Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

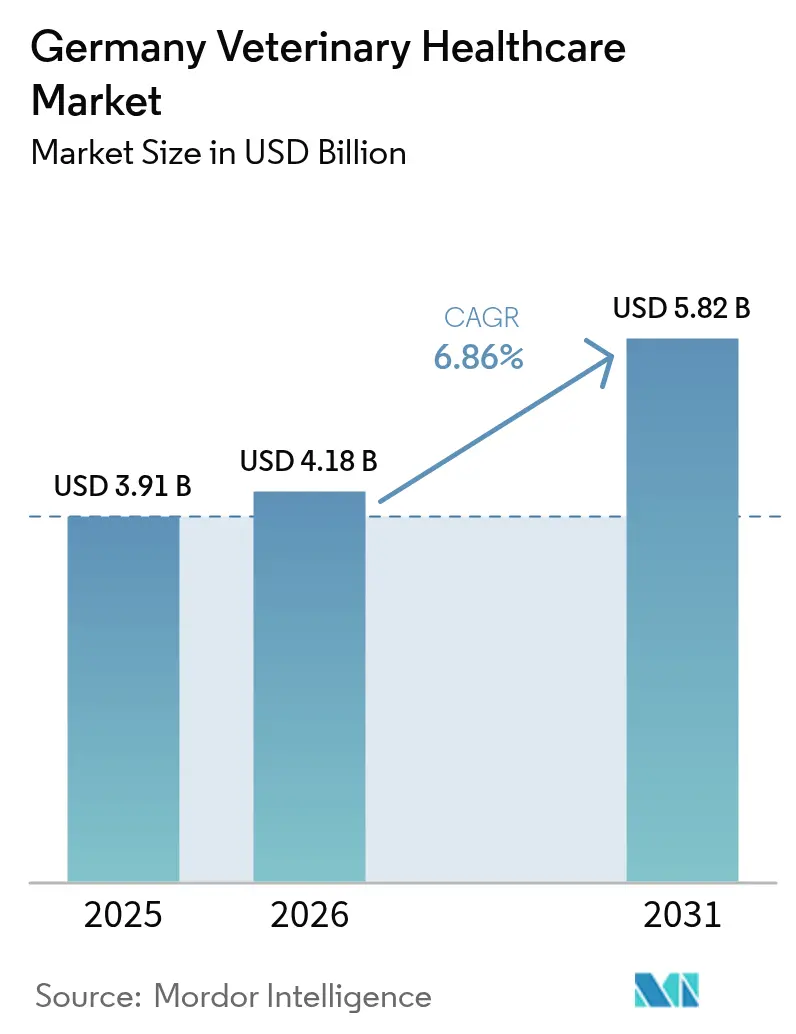

| Base Year Market Size (2025) | USD 3.91 Billion |

| Market Size (2026) | USD 4.18 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 6.86% CAGR |

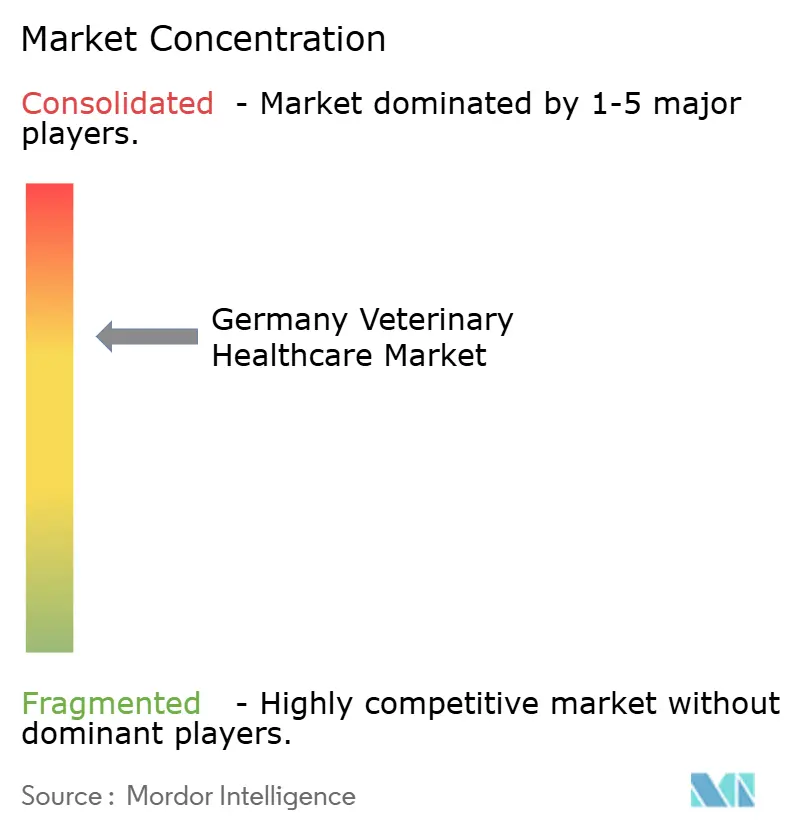

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Veterinary Healthcare Market Analysis by Mordor Intelligence

Germany veterinary healthcare market size in 2026 is estimated at USD 4.18 billion, growing from 2025 value of USD 3.91 billion with 2031 projections showing USD 5.82 billion, growing at 6.86% CAGR over 2026-2031. Steady companion-animal ownership, stricter livestock health mandates and rapid diagnostic innovation sustain this expansion. A pet population of 33.9 million animals underpins recurrent demand, while increasing zoonotic threats and the first domestic foot-and-mouth disease case since 1988 reinforce the need for robust preventive programs. Digital tools such as AI-powered hematology analyzers and teleconsultation platforms improve practice efficiency and support rural coverage gaps. Corporate consolidation among manufacturers accelerates product rollouts, and rising pet insurance uptake broadens affordability for higher-value care. However, workforce shortages and mandatory fee schedules temper near-term growth momentum.

Key Report Takeaways

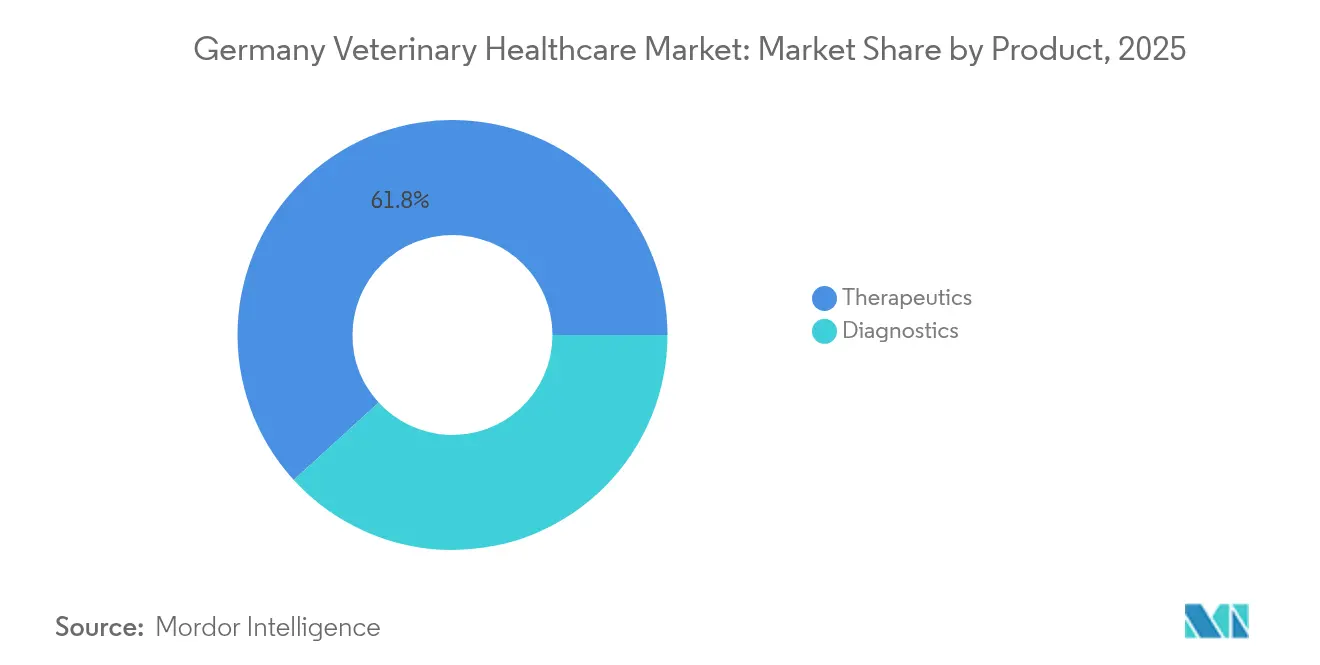

- By product type, therapeutics led with 61.78% Germany veterinary healthcare market share in 2025, while diagnostics are projected to expand at a 7.42% CAGR through 2031.

- By animal type, dogs and cats accounted for 46.02% of Germany veterinary healthcare market size in 2025; poultry is set to grow at a 6.88% CAGR to 2031.

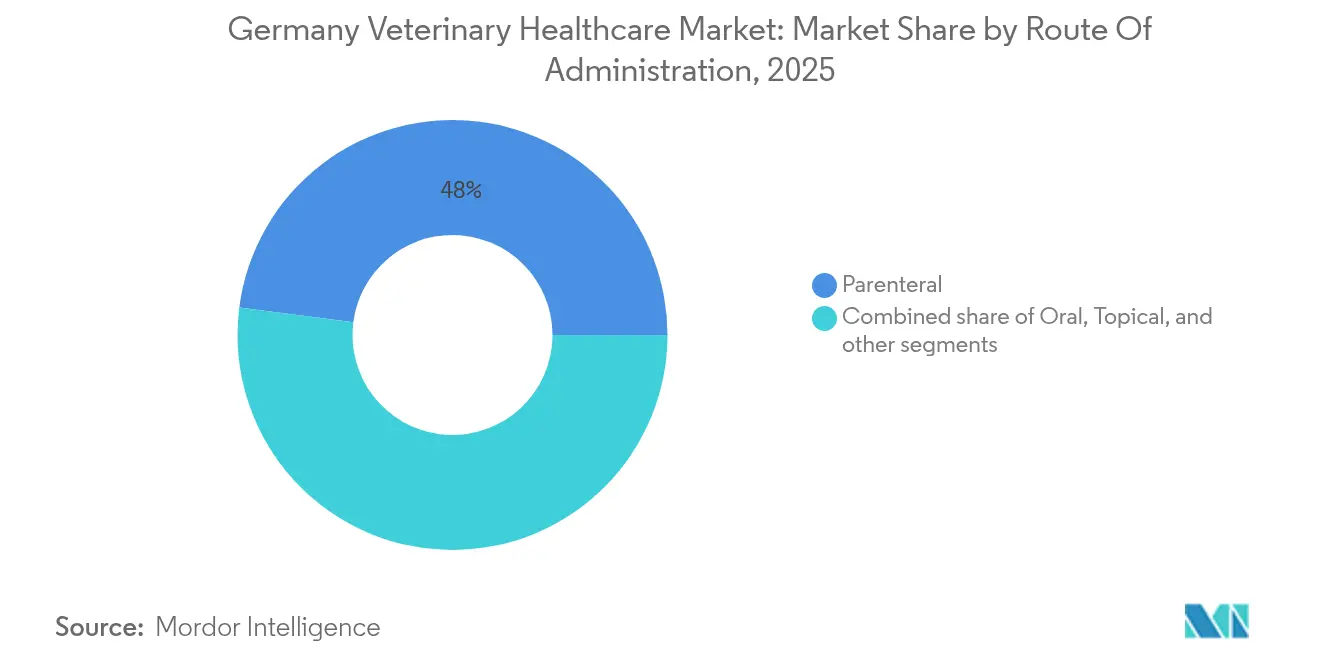

- By route of administration, parenteral formulations held 47.95% Germany veterinary healthcare market share in 2025, whereas oral products are advancing at a 6.58% CAGR.

- By end user, hospitals and clinics commanded 57.12% Germany veterinary healthcare market size in 2025; point-of-care testing settings show the fastest trajectory at 7.71% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Veterinary Healthcare Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in companion animal population | +1.2% | Urban centers nationwide | Medium term (2-4 years) |

| Rise in zoonotic disease incidence | +0.8% | National with rural focus | Short term (≤2 years) |

| Government animal health initiatives | +0.6% | Nationwide, EU-aligned | Long term (≥4 years) |

| Advancements in veterinary diagnostics and telehealth | +1.1% | Metropolitan areas | Medium term (2-4 years) |

| Expansion of pet insurance coverage | +0.4% | Nationwide | Long term (≥4 years) |

| Shift toward preventive livestock care | +0.7% | Intensive farming regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Companion Animal Population

Rising pet ownership supports continuous service demand as 44% of German households kept at least one animal in 2024[1]Zentralverband Zoologischer Fachbetriebe, “Domestic Animal Statistics 2024,” zzf.de. Generational shifts position pets as family members, prompting willingness to pay for advanced treatments. Singles and couples in urban apartments boost per-capita spending, and post-pandemic adoption rates among families with children anchor long-term growth. This environment sustains specialty clinics, oncology services and nutrition counseling.

Rise in Zoonotic Disease Incidence

Climate change and cross-border trade intensify pathogen spread. Vector-borne threats such as Lyme borreliosis, affecting up to 200,000 people yearly, push owners toward tick preventives[2]Robert Koch-Institut, “Vector-borne Diseases in Germany,” rki.de. Schmallenberg seroprevalence jumped to 40.15% in 2023, underscoring viral unpredictability. The January 2025 foot-and-mouth outbreak triggered rapid containment, illustrating how one event reverberates across supply chains. Robust surveillance and vaccination programs therefore gain priority.

Government Animal Health Initiatives

Implementation of the Veterinary Medicinal Products Act aligns national policy with EU Regulation 2019/6, targeting a 50% antibiotic-use reduction by 2030. DART 2030 harmonizes human-animal antimicrobial stewardship, and mandatory herd-health management lifts dairy yields to 10,195 kg per cow. Federal funding for the Hannover skills lab strengthens clinical training capacity, mitigating workforce shortages.

Advancements in Veterinary Diagnostics and Telehealth

Point-of-care tools from Zoetis provide reference-lab quality hematology in minutes, shortening decision cycles. AI cytology systems streamline lymph-node screening, and wearable sensors derive real-time vitals without restraint. Teleconsult uptake remains modest due to legal ambiguity, yet remote follow-ups reduce clinic congestion and expand rural reach.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced veterinary care | -0.9% | Strongest in rural areas | Medium term (2-4 years) |

| Stringent regulatory approval process | -0.5% | Nationwide, EU oversight | Long term (≥4 years) |

| Shortage of skilled veterinary professionals | -0.7% | Rural and small-city clinics | Short term (≤2 years) |

| Ethical concerns over animal testing in R&D | -0.3% | Nationwide, academic hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Veterinary Care

Mandatory fee revisions raised procedure prices by roughly 50% in 2022, straining budgets despite quality benefits. Limited insurance penetration means owners self-finance surgeries and MRI scans, sometimes deferring care. Livestock producers weigh premium vaccines against thin margins, and escalating student debt discourages clinic startups in low-income districts, sustaining access disparities.

Stringent Regulatory Approval Process

Dual authority oversight requires extensive dossiers and pharmacovigilance reporting, extending time-to-market for novel drugs. Smaller manufacturers shoulder disproportionate costs, often partnering with larger firms or exiting. New PFAS guidelines for feed additives introduce additional data demands, while antimicrobial-reduction targets mandate expensive reformulations before launch.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutics Dominate Amid Diagnostics Innovation

Therapeutics contributed 61.78% of Germany veterinary healthcare market size in 2025, anchored by vaccines and parasiticides. Poultry immunizations against Marek’s disease and avian influenza remain critical, and targeted antiparasitics protect companion animals from vector-borne diseases. Anti-infectives face volume curbs but benefit from premium pricing for last-resort molecules. Medical feed additives provide non-antibiotic growth support across swine and broilers.

Diagnostics, expanding at 7.42% CAGR, capture value from molecular panels that match therapies to BRAF or KIT mutations in canine cancers. AI-assisted imaging increases radiograph throughput, while on-farm PCR kits satisfy rapid outbreak containment rules. This convergence of regulatory demand and technology fuels segment acceleration.

By Animal Type: Companion Animals Lead While Poultry Accelerates

Dogs and cats maintained 46.02% Germany veterinary healthcare market share in 2025, reflecting high household penetration and willingness to fund specialty oncology or orthopedic interventions. Feline-specific anxiety therapies such as pregabalin oral solutions intend to close the care gap where only 40% of cats visit clinics annually.

Poultry, forecast to grow at 6.88% CAGR, responds to dense production environments needing comprehensive vaccination and water-quality oversight. H5N1 events have validated investment in multivalent vaccines, and PFAS-free feed additives gain traction to meet export standards.

By Route of Administration: Parenteral Dominance Challenged by Oral Innovation

Injectables held 47.95% Germany veterinary healthcare market share in 2025, valued for dose accuracy and fast onset in herd-health campaigns. Monoclonal antibodies such as bedinvetmab exemplify premium parenterals with documented safety from 25 million global doses.

Oral delivery, rising at 6.58% CAGR, capitalizes on owner preference for stress-free administration. Longevity tablets targeting canine metabolic decline and palatable suspensions for feline anxiety epitomize this convenience trend. In livestock, medicated feed offers scalable distribution while complying with new residue limits.

By End User: Hospitals Dominate While Point-of-Care Testing Surges

Hospitals and clinics captured 57.12% Germany veterinary healthcare market size in 2025, providing surgical suites and imaging. Workforce shortages—affecting 78.5% of European countries—propel consolidation under corporate groups capable of cross-regional staffing.

Point-of-care settings, advancing at 7.71% CAGR, integrate cartridge-based CBC analyzers that run 90-second panels, cutting external lab costs. Rural mobile clinics employ these devices to deliver immediate treatment plans, raising standards without brick-and-mortar expansion.

Geography Analysis

Germany anchors Europe’s largest companion-animal economy with EUR 7 billion in 2024 sales. Urban corridors such as Berlin-Hamburg host dense clinic networks, whereas low veterinarian density in eastern rural districts necessitates telehealth and mobile units. Federal surveillance infrastructure, including the Friedrich-Loeffler-Institut, coordinates rapid antigen bank deployment during outbreaks. National antimicrobial sales fell from 89.2 mg/PCU in 2016 to 69.9 mg/PCU in 2022, positioning Germany as a regional benchmark. Cross-border alignment with EU One-Health programs facilitates sharing of genomic pathogen data, strengthening predictive analytics.

Competitive Landscape

Germany’s veterinary healthcare market remains moderately consolidated, with the Bundesverband für Tiergesundheit’s 25 member companies controlling more than 90% of national sales. Market leadership rests with multinational firms such as Zoetis, Boehringer Ingelheim, Elanco and Ceva that benefit from extensive product portfolios and established distribution networks. Their scale supports sustained R&D spending, helping them navigate Germany’s dual-agency approval system and maintain high entry barriers for smaller rivals.

Technology adoption has become the primary competitive lever. Zoetis introduced AI-powered point-of-care hematology and cytology platforms that shorten diagnostic turnaround times and deepen clinic relationships. Boehringer Ingelheim expanded its vaccine pipeline by acquiring Saiba Animal Health, underscoring a strategic shift toward biologics for chronic pet diseases. Start-ups such as Loyal target niche opportunities, including longevity therapeutics for senior dogs, highlighting white-space areas that incumbents are now watching closely.

Practice ownership is slowly corporatizing: 16% of European veterinarians now work in consolidated groups, though Germany trails the UK’s penetration rate. Corporate chains leverage group purchasing and centralized digital records to improve margins while addressing rural staffing gaps created by nationwide veterinarian shortages. Strict antimicrobial-reduction targets and new PFAS feed regulations further favor well-capitalized players that can fund reformulations and compliance systems. Overall, the competitive field rewards scale, regulatory expertise and rapid integration of digital tools.

Germany Veterinary Healthcare Industry Leaders

Boehringer Ingelheim International GmbH

Zoetis, Inc

Elanco Animal Health

Ceva Animal Health

Vetoquinol S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zoetis reported Librela’s clinical trial results showing equivalent pain relief to meloxicam with fewer adverse events.

- February 2025: Elanco and Medgene agreed to co-market an H5N1 dairy-cattle vaccine targeting North American and potential EU demand.

- January 2025: Germany confirmed its first foot-and-mouth disease outbreak since 1988 in Brandenburg water buffaloes.

- September 2025: Zoetis launched the Vetscan OptiCell cartridge-based AI hematology analyzer.

- December 2024: Loyal’s LOY-002 received FDA confirmation of reasonable effectiveness for age-related canine therapies.

Germany Veterinary Healthcare Market Report Scope

As per the scope of the report, veterinary healthcare comprises the products used in the diagnosis and treatment of diseases in animals.

The Germany Veterinary Healthcare Market is Segmented by Product (Therapeutics (Vaccines, Parasiticides, Anti-infectives, Medical Feed Additives, and Other Therapeutics) and Diagnostics (Immunodiagnostic Tests, Molecular Diagnostics, Diagnostic Imaging, Clinical Chemistry, and Other Diagnostics), and Animal Type (Dogs and Cats, Horses, Ruminants, Swine, Poultry, and Other Animals). The report offers value (in USD million) for the above segments.

By Product

| By Therapeutics | Vaccines |

| Parasiticides | |

| Anti-infectives | |

| Medical Feed Additives | |

| Other Therapeutics | |

| By Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Clinical Chemistry | |

| Other Diagnostics |

By Animal Type

| Dogs and Cats |

| Horses |

| Ruminants |

| Swine |

| Poultry |

| Other Animals |

| By Product | By Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-infectives | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| By Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Clinical Chemistry | ||

| Other Diagnostics | ||

| By Animal Type | Dogs and Cats | |

| Horses | ||

| Ruminants | ||

| Swine | ||

| Poultry | ||

| Other Animals | ||

Key Questions Answered in the Report

How large is the Germany veterinary healthcare market in 2026?

The sector is valued at USD 4.18 billion in 2026 and is projected to reach USD 5.82 billion by 2031.

Which segment holds the biggest share of spending?

Therapeutic products, mainly vaccines and parasiticides, hold 61.78% of total outlays in 2025.

What growth rate is expected for diagnostics?

Diagnostics are forecast to post a 7.42% CAGR through 2031 as AI and point-of-care tools gain traction.

Why is poultry healthcare a focus area?

Intensive production systems and recurring avian influenza outbreaks push poultry to the fastest segment growth at 6.88% CAGR.

How are workforce shortages being addressed?

Clinics increasingly deploy telemedicine and AI diagnostics, and universities have expanded simulation labs to accelerate graduate readiness.

Page last updated on: