Veterinary Biologics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

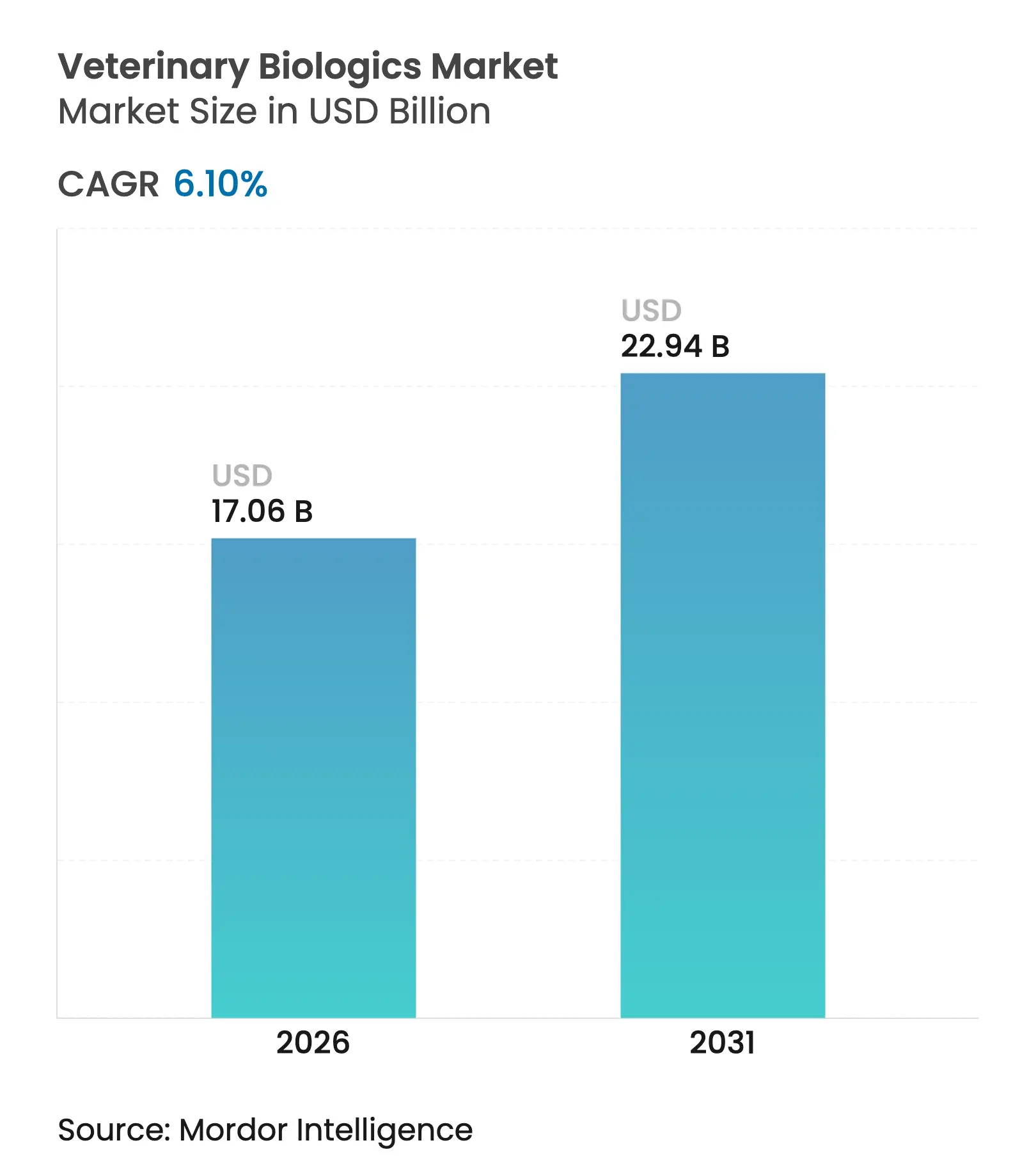

| Market Size (2026) | USD 17.06 Billion |

| Market Size (2031) | USD 22.94 Billion |

| Growth Rate (2026 - 2031) | 6.10 % CAGR |

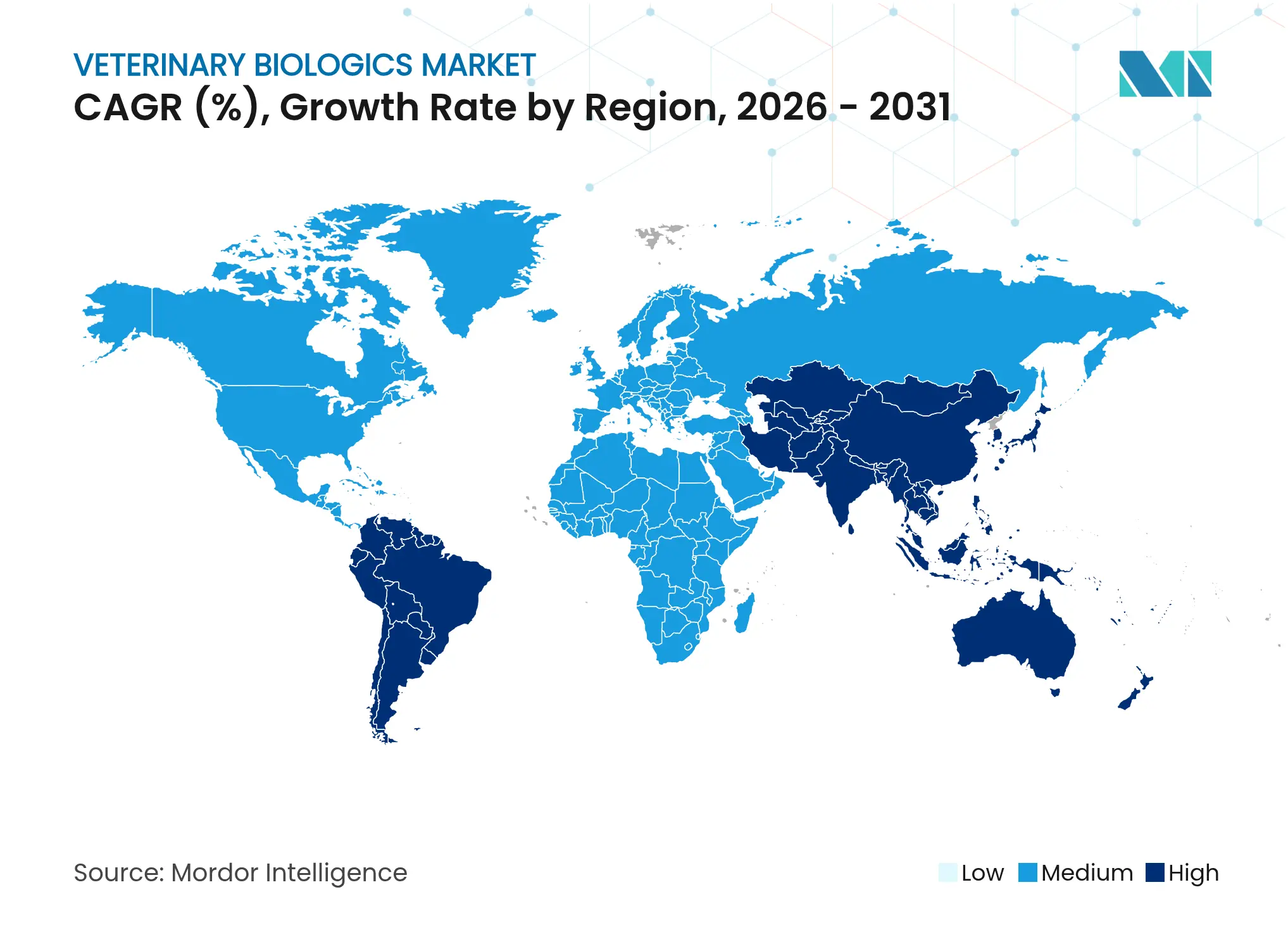

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Veterinary Biologics Market Analysis by Mordor Intelligence

The veterinary biologics market size is expected to grow from USD 16.08 billion in 2025 to USD 17.06 billion in 2026 and is forecast to reach USD 22.94 billion by 2031 at 6.10% CAGR over 2026-2031. Sustained growth stems from mandatory livestock vaccination programs, rising companion-animal health expenditure, and accelerated adoption of recombinant, vector-based, and mRNA platforms. Producers gain predictable revenue streams because vaccination protocols are embedded in food-safety and export regulations, while pet owners’ willingness to pay for preventive care supports premium pricing. Digital procurement channels and AI-enabled antigen discovery shorten development cycles and widen product accessibility, reinforcing the upward trajectory of the veterinary biologics market.

Key Report Takeaways

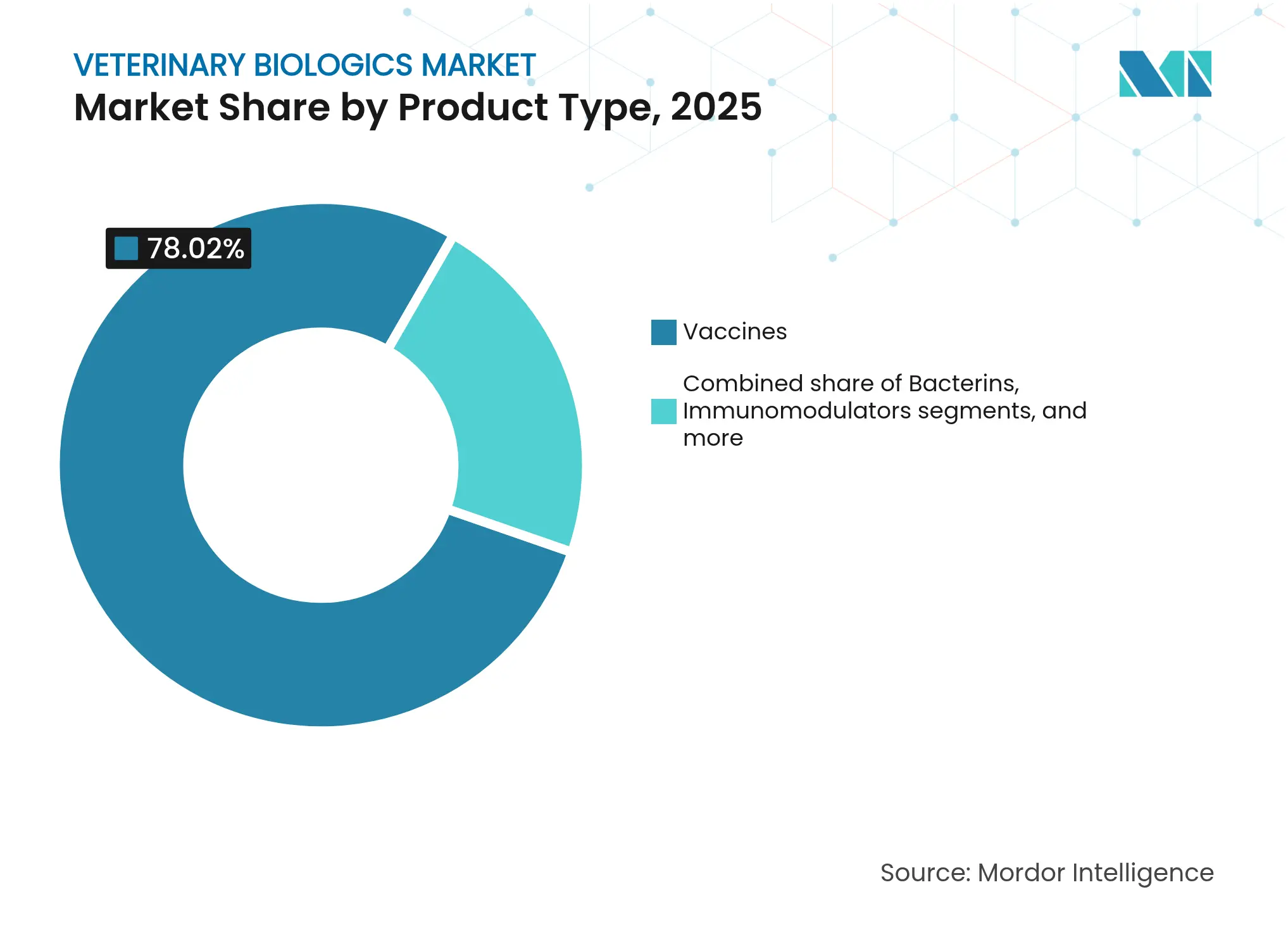

- By product type, vaccines led with 78.02% of the veterinary biologics market share in 2025; the same segment is projected to grow at a 6.33% CAGR through 2031.

- By animal type, livestock accounted for 58.35% share of the veterinary biologics market size in 2025, while companion animals record the fastest 7.92% CAGR to 2031.

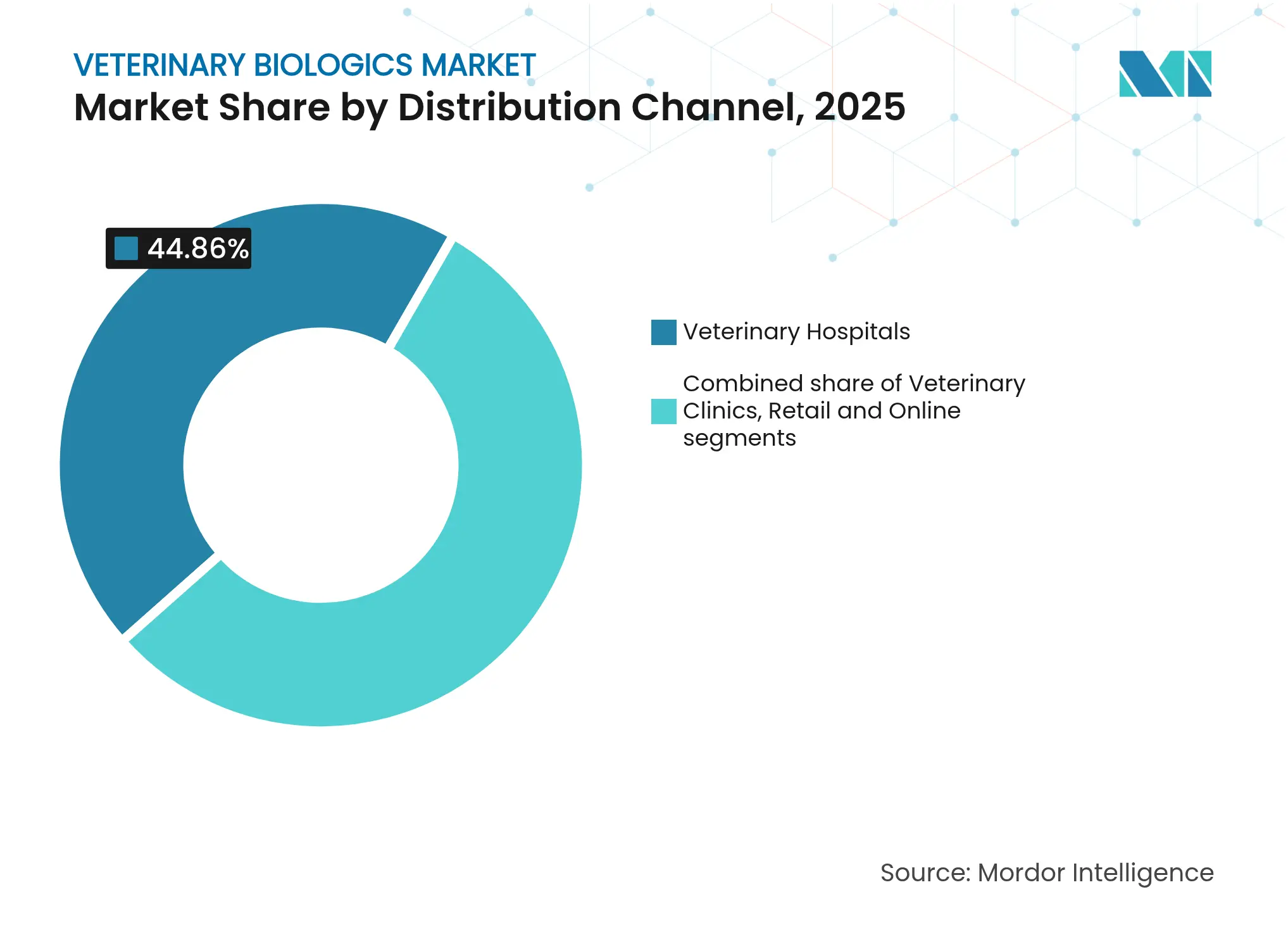

- By distribution channel, veterinary hospitals held 44.86% share in 2025; e-commerce pharmacies expand most rapidly at 8.86% CAGR.

- By technology, live attenuated vaccines commanded 42.65% share in 2025, whereas inactivated vaccines display the highest 8.61% CAGR through 2031.

- By geography, North America dominated with 37.92% share in 2025; Asia-Pacific shows the strongest 8.08% CAGR driven by livestock intensification and regulatory harmonization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Biologics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Vaccination Mandates for Livestock & Pets

Vaccination Mandates for Livestock & Pets

| +1.2% | Global; strongest in North America and EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global; strongest in North America and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Recombinant & Vector-Based Vaccine Approvals

Recombinant & Vector-Based Vaccine Approvals

| +0.8% | North America and EU leading; APAC following | Long term (≥ 4 years) | |||

Companion-Animal Spending Growth

Companion-Animal Spending Growth

| +0.7% | North America and EU core markets | Short term (≤ 2 years) | |||

mRNA Platforms Enter Veterinary Pipeline

mRNA Platforms Enter Veterinary Pipeline

| +0.6% | Global; early adoption in North America and EU | Long term (≥ 4 years) | |||

AI-Driven Antigen Discovery

AI-Driven Antigen Discovery

| +0.5% | Global, concentrated in major pharmaceutical hubs | Medium term (2-4 years) | |||

One-Health Stockpile Funding

One-Health Stockpile Funding

| +0.4% | Global, with priority in pandemic-prone regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Vaccination Mandates for Livestock & Pets

Regulators in major meat-exporting regions tighten vaccination schedules, turning biologics into a non-discretionary cost line for producers. The U.S. National One Health Framework released in 2025[1]U.S. Food and Drug Administration, “Animal and Veterinary Innovation Agenda,” fda.gov synchronizes CDC and USDA requirements, boosting bulk procurement of multivalent vaccines. EU directives mirror this stance, obliging exporters to show proof of comprehensive immunization. As producers prefer single-source suppliers for compliance ease, established firms with broad catalogs consolidate demand, creating resilient cash flows despite cyclical farm-gate margins.

Recombinant & Vector-Based Vaccine Approvals

The European Medicines Agency cleared nine veterinary vaccines[2]European Medicines Agency, “Veterinary Medicines Highlights 2023,” ema.europa.eu in 2024, six of which rely on recombinant or vector technologies, versus a single biologic two years earlier. Parallel FDA fast-track programs cut review cycles to as little as four years. Recombinant platforms offer batch consistency and lower contamination risks, making them attractive for diseases such as porcine reproductive and respiratory syndrome. Smaller innovators with platform specialization leverage the regulatory tailwind, compelling incumbents to upgrade pipelines or seek licensing deals to stay competitive.

Companion-Animal Spending Growth

Average U.S. household veterinary bills climbed 7.1% year on year, exceeding overall pet-care inflation at 4.2% and signaling robust price tolerance for preventive biologics. Lifestyle vaccines for kennel cough and Lyme disease gain traction as owners humanize pets and equate animal care with family health. Low insurance penetration near 3% implies untapped reimbursement potential that could further normalize higher biologics outlays, bolstering margins for firms focused on companion-animal portfolios.

mRNA Platforms Enter Veterinary Pipeline

The success of human mRNA vaccines during COVID-19 spurred animal-health adaptations. Zoetis and partners advance mRNA candidates targeting respiratory pathogens in cattle, promising faster antigen updates than cell-culture or egg-based processes. Lipid-nanoparticle reformulations improve thermostability, easing cold-chain strain in remote farming zones. Scalable micro-bioreactor production reduces facility footprints, potentially lowering barriers for mid-tier biotech entrants while forcing larger manufacturers to modernize capacity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Multi-Region Licensure & Batch-Release Fees

Multi-Region Licensure & Batch-Release Fees

| -0.9% | Highest in EU and Japan | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Highest in EU and Japan

|

Impact Timeline

:

Long term (≥ 4 years)

|

High Cold-Chain & Lyophilization Costs

High Cold-Chain & Lyophilization Costs

| -0.6% | Global; most acute in developing economies | Medium term (2-4 years) | |||

Patent Thickets Around Novel Adjuvants Slow Entrants

Patent Thickets Around Novel Adjuvants Slow Entrants

| -0.4% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

Bio-Manufacturing Capacity Diverted to Human Biologics

Bio-Manufacturing Capacity Diverted to Human Biologics

| -0.3% | Global, most severe during health emergencies | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Multi-Region Licensure & Batch-Release Fees

Application charges of USD 581,735 per product in the U.S. and duplicate validation studies in Europe or Japan multiply development budgets by up to five times versus single-market filings. Batch-release testing can add USD 100,000 per lot[3]Federal Register, “Animal Drug User Fee Rates and Payment Procedures for Fiscal Year 2025,” federalregister.gov, slowing launches for innovative modalities such as mRNA where regulatory precedents are limited. Smaller firms often out-license candidates rather than shoulder these hurdles, concentrating leverage among large companies that can amortize compliance overhead across extensive portfolios.

High Cold-Chain & Lyophilization Costs

Temperature-controlled logistics raise distribution expenses by up to 60% compared with ambient-stable drugs. Installing a single lyophilizer can cost USD 5 million and entails 24-month lead times, restricting surge capacity during disease outbreaks. When human vaccine demand surges, shared facilities pivot, squeezing veterinary lines. Manufacturers pursue thermostable formulations, but reformulation requires new stability data and regulatory resubmission, delaying time-to-market for cost-sensitive regions.

Segment Analysis

By Product Type: Vaccines capture growth while retaining leadership

The vaccines segment held 78.02% of the veterinary biologics market share in 2025 and maintained the fastest 6.33% CAGR through 2031. Robust performance reflects broad immunization mandates and ongoing platform upgrades from traditional live and killed products to recombinant, vector, and mRNA constructs. Vaccines remain the backbone of livestock health programs, yet companion-animal protocols for lifestyle diseases enlarge total addressable demand. Antisera and immunoglobulins continue to serve post-exposure treatment niches but contribute limited incremental growth. Diagnostic kits register steady uptake as surveillance programs widen; however, revenue contribution stays modest compared with therapeutic categories. Bacterins gain attention in aquaculture and poultry where antibiotic-resistance concerns intensify preventive strategies. Immunomodulators, including cytokine enhancers and probiotics, draw pet-owner interest for holistic wellness offerings. The “others” bucket houses early-stage cell and gene therapies that could redefine prophylaxis but remain marginal within the current veterinary biologics market.

Second-generation vaccine modalities support premium price realization. Recombinant antigens cut contamination risk, vector vaccines stimulate cellular immunity crucial for complex pathogens, and mRNA candidates promise rapid strain matching. These advances let manufacturers position upgraded products as cost-effective over an animal’s lifespan, strengthening reimbursement arguments as insurers slowly expand companion-animal coverage. Elanco’s agreement with Medgene to commercialize highly pathogenic avian influenza vaccines underscores how incumbents partner to bridge pipeline gaps and respond to emergent threats. Growing interest in polyvalent combinations simplifies handling for producers and companion-animal clinics, further cementing the primacy of vaccines within the veterinary biologics market.

Note: Segment shares of all individual segments available upon report purchase

By Animal Type: Companion animals outpace livestock momentum

Livestock retained 58.35% of the veterinary biologics market size in 2025, anchored by compulsory vaccination protocols that safeguard trade access and food safety. Producers rely on bulk multivalent vaccines to control endemic diseases, ensuring dependable baseline demand. Growth, however, moderates as farm margins press down on per-head spending, and biologics remain a regulated input cost. In contrast, companion animals expand at an 7.92% CAGR as owners equate pet welfare with household health. Premium formulations addressing lifestyle diseases command higher price points, buoyed by willingness to pay for perceived quality-of-life enhancements.

Urbanization in advanced economies lifts dog and cat ownership densities, pushing veterinary consultations up and creating recurring revenue for booster programs. Equine biologics add a high-value but niche layer, tied to racing and breeding economics. Zoetis reported 14% year-on-year growth in companion-animal sales in 2025, triple the livestock rate, illustrating the segment divergence. The trajectory suggests manufacturers will progressively skew R&D budgets toward companion-animal indications, seeking margin expansion while maintaining foundational livestock lines.

By Distribution Channel: Digital platforms reshape procurement

Veterinary hospitals accounted for 44.86% of the veterinary biologics market in 2025, leveraging clinician trust and the need for professional administration of many biologics. Yet e-commerce pharmacies exhibit a 8.86% CAGR to 2031 as practices and owners embrace online ordering for routine vaccines and refills. Price transparency, auto-shipping, and doorstep delivery ease purchasing friction, especially for clinics serving dispersed farming communities. Veterinary clinics, smaller than hospitals, operate hybrid models, adopting digital wholesalers for commodity lines while retaining direct sales representatives for high-touch products.

Retail chains integrate veterinary corners to lift foot traffic, exemplified by Tractor Supply’s acquisition of Allivet, which broadens reach into prescription-only pet medicines. This omnichannel reality forces manufacturers to segment go-to-market strategies, balancing volume growth via web platforms with the clinical support demanded by complex biologics. E-commerce penetration remains lower in emerging markets where regulatory clarity on prescription fulfilment is evolving, but mobile connectivity could accelerate uptake, expanding the overall veterinary biologics market.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Inactivated vaccines secure share gains

Live attenuated products held 42.65% share of the veterinary biologics market in 2025, favored for robust immunogenicity. Nevertheless, inactivated vaccines grow fastest at 8.61% CAGR owing to safety, cold-chain, and production advantages. Heat-killed and chemically inactivated antigens simplify biosafety requirements, facilitating manufacture in lower-containment facilities. Subunit and recombinant constructs further refine antigen presentation, reducing adverse-event risk and aligning with welfare expectations. DNA and RNA technologies, though nascent, showcase powerful scalability and speed for variant adaptation, aligning with One Health preparedness initiatives.

Vector platforms retain a critical role where dual humoral–cellular immunity is vital. Regulatory guidance from the FDA on recombinant protein products clarifies dossier expectations, streamlining approvals and encouraging broader adoption. Cost-efficiency will increasingly govern platform choice as manufacturers weigh yield, facility reuse, and supply consistency. As a result, technology diversity will coexist, allowing the veterinary biologics market to match pathogen complexity with tailored solutions.

Geography Analysis

North America controlled 37.92% of the veterinary biologics market share in 2025 while advancing at a 5.72% CAGR through 2031. Demand draws strength from entrenched vaccination policies, high pet-ownership rates, and innovation ecosystems clustered around pharmaceutical hubs. The 2025 National One Health Framework elevates strategic stockpiles for zoonotic threats, guaranteeing volume off-take for prioritized products. Canada extends similar mandates, and integration with U.S. meat supply chains propagates biologics adoption standards south into Mexico, where commercial cattle operations expand cold-chain coverage, underpinning future uptake.

Europe registers a 5.97% CAGR, propelled by harmonized regulations and accelerated approvals. The EMA’s authorization of six biotechnological vaccines in 2024 signals regulatory appetite for advanced modalities. Germany and the United Kingdom drive premium companion-animal demand, while France and Italy contribute steady livestock consumption. Spain benefits from agricultural modernization funds that integrate disease-control programs, and Eastern European members implement EU export-compliance vaccination regimes, enlarging addressable volumes.

Asia-Pacific represents the most dynamic territory, growing 8.08% annually as China and India intensify livestock operations and urban middle classes fuel veterinary clinic expansions. African swine fever recovery programs in China accelerate bulk hog vaccine orders, while India’s urban pet ownership supports double-digit biologics sales growth. Mature markets such as Japan and Australia command high per-animal spend and quickly adopt novel technologies. Regional manufacturing capacity draws foreign direct investment owing to cost efficiency, reinforcing supply security and lowering landed costs for local distributors, thereby enlarging the regional veterinary biologics market size.

Competitive Landscape

Market Concentration

The veterinary biologics market is moderately consolidated. Zoetis, Boehringer Ingelheim, and Merck Animal Health anchor global supply through expansive catalogs that cover core livestock and companion-animal needs. These companies extend vertical integration by investing in raw-material sourcing and fill-finish capacity to shield margins from supply disruptions. Capital expenditure trends are visible in Merck’s USD 895 million Kansas expansion announced in May 2025, which scales bulk antigen production and adds dedicated R&D laboratories.

Innovation pipelines pivot to mRNA, vector, and AI-enabled discovery. Large players form development partnerships with smaller biotech firms to access platform know-how while leveraging regulatory expertise and global distribution. Elanco’s deal with Medgene for highly pathogenic avian influenza vaccine commercialization shows the blend of startup agility and incumbent reach. Patent estates on adjuvant systems and delivery technologies create competitive moats, while biosimilar opportunities may open after key patent expiries post-2030. Regional players, particularly in India and China, pursue cost-advantage strategies in inactivated and conventional vaccines, challenging global brands in local tenders.

Manufacturers increasingly differentiate through service models: predictive analytics for disease-outbreak forecasting, on-farm vaccination compliance dashboards, and remote cold-chain monitoring. These value-added layers deepen customer lock-in and complement product offerings. Competitive intensity continues to rise as e-commerce channels broaden access, pressuring list prices for commoditized antigens but simultaneously expanding the absolute size of the veterinary biologics market by tapping underserved geographies.

Veterinary Biologics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Merck Animal Health announced a USD 895 million investment to expand its biologics manufacturing facility in De Soto, Kansas, including USD 35 million for new R&D laboratories.

- February 2025: Elanco Animal Health entered an agreement with Medgene to commercialize a highly pathogenic avian influenza vaccine for dairy cattle.

- February 2025: Biovet, part of the Bharat Biotech group, secured CDSCO approval for Biolumpivaxin, a lumpy skin disease vaccine for cattle and buffaloes.

- May 2024: The NSW Government reported successful pilot production of an mRNA vaccine against the border disease virus manufactured at the UNSW RNA Institute in Sydney.

Table of Contents for Veterinary Biologics Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Robust Livestock & Companion-Animal Vaccination Mandates

- 4.2.2Surge in Recombinant & Vector-Based Vaccine Approvals

- 4.2.3Companion-Animal Spend Outpaces Overall Pet-Care Inflation

- 4.2.4mRNA Platforms Enter Veterinary Pipeline Post-Covid-19

- 4.2.5AI-Driven Antigen Discovery Cuts Development Timelines

- 4.2.6One-Health Stockpile Funding for Transboundary Diseases

- 4.3Market Restraints

- 4.3.1Stringent Multi-Region Licensure & Batch-Release Testing

- 4.3.2High Cold-Chain & Freeze-Dry Capacity Costs

- 4.3.3Patent Thickets Around Novel Adjuvants Slow Entrants

- 4.3.4Bio-Manufacturing Capacity Diverted to Human Biologics

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Industry Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Antisera & Immunoglobulins

- 5.1.2Bacterins

- 5.1.3Diagnostic Kits

- 5.1.4Immunomodulators

- 5.1.5Vaccines

- 5.1.6Others

- 5.2By Animal Type

- 5.2.1Companion Animals

- 5.2.2Livestock Animals

- 5.2.3Other Animals

- 5.3By Distribution Channel

- 5.3.1Veterinary Hospitals

- 5.3.2Veterinary Clinics

- 5.3.3Retail and Online

- 5.4By Technology

- 5.4.1Live Attenuated

- 5.4.2Inactivated / Killed

- 5.4.3Sub-unit & Recombinant

- 5.4.4DNA / RNA

- 5.4.5Vector-based

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Competitive Benchmarking

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1AniCura Group

- 6.4.2Biogénesis Bagó

- 6.4.3Boehringer Ingelheim Animal Health

- 6.4.4Ceva Santé Animale

- 6.4.5Dechra Pharmaceuticals

- 6.4.6Elanco Animal Health

- 6.4.7Hester Biosciences

- 6.4.8HIPRA

- 6.4.9Huvepharma

- 6.4.10Indian Immunologicals Ltd.

- 6.4.11Laboratorio Avi-Mex S.A. de C.V.

- 6.4.12Meiji Animal Health

- 6.4.13Merck & Co., Inc.

- 6.4.14Ourofino Saúde Animal

- 6.4.15Phibro Animal Health Corporation

- 6.4.16Vaxxinova International BV

- 6.4.17Vetoquinol S.A.

- 6.4.18Virbac S.A.

- 6.4.19WuXi Biologics

- 6.4.20Zoetis Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Veterinary Biologics Market Report Scope

As per the report’s scope, veterinary biologics are products developed to diagnose, manage, or prevent animal diseases. These include vaccines, antibody-based treatments, and diagnostic test kits. Derived from living organisms and biological processes, veterinary biologics function through immunological mechanisms.

The veterinary biologics market is segmented by product type, animal, and distribution channel. By product type, the market has been segmented into vaccines, bacterins, antisera, diagnostic kits, others. Others include growth promoters & allergenic extracts. Based on animal, the market is segmented into companion animals, livestock, and equine. Companion animals have been further segmented into canine, avian, and feline. Livestock segment have been segmented into aquatic, bovine, porcine, ovine, and poultry. By distribution channel, the market covers veterinary clinics, veterinary hospitals, and retail pharmacies. Geographically, the market includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report details market size and forecasts for 17 countries across these regions, with valuations presented in USD.