Veterinary Orthopedics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

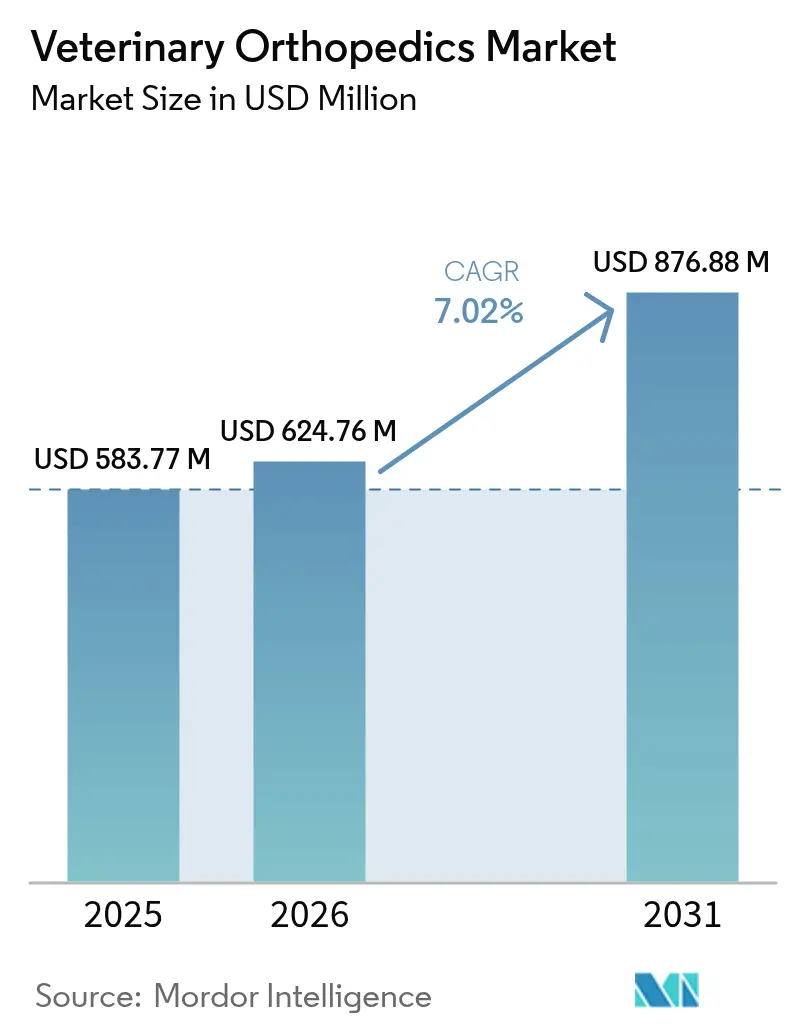

| Market Size (2026) | USD 624.76 Million |

| Market Size (2031) | USD 876.88 Million |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

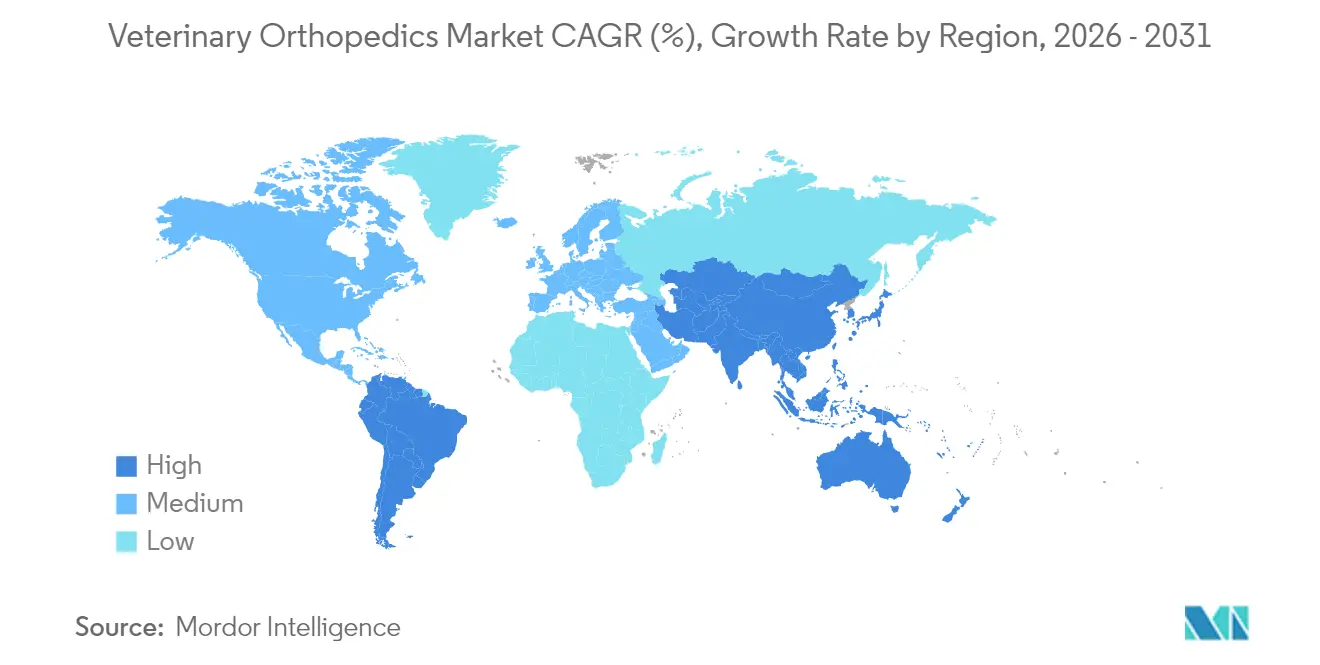

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Orthopedics Market Analysis by Mordor Intelligence

The veterinary orthopedics market size was valued at USD 583.77 million in 2025 and estimated to grow from USD 624.76 million in 2026 to reach USD 876.88 million by 2031, at a CAGR of 7.02% during the forecast period (2026-2031). This trajectory is anchored in three structural shifts: pet humanization that normalizes premium care, rapid advances in additive manufacturing that yield patient-specific implants, and the steady build-out of referral-grade facilities in emerging regions. Surgical interventions remain the definitive solution for dysplasia, cruciate injuries and advanced osteoarthritis, so procedure volumes are largely non-discretionary. Market leaders continue to bundle implants, instruments and surgeon training, a strategy that raises switching costs and supports recurring revenue from replacement hardware as animals age. At the same time, new corporate practice groups in Asia view orthopedics as a margin-rich service line, accelerating capital investment in arthroscopy suites and CT-guided planning tools.

Key Report Takeaways

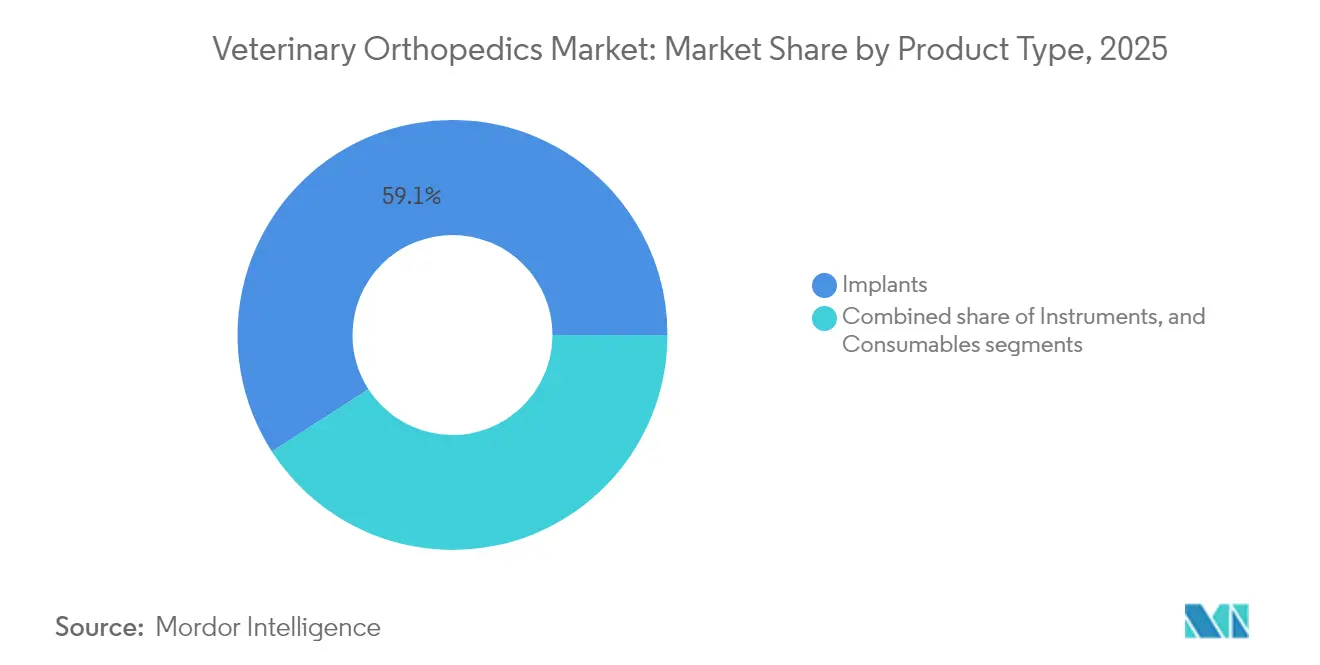

- By product type, implants held 59.12% of the veterinary orthopedics market share in 2025; implants segment is projected to grow at an 7.78% CAGR through 2031.

- By animal type, canine procedures represented 47.10% of 2025 revenue, while feline procedures are forecast to post the fastest growth at 8.05% CAGR to 2031.

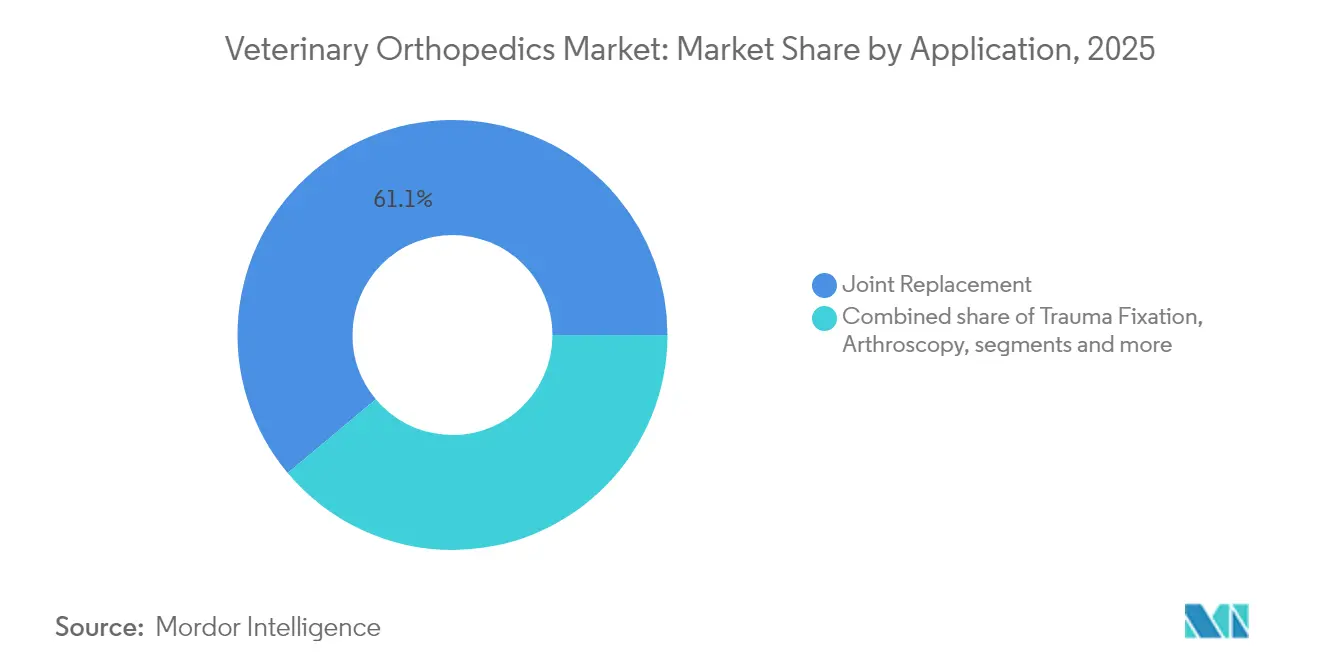

- By application, joint replacement accounted for 61.10% of the veterinary orthopedics market size in 2025; trauma fixation is expected to register an 8.22% CAGR between 2026-2031.

- By end-user, hospitals and referral centers controlled 70.65% revenue in 2025, whereas specialty orthopedic clinics are anticipated to expand at 9.35% CAGR through 2031.

- By geography, North America led with 47.80% share in 2025; Asia-Pacific is set to advance at a 9.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Orthopedics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet ownership & expanding veterinary workforce | +1.8% | Global, with strongest impact in APAC | Medium term (2-4 years) |

| National animal-welfare funding & insurance expansion | +1.2% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Surge in obesity-linked orthopedic disorders | +2.1% | Global, particularly developed markets | Short term (≤ 2 years) |

| Advances in 3-D printed & patient-specific implants | +1.5% | North America & EU, with adoption in APAC | Medium term (2-4 years) |

| Growing adoption of minimally-invasive arthroscopy | +0.9% | Global, led by North America | Short term (≤ 2 years) |

| Equine sports medicine demand in emerging economies | +0.6% | APAC, MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership & Expanding Veterinary Workforce

Global pet ownership continues to climb, with U.S. expenditures alone projected to hit USD 279 billion by 2030. Millennials and Gen Z increasingly treat pets as family, prompting demand for surgical options once reserved for elite equine athletes. Newly chartered veterinary colleges in China and India add capacity, yet graduate distribution skews toward urban hubs, leaving rural practices understaffed. The American Association of Veterinary Medical Colleges forecasts a 24% shortfall—70,092 veterinarians needed versus 52,926 expected graduates by 2032. This imbalance fuels practice consolidation and wider use of teleconsults that route complex orthopedic cases to referral centers.

National Animal-Welfare Funding & Insurance Expansion

Government subsidies and pet insurance uptake reduce out-of-pocket costs for surgery, stimulating procedure volumes. Scandinavian markets exceed 80% insurance penetration, creating transparent fee schedules that streamline reimbursement.[1]Frontiers in Veterinary Science, “Insurance Penetration and Price Transparency in Companion Animal Care,” frontiersin.org The U.S. Rural Veterinary Workforce Act proposes loan forgiveness for clinicians serving shortage areas, a model now studied by regulators in Australia and Japan. On the product side, anatomically contoured 3.5 LCP distal femoral plates tailored to medium and large breeds illustrate how targeted funding can fast-track device development.

Surge in Obesity-Linked Orthopedic Disorders

Obesity affects 30-50% of dogs and accelerates hip dysplasia, cruciate tears and degenerative joint disease, pushing conservative cases toward surgery sooner.[2]USDA Shortage Area Map 2025, dvm360.com A lifetime cost study found surgical management of canine hip osteoarthritis cheaper than prolonged medical therapy for dogs under eight, reframing surgery as a cost-effective first-line option. Practices now bundle weight-loss plans with TPLO or total hip replacement to preserve long-term mobility. A cohort review of 450,000 dogs placed osteoarthritis prevalence at 2.5%, underscoring the scale of unmet need.

Advances in 3-D Printed & Patient-Specific Implants

Additive manufacturing enables implants that mirror breed-specific anatomy, reducing intra-operative adjustments and promoting osseointegration. VCA Animal Hospitals opened dedicated 3-D printing labs that output custom plates and cutting guides on-site. Laser-printed cobalt-chromium-molybdenum knee implants now match the fatigue strength of forged devices while cutting lead times from weeks to days. The American Academy of Orthopaedic Surgeons lists veterinary devices as a near-term growth avenue for 3-D printing. Still, regulatory pathways remain in flux; the FDA only recently issued draft guidance on metallic coatings for patient-matched implants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of implants, surgery & after-care | -1.9% | Global, most severe in emerging markets | Short term (≤ 2 years) |

| Shortage of board-certified veterinary surgeons | -1.4% | Global, particularly rural areas | Medium term (2-4 years) |

| Limited reimbursement outside North America & EU | -0.8% | APAC, MEA, South America | Long term (≥ 4 years) |

| Regulatory lag for novel biomaterials & devices | -0.5% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Implants, Surgery & After-Care

TPLO procedures range from USD 4,900–6,500 in the United States, with complex cases topping USD 10,000, steering price-sensitive owners toward cross-border care in Mexico at roughly USD 3,500. In Europe, median costs swing from €72 in Sweden to €230 in Denmark for basic repairs, reflecting divergent reimbursement models. Chain hospitals often levy higher fees than independent clinics, widening access gaps. Post-operative rehab, physiotherapy and potential revision surgeries add to the financial burden, amplifying cost as the leading barrier to early intervention.

Shortage of Board-Certified Veterinary Surgeons

Seventy-three percent of animal shelters report veterinarian shortages, and 74% lack adequate technical staff, curbing surgical capacity. The USDA flagged 243 veterinary shortage areas in 2025, the highest on record.[3]Royal Canin Academy, “The Obesity Epidemic in Companion Animals,” royalcanin.com Rising debt loads and high burnout rates have pushed new graduates toward small-animal general practice in urban centers, leaving rural regions without referral access. Limited residency slots in orthopedics further constrict supply. Although the American Veterinary Medical Association projects workforce equilibrium by 2035, its scenario assumes static demand and does not fully capture the growing complexity of orthopedic caseloads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Implants Sustain Revenue Leadership

Implants delivered 59.12% of the veterinary orthopedics market in 2025, and the sub-segment is on track for an 7.78% CAGR through 2031. Plates and screws dominate, thanks to locking compression technology that cuts surgical time and boosts union rates. Pins, wires and nails are the breakout category, supported by external fixation methods like the SPIDER technique that remove the need for postoperative coaptation. The veterinary orthopedics market size for implants is set to grow by USD 147.5 million over the forecast window, mirroring parallel innovations in human trauma hardware.

Instruments hold a smaller but resilient share as referral hospitals outfit arthroscopy suites and integrate CT-guided drill jigs. Consumables remain price-elastic; private-label absorbable suture and biologic cements now enter formularies of large clinic groups. Digital convergence looms: Johnson & Johnson demonstrated a veterinary adaptation of its robotic arthroplasty platform, signaling impending automation of drill trajectories and cut blocks. Such systems reinforce implant pull-through by relying on proprietary instrumentation.

By Animal Type: Dogs Lead, Cats Accelerate

Canine patients generated 47.10% of 2025 revenue, supported by high incidence of hip dysplasia and cruciate injuries in large breeds. Breed-specific studies on Legg-Calvé-Perthes in toy breeds and iliopsoas strain in working dogs drive implant refinements that preserve range of motion. Feline cases, often under-diagnosed due to subtle pain signs, now show 8.05% CAGR as owners accept advanced imaging and custom narrow-diameter screws. The veterinary orthopedics market size for feline implants is forecast to climb from USD 68.07 million in 2026 to USD 100.25 million by 2031.

Equine sports medicine retains a premium niche: performance-metric tracking in racehorses leads to early detection of micro-fractures, fueling demand for arthroscopic chip removal and locking plate fixation. Exotic species represent a small but visible frontier; 3-D printed beak prostheses for parrots and hinged shell implants for turtles illustrate the expansion of surgical reach beyond traditional companions.

By Application: Replacement Maturity, Trauma Momentum

Joint replacement captured 61.10% of the veterinary orthopedics market size in 2025 as total hip replacement moved from experimental to routine in referral centers. Movora alone has surpassed 100,000 cumulative hip and stifle implants, underpinned by surgeon certification courses that standardize outcomes. Improvements in cementless cup designs now mirror human acetabular components, driving lower revision rates and higher owner satisfaction.

Trauma fixation is the fastest-growing application at 8.22% CAGR, stimulated by geriatric pet demographics and multi-fragment fractures from high-energy impacts. Locking plate constructs and hybrid external-internal fixation expand treatable case profiles. The SPIDER frame permits stable alignment of metacarpal fractures without casting, shortening recovery time. Arthroscopy, though still a minority share, spreads rapidly as equipment costs fall; equine surgeons routinely debride osteochondral lesions arthroscopically, a practice now migrating to canine sport patients.

By End-User: Referral Hospitals Dominate, Specialty Clinics Bloom

Hospitals and referral centers performed 70.65% of orthopedic procedures in 2025, a reflection of concentrated CT, MRI and laminar-flow operating theaters. Yet specialty clinics targeting orthopedics display a 9.35% CAGR to 2031 as surgeons spin off from corporate chains to offer bespoke care models. The veterinary orthopedics market share held by specialty centers is projected to climb to 21.60% by 2031, signaling a gradual decentralization of complex surgery.

Academic institutes, although a small slice, set training standards and validate new techniques through peer-reviewed trials. The 23rd Federation of Asian Veterinary Associations Congress accepted 102 orthopedic abstracts for oral presentation, confirming academia’s catalytic role in regional skills transfer. Corporate buyers such as Enovis and DJO view veterinary channels as strategic extensions of human ortho portfolios, injecting capital for faculty-run cadaver labs that upskill community clinicians.

Geography Analysis

North America commanded 47.80% of 2025 revenue, benefiting from 3.5 million insured pets and dense networks of board-certified surgeons. The average practice deploys two digital radiography units and maintains referral ties with at least one advanced imaging center, creating seamless pathways from diagnosis to implant placement. Johnson & Johnson leverages its DePuy Synthes catalog to supply TPLO systems that have logged over 500,000 canine procedures with a complaint rate of 0.006%. Despite market maturity, procedure frequency rises as owners replace first-generation implants or address contralateral cruciate disease.

Europe exhibits robust but heterogeneous growth. Scandinavian nations set the benchmark with reimbursement models that cap owner co-pays and mandate transparent fee disclosures, compressing price dispersion. Germany reports a 14-week waiting period for elective arthroscopy, signaling demand outstripping specialist capacity. Southern Europe lags due to lower insurance uptake, yet equine studs in Spain and Italy invest heavily in arthroscopic chip removal to preserve bloodstock value.

Asia-Pacific is the fastest-growing region at 9.62% CAGR. China’s companion animal hospital count rose 11% in 2024, each clinic serving 6,862 pets versus 5,485 in the United States, pointing to latent surgery volumes. Australia records the world’s highest per-capita dog ownership, and its universities now produce 1,200 veterinary graduates annually, many entering small-animal orthopedics. Japan’s drug-device review framework expedites advanced implant approvals, smoothing entry for global manufacturers. The Middle East and Africa remain nascent but promising. Gulf states establish equine rehabilitation centers that require titanium locking plates for performance stallions. Kenya’s first referral orthopedic clinic opened in 2024 and already trains interns on TPLO procedures, underscoring the diffusion of standards. South America’s trajectory is mixed: Brazil hosts 55 accredited veterinary schools yet suffers currency volatility that hinders import of high-value implants. Still, local foundries begin machining stainless-steel plates under ISO-13485 to cut costs.

Competitive Landscape

The veterinary orthopedics market blends diversified human-device giants with focused animal-health specialists. DePuy Synthes extends AO Foundation research to launch species-specific locking plates, retaining surgeons through bundled saw-blade consumables. Movora’s end-to-end joint replacement portfolio spans implants, instruments and surgeon education, a turnkey model that cultivates brand loyalty and lifts repeat sales. BioMedtrix differentiates via modular hip stems sized for toy breeds, addressing an underserved niche.

M&A reshapes boundaries: Enovis agreed to acquire LimaCorporate in 2025, adding cementless metallurgy that can migrate into veterinary stems. DJO’s purchase of Companion Animal Health signals growing cross-pollination between rehabilitation modalities and implant businesses. Start-ups focus on 3-D printed patient-matched plates and absorbable screw polymers aimed at feline fractures. Regulatory agility becomes a competitive variable as the FDA finalizes coating guidelines that will dictate future approval pathways for porous tantalum and calcium-phosphate layered implants.

Digital surgery platforms loom large. Johnson & Johnson’s prototype robotic assistant demonstrates half-millimeter repeatability in saw-cut alignment on canine tibiae, pointing to reduced revisions. KYON partners with software developers to deliver AI-driven pre-op planning that auto-selects implant size from CT scans. Market entrants that pair hardware with cloud analytics may capture value beyond device margins by monetizing data on gait outcomes and revision risk.

Veterinary Orthopedics Industry Leaders

BioMedtrix

Veterinary Orthopedic Implants

KYON

B. Braun SE

Integra LifeSciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Researchers proposed a multimodal management framework for osteoarthritis in growing dogs after analyzing 450,000 cases and validating a 2.5% prevalence rate.

- March 2025: A comparative study confirmed that modified TPLO with tibial tuberosity transposition delivered positive outcomes for Grade IV patellar luxation and cruciate disease in small breeds.

- March 2025: The U.S. Congress reintroduced the Rural Veterinary Workforce Act, offering loan forgiveness to clinicians serving shortage areas.

- February 2024: VCA Animal Hospitals opened a 3-D printing lab at VCA Northwest Veterinary Specialists to produce patient-specific orthopedic implants.

Global Veterinary Orthopedics Market Report Scope

As per the scope, Veterinary Orthopedics deals with the diseases and injuries related to bones, joints, ligaments, tendons and others. The veterinary Orthopedics market is Segmented By Type, End-User and Geography.

| Implants | Plates and Screws |

| Pins, Wires and Nails | |

| External Fixators | |

| Instruments | |

| Consumables |

| Canine |

| Feline |

| Equine |

| Others |

| Joint Replacement |

| Trauma Fixation |

| Arthroscopy |

| Others |

| Veterinary Hospitals and Referral Centers |

| Specialty Orthopedic Clinics |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Implants | Plates and Screws |

| Pins, Wires and Nails | ||

| External Fixators | ||

| Instruments | ||

| Consumables | ||

| By Animal Type | Canine | |

| Feline | ||

| Equine | ||

| Others | ||

| By Application | Joint Replacement | |

| Trauma Fixation | ||

| Arthroscopy | ||

| Others | ||

| By End User | Veterinary Hospitals and Referral Centers | |

| Specialty Orthopedic Clinics | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the veterinary orthopedics market?

The veterinary orthopedics market reached USD 624.76 million in 2026 and is projected to hit USD 876.88 million by 2031.

Which product category leads revenue?

Implants held 59.12% of global revenue in 2025, driven by locking plates and 3-D printed patient-specific devices.

Which region is growing fastest?

Asia-Pacific is expanding at a 9.62% CAGR through 2031 thanks to rising pet ownership and rapid clinic expansion.

How is 3-D printing changing veterinary orthopedics?

Custom implants reduce surgical time, improve fit and are now produced in dedicated hospital labs, accelerating adoption.

Page last updated on: