United States Hand Sanitizer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

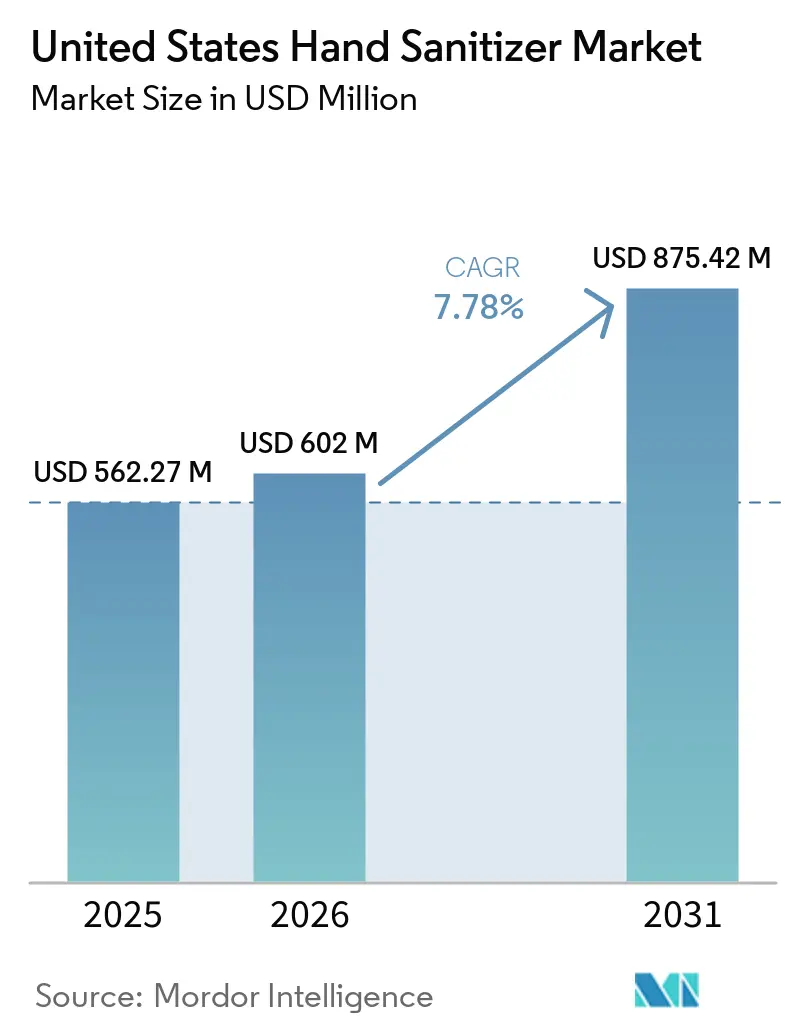

| Base Year Market Size (2025) | USD 562.27 Million |

| Market Size (2026) | USD 602 Million |

| Market Size (2031) | USD 875.42 Million |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

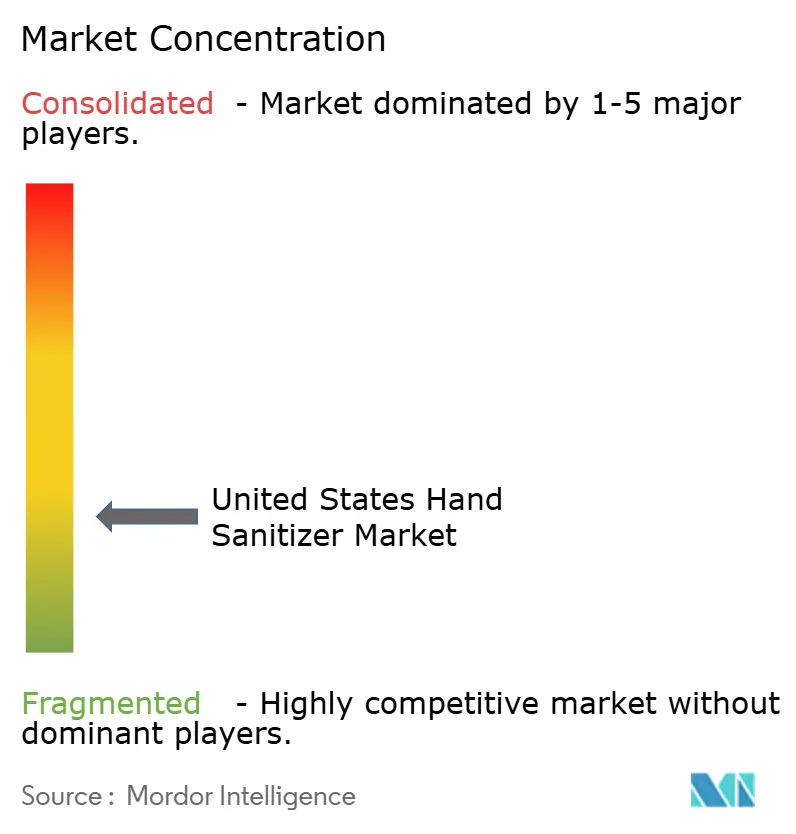

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Hand Sanitizer Market Analysis by Mordor Intelligence

The United States hand sanitizer market size is expected to grow from USD 562.27 million in 2025 to USD 602 million in 2026 and is forecast to reach USD 875.42 million by 2031, at a 7.78% CAGR over 2026-2031. The United States hand sanitizer market is entering a more mature phase, with growth increasingly driven by product innovation and consumer demand for premium, skin-friendly solutions. The Centers for Disease Control and Prevention (CDC) continues to recommend alcohol-based sanitizers with at least 60% ethanol as the preferred hand hygiene option when soap and water are unavailable, reinforcing their relevance across retail and institutional channels[1]Source: Centers for Disease Control and Prevention (CDC), "Hand Sanitizer Facts," cdc.gov. Evolving formulations, including natural, moisturizing, and dermatologist-tested variants, are strengthening the category’s value proposition. At the same time, increasing awareness of skin health concerns and the limitations of repeated alcohol use is supporting consumer demand for gentler alternatives. Institutional procurement cycles also sustain stable demand by ensuring consistent replenishment across healthcare, foodservice, and corporate environments. These factors indicate a resilient and increasingly differentiated market, where innovation and premiumization remain key drivers of sustained market relevance.

Key Report Takeaways

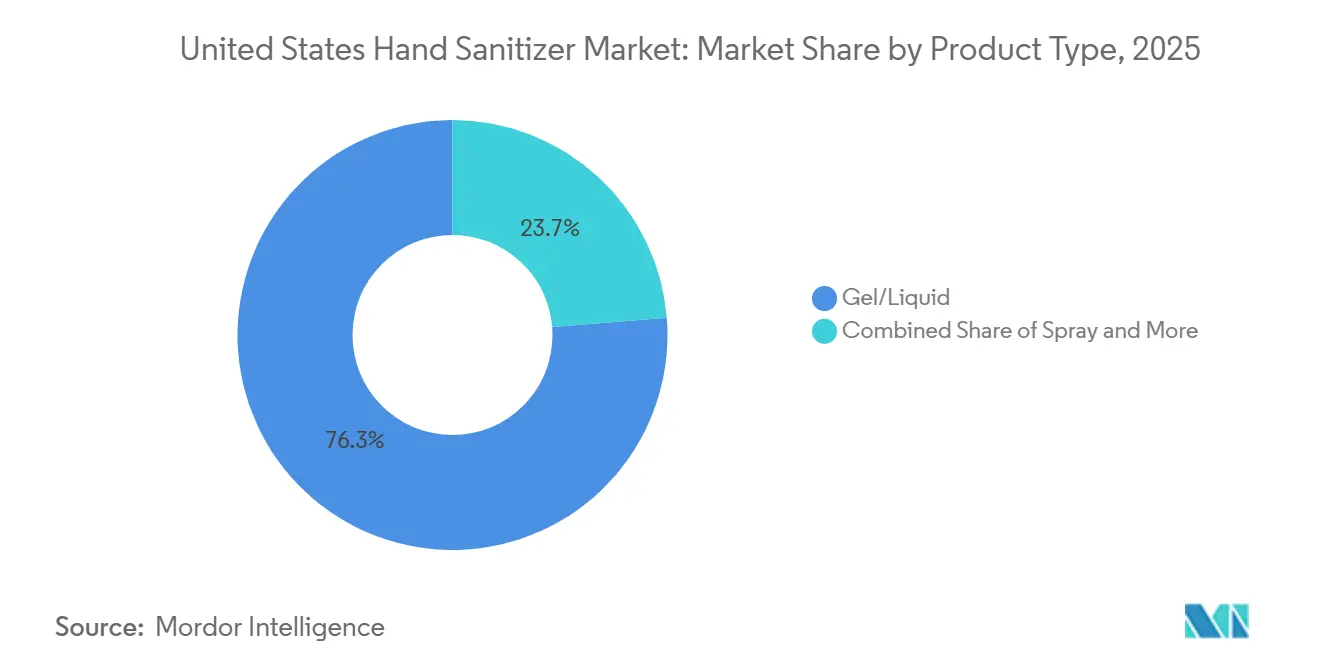

- By product type, gel/liquid led the United States hand sanitizer market with a share of 76.27% in 2025, while spray is anticipated to register the fastest CAGR of 8.46% during 2026-2031.

- By end user, adults retained 87.74% share in 2025, whereas kids/children are forecast to expand at a 8.99% CAGR through 2031.

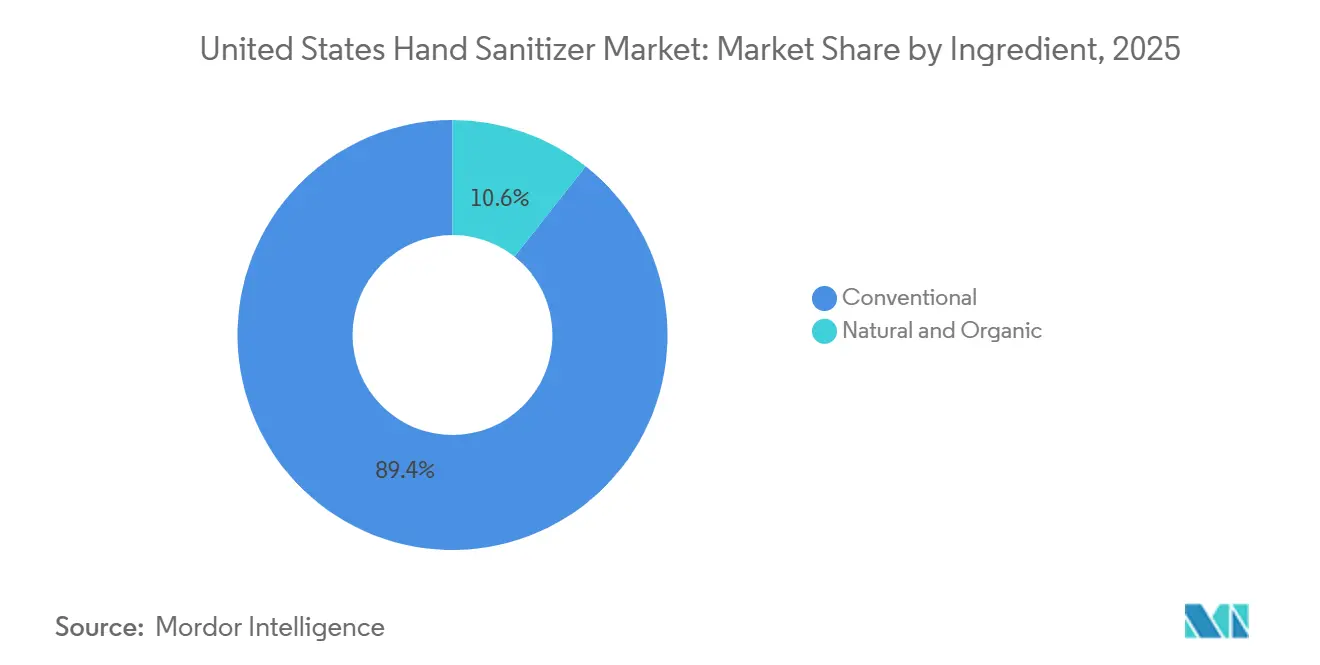

- By ingredients, conventional held 89.37% of 2025 revenue, but natural and organic are expected to grow fastest at 8.79% through 2031.

- By end use, commercial led the United States hand sanitizer market with a share of 59.83% in 2025, and is anticipated to register the fastest CAGR of 8.32% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Hand Sanitizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward skin-friendly and naturally derived sanitizer formulations | +1.6% | National; strongest concentration in West Coast and Northeast metro markets | Medium term (2-4 years) |

| Popularity of portable and on-the-go hand hygiene solutions | +1.3% | National; elevated intensity in urban cores: New York, Los Angeles, Chicago, Houston | Short term (≤ 2 years) |

| Increasing hand hygiene awareness among families with young children | +1.0% | National; suburban growth corridors in Southeast and Mountain West showing fastest uptake | Medium term (2-4 years) |

| Commercial hygiene standards sustaining institutional sanitizer demand | +1.3% | National; healthcare-dense states: California, Texas, Florida, New York | Long term (≥ 4 years) |

| Adoption of eco-friendly and refillable packaging solutions | +0.5% | West Coast–led; policy-driven momentum in California and Washington with Northeast spill-over | Medium term (2-4 years) |

| Consumer preference for fast-drying, non-sticky gel and spray formulations | +0.4% | National; United States consumer preference skewing toward gel parity in retail and spray in portable formats | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift toward skin-friendly and naturally derived sanitizer formulations

The United States hand sanitizer market is increasingly influenced by consumers shifting toward skin-friendly and naturally derived formulations, as preference for conventional ethanol-based products declines. According to studies by the National Center for Biotechnology Information (NCBI), repeated use of alcohol-based virucidal sanitizers can significantly affect skin health by reducing skin hydration and increasing erythema and transepidermal water loss, with mean hydration changes exceeding 10 arbitrary units (AU) after just three days of repeated application[2]Source: National Center for Biotechnology Information, "The Effect of Alcohol‐Based Virucidal Hand Sanitizers on Skin Barrier Function—A Randomised Experimental Study," pmc.ncbi.nlm.nih.gov. These findings have strengthened consumer concerns and accelerated demand for clean-label products enriched with aloe vera, vitamin E, and plant-based alcohol, positioning them as premium alternatives in the marketplace. Brands that align effectively with these skin-health claims are capturing higher-value segments, while manufacturers focused only on conventional product refinements risk losing relevance in a market increasingly shaped by innovation and premiumization.

Popularity of portable and on-the-go hand hygiene solutions

The United States hand sanitizer market is increasingly influenced by rising demand for portable and on-the-go hygiene solutions. Compact sprays and mini bottles are becoming independent purchase drivers rather than impulse add-ons. These formats have expanded across mainstream retail channels and subscription models, creating a recurring replenishment cycle that complements institutional bulk purchasing. Church & Dwight’s acquisition of Touchland for up to USD 880 million, with completion indicated for 2025 and Touchland generating USD 130 million in annual revenue, represents a strategic investment in the premium, design-led portable format category. The deal highlights the commercial value of aesthetics, fragrance variety, and packaging differentiation. Among younger urban consumers, hand sanitizer has effectively become a personal care accessory, influenced by the same purchase criteria as skincare. This shift positions portability as a key driver of customer loyalty and brand equity. As a result, future growth will depend as much on lifestyle alignment and design credibility as on functional efficacy.

Increasing hand hygiene awareness among families with young children

The United States hand sanitizer market is evolving as households with young children place greater emphasis on school-age hygiene as a deliberate and essential priority. Published toxicological evidence confirms that conventional alcohol-based sanitizers pose a disproportionate skin-safety risk for pediatric users due to higher dermal absorption rates, thinner epidermal barriers, and the risk of accidental ingestion, as documented in peer-reviewed literature published by the National Center for Biotechnology Information[3]Source: National Center for Biotechnology Information, "Toxicity of chemical-based hand sanitizers on children and the development of natural alternatives: a computational approach," pmc.ncbi.nlm.nih.gov. In response, brands such as The Honest Company and Babyganics offer gentle formulations based on benzalkonium chloride and plant-derived active ingredients, often supported by clean-label or organic certifications that help build parental confidence. These products hold premium positioning in direct-to-consumer and specialty retail channels, reflecting parents’ willingness to prioritize safety over price sensitivity. Beyond near-term demand, this shift is shaping long-term consumer behavior, as children who regularly use non-alcoholic or natural sanitizers are likely to carry those preferences into adulthood, supporting sustained brand loyalty and influencing the broader market trajectory beyond the current forecast horizon.

Commercial hygiene standards sustaining institutional sanitizer demand

The United States hand sanitizer market continues to benefit from commercial hygiene standards that sustain institutional demand and structurally insulate this segment from consumer behavioral cycles. Healthcare facilities remain the most procurement-locked sub-segment, as the Centers for Disease Control and Prevention’s updated 2024 hand hygiene guidelines recommend alcohol-based sanitizers as the preferred clinical method unless hands are visibly soiled[4]Source: Centers for Disease Control and Prevention (CDC), "Clinical Safety: Hand Hygiene for Healthcare Workers," cdc.gov. This recommendation creates a near-mandatory usage occasion and drives scheduled replenishment. Persistent compliance gaps in hospitals continue to support innovation in dispenser technology, as demonstrated by SC Johnson Professional’s planned July 2025 launch of Alcare Extra with OPTIDOSE, a clinically dosed system designed to improve adherence. Beyond healthcare, the United States Food and Drug Administration safety requirements govern the foodservice sector and mandate sanitizer availability at food-contact points, ensuring recurring replenishment cycles that remain resilient to discretionary consumer cutbacks. The Clorox-GOJO combination further strengthens institutional consolidation by using bundled dispenser-and-refill arrangements to reinforce incumbent positions in group purchasing contracts, underscoring the durability of institutional demand as a core driver of market stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer reliance on soap-and-water handwashing | -0.7% | National; stronger drag in rural and suburban markets with high household soap attachment | Long term (≥ 4 years) |

| Skin dryness and irritation associated with alcohol-based sanitizers | -0.5% | National; elevated clinical relevance in healthcare worker populations across major metro areas | Medium term (2-4 years) |

| Strict FDA oversight on product claims and ingredient compliance | -0.4% | National; disproportionately impacts smaller manufacturers and new market entrants | Medium term (2-4 years) |

| Sustainability concerns surrounding single-use plastic packaging | -0.3% | West Coast–led (California, Oregon, and Washington); emerging in Northeast; regulatory acceleration anticipated after 2026 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer reliance on soap-and-water handwashing

The United States hand sanitizer market faces a structural restraint as consumers continue to rely on soap-and-water handwashing. The Centers for Disease Control and Prevention continues to recommend handwashing for visibly soiled hands and positions hand sanitizers as an alternative when sinks are unavailable. This guidance reinforces the perception of hand sanitizers as situational products rather than habitual-use products in household settings, limiting product velocity among demographic groups with consistent access to sink infrastructure. Although hand sanitizers offer clear advantages, including improved compliance, no-rinse convenience, and reduced irritation compared to detergent-based soaps, brands have not communicated these benefits effectively to general consumers. This communication gap has limited consumer persuasion. To address this, brands need to invest in consumer education that goes beyond germ-kill claims and supports the development of habitual usage occasions, particularly in domestic, childcare, and outdoor contexts where portable formats can offer clear convenience over traditional handwashing.

Skin dryness and irritation associated with alcohol-based sanitizers

The United States hand sanitizer market faces a restraint due to skin dryness and irritation associated with the frequent use of alcohol-based formulations, as growing clinical evidence highlights their impact on the skin barrier. Research published in Cureus and other peer-reviewed studies links high-frequency sanitizer use to dryness, cracking, and contact dermatitis. These conditions stem from ethanol’s lipid-emulsifying properties, which deplete the protective layer of the stratum corneum. For healthcare workers and other professionals with intensive hand hygiene routines, this issue represents an occupational health concern rather than a cosmetic problem, creating pressure to shift toward benzalkonium chloride alternatives or emollient-enriched formulations. Survey data further shows that dermatitis prevalence rises sharply with frequent use of high-alcohol gels, underscoring the need for product innovation that balances antimicrobial efficacy with skin health. Companies that successfully integrate emollients and optimize hydration without compromising product performance are well-positioned to secure institutional contracts. As a result, skin-safety concerns remain a critical market restraint while also influencing research and development investment and competitive strategy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gel/Liquid Commands Share as Spray Formats Accelerate

Gel and liquid formats continue accounting for the largest share of the United States hand sanitizer market, generating 76.27% of revenue in 2025. Their leading position is supported by long-standing consumer acceptance, compatibility with institutional dispenser systems, and broad regulatory clearance, which make them the preferred choice across healthcare, foodservice, and corporate environments. Although other formats are gaining traction, gels and liquids remain central to institutional procurement cycles, reinforcing their leadership through consistent performance, operational reliability, and ease of integration into established hygiene protocols.

In contrast, spray formats are expected to be the fastest-growing product type, registering a CAGR of 8.46% from 2026 to 2031. Portability, precision-dose application, and alignment with premium and wellness positioning are driving their adoption, supporting the transition of sprays from niche offerings to mainstream retail products. GOJO’s July 2025 launch of PURELL Hand Sanitizer Spray is expected to highlight the strategic importance of this segment, as design-led packaging and fragrance differentiation position sprays as lifestyle-oriented products for younger, urban consumers. This strong growth indicates a structural shift in consumer behavior, positioning spray sanitizers as a key contributor to future market expansion and competitive differentiation.

By End User: Adult Segment Holds Structural Dominance While Kids Drive Premium Expansion

In the United States hand sanitizer market, the adult segment maintains its structural dominance, accounting for 87.74% of revenue in 2025. This leadership reflects two demand streams: institutional procurement by healthcare facilities, foodservice operators, and office-based organizations, and retail purchases for household use. Within this broad base, health-conscious adults under 40 are driving a premiumization trend by seeking products that combine skin-care benefits with antimicrobial efficacy. Brands that successfully position sanitizers as both protective and nourishing are capturing higher margins and strengthening customer loyalty, making the adult segment the most influential driver of overall market value.

By contrast, the kids/children segment is projected to be the fastest-growing end-user category, registering an 8.99% CAGR from 2026 to 2031. Parental demand for gentle, non-toxic formulations designed for sensitive pediatric skin is driving growth, supported by toxicological evidence that highlights the disproportionate risks associated with conventional alcohol-based products. Brands such as The Honest Company and Babyganics have built consumer trust through clean-label and organic certifications, commanding significant price premiums while reassuring parents about product safety. Seasonal demand cycles, such as back-to-school and flu season, further support recurring purchases. The segment’s long-term impact lies in shaping future consumer preferences, as children raised on natural or non-alcohol sanitizers are likely to carry those habits into adulthood, creating enduring brand loyalty and extending the premiumization trend across generations.

By Ingredients: Conventional Holds Scale While Natural and Organic Resets Expectations

Conventional formulations remain the largest ingredient category in the United States hand sanitizer market and accounted for 89.37% of revenue in 2025. Strong institutional adoption supports their dominance, as the Centers for Disease Control and Prevention, the United States Food and Drug Administration, and healthcare accreditation frameworks explicitly endorse alcohol-based protocols. This reliance ensures that conventional sanitizers remain central to procurement cycles across hospitals, foodservice, and corporate environments, where compliance and regulatory certainty take priority over product experimentation. Broad institutional use reinforces conventional formats as the market’s volume anchor, even as consumer preferences start to evolve.

In contrast, natural and organic ingredient variants represent the fastest-growing segment, projected to record an 8.79% CAGR from 2026 to 2031. Consumer demand for clean-label, plant-derived, and skin-compatible formulations drives this momentum, while brands use certifications such as United States Department of Agriculture Organic and Ecocert to build trust and support premium positioning. Although the United States Food and Drug Administration monograph standards limit the extent to which “naturalness” can influence the antimicrobial core, innovation in secondary ingredients, skin-health claims, and sustainable packaging is reshaping consumer expectations. This trajectory positions natural formulations to expand first across retail, kids, and premium adult channels, gradually reshaping the competitive landscape and signaling a long-term shift toward premiumization and differentiated value creation.

By End Use: Commercial Anchors Revenue; Residential Gains Through Premiumization

The commercial end-use segment anchors the United States hand sanitizer market and accounted for 59.83% of revenue in 2025. It is also projected to be the fastest-growing category, registering an 8.32% CAGR from 2026 to 2031. This position reflects the scale of institutional replenishment cycles across healthcare, foodservice, education, and corporate facilities, supported by the increasing adoption of touch-free and Internet of Things-enabled dispenser systems. Investments in wall-mounted and free-standing dispensers help secure refill contracts, generate recurring revenue streams, reduce customer churn, and improve demand predictability for established suppliers. The commercial segment’s structural dominance underscores its role as both the primary volume contributor and a key driver of innovation in institutional hygiene.

By contrast, the residential segment has higher price sensitivity, portability-driven purchasing occasions, and rising household hygiene awareness, particularly among families with school-age children. Electronic commerce has expanded access to a broader assortment of formats and clean-label brands, enabling direct-to-consumer strategies that bypass traditional retail gatekeepers and capture margin-accretive pricing. While commercial demand is expected to remain entrenched, residential premiumization is increasing per-unit value and gradually narrowing the revenue gap between the two segments. Brands that manage differentiated assortment strategies across channels are best positioned to capture margin expansion in residential applications while defending scale in commercial applications, supporting balanced growth across both end-use categories.

Geography Analysis

The United States hand sanitizer market’s geographic dynamics reflect the interplay of healthcare infrastructure, demographic growth, and consumer wellness preferences. The Southern region holds the largest footprint, with Texas and Florida driving demand through their extensive healthcare networks, tourism industries, and commercial activity across hospitality, retail, and food service. Institutional procurement in these states operates at scale, supported by hospital group purchasing agreements. At the same time, the hospitality sector’s operational need for point-of-service sanitizer availability drives recurring bulk demand. This combination of institutional density and demographic expansion positions the South as the most structurally durable regional market through the forecast period.

The Northeast corridor, led by New York, New Jersey, and Massachusetts, has the highest per-capita institutional density, supported by academic medical centers, urban transit systems, and concentrated professional services offices. The Midwest, including states such as Ohio, Illinois, and Michigan, functions as both a manufacturing hub and a stable demand base, supported by strong business-to-business distribution infrastructure and healthcare procurement. Meanwhile, the West, particularly California, stands out for its consumer preference for premium and natural formulations. Regulatory frameworks around sustainability and packaging are encouraging brands to adopt refillable and recycled-content solutions ahead of national standards. Western trends often serve as early indicators of the direction of national formulation and packaging practices.

Rural and underserved markets represent the remaining frontier. These markets have historically lagged urban adoption due to lower institutional density and greater reliance on sink infrastructure. However, telehealth expansion, community health investment, and e-commerce are progressively narrowing this gap by enabling clinics, schools, and households to access sanitizer products more consistently. Together, these geographic dynamics position the South and Northeast as the most durable growth anchors, the West as the premium value driver, and the Midwest and rural regions as the long-tail volume base that supports manufacturing scale for national brands.

Competitive Landscape

The competitive landscape of the United States hand sanitizer market is moderately fragmented, with large-scale companies operating alongside regional and specialty players. The most significant consolidation move is expected to be The Clorox Company’s USD 2.25 billion acquisition of GOJO Industries in April 2026, which would create Clorox Purell as the largest single entity in the category. This integration would combine Purell’s leading retail and business-to-business presence with Clorox’s consumer brand infrastructure, strengthening leadership through installed dispenser bases, group purchasing organization relationships, and retail planogram dominance. Other major institutional competitors, such as Ecolab, SC Johnson Professional, Reckitt Benckiser, and Medline Industries, compete through dispenser technology innovation, compliance-oriented solutions, and bundled hygiene contracts that structurally limit price-driven switching. SC Johnson Professional’s planned launch of Alcare Enhanced, featuring OPTIDOSE Hand Sanitizer in 2025, which embeds telemetry and compliance monitoring into dispenser systems, highlights how software-enabled customer retention is becoming a competitive advantage in institutional markets.

White space opportunities remain in premium retail and direct-to-consumer channels, where format innovation, clean-label positioning, and design-led branding support pricing well above commodity sanitizers. Church & Dwight’s acquisition of Touchland signals consolidation in this space, while niche and regional entrants with authentic natural formulation credentials continue to find room for differentiation. The natural and organic ingredient segment is particularly attractive for mid-sized players with strong direct-to-consumer infrastructure, as it offers defensible premium positioning without directly challenging Clorox Purell’s institutional stronghold.

At the same time, private-label expansion by major retailers is intensifying margin pressure in commodity gel formats, accelerating the need for branded players to shift toward differentiated, premium-positioned lines. Retailers’ lower-priced proprietary offerings are reshaping competitive dynamics, forcing national brands to emphasize natural formulation credibility, healthcare-grade efficacy claims, and packaging innovation to maintain relevance. As a result, incumbents are defending scale through institutional contracts, while challengers are pursuing growth through premiumization and consumer-centric innovation.

United States Hand Sanitizer Industry Leaders

-

GOJO Industries, Inc.

-

Reckitt

-

Procter & Gamble Company

-

Ecolab Inc.

-

Kimberly-Clark Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Clorox Company acquired GOJO Industries, expanding its product portfolio to include the Purell brand and GOJO's health and hygiene solutions. The acquisition brought together two companies with a shared commitment to making the world cleaner and healthier. It also enabled Clorox to leverage complementary consumer brand-building expertise and business-to-business capabilities to deliver a more comprehensive product offering and create near- and long-term strategic value.

- July 2025: GOJO Industries, makers of PURELL, launched its newest innovation: PURELL Hand Sanitizer Spray. This new format delivered the same trusted germ-killing efficacy as PURELL gel in a light, refreshing spray, making it suitable for consumers with busy, on-the-go lifestyles. According to GOJO, “PURELL Hand Sanitizer Spray was four times more effective than a more expensive hand sanitizer mist. It killed germs quickly and left hands feeling clean, refreshed, and lightly scented.” Available in three mist varieties, such as Lavender and Verbena, Tangerine and Pear, and Unscented, the sprays were infused with essential oils and were free from harsh dyes, parabens, phthalates, and sulfates.

- July 2025: SC Johnson Professional launched Alcare Enhanced with OPTIDOSE technology, the latest addition to its Alcare Enhanced portfolio of foaming hand sanitizers. This solution used OPTIDOSE technology to deliver a precise and clinically proven dose of hand sanitizer to healthcare professionals, addressing hand hygiene compliance requirements. The OPTIDOSE technology dispensed a 1.5 milliliter dose of the trusted Alcare Enhanced foaming hand sanitizer with every push. A single dose provided enough foam to fully cover hands and keep them wet for 20 to 30 seconds, supporting proper hand sanitizing technique. The technology was also compatible with the Proline Manual dispenser, offering versatility for healthcare facilities.

United States Hand Sanitizer Market Report Scope

Hand sanitizer is a topical antimicrobial solution designed to reduce or eliminate germs on the hands when soap and water are not readily available. It is most commonly formulated with alcohols such as ethanol or isopropyl alcohol, which act as rapid‑acting antiseptics, though non‑alcohol alternatives like benzalkonium chloride are also used in certain products.

The United States hand sanitizer market is segmented based on product type, end users, ingredients, and end use. By product type, the market is segmented into gel/liquid, spray, and other product types. By end user, the market is segmented into adults and kids/children. By ingredient, the market is segmented into conventional and natural and organic. By end use, the market is segmented into residential and commercial. The market forecasts are provided in terms of value (USD).

| Gel/Liquid |

| Spray |

| Other Product Type |

| Adult |

| Kids/Children |

| Conventional |

| Natural and Organic |

| Residential |

| Commercial |

| By Product Type | Gel/Liquid |

| Spray | |

| Other Product Type | |

| End User | Adult |

| Kids/Children | |

| By Ingredients | Conventional |

| Natural and Organic | |

| End Use | Residential |

| Commercial |

Key Questions Answered in the Report

What is the current size of the United States hand sanitizer market?

The market is valued at USD 562.27 million in 2025 and is projected to reach USD 875.42 million by 2031, reflecting a healthy CAGR of 7.78% between 2026 and 2031.

Which product type leads the market?

Gel/liquid formats dominate with 76.27% share in 2025, while sprays are the fastest‑growing at 8.46% CAGR.

Who are the main end users?

Adults hold 87.74% share in 2025, but kids/children are the fastest‑growing group at 8.99% CAGR.

What ingredient trends stand out?

Conventional sanitizer products lead with 89.37% share, while natural and organic variants grow fastest at 8.79% CAGR

Which end‑use setting drives demand?

Commercial settings anchor the market at 59.83% share in 2025 and also grow fastest at 8.32% CAGR, thanks to institutional contracts and dispenser adoption.

Page last updated on: