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biologics Gain as Antibiotics Face Regulatory Headwinds

Drugs controlled a 57.11% share in 2025, but vaccines are on track for a 10.62% CAGR, a pivot that mirrors antibiotic-stewardship mandates. Parasiticides, such as NexGard and Credelio, generated more than USD 1 billion combined in 2025, buoyed by warming climates that extend flea and tick seasons. Anti-infective sales declined 18% year-over-year in Europe, as the use of fluoroquinolones and cephalosporins decreased. Recombinant vaccines offer DIVA capability, and Zoetis’s Fostera Gold PCV MH earned USD 180 million in 2025 by bundling protection against two porcine pathogens. Amino-acid feed additives expanded by 9% as producers sought growth promotion without antibiotics.

By Animal Type: Livestock Industrialization Narrows Companion-Animal Lead

Companion animals accounted for 55.93% of 2025 revenue; however, livestock treatments are projected to have a 12.26% CAGR, a rate that will progressively narrow the gap. Dogs represented 62% of companion-animal turnover thanks to higher dosing volumes and a greater orthopedic surgery burden. Cats followed at 32%, boosted by feline-specific biologics such as Solensia. Cattle remain the largest livestock spenders by absolute value. Yet, poultry is expected to grow fastest as China, India, and the United States vaccinate billions of birds at a minimal per-dose cost. The swine sector's recovery from African swine fever has led to high vaccine uptake, reaching 78% of commercial farms by 2025.

By Mode of Delivery: Topical Gains as Owner Administration Rises

Parenteral products accounted for 47.88% of sales in 2025, but topical revenues are projected to grow at a 10.06% CAGR through 2031. Owner-applied parasiticides, such as Frontline and Advantage, together generated USD 340 million in 2025, with the convenience of once-monthly applications driving compliance. Oral chewables accounted for 38% of the 2025 turnover, led by heartworm and flea preventives, which achieved a 94% palatability acceptance rate. Transdermal offerings remain rare due to fur interference and variability in absorption, which limits category expansion. Automated injection in poultry operations sliced labor costs to USD 0.08 per bird, anchoring parenteral dominance in industrial livestock.

By End User: Clinics Gain Share as Telemedicine Routes Prescriptions

Veterinary hospitals owned 58.14% of the 2025 spend, underpinned by 24-hour emergency and surgical capabilities. Clinics, numbering about 28,000 in the United States, are set for a 12.75% CAGR through 2031, propelled by telehealth partnerships that funnel prescription volumes without in-person exams. Home-care settings captured 18% of 2025 revenue as owners administered chronic treatments purchased online. Corporate consolidators expanded footprints and negotiated 15-20% pharmaceutical discounts, widening margin advantages. Research institutes kept 4% of spending, supporting 42 investigational new animal drug studies in 2025.

Geography Analysis

North America generated 41.46% of the 2025 revenue, driven by 85 million U.S. pet households and an annual per-pet spend exceeding USD 1,500. The region’s regulatory emphasis on antimicrobial stewardship pushes vaccine adoption, while e-pharmacy leadership expands access. Europe captured 28% of 2025 sales as pet insurance coverage exceeded 25% in the United Kingdom and Sweden, stabilizing out-of-pocket expenses. Regulation (EU) 2019/6 reinforces the use of preventive biologics, and pain-management rules increase analgesic uptake in livestock.

The Asia-Pacific region is poised for an 11.86% CAGR and is gradually challenging North American dominance as China rebuilds its hog herd and India scales up poultry capacity. Rising urban disposable incomes lift companion-animal demand; tier-1 Chinese cities alone counted 121 million pets in 2025. Cold-chain gaps remain a constraint; however, domestic biologics manufacturing investments are ramping up, signaling a long-term upside for the veterinary medicine market.

South America contributed 9% of 2025 turnover, chiefly from Brazil’s 234 million-head cattle herd; however, per-animal spend lags global averages because producers favor generics. Middle East & Africa held 6%, with equine therapeutics in GCC countries and South African vaccines against foot-and-mouth disease anchoring demand. Regional growth prospects depend on improving cold-chain infrastructure and gains in purchasing power.

Regulatory Landscape

Veterinary medicines regulation continues to tighten around antimicrobial stewardship, residues, and pharmacovigilance across major markets. In the European Union, Regulation (EU) 2019/6 remains the core framework governing marketing authorizations and post-market surveillance, with the European Medicines Agency (EMA) and its Committee for Veterinary Medicinal Products (CVMP) steering 2026 work priorities. These priorities include facilitating development via veterinary scientific advice and maintaining updates tied to maximum residue limits (MRLs). The practical effect is a continued shift from routine antibiotic use toward preventive vaccines, recombinant platforms, and other alternatives aligned with food-chain compliance needs.

In the United States, the FDA Center for Veterinary Medicine (CVM) continues to manage approvals and policy under the Federal Food, Drug, and Cosmetic Act, with FY 2026 animal drug user fee rates (ADUFA/AGDUFA) in effect through September 30, 2026, shaping sponsor budgeting and review planning. The FDA also issued final Guidance for Industry (GFI) #96 in June 2026 on anthelmintic effectiveness for ovines, reinforcing method and evidence expectations in parasiticide development. In Great Britain, the Veterinary Medicines (Amendment etc.) Regulations 2024 (in force May 2024) updated domestic requirements post-Brexit. Government guidance also flags a new SPS agreement targeted for mid-2027, with further business guidance expected in autumn 2026, which adds compliance planning complexity for manufacturers and distributors serving UK and EU supply routes.

Value Chain Analysis

The veterinary medicine value chain spans discovery and multi-species development, regulatory submission and review, GMP manufacturing (including sterile biologics and cold-chain-dependent vaccines), and route-to-market through specialized animal health distributors and veterinary providers. Upstream dependencies include APIs, excipients, packaging, and biologics inputs, while midstream operations depend on validated quality systems that can withstand regulator inspections across jurisdictions. Downstream, manufacturers rely on veterinary hospitals and clinics for prescribing and administration, alongside e-pharmacy and home-care channels that are expanding access for chronic therapies. Even with that access, exclusivity arrangements and channel rules can still limit product availability in some markets.

Distribution and service layers are consolidating into broader platforms that bundle logistics, practice technology, diagnostics, and replenishment programs, tightening control over inventory flow and customer capture. 2026 deal activity highlights the pull toward integrated platforms: Covetrus and MWI Animal Health announced a merger to combine distribution and technology platforms, while Zoetis pursued capability additions in diagnostics and precision animal health through acquisitions. At the same time, manufacturing delays, API and raw material constraints, and higher compliance burdens for international facilities continue to create episodic shortages. These constraints also push prioritization toward higher-volume SKUs, particularly for cold-chain biologics and specialty products.

Competitive Landscape

The veterinary medicine market remains moderately consolidated, with Zoetis, Boehringer Ingelheim Animal Health, Elanco, and Merck Animal Health collectively controlling a significant portion of global revenue through vertically integrated pipelines and multiregional distribution. Smaller firms exploit white-space niches; Ceva leads the recombinant poultry vaccines market, Virbac pursues exotic-pet dermatologics, and Phibro focuses on feed-mill additives. M&A activity continues: Mars Veterinary Health acquired 180 U.S. clinics in 2025, expanding its network to 3,200 sites and integrating product sales with its services.

Technology investments target recombinant-vaccine plants, with Boehringer Ingelheim allocating EUR 150 million in 2025 to its Lyon capacity, which halves the production cycle time. Merck Animal Health filed patents for a thermostable Newcastle disease vaccine stable at 25 °C for six months, addressing cold-chain gaps in tropical markets. The competitive playbook increasingly pairs digital outreach with value-added diagnostics, as IDEXX and Heska bundle point-of-care analyzers with auto-reorder reagent programs to lock in clinic subscriptions.

Barriers to entry remain high: navigating multi-region approval costs of USD 8-12 million per product, maintaining GMP biologics plants, and funding robust safety studies across multiple species. Nonetheless, venture funding in pet-focused MAbs signals an appetite for differentiated modalities with rapid ramp-up potential, as illustrated by Cytopoint’s USD 300 million in global sales within three years of launch.

Veterinary Medicine Industry Leaders

Ceva Santé Animale

Boehringer Ingelheim Animal Health

Elanco Animal Health

Merck Animal Health

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Biologics capacity buildout and specialized vaccine manufacturing create visible whitespace for improving supply resilience and access, particularly for recombinant and autogenous vaccines that require tighter GMP controls. Merck Animal Healths USD 895 million investment announced in May 2025 to expand manufacturing and R&D in De Soto, Kansas, focused on large-molecule vaccines and biologics, and Cevas planned new 7,000 m2 vaccine plant at Ceva Phylaxia in Monor, Hungary (scheduled for operation at end-2026) highlight ongoing scaling in high-barrier categories. Dopharma and Ripac-Labor also advanced a new autogenous vaccine production facility in Potsdam, Germany, with an end-2026 commissioning target, supporting an opportunity set around farm-specific solutions where antimicrobial stewardship and biosecurity programs tighten.

Precision animal health and clinic productivity tools offer another opportunity lane as diagnostics and digital workflows become more embedded in prescribing and monitoring. The 2026 acquisition activity by Zoetis in diagnostics and genomics (VitalRADS and Neogens animal genomics business) illustrates a commercial push to connect testing, data, and therapeutics, which can improve targeting of parasiticides, pain biologics, and chronic-care regimens in companion animals. It also supports herd-level decisions in production animals. On the public-private side, the European Partnership on Animal Health and Welfare launched in 2024 with a EUR 360 million, seven-year budget provides a structured vehicle for collaborative R&D and data-driven animal health programs, reinforcing demand for validated vaccine platforms, residue-compliant treatments, and surveillance-linked products that fit modern stewardship policies.

Recent Industry Developments

- July 2026: Zoetis entered a definitive agreement to acquire VitalRADS, expanding its diagnostics capabilities and extending its footprint in veterinary workflows. The move strengthens Zoetis position in test-to-treatment pathways where diagnostics influence therapeutic selection and monitoring. It also supports deeper integration with clinic and hospital purchasing behavior as diagnostics and medicines become more tightly bundled.

- June 2026: Elanco received USDA approval for TruCan Ultra Lyme-L4, a combination vaccine for canine Lyme and leptospirosis. The approval broadens Elancos preventive portfolio in companion animals and aligns with rising demand for vaccines as antimicrobial stewardship tightens. It also adds a differentiated format that supports practice efficiency and owner compliance in routine vaccination schedules.

- October 2024: Boehringer Ingelheim opened an expanded research and development facility in Athens, Georgia, adding new laboratory and administrative space. The investment increases local R&D capacity for animal health programs and supports faster iteration across biologics and therapeutics pipelines. Expanded infrastructure also helps strengthen regional talent attraction and cross-functional development throughput.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of medicines used to prevent, treat, and manage animal health conditions, for companion and livestock animals, sold through typical veterinary and pharmacy channels across major regions.

Scope exclusions: veterinary services, diagnostics, and medical devices are not counted unless they are bundled into the medicine value reported in public financial statements.

Segmentation Overview

- By Product Type

- Drugs

- Anti-infectives

- Anti-inflammatory

- Parasiticides

- Biologics / Vaccines

- Other Drugs

- Vaccines

- Inactive Vaccines

- Attenuated Vaccines

- Recombinant Vaccines

- Other Vaccines

- Medicated Feed Additives

- Aminoacids

- Antibiotics

- Other Medicated Feed Additives

- Drugs

- By Animal Type

- Companion Animals

- Dogs

- Cats

- Other Companion Animals

- Livestock Animals

- Cattle

- Poultry

- Swine

- Sheep & Goats

- Other Livestock

- Companion Animals

- By Mode of Delivery

- Parenteral

- Oral

- Topical

- Other Mode of Delivery

- By End User

- Veterinary Hospitals

- Veterinary Clinics

- Home-care Settings

- Research & Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what is being counted and how it is recorded in public statistics. We review sources such as the US FDA Center for Veterinary Medicine, the USDA and related animal health publications, the European Medicines Agency, and the World Organisation for Animal Health (WOAH) to track policy shifts and disease surveillance signals. For trade and supply indicators, references like UN Comtrade and national customs releases help check flows for animal health preparations, though import codes do not perfectly map to each therapy group.

To keep the model grounded in commercial reporting, we also use company annual reports, 10-K style filings, investor presentations, and reputable press coverage to track product revenue lines and mix changes. Patent databases are reviewed to gauge innovation intensity and timing, and a paid subscription focused on company financials and news helps standardize peer comparisons and corporate actions. This list is illustrative, and many other public sources are also referenced for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that are hard to read from public sources, especially demand drivers by species and how realized pricing moves with product mix. We speak with manufacturers, distributors, veterinary hospital and clinic stakeholders, and practicing professionals across APAC, EMEA, and the Americas, so the inputs reflect purchasing behavior and channel margins observed in day-to-day buying.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 44% |

| Mid tier: 48% | Functional/Unit leaders: 36% | EMEA: 31% |

| Smaller Players: 22% | Managers: 52% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built mainly from a top-down demand pool, where animal population and disease incidence signals are translated into treated cases and typical therapy use, then converted into value using pricing benchmarks by product class. Since reporting practices differ by country, we normalize inputs to a consistent currency year and align them to the same definition of veterinary drugs, vaccines, and medicated feed additives.

To keep the total realistic, selective bottom-up checks are run on sampled supplier revenue exposure, channel markups, and a few volume times average selling price approximations where public data is available. When visibility is limited, such as for smaller local brands or informal channels, the shortfall is estimated using proxy indicators like veterinary visit intensity, livestock production cycles, and import dependence, then reviewed against interview feedback. For forecasting, scenario analysis is used around a base case, with key drivers including pet adoption and spend per visit, livestock inventory trends, preventive vaccination uptake, anti-infective stewardship rules, and price and mix movement. Assumptions are adjusted only after reasonableness checks across regions and species.

Data Validation & Update Cycle

Validation is done by comparing model outputs with independent signals that should move in the same direction, such as animal population shifts, major outbreak cycles, and reported category growth in public filings. Outliers are flagged, and we re-check whether the issue comes from a scope mismatch, a one-time pricing jump, or a country data break that needs smoothing.

Before sign-off, the build is reviewed in steps by another analyst to confirm that formulas, year alignment, and currency conversion choices are consistent. The report is refreshed annually, and interim updates are made when material events occur, such as new regulations, large acquisitions, or unusual disease events that change demand. Right before delivery, the latest public releases are re-scanned so clients receive an updated view rather than an older snapshot.

Mordor Intelligence's Veterinary Medicine Market Sizing Compared With Other Published Estimates

Different published market sizes can vary in veterinary medicine, even when they claim to cover the same topic. The spread usually comes from what is included as medicine versus adjacent categories, the year used for currency conversion, and whether values reflect manufacturer-level pricing or downstream selling prices.

In practice, gaps are often driven by whether medicated feed additives are fully counted, how companion and livestock demand is balanced in the same total, and how price changes are applied when product mix shifts toward newer parasiticides or specialty therapies. Another common driver is refresh cadence, since outbreak effects and regulatory stewardship actions can change volumes quickly, and older models may still carry forward outdated penetration assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 42.88 B (2025) | |

| Global Consultancy A | USD 31.08 B (2024) | Uses a manufacturer-level valuation approach (factory-gate style) and a different base year, which typically sits below end-market values that include channel markups and later-year price and mix effects. |

| Regional Consultancy B | USD 36.11 B (2024) | Anchors the estimate to a 2024 base with a broader route and end-user framing, which can compress totals when treated case growth and pricing are not fully re-leveled for later-year mix changes. |

The table shows that the biggest differences come from valuation level and timing, and then from how quickly pricing and product mix are refreshed in the assumptions. When channel markups, species demand balance, and later-year price normalization are handled consistently, the 2025 total lands higher than 2024 manufacturer-led views, a choice applied by Mordor Intelligence.

Key Questions Answered in the Report

How large is the veterinary medicine market in 2026?

The veterinary medicine market size stood at USD 46.72 billion in 2026 and is projected to reach USD 64.37 billion by 2031.

Which product category is growing fastest?

Vaccines are set for a 10.62% CAGR through 2031 as regulators restrict antibiotic use and producers pivot to preventive care.

Which region will post the highest growth?

Asia-Pacific is forecast to record an 11.86% CAGR, driven by China’s swine-herd rebound and India’s poultry expansion.

Why are biologics gaining momentum?

Regulatory antibiotic-stewardship rules and high owner willingness to pay for premium therapies make monoclonal antibodies and recombinant vaccines attractive.

What is driving clinic-level growth?

Telemedicine platforms channel chronic-care prescriptions to lower-overhead clinics, supporting a projected 12.75% CAGR for this end-user segment.

Page last updated on: