Veterinary Eye Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

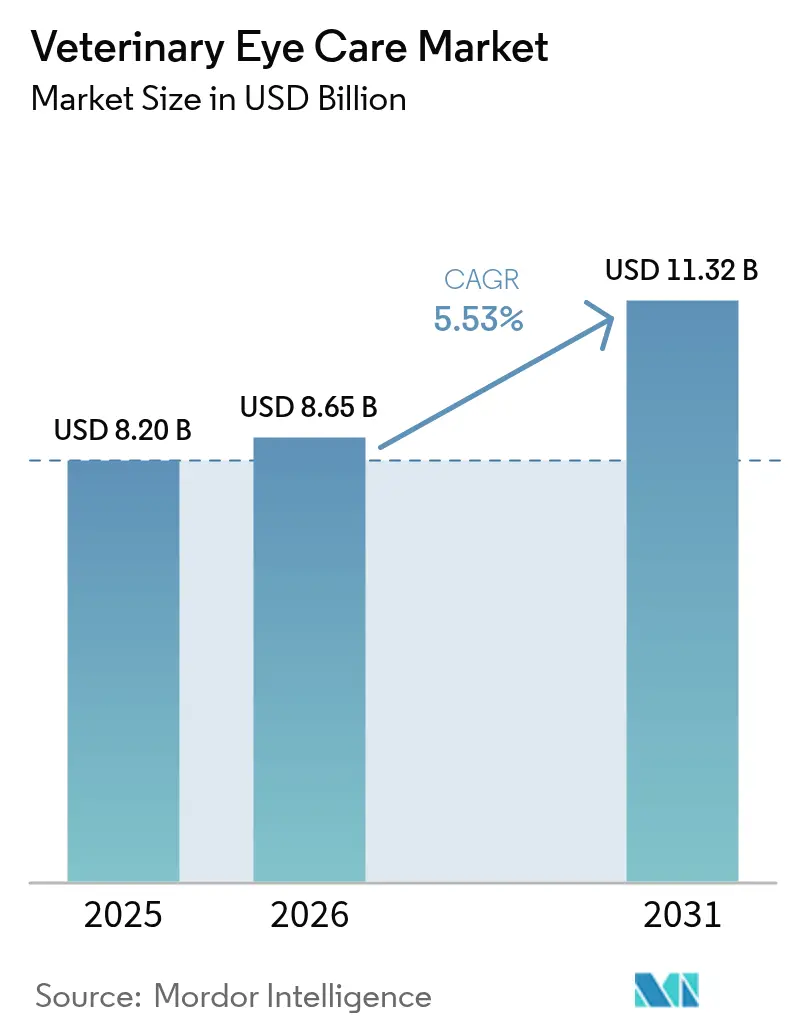

| Market Size (2026) | USD 8.65 Billion |

| Market Size (2031) | USD 11.32 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Eye Care Market Analysis by Mordor Intelligence

The veterinary eye care market size was valued at USD 8.20 billion in 2025 and estimated to grow from USD 8.65 billion in 2026 to reach USD 11.32 billion by 2031, at a CAGR of 5.53% during 2026-2031. Owners increasingly view ocular interventions as basic care rather than electives, so demand is rising even as routine wellness visits decline. Insurers now reimburse high-value surgeries such as canine cataract extraction, which lowers owners’ out-of-pocket burden and encourages procedure uptake. Referral networks in the United States and Western Europe continue to expand, yet a global shortage of board-certified ophthalmologists pushes clinics toward tele-ophthalmology for triage and toward simplified lasers for in-house care. Regulatory tightening around injectable-grade sterility helps large manufacturers defend premium drug pricing, but it also postpones generic entry. Simultaneously, regenerative gels, crosslinking kits, and stem-cell injectables are moving from university trials into commercial pilots, adding new revenue streams over the next five years.

Key Report Takeaways

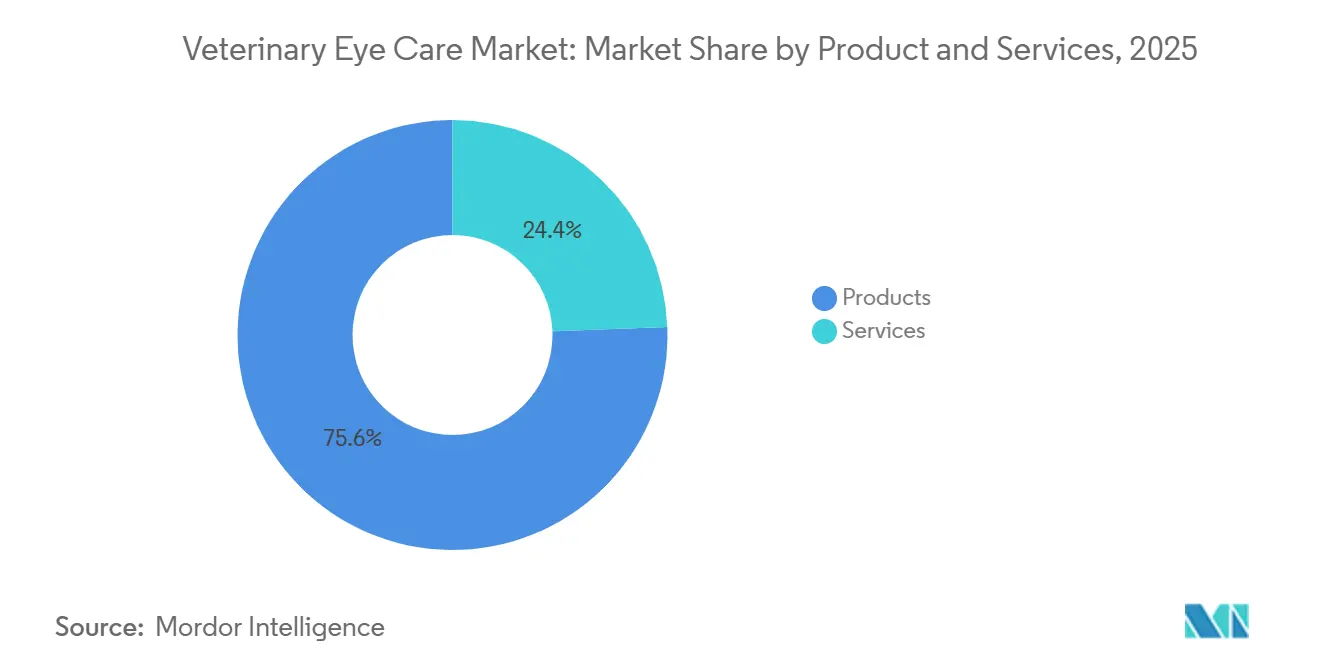

- By products and services, products led with 75.55% of the Veterinary Eye Care market share in 2025; services are forecast to expand at a 6.85% CAGR through 2031.

- By animal type, dogs accounted for a 50.53% share of the Veterinary Eye Care market size in 2025, and horses are projected to grow at a 6.75% CAGR over 2026-2031.

- By application, keratoconjunctivitis sicca held a 32.15% share in 2025, while corneal ulcers and injuries are set to grow at a 7.82% CAGR to 2031.

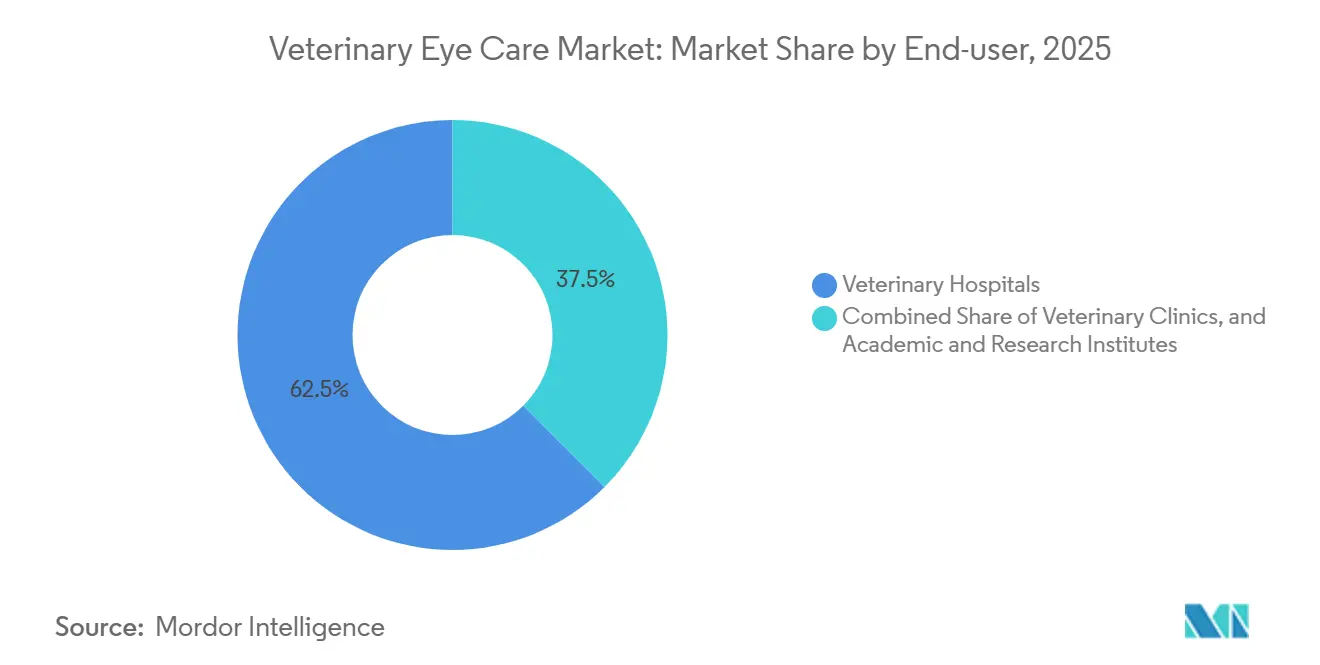

- By end user, veterinary hospitals commanded 62.52% revenue share in 2025, whereas veterinary clinics are forecast to register a 6.12% CAGR through 2031.

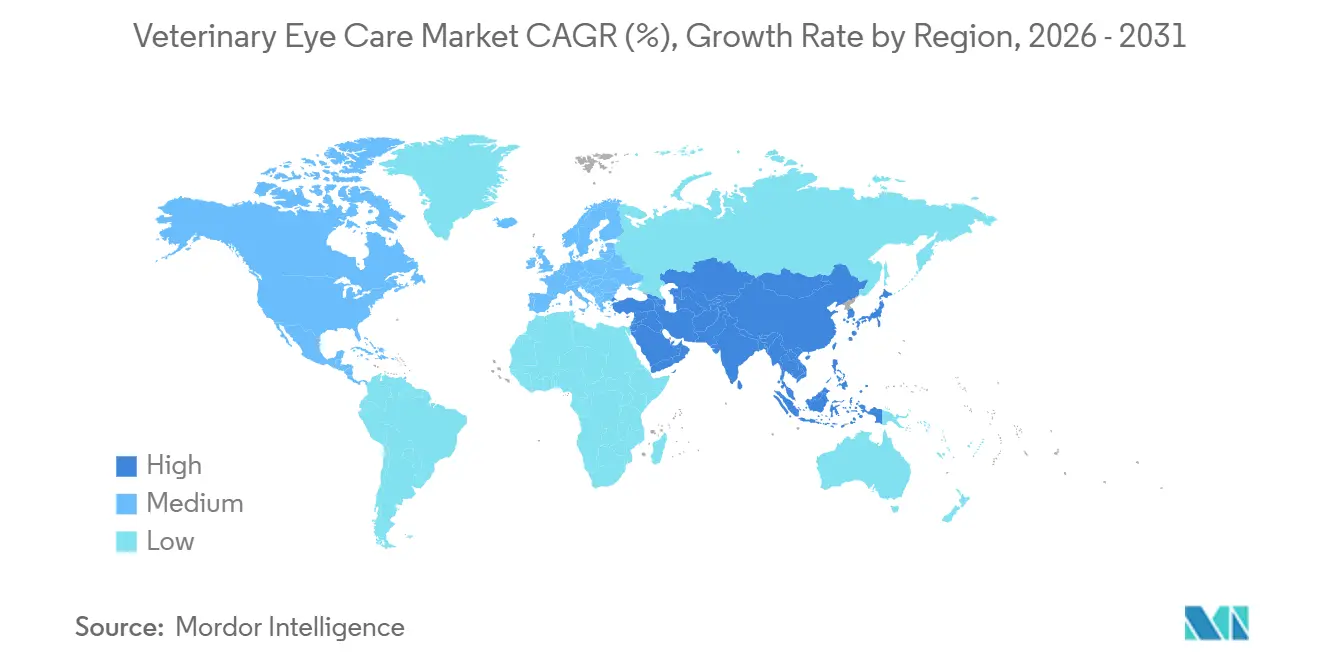

- By geography, North America held a 38.62% share in 2025, and Asia-Pacific is expected to advance at a 6.22% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Eye Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Pet Ownership & Spend on Advanced Veterinary Care | +1.2% | North America, Western Europe, Urban Asia-Pacific | Medium term (2-4 years) |

| Rising Prevalence of Ocular Disorders in Companion Animals | +1.0% | North America, Europe | Long term (≥ 4 years) |

| Expanding Portfolio of Topical Ophthalmic Drugs & Ointments | +0.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Demand for Minimally Invasive Ophthalmic Surgeries | +0.9% | North America, Western Europe, Australia, Japan | Medium term (2-4 years) |

| AI-Enabled Imaging & Tele-Ophthalmology Adoption | +0.6% | North America, Europe, China, India | Long term (≥ 4 years) |

| Stem-Cell And Other Regenerative Corneal-Repair Therapies | +0.5% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Pet Ownership & Spend on Advanced Veterinary Care

United States households kept 87.3 million dogs and 76.3 million cats in 2025, and the average annual spend per dog and per cat reached USD 598 and USD 529, respectively[1]American Veterinary Medical Association, “Pet Ownership Statistics,” avma.org. Routine wellness traffic fell, yet ophthalmology referrals rose, revealing a shift toward interventions that deliver a visible quality-of-life lift. Surveyed owners cite affordability and appointment scarcity as primary barriers, yet 37% still prioritize eye surgery when vision loss threatens activity levels. Millennials and Generation Z over-index on specialty procedures because they view pets as family. Although total veterinary expenditures dipped 4% between 2023 and 2024, clinics that prove rapid clinical gains continue to defend premium fees.

Rising Prevalence of Ocular Disorders in Companion Animals

A multi-year study covering 2021-2024 found ocular disease in 2.77% of dogs, led by cataracts, corneal ulcers, and conjunctivitis. Breed selection amplifies risk as French Bulldogs and Pinschers share narrow gene pools that magnify hereditary problems. The ACVO Blue Book now tracks more than 200 breed-linked eye defects, helping breeders test early, yet commercial incentives still favor popular brachycephalic lines. Equine recurrent uveitis affects up to 25% of horses in some regions, creating new demand for long-acting implants. Wider use of genetic screens uncovers subclinical lesions sooner, so the addressable population keeps rising.

Expanding Portfolio of Topical Ophthalmic Drugs & Ointments

The FDA lists cyclosporine 0.2% ointment, triple-antibiotic gels, and gentamicin drops under 21 CFR Part 524. Dechra added Remend Corneal Repair Gel in 2024, and early field data show faster epithelialization than standard therapy. Tarsus is repurposing Lotilaner 0.25% solution for canine blepharitis after its human approval. New sterility guidance issued in 2024 is driving manufacturers to upgrade their filling lines, delaying smaller entrants but ensuring product safety. As formularies widen, clinics gain drug choices that match disease stage and owner budget.

Demand for Minimally Invasive Ophthalmic Surgeries

Phacoemulsification restores vision in more than 90% of canine cataract cases when performed by specialists. Laser cyclophotocoagulation and shunt implantation now treat glaucoma without enucleation, preserving appearance and comfort. Equipment costs exceeding USD 50,000 continue to limit adoption in rural clinics. To close gaps, vendors bundle lasers with remote mentoring so general practitioners can start with lower case volumes. Insurers cover most of the cost, yet uninsured animals still risk blindness, so tiered pricing and leasing are under trial.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Ocular Equipment & Surgery | -0.9% | Price-sensitive Asia-Pacific and Latin America | Medium term (2-4 years) |

| Limited Insurance Reimbursement for Veterinary Eye Care | -0.7% | North America, Europe | Long term (≥ 4 years) |

| Stringent Regulatory Approval Timelines for Veterinary Drugs | -0.4% | FDA-CVM and EMA jurisdictions | Long term (≥ 4 years) |

| Shortage of Board-Certified Veterinary Ophthalmologists | -0.8% | Rural North America, Southern Europe, Emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Ocular Equipment & Surgery

Phaco units, OCT scanners, and diode lasers each exceed USD 50,000, which sidelines many single-doctor practices. Average canine cataract claims reached USD 5,785.40 between 2019-2024, with owners still paying USD 1,428.60 after insurance. Clinics in Latin America and India struggle with import duties and currency fluctuations that further inflate prices. Subscription leasing is being tested, yet low case volumes in rural markets complicate break-even projections. Consequently, uninsured animals often lose eyes to budget-friendly enucleation, holding back global procedure counts.

Limited Insurance Reimbursement for Veterinary Eye Care

Trupanion covers hereditary eye disease but imposes waiting periods, while Embrace aggregates bilateral conditions and caps payouts. United Kingdom policies classify time-limited and lifetime coverage differently, confusing owners about eligibility for long-term therapies. In the Asia-Pacific region, insurance penetration sits in the single digits, so elective surgeries remain out of reach for most. Misaligned definitions fuel distrust and delay care until vision loss becomes irreversible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products & Services: Services Grow as Tele-Ophthalmology Scales

Services generated rapid momentum, increasing at a 6.85% CAGR for 2026-2031, while products preserved a 75.55% revenue lead in 2025. Clinics increasingly unbundle diagnostics, surgery, and follow-up care from product sales, creating recurring service revenue. Tele-ophthalmology sessions let general practitioners triage conjunctivitis or dry eye before escalating complex ulcers. Even though no AI platform meets validation standards today, remote guidance already reduces referral wait times. The trajectory suggests that the Veterinary Eye Care market will continue to shift toward bundled procedure-plus-monitoring packages.

Drugs remain the backbone of revenue, anchored by cyclosporine ointment and triple-antibiotic gels registered under 21 CFR Part 524. Dechra’s 2024 regenerative gel added a premium tier that accelerates corneal recovery and lowers surgery rates. Instruments and implants remain niche but command high prices due to precision engineering. Diagnostic devices such as rebound tonometers now occupy reception desks in mainstream clinics, narrowing the referral funnel and lifting procedure capture rates inside primary practices.

By Animal Type: Equine Uveitis Drives Premium Pricing

Dogs accounted for 50.53% of 2025 revenue, reflecting both population dominance and a genetic predisposition to cataracts and KCS. Yet the fastest growth lies in equine cases, where suprachoroidal cyclosporine implants fetch above USD 2,000 per eye. Owners of performance horses accept these costs to preserve their sport careers. Cats add volume with viral conjunctivitis and corneal sequestrum, but lower price points limit category value. Niche exotic rabbits and birds grow slowly as urban clinics add small-mammal service lines.

Dogs will retain mass-market importance, yet horses add disproportionate dollars per procedure. As stem-cell research matures, premium therapies may first migrate to equine referrals, then trickle into canine practice. Clinics that build mixed-animal expertise gain a hedge against demand swings inside any single species pool.

By Application: Corneal Ulcers Benefit From Regenerative Innovation

Keratoconjunctivitis sicca still topped with 32.15% share in 2025, thanks to chronic drug therapy. However, corneal ulcers post the fastest 7.82% CAGR because regenerative crosslinking, amniotic grafts, and platelet-rich plasma shorten healing. Clinics monetizing these techniques capture new revenue while reducing repeat drug visits. Glaucoma maintains clinical urgency but carries a poorer prognosis, so enucleation persists where laser shunts are unavailable.

Corneal innovations showcase how research can move from human protocols to pets within 5 years. As clinical evidence solidifies, reimbursement support may broaden, driving even stronger expansion. Clinics that master crosslinking now will set local standards before competitors catch up.

By End-User: Clinics Democratize Access Through Equipment Adoption

Veterinary hospitals accounted for 62.52% of 2025 sales because they own phaco machines and OCT systems, yet general clinics grew 6.12% annually as they bought rebound tonometers and fundus cameras. This democratization reduces wait times and captures moderate cases locally. Academic centers host the most advanced imaging, but their market share remains minor. Tele-ophthalmology gives small clinics instant specialist input, improving case triage and owner confidence.

As the Veterinary Eye Care market size expands, hospitals will keep complex surgery volume, yet clinics will own the routine ulcer, KCS, and early glaucoma pipeline. Equipment vendors who offer leasing and online training stand to win first-time buyers in suburban practices.

Geography Analysis

North America retained 38.62% of 2025 global revenue, driven by dense specialty networks and 25%-plus pet insurance penetration. Average U.S. spend per dog touched USD 598 while overall vet spending slipped 4% as owners skipped routine checks but not sight-saving surgery. FDA sterility rules rolled out in 2024 give U.S. drug standards outsized global influence. Canada and Mexico expand steadily, though rural shortages of specialists mirror those in the U.S. farm belt.

Asia-Pacific records the quickest 6.22% CAGR through 2031. China’s urban singles and seniors drive companion adoption, yet care remains city-centric. Japan’s aging society values pet companionship, channeling spending into advanced surgery. Australia benefits from high insurance uptake and seamless EU-aligned regulation for imported devices. India and South Korea attract private equity to build multi-location chains that embed ophthalmology suites. Board-certified ophthalmologists remain rare, so simplified lasers and remote mentoring gain traction.

Europe offers mature demand, with Germany, the United Kingdom, and France leading specialty density. The EMA streamlines cross-border approvals, yet Eastern Europe faces staffing gaps. The United Kingdom’s mix of lifetime and time-limited insurance plans affects reimbursement consistency. In the Middle East and Africa, only the United Arab Emirates and South Africa host sizeable referral centers, while Latin America’s Brazil and Argentina grow but wrestle with currency and import duty volatility.

Regulatory Landscape

Veterinary ophthalmic therapeutics are primarily regulated as animal drugs, with core U.S. requirements covered under FDA Center for Veterinary Medicine pathways such as NADA/ANADA and relevant monographs including 21 CFR Part 524 for ophthalmic and topical dosage-form new animal drugs. On the device side, the FDA treats veterinary ophthalmic instruments as animal medical devices; these products generally do not go through premarket approval or 510(k), but they are still subject to adulteration and misbranding provisions, which affects how manufacturers label, distribute, and support clinic use.

International harmonization and manufacturing quality expectations also shape development timelines and costs. VICH GL61 (recommended in February 2024) reinforces Quality by Design expectations for veterinary pharmaceutical development, while EMA guidance on manufacture of veterinary finished dosage forms continues to anchor EU-aligned quality systems for sterile ophthalmic products. In the United States, the FDA CVM published the MUMS Blueprint for Success: 2026-2028 (June 2026), supporting modernization of minor use and minor species development pathways, and technical amendments to animal drug regulations were codified via a final rule effective April 2026, reflecting ongoing clarification of regulatory text impacting dossier maintenance and labeling accuracy.

Competitive Landscape

The veterinary eye care market is moderately fragmented. Zoetis, Elanco, and Dechra anchor drug portfolios, while niche innovators such as Tarsus transfer human ophthalmic molecules to pets. Dechra’s acquisition of Novartis eye brands and the launch of Remend Gel illustrate how incumbents add regenerative assets. Bausch + Lomb and Alcon sell adapted instruments, yet their veterinary footprint stays secondary to human lines. Covetrus bundles product supply with software that logs fundus images directly into practice records.

Equipment specialists Topcon, Eickemeyer, and Neogen compete on intuitive interface and price to secure first-time clinic buyers. Tele-ophthalmology startups Vetster and Pawp chase subscription models, but AI validation gaps delay fully automated grading. Academic centers license stem-cell patents to biotech spin-offs, yet FDA biologic ambiguity deters venture-scale growth. Corporate practice consolidators now negotiate group buy contracts that bundle tonometers with cloud image storage, raising entry barriers for small suppliers.

Incumbents who integrate drugs, devices, and digital consults under one brand may build sticky ecosystems. Meanwhile, the shortage of board-certified ophthalmologists sustains premium professional fees, prompting equipment makers to design platforms that allow supervised laser work by general practitioners.

Veterinary Eye Care Industry Leaders

Bausch & Lomb Incorporated

Innovacyn, Inc.

Zoetis

Dechra Pharmaceuticals, PLC

Elanco

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Named clinical programs and translational research are carving out more visible whitespace across retinal disease workups and advanced therapeutics for companion animals. The University of Pennsylvania School of Veterinary Medicine established the Retinal Health Clinic at Ryan Hospital (November 2024) and launched DogAEye, an AI-based clinical decision support tool for early detection of progressive retinal atrophy (December 2025). Together, these initiatives support image-driven triage, more standardized grading, and referral coordination in markets constrained by a shortage of board-certified veterinary ophthalmologists.

Therapeutic innovation opportunities are also emerging around ocular surface management and translational drug development. In the United Kingdom, Samaxia introduced Lacri+ Vitamin A, a preservative-free ophthalmic ointment developed by MP Labo for cats and dogs (May 2026), pointing to continued premiumization of chronic ocular-surface maintenance beyond standard lubricants. Curative Biotechnology announced a sponsored research agreement with Penn Vet to evaluate a GMP-grade, metformin-based topical ophthalmic formulation in a canine retinal degeneration model (May 2026), which adds a concrete route for industry-academic partnerships that use veterinary ophthalmology as a translational platform for inherited retinal disease programs.

Recent Industry Developments

- July 2026: Zoetis launched Lenivia (izenivetmab injection) in Canada and European Union member states for long-acting osteoarthritis pain management in dogs. While not an ophthalmic therapy, broader adoption of long-acting biologics in canine practice supports clinic comfort with premium injections and follow-up protocols, which can help specialty-care uptake for high-value eye procedures.

- October 2025: HICC Pet released rinse-free Oral Care Gel and Eye Relief Gel based on hypochlorous acid to simplify at-home hygiene routines. The release underscores continued commercialization of OTC-style eye relief solutions that can increase consumer pull-through at the retail and e-commerce layer, complementing clinic-led management of chronic ocular surface conditions.

- August 2024: Dechra targeted ophthalmic conditions with the launch of Ophtocycline ointment. The addition of another branded ophthalmic product expands treatment options in veterinary formularies and supports portfolio breadth for suppliers competing across both acute infection management and longer-cycle ocular care.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the veterinary eye care market covers spending on veterinary products and services used to diagnose, treat, and manage eye conditions in animals, across routine care and specialty ophthalmology settings.

Scope exclusions: Human ophthalmology products, farm management costs unrelated to eye health, and general veterinary care that is not linked to ocular diagnosis or treatment are not counted.

Segmentation Overview

- By Products & Services

- Product

- Ophthalmic Drugs

- Surgical Instruments

- Diagnostic Devices & Imaging

- Ocular Implants & Disposables

- Services

- Ophthalmic Surgical Services

- Diagnostic Imaging Services

- Tele-Ophthalmology & Consultation

- Post-operative Care Services

- Product

- By Animal Type

- Dogs

- Cats

- Horses

- Other Animals

- By Application

- Keratoconjunctivitis Sicca (Dry Eye)

- Conjunctivitis

- Corneal Ulcers & Injuries

- Glaucoma

- Uveitis & Retinal Disorders

- Others

- By End-user

- Veterinary Hospitals

- Veterinary Clinics

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping how animal eye conditions are typically diagnosed and treated, then aligning those care pathways with data that can be cross-checked in public sources. We used official and public bodies for product and care context, including the US FDA Center for Veterinary Medicine, the USDA for animal population and agriculture statistics, the World Organisation for Animal Health (WOAH) for animal health reporting, and the American Veterinary Medical Association for veterinarian workforce and practice trends.

We also reviewed peer-reviewed veterinary ophthalmology journals to anchor the common disease categories and treatment pathways. For product focus, distribution shifts, and pricing signals, we reviewed company filings, investor presentations, and reputable press. Where helpful, paid subscriptions for company financials and intelligence and patent databases were used to confirm company exposure and innovation direction, without relying on a single datapoint. The sources listed here are illustrative, and we also reviewed additional public documents to cross-check figures and clarify assumptions.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk research cannot fully show, especially utilization patterns, referral behavior, and practical price realization in clinics and hospitals. We interviewed and surveyed veterinarians, specialty ophthalmology staff, distributors, and industry experts across major regions, so assumptions on diagnosis rates, treatment mix, and procedure intensity could be adjusted to reflect how practices operate.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 53% |

| Mid tier: 55% | Functional/Unit leaders: 26% | EMEA: 29% |

| Smaller Players: 14% | Managers: 60% | Americas: 18% |

Market-Sizing & Forecasting

We sized the market using a top-down and bottom-up approach. The top-down view builds value from the treated animal pool and the care intensity seen in general practice and referral settings, then it is checked against selective supply-side signals. In practice, we start with animal population and visit behavior, then apply diagnosis and treatment rates for common eye conditions, and convert those into value using realistic price bands.

Inputs used in the model include the companion animal base and ownership trends, referral and specialty ophthalmology penetration, procedure and product mix by condition (such as cataract care, glaucoma management, and infectious eye treatment), average pricing for diagnostics and interventions, and the share of cases handled in clinics versus specialty hospitals. Where detailed country-level data is limited, we use regional analogs and adjust for differences in veterinary access, affordability, and care standards. These adjustments were validated through interviews.

Forecasts are built using scenario analysis anchored to expected changes in pet spending, specialty capacity, and adoption of newer diagnostics and therapies, then refined using interview consensus on how quickly practice patterns are shifting. We review the outputs to keep growth consistent with underlying demand signals, rather than letting results hinge on one aggressive assumption.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent checks, and we run variance reviews at the country and regional level so unusual jumps in volume or pricing get flagged early. When an outlier appears, analysts revisit underlying inputs, re-check source notes, and re-contact relevant respondents to confirm whether the shift is real.

A multi-step review is followed before sign-off, including a second-analyst pass on calculation accuracy and logic consistency across regions and care settings. Reports are refreshed annually, and interim updates are made when major events can shift demand, pricing, or care delivery. Before delivery, a final update pass is completed so clients receive the most current view available at publication time.

Mordor Intelligence's Veterinary Eye Care Market Estimate Compared With Other Published Estimates

Published estimates for veterinary eye care can look far apart because the counted spend is not always the same, and the starting demand signal can differ. Even when the same year is quoted, currency timing, inflation handling, and whether services are included can move the value materially.

By tracking treated case volumes, care-setting mix, and average price progression, Mordor Intelligence keeps the veterinary eye care total tied to products plus clinical services, instead of narrowing the model only to ophthalmic equipment shipments or a single therapy bucket.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.65 B (2026) | |

| Trade Journal A | USD 0.49 B (2024) | This estimate is scoped to veterinary ophthalmology equipment, which leaves out recurring service revenue and drug-based treatments used in day-to-day eye care. |

| Industry Publisher B | USD 0.12 B (2024) | This estimate appears to cover a narrower eye care subset with lighter service capture, and it can swing based on small-sample pricing assumptions and uneven country coverage. |

The table shows that scope selection, especially whether services are counted alongside products, is usually the largest reason for the spread. When the included spend categories, geography coverage, and pricing logic are kept consistent, the market size can be traced back to clear demand and utilization drivers and repeated in future refreshes.

Key Questions Answered in the Report

What is the projected value of the Veterinary Eye Care market by 2031?

The market is forecast to reach USD 11.32 billion by 2031 at a 5.53% CAGR.

Which product category holds the largest share today?

Ophthalmic drugs and related products accounted for 75.55% of 2025 revenue.

Which animal group is growing fastest in eye-care spending

Horses are expected to post a 6.75% CAGR through 2031, fueled by treatments for recurrent uveitis.

Why are clinics adopting rebound tonometers?

The devices let general practitioners detect glaucoma quickly, reducing referrals and expanding in-house care.

How does the shortage of specialists affect market growth?

Limited ophthalmologist availability increases wait times and drives investment in tele-ophthalmology and simplified surgical equipment.

What regulatory change most affects new ophthalmic drugs?

FDA guidance issued in 2024 requires injectable-grade sterility for all liquid formulations, raising development costs.

Page last updated on: