Industrial Safety Gloves Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

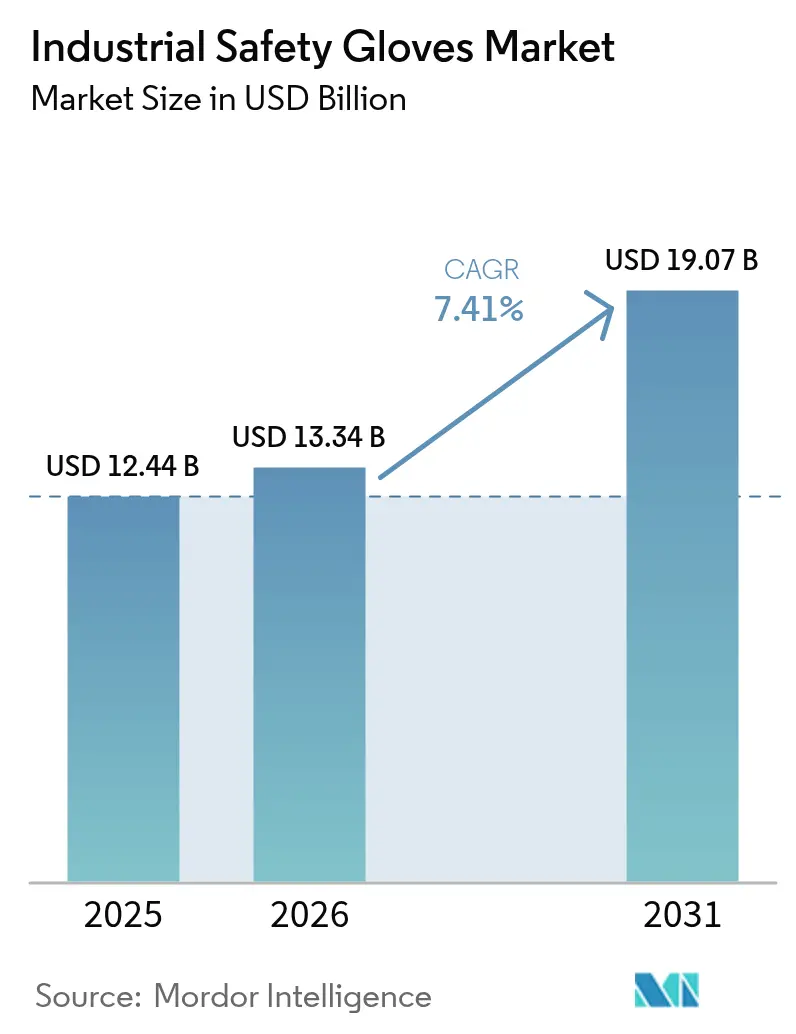

| Market Size (2026) | USD 13.34 Billion |

| Market Size (2031) | USD 19.07 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Industrial Safety Gloves Market Analysis by Mordor Intelligence

The global industrial safety gloves market size was valued at USD 12.44 billion in 2025 and estimated to grow from USD 13.34 billion in 2026 to reach USD 19.07 billion by 2031, registering a compound annual growth rate (CAGR) of 7.41% during the forecast period 2026-2031. The global industrial safety gloves market is growing due to increased workplace safety awareness and the enforcement of stricter occupational protection regulations across industries such as manufacturing, construction, oil & gas, healthcare, and chemicals. Rapid industrialization and automation have heightened worker exposure to mechanical, chemical, thermal, and biological hazards, driving the adoption of task-specific protective gloves, including cut-resistant, chemical-resistant, and heat-resistant types. Additionally, the expansion of e-commerce logistics and warehousing has increased the need for hand protection in material handling activities. The healthcare sector also continues to demand high-performance disposable gloves for hygiene control. Innovations in materials such as nitrile, neoprene, and high-performance fibers have enhanced durability, comfort, and grip, leading to higher replacement rates and broader adoption, thereby contributing to market growth.

Key Report Takeaways

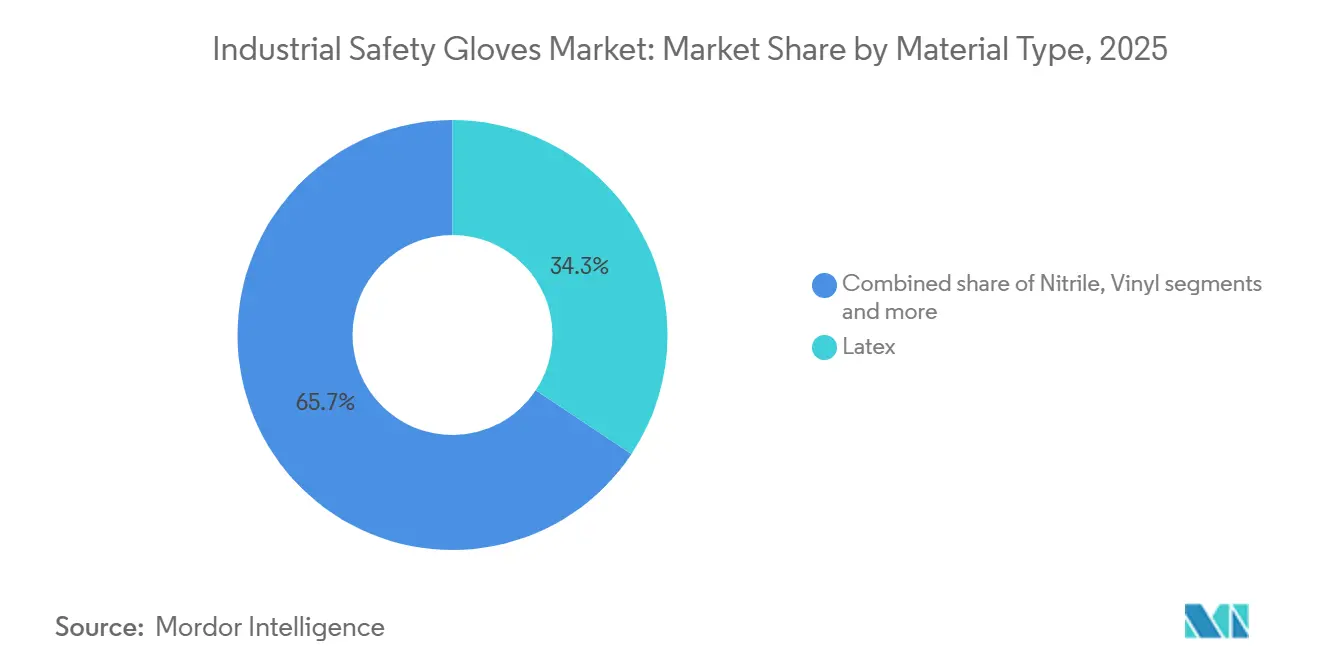

- By material type, latex captured 34.34% of 2025 industrial safety gloves market share while HPPE is projected to expand at an 8.67% CAGR during 2026-2031.

- By product type, reusable gloves led with 76.88% of 2025 revenue; disposable gloves are forecast to grow at an 8.13% CAGR through 2031.

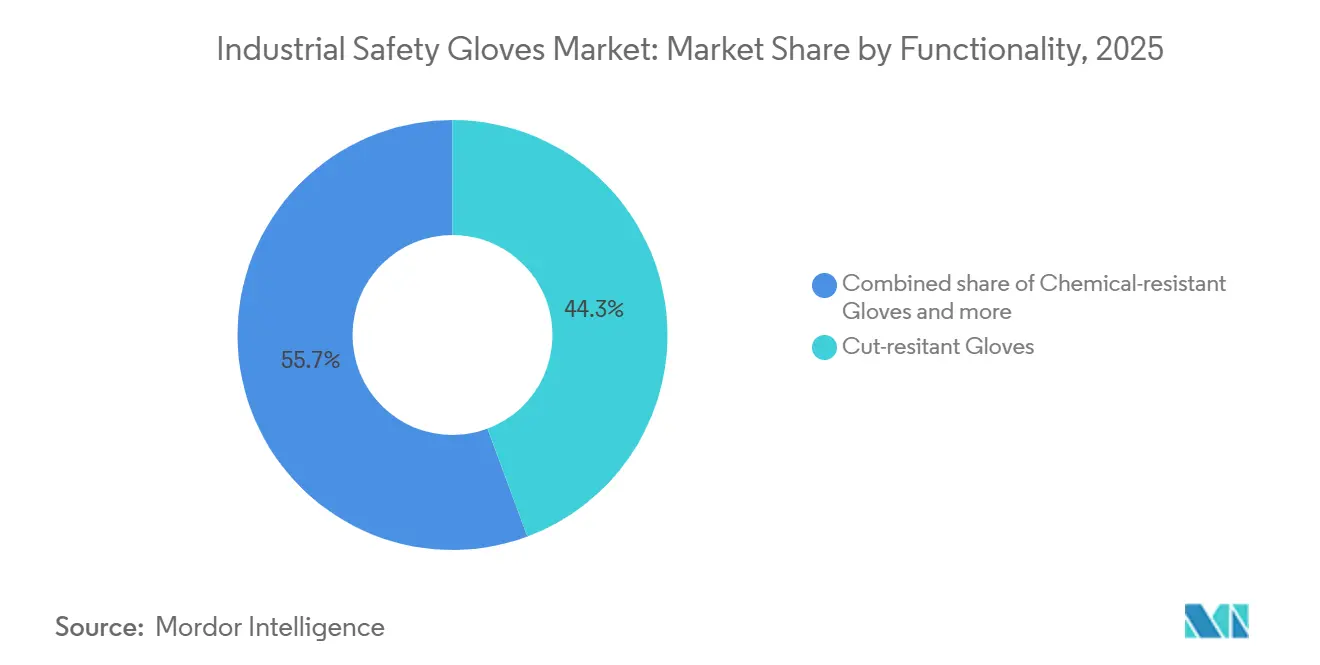

- By functionality, cut-resistant gloves accounted for 44.32% share in 2025 and heat- and flame-resistant gloves are advancing at an 8.85% CAGR to 2031.

- By end-user, automotive held 24.54% of 2025 demand, whereas pharmaceutical manufacturing is poised for an 8.91% CAGR between 2026-2031.

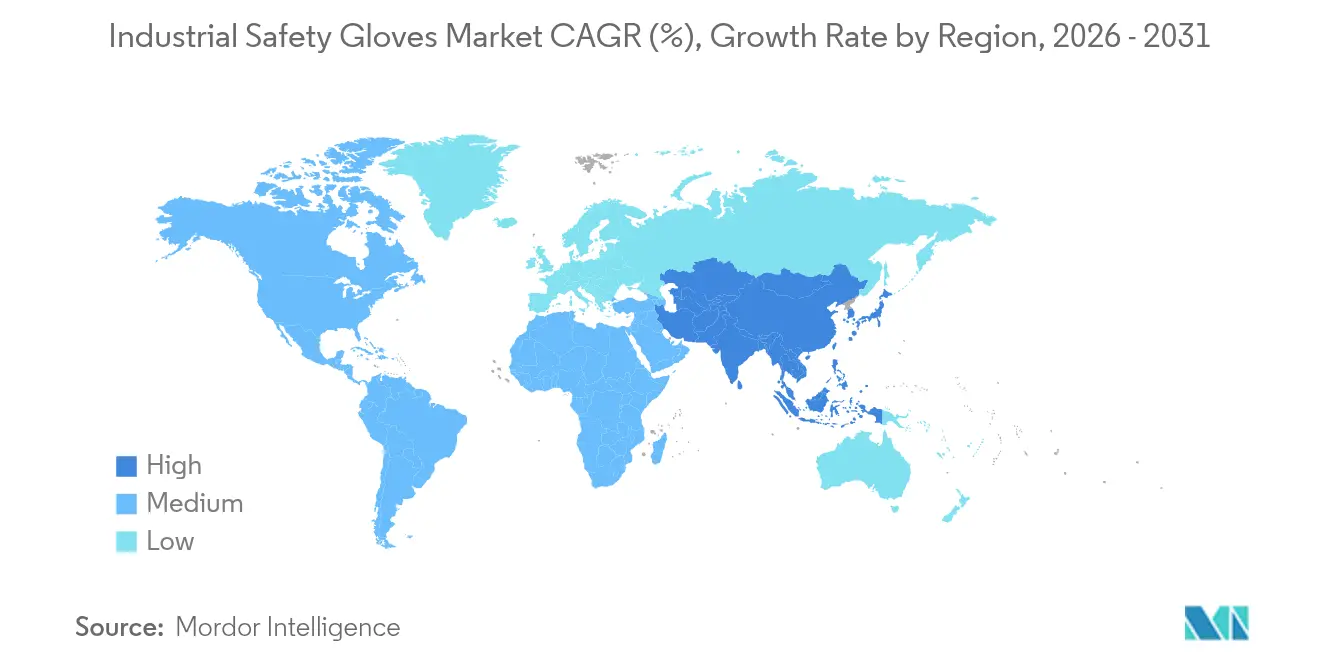

- By geography, North America commanded 32.44% of value in 2025; Asia-Pacific is the fastest-growing region at an 8.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Safety Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict global workplace health and safety rules | +1.8% | Global, with strongest enforcement in North America and European Union | Medium term (2-4 years) |

| Growing focus on employee safety and protection | +1.3% | Global, particularly in developed markets | Long term (≥ 4 years) |

| Expansion of industries such as automotive, construction, mining, chemicals, and oil & gas | +1.5% | Asia-Pacific core, spillover to Middle East and South America | Medium term (2-4 years) |

| Increasing industrial accidents and injury incidents | +1.0% | Global, with higher incidence in emerging manufacturing hubs | Short term (≤ 2 years) |

| Advancements in glove materials | +1.6% | Global, led by innovation centers in North America and Europe | Long term (≥ 4 years) |

| Higher demand for disposable gloves, particularly in healthcare and pharma sectors | +1.4% | North America, Europe, and Asia-Pacific pharmaceutical clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict global workplace health and safety rules

Stricter occupational safety regulations globally are driving the demand for industrial safety gloves, as companies are required to provide adequate hand protection to prevent injuries and avoid legal repercussions. Regulatory authorities are intensifying inspections, enforcing compliance standards, and imposing higher financial penalties, prompting employers to standardize personal protective equipment in industries such as manufacturing, construction, and chemical handling. For instance, the Occupational Safety and Health Administration (OSHA) set the maximum penalty for a serious violation at USD 16,550 per violation in 2025, significantly increasing the cost of non-compliance[1]Source: Occupational Safety and Health Administration, "OSHA Penalties," osha.gov. Consequently, organizations are increasingly adopting certified protective gloves as a preventive measure, contributing to market growth.

Expansion of industries such as automotive, construction, mining, chemicals, and oil & gas

The expansion of labor-intensive and hazard-prone industries significantly drives the demand for industrial safety gloves, as workers often handle sharp tools, heavy materials, oils, solvents, and high-temperature equipment. These industries include manufacturing, construction, automotive, and chemical processing, where the risk of injuries is high due to the nature of tasks performed. Increasing production capacities and infrastructure projects necessitate protective hand gear to minimize injury risks and ensure uninterrupted operations. For example, according to data published by India’s Ministry of Heavy Industries in February 2026, referencing the Society of Indian Automobile Manufacturers (SIAM), the automobile industry alone accounts for nearly 15% of the country’s GST revenue and supports approximately 30 million jobs across the value chain[2]Source: Ministry of Heavy Industries, "STATUS OF HEAVY INDUSTRIES SECTOR," pib.gov.in. The scale of such extensive industrial workforces sustains the consistent procurement of protective gloves to safeguard workers and comply with regulations. Additionally, stringent safety standards and government regulations further emphasize the importance of using industrial safety gloves in these sectors to prevent workplace accidents and ensure employee well-being.

Advancements in glove materials

Advancements in glove materials are driving the increased adoption of industrial safety gloves by enhancing both protection and usability. Manufacturers are introducing high-performance fibers, engineered polymers, and multi-layer coatings that offer improved resistance to cuts, punctures, chemicals, and heat, while maintaining a lightweight and flexible design. Features such as enhanced breathability, improved grip in oily conditions, touchscreen compatibility, and ergonomic fit help reduce worker fatigue and boost productivity, encouraging consistent glove usage during tasks. Additionally, longer durability and washable designs reduce replacement frequency, making these gloves more cost-effective for employers. These improvements in performance and comfort are expanding their application in precision manufacturing, electronics, automotive assembly, and chemical handling, thereby driving market growth.

Higher demand for disposable gloves, particularly in healthcare and pharma sectors

The increasing hygiene and contamination-control requirements in healthcare and pharmaceutical production are driving the rising demand for disposable safety gloves. Hospitals, laboratories, and pharmaceutical manufacturing facilities depend on single-use gloves to prevent cross-contamination among personnel, equipment, and sterile products, necessitating frequent replacements during daily operations. Regulatory guidelines further support this practice. For instance, the U.S. FDA’s Guidance for Industry: Sterile Drug Products Produced by Aseptic Processing - Current Good Manufacturing Practice recommends that sterile gloves be regularly sanitized or replaced after initial gowning to reduce contamination risks[3]Source: Food and Drug Administration , "Guidance for Industry: Sterile Drug Products Produced by Aseptic Processing - Current Good Manufacturing Practice," fda.gov. These stringent procedural standards lead to consistent, high-volume glove usage, positioning disposable gloves as a significant growth driver in the global industrial safety gloves market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating and increasing prices of latex, nitrile, and polymer inputs | -1.2% | Global, most acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Strong competition from low-cost, lower-quality manufacturers | -0.9% | Asia-Pacific and Middle East, with spillover to price-sensitive segments globally | Medium term (2-4 years) |

| Commoditization causing pricing pressure and reduced margins | -0.7% | Global, particularly affecting mid-tier manufacturers | Long term (≥ 4 years) |

| Low PPE awareness and adoption in many emerging markets | -0.5% | South Asia, Sub-Saharan Africa, and parts of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating and increasing prices of latex, nitrile, and polymer inputs

Fluctuations in the prices of key raw materials, including natural latex, nitrile rubber, and synthetic polymers, pose a challenge to the industrial safety gloves market by increasing production costs and reducing pricing stability. These materials rely on petrochemical feedstocks and agricultural supply conditions, making them vulnerable to crude oil price fluctuations, weather-related disruptions, and supply chain issues. Sudden cost increases strain manufacturers' profit margins and often result in higher product prices for end users, discouraging bulk purchases, particularly among small and medium-sized industries. Unstable input costs also complicate long-term contracts and inventory management, delaying purchasing decisions and hindering consistent market growth.

Strong competition from low-cost, lower-quality manufacturers

Intense competition from low-cost producers, particularly unorganized or non-certified manufacturers, constrains the global industrial safety gloves market by exerting downward pressure on pricing and reducing profit margins for established brands. These suppliers often provide low-cost products that attract cost-sensitive buyers, despite not meeting durability or safety performance standards. Consequently, premium manufacturers face challenges in demonstrating value and justifying higher prices, especially in developing industrial regions where procurement decisions are primarily cost-driven. This competitive landscape discourages investment in advanced materials and innovation, while also hindering the adoption of certified high-performance gloves, ultimately restricting overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: HPPE Disrupts Latex Dominance

The latex segment accounted for a 34.34% market share in 2025, while High-Performance Polyethylene (HPPE) industrial safety gloves are projected to grow at a rate of 8.67% during the forecast period from 2026 to 2031. The demand for latex industrial safety gloves is driven by their superior elasticity, tactile sensitivity, and secure grip, making them ideal for precision handling tasks in sectors such as healthcare, food processing, laboratories, and light manufacturing. Their snug fit enhances dexterity and reduces worker fatigue, promoting consistent use during repetitive tasks. Additionally, latex gloves provide effective protection against biological contaminants and mild chemicals, while being cost-efficient compared to many synthetic alternatives. This combination of comfort, hygiene control, and affordability makes them a practical choice for high-volume, single-use applications.

The growth of HPPE industrial safety gloves is attributed to increasing demand for advanced cut-resistant protection in heavy-duty industries such as metal fabrication, automotive assembly, glass handling, and construction. HPPE fibers offer a high strength-to-weight ratio, enabling gloves to remain lightweight and flexible while providing protection against sharp edges and abrasion. Their durability, extended service life, and resistance to oils and mechanical stress reduce the frequency of replacements and enhance productivity. These attributes make HPPE gloves an appealing option for employers prioritizing worker safety and long-term cost efficiency.

By Product Type: Disposable Gains Despite Reusable Lead

Reusable gloves commanded 76.88% of market value in 2025, reflecting their dominance in automotive assembly, construction, and general manufacturing, where multi-shift durability and launderability deliver lower per-use costs. Yet disposable gloves are expanding at 8.13% annually through 2031, driven by pharmaceutical cleanroom protocols, food safety regulations, and healthcare infection control standards that mandate single-use products. The demand for reusable industrial safety gloves is primarily driven by heavy-duty industries such as construction, metalworking, mining, and oil & gas, where workers are regularly exposed to risks like abrasion, cuts, heat, and chemicals. Employers favor durable gloves made from coated fabrics, leather, or engineered fibers due to their longer lifespan, cost-effectiveness by reducing frequent replacements, and enhanced protection for high-risk tasks. Additionally, sustainability initiatives promote the use of reusable gloves, as they produce less waste and support extended operational cycles while maintaining safety standards.

The demand for disposable industrial safety gloves is increasing due to stringent hygiene and contamination-control requirements in industries such as healthcare, pharmaceuticals, food processing, laboratories, and cleanroom manufacturing. These industries rely on single-use gloves to prevent cross-contact between workers, equipment, and sensitive products, necessitating frequent glove changes during routine operations. Their ease of use, consistent cleanliness, and ready availability make them indispensable for short-duration tasks and environments where strict sanitation standards must be upheld.

By Functionality: Heat Resistance Surges on Battery Manufacturing

Cut-resistant gloves accounted for 44.32% of the functionality segment in 2025, driven by demand from automotive assembly, construction, and metal fabrication industries. However, heat and flame-resistant variants are projected to grow at the fastest rate, with an annual growth of 8.85% through 2031. Cut-resistant gloves are increasingly in demand in industries where workers handle sharp materials, including sheet metal, glass, blades, and engineered components. Sectors such as manufacturing, automotive assembly, logistics, warehousing, and construction require gloves that protect against lacerations while maintaining dexterity for precise tasks. The use of automated cutting tools and faster production lines has heightened the risk of injuries, prompting employers to provide high-strength fiber gloves that offer both flexibility and reliable mechanical protection, thereby reducing accidents and minimizing downtime.

Heat and flame-resistant gloves are primarily used in applications involving high temperatures, sparks, and molten materials, such as welding, foundries, forging, glass production, and oil and gas maintenance. These gloves enable workers to handle hot equipment and surfaces safely without compromising grip or dexterity. The adoption of insulated and flame-retardant materials is driven by stricter fire-safety regulations and the need to prevent burn injuries. Companies increasingly rely on specialized thermal protective gloves to enhance worker safety and ensure uninterrupted operations in high-temperature environments.

By End-User: Pharmaceutical Outpaces Automotive

The automotive sector held a 24.54% share among end-users in 2025, the largest across all categories. However, pharmaceutical manufacturing is expected to grow at the fastest rate of 8.91% annually through 2031. The automotive industry involves significant manual handling of metal parts, tools, lubricants, and assembly equipment, posing risks such as cuts, abrasions, and oil exposure. Workers engaged in welding, stamping, painting, and component assembly require gloves that ensure grip, dexterity, and mechanical protection while maintaining productivity. The rise in vehicle production, intricate component designs, and the adoption of automated machinery have heightened safety demands, leading manufacturers to standardize protective gloves across assembly lines to minimize injuries and avoid production disruptions.

Pharmaceutical facilities require stringent contamination control and sterile handling during drug formulation, packaging, and laboratory testing, necessitating the consistent use of safety gloves. Employees must avoid direct contact with active ingredients, chemicals, and sterile products, which demands frequent glove changes and adherence to high hygiene standards. Compliance with quality assurance protocols and cleanroom practices drives the use of certified protective gloves to ensure product integrity, worker safety, and regulatory compliance throughout manufacturing processes.

Geography Analysis

North America commanded 32.44% of global market value in 2025, sustained by stringent OSHA enforcement, high PPE compliance rates, and a shift toward premium-performance gloves in automotive and pharmaceutical manufacturing. In North America, the demand for industrial safety gloves is driven by the region's emphasis on workplace liability prevention and compliance with insurance regulations. Companies actively invest in protective equipment to minimize compensation claims and legal risks. Additionally, the increasing use of advanced manufacturing technologies, such as robotics and precision equipment, necessitates specialized hand protection that supports fine motor control during human-machine interactions. The presence of large, organized distributors and safety supply contracts promotes standardized procurement of personal protective equipment (PPE) across multi-site enterprises. Furthermore, workforce training programs and union safety practices contribute to consistent glove usage in industrial facilities.

Asia-Pacific is expanding at 8.53% annually through 2031, the fastest among all regions, driven by manufacturing capacity additions in China, India, and Southeast Asia and by improving regulatory enforcement in developed markets like Japan, South Korea, and Australia. In the Asia-Pacific region, the industrial safety gloves market is primarily driven by the rapid growth of small and medium-scale manufacturing clusters and contract production hubs. These facilities, which supply global brands, are required to adhere to buyer audit standards for worker protection. Export-oriented factories are increasingly adopting standardized protective equipment to comply with international sourcing requirements and pass third-party compliance inspections. Additionally, the expansion of technical education and vocational training programs is raising awareness of workplace injury prevention among new workers. The development of organized industrial parks and special economic zones further supports centralized procurement of protective gear, ensuring steady demand for gloves across the region.

In Europe, the industrial safety gloves market is driven by a strong focus on worker ergonomics and long-term occupational health. Companies are adopting protective gear designed to minimize strain and enhance comfort during prolonged work shifts. Employers are increasingly incorporating safety equipment into productivity initiatives, prioritizing gloves that improve grip precision and reduce handling errors in high-quality manufacturing sectors such as machinery, aerospace components, and precision engineering. Additionally, sustainability objectives are fostering the adoption of recyclable and responsibly sourced protective products. Structured worker training and certification programs further support the consistent use of protective equipment across industrial workplaces.

Competitive Landscape

The global industrial safety gloves market is moderately consolidated, with major multinational manufacturers such as 3M, Ansell, Honeywell, Top Glove, and Radians, Inc. dominating the market. These companies leverage extensive product portfolios and global distribution networks to maintain strong relationships with large industrial buyers. They focus on providing certified, application-specific protection and consistent product quality. Meanwhile, numerous regional and private-label manufacturers compete intensely, particularly in price-sensitive segments, creating ongoing competitive pressure in standard protective glove categories.

Market competition is characterized by two distinct strategies. Established international brands prioritize expanding high-performance product lines, enhancing technical capabilities, and differentiating through advanced materials and specialized designs tailored for demanding industrial applications. On the other hand, smaller and regional manufacturers focus on cost-efficient production and competitive pricing to secure volume contracts, particularly in markets where affordability takes precedence over advanced performance features.

Innovation plays a key role in market differentiation, with manufacturers developing multifunctional protection solutions and ergonomically designed gloves for complex industrial tasks. Efforts are also directed toward connected protective equipment and advancements in material engineering to improve durability and user comfort. However, the adoption of advanced solutions remains gradual, as buyers often weigh performance benefits against cost considerations. This dynamic allows both premium and value-oriented suppliers to coexist within the competitive landscape.

Industrial Safety Gloves Industry Leaders

-

3M Corporation

-

Ansell Limited

-

Top Glove Corporation Berhad

-

Honeywell International Inc.

-

Radians, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hyderabad-based Wadi Surgicals, a prominent Indian manufacturer of nitrile gloves, launched accelerator-free nitrile gloves under its Enliva brand, representing a notable product development. Developed through extensive research and international technical collaboration, these gloves are the first of their kind in India, offering enhanced hand protection by reducing skin irritation and allergy risks.

- May 2025: Wadi Surgicals, a Hyderabad-based nitrile gloves manufacturer, has launched India’s first accelerator-free nitrile gloves under its flagship brand, Enliva. Developed through extensive R&D, these gloves eliminate chemical accelerators like thiurams, carbamates, and MBTs, which are linked to allergic contact dermatitis. Manufactured with non-sensitizing crosslinking agents, the gloves ensure dermatological safety, mechanical strength, and chemical resistance.

- April 2025: China-based Intco Medical launched its proprietary Syntex synthetic disposable latex gloves in the global market, offering an alternative to traditional natural latex products. The Syntex range is designed to improve performance, safety, and durability while addressing the limitations of natural latex materials. These gloves meet EN455 and EN374 standards and comply with FDA and EU CE regulations, making them suitable for use in healthcare, food handling, and industrial safety applications.

- April 2024: MAPA Professional introduced Ultrane 664 eco-designed gloves featuring recycled polyester construction, addressing sustainability requirements in industrial applications. The product launch reflects growing environmental consciousness in PPE procurement decisions.

- April 2024: Medicom inaugurated its EUR 88 million ManiKHeir nitrile glove facility in Bessé-sur-Braye, France. This marks Europe's inaugural single-use nitrile glove manufacturing plant, boasting an impressive annual capacity of 900 million gloves. Designed to bolster the European supply chain, the facility incorporates advanced features like integrated water treatment systems and recyclable nitrile rubber technology, addressing vulnerabilities laid bare during the pandemic.

- February 2024: Ansell had launched the MICROFLEX® Mega Texture 93-256, an ultra-textured nitrile disposable glove. This orange glove ensured industrial workers enjoyed a confident grip alongside durable protection. Auto shop workers, in particular, found it ideal due to its tear resistance, high visibility, and enhanced grip. The MICROFLEX® 93-256 acted as a crucial barrier for automotive workers, shielding them from everyday hazards like oils, grime, chemicals, and even carcinogens.

Global Industrial Safety Gloves Market Report Scope

Industrial safety gloves are personal protective equipment worn during work projects that cover and protect the hands from the wrist to the fingers. The industrial safety gloves market is segmented by Material Type, Product Type, End-user, and by Geography. Based on material type, it is segmented into latex, nitrile, HPPE, and other material types. By product type market is segmented into reusable gloves and disposable gloves. By end-user, the market is further segmented into automotive, construction, food industry, pharmaceutical, mining, oil and gas, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

| Latex |

| Nitrile |

| High-Performance Polyethylene (HPPE) |

| Vinyl |

| Neoprene |

| Others |

| Disposable Gloves |

| Reusable Gloves |

| Cut-resitant Gloves |

| Chemical-resistant Gloves |

| Heat/Flame-resistant Gloves |

| Others |

| Automotive |

| Construction |

| Food Industry |

| Pharmaceutical |

| Mining |

| Oil and Gas |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Russia | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Material Type | Latex | |

| Nitrile | ||

| High-Performance Polyethylene (HPPE) | ||

| Vinyl | ||

| Neoprene | ||

| Others | ||

| By Product Type | Disposable Gloves | |

| Reusable Gloves | ||

| By Functionality | Cut-resitant Gloves | |

| Chemical-resistant Gloves | ||

| Heat/Flame-resistant Gloves | ||

| Others | ||

| By End-User | Automotive | |

| Construction | ||

| Food Industry | ||

| Pharmaceutical | ||

| Mining | ||

| Oil and Gas | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will global demand for industrial safety gloves grow from 2026 to 2031?

Aggregate consumption value is expected to rise at a 7.41% CAGR, lifting the industrial safety gloves market size from USD 13.34 billion to USD 19.07 billion.

Which material will gain the most share by 2031?

HPPE gloves are projected to record the highest growth, expanding at 8.67% annually as automotive and construction buyers upgrade to ANSI A9 cut levels.

Which region will add the largest absolute revenue over the forecast window?

Asia-Pacific is forecast to grow at 8.53% a year, benefiting from new manufacturing lines in China, India and Vietnam along with tightening regional standards.

Which end-user segment shows the strongest growth potential?

Pharmaceutical manufacturing registers the fastest 8.91% CAGR because biomanufacturing expansion and GMP rules demand specialized chemical-resistant disposable gloves.

Page last updated on: