Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.92 Billion |

| Market Size (2026) | USD 17.98 Billion |

| Market Size (2031) | USD 24.4 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Veterinary Healthcare Market Analysis by Mordor Intelligence

The Europe veterinary healthcare market size is expected to grow from USD 16.92 billion in 2025 to USD 17.98 billion in 2026 and is forecast to reach USD 24.4 billion by 2031 at 6.29% CAGR over 2026-2031. This expansion is propelled by widespread pet humanization, regulatory reforms that accelerate product approvals, and strong corporate investment in clinical infrastructure. Rising disposable incomes support higher out-of-pocket spending on routine and advanced treatments, while digital platforms enhance practice efficiency and client engagement. Consolidation among hospital chains unlocks purchasing power for diagnostics and biologics, and successful commercialization of monoclonal antibodies signals a shift toward precision therapeutics. Simultaneously, livestock producers adopt biosafe vaccines to curb antimicrobial resistance, sustaining demand across farm-animal lines.

Key Report Takeaways

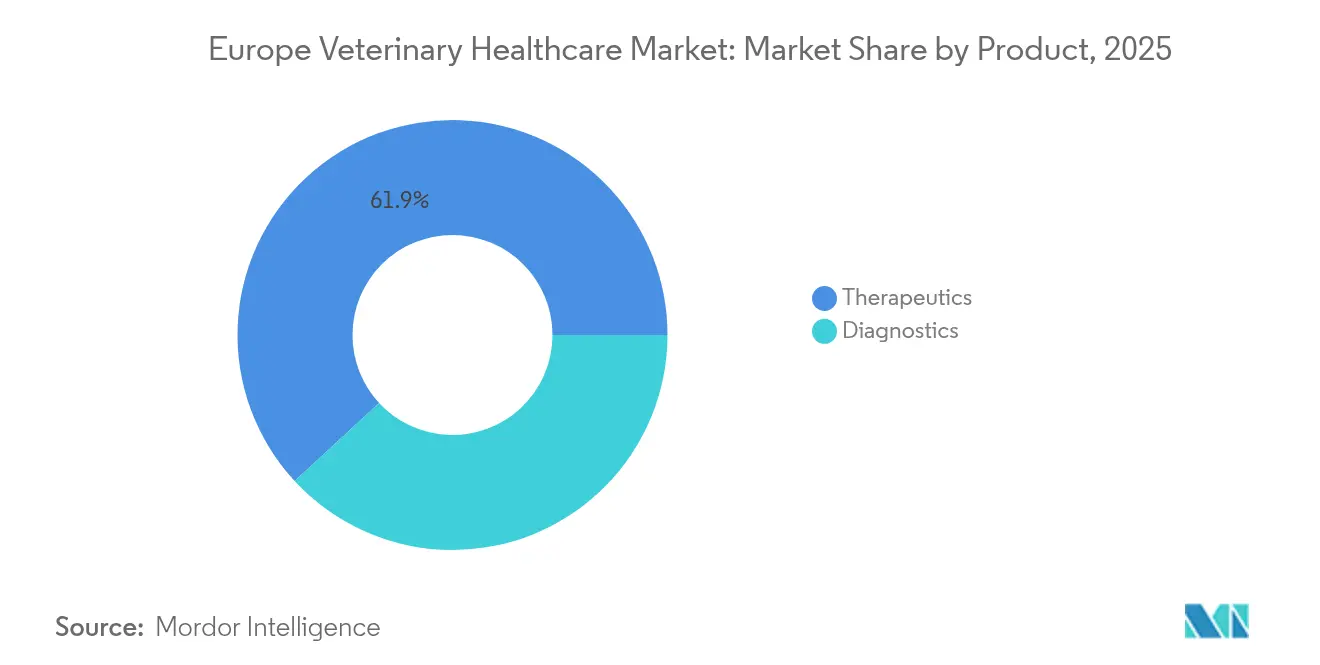

- By product, therapeutics led with 61.88% revenue share in 2025; diagnostics is advancing at a 7.18% CAGR through 2031.

- By animal type, companion animals captured 46.10% of Europe veterinary healthcare market share in 2025, while the poultry segment is forecast to expand at a 6.62% CAGR to 2031.

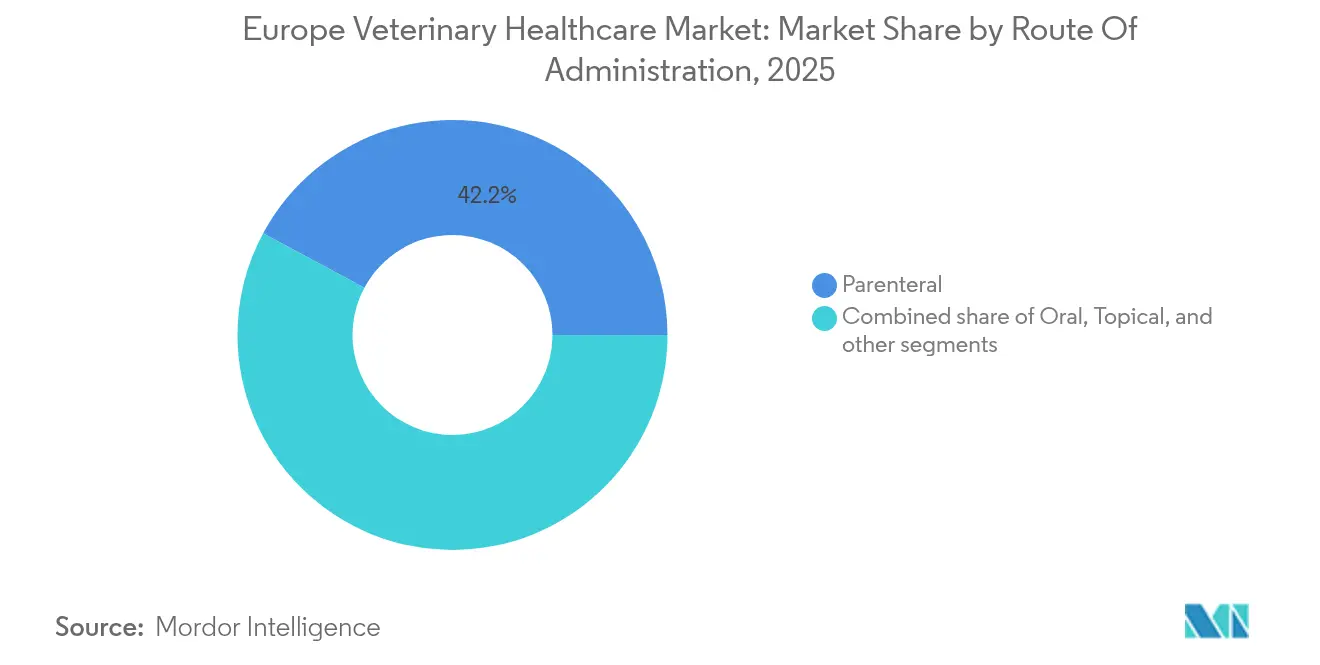

- By route of administration, parenteral products accounted for 42.15% of the Europe veterinary healthcare market size in 2025; oral formulations record the fastest growth at a 6.51% CAGR between 2026 and 2031.

- By end user, hospitals and clinics held 54.85% of the Europe veterinary healthcare market in 2025, whereas point-of-care settings are projected to rise at a 7.62% CAGR to 2031.

- By geography, Germanyheld 40.85% of the Europe veterinary healthcare market in 2025, whereas United Kingdom is projected to grow at a 7.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Veterinary Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising companion animal ownership | +1.8% | Germany, UK, France with spillover to Southern Europe | Medium term (2-4 years) |

| Growing government and institutional animal-welfare support | +1.2% | EU-wide, strongest in Nordic countries and Germany | Long term (≥ 4 years) |

| Continuous technological innovations in veterinary healthcare | +1.5% | Global, early adoption in UK, Germany, Netherlands | Short term (≤ 2 years) |

| Expanding pet-insurance penetration | +0.9% | Germany, Spain, UK; expanding in Italy and France | Medium term (2-4 years) |

| Increasing adoption of digital veterinary solutions | +0.7% | UK, Germany, Nordic countries with gradual European rollout | Short term (≤ 2 years) |

| Favorable European Union regulatory reforms | +0.6% | EU-wide with harmonized implementation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Ownership

More than 90 million European households keep pets, anchoring long-run demand for veterinary care. Germany tops the region, with pets in 45% of homes and accelerating insurance uptake that reduces treatment price sensitivity. Italy follows with a 60.2 million animal population, translating into robust preventive-care spending. Urban owners channel discretionary income toward wellness plans, premium foods, and chronic-disease management. Nordic nations illustrate the linkage between ownership and insurance: Sweden insured 83% of dogs and 69% of cats in 2023. As pets live longer, companion-animal healthcare needs diversify into oncology, endocrinology, and geriatric pain control.

Growing Government and Institutional Animal-Welfare Support

Regulation (EU) 2019/6 standardizes product approval procedures, restricts prophylactic antibiotics, and improves medicine traceability. The forthcoming welfare package, expected in 2026, extends oversight to transport and slaughter, driving greater vaccine and analgesic uptake. Public spending supports new university programs that address rural veterinary shortages, especially in Germany, Spain, and the UK. The European Medicines Agency 2025 Strategy prioritizes One-Health measures against antimicrobial resistance, spurring demand for non-antibiotic therapies. These policies collectively nurture a growth-oriented operating climate for manufacturers and service providers.

Continuous Technological Innovations in Veterinary Healthcare

Biotechnology delivers first-in-class monoclonal antibodies such as bedinvetmab for canine osteoarthritis, now commercial in over 25 countries. Point-of-care equipment leverages reagent-free spectroscopy, delivering 83-100% accuracy for feline leukocyte counts and shrinking diagnostic turnaround. Recent EMA approvals include nine novel vaccines, triple the 2022 tally, underscoring innovation velocity. Corporate R&D agendas increasingly target chronic conditions—diabetes, atopic dermatitis, osteoarthritis—previously managed off-label or via human drugs. Cloud-based imaging and AI-assisted pathology embed decision support directly into practice workflows, sharpening service differentiation.

Expanding Pet-Insurance Penetration

Pet-insurance premiums reached USD 887 million in Germany in 2022, part of a European market that accounts for two-fifths of global revenue. Accident-only products dominate but comprehensive plans grow fastest as owners seek coverage for preventive and chronic-care expenses that now compose over half of annual invoices. High penetration markets such as the UK stimulate adoption of MRI, CT, and targeted biologics that would otherwise be cost-prohibitive. Insurers collaborate with clinics on subscription wellness models that smooth cash flows and encourage compliance with vaccination and dental guidelines. Rising claim volumes necessitate price transparency and peer-benchmarking tools to curb inflation risk.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit veterinary products | −0.8% | Eastern Europe primary concern with spillover to Western markets | Medium term (2-4 years) |

| Escalating veterinary service costs | −1.2% | Nordic countries and UK most affected, spreading to Continental Europe | Short term (≤ 2 years) |

| Regulatory uncertainty post-Brexit | −0.5% | UK and Northern Ireland with EU trade implications | Short term (≤ 2 years) |

| Shortage of rural veterinary professionals | −0.7% | Rural areas across all European countries with varying intensity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Veterinary Service Costs

Median fees for common procedures rose 2–24% across Nordic markets between 2022 and 2023; corporate chains posted annual price hikes outpacing independents[1]Frontiers in Veterinary Science, “Veterinary Price Trends in Nordic Countries,” frontiersin.org. Spain illustrates the trend, with spend climbing from EUR 2.613 billion in 2022 to a projected EUR 3.800 billion in 2030 while a 21% VAT compounds consumer burden. Technology upgrades, higher wage expectations, and private-equity return targets fuel inflation. Price comparison portals such as Sweden’s Vetpris emerge but cannot offset the structural cost floor set by advanced equipment and biologics. Budget-constrained owners delay care, risking welfare setbacks and public-health repercussions.

Shortage of Rural Veterinary Professionals

Ageing practitioners retire faster than replacements arrive, leaving livestock regions underserved[2]Federation of Veterinarians of Europe, “Rural Veterinary Shortage Report,” fve.org. Governments deploy bursaries and mobile-clinic grants, yet student debt loads deter graduates from mixed practice. Telemedicine alleviates minor cases but cannot replace on-site large-animal interventions. Resultant delays in disease detection threaten food-chain security and inflate emergency-call costs, reinforcing urban-rural service disparities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutics Dominance Amid Diagnostic Innovation

Therapeutics represented 61.88% of Europe veterinary healthcare market share in 2025, anchored by vaccines, parasiticides, and anti-infectives. Europe veterinary healthcare market size for therapeutics grew steadily as corporates leveraged centralized buying to stock high-margin biologics. Vaccines such as VAXXITEK posted 15.2% expansion in early 2025, reflecting poultry producers’ heightened biosecurity protocols. Parasiticides remained resilient through flagship brands like NEXGARD, although antibiotic stewardship capped systemic-antibacterial volumes. Diagnostics, while smaller, register a 7.18% CAGR as clinics adopt AI-driven imaging and reagent-free hematology devices that compress lab timelines and lift compliance. Immunodiagnostic kits retain the largest slice, yet molecular assays and digital radiography accelerate fastest, propelled by insurance reimbursement and corporate back-office integrations.

Diagnostic momentum elevates practice profitability and improves case-outcome transparency, reinforcing client trust. EMA’s 2023 approval list, with nine new vaccines, signals sustained pipeline vitality that will sustain the Europe veterinary healthcare market long term. The line between therapy and diagnosis blurs as companion-animal monoclonal antibodies double as biomarkers, foreshadowing integrated care bundles. Product-life-cycle extensions through chewable formulations and combination parasiticide-vaccines create cross-selling opportunities within corporatized clinic networks.

By Animal Type: Companion Animals Drive Growth

Europe veterinary healthcare market size for dogs and cats equaled 46.10% of 2025 revenue, underpinned by expanding insurance, urban lifestyles, and longevity-linked morbidities. German households alone spent heavily on premium services, reinforcing the Europe veterinary healthcare market leadership of companion animals. Poultry edges ahead as fastest riser at 6.62% CAGR, mirroring the shift toward high-density, antibiotic-free production. Horses command niche but high-value consumption in equine cardiology and orthopedic interventions, particularly across France and Germany. Swine and ruminant segments adopt combination vaccines to satisfy regulatory curbs on metaphylaxis. Aquaculture emerges through DNA-based salmon vaccines following MSD’s aqua acquisition, diversifying growth vectors.

The companion sector benefits from human-grade facility investments that mirror small-animal ICU standards. Cross-species product transfers accelerate pipeline efficiency, evidenced by feline diabetes solutions adapted from human endocrinology. Livestock categories confront margin compression from producer consolidation and retail price pressure, steering demand toward cost-effective broad-spectrum biologics and nutraceuticals.

By Route of Administration: Parenteral Leadership Faces Oral Growth

Parenteral formats comprised 42.15% of Europe veterinary healthcare market in 2025, owing to their indispensability for mass vaccination and rapid therapeutic onset. Nonetheless, owner preference and advances in taste-masking elevate oral dosage forms at a 6.51% CAGR. Subcutaneous injections of antibodies like Librela gain favor for monthly arthritis relief, while SENVELGO illustrates oral-route innovation for feline diabetes. Topical spot-ons sustain parasite-control leadership in outdoor cats and dogs, complemented by collars with extended-release technology. Livestock segments continue to favor injectables for herd-level immunization efficiency, yet aquaculture pioneers immersion and in-feed vaccine strategies to minimize stress.

Oral-route gains hinge on dosing compliance and reduced administration anxiety—critical where pet-owner demographics skew toward first-time adopters. Parenteral dominance will hold in critical-care and production-animal realms, but formulators prioritize dual-pathway pipelines to capture shifting consumer expectations within the Europe veterinary healthcare market.

By End User: Hospitals Lead While Point-of-Care Accelerates

Hospitals and clinics generated 54.85% of Europe veterinary healthcare market revenue in 2025, buoyed by many-site corporates that negotiate volume discounts and roll out standardized care pathways. Point-of-care sites, encompassing mobile practices and in-house testing stations, grow at 7.62% CAGR, fortified by compact analyzers and smartphone imaging. Reference laboratories retain complex cytology and genomics workups, while academic institutes sustain translational research that feeds commercial pipelines.

Corporate groups like IVC Evidensia funnel capital toward MRI suites, oncology wings, and 24/7 emergency facilities, setting service benchmarks that independents emulate. Mobile clinicians deploy cloud-based records and portable sonography to capture rural demand where fixed clinics are sparse. Hospitals’ scale enables clinical trials for blockbuster therapies, granting early adopter advantage and further anchoring their Europe veterinary healthcare market role.

Geography Analysis

Germany’s Europe veterinary healthcare market share eclipsed 40.85% in 2025. Strong insurance adoption and a robust regulatory regime underpin sustained spending on preventive vaccines and chronic-care biologics. Domestic champions like Boehringer Ingelheim supply innovation pipelines, anchoring pharma R&D clusters. High urbanization fuels demand for advanced imaging and dental suites, yet a widening rural skills gap hampers livestock service reach.

The United Kingdom remains a growth engine despite Brexit-related medicine-supply uncertainty. Corporate acquisitions, exemplified by Mars Petcare’s Linnaeus purchase, intensify competition and broaden 24-hour specialty coverage. The 2024 Veterinary Medicines Regulations simplify domestic approvals and limit antibiotic prophylaxis, aligning with EU practices but requiring dual reporting for cross-border products. Northern Ireland’s potential supply cliff in late 2025 clouds medium-term forecasting, although contingency warehousing and mutual-recognition negotiations aim to avert shortages.

France and Italy contribute material upside based on large pet populations and private-equity funded clinic roll-ups. Italy’s Animalia network surpasses 75 sites, channeling capital into CT scanners and endoscopy, while French start-ups pilot AI decision support for calf health. Spain posts rapid expenditure growth but contends with 21% VAT and ongoing price-transparency debates. Nordic nations exhibit near-saturation insurance levels that buffer owners from rising tariffs and sustain high compliance with annual exams. Eastern Europe lags in per-capita spend yet offers outsize growth potential as EU alignment introduces stringent pharmacovigilance and animal-welfare statutes.

Regulatory Landscape

Veterinary medicinal products in the EU are governed under Regulation (EU) 2019/6, with oversight handled by the European Medicines Agency (EMA) and its Committee for Medicinal Products for Veterinary Use (CVMP). The regime emphasizes pharmacovigilance, product availability, and antimicrobial stewardship. EMA monitoring is supported by tools such as the Antimicrobial Sales and Use (ASU) Platform, which supports One Health policy execution across EU and EEA markets.

A key compliance inflection point is on 16 July 2026, when the veterinary-specific Good Manufacturing Practice framework introduced via Implementing Regulations (EU) 2025/2091 and 2025/2154 becomes fully applicable across Member States. This increases execution requirements for manufacturers and marketing authorization holders, including formalized quality agreements and veterinary-tailored GMP expectations. Alongside this, Implementing Regulation (EU) 2026/857, published 16 April 2026 and applicable from 16 July 2026, sets rules for retention of samples for veterinary medicinal products repackaged for parallel trade, tightening traceability and post-market controls for cross-border supply flows. CVMPs 2026 work plan also continues to prioritize innovative veterinary medicinal products and new technologies under the networks strategy to 2028.

Competitive Landscape

Europe veterinary healthcare market competition combines moderate concentration with rapid new-entrant innovation. Top corporates including IVC Evidensia, Mars Petcare, and CVS Group expand footprints via aggressive M&A, achieving purchasing leverage over suppliers. Boehringer Ingelheim invested EUR 5.8 billion in R&D and plans 20 additional launches by 2026, reinforcing its biologics edge. Zoetis drives biotechnology leadership through Librela rollouts and invests in feline antibody follow-ons. Vimian Group unveiled 111 products in 2023, spanning AI diagnostics and molecular allergy assays, signaling nimble specialist disruption.

Digital innovators target practice pain-points: automated triage, inventory management, and data analytics for pricing oversight. Reference-lab alliances enable independent clinics to access next-generation sequencing without capex outlays.

Supply-chain collaboration with insurers yields bundled wellness subscriptions that stabilize cash flows and lock in loyalty. Counterfeit mitigation alliances between manufacturers and e-commerce platforms enhance brand protection and product authenticity. Rural service gaps remain relatively uncontested, offering white-space for mobile mixed-animal ventures and tele-mentoring solutions.

Europe Veterinary Healthcare Industry Leaders

Ceva Santé Animale

ECO Animal Health Group PlC

Idexx Laboratories, Inc.

MSD Animal Health

Boehringer Ingelheim International GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven antimicrobial stewardship and pharmacovigilance requirements are creating clearer whitespace for non-antibiotic disease management across companion and production animals, especially where offerings can reduce antibiotic dependence while supporting outcomes. EMA infrastructure, including the Antimicrobial Sales and Use (ASU) Platform, combined with CVMP activity in 2026, including updated risk management plan templates for novel therapy veterinary medicinal products and targeted guideline updates, is raising expectations for evidence generation and lifecycle management.

Opportunities are also forming where diagnostics, genomics, and digital decision support converge inside clinics and across livestock production chains. For companion animals, diagnostic adoption is supported by product availability steps such as IDEXX making its Cancer Dx Panel available in the United Kingdom in 2026 for earlier detection of canine lymphoma, enabling more structured oncology pathways in hospital and clinic settings. In livestock, poultry vaccination and biosecurity investment continues to be a demand pool, illustrated by ECO Animal Health Group’s EU marketing authorization and 2026 launch actions for ECOVAXXIN MS in the EU, alongside European Commission-supported work on data-driven bioactive solutions, including European Innovation Council-supported AI-led approaches aimed at reducing antibiotic reliance.

Recent Industry Developments

- June 2026: ECO Animal Health Group PLC held an official launch event in Madrid for its ECOVAXXIN MS poultry vaccine following EU marketing authorisation. The rollout adds a new marketed vaccine option for Mycoplasma synoviae control in layers and breeders, supporting higher vaccination intensity as producers manage disease pressure under tighter antimicrobial stewardship.

- April 2026: IDEXX Laboratories, Inc. announced UK availability of the IDEXX Cancer Dx Panel for early detection of canine lymphoma. The launch broadens access to advanced oncology screening in a major European veterinary services market and supports higher-throughput, earlier-stage case finding within clinic-based diagnostics workflows.

- October 2024: Ceva Sante Animale inaugurated a new European logistics platform in Montpon-Menesterol, France, designed to serve more than 100 countries. The added logistics capacity supports supply continuity for vaccines and other animal health products moving through Europe, improving resilience against temperature-controlled distribution constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending in Europe on veterinary therapeutics and diagnostics used to prevent, detect, and treat diseases in companion animals and livestock, as purchased through veterinary clinics, hospitals, and related channels.

Scope exclusions: It excludes human healthcare and general pet services that do not involve veterinary diagnosis or treatment decisions.

Segmentation Overview

- By Product

- Therapeutics

- Vaccines

- Parasiticides

- Anti-Infectives

- Medical Feed Additives

- Other Therapeutics

- Diagnostics

- Immunodiagnostic Tests

- Molecular Diagnostics

- Diagnostic Imaging

- Clinical Chemistry

- Other Diagnostics

- Therapeutics

- By Animal Type

- Dogs & Cats

- Horses

- Ruminants

- Swine

- Poultry

- Other Animal Types

- By Route Of Administration

- Oral

- Parenteral

- Topical

- Other Route of Administrations

- By End User

- Veterinary Hospitals & Clinics

- Reference Laboratories

- Point-Of-Care / In-House Testing Settings

- Academic & Research Institutes

- Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a Europe demand view using public statistics and regulatory signals, then aligning it to how veterinary therapeutics and diagnostics are sold and used country by country. We relied on sources such as Eurostat for livestock and trade series, the European Medicines Agency for veterinary product and policy context, and national statistics offices for pet ownership and animal population indicators.

To keep inputs practical, we also reviewed sources such as peer reviewed veterinary journals for disease prevalence and treatment practices, association and federation websites that outline animal health priorities, and reputable press coverage for pricing and policy changes. Company annual reports and investor presentations helped sanity check revenue splits and Europe exposure. For consistency checks on reported sales trends, a paid subscription was used for company financials and news updates. The desk sources listed are illustrative only, since many other public and paid references were used to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary discussions were used to pressure test adoption, pricing movement, and channel mix across key European countries. We also confirmed what should be counted as therapeutics versus diagnostics inside real purchasing workflows. We spoke with a mix of manufacturers, distributors, and veterinary hospital and clinic leaders, plus lab and imaging focused stakeholders, so the assumptions from desk work could be corrected where local practice patterns differed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | |

| Mid tier: 47% | Functional/Unit leaders: 35% | |

| Smaller Players: 17% | Managers: 49% |

Market-Sizing & Forecasting

Sizing was built using a top-down structure where country level animal populations and care utilization indicators reconstruct the addressable treatment and testing pool. That pool is translated into value using observed pricing and product mix. We then cross checked totals with selective bottom-up approximations, mainly supplier revenue exposure to Europe, sampled price per dose or test, and volume proxies shared by channel participants. Where coverage was uneven by country, we adjusted for gaps to keep the totals consistent.

Inputs that materially shaped the model included companion animal and livestock population trends, vaccination and parasite control seasonality, antimicrobial stewardship actions that shift therapy choices, diagnostic testing intensity in clinics and labs, and average selling price movement by product type. Forecasting used scenario analysis anchored to expected animal population shifts, clinic visit frequency, and pricing progression. The ranges were then narrowed using what primary respondents indicated as realistic uptake and budget behavior over the next few years.

Data Validation & Update Cycle

Outputs were checked against independent signals such as regulatory approvals, trade movements for relevant product categories, and observable changes in clinic and lab activity. We then reviewed results for outliers at the country and product level. When a variance could not be explained by a documented driver, we revisited the assumption. If needed, respondents were re-contacted to confirm whether it reflected a one-off event or a structural shift.

A multi step internal review is completed before sign-off so the numbers and the story align, and the model math remains traceable. Reports are refreshed annually, with interim updates when material events occur, followed by a final pre-delivery check so clients receive the latest view.

Mordor Intelligence's Europe Veterinary Healthcare Market Market Size Compared With Other Published Estimates

Published market sizes for Europe veterinary healthcare can look far apart because the included product set, the year used, and even the currency timing are not always treated consistently. Differences also come from how firms convert animal health activity into revenue, since utilization and pricing assumptions move totals quickly.

Some estimates describe a narrower Europe opportunity that reads closer to medicines only, and diagnostics may be treated as an optional add-on. In Mordor Intelligence, the total is built by counting both therapeutics and diagnostics across major European countries, then validating the split with clinic and lab purchase patterns before forecasting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 24.40 B (2031) | |

| Industry Publisher A | USD 2.20 B (2025) | Uses a much narrower reported total that appears closer to selected medicine categories, and its unit presentation in millions and longer forecast window can mask scope and currency timing differences. |

| Market Publisher B | USD 10.96 B (2025) | Frames the market as veterinary medicine and may not fully capture diagnostics value, and it relies more on product category rollups without the same level of country level utilization checks. |

The spread in values is mostly explained by what is counted, especially diagnostics inclusion, and by which year is quoted as the headline number. Once scope is aligned and assumptions are tied back to animal populations, clinic activity, and price progression, the estimate becomes easier to replicate and defend in planning discussions.

Key Questions Answered in the Report

What is the projected value of the Europe veterinary healthcare market by 2031?

It is valued at USD 24.4 billion, with a 6.29% CAGR projected over 2026-2031.

Which product category is expanding fastest?

Diagnostics registers the highest growth at a 7.18% CAGR, outpacing therapeutics.

Why is poultry health spending rising quickly?

Sustained avian influenza surveillance and tighter biosecurity rules push poultry segment growth at 6.62% CAGR.

What is driving the shift toward point-of-care testing in clinics?

Compact analyzers deliver lab-quality results in minutes, improving treatment speed and client satisfaction while generating recurring consumables revenue.

How is consolidation affecting vet service pricing?

Corporate practice ownership near 60% draws CMA scrutiny as fees rise, creating calls for greater transparency.

Page last updated on: