Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

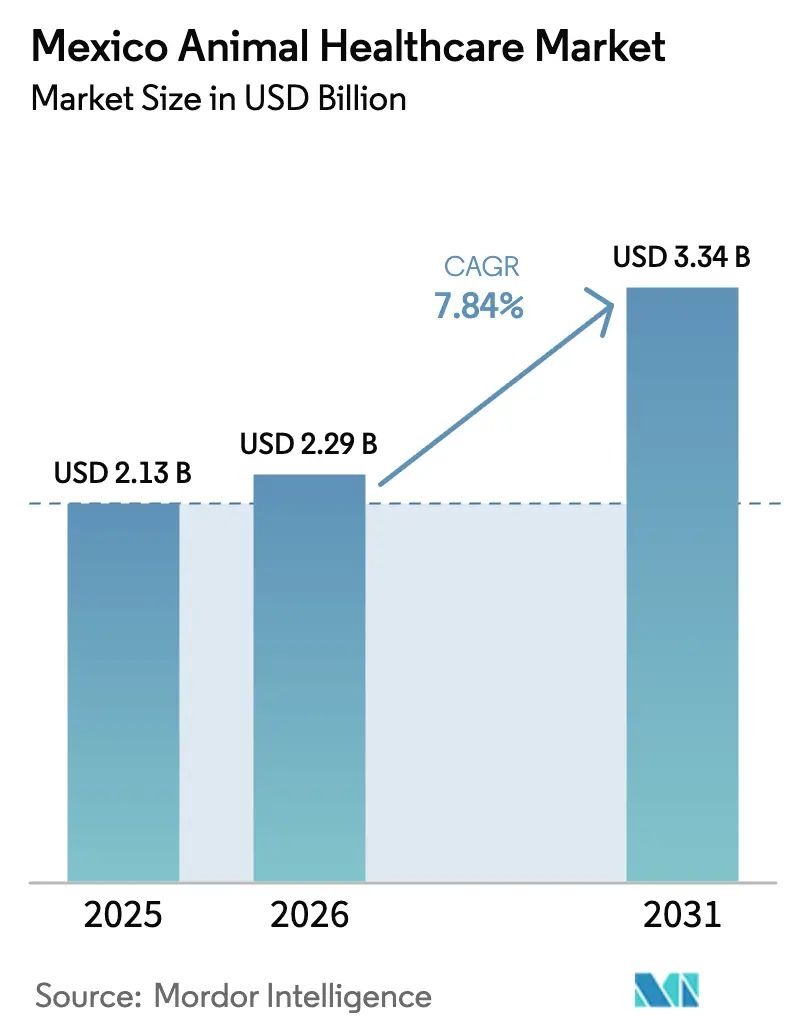

| Base Year Market Size (2025) | USD 2.13 Billion |

| Market Size (2026) | USD 2.29 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 7.84% CAGR |

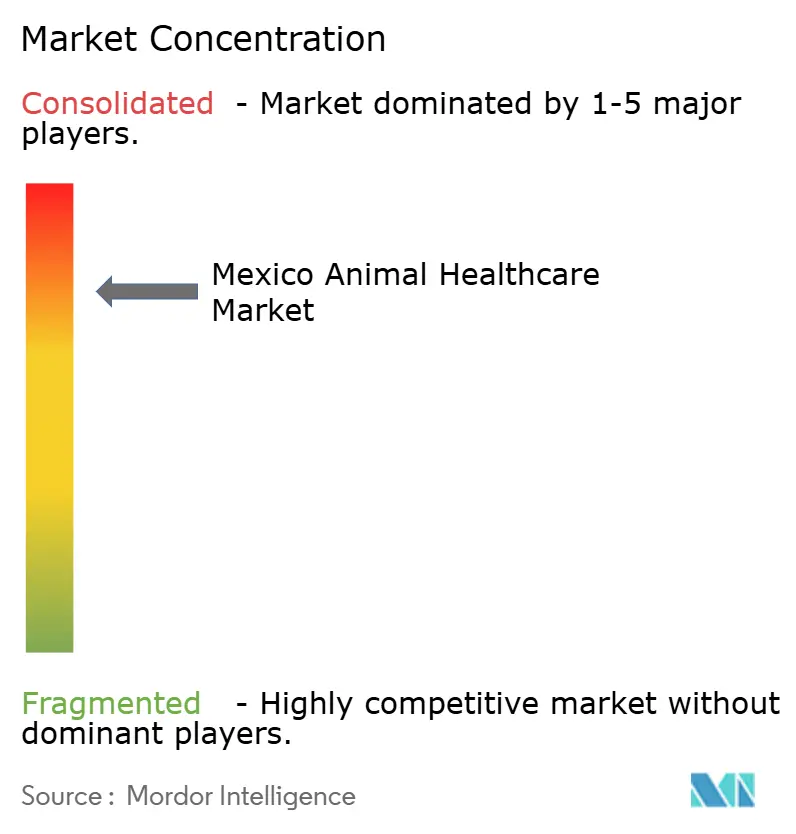

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Animal Healthcare Market Analysis by Mordor Intelligence

The Mexico Animal Healthcare Market size is expected to increase from USD 2.13 billion in 2025 to USD 2.29 billion in 2026 and reach USD 3.34 billion by 2031, growing at a CAGR of 7.84% over 2026-2031.

Strong livestock fundamentals, widening companion-animal ownership, and targeted government biosecurity programs underpin this advance. Structural advantages include Mexico’s status as the world’s fifth-largest cattle producer, a modernizing poultry industry, and improving access to innovative therapeutics and diagnostics. Competitive intensity has increased since the 2024–2025 screwworm crisis, prompting substantial public-private investments in sterile fly production and driving demand for advanced pest-control products. Cross-border trade remains a double-edged factor, with exports of live cattle and animal protein bolstering revenue. Yet, temporary disease-related suspensions highlight the importance of resilient surveillance systems and digital veterinary platforms.

Key Report Takeaways

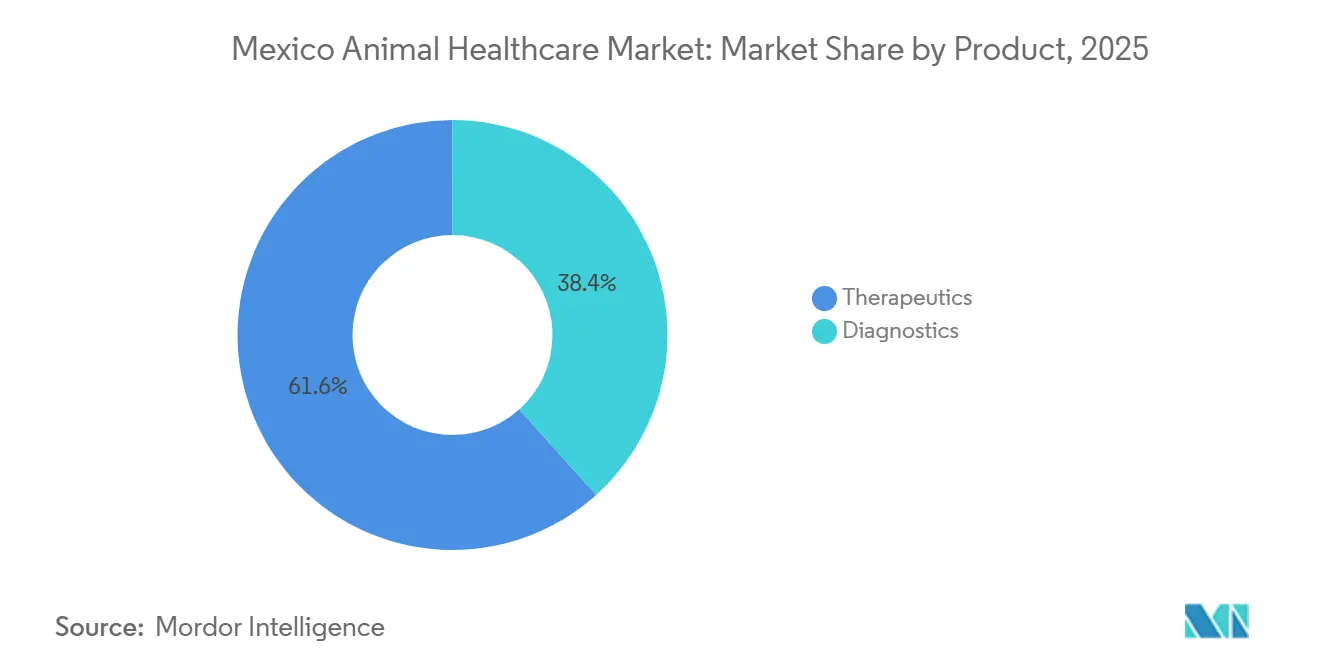

- By product category, therapeutics captured 61.65% of the Mexico animal healthcare market share in 2025, while diagnostics is projected to expand at a 8.81% CAGR through 2031.

- By animal type, dogs and cats accounted for 48.43% share of the Mexico animal healthcare market size in 2025; poultry is advancing at a 8.76% CAGR through 2031.

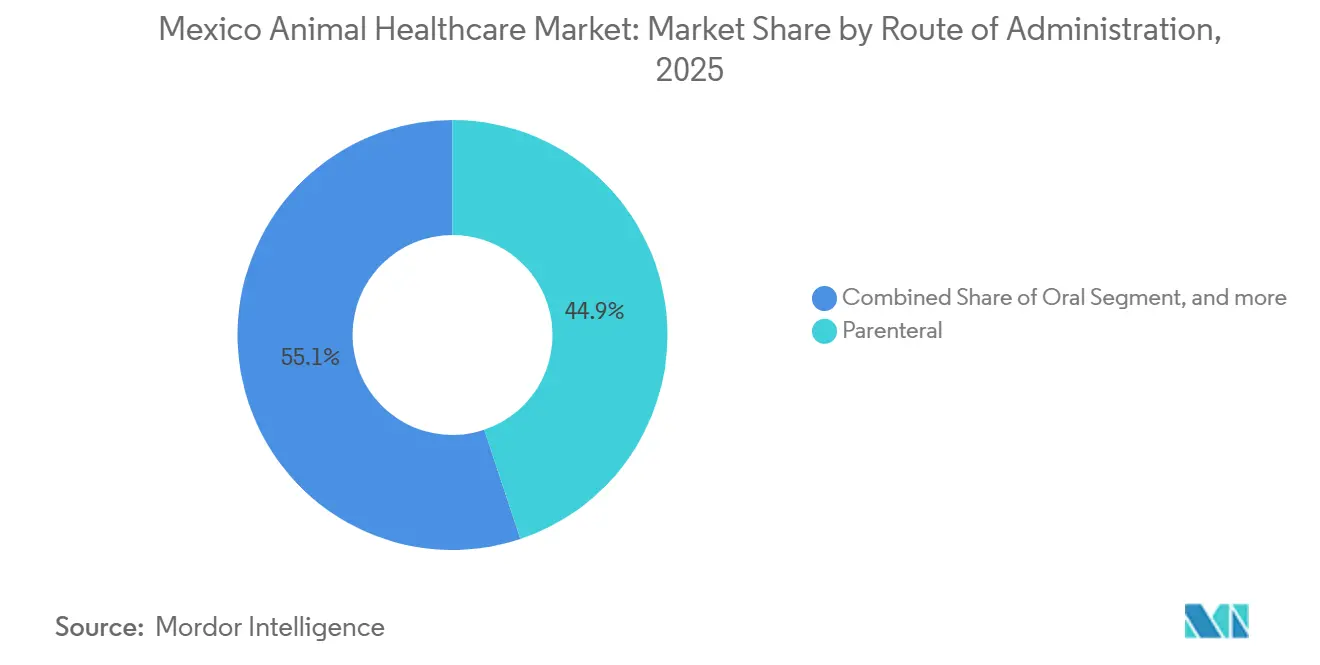

- By route of administration, parenteral products led with 44.87% share in 2025, whereas oral formulations are forecast to grow at a 8.42% CAGR to 2031.

- By end user, veterinary hospitals and clinics held 60.43% share of the Mexico animal healthcare market size in 2025; point-of-care settings are recording the highest projected CAGR at 8.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Animal Healthcare Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising companion animal expenditure | +2.1% | Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Expansion of livestock industry and protein demand | +1.8% | Veracruz, Jalisco, San Luis Potosí | Long term (≥4 years) |

| Technological innovation in diagnostics and therapeutics | +1.5% | Urban centers expanding to rural areas | Medium term (2-4 years) |

| Government support for animal-health programs | +1.2% | National focus, emphasis on southern border states | Short term (≤2 years) |

| Growing penetration of pet-insurance solutions | +0.9% | Urban Mexico, moving into secondary cities | Medium term (2-4 years) |

| Digital transformation of veterinary services | +0.4% | Metropolitan areas; pilot livestock regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Expenditure

Urban pet ownership continues to reshape the Mexico animal healthcare market, with dogs and cats commanding nearly half of total demand. In June 2025, the Similares pharmacy chain launched Simi Pet Care, signaling retail recognition of companion-animal potential and extending low-cost veterinary medicines to price-sensitive consumers. Preventive visits, premium nutrition, and specialty treatments are increasingly common, supported by 2024 legislation that created free public veterinary clinics to raise the baseline standard of care. Together, private and public channels are broadening service coverage, spurring demand for diagnostics and vaccines, and building customer expectations for quality across the Mexico animal healthcare market.

Expansion of Livestock Industry and Animal Protein Demand

Livestock production generates more than 565 billion pesos annually and employs over 828,000 people, ensuring steady therapeutic consumption for cattle, swine, and poultry[1]Servicio Nacional de Sanidad, Inocuidad y Calidad Agroalimentaria, “Sector Pecuario Genera 565 Mil Millones de Pesos,” gob.mx/senasica. Sector investment pledges of 105 billion pesos focus on plant upgrades and sustainability, while the July 2025 methane-reduction strategy requires specialized veterinary input on feed additives and genetics. Maintaining monthly cattle-export revenue of USD 25–30 million hinges on stringent surveillance, traceability, and certification—areas that continually enlarge the addressable base for the Mexico animal healthcare market.

Technological Innovation in Veterinary Diagnostics and Therapeutics

Artificial-intelligence tools for behavior scoring and body-condition monitoring, already common in major dairies, are diffusing to midsize producers and companion-animal clinics[2]PubMed Central, “AI-Enabled Health Monitoring in Latin American Livestock,” ncbi.nlm.nih.gov. Precision technologies shorten response times, support antimicrobial-stewardship goals, and underpin the rapid growth of point-of-care testing. Mexico’s large-scale sterile-insect program exemplifies its readiness to deploy biotech solutions, with 885 million sterile flies released since November 2024 to curb screwworm spread.

Government Support for Animal Health and Biosecurity Programs

SENASICA’s emergency spending after the screwworm outbreak funded inspections, mobile labs, and cross-border coordination. The August 2025 bilateral action plan with the United States secures ongoing financing for sterile-fly capacity, while Plan Mexico incentives bolster local drug manufacturing. COFEPRIS process reforms raised 2024 medical-device approvals by 26.22%, accelerating access for novel diagnostics that enrich the Mexico animal healthcare market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Veterinary Care And Products | -1.4% | National, most acute in rural and low-income urban districts | Medium term (2-4 years) |

| Limited Veterinary Infrastructure In Rural Areas | -1.1% | Southern states and remote livestock-dense regions | Long term (≥4 years) |

| Prevalence Of Counterfeit And Illegal Veterinary Medicines | -0.8% | National, with higher incidence in informal rural markets and online channels | Short term (≤2 years) |

| Regulatory Complexity And Approval Delays For New Products | -0.6% | National, affecting small and mid-size manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Veterinary Care and Products

Price sensitivity limits uptake of premium pharmaceuticals outside major metros. SENASICA’s February 2025 counterfeit-drug alert underscored risks when producers turn to unregulated channels. Currency swings elevate import costs for advanced biologics, while compliance fees keep legitimate prices high. Low-cost retail clinics and free public services soften the constraint but also compress margins for full-service hospitals in the Mexico animal healthcare market.

Limited Veterinary Infrastructure in Rural Areas

Veterinary density skews heavily toward cities, leaving gaps in regions with the highest livestock densities. Budget limits at SENASICA restrict the frequency of on-farm inspections, prompting partnerships with producer groups and foreign agencies. Mobile units and telehealth pilots show promise yet require broadband investments and training to translate into broad rural coverage, tempering growth for the Mexico animal healthcare market over the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutics Dominance Meets Diagnostic Innovation

Therapeutics commanded 61.65% of the Mexico animal healthcare market share in 2025, reflecting entrenched treatment-oriented practices across livestock and companion-animal segments. Demand spikes following the screwworm outbreak sustained high volumes for parasiticides, wound treatments, and antibiotics. Agrovet Market’s February 2025 launch of Opticlox for bovine eye infections illustrates continuing formulation upgrades aimed at high-value cattle.

Recent shifts toward surveillance and export compliance are expanding diagnostics faster than any other category at a 8.81% CAGR, underpinning an incremental lift in the Mexico animal healthcare market size. Point-of-care test kits provide immediate, actionable results for ranchers facing tight shipment windows, while immunoassays and molecular panels gain currency in urban clinics catering to preventive-care minded pet owners. Modalities such as digital radiography are also moving into secondary cities, narrowing the historical gap with human healthcare standards.

By Animal Type: Companion Animals Lead While Poultry Accelerates

Urban dogs and cats represent 48.43% of volume and value demand, riding a wave of humanization that fuels specialty diets, vaccinations, and dental care. Insurance uptake and retail clinic chains both amplify expenditure depth within the companion cohort. Alongside, poultry health needs are expanding more rapidly than any other animal type, growing at a 8.76% CAGR as integrated producers tighten biosecurity after 2024 avian-influenza scares.

Beef and dairy cattle remain cornerstone users of reproductive hormones and mastitis-control drugs, leveraging Mexico’s fifth-place global herd ranking to secure export premiums. Swine and equine segments contribute stable baseline volumes, whereas aquaculture therapeutics hint at emerging niches that could widen the Mexico animal healthcare market size over the next decade.

By Route of Administration: Parenteral Preference Shifts Toward Oral Convenience

Parenteral formulations retained 44.87% share in 2025 due to precision-dose requirements in vaccination programs and emergency therapeutic interventions across intensive feedlots. Injectable oxytetracycline, antiparasitics, and reproductive hormones stay routine for veterinarians focused on compliance and efficacy.

Labor pressures and animal-handling constraints are steering producers toward palatable boluses and chewable tablets that underpin the 8.42% CAGR forecast for oral products through 2031. Sustained-release coatings lessen labor visits and stress, proving attractive for backyard poultry and companion-animal owners alike. Topicals remain indispensable for ectoparasite control, especially in the wake of screwworm, while intramammary tubes continue as specialized staples in the dairy sector of the Mexico animal healthcare market.

By End User: Clinical Settings Dominate While Point-of-Care Surges

Veterinary hospitals and clinics delivered 60.43% of 2025 revenue, anchored by surgery suites, imaging, and multi-disciplinary care clustered in metropolitan areas. Their role as referral centers ensures continuing demand for high-margin biologics and advanced diagnostics.

Decentralized models are scaling faster, with point-of-care environments anticipated to expand at an 8.54% CAGR as portable sensors and rapid tests proliferate. Livestock operators value on-the-spot diagnoses that avert shipment delays, while pet owners appreciate convenience and cost transparency. Reference labs sustain growth on the back of antimicrobial-resistance tracking, whereas academic institutions focus research on endemic challenges such as brucellosis that influence export eligibility for the Mexico animal healthcare market.

Competitive Landscape

The Mexico animal healthcare market is highly concentrated. Multinationals including Zoetis, Boehringer Ingelheim, and Elanco leverage global R&D pipelines and extensive distributor networks to keep leadership positions. Local producers like Laboratorios Tornel and Avimex differentiate through price and regional-disease focus.

Competitive tension rose sharply during the screwworm emergency, as companies capable of supplying larvicides and wound dressings experienced demand spikes. Similares’ June 2025 rollout of Simi Pet Care injected low-price pressure into the companion-animal segment, compelling independent clinics to pivot toward specialized or premium services. Digital platforms are emerging as strategic differentiators, enabling smaller players to overcome distribution constraints and reach underserved geographies with teleconsultations and e-commerce drug sales.

Strategic collaborations between foreign innovators and domestic distributors remain common, driven by COFEPRIS’ streamlined approval timelines that still benefit from experienced local guidance. Technology-oriented start-ups focusing on sensor-based herd monitoring or AI-powered imaging are attracting venture funding, signaling a shift toward data-heavy solutions in the Mexico animal healthcare industry.

Mexico Animal Healthcare Industry Leaders

Zoetis Inc.

Ceva Santé Animale

Merck Animal Health

Elanco Animal Health

Boehringer Ingelheim Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mexico launched a pilot rabies vaccination program in five states—Michoacan, Oaxaca, Nayarit, Durango, and Jalisco—using intradermal doses to address wild animal rabies risks. The initiative coincided with World Zoonoses Day and aims to protect populations exposed to wild animals.

- May 2025: Farmacias Similares launched Simi Pet Care clinics, marking its entry into Mexico’s growing veterinary market. This move aims to capitalize on the increasing popularity of pet ownership and the rising demand for veterinary services. The sector's expansion reflects a heightened focus on animal welfare and regulatory developments in the country.

- September 2024: Mexico City's Ministry of Health, via its Public Health Services, unveiled a reinforcement campaign for rabies vaccinations in canines and felines. The initiative aims to administer 405,902 doses to dogs and cats across the capital's 16 municipalities.

- September 2024: Martí Batres, one of the leading the Mexico City Government, inaugurated the "Michigan, City of Cats" animal shelter. This new facility will be situated within the Animal Surveillance Brigade, part of the capital's Citizen Security Secretariat.

Mexico Animal Healthcare Market Report Scope

As per the scope of the report, the Mexican animal healthcare market comprises therapeutic and diagnostic products and solutions for companion and farm animals. Companion animals can be tamed or adopted for companionship, while farm animals are raised for meat and milk-related products. Companion animals include dogs, cats, and horses. Farm animals include bovine, poultry, and porcine.

The Mexico Animal Healthcare Market Report is Segmented by Product (Therapeutics [Vaccines, Parasiticides, Anti-Infectives, Medical Feed Additives, and Other Therapeutics], Diagnostics [Immunodiagnostic Tests, Molecular Diagnostics, Diagnostic Imaging, Clinical Chemistry, and Other Diagnostics]), Animal Type (Dogs & Cats, Horses, Ruminants, Swine, Poultry, and Other Animal Types), Route of Administration (Oral, Parenteral, Topical, and Other Route of Administrations), and End User (Veterinary Hospitals & Clinics, Reference Laboratories, Point-Of-Care/In-House Testing Settings, and Academic & Research Institutes). The report offers the value (in USD million) for the above segments.

By Product

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-Infectives | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Clinical Chemistry | |

| Other Diagnostics |

By Animal Type

| Dogs & Cats |

| Horses |

| Ruminants |

| Swine |

| Poultry |

| Other Animal Types |

By Route Of Administration

| Oral |

| Parenteral |

| Topical |

| Other Route of Administrations |

By End User

| Veterinary Hospitals & Clinics |

| Reference Laboratories |

| Point-Of-Care / In-House Testing Settings |

| Academic & Research Institutes |

| By Product | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-Infectives | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Clinical Chemistry | ||

| Other Diagnostics | ||

| By Animal Type | Dogs & Cats | |

| Horses | ||

| Ruminants | ||

| Swine | ||

| Poultry | ||

| Other Animal Types | ||

| By Route Of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Other Route of Administrations | ||

| By End User | Veterinary Hospitals & Clinics | |

| Reference Laboratories | ||

| Point-Of-Care / In-House Testing Settings | ||

| Academic & Research Institutes | ||

Key Questions Answered in the Report

How large is the Mexico veterinary healthcare market in 2026?

It is valued at USD 2.29 billion and is projected to reach USD 3.34 billion by 2031, reflecting a 7.84% CAGR.

Which product group dominates animal-health spending in Mexico?

Therapeutics leads with 61.65% share, driven by routine vaccinations, antiparasitics, and anti-infectives.

Which animal category shows the fastest growth?

Poultry health expenditure is advancing at a 8.76% CAGR due to intensified biosecurity and protein-demand trends.

What is driving adoption of diagnostics in Mexican veterinary practice?

Export-compliance pressures, preventive-care preferences, and point-of-care rapid tests are fueling a 8.81% CAGR in diagnostics.

How is the screwworm outbreak influencing market dynamics?

It has accelerated investment in sterile-insect control, wound therapeutics, and cross-border surveillance technologies.

Which regions concentrate the highest veterinary spending?

Northern states dominate due to intensive livestock trade, while the central corridor is the fastest-growing companion-animal hub.

Page last updated on: