United States Hand Protection Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

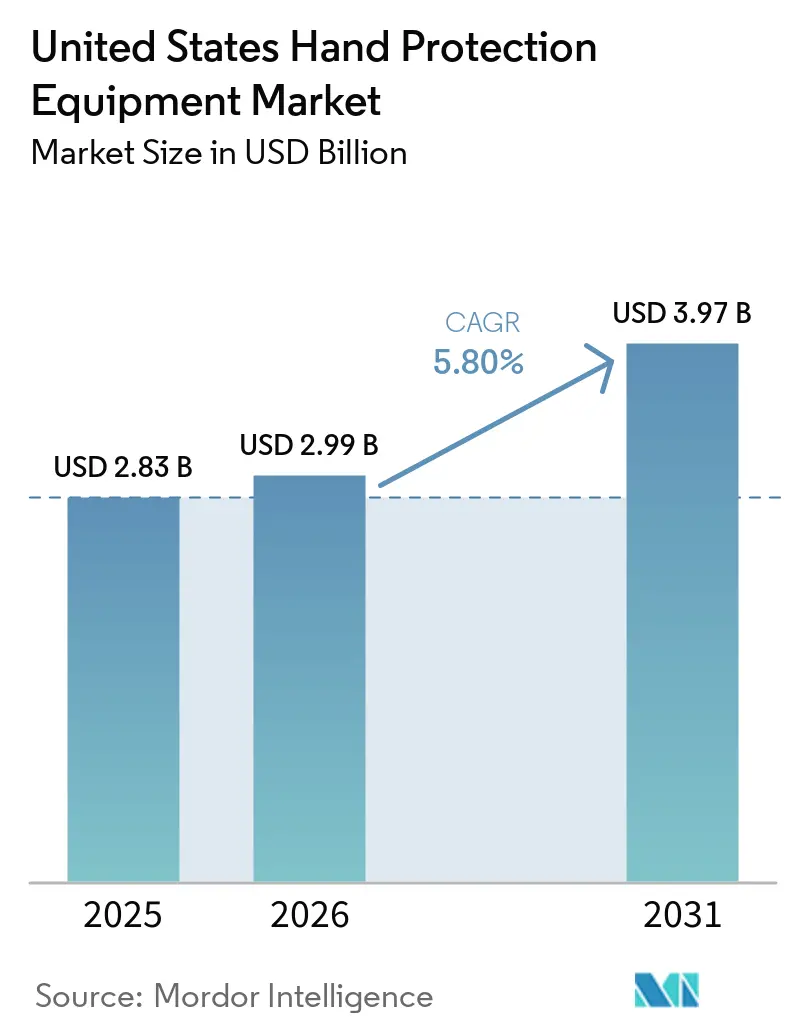

| Base Year Market Size (2025) | USD 2.83 Billion |

| Market Size (2026) | USD 2.99 Billion |

| Market Size (2031) | USD 3.97 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Hand Protection Equipment Market Analysis by Mordor Intelligence

The United States protection equipment market size was valued at USD 2.83 billion in 2025 and is estimated to grow from USD 2.99 billion in 2026 to reach USD 3.97 billion by 2031, at a CAGR of 5.8% during the forecast period (2026-2031). Mandatory fit and infection-control requirements, coupled with broader healthcare use and a rising demand for high-performance materials in industrial settings, are driving growth in the U.S. protective equipment market. Trade actions are reshaping sourcing patterns, particularly in the medical nitrile gloves market. This shift is steering buyers towards diversified supply chains outside of China and prompting selective investments in domestic manufacturing. While competitive dynamics remain balanced between global brands and regional specialists, the premium segment has tightened following recent acquisitions by Ansell and Protective Industrial Products. The U.S. protective equipment market is bolstered by resilient demand in healthcare and regulated industrial workflows, where glove use is often tied to compliance rather than a discretionary expense[1]Source: United States Bureau of Labor Statistics," Employer-Reported Workplace Injuries and Illnesses (Annual) News Release", bls.gov. However, growth in the U.S. protection equipment market is tempered, not rapid, due to automation in certain industrial processes and ongoing price pressures in standard disposable formats.

Key Report Takeaways

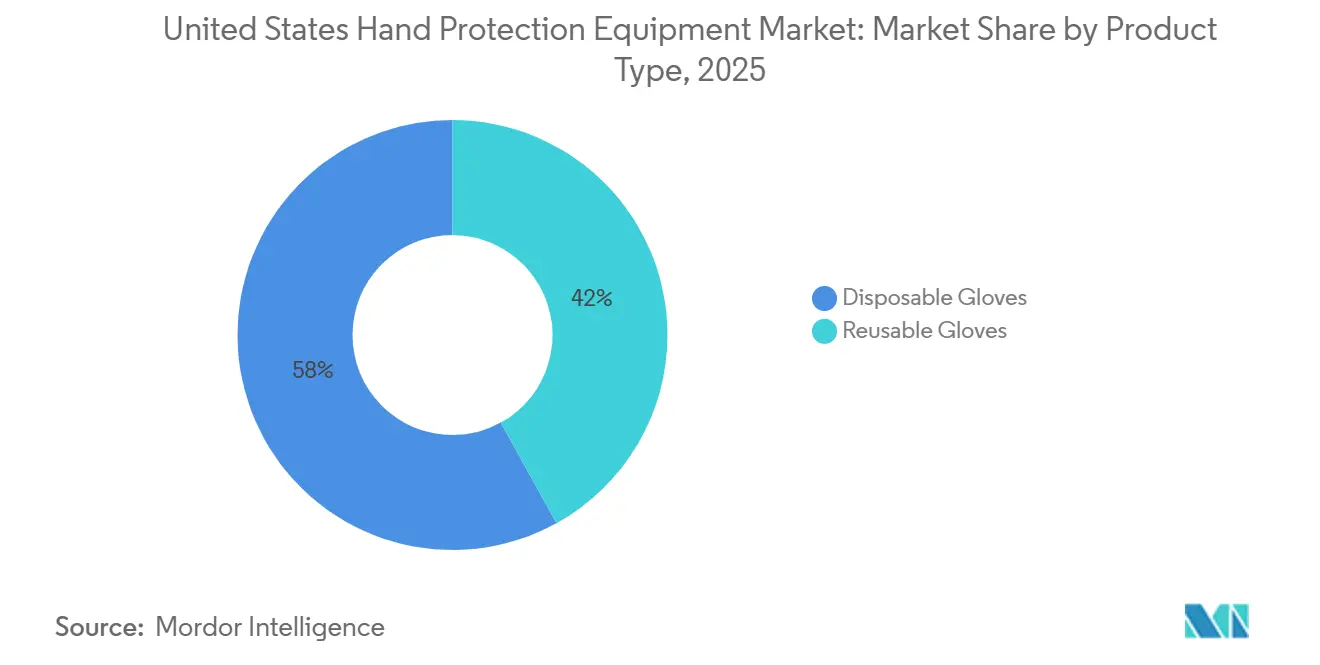

- By product type, disposable gloves accounted for the largest share of the market, at 58.1% in 2025, while reusable gloves are projected to grow at the fastest CAGR of 8.8% during 2026-2031.

- By raw material, natural rubber and latex accounted for the largest share of the market, at 32.2% in 2025, while nitrile is projected to grow at the fastest CAGR of 9.5% during 2026-2031.

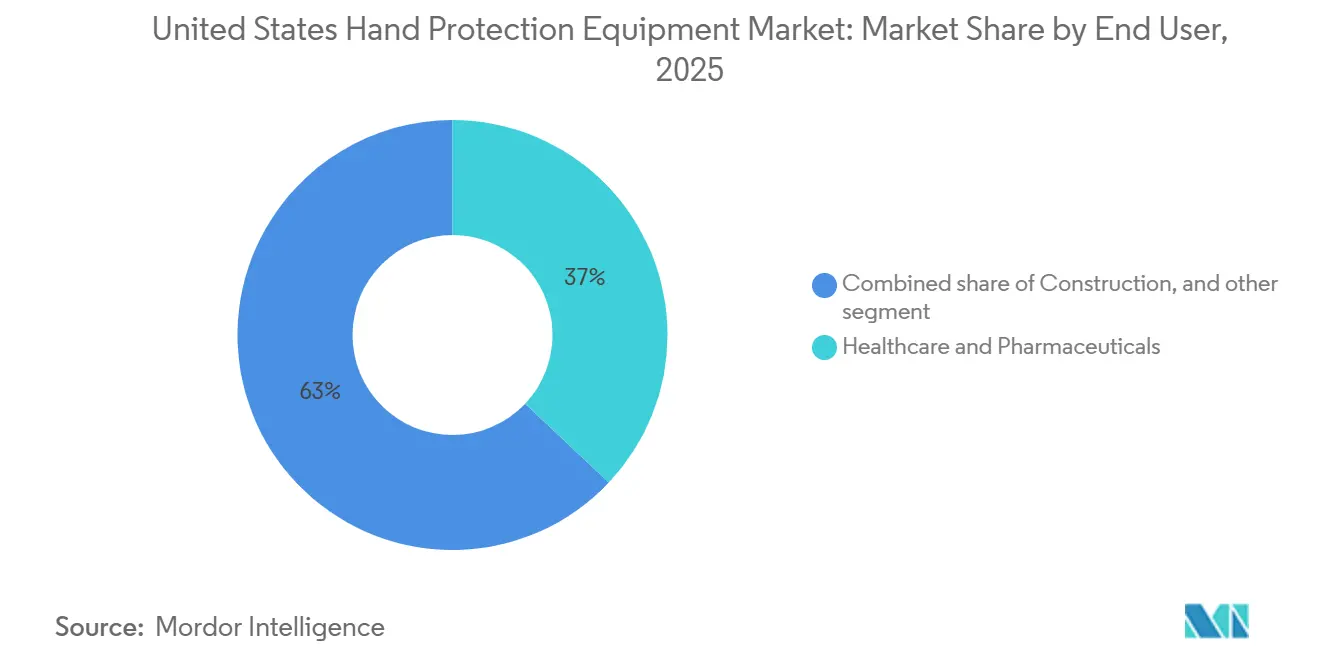

- By end user, healthcare and pharmaceuticals accounted for the largest share of the market, at 37.1% in 2025, and are projected to grow at the fastest CAGR of 9.1% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Hand Protection Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OSHA-Driven PPE Compliance Across Industrial and Healthcare Workflows | +1.5% | National, with concentrated gains in construction and healthcare-dense states such as Texas, Florida, California, and New York | Short term (≤ 2 years) |

| Rising Shift Toward Latex-Free and Chemical-Resistant Nitrile Adoption | +1.2% | National, with early adoption across medical hubs and chemical-handling clusters | Medium term (2-4 years) |

| Growing Workplace Injury Prevention Spending in High-Hazard Industries | +1.0% | National, with the strongest relevance in construction, mining, and oil and gas corridors | Medium term (2-4 years) |

| Aging Workforce and Higher Safety Protocol Intensity in Healthcare and Manufacturing | +0.8% | National, with sharper effects in older industrial labor pools and healthcare-heavy states | Long term (≥ 4 years) |

| Sensor-Enabled and Smart Glove Adoption for Human-Machine Interaction | +0.5% | National, with early uptake in advanced manufacturing and defense-linked production corridors | Long term (≥ 4 years) |

| Sustainability Pressure on Single-Use Glove Materials and Waste Handling | +0.4% | Strongest on the West Coast and in institutional procurement systems with formal sustainability screens | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OSHA-Driven PPE Compliance Across Industrial and Healthcare Workflows

In the U.S. protection equipment market, regulatory compliance stands as the most steadfast pillar of demand. In December 2024, OSHA rolled out revisions to 29 CFR 1926.95, mandating that construction employers provide each worker with properly fitting PPE, including gloves[2]Source: Occupational Safety and Health Administration, " Personal Protective Equipment in Construction", osha.gov. This January 2025 rule change amplifies replacement demand, as employers now seek a broader size range, moving away from a limited stock profile. The shift complicates procurement, often benefiting larger distributors and established brands with more extensive inventories. In the healthcare sector, CMS, on April 28, 2025, broadened the Enhanced Barrier Precautions, specifying more scenarios for glove use when caring for nursing home residents with chronic wounds or indwelling devices. Collectively, these regulatory shifts bolster the recurring demand in the U.S. protection equipment market, underscoring that glove usage is now a mandated practice, not just an optional purchase.

Rising Shift Toward Latex-Free and Chemical-Resistant Nitrile Adoption

Across healthcare, laboratories, food handling, and chemical-intensive industries, the U.S. market for protective equipment is increasingly leaning towards nitrile. Starting January 1, 2025, the USTR tariff schedule hiked duties on Chinese medical-grade nitrile gloves to 50%, with a further increase to 100% set for January 1, 2026. This significant policy shift altered the landed cost of Chinese supplies entering the U.S. As a result, importers and institutional buyers are now more inclined to diversify their sources, turning to Malaysia, Vietnam, India, and select domestic capacities. Nitrile's appeal lies in its latex-free nature, enhanced puncture resistance, and superior chemical compatibility, making it ideal for demanding applications. Specifications in hospitals and laboratories are increasingly prioritizing performance standards, such as ASTM D6978 for chemotherapy-drug resistance, driving a trend of premiumization in the U.S. protective equipment market.

Growing Workplace Injury Prevention Spending in High-Hazard Industries

In high-risk workplaces across the U.S., spending on hand protection is closely linked to injury prevention priorities. In 2024, the Bureau of Labor Statistics reported 2.5 million nonfatal workplace injuries and illnesses. Notably, the healthcare and social assistance sector recorded a total case rate of 3.4 per 100 full-time equivalent workers, surpassing the private industry average of 2.3. Industries such as construction, oil and gas, mining, and metalworking continue to prioritize cut-resistant, abrasion-resistant, and chemical-resistant gloves due to the heightened severity of injuries in these settings. In 2025, OSHA used over 370,000 Form 300A submissions to update its Injury Tracking Application, enhancing employer benchmarking visibility and amplifying safety investment decisions. Consequently, many buyers are transitioning from budget gloves to higher-performance alternatives that promise enhanced durability and worker protection. This trend bolsters value growth in the U.S. protective equipment market, even amidst moderate unit growth.

Aging Workforce and Higher Safety Protocol Intensity in Healthcare and Manufacturing

Demographic shifts are bolstering demand in the U.S. protective equipment market. In December 2025, the U.S. Census Bureau highlighted that 24% of the national workforce was aged 55 or older. As older workers dominate, there's a heightened demand for glove designs that prioritize comfort, emphasizing better fit, grip, and reduced strain, especially in repetitive tasks. In the healthcare sector, the American Hospital Association noted that in 2025, hospitals shelled out over USD 1 trillion on workforce costs. With wages climbing by 5.6%, there's an amplified emphasis on workflows that mitigate retraining challenges and prevent lapses in infection control[3]Source: American Hospital Association, " Costs of Caring: Challenges Facing America’s Hospitals as They Care for Patients in 2026", aha.org. Such dynamics make a compelling case for prioritizing ergonomics and compliance during procurement evaluations, ultimately driving demand for higher-specification products in the U.S. protective equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation and AI Lowering Manual-Hand Exposure in Some Industrial Tasks | -0.7% | National, with higher relevance in automotive,electronics, and pharmaceutical automation hubs | Long term (≥ 4 years) |

| Volatility in Nitrile, Latex, and Polymer Feedstock Costs | -0.6% | National, with the strongest effect on import-dependent supply chains and domestic compounders | Short term (≤ 2 years) |

| Certification Delays for Novel Materials and Performance Claims | -0.4% | National, particularly for healthcare and advanced industrial product launches | Medium term (2-4 years) |

| Procurement Price Pressure and Commoditization in Standard Disposable Gloves | -0.3% | National, strongest in hospital group purchasing contracts and high-volume distributor channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automation and AI Lowering Manual-Hand Exposure in Some Industrial Tasks

Parts of the U.S. protection equipment market are feeling the pinch of automation, particularly in industrial workflows where manual touch is being systematically eliminated. In 2025, North American robot orders climbed by 6.6%, underscoring the shift of automated assembly, handling, and inspection from just the automotive sector to a wider array of manufacturing applications. In the realm of pharmaceutical manufacturing, operations such as sterile fill-finish are turning to barrier technologies and automated systems to minimize reliance on manual, glove-dependent tasks. While this shift doesn't significantly dampen demand for gloves in healthcare or food services, it does temper demand intensity in select premium industrial sectors. The impact unfolds gradually, not suddenly, but it effectively caps volume growth in certain segments of the U.S. protection equipment market. As a result, companies boasting robust industrial portfolios are finding it essential to align their volume expectations with a push towards higher-value innovations and a focus on replacement demand.

Volatility in Nitrile, Latex, and Polymer Feedstock Costs

In the U.S. protection equipment market, feedstock volatility poses a significant challenge. Glove manufacturers, reliant on petrochemical and natural rubber inputs, grapple with unpredictable pricing. Rapid fluctuations in input costs pressure suppliers, impacting contract pricing, inventory strategies, and margin management, particularly for commodity disposables. This challenge is pronounced for channels that depend on imports, source finished gloves or upstream compounds from Asia, and sell them into the U.S. market, which is sensitive to pricing. Manufacturers find it increasingly challenging to uphold long-term price commitments, especially when procurement teams advocate for reduced unit costs. Furthermore, delays in certifying new materials, coupled with the commoditization of standard disposable products, hinder the swift rollout of premium products. This dynamic keeps a substantial portion of demand tethered to price-driven purchases. Collectively, these challenges constrain the U.S. protection equipment market's ability to swiftly translate operational demand into robust revenue growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reusable Formats Gaining Ground on Sustainability and Total Cost Logic

In 2025, disposable gloves dominated the U.S. protection equipment market, commanding a 58.1% share, clearly outpacing other segments. Their widespread adoption spans healthcare, food processing, and cleaning sectors, underscoring the ongoing need for single-use practices to control contamination. Highlighting the segment's vitality, U.S. imports of disposable gloves reached a staggering 44.1 billion units in the first seven months of 2025 alone. Stringent product standards and compliance regulations anchor this segment, as buyers prioritize consistent quality, especially for food-related and medical applications. However, this segment grapples with greater commoditization in procurement than many premium categories. While this dynamic boosts volume, it complicates value creation, pushing suppliers to stand out through factors like fit, consistent performance, or reliable supply.

Reusable gloves are emerging as the fastest-growing segment of the U.S. protective equipment market, with projections indicating an 8.8% CAGR from 2026 to 2031. The strongest growth is observed in sectors where buyers prioritize cost over the glove's unit price, such as chemical handling, construction, mining, and heavy industry. Here, glove lifespan, cut resistance, and chemical resilience take precedence. Furthermore, there's a notable trend linking reusable gloves to sustainability, with institutions increasingly favoring products that boast reduced lifecycle impacts and robust environmental credentials. A 2025 piece in Antimicrobial Resistance & Infection Control highlighted the dual benefits of optimizing glove use: bolstering patient safety while managing healthcare costs. While reusable gloves aren't yet overshadowing disposables, they're carving out a larger share of premium revenue in the U.S. protective equipment market. This trend positions established specialty suppliers more favorably than those leaning heavily on high-volume commodity lines.

By Raw Material: Nitrile Chemistry Rewriting Supply Chain Architecture

In 2025, natural rubber and latex accounted for a dominant 32.2% share of the U.S. protective equipment market. Their prominence is anchored in tactile sensitivity and surgical precision, underscoring the importance of glove feel in operating rooms. The recent 2025 perioperative guidelines emphasize glove-change protocols during invasive procedures, bolstering demand for surgical gloves in the U.S. protective equipment sector. While natural rubber and latex are pivotal in scenarios prioritizing dexterity over extensive chemical protection, allergy concerns curtail their expansion in numerous institutional settings. This positions the segment as well-established, yet with a constrained growth trajectory compared to synthetic materials, which are steadily gaining traction in the U.S. protection equipment market.

Nitrile emerges as the fastest-growing segment, with projections indicating a 9.5% CAGR for nitrile-based gloves in the U.S. protection equipment market from 2026 to 2031. The surge in demand is multifaceted: nitrile's latex-free nature, enhanced puncture resistance, and versatility across laboratory, healthcare, and chemical-handling applications. Additionally, U.S. trade policies, notably Section 301 tariffs on Chinese medical-grade nitrile gloves, have reshaped sourcing economics, prompting investments in diversified domestic supply chains. A testament to this shift is the U.S. Medical Glove Company's planned USD 200 million to USD 240 million investment in Cincinnati, highlighting how tariffs have bolstered the case for onshoring, a move that would have been challenging to advocate previously. Furthermore, medical-grade nitrile's adherence to compliance standards such as ISO 13485:2016 and FDA 510(k) requirements favors established suppliers with validated quality systems. Consequently, nitrile not only stands out as a growth driver in the U.S. protective equipment market but also plays a pivotal role in reshaping supply chain strategies.

By End Use: Healthcare Demand Compounding Across Both Volume and Specification Intensity

In 2025, healthcare and pharmaceuticals dominated the U.S. protective equipment market, capturing 37.1%. This segment not only led in market share but also exhibited the highest compliance intensity. The emphasis on gloves in this sector is paramount, given their roles in infection prevention, patient contact, sterile handling, and laboratory practices. In a move underscoring this importance, CMS, in its 2025 update to Enhanced Barrier Precautions, broadened mandatory gloving requirements in nursing homes, boosting their routine use in long-term care. Highlighting the financial stakes, the American Hospital Association noted that hospitals shelled out over USD 1 trillion on workforce costs in 2025. This hefty investment fuels a keen interest in products and processes that mitigate complications, reduce retraining needs, and bolster infection control. Further validating the emphasis on gloving, a 2025 multisite VA study featured in the American Journal of Infection Control advocated broader gloving to combat Clostridioides difficile. Collectively, these factors underscore healthcare's pivotal role in driving demand within the U.S. protective equipment market.

Forecasts suggest that from 2026 to 2031, healthcare and pharmaceuticals will lead the pack with a projected 9.1% CAGR. This dual leadership in both current market share and anticipated growth underscores a rising demand, fueled by increased usage and heightened specification standards. Institutions like hospitals, nursing homes, laboratories, and pharmaceutical facilities are increasingly integrating glove-dependent protocols into their infection control and contamination management processes. Reinforcing this trend are OSHA's bloodborne pathogen enforcements, stringent hospital procurement standards, and the cleanliness mandates of the pharmaceutical sector. While sectors like construction, oil and gas, food processing, and mining remain significant, especially for reusable and cut-resistant formats, they fall short of matching the volume and specification intensity that healthcare commands. While ANSI and ASTM performance benchmarks continue to cater to industrial demands, the most pronounced growth trajectory in the U.S. protective equipment market is undeniably anchored in healthcare and pharmaceuticals. This trend suggests a tighter alignment of the market with institutional compliance trends rather than the ebb and flow of industrial cycles.

Geography Analysis

According to the source narrative, the Southeast emerges as the dominant hub for protective equipment demand in the U.S. Major healthcare networks in Texas, Florida, and Georgia are driving a robust demand for medical nitrile gloves. Notably, health systems in Texas and Florida are shifting their procurement to favor nitrile gloves exclusively. Additionally, the Gulf Coast and Permian Basin energy corridor in the Southeast underscores the need for chemical-resistant and heavy-duty reusable gloves in oil and gas operations. This blend of a vast healthcare landscape and an active industrial sector positions the Southeast as the leading demand center for protective equipment in the U.S., serving both high-volume disposable items and premium industrial products.

The Midwest is witnessing the most pronounced growth in the U.S. protective equipment market. States like Michigan, Ohio, Indiana, and Illinois are pivotal demand centers for industrial gloves, driven by sectors such as automotive, food processing, and manufacturing. Furthermore, the region is bolstering its significance with domestic production investments, highlighted by U.S. Medical Glove Company’s facility in Cincinnati and its notable USD 63.6 million contract with the Department of Defense and HHS, finalized in Q1 2025. Census data reveal that the Midwest's older manufacturing workforce is increasingly leaning towards ergonomic and specialized glove demands. Consequently, the Midwest is not just a major industrial user but is also emerging as a crucial node for supply security and onshoring in the U.S. protective equipment landscape.

While the U.S. protective equipment market operates on a national scale, regional dynamics showcase a diverse landscape. The Northeast, particularly the corridor stretching from Boston to New York and Philadelphia, plays a vital role in pharmaceutical manufacturing and research hospitals, driving demand for cleanroom-grade gloves. On the West Coast, there's a pronounced preference for latex-free, premium, and sustainability-focused products, as institutional buyers often set the pace for material and procurement standards. Moreover, OSHA’s January 2025 PPE fit rule holds significant weight in the Northeast and Pacific Coast construction sectors, where a diverse workforce underscores the importance of size coverage and fit. Thus, regional demand is shaped by a confluence of factors from healthcare density and manufacturing activities to energy operations and regulatory nuances. This multifaceted demand landscape ensures a balanced distribution of the U.S. protective equipment market across various regions, rather than a concentration in one area. It also highlights the necessity for suppliers to maintain a national distribution network while tailoring their product offerings to specific regions. Companies adept at catering to hospital systems, industrial distributors, and public-sector entities across diverse regions are poised for success as the U.S. protective equipment market evolves.

Competitive Landscape

The United States protection equipment market is moderately concentrated. While large global manufacturers set quality standards and dictate premium prices, regional specialists and distributor-led brands carve out niches in specific applications. A significant shift has been the consolidation of portfolios at the premium end of the U.S. protection equipment market. Ansell's acquisition of Kimberly-Clark's PPE assets bolstered its contamination-control and laboratory offerings, integrating brands like Kimtech and KleenGuard, with orders starting in March 2025. In May 2025, Protective Industrial Products took over Honeywell's PPE business, adding brands such as North, KCL, Fendall, and Salisbury to its global portfolio. These strategic moves have reduced the number of major brands competing at the premium tier, even as the lower-tier disposable segment remains crowded.

Supply-chain credibility emerges as a key competitive theme in a tariff-driven procurement landscape. With Section 301 tariffs altering the risk dynamics of Chinese-origin medical nitrile gloves, buyers now prioritize transparent country-of-origin documentation, reliable U.S. inventory, and access to multi-country manufacturing. Ansell's facility in Tamil Nadu, which commenced production in February 2025 at 60 million pairs annually, aims to ramp up to 145 million pairs by 2027, bolstering its stance on non-China sourcing. Top Glove noted a significant uptick in North American sales in the first half of fiscal 2026, while Hartalega expanded Plant 9 with new lines set to launch by March 2026, underscoring how Malaysian production is seizing demand previously centered in China. This shift indicates that, in the U.S. protection equipment market, competitive advantage hinges as much on sourcing strategies and trade resilience as on product variety. Suppliers boasting stable lead times and diverse manufacturing locations find themselves in a stronger negotiating position with hospitals, distributors, and industrial clients.

Innovation is a pivotal force in the U.S. protective equipment market. Ansell's January 2026 introduction of the TouchNTuff 93-800 glove, which melds acetone resistance with over 60% bio-based carbon content, exemplifies the fusion of chemical performance and sustainability in disposable gloves. SHOWA's EBT nitrile glove line, designed for biodegradability, offers product differentiation that's challenging for price-centric competitors to replicate quickly. Recent advancements in cut-resistant and ergonomic industrial gloves highlight branded suppliers' efforts to shift the competitive focus from mere price comparisons to tangible use-case value. This shift is crucial given the intense procurement pressures and limited pricing power in commodity-disposable categories. Consequently, the U.S. protection equipment market exhibits a dual structure: fierce price competition in standard disposables contrasts with robust margins in certified, sustainable, and technologically advanced products. This dynamic is poised to remain a defining aspect of the competition in the coming years.

United States Hand Protection Equipment Industry Leaders

-

Ansell Limited

-

Honeywell International Inc.

-

3M

-

Protective Industrial Products, Inc.

-

MCR Safety

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Ansell unveiled its HyFlex sustainable cut-resistance series, crafted from over 50% recycled post-consumer PET sourced from eco-yarn. Coated with a DMF-free polyurethane, this series offers wear resistance up to 4 times that of standard PU coatings. Aimed at light-to-medium industrial tasks, the launch underscores a commitment to reducing CO2 emissions by 25%, marking a significant ESG pledge in the premium industrial gloves market.

- March 2026: Lakeland Fire + Safety secured additional

- February 2026: Lakeland Fire + Safety clinched a major multi-year contract with 7 County Fire and Rescue Services in the UK, tasked with supplying the Ultimate Glow+ structural firefighting gloves. This contract further cements Lakeland's stature as a certified public safety supplier.

- October 2025: Ansell introduced its HyFlex Precision Comfort Series, integrating AEROFIT Technology. This innovative series features a flexible foam nitrile coating that's 30% thinner, enhancing tactile control. It promises cut and abrasion protection while ensuring premium ergonomic comfort for industrial glove users.

United States Hand Protection Equipment Market Report Scope

| Disposable Gloves |

| Reusable Gloves |

| Natural Rubber and Latex |

| Nitrile Gloves |

| Neoprene |

| Vinyl |

| High-Performance Polyethylene |

| Other Raw Materials |

| Healthcare and Pharmaceuticals |

| Construction |

| Oil and Gas |

| Food Industry |

| Mining |

| Other End Uses |

| By Product Type | Disposable Gloves |

| Reusable Gloves | |

| By Raw Material | Natural Rubber and Latex |

| Nitrile Gloves | |

| Neoprene | |

| Vinyl | |

| High-Performance Polyethylene | |

| Other Raw Materials | |

| By End Use | Healthcare and Pharmaceuticals |

| Construction | |

| Oil and Gas | |

| Food Industry | |

| Mining | |

| Other End Uses |

Key Questions Answered in the Report

What is the 2031 outlook for the United States protection equipment space?

The United States protection equipment market is forecast to reach USD 3.97 billion by 2031 from USD 2.99 billion in 2026, growing at a 5.8% CAGR over 2026-2031.

Which product category leads current demand in the United States?

Disposable gloves lead current demand with a 58.1% share in 2025, supported by healthcare, food processing, and cleaning applications that still require single-use protection.

Which glove material is expected to grow the fastest through 2031?

Nitrile is the fastest-growing raw material segment at a 9.5% CAGR, helped by latex-free positioning, chemical resistance, and tariff-driven sourcing shifts.

Why does healthcare remain the most important end-use area?

Healthcare and pharmaceuticals held 37.1% share in 2025 and is also the fastest-growing end-use segment at 9.1% CAGR because glove usage is tied to infection control and compliance rules.

Page last updated on: