Industrial Protective Footwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.26 Billion |

| Market Size (2031) | USD 14.41 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Protective Footwear Market Analysis by Mordor Intelligence

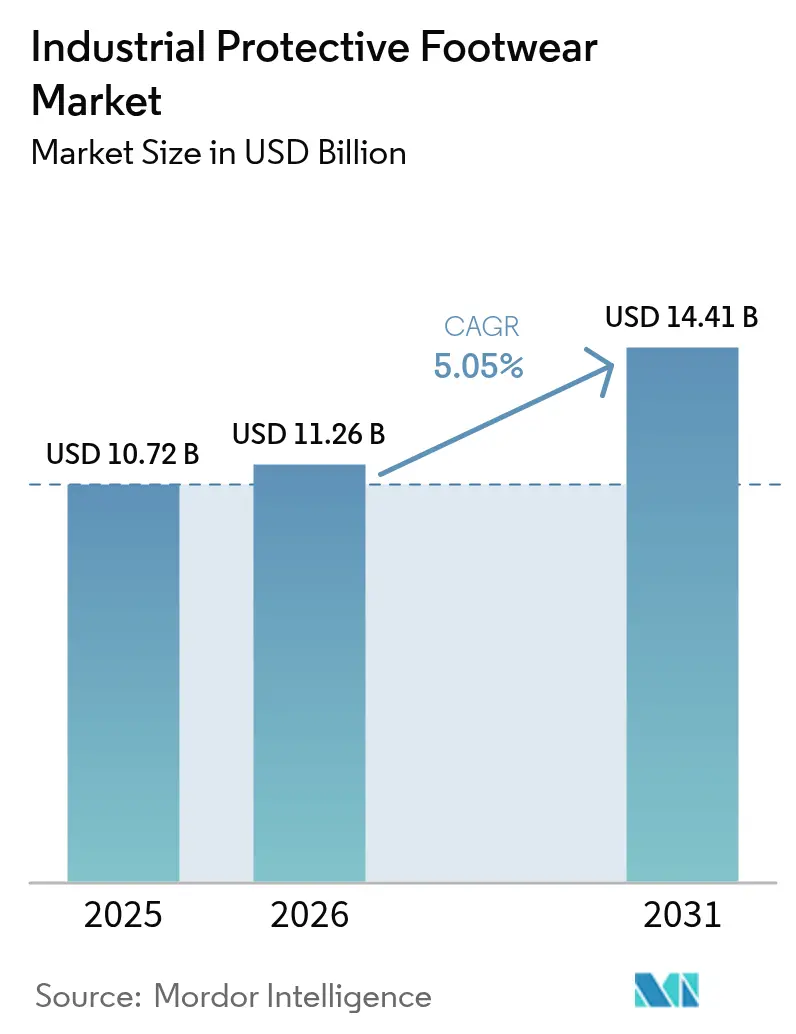

The industrial protective footwear market size was valued at USD 10.72 billion in 2025 and estimated to grow from USD 11.26 billion in 2026 to reach USD 14.41 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031). Robust construction pipelines, stringent safety mandates, and swift material innovations bolster this growth. The rising acceptance of composite toe caps and breathable membranes among workers is noteworthy. Furthermore, updated OSHA 29 CFR 1910.136 mandates have intensified fit-testing and performance standards across job sites. Increased infrastructure investments in Asia and the Middle East are driving demand[1]Source: U.S. Department of Labor, Occupational Safety and Health Administration, “29 CFR 1910.136 Personal Protective Equipment,” osha.gov. Additionally, the emergence of "smart" boots, integrated with IoT sensors, is steering procurement choices towards data-centric safety solutions. While challenges like counterfeit trade and price sensitivity among smaller contractors persist, the market finds favor in corporate ESG targets, especially those emphasizing bio-based and recycled materials.

Key Report Takeaways

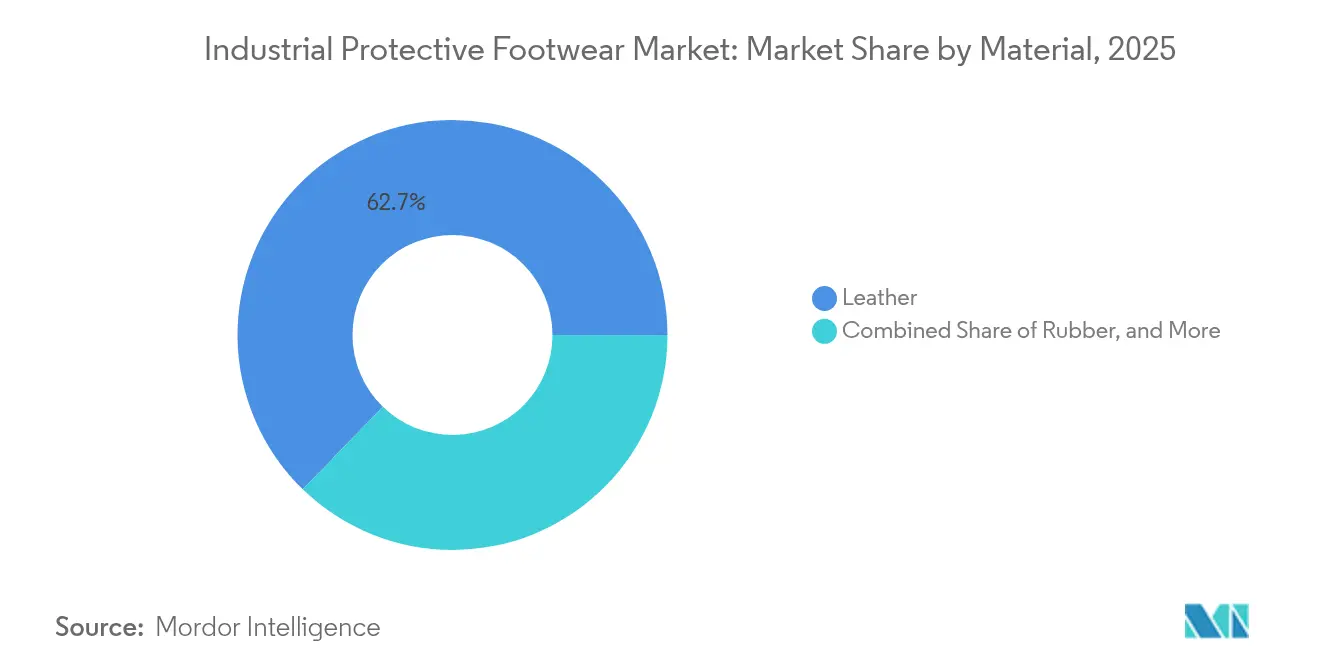

- By material, leather led with 62.74% of the industrial protective footwear market share in 2025; the rubber segment is forecast to expand at a 6.49% CAGR through 2031.

- By product type, boots accounted for 66.92% of the industrial protective footwear market size in 2025, while shoes are projected to post the fastest 5.46% CAGR to 2031.

- By end-user industry, construction held a 20.61% share of the industrial protective footwear market in 2025, whereas oil and gas is poised to rise at a 6.68% CAGR through 2031.

- By distribution channel, offline retail dominated with 92.98% revenue share in 2025; online platforms are expected to grow at a 6.11% CAGR to 2031.

- By geography, North America commanded 28.21% of the industrial protective footwear market size in 2025, while Asia-Pacific is projected to register the fastest 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Protective Footwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased focus on workplace safety and regulatory compliance | +1.0% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Rapid infrastructure build boosting PPE spend | +1.2% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Adoption of innovative, lightweight, and ergonomic footwear designs | +0.8% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Corporate ESG mandates favouring bio-based and recycled materials | +0.6% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Deployment of connected "smart" safety boots (IoT sensors) | +0.4% | North America and Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Heightened demand for electrical hazard protection boots | +0.3% | Global, concentrated in utilities and energy sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased focus on workplace safety and regulatory compliance

As governments tighten workplace safety standards, the adoption of protective footwear is on the rise, driven by intensified regulatory enforcement. Under OSHA's 2025 updates, employers must ensure proper protective footwear selection and worker training across construction, manufacturing, and general industry applications. These updates, mandated under 29 CFR 1910.136, come from the Occupational Safety and Health Administration. While the Bureau of Labor Statistics noted a total of 2.6 million nonfatal workplace injuries in 2023, marking an 8.4% drop from 2022, certain sectors still grapple with foot and ankle injuries. Specifically, construction sees an incidence rate of 8.14%, agriculture at 10.23%, and transportation leading with 11.06%. In Europe, markets are aligning with the EN ISO 20345:2022 standards. These harmonized requirements not only bolster worker protection but also streamline cross-border trade. Such regulatory alignment reduces compliance fragmentation, allowing manufacturers to capitalize on economies of scale across major markets. Analyzing the healthcare sector, slip, trip, and fall incidents are notably influenced by slipping, accounting for 42.9% of cases. However, trials conducted by the NHS, as reported by the Health and Safety Executive, highlight that slip-resistant footwear can cut these incident rates by 37%[2]Source: Mark Liddle et al., “Work-related Slip, Trip and Fall Injuries Reported by National Health Service Staff,” injuryprevention.bmj.com.

Rapid infrastructure build boosting PPE spend

As construction and energy projects expand, emerging markets are ramping up infrastructure investments, leading to a sustained demand for industrial protective footwear. The U.S. Census Bureau highlighted a correlation between rising construction spending and the procurement cycles of protective equipment. This is especially evident in heavy construction and infrastructure segments, which have a pronounced need for specialized safety footwear. Meanwhile, in the Asia-Pacific, urbanization and industrial growth are driving infrastructure development, spurring demand for protective footwear in construction, mining, and energy sectors. In India, Southeast Asia, and the Middle East, government infrastructure programs are enforcing international safety standards, paving the way for certified protective footwear manufacturers to enter the market. Trends in supply chain localization are bolstering regional manufacturing, curbing import dependencies, and addressing the surging infrastructure demand. Furthermore, the ripple effect of infrastructure spending touches not just direct construction but also maintenance, utilities, and ancillary industries, all of which emphasize protective footwear compliance. Highlighting this trend, Saudi Arabia's new PPE technical regulation underscores how nations with a focus on infrastructure are weaving safety mandates into their broader development strategies, as noted by the Saudi Standards Authority.

Adoption of innovative, lightweight, and ergonomic footwear designs

Ergonomic innovation transforms worker acceptance and productivity outcomes as manufacturers address comfort-performance trade-offs in protective footwear design. Research demonstrates that traditional safety footwear weighing 550-650 grams per foot significantly impairs gait parameters compared to 250-300 gram sneakers, with 83.3% of workers reporting discomfort, including heaviness (92%), excessive sweating (73.3%), and toe-cap pressure (60%), according to the MDPI Clinical Study. Advanced materials integration, including lightweight composites and breathable membranes, addresses these ergonomic challenges while maintaining safety certification compliance under ASTM F2413 and EN ISO 20345 standards. Manufacturing innovations leverage 3D printing, parametric design, and sensor integration to create customized protective footwear that improves worker comfort and reduces fatigue-related incidents. Polyurethane insole technology, informed by military research, demonstrates superior performance in reducing musculoskeletal discomfort during prolonged standing applications. Smart design approaches incorporate anti-fatigue features, moisture management, and anatomical fit optimization to enhance worker compliance and safety outcomes.

Corporate ESG mandates favoring bio-based and recycled materials

As corporations weave environmental criteria into their protective footwear procurement, material selection is undergoing a sustainability-driven transformation. Consumers are showing a readiness to pay extra for sustainable features in footwear, such as vegan materials and 100% recycled content. This trend underscores a market shift towards eco-friendly alternatives, with perceived sustainability playing a pivotal role in purchase decisions, as highlighted by the MDPI Sustainability Study. In the realm of bio-based materials, innovations like natural rubber substitutes from guayule and Russian dandelion are emerging. These alternatives not only lessen the industry's reliance on petroleum but also uphold the performance standards essential for industrial use. According to the MDPI Sustainability Research, protective footwear insoles are benefiting from a blend of recycled polyester (rPET) non-woven fabrics and polyurethane lamination[3]Source: Alberto Arceri et al., “Safety Footwear Impact on Workers’ Gait and Foot Problems,” mdpi.com. This combination not only ensures durability and antibacterial properties, boasting a 92% reduction in bacteria, but also retains mechanical performance even after enduring 50,000 Martindale abrasion cycles. Life cycle assessment studies, as per the MDPI LCA Study, highlight that a staggering 79.8% of the carbon footprint in professional safety boots stems from material production and component manufacturing. Notably, leather uppers contribute 39.9% and polyurethane soles account for 30.1% of these emissions. In response, corporate procurement policies are evolving, increasingly mandating minimums for recycled content and showing a preference for bio-based materials. This shift is not just about sustainability; it's about carving out competitive advantages for manufacturers who embrace circular economy principles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of low-cost counterfeit products | -0.7% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| High price elasticity among SME contractors in emerging markets | -0.5% | Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Complex regulatory compliance and certification costs | -0.4% | Global, with varying impact by regulatory jurisdiction | Medium term (2-4 years) |

| Lack of industry and worker awareness in small and medium enterprises | -0.3% | Emerging markets, rural industrial areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of low-cost counterfeit products

Counterfeit protective footwear not only jeopardizes worker safety but also distorts market dynamics, putting legitimate manufacturers at a disadvantage. An OECD analysis highlights the gravity of the issue, revealing a global counterfeit trade exceeding USD 467 billion[4]Source: Organisation for Economic Co-operation and Development, “Global Trade in Fakes,” oecd.org. Alarmingly, footwear accounts for a staggering 62% of all seized counterfeit goods, as detailed in the OECD Counterfeit Report. Testing by the British Safety Industry Federation uncovered a troubling trend: a significant volume of non-compliant safety footwear in UK markets. These counterfeits, while visually convincing, often fall short of basic safety standards. In a striking example of the widespread nature of this issue, authorities in the Philippines confiscated counterfeit footwear valued at PHP 152 million, underscoring the challenge faced by protective equipment markets, especially in developing nations. Such counterfeit products not only lack essential safety certifications but also utilize inferior materials and often don't pass performance tests. This oversight poses significant liability risks for employers and endangers workers. The rise of online marketplaces has further exacerbated the issue, streamlining the distribution of counterfeit goods and complicating detection and enforcement efforts for both regulatory bodies and genuine manufacturers.

High price elasticity among SME contractors in emerging markets

Despite the safety benefits, small and medium enterprises (SMEs) in emerging markets remain hesitant to adopt premium protective footwear solutions due to significant price sensitivity. An analysis by the Asian Development Bank highlights that MSMEs in South Asia grapple with persistent financing challenges. Bank lending to these enterprises constitutes a mere 7.0% of GDP, and they face a non-performing loan (NPL) rate of 13.6%, notably higher than the overall bank NPL rate of 8.8%, as detailed in the Asian Development Bank's SME Monitor. This limited access to formal financing hampers SMEs' ability to invest in safety equipment upgrades, posing challenges for manufacturers of protective footwear aiming to cater to this market. Research from UNIDO on SME development underscores that small enterprises often prioritize short-term operational costs over long-term safety investments, especially in the face of weak regulatory enforcement. Furthermore, local manufacturers, by leveraging lower-cost materials and simplified designs, exert price competition, putting downward pressure on the pricing of premium protective footwear in these emerging markets. This challenge is exacerbated in segments of the informal economy, where safety regulations are loosely enforced, and cost considerations heavily influence purchasing decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Leather Dominance Faces Sustainable Alternatives

In 2025, leather commands a dominant 62.74% market share, thanks to its unmatched durability, breathability, and acceptance in various industrial applications. Chrome-tanned leather, known for its abrasion resistance and comfort, is the go-to choice in construction and manufacturing, where all-day wear comfort is paramount. Yet, as environmental concerns rise and corporate sustainability becomes a mandate, material preferences shift. Notably, a study by MDPI highlights that leather uppers account for 39.9% of the carbon footprint in professional safety boots. Meanwhile, synthetic leather is gaining ground, boasting enhanced performance and a smaller environmental footprint. Rubber segments, on the other hand, are on a growth trajectory, expanding at a 6.49% CAGR through 2031, driven by heightened demand in the oil, gas, and chemical processing sectors for their chemical resistance.

As the material landscape shifts, manufacturers are turning to bio-based alternatives and recycled content to align with ESG mandates. Innovations in natural rubber, sourced from guayule and Russian dandelion, are curbing petroleum reliance without compromising the performance standards essential for industrial protective footwear, as highlighted in the MDPI Rubber Textiles Review. Advanced composites and textile-rubber blends are carving out niches, offering specialized properties like electrical hazard protection and extreme temperature resistance. Furthermore, regulatory frameworks like ASTM F2413 and EN ISO 20345:2022 guarantee material performance across the board, fostering innovation while upholding safety standards.

By Product Type: Boots Lead Despite Shoe Segment Growth

In 2025, boots command a dominant 66.92% share of the protective footwear market, thanks to their superior ankle protection and adaptability across various industrial settings. Such high-ankle protection is vital in sectors like construction, mining, and heavy manufacturing, where workers contend with hazards ranging from falling objects to chemical exposure. The boot segment is also reaping the rewards of technological advancements, with manufacturers now integrating lightweight materials, ergonomic designs, and smart sensor features, all while upholding stringent protection standards. In contrast, shoes are witnessing a more rapid growth, projected at a 5.46% CAGR through 2031. This surge is largely attributed to their adoption in light manufacturing, logistics, and service sectors, where the emphasis shifts from ankle protection to worker comfort.

Innovations in product design are increasingly targeting traditional comfort issues, all while upholding safety standards. Research from the MDPI Clinical Study highlights a significant concern: conventional safety boots, typically weighing between 550-650 grams, hinder worker mobility and lead to discomfort for 83.3% of users. This revelation is fueling a growing demand for lighter alternatives. Meanwhile, low-ankle shoe designs are gaining traction among workers in warehousing, food processing, and healthcare. In these sectors, the emphasis is on mobility and comfort, often sidelining the need for stringent ankle protection. This evolution in product types mirrors the shifting dynamics of the workplace. As service sectors burgeon and traditional heavy industries embrace automation, the focus is not just on mitigating physical hazards but also on ensuring foot protection remains paramount.

By End-User Industry: Construction Leads While Energy Sectors Accelerate

In 2025, the construction sector commands a leading market share of 20.61%, buoyed by global infrastructure initiatives and stringent safety mandates. These regulations necessitate protective footwear for all construction endeavors. The construction sector's prominence is underscored by its vast employment scale and the myriad hazards on-site, from falling objects and puncture risks to electrical dangers and slippery surfaces. As construction spending rises, so does the demand for protective footwear, driven by regulations that enforce proper PPE usage for every worker, irrespective of project size or duration. Following closely, the manufacturing sector emerges as a key end-user, seeking specialized protective footwear for tasks ranging from assembly lines and material handling to machinery operation, spanning industries like automotive, electronics, and consumer goods.

Meanwhile, the oil and gas sector is poised for the swiftest growth, projected at a 6.68% CAGR through 2031. Heightened offshore drilling activities, unconventional energy extraction, and the burgeoning development of renewable energy infrastructures fuel this surge. Given the nature of their operations, these industries mandate specialized protective footwear. Such footwear not only boasts chemical resistance and protection against electrical hazards but also excels in extreme temperature performance, often commanding a premium price. Mining operations, on the other hand, prioritize puncture-resistant soles, robust ankle support, and durability to withstand both underground and surface challenges. The chemical and pharmaceutical sectors seek footwear tailored to resist specific chemical exposures and ensure compatibility with cleanroom standards. Additionally, as grid modernization and renewable energy initiatives unfold, the utilities and energy sectors are broadening their protective footwear needs, addressing new workplace hazards that demand specialized safeguards.

By Distribution Channel: Offline Dominance Challenged by Digital Growth

In 2025, offline channels command a dominant 92.98% share, underscoring the industrial sector's preference for hands-on inspection, fitting, and relationship-driven purchasing. Safety equipment dealers, industrial suppliers, and direct manufacturers not only distribute protective footwear but also offer the essential consultation and service support that industrial buyers seek. This offline inclination is largely due to the challenges of replicating proper fitting, product demonstrations, and technical support in a digital realm. Given the multi-stakeholder nature of industrial procurement, established supplier relationships and physical product evaluations play a pivotal role.

Online channels, while starting from a modest base, are projected to grow at a 6.11% CAGR through 2031. The digital transformation of industrial procurement and advancements in B2B e-commerce fuel this growth. Digital platforms entice cost-conscious buyers and smaller enterprises with a broader product selection, competitive pricing, and efficient ordering processes. This online surge mirrors the overarching digitalization of industrial supply chains, bolstered by better logistics, digital payment innovations, and virtual fitting technologies. Yet, despite this online momentum, offline channels are poised to retain their dominance throughout the forecast period, given the specialized nature of protective footwear purchases and the critical importance of fit for worker safety and comfort.

Geography Analysis

In 2025, North America holds a commanding 28.21% market share, buoyed by stringent OSHA regulations, a booming construction sector, and advanced manufacturing industries that prioritize worker protection. Under the mature regulatory framework of 29 CFR 1910.136, the Occupational Safety and Health Administration mandates protective footwear across construction, manufacturing, and general industries, ensuring stable demand even in fluctuating economic conditions. Rising construction spending and infrastructure investments in the U.S. bolster the demand for protective footwear. Meanwhile, Canada's mining and energy sectors have their own specialized product needs. North America is at the forefront of technological advancements, being the first to adopt smart protective footwear equipped with IoT sensors and connectivity. Additionally, Mexico's burgeoning automotive and electronics assembly sectors, coupled with the advantages of NAFTA trade relationships, further amplify the regional market and streamline cross-border supply chains.

Europe's market is significantly influenced by the harmonized EN ISO 20345:2022 standards, which not only unify safety requirements across member states but also enhance trade and manufacturing efficiency. The continent's strong focus on worker protection, environmental sustainability, and corporate social responsibility has led to a surge in demand for premium protective footwear, especially those crafted from eco-friendly materials and boasting advanced safety features. European manufacturers are at the forefront of developing sustainable materials, integrating bio-based alternatives and recycled content to align with corporate ESG mandates. Major markets like Germany, the United Kingdom, and France thrive due to their robust manufacturing, construction, and energy sectors. Furthermore, the European regulatory framework, under PPE Regulation 2016/425, not only upholds stringent safety standards but also fosters innovation in the design and materials of protective footwear.

Asia-Pacific is poised to be the fastest-growing region, with a projected CAGR of 7.18% through 2031. This growth is fueled by rapid industrialization, infrastructure development, and a push for enhanced safety standards in emerging economies. China's stronghold in manufacturing and its aggressive infrastructure investment programs lead to a surge in demand for protective footwear. Concurrently, India's expanding industrial and construction sectors further propel the market. While the region benefits from government initiatives advocating workplace safety and regulatory adherence, the enforcement of these regulations varies widely between developed and developing nations. Mature markets like Japan and Australia uphold stringent safety standards, whereas Southeast Asian nations, including Indonesia, Thailand, and Vietnam, are witnessing swift growth, largely driven by manufacturing expansion and an influx of foreign investments. This regional growth trajectory mirrors the rising industrial activities and a gradual uptick in safety awareness and regulatory enforcement across varying economic landscapes.

South America, along with the Middle East and Africa, stands as an emerging market with vast growth potential. This potential is largely attributed to activities in natural resource extraction, infrastructure development, and industrial expansion. In Brazil, sectors like mining, oil and gas, and construction fuel the demand for protective footwear. Argentina and Chile bolster this demand through their mining and energy industries. The Middle East, with its oil and gas industry and expansive infrastructure projects, underscores the necessity for protective footwear compliance. Highlighting regional strides in workplace safety, Saudi Arabia has introduced a new PPE technical regulation [Saudi Standards Authority]. In Africa, while the mining sectors in South Africa and Nigeria drive the demand for specialized protective footwear, the market's growth is tempered by economic challenges and hurdles in regulatory enforcement. As these regions continue to evolve economically and heighten their safety awareness, they present promising long-term growth opportunities.

Regulatory Landscape

Industrial protective footwear demand is supported by workplace PPE requirements and product safety standards that set minimum performance for toe protection, puncture resistance, slip resistance, and electrical hazard protection. In the United States, OSHA 29 CFR 1910.136 defines employer obligations for protective footwear selection and use, and it is commonly implemented through compliance with ASTM F2413 performance testing and labeling. In Europe, market access is tied to PPE Regulation (EU) 2016/425, with EN ISO 20345:2022 used as the technical benchmark for safety footwear conformity across EU/EEA supply chains.

Regulatory requirements continue to evolve, which keeps certification and documentation burdens active for manufacturers and importers. In June 2026, the European Union updated harmonised standards for personal protective equipment under Regulation (EU) 2016/425, reinforcing the need to track harmonised standard lists and maintain valid conformity assessment routes. Outside Europe and North America, destination markets also refresh mandatory testing regimes, including China’s revised mandatory footwear testing standard GB 25038-2024, effective 1 June 2025, which affects test planning, labeling, and time-to-market for suppliers serving China-centric industrial customers.

Value Chain Analysis

The value chain includes (1) raw materials such as leather, rubber, PU/EVA polymers, textiles and membranes, plus protective components including steel or composite toe caps and puncture-resistant plates, (2) component manufacturing (outsoles, midsoles, insoles, toe caps, fasteners), (3) upper preparation and assembly (cutting, stitching, lasting), (4) final assembly using cementing, injection molding, vulcanizing, or direct soling processes, followed by finishing, packing, and (5) compliance testing and certification aligned to key standards, including ASTM F2413 in the United States and EN ISO 20345 under EU PPE Regulation 2016/425. Quality gates typically focus on sample approval versus bulk-run consistency, and on final inspection where non-conformities can trigger rework, scrap, or shipment delays.

Manufacturing and sourcing are geographically split: high-volume, cost-competitive production is concentrated across Asian hubs (notably China, Vietnam, India, and Indonesia), while premium or technically differentiated safety footwear is often produced in higher-compliance facilities in Europe and the United States. Downstream, distribution is led by industrial dealers, safety specialists, and B2B wholesalers, supported by emerging digital procurement platforms used by smaller enterprises and multi-site buyers. Sustainability and traceability pressures are increasingly shaping upstream material choices (recycled content, alternative rubbers, lower-impact polymers) and downstream customer qualification, particularly where corporate ESG audits require product-level documentation and consistent labeling across regions.

Competitive Landscape

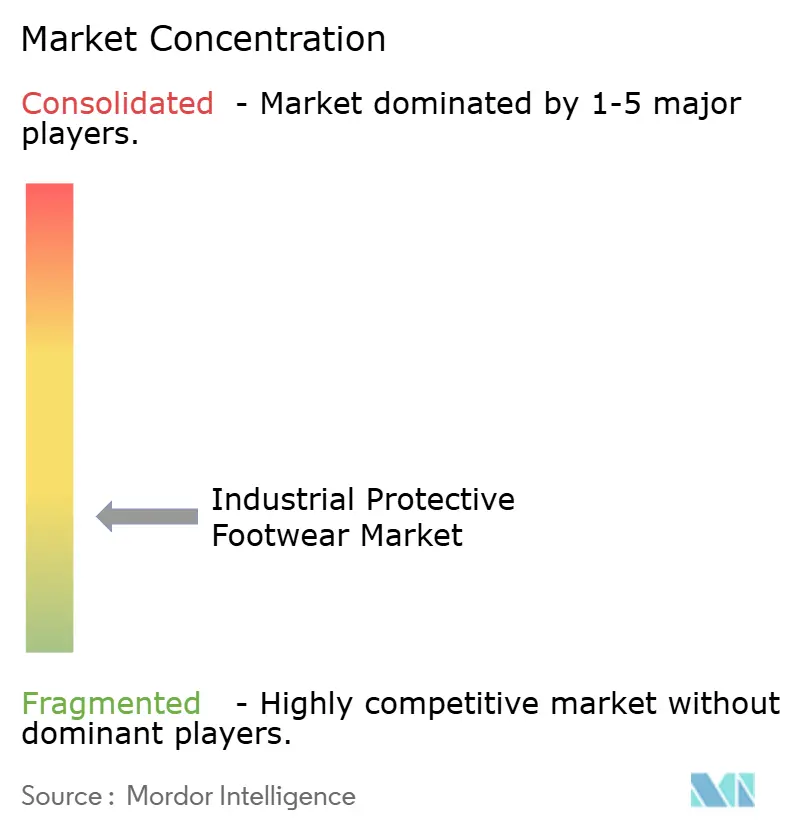

The industrial protective footwear market is moderately concentrated, with global brands, regional specialists, and lifestyle crossovers competing for prominence. In November 2024, Honeywell's divestiture of its USD 1.325 billion PPE unit to Protective Industrial Products (PIP) reshaped vendor portfolios, signaling a shift towards specialized safety players. Multinationals like VF Corporation, Wolverine World Wide, Bata, and Uvex offer a wide range, from classic leather to high-tech boots, while niche players rapidly innovate with eco-materials and integrated sensors.

Comfort and connectivity drive innovation. Companies utilize 3-D knitting, carbon-fiber toe caps, and energy-return EVA midsole foams to reduce weight while meeting ASTM F2413 impact standards. Initial trials of LTE-enabled geofencing boots in petrochemical sites saw a notable drop in “man-down” incidents, leading to larger tenders. While costs pose challenges, decreasing sensor prices and escalating liability premiums make a compelling case for smart footwear in high-risk areas.

Sustainability emerges as a key focus. Brands now provide carbon scorecards for each SKU and collaborate with chemical recyclers to transform PU off-cuts into fresh midsoles. Licensing agreements, like the 2024 Warson-Authentic Brands Group deal for DC Shoes and ROXY safety lines, leverage consumer brand strength to introduce lifestyle-inspired designs on factory floors. With tightening ESG audits, supply contracts are increasingly dependent on traceable materials, verified recycled content, and clear labor practices, driving consolidation among suppliers who can manage the reporting demands.

Industrial Protective Footwear Industry Leaders

Honeywell International Inc.

VF Corporation

Bata Corporation

Dunlop Protective Footwear

Wolverine World Wide Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product differentiation is moving beyond core protection into comfort engineering, moisture management, and task-specific performance, which creates room for suppliers that can deliver certified protection alongside measurable wearability gains. In June 2026, SINTEF presented a safety shoe concept built around replaceable midsoles tuned to user weight and tasks, and reported a 52% reduction in climate footprint when replacing leather with alternative materials, linking comfort innovation with procurement sustainability filters. Research activity also supports advanced insole concepts, including a 2026 MoonWalking pneumatic insole prototype designed to redistribute plantar pressure, reinforcing the opportunity for premium insoles and modular comfort systems that fit within existing certification requirements.

Brand and manufacturing moves in 2026 point to whitespace for new entrants and regional capacity, particularly where local supply can reduce lead times and improve compliance control. Adidas and GLO Brands B.V. announced the ADIDAS PRO WORK safety footwear range in June 2026 (with retail availability slated for August 2026), introducing sports-performance design language and metal-free, ESD-oriented positioning into industrial channels. On the supply side, Nigeria-based Yikodeen confirmed a July 2026 expansion of its Ejigbo, Lagos facility to over 5,000 pairs per day, signaling investment in domestic production capacity that can support large employers and public procurement, particularly in markets prioritizing certified PPE availability and local manufacturing development.

Recent Industry Developments

- July 2026: Yikodeen Company Ltd confirmed an expansion of its Ejigbo, Lagos safety-footwear facility, lifting output capacity to over 5,000 pairs per day. The added throughput supports faster fulfillment for industrial and institutional buyers and strengthens local supply availability in West Africa. Higher in-region capacity also increases competitive pressure on imported brands in price-sensitive tenders where lead time and serviceability matter.

- June 2026: Adidas and GLO Brands B.V. announced the ADIDAS PRO WORK safety footwear range, with retail availability slated for August 2026, bringing sports-performance design language and metal-free, ESD-oriented positioning into industrial channels. The collaboration expands the competitive landscape for premium safety footwear in industrial procurement, with potential to influence worker acceptance and compliance in regulated environments.

- June 2025: China implemented the revised mandatory footwear testing standard GB 25038-2024, effective 1 June 2025, influencing test planning, labeling, and time-to-market for suppliers serving China-centric industrial customers. Companies are adjusting test plans and lab validation strategies to align with the updated standard.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers industrial protective footwear that is bought and used as personal protective equipment to reduce workplace injuries, including safety shoes and safety boots across major industrial work environments.

Scope exclusions: Everyday casual footwear and fashion-led work boots that are not certified or bought for industrial safety use are excluded from this sizing.

Segmentation Overview

- By Material

- Leather

- Synthetic Leather

- Rubber

- Other Materials

- By Product Type

- Boots (high ankle protection)

- Shoes (low ankle protection)

- By End-User Industry

- Construction

- Manufacturing

- Oil and Gas

- Mining

- Chemicals

- Pharmaceuticals and Healthcare

- Logistics and Transportation

- Utilities and Energy

- Food and Beverage

- Other Industries

- By Distribution Channel

- Online Channel

- Offline Channel

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to keep assumptions tied to real world safety and employment signals. We referenced public sources such as OSHA guidance and injury statistics, ILO labor and employment indicators, Eurostat industry and labor data, and UN Comtrade trade flows for footwear categories, along with standards bodies such as ISO and EN-related documentation for safety requirements.

To make the inputs practical, we also reviewed annual reports, investor presentations, and press releases from relevant manufacturers and distributors, and then mapped these to end user activity in sectors like construction, manufacturing, mining, and oil and gas. In a few places, paid databases were used for company financials and intelligence, shipment-level import and export checks, and patent lookups to understand material and toe cap innovation intensity. The sources listed here are illustrative, and many other public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is actually purchased and replaced in the field, and on testing pricing and mix assumptions across safety shoes versus boots and key material types. We spoke with stakeholders across manufacturers, distributors, safety managers, and procurement teams, and then used follow up calls to reconcile differences by region and end user exposure, so the final model assumptions stayed realistic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 15% | APAC: 51% |

| Mid tier: 50% | Functional/Unit leaders: 33% | EMEA: 31% |

| Smaller Players: 18% | Managers: 52% | Americas: 18% |

Market-Sizing & Forecasting

The core sizing was built using a top-down approach where the demand pool is reconstructed from industrial employment by sector, PPE compliance intensity, and the typical replacement cycle for safety footwear, which is then converted into value using region-specific average selling prices. To make sure the totals did not drift, results were corroborated with selective bottom-up checks such as sampled price lists across channels, distributor feedback on volumes, and manufacturer revenue splits that are clearly attributable to protective footwear.

Key inputs used in the model include industrial workforce levels, construction and manufacturing output trends, workplace safety enforcement and certification adoption, replacement frequency by job risk, and mix shifts between boots and shoes and between leather and rubber based materials. Forecasts were built using scenario analysis, where the path of employment growth and industrial activity is paired with expected ASP progression, and then reviewed with primary respondents so we stayed aligned with how pricing and demand are evolving in their pipelines. When bottom-up checks were incomplete for smaller markets, gaps were handled through ratio-based estimation using nearby country benchmarks and trade flow directionality, and then tested back against the overall regional totals.

Data Validation & Update Cycle

Validation was done in several steps so the market value was not driven by one data stream. We compared modeled demand against independent signals such as import and export movements, changes in sector employment, and channel feedback on price points, and then reviewed variances at the region level before sign-off.

Outliers were flagged when growth or ASP movements looked inconsistent with safety regulation timing, raw material cost direction, or replacement behavior mentioned by respondents, and we re-contacted sources when gaps were material. Reports are refreshed annually, with interim updates when major events can shift industrial activity or pricing assumptions. Before delivery, a final analyst pass is done to ensure the latest macro indicators and currency context are reflected in the published numbers.

Mordor Intelligence's Industrial Protective Footwear Market Size Compared Against Other Published Estimates

Published market values for industrial protective footwear can look far apart because the boundaries and timing choices are not always the same. Differences usually come from what is counted as industrial safety footwear versus adjacent workwear, what year the currency conversion is locked to, and how average selling price is trended over the forecast period.

A refresh-led model reduces drift when input prices and exchange rates move quickly, and it also forces a consistent check between replacement demand and channel pricing at the same point in time, which is why the 2026 value in this study is maintained through an annual update pass and interim checks for material pricing and currency timing before being finalized by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.26 B (2026) | |

| Global Consultancy A | USD 12.05 B (2025) | Uses a different base year and may include broader industrial work footwear categories, so the 2025 value can sit higher when casual work boots and non-certified ranges are not cleanly excluded. The estimate is also sensitive to how ASP inflation is carried from 2024 into 2025 without matching it to replacement cycle checks. |

| Industry Publisher B | USD 10.70 B (2025) | Applies a slower growth path and can understate value if pricing is averaged across regions without adjusting for channel mix and higher priced certified products. In addition, currency conversion timing and limited validation against trade and employment signals can pull the 2025 number downward. |

The spread across the three figures is mainly explained by base year selection, how tightly certified industrial safety footwear is separated from adjacent work footwear, and how ASP is carried forward with currency consistency. By anchoring demand to industrial workforce exposure and replacement behavior, and then checking pricing and mix through primary feedback and external signals, our estimate stays traceable to a few repeatable steps instead of relying on one broad multiplier.

Key Questions Answered in the Report

What is the current value of the industrial protective footwear market?

The market was valued at USD 11.26 billion in 2026 and is forecast to hit USD 14.41 billion by 2031.

Which region is growing fastest for protective footwear demand?

Asia-Pacific is projected to register the quickest growth at a 7.18% CAGR through 2031 due to infrastructure expansion and tightening safety enforcement.

Why are smart safety boots gaining traction?

IoT-enabled boots provide real-time location and fatigue data, helping employers cut incident rates and justify higher purchase prices with measurable safety gains.

Which end-user sector leads consumption?

Construction remains the largest consumer, holding 20.61% share in 2025, driven by global infrastructure projects that mandate protective footwear on every site.

What challenges limit adoption in emerging markets?

Counterfeit products and high price sensitivity among small contractors suppress premium-boot uptake, especially where regulatory enforcement is limited.

Page last updated on: