Veterinary Cardiology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

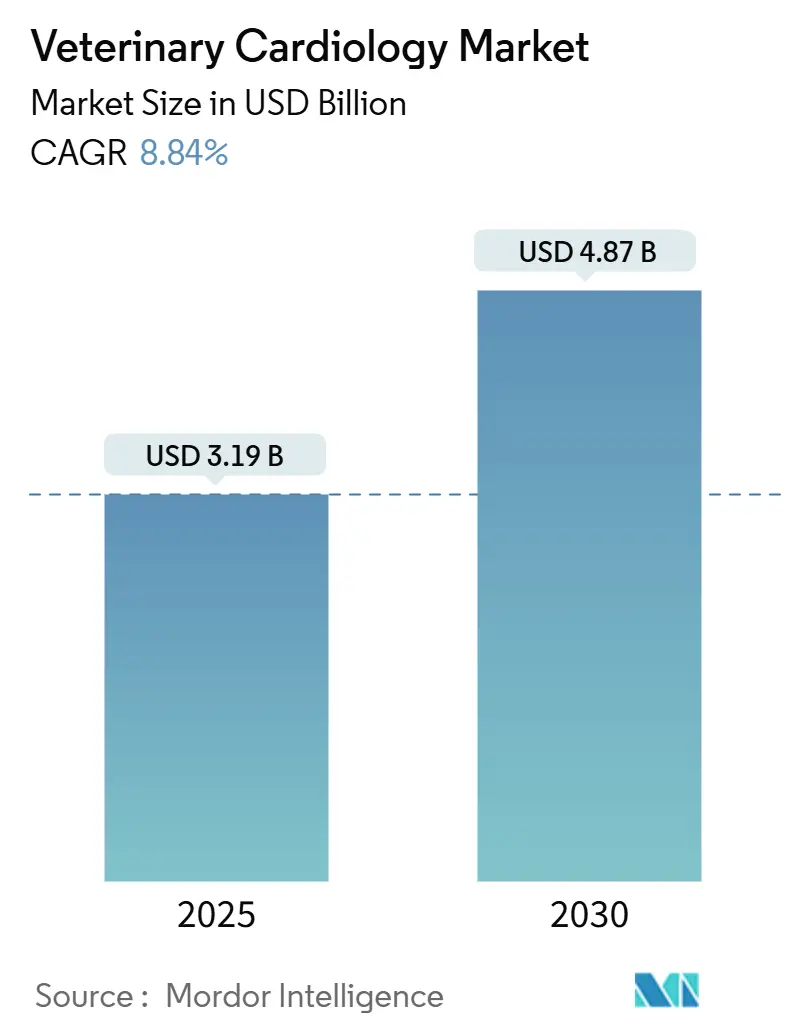

| Market Size (2025) | USD 3.19 Billion |

| Market Size (2030) | USD 4.87 Billion |

| Growth Rate (2025 - 2030) | 8.84% CAGR |

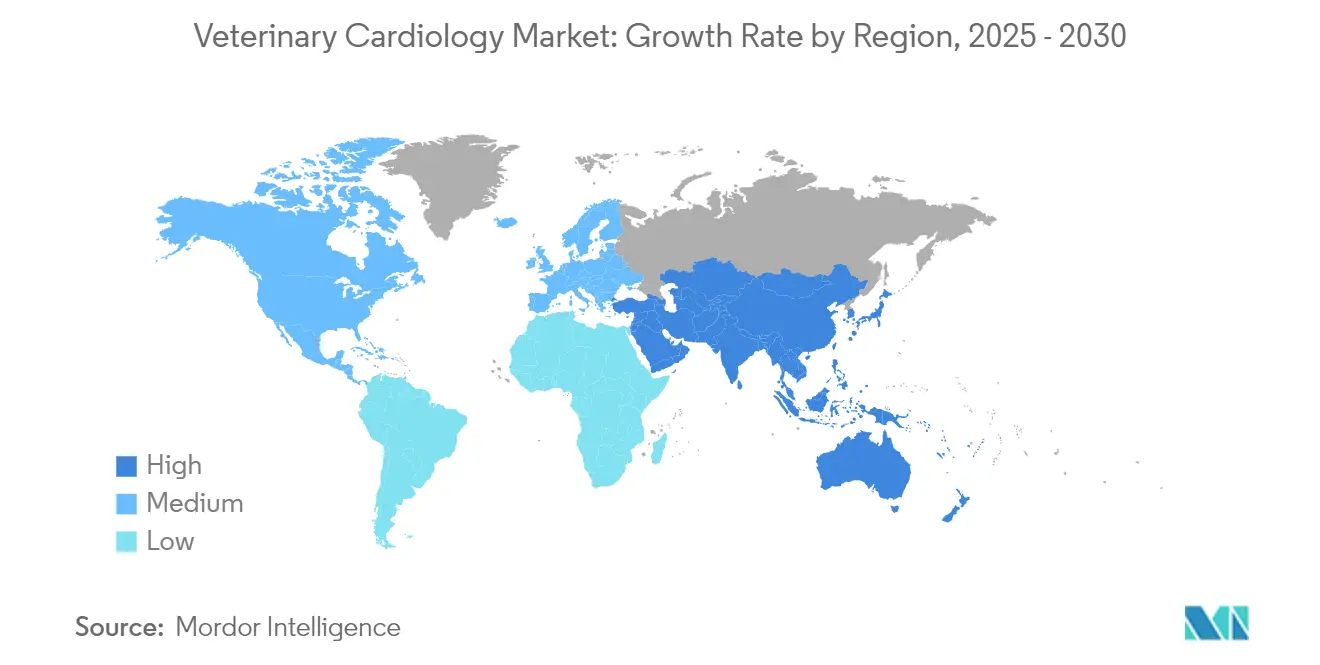

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Cardiology Market Analysis by Mordor Intelligence

The Veterinary Cardiology Market size is estimated at USD 3.19 billion in 2025, and is expected to reach USD 4.87 billion by 2030, at a CAGR of 8.84% during the forecast period (2025-2030).

Veterinary Cardiology Market Overview

The veterinary cardiology industry is experiencing significant transformation driven by increasing pet ownership and rising expenditure on animal healthcare. The North American pet insurance sector demonstrated remarkable growth, with a 21.9% increase in 2023, pushing the industry beyond the USD 4 billion milestone, per the North American Pet Health Insurance Association (NAPHIA). This surge in insurance coverage has enabled more pet owners to pursue advanced cardiac treatments for their animals. Expanding specialized veterinary facilities and clinics across major markets has created a robust infrastructure for delivering sophisticated cardiac care. Additionally, integrating digital health solutions and telemedicine platforms has enhanced access to veterinary cardiology services, particularly benefiting pet owners in remote areas.

Technological advancements have revolutionized diagnostic and treatment capabilities in veterinary cardiology. The successful implementation of minimally invasive surgical techniques, such as the groundbreaking mitral valve repair procedures, has significantly improved treatment outcomes. For instance, the University of Florida College of Veterinary Medicine's pioneering open-heart surgery program completed over 40 successful surgeries in its first year of operation during 2023-2024, according to the college’s published August 2024 article. Adopting advanced imaging technologies, including 3D echocardiography and cardiac MRI, has enhanced the precision of diagnosis and treatment planning. These innovations have particularly benefited the treatment of complex cardiac conditions that previously had limited therapeutic options.

The industry has significantly shifted towards preventive cardiac care and early intervention strategies. Veterinary practices are increasingly implementing comprehensive screening programs and regular cardiac health assessments. Integrating artificial intelligence (AI) and machine learning (ML) algorithms in diagnostic tools has enhanced the ability to identify cardiac abnormalities at earlier stages. Furthermore, developing specialized cardiac monitoring devices and wearable technology for pets has enabled continuous tracking of cardiac health parameters, allowing for more proactive management of cardiac conditions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Cardiology Market Trends and Insights

High Prevalence of Cardiac Disorders in Companion Animals

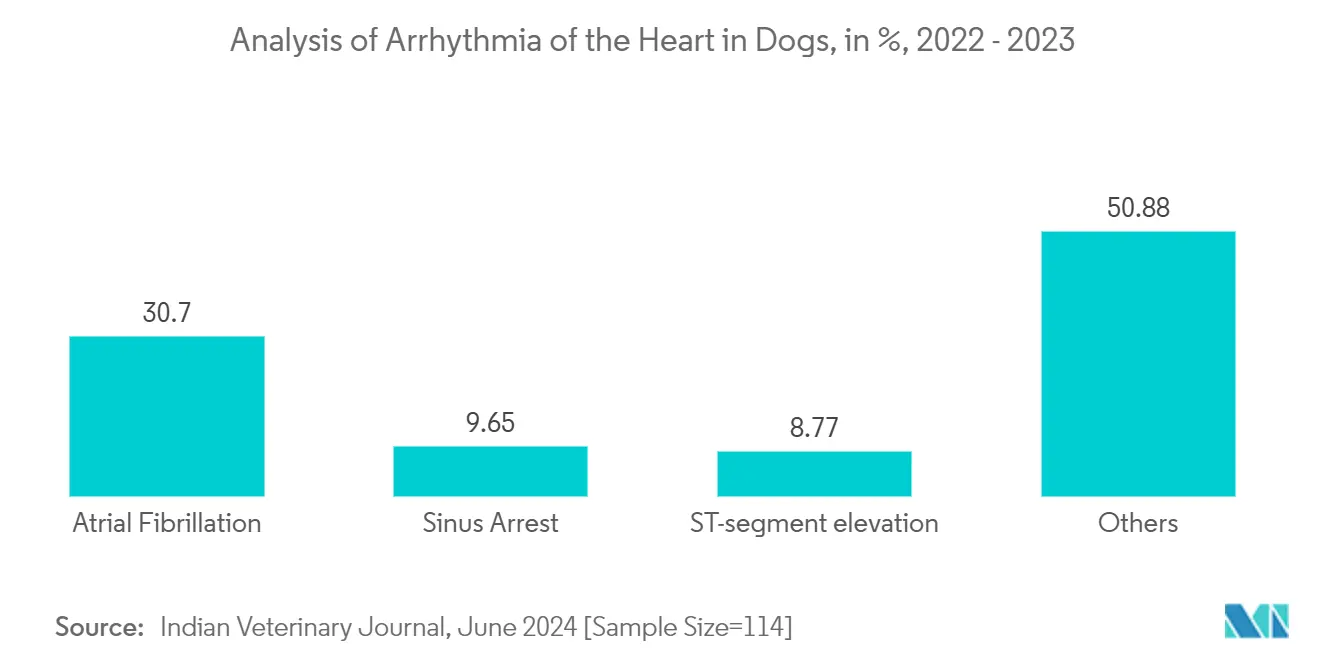

The increasing prevalence of cardiac disorders among companion animals, particularly dogs, has emerged as a significant driver for the veterinary cardiology market. Several research indicates that approximately 10% of all dogs seen in primary care animal settings are diagnosed with heart disease, with this figure rising dramatically to over 60% in older dogs. This high prevalence is particularly evident in cases of myxomatous mitral valve disease (MMVD), which accounts for 75% of canine heart disease cases in the U.S., primarily affecting heart valves. Results of a comprehensive study, published in The Indian Veterinary Journal in June 2024 and conducted between July 2022 and September 2023 examining 435 dogs with generalized diseases, revealed that 26.21% displayed various types of cardiac arrhythmias, including atrial fibrillation (30.70%), sinus arrest (9.65%), and ST-segment elevation (8.77%), highlighting the significant burden of cardiac conditions in companion animals.

The growing awareness of cardiac health in production animals has also contributed to market growth, with congenital heart disease (CHD) emerging as a significant concern in cattle populations. Results from a study published in the Large Animal Review in February 2023 indicate that CHD prevalence ranges from 0.2% to 2.7% in cattle, emphasizing the need for specialized cardiac care across various animal species and demonstrating the growing requirement for the sophistication and effectiveness of veterinary cardiac treatments. Such factors have encouraged more pet owners to seek advanced cardiac care for their animals, further driving market growth and innovation in veterinary cardiology.

Growth in Veterinary Pharmaceuticals and Diagnostics

The veterinary cardiology market is experiencing substantial growth driven by significant pharmaceutical solutions and diagnostic technology advancements. The introduction of innovative medications and treatment options has revolutionized the management of cardiac conditions in animals. For instance, in June 2024, the launch of the VETMEDIN solution for managing congestive heart failure (CHF) in dogs marked a significant milestone as the first FDA-approved oral solution for canine CHF treatment. Additionally, the FDA approval of generic Pimomedin (pimobendan) chewable tablets in April 2024 for treating mild to severe congestive heart failure in dogs has improved treatment accessibility and affordability, demonstrating the market's response to the growing demand for effective cardiac medications.

The diagnostic segment has witnessed remarkable technological advancement by integrating sophisticated tools and techniques. For example, in November 2024, the introduction of Dashboard Vet's new feature enabling direct sharing of equine ECGs with veterinarians represents a significant step toward digital transformation in veterinary cardiology diagnostics. The rising cost of urban veterinary services, which increased by 7.9% from February 2023 to February 2024 as per the Bureau of Labor Statistics, reflects the growing investment in advanced diagnostic and treatment capabilities. The development of non-invasive diagnostic procedures such as advanced echocardiography, electrocardiography, and specialized blood tests further supports this trend. Veterinary Ultrasound Devices are increasingly being adopted for accurate cardiac imaging and echocardiography procedures in veterinary hospitals and specialty clinics. The continuous innovation in diagnostic technologies, coupled with the increasing adoption of digital platforms for veterinary care, has created a robust ecosystem for growing veterinary cardiology services.

Segment Analysis

Companion Animals Segment in Veterinary Cardiology Market

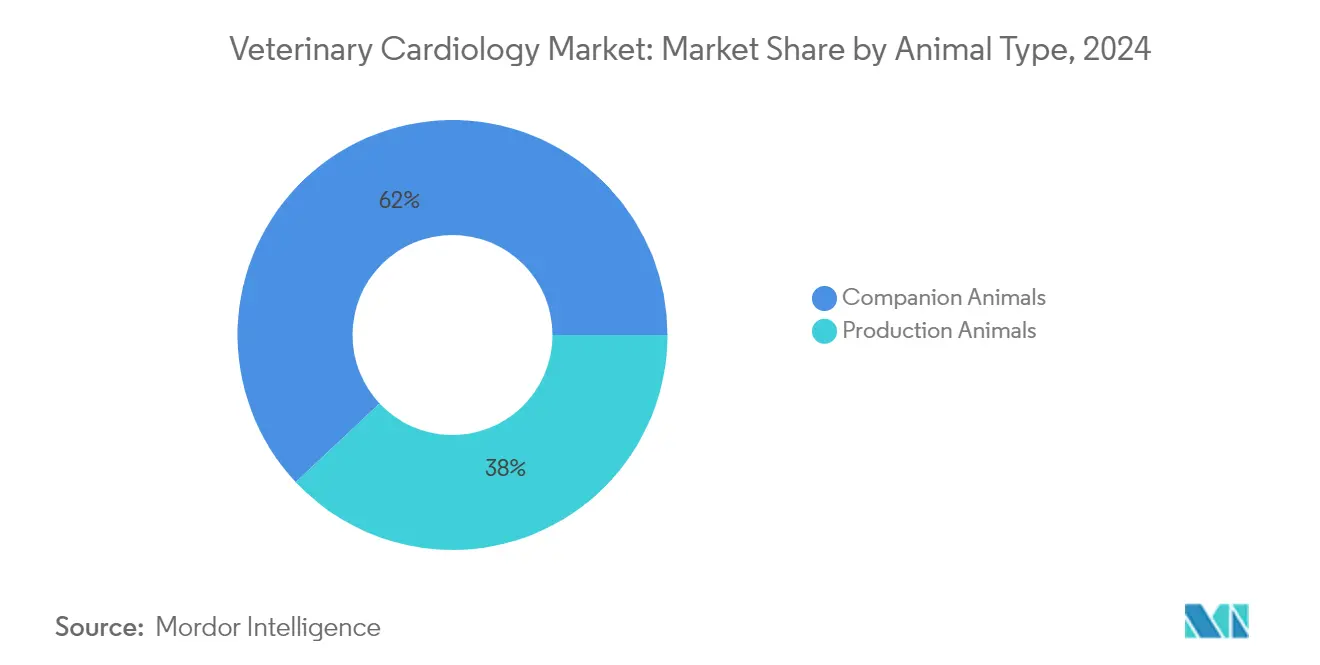

The companion animals segment dominates the veterinary cardiology market, commanding more than 60% market share in 2024, and is also expected to experience the fastest growth trajectory from 2025-2030. This segment's prominence is primarily attributed to the increasing prevalence of cardiac disorders in pets, particularly dogs and cats, coupled with rising pet ownership rates globally. The segment's robust performance is further strengthened by growing pet insurance penetration rates and increased willingness among pet owners to invest in advanced veterinary treatments. Technological advancements in diagnostic tools designed for companion animals have significantly enhanced the segment's market position. The emergence of specialized veterinary cardiology clinics and the integration of telemedicine services have also contributed to the segment's expansive market share. Moreover, the growing emotional bond between pets and their owners has increased spending on preventive cardiac care, driving both market share and growth rate.

Production Animals Segment in Veterinary Cardiology Market

The production animals segment represents a vital component of the Veterinary Cardiology Market, focusing on livestock and commercial farming animals. This segment's growth is primarily driven by the increasing demand for quality livestock healthcare and the economic importance of maintaining healthy production animals. Rising investments in research and development for the production of animal-specific cardiac treatments have enhanced the segment's market presence. Additionally, integrating digital health monitoring systems in commercial farming has improved the early detection and treatment

Veterinary Cardiology Market Product Type Segment Analysis

Pharmaceuticals Segment in Veterinary Cardiology Market

The pharmaceuticals segment dominated the veterinary cardiology market in 2024. The substantial market presence is primarily attributed to the increasing prevalence of cardiac disorders in companion animals and the growing demand for specialized veterinary medications. The extensive portfolio of cardiac medications available for various animal cardiovascular conditions further strengthens the segment's dominance. The widespread adoption of preventive healthcare measures and the development of novel drug formulations designed explicitly for veterinary cardiology applications have enhanced treatment outcomes and have significantly contributed to the segment's growth.

Diagnostics Segment in Veterinary Cardiology Market

The diagnostics segment is projected to emerge as the fastest-growing segment in the veterinary cardiology market during the forecast period 2025-2030. This remarkable growth trajectory is driven by technological advancements in diagnostic imaging equipment and the increasing adoption of point-of-care testing solutions. Integrating AI and ML in veterinary diagnostic tools has revolutionized animal cardiac disease detection accuracy and efficiency. Rising investments in veterinary healthcare infrastructure and a focus on early disease detection drive segment growth. Specialized veterinary cardiology centers and advanced diagnostic equipment are creating growth opportunities. Portable, user-friendly diagnostic devices improve access to cardiac care in various veterinary settings.

Veterinary Cardiology Market Indication Type Segment Analysis

Congestive Heart Failure Segment in Veterinary Cardiology Market

Congestive Heart Failure (CHF) emerged as the dominant veterinary cardiology segment, commanding most of the market share in 2024. This substantial market position is primarily attributed to the increasing prevalence of CHF in aging companion animals, particularly dogs and cats. The segment's dominance is also supported by the growing awareness among pet owners about early detection and management of heart failure symptoms. Additionally, the development of novel pharmaceutical interventions and improved treatment protocols have contributed to better disease management and increased market value.

Arrhythmias Segment in Veterinary Cardiology Market

The arrhythmias segment is projected to emerge as the fastest-growing segment in the veterinary cardiology market during the forecast period 2025-2030, with an estimated CAGR of 9-10%. The growth trajectory is primarily driven by technological advancements in cardiac monitoring devices and increased adoption of sophisticated diagnostic equipment in veterinary practices. The segment's expansion is further fueled by the introduction of innovative monitoring solutions, including wearable devices and remote monitoring systems, which have revolutionized arrhythmia detection and management in veterinary medicine. Growing investments in research and development for novel therapeutic approaches and the increasing availability of specialized veterinary cardiac care services are expected to sustain this segment's rapid growth throughout the forecast period.

Veterinary Cardiology Market Distribution Channel Segment Analysis

Direct Sales Segment in Veterinary Cardiology Market

Direct sales dominate the veterinary cardiology market with more than 70% share due to strong manufacturer-veterinary facility relationships, ensuring a consistent supply of essential cardiology diagnostic products and medications. The segment's growth is further reinforced by the preference of veterinary hospitals and clinics for direct procurement channels, which offer benefits such as bulk purchasing options, specialized product support, and immediate access to technical assistance. Direct sales channels also facilitate better quality control, regulatory compliance, and product traceability, which is crucial in the veterinary cardiology sector. The segment's robust performance is supported by the increasing number of veterinary facilities and the growing demand for specialized cardiac care products for companion and production animals.

Online Sales Segment in Veterinary Cardiology Market

The online sales segment is emerging as the fastest-growing distribution channel in the veterinary cardiology market and is projected to experience significant expansion from 2025 to 2030. This remarkable growth is driven by the increasing adoption of digital platforms for veterinary product procurement, enhanced by improved logistics networks and the convenience of online ordering systems. Veterinary professionals increasingly embrace online platforms for their procurement needs, attracted by competitive pricing, broader product selection, and the convenience of 24/7 ordering capabilities. The trend toward digital transformation in veterinary practices and the rising demand for contactless purchasing options continue to fuel the segment's growth trajectory.

Veterinary Cardiology Market End-Use Segment Analysis

Veterinary Hospitals Segment in Veterinary Cardiology Market

The veterinary hospitals segment dominated the veterinary cardiology market in 2024, with more than 50% market share. This substantial market presence is attributed to the adoption of sophisticated diagnostic equipment and the specialized expertise in these facilities. The segment's leadership position is reinforced by the increasing complexity of veterinary cardiac procedures requiring professional intervention. The segment's growth is supported by the increasing complexity of veterinary cardiac treatments and the need for specialized medication management. Advanced cardiac monitoring systems, specialized surgical facilities, and the presence of trained veterinary professionals have made these institutions the primary choice for pet owners seeking cardiac care for their animals. The segment's growth is further supported by the increasing willingness of pet owners to invest in quality healthcare. The concentration of specialized veterinary services in these establishments has created a comprehensive ecosystem for managing complex cardiac conditions in companion and production animals.

Veterinary Clinics Segment in Veterinary Cardiology Market

The veterinary clinic segment maintains a significant presence in the veterinary cardiology market as a crucial link between veterinary care providers and pet owners. This segment benefits from its ability to provide immediate access to cardiac medications and specialized veterinary cardiology diagnostics at the point of care. Integrating pharmacy services within veterinary clinics ensures proper medication dispensing and enables direct consultation between veterinarians and pharmacy staff. Additionally, the integration of cutting-edge technologies like digital imaging systems and remote monitoring capabilities has enhanced these facilities' diagnostic and treatment capabilities. The segment continues to evolve with the introduction of new cardiac treatment protocols, maintaining its relevance in the veterinary cardiology ecosystem.

Geography Analysis

Veterinary Cardiology Market in North America

North America represents the dominant force in the global veterinary cardiology market, characterized by advanced veterinary healthcare infrastructure and high pet ownership rates. The region's market is driven by increasing pet insurance adoption, growing awareness about animal cardiac health, and continuous technological advancements in veterinary cardiology. The presence of leading veterinary hospitals, research institutions, and major market players further strengthens the region's position. The United States, Canada, and Mexico collectively contribute to the region's prominence, with each country showing distinct growth patterns and market characteristics.

Veterinary Cardiology Market in United States

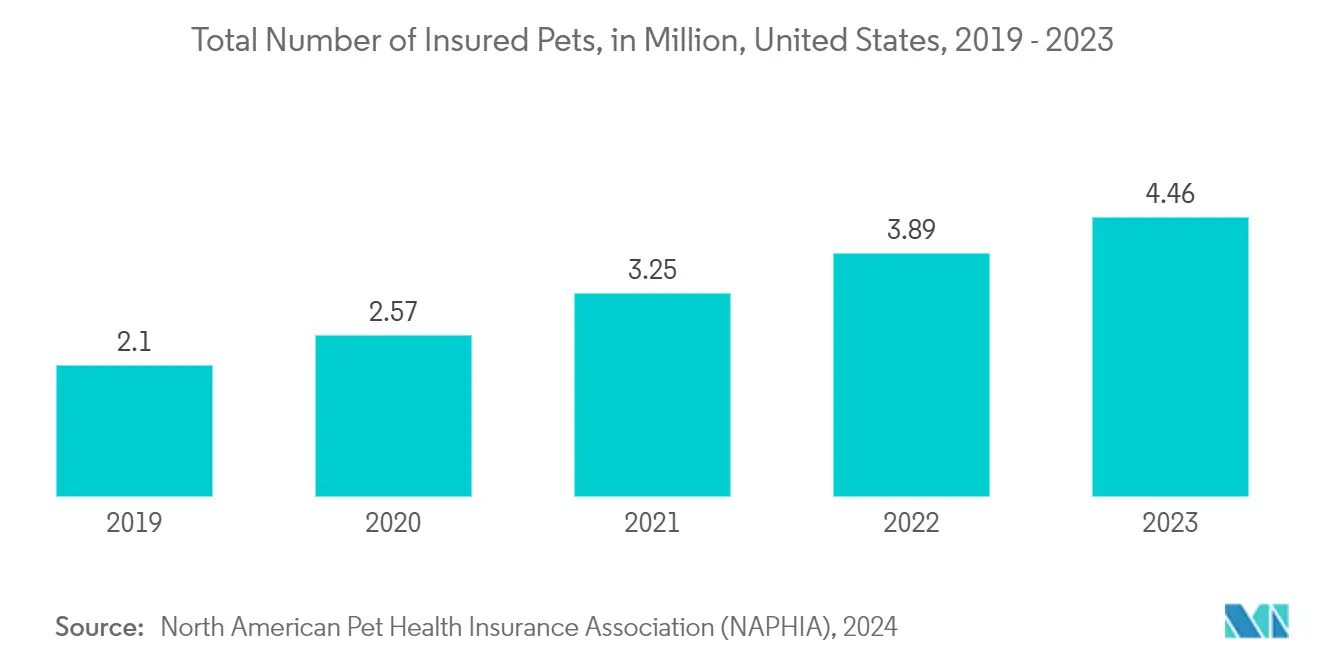

The United States stands as the largest market within North America, commanding more than ~30% of the global veterinary cardiology market share in 2024. The country's market leadership is supported by its robust veterinary healthcare infrastructure, high pet ownership rates, and advanced technological adoption. The presence of leading veterinary medical schools, research institutions, and pioneering surgical programs, such as the University of Florida's groundbreaking open-heart surgery program for dogs, demonstrates the country's commitment to advancing veterinary cardiology. The market is further strengthened by increasing pet insurance penetration, with more than 5.6 million pets insured out of over 86 million pet-owning households.

Veterinary Cardiology Market in Canada

Canada emerges as the fastest-growing market in North America, with an impressive projected growth rate of around 8% from 2025 to 2030. This surge can be attributed to a rise in pet adoptions, heightened awareness of preventive veterinary care, and bolstered investments in veterinary healthcare infrastructure. Moreover, with backing from both government initiatives and private investments, Canadian veterinary institutions are placing a pronounced emphasis on specialized cardiac care.

Veterinary Cardiology Market in Europe

Europe represents a significant market for veterinary cardiology, characterized by its sophisticated veterinary healthcare systems and strong focus on animal welfare. The region benefits from well-established veterinary education institutions, research centers, and a high concentration of skilled veterinary professionals. The market dynamics vary across different countries, each contributing uniquely to the regional market.

Veterinary Cardiology Market in Germany

Germany emerges as the largest veterinary cardiology market in Europe, holding approximately a quarter of the regional market share in 2024. The country's market leadership is attributed to its advanced veterinary healthcare infrastructure, strong research capabilities, and high standards of animal care. The German market is characterized by the presence of leading veterinary hospitals, research institutions, and a robust regulatory framework supporting animal healthcare, including the comprehensive Animal Welfare Act.

Veterinary Cardiology Market in the United Kingdom

The United Kingdom veterinary cardiology market is anticipated to grow rapidly, driven by increasing pet insurance adoption. Approximately 3.7 million people carry pet insurance policies covering 4.3 million pets. The veterinary cardiology sector also benefits from continuous technological advancements, strong research initiatives, and growing awareness about pet cardiac health among owners.

Veterinary Cardiology Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market in the global veterinary cardiology landscape, characterized by increasing pet ownership, rising disposable incomes, and growing awareness about animal healthcare. Countries like China, Japan, India, Australia, South Korea, and Thailand are witnessing significant developments in veterinary healthcare infrastructure and services. The region's market is driven by technological advancements, increasing investments in veterinary healthcare facilities, and growing adoption of pet insurance.

Veterinary Cardiology Market in China

China stands as the largest market for veterinary cardiology in the Asia-Pacific region. The country's market leadership is supported by its large pet population, increasing pet ownership rates, and significant investments in veterinary healthcare infrastructure. The presence of numerous veterinary centers, including New Ruipeng's network of 1,400 centers across 80 cities, demonstrates the market's robust growth and development potential.

Veterinary Cardiology Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's market growth is driven by increasing pet adoption rates, rising awareness about animal healthcare, and significant investments in veterinary infrastructure. In May 2024, Future Generali India Insurance reported that India ranks among the world's fastest-growing pet markets, boasting an annual growth rate nearing 14%. Projections indicate that India's pet care market could reach a valuation of US$ 800 million by 2025. Recent initiatives like 'Drools Vet Thrive' launched in October 2023 and aimed at upgrading veterinary clinics across the country exemplify the market's development trajectory and commitment to improving veterinary cardiac care services.

Veterinary Cardiology Market in Middle East & Africa

The Middle East & Africa region demonstrates growing potential in the veterinary cardiology market, with an increasing focus on developing advanced veterinary care facilities and professional expertise. The region's market is characterized by rising awareness about animal healthcare, growing investments in veterinary infrastructure, and increasing adoption of modern treatment methodologies. Saudi Arabia represents the largest market in the region, driven by government initiatives and technological advancements, while the UAE emerges as the fastest-growing market, supported by initiatives like the Middle East Animal Veterinary Conference (MEAVC) and increasing investments in specialized veterinary care facilities.

Veterinary Cardiology Market in South America

Latin America's veterinary cardiology market is experiencing significant transformation, driven by increasing awareness about animal cardiac health and improving veterinary healthcare infrastructure. The region's market is characterized by growing collaboration between veterinary institutions, increasing professional training opportunities, and rising investments in specialized care facilities. Brazil emerges as both the largest and fastest-growing market in the region, supported by strategic investments and expansion of high-quality veterinary care providers like WeVets, while Argentina contributes significantly to the regional market development.

Competitive Landscape

Top Companies in Veterinary Cardiology Market

The veterinary cardiology market is led by key players, including Boehringer Ingelheim, Cronus Pharma, Esaote SpA, FUJIFILM, GE Healthcare, IDEXX, IMV Companion Animal Ltd, Merck & Co., Inc, Shenzhen Mindray Animal Medical Technology Co., LTD., and Zoetis Inc. These companies consistently focus on product innovation, particularly in developing advanced diagnostic tools and pharmaceutical solutions for animal cardiac care. The industry witnesses regular launches of novel medications and diagnostic equipment, with companies investing heavily in research and development to address emerging cardiac conditions in animals. Strategic partnerships between pharmaceutical companies and veterinary hospitals have become increasingly common, enabling better market penetration and enhanced service delivery. Geographic expansion remains a key growth strategy, particularly in emerging markets, with companies establishing regional manufacturing facilities and distribution networks to serve local markets better.

Market Consolidation Drives Industry Evolution Forward

The veterinary cardiology market is moderately consolidated, with global pharmaceutical giants and specialized veterinary care providers. Large pharmaceutical firms leverage research capabilities and global distribution networks, while niche players focus on specific segments and regions. As larger companies expand their portfolios and geographic reach, the market has seen significant mergers and acquisitions, particularly involving technology-driven startups and regional players.

Collaborations among industry players, research institutions, and veterinary care providers shape competitive dynamics. Strategic alliances combine strengths in drug development, diagnostics, and clinical expertise. Emerging market players gain prominence through targeted products and strong local ties with veterinary practitioners. Medical device manufacturers also contribute by adapting human healthcare technologies for veterinary use, diversifying the competitive landscape.

Innovation and Accessibility Drive Future Success

Success in the veterinary cardiology market depends on developing cost-effective, high-quality solutions. Market leaders are integrating pharmaceuticals with diagnostics and monitoring systems while investing in digital technologies and telemedicine to enhance service delivery. Building strong relationships with veterinary hospitals and clinics remains critical for service delivery and product adoption.

The market's future relies on addressing the demand for specialized cardiac care while managing regulatory and cost challenges. Key success factors include innovative drug delivery systems, improved diagnostic accuracy, and product affordability. Companies must also raise awareness among pet owners and veterinary professionals through educational initiatives. Adapting to regulatory changes, maintaining quality standards, building resilient supply chains, and ensuring operational flexibility are essential for sustained market presence.

Veterinary Cardiology Industry Leaders

Boehringer Ingelheim

Esaote SpA

FUJIFILM

GE Healthcare

Merck & Co., Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: VETiNSTANT, an animal healthcare tech startup, partnered with IIT-Madras Incubation Cell in India to launch Exam D, a non-invasive device for diagnosing animal health. Paired with a mobile app, it connects pets and veterinarians for timely care. Exam D has two versions: one measures temperature and auscultates the heart, lungs, and abdomen, while the other adds SpO2 and heart rate readings. Pet owners can easily use it to measure temperature, heart rate, and respiratory sounds by placing it near their pet. The data can be shared with a veterinarian via telemedicine for analysis

- January 2024: A team of doctors at Chulalongkorn University in Thailand successfully performed minimally invasive mitral valve repair (MVR) surgery using a mitral clamp on a dog - the first such procedure in the country. This innovative technique eliminates the need for an artificial heart/lung machine and offers benefits like reduced surgical wounds and faster recovery.

- April 2023: The Columbus Zoo and Aquarium in Ohio partnered with the Great Ape Heart Project to enhance cardiac care for great apes. This collaboration aims to improve the understanding and treatment of heart disease in gorillas, orangutans, bonobos, and chimpanzees.

- January 2023: Invoxia launched a USD 149 smart dog collar that monitors heartbeat and location, with data subscriptions starting at USD 8.25 monthly. Its sensor and AI technology track respiratory and heart vitals, activity, and location, offering insights into a dog's health and well-being. Developed with veterinary specialists, the collar supports preventive pet care by detecting health issues early and alerting owners for timely treatment.

- January 2023: The 40th annual Veterinary Meeting & Expo (VMX) was organized in Florida, bringing together veterinary professionals from over 65 countries to discuss the latest advancements in animal medicine, including cardiology diagnostics and treatments.

Global Veterinary Cardiology Market Report Scope

As per the scope of the report, veterinary cardiology refers to the equipment and drugs required for diagnosing and treating diseases of the heart of companion and farm animals.

The veterinary cardiology market is segmented by animal type, product type, indication, distribution channel, end-use, and geography. By animal type, the market is bifurcated into companion animals and production animals. Based on product type, the market is bifurcated into pharmaceuticals and diagnostics. On the basis of indication, the market is segmented into congestive heart failure (CHF), arrhythmia, and others. By distribution channel, the market is bifurcated into direct sales and online sales. Based on end-use, the market is segmented into Veterinary hospitals, veterinary clinics, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the market sizes and forecasts for major countries across different regions. The market size is provided for each segment in terms of value (USD).

| Companion Animals |

| Production Animals |

| Pharmaceuticals |

| Diagnostics |

| Congestive Heart Failure |

| Arrhythmias |

| Others |

| Direct Sales |

| Online Sales |

| Veterinary Hospitals |

| Veterinary Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Animal Type | Companion Animals | |

| Production Animals | ||

| By Product Type | Pharmaceuticals | |

| Diagnostics | ||

| By Indication | Congestive Heart Failure | |

| Arrhythmias | ||

| Others | ||

| By Distribution Channel | Direct Sales | |

| Online Sales | ||

| By End-Use | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Veterinary Cardiology Market?

The Veterinary Cardiology Market size is expected to reach USD 3.19 billion in 2025 and grow at a CAGR of 8.84% to reach USD 4.87 billion by 2030.

What is the current Veterinary Cardiology Market size?

In 2025, the Veterinary Cardiology Market size is expected to reach USD 3.19 billion.

Which is the fastest growing region in Veterinary Cardiology Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Veterinary Cardiology Market?

In 2025, the North America accounts for the largest market share in Veterinary Cardiology Market.

What years does this Veterinary Cardiology Market cover, and what was the market size in 2024?

In 2024, the Veterinary Cardiology Market size was estimated at USD 2.91 billion. The report covers the Veterinary Cardiology Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Veterinary Cardiology Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: