Veterinary Ultrasound Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 515.64 Million |

| Market Size (2031) | USD 724.90 Million |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

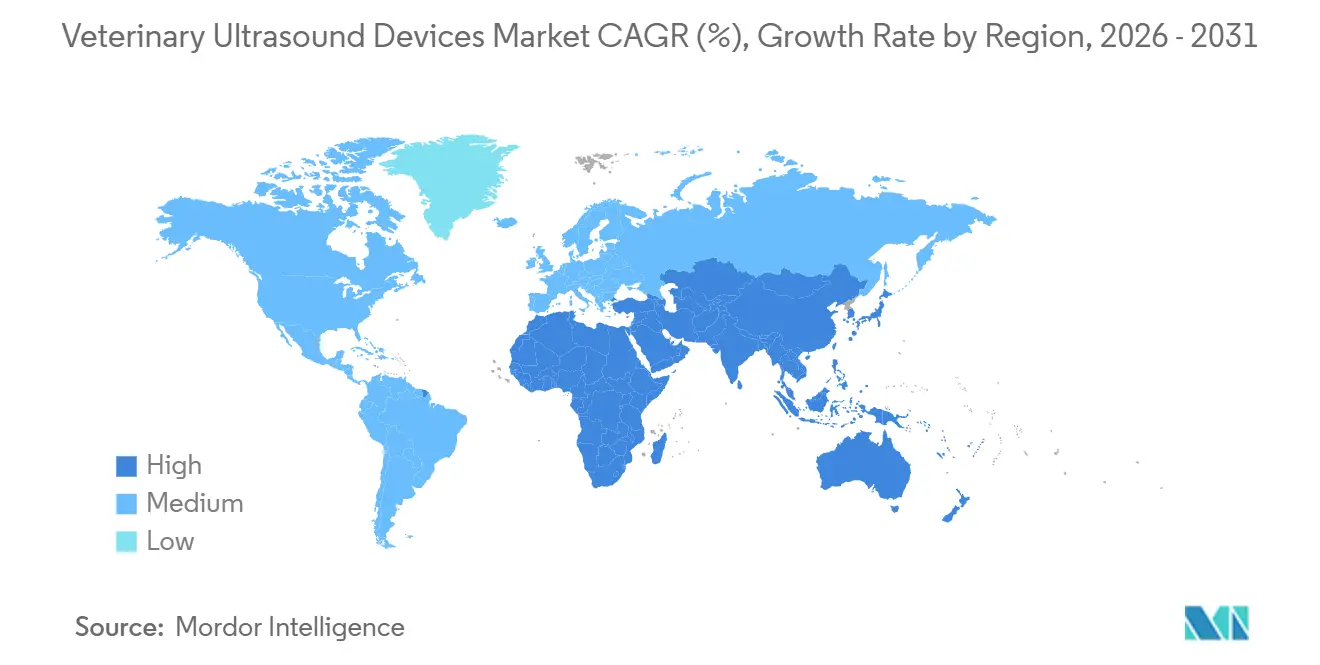

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

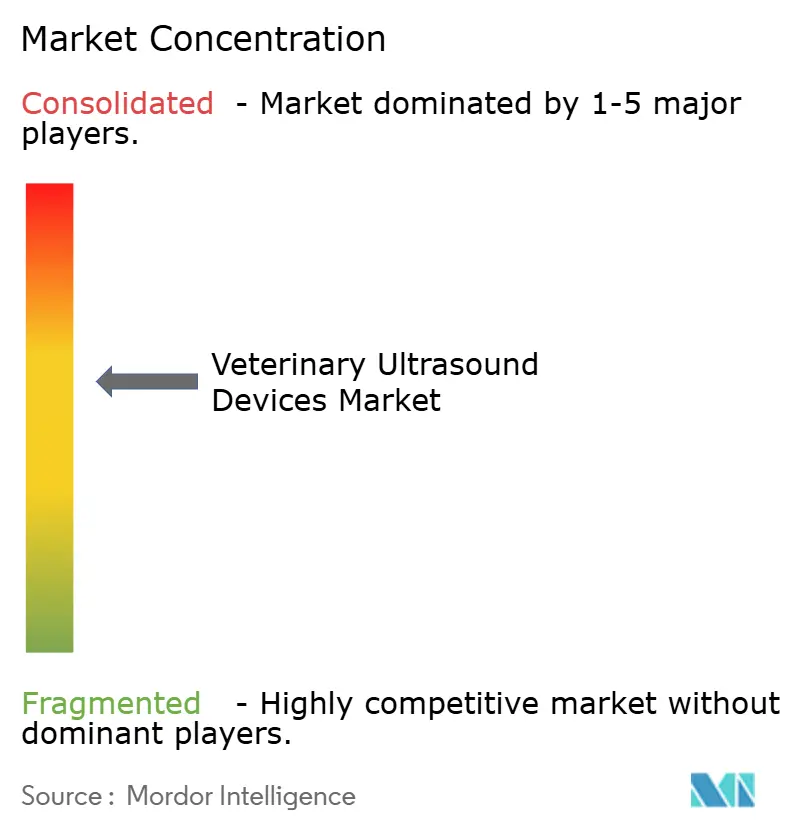

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Ultrasound Devices Market Analysis by Mordor Intelligence

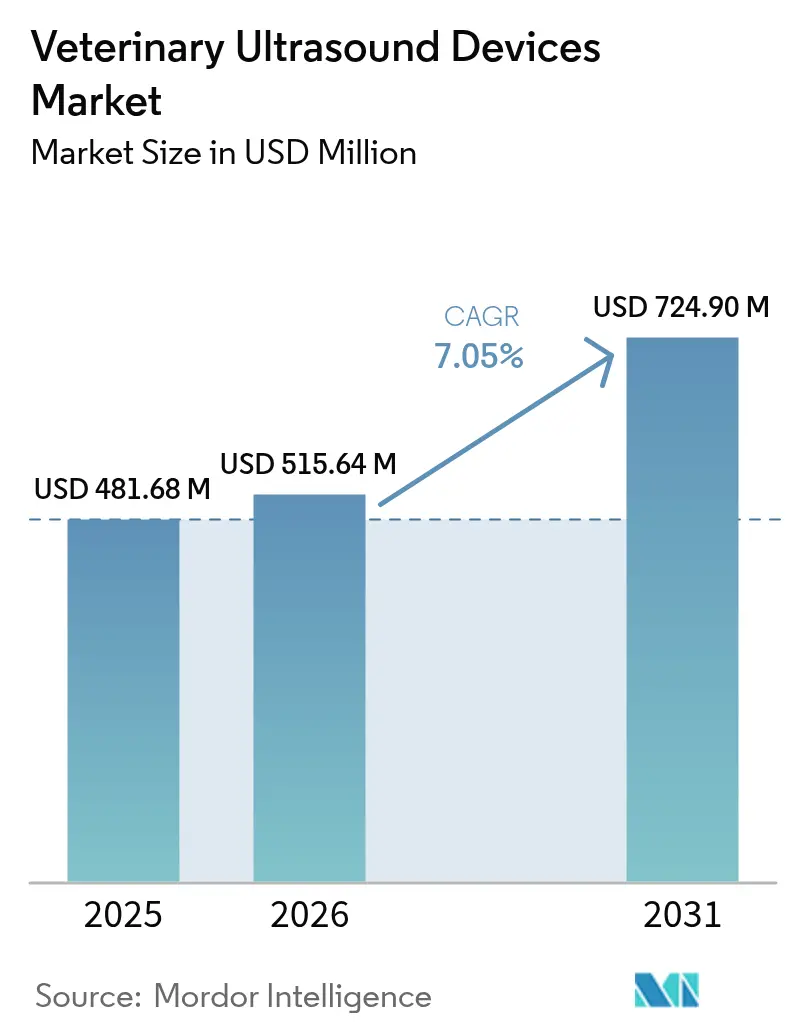

The Veterinary Ultrasound Devices Market size is expected to increase from USD 481.68 million in 2025 to USD 515.64 million in 2026 and reach USD 724.90 million by 2031, growing at a CAGR of 7.05% over 2026-2031.

Rising pet healthcare spending, corporate consolidation of primary-care clinics, and lower-cost handheld probes are broadening access to point-of-care imaging in companion animals. Livestock producers rely on ultrasound to tighten breeding intervals, and demand for Doppler platforms is escalating as cardiology protocols become routine in dogs, cats, and performance horses. The European Union’s Cyber Resilience Act is already shaping product roadmaps by mandating long-term software support, a requirement that favors vendors with established cybersecurity teams. Meanwhile, subscription and leasing options are easing capital barriers for small practices, keeping replacement cycles brisk even in price-sensitive regions.

Key Report Takeaways

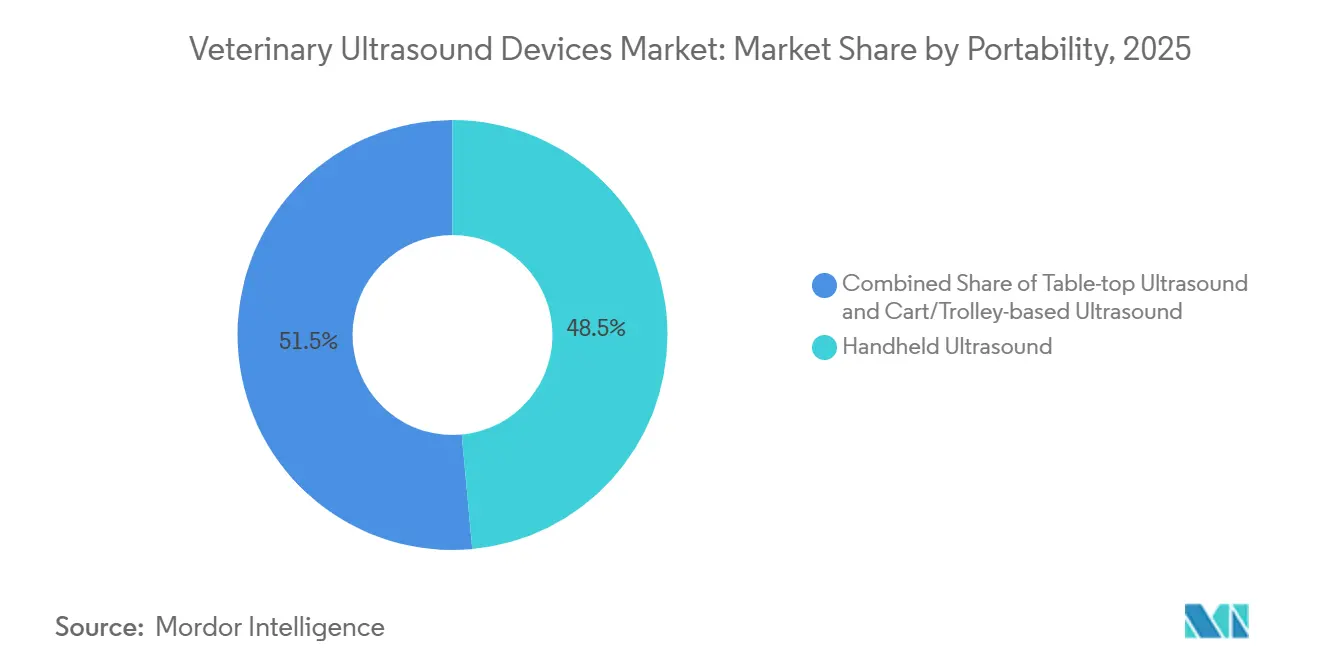

- By portability, cart-based systems led the veterinary ultrasound devices market with 48.53% market share in 2025, while handheld devices posted the highest CAGR at 9.43% through 2031.

- By technology, two-dimensional platforms held 56.92% of the veterinary ultrasound devices market in 2025, yet Doppler units are forecast to expand at a 9.32% CAGR through 2031.

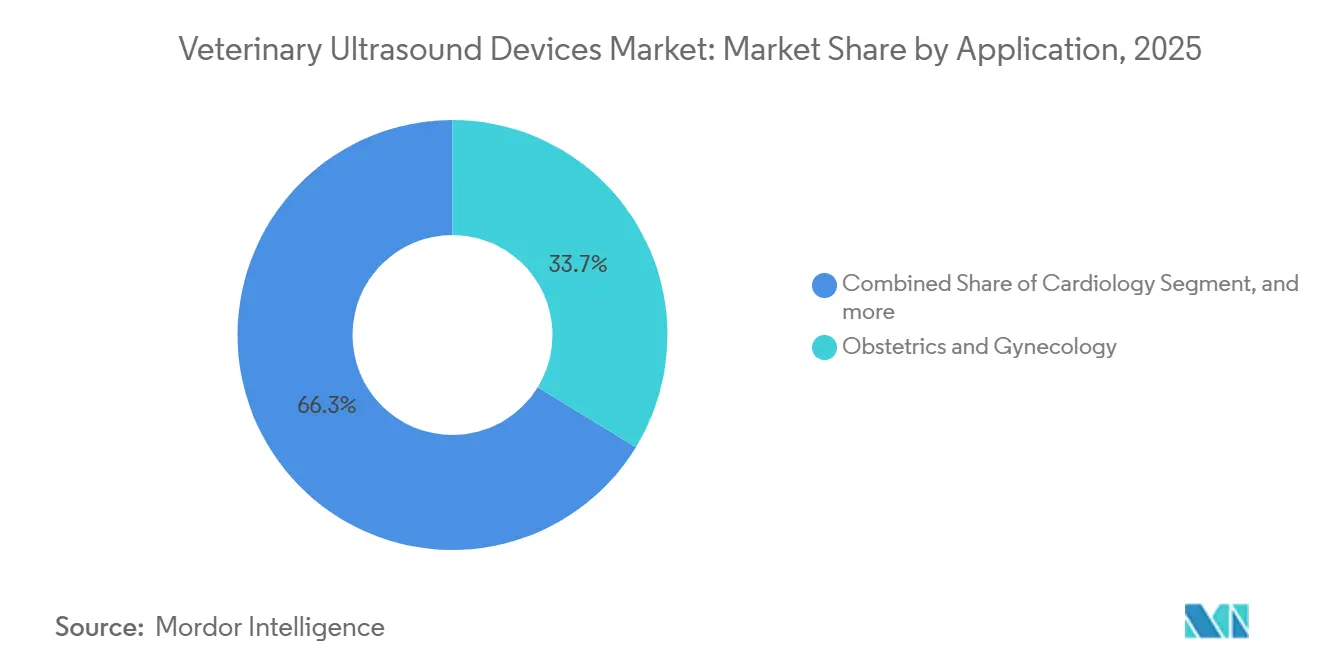

- By application, obstetrics and gynecology accounted for 33.74% of revenue in 2025, whereas cardiology is advancing at a 10.55% CAGR over 2026-2031.

- By animal type, livestock accounted for 52.98% of the veterinary ultrasound devices market size in 2025, while companion animals registered the fastest 9.54% CAGR to 2031.

- By end user, veterinary hospitals held a 60.54% share in 2025, yet clinics are growing the fastest at a 10.43% CAGR thanks to point-of-care adoption.

- By geography, North America led with a 42.54% share in 2025, though Asia-Pacific is set to grow at an 8.54% CAGR because of government-backed livestock biotech programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Companion Animal Healthcare Expenditure | +1.8% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Increasing Adoption of Handheld Ultrasound Devices | +1.5% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Technological Advancements in Veterinary Ultrasound Imaging | +0.9% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Growing Demand for Reproductive Monitoring in Intensive Livestock Farming | +1.0% | Dairy and beef regions worldwide | Long term (≥ 4 years) |

| Emergence of Subscription-Based Ultrasound Equipment Models | +0.8% | North America, Europe, Australia, urban Latin America | Short term (≤ 2 years) |

| Integration of Artificial Intelligence and Tele-Ultrasound Workflows | +1.2% | North America, Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Healthcare Expenditure

Pet owners in the United States spent USD 38.3 billion on veterinary care in 2023, and insured pets undergo 2.4 times more imaging than uninsured cohorts[1]American Veterinary Medical Association, “U.S. Veterinary Workforce Study 2024,” avma.org. Corporate groups now own more than one-quarter of U.S. clinics, enabling fleet procurement and standardized ultrasound protocols. Elective abdominal and cardiac scans for geriatric pets are increasingly routine, yet the 2024 decline in clinic visits shows that discretionary imaging remains sensitive to macroeconomic pressures. Standardized vendor service contracts are helping clinics contain maintenance costs, smoothing revenue during slowdowns. The overall effect is sustained demand for affordable, easy-to-use scanners that preserve diagnostic margins even when visit volumes fluctuate.

Increasing Adoption of Handheld Ultrasound Devices

Handheld probes are expanding at a 9.43% CAGR as chip-based transducers cut manufacturing costs and shrink device footprints. Butterfly’s iQ3, cleared in January 2024, introduced automated 3D models that expedite anatomy identification for non-radiologists, while GE’s Vscan Air, distributed by Sound Technologies, brings wireless imaging to stall-side equine exams. Monthly leasing plans under USD 800 reduce upfront outlays by 80%, encouraging adoption in single-doctor clinics. Portability is most valuable in large-animal practice and in emergency cages, where cart systems are impractical, though image penetration remains limited in obese patients and in deep-abdomen scans. Continuous software upgrades delivered over Wi-Fi help practices avoid technology obsolescence during multi-year repayment schedules.

Integration of Artificial Intelligence and Tele-Ultrasound Workflows

A 2024 joint statement from the American and European Colleges of Veterinary Radiology endorsed AI tools as accuracy enhancers when a trained clinician oversees final interpretation. Butterfly’s AI B-line counter cut interpretation time by 40% in dogs with pulmonary edema, standardizing results across varying skill levels. Cloud platforms now allow residency programs to meet training mandates through remote image review, widening access to specialist oversight. Cybersecurity risk is growing as ransomware groups target clinic PACS; ISO 27001 certification and the EU Cyber Resilience Act push vendors to embed security-by-design. Practices increasingly evaluate encryption, user-access controls, and patch support during procurement.

Growing Demand for Reproductive Monitoring in Intensive Livestock Farming

Ultrasound pregnancy checks as early as 28 days post-breeding shorten calving intervals by up to 15 days compared with palpation. Fetal sexing between 60 and 85 days optimizes heifer retention and cash-flow timing. Doppler scans of corpus luteum vascularization predict progesterone status, improving conception rates in timed artificial insemination. Governments in Asia-Pacific tie livestock grants to the adoption of advanced diagnostics, pushing uptake in dairy and beef operations. Nevertheless, device cost and operator scarcity keep manual methods prevalent among smallholders, leaving room for entry-level scanners coupled with remote training.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Ultrasound Systems | −0.9% | Latin America, South Asia, Africa | Medium term (2-4 years) |

| Shortage of Ultrasound-Trained Veterinary Professionals | −0.7% | Rural and underserved regions worldwide | Long term (≥ 4 years) |

| Limited Reimbursement for Large-Animal Diagnostic Imaging | −0.6% | Livestock markets in North America, Latin America, Asia-Pacific | Medium term (2-4 years) |

| Cybersecurity Concerns over Cloud-Connected Ultrasound Devices | −0.5% | North America, European Union, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Ultrasound Systems

Premium cart systems with Doppler and contrast modules range from USD 15,000 to USD 50,000, a hurdle for clinics averaging fewer than 10 scans per week. Handheld units retail for USD 3,999–8,000 but lack depth penetration for large-animal abdomen work, forcing practices to compromise between price and capability. Subscription bundles that wrap hardware, software, and service into a single monthly fee lower risk, yet rural clinics with low case volume still struggle to meet breakeven within a typical five-year term. Corporate consolidators negotiate fleet discounts, putting independent practitioners at a relative cost disadvantage.

Shortage of Ultrasound-Trained Veterinary Professionals

The American College of Veterinary Radiology underscores that image quality and interpretation remain operator-dependent and recommends credentialed oversight[2]American College of Veterinary Radiology, “Ultrasound Position Statement,” acvr.org. Pathways such as the Registered Veterinary Medical Sonographer credential require extensive human-sonography experience and 6 months of veterinary mentorship, limiting the number of graduates each year. Rural mixed-animal practices cannot justify hiring dedicated sonographers, and distance to specialists prolongs referral wait times[3]Association for Veterinary Radiology and Ultrasound, “RVMS Credential Requirements,” avru.org. AI-assisted presets help standardize acquisition, but liability concerns dissuade clinics from relying solely on algorithms, keeping human expertise in short supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Portability: Handheld Devices Gain Ground Despite Cart Dominance

Cart systems retained 48.53% veterinary ultrasound devices market share in 2025 due to superior image quality, probe diversity, and ergonomic consoles prized by referral hospitals. They remain the platform of choice for deep abdominal, cardiac, and guided interventional studies, especially in obese or large-breed dogs. Vendors bundle multi-frequency probes and integrated PACS links, ensuring compatibility with existing workflows.

Handheld devices are growing at a 9.43% CAGR as sub-USD 8,000 pricing and single-probe versatility attract primary-care clinics. The veterinary ultrasound devices market size for this segment is projected to expand steadily as subscription models allow users to upgrade to newer revisions mid-contract. Image resolution continues to improve through semiconductor transducers, and military-drop specifications make these units viable for barn calls. Limitations in penetration depth and battery life still favor carts for complex cardiology or large-animal abdomen scans.

By Technology: Doppler Ultrasound Surges as Cardiology Applications Expand

Two-dimensional systems accounted for 56.92% of revenue in 2025 because they meet routine abdominal and obstetric needs at comparatively low cost. Rapid boot times and familiar interfaces keep workflow efficient for high-volume practices. The veterinary ultrasound devices market for 2-D will continue to grow, though the share will shift incrementally to Doppler platforms.

Doppler units are advancing at a 9.32% CAGR as clinics embrace echocardiography and livestock breeders adopt blood-flow assessment of the corpus luteum. The veterinary ultrasound devices market share for Doppler is set to rise further, with vendors embedding the feature in mid-tier carts and even handheld devices. Training programs now teach Doppler basics early, broadening the user base. Three- and four-dimensional imaging remains niche, limited to teaching hospitals due to equipment cost and longer scan times, yet its volumetric data aids complex cardiac surgical planning.

By Application: Cardiology Accelerates While Obstetrics Matures

Obstetrics and gynecology accounted for 33.74% of revenue in 2025, reflecting decades of use for pregnancy confirmation and fetal viability checks in both livestock and pets. Growth is leveling in mature markets as protocols stabilize and insurance coverage normalizes fees.

Cardiology is the fastest-growing application, with a 10.55% CAGR, driven by greater screening for congenital and acquired heart diseases. Clinics add Doppler-capable handhelds to perform cage-side FAST and basic echo triage. The veterinary ultrasound devices market for cardiac use is forecast to expand rapidly as AI modules automate chamber measurements, enabling non-specialists to capture diagnostic clips. Musculoskeletal and emergency ultrasound rounds out demand, benefiting from portables that fit into tight ICU spaces.

By Animal Type: Companion Animals Gain as Livestock Dominates Volume

Livestock still accounted for 52.98% of revenue in 2025, buoyed by herd-level fertility programs that justify capital outlays through shorter calving intervals and higher conception rates. Mobile practitioners favor rugged handhelds that withstand harsh outdoor environments.

Companion animals grow at a 9.54% CAGR thanks to rising pet insurance coverage and owner willingness to pay for preventive cardiac and abdominal scans. The veterinary ultrasound devices market size for pets is therefore increasing faster than the production-animal segments. Geriatric care protocols now recommend annual echo checks in predisposed breeds, driving sustained scanner utilization in small-animal clinics.

By End User: Veterinary Clinics Outpace Hospitals as POCUS Proliferates

Referral hospitals accounted for 60.54% of revenue in 2025, supported by board-certified radiologists who operate high-end carts with Doppler, CEUS, and 3D packages. They handle complex cases and training rotations, maintaining strong replacement demand.

General clinics, however, post a 10.43% CAGR because handheld adoption enables them to retain imaging revenue rather than referring cases. The veterinary ultrasound devices market size for clinics is expanding as consolidators sign fleet contracts that bundle hardware, cloud storage, and services. Mobile services and academia form a smaller but steady niche that values durability and teaching features.

Geography Analysis

North America led with a 42.54% share in 2025, driven by high per-patient spending and early POCUS adoption. U.S. corporate groups negotiate nationwide equipment deals, boosting vendor volume for integrated archiving. Canada and Mexico are growing steadily as dairy and beef producers formalize reproductive ultrasound protocols. Inflation curtailed elective visits in 2024, but leasing plans soften budget shocks, sustaining replacement cycles.

Asia-Pacific is the fastest-growing region, with a 8.54% CAGR, underpinned by government mandates for livestock disease surveillance and expanding pet ownership in megacities. China’s vast swine and dairy sectors drive cart deployments, while Japan and South Korea favor compact Doppler units for small-animal cardiology. India’s cooperative dairies adopt portable scanners, though a shortage of trained users slows rural penetration. Australian clinics act as early adopters, trialing AI modules before regional rollout.

Europe maintains solid demand, spurred by stringent animal welfare rules and high pet ownership. Germany, France, and the United Kingdom dominate revenue, and the EU Cyber Resilience Act will obligate five-year patch support from December 2027, likely consolidating market power among cybersecurity-prepared vendors. Eastern Europe expands as veterinary infrastructure modernizes. The Middle East focuses on equine sports medicine, and Latin America leverages ultrasound for beef herd fertility, though cost constraints hinder mass adoption of handheld ultrasound.

Competitive Landscape

The market is moderately fragmented. Multinational imaging companies—GE HealthCare, FUJIFILM Sonosite, Mindray, Canon, and Siemens Healthineers—cross-sell veterinary-tuned versions of their human units, leveraging global service networks. Specialized firms such as Heska and IMV Imaging emphasize species-specific presets and rugged housings. Butterfly Network disrupts with semiconductor-based handhelds priced below USD 8,000, bundling AI features that simplify scanning for primary-care clinicians. GE’s 2023 partnership with Sound Technologies channels the Vscan Air into U.S. clinics via an established veterinary distributor, accelerating market penetration.

Cybersecurity compliance is emerging as a differentiator as the EU regulation mandates long-term patching and vulnerability reporting. Vendors with mature DevSecOps processes can absorb the added cost, squeezing smaller rivals. Consolidation among clinic groups concentrates purchasing power, favoring suppliers able to integrate hardware with enterprise PACS and electronic records. Chinese manufacturers, including Mindray and SonoScape, compete aggressively on price, forcing incumbents to highlight training, service, and AI workflow advantages rather than pure hardware specs.

Veterinary Ultrasound Devices Industry Leaders

Esaote SpA

IMV Imaging

Canon Inc.

Siemens Healthcare GmbH

FUJIFILM Sonosite Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: IMV Technologies launched its next generation of ImaGo fertility scanners to offer vets one of the most durable ultrasound scanners available for field use.

- May 2024: Esaote North America, Inc. unveiled the MyLab Omega eXP VET, a cutting-edge portable ultrasound system designed to elevate veterinary care. A combination of unparalleled robustness, accuracy, and lightning-fast performance, the MyLab Omega eXP VET offers veterinarians a new level of flexibility and precision in diagnostic imaging, anytime, everywhere.

Global Veterinary Ultrasound Devices Market Report Scope

As per the scope of the report, veterinary ultrasound devices are medical imaging tools used to visualize internal organs and tissues in animals. They utilize high-frequency sound waves to create real-time images for diagnosis. These devices are essential for non-invasive examinations in veterinary medicine.

The Veterinary Ultrasound Devices Market is Segmented by Portability (Handheld, Table-Top, and Cart/Trolley-Based), Technology (2-D, Doppler, 3-D/4-D, and Contrast-Enhanced), Application (Obstetrics & Gynecology, Cardiology, Musculoskeletal, Abdominal & Internal Medicine, and Emergency & Critical Care), Animal Type (Companion Animals, Livestock Animals, and Other Animals), End User (Veterinary Clinics, Veterinary Hospitals, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Handheld Ultrasound |

| Table-Top Ultrasound |

| Cart/Trolley-Based Ultrasound |

| 2-Dimensional Ultrasound |

| Doppler Ultrasound |

| 3-D/4-D Ultrasound |

| Contrast-Enhanced Ultrasound |

| Obstetrics & Gynecology |

| Cardiology |

| Musculoskeletal |

| Abdominal & Internal Medicine |

| Emergency & Critical Care |

| Companion Animals | Dogs |

| Cats | |

| Other Small Companion Animals | |

| Livestock Animals | Horse |

| Cattle | |

| Other Livestock Animals | |

| Other Animals |

| Veterinary Clinics |

| Veterinary Hospitals |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Portability | Handheld Ultrasound | |

| Table-Top Ultrasound | ||

| Cart/Trolley-Based Ultrasound | ||

| By Technology | 2-Dimensional Ultrasound | |

| Doppler Ultrasound | ||

| 3-D/4-D Ultrasound | ||

| Contrast-Enhanced Ultrasound | ||

| By Application | Obstetrics & Gynecology | |

| Cardiology | ||

| Musculoskeletal | ||

| Abdominal & Internal Medicine | ||

| Emergency & Critical Care | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Other Small Companion Animals | ||

| Livestock Animals | Horse | |

| Cattle | ||

| Other Livestock Animals | ||

| Other Animals | ||

| By End User | Veterinary Clinics | |

| Veterinary Hospitals | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving the fastest growth segment in veterinary ultrasound?

Handheld devices, growing at 9.43% CAGR, gain traction through lower pricing, AI presets, and leasing plans that fit clinic budgets.

Which application area is expanding the quickest?

Cardiology leads with 10.55% CAGR as Doppler echocardiography becomes standard for pre-anesthetic screening and chronic disease management.

Why is Asia-Pacific the most attractive growth region?

Government livestock surveillance mandates and rising urban pet ownership push demand, resulting in an 8.54% regional CAGR.

How are cybersecurity rules affecting product design?

The EU Cyber Resilience Act obliges at least five years of security patches and rapid vulnerability reporting, favoring vendors with mature DevSecOps.

What financing options help small clinics acquire ultrasound?

Subscription and leasing programs cut upfront costs by up to 80% and allow mid-contract hardware upgrades as technology improves.

How significant is AI in veterinary ultrasound today?

AI tools now reduce scan interpretation time by up to 40% and enable remote specialist oversight, though professional judgment remains essential.

Page last updated on: