Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 78.23 Billion |

| Market Size (2031) | USD 101.06 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

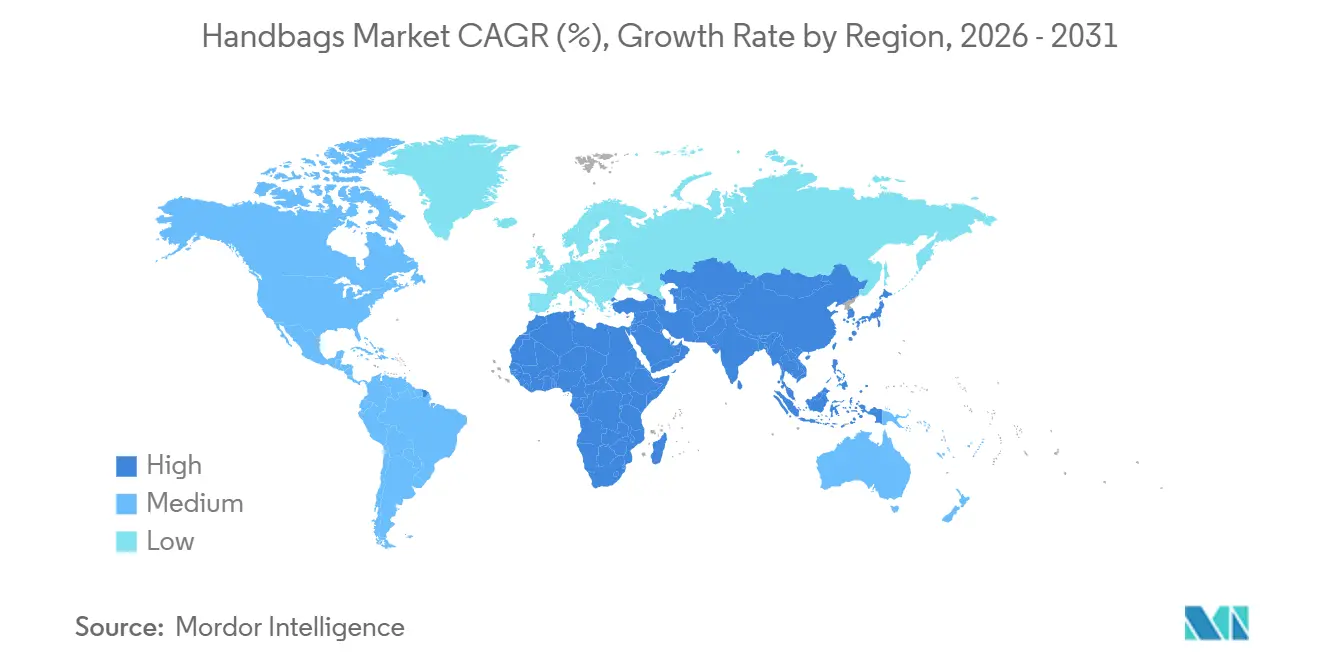

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

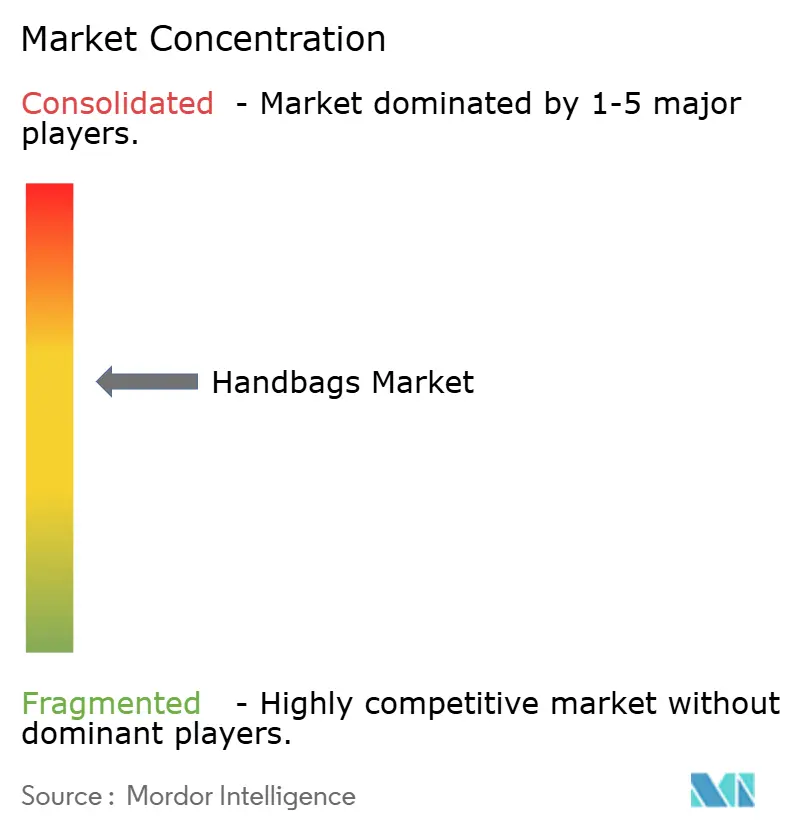

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Handbags Market Analysis by Mordor Intelligence

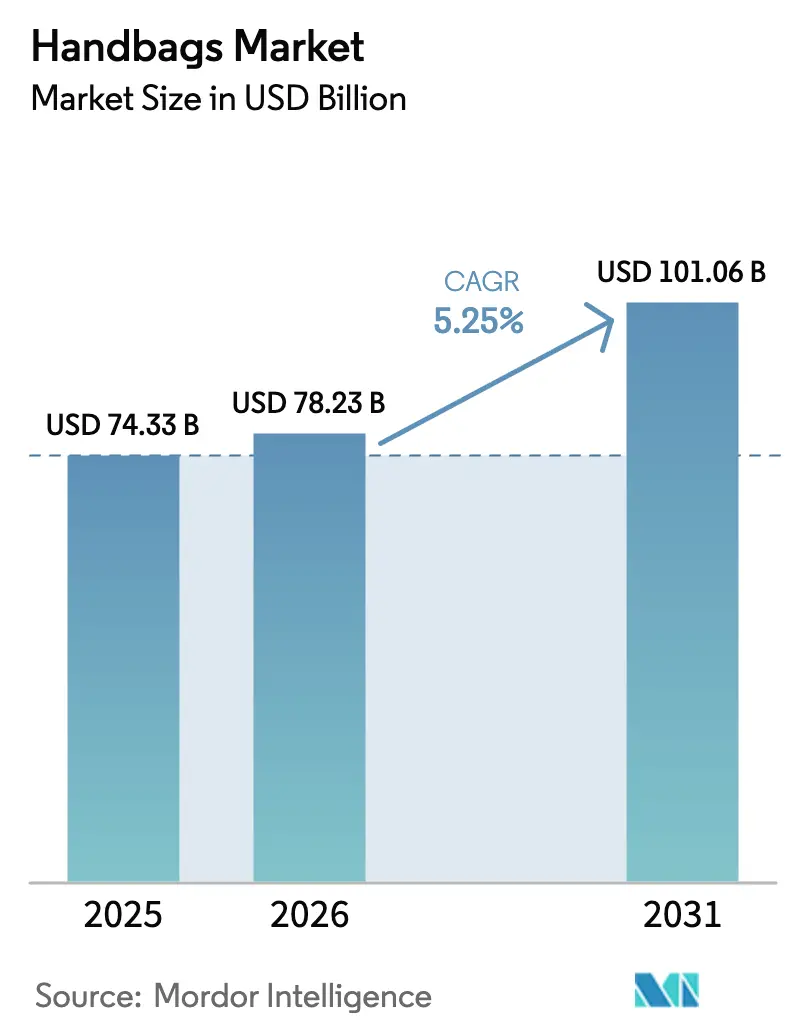

The Handbags Market size was valued at USD 74.33 billion in 2025 and estimated to grow from USD 78.23 billion in 2026 to reach USD 101.06 billion by 2031, at a CAGR of 5.25% during the forecast period (2026 to 2031), confirming steady global demand and brand diversification. The trajectory suggests pricing power has plateaued, prompting brands to shift their focus to volume growth, experiential selling, and material innovation to maintain margins. Totes remain the anchor product, social commerce accelerates discovery, and regulatory pressure on materials nudges companies toward bio-fabricated leather and a circular economy. Cross-border purchasing, particularly by Chinese travelers, creates geographic arbitrage that influences inventory allocation, while the resale channel compresses primary-market pricing and highlights provenance. Competitive intensity is rising as direct-to-consumer entrants leverage influencer marketing and agile supply chains to capture market share in the handbags market.

Key Report Takeaways

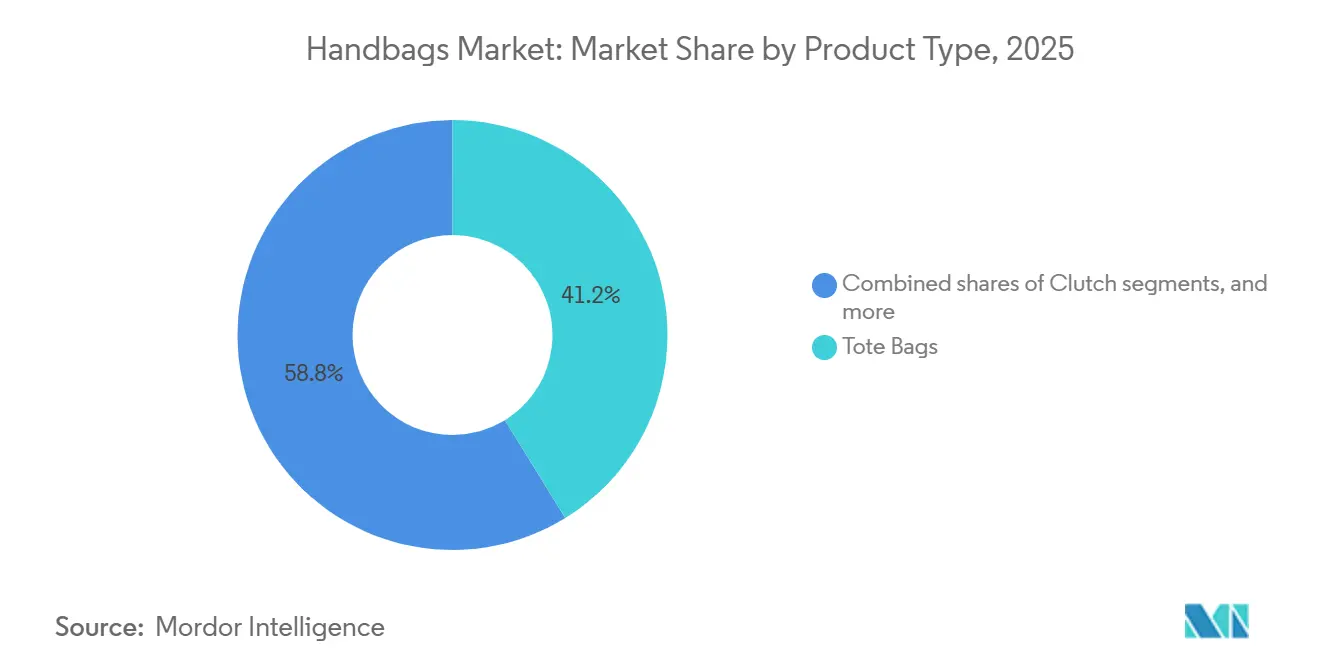

- By product type, tote bags commanded 41.21% of the handbags market share in 2025, while bucket bags are projected to grow at a 5.49% CAGR to 2031.

- By category, the mass segment held 63.57% share of the handbags market size in 2025; the premium segment is forecast to expand at 5.91% CAGR through 2031.

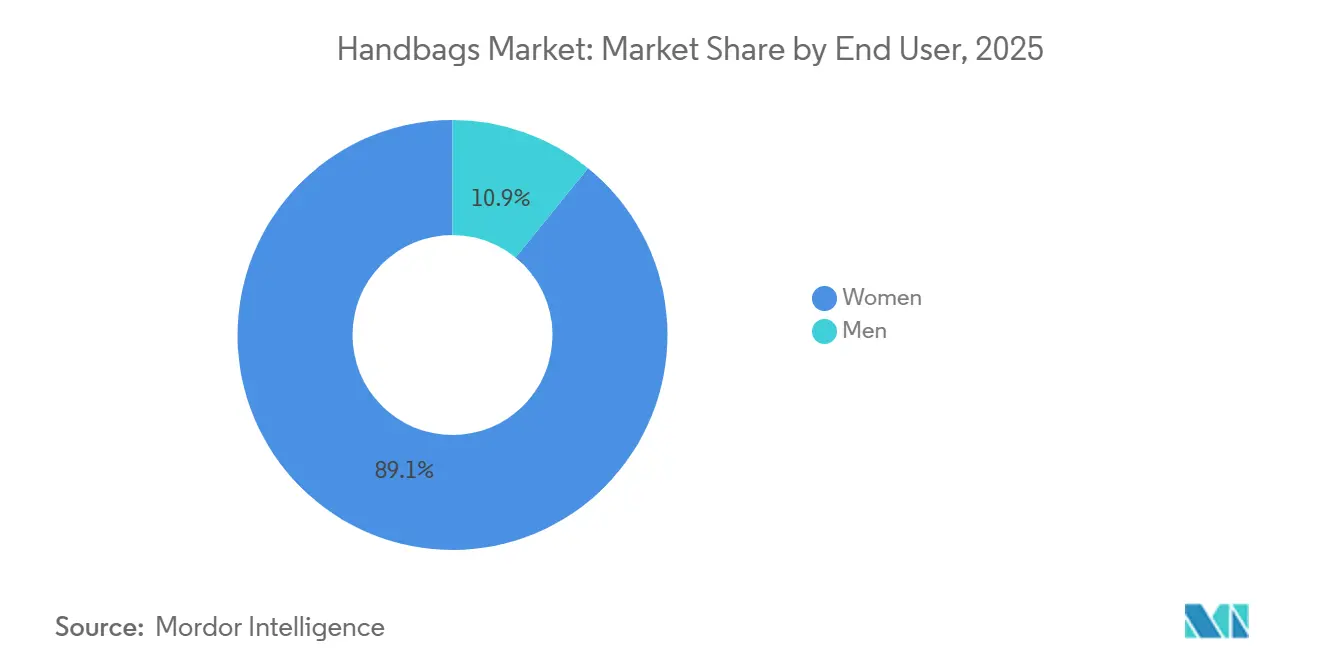

- By end user, women accounted for 89.14% share of the handbags market size in 2025, whereas the men’s segment shows the highest 5.79% CAGR outlook to 2031.

- By distribution channel, offline retail retained 62.68% share of the handbags market in 2025; online channels led growth at a 6.07% CAGR through 2031.

- By geography, the Asia-Pacific region captured 43.06% of the handbags market share in 2025 and is projected to advance at a 6.23% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Handbags Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in outstation and leisure travel | +1.2% | Global, with the strongest recovery in the Middle East, Europe, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Rising female workforce and purchasing power | +0.9% | India, Southeast Asia, the Middle East; spillover to urban centers in South America and Africa | Long term (≥ 4 years) |

| Changing fashion trends and consumer preferences | +0.8% | Global, North America and Asia-Pacific | Short term (≤ 2 years) |

| Product innovation and sustainability trends | +1.0% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Social media and influencer-led brand discovery | +1.1% | China, North America, Southeast Asia | Short term (≤ 2 years) |

| Product innovation in raw material and design | +0.7% | Global, Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increase in outstation and leisure travel

The growing popularity of outstation and leisure travel is significantly boosting the demand for handbags, particularly those that are travel-friendly and stylish. According to the World Travel and Tourism Council (WTTC), in 2024, the Travel and Tourism sector contributed 10% to the global economy, amounting to USD 10.9 trillion. The WTTC forecasts that by 2035, tourism will inject USD 16.5 trillion into the global economy, accounting for 11.5% of global GDP[1]Source: Tourism Growth, "Global Travel and Tourism is Strong Despite Economic Headwinds," wttc.org. This increase in tourism, supported by relaxed travel restrictions and the availability of budget airlines, is encouraging consumers to invest in luggage and leather goods, including handbags, for weekend getaways and vacations. To meet travelers' needs, brands are introducing innovative products. For example, Dagne Dover launched its Petra Convertible Tote, a sleek hybrid tote-backpack featuring a padded laptop compartment, trolley sleeve, and multiple organizational pockets designed specifically for professionals who balance travel and work demands.

Rising female workforce participation

As more women enter the workforce, the demand for handbags that are both stylish and functional is increasing. Women now seek bags that can carry essentials like laptops, documents, and personal items while complementing their professional attire. According to the World Bank, the global female labor force participation rate reached 40.2% in 2024, reflecting this growing trend [2]Source: The World Bank Group, "Labor force, female (% of total labor force)", www.worldbank.org. Office-friendly handbags, such as structured totes, satchels, and laptop-compatible crossbody bags, are becoming more popular because they combine practicality with fashion. To cater to these needs, brands are designing bags with features like multiple compartments for better organization and convenience. For example, Michael Kors launched the Jet Set Travel Large Logo Tote in 2024, which offers a spacious and organized interior, making it ideal for working women. This shift shows how handbags are no longer just fashion statements but have become essential tools for modern working women, balancing style and functionality to meet their daily needs.

Changing fashion trends and consumer preferences

The handbags market is increasingly dividing along the lines of price and style. Between 2021 and 2024, unit sales in the USD 250-500 segment grew, while handbags priced above USD 1,000 saw declining volumes, reflecting consumer resistance to aspirational pricing. North America shows the highest concentration in the USD 250-500 range, whereas Asia-Pacific shows greater acceptance of entry-level products. This shift points to a broader change in consumer priorities, with shoppers focusing on cost-per-wear rather than brand heritage and favoring versatile silhouettes such as totes and crossbody bags that suit multiple occasions. The resale market, expanding two to three times faster than primary sales, has added a new layer to purchasing decisions. Buyers increasingly view handbags as investable assets with predictable depreciation, driving demand for brands with strong secondary-market liquidity, including Hermès, Chanel, and Louis Vuitton. In China, small leather goods, such as cardholders and pouches, also experienced notable growth in 2024, indicating that consumers are trading down within their luxury portfolios while continuing to engage with their preferred brands.

Product innovation and sustainability trends

Material innovation in the handbags industry has moved rapidly from experimental applications to large-scale implementation, driven by both regulatory requirements and consumer demand for traceable, environmentally friendly alternatives to traditional leather. Under the EU’s Ecodesign for Sustainable Products Regulation, which will require Digital Product Passports by 2027, brands must report the environmental impact of every material used, from tanning chemicals to packaging films. While this is expected to add 2%-4% to the cost of goods sold, it also provides an opportunity for brands to position themselves as leaders in transparent and sustainable supply chains (European Commission)[3]Source: EUROPEAN COMMISSION, “Ecodesign for Sustainable Products Regulation,” ec.europa.eu. Vegan leathers made from plant-based sources such as pineapple leaves, apple peels, and cactus were valued at USD 39.5 billion in 2022 and are expected to reach USD 74.5 billion by 2030. Handbags are among the leading applications for these materials, as they have lower durability requirements than footwear (European Commission). Extended Producer Responsibility (EPR) regulations in countries like France, Germany, and the Netherlands now require brands to cover the cost of collecting and recycling products at the end of their life cycle. While this increases operational expenses, it also opens the door to closed-loop systems, where used handbags are dismantled and repurposed as raw materials for new products, supporting circular-economy initiatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit proliferation and brand dilution | -0.8% | Global, Europe, and online marketplaces | Short term (≤ 2 years) |

| Regulatory hurdles and compliance issues | -0.5% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Environmental concerns regarding materials | -0.4% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Volatile hide prices and supply shocks | -0.6% | Global, North America, Asia-Pacific, and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit proliferation and brand dilution

Counterfeit handbags not only flood the market but also undermine brand equity, compromise pricing integrity, and erode consumer trust. In 2024, U.S. Customs and Border Protection seized over USD 380 million worth of counterfeit handbags, wallets, and accessories, underscoring the prominence of the category in intellectual property violations[4]Source: US CUSTOMS AND BORDER PROTECTION, “Trade Enforcement Statistics 2024,” cbp.gov. Online marketplaces have become the primary distribution channel for these counterfeits. Yet, algorithmic detection struggles against astute sellers who rotate listings, use obfuscated brand names, and exploit cross-border shipping loopholes. The emergence of high-quality "superfakes" that closely mimic stitching, hardware, and even serial numbers has made authentication challenging for consumers. This difficulty has led some buyers to authorized resale platforms like The RealReal and Vestiaire Collective, which offer third-party verification. As the market becomes saturated with counterfeits, the aspirational value of owning an authentic item diminishes, resulting in brand dilution. In response, brands are adopting advanced anti-counterfeiting technologies, such as blockchain-based provenance tracking, Near Field Communication (NFC)-embedded tags, and forensic-grade material markers.

Regulatory hurdles and compliance issues

In the U.S., import tariffs on handbags range from 5% to 20%, depending on the material and country of origin. The European Union, on the other hand, imposes tariffs ranging from 10% to 15% on non-preferential trade partners. The U.S. International Trade Commission highlights that these varying tariffs create cost imbalances, influencing both sourcing and retail pricing strategies. Labeling mandates necessitate disclosures about the country of origin, material content, and care instructions. Non-compliance can result in penalties, product recalls, and tarnished brand reputation. The EU's REACH regulation, managed by the European Chemicals Agency, limits over 200 chemical substances in leather goods[5]Source: EUROPEAN CHEMICALS AGENCY, “REACH Regulation,” echa.europa.eu. This includes bans on chromium VI in tanned leather, azo dyes, and phthalate plasticizers. As a result, brands must audit tanneries and perform batch testing to ensure compliance. Per- and polyfluoroalkyl substances (PFAS) restrictions, already in place in California and Maine, are under consideration in several U.S. states and the EU. These restrictions prohibit per- and polyfluoroalkyl substances, often found in water-repellent coatings and stain treatments. The California Department of Toxic Substances Control reports that this has necessitated reformulating finishing processes, with input costs rising by 5% to 10%. In France, Germany, and the Netherlands, Extended Producer Responsibility mandates compel brands to fund the collection, sorting, and recycling of end-of-life products. While this adds an additional 1% to 2% to the cost of goods sold, it also offers brands an opportunity to differentiate themselves through circularity, as noted by the European Commission.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tote Dominance Meets Bucket-Bag Momentum

In 2025, tote bags held a 41.21% market share, reflecting their versatility across work, travel, and everyday use. Bucket bags are projected to grow at a 5.49% rate through 2031, driven by demand for hands-free, minimalist designs favored by younger consumers. While satchels retain a niche following, their growth has stalled amid the shift to hybrid work, leading to reduced demand for structured, office-centric styles. Clutches continue to lose relevance as social settings become more casual, whereas niche formats such as hobo, saddle, and belt bags remain trend-driven, with belt bags seeing renewed momentum in 2024–2025 due to their integration into athleisure and festival wear.

In the men’s segment, leather shoulder bags and weekender styles are gaining traction as functional alternatives to traditional briefcases, while nylon bags are being replaced by more durable and resale-friendly materials, such as leather and canvas. From a pricing perspective, totes priced between USD 250 and USD 500 led unit sales in 2024, while volumes softened for bags above USD 1,000, indicating growing price sensitivity. Brands are responding by offering entry-level totes with simplified designs to preserve volume, while limiting exotic materials and limited editions to ultra-high-net-worth consumers.

By Category: Premium Outpaces Mass on Margin Discipline

The mass segment accounted for 63.57% of market share in 2025; however, the premium category is projected to expand at a CAGR of 5.91% through 2031, signaling a strategic shift by brands toward protecting margins rather than pursuing volume growth. Mass-market handbags, typically priced below USD 250, cater to entry-level consumers and fast-fashion shoppers who value affordability and rapid trend turnover. Despite its scale, this segment faces increasing margin pressure from rising production costs, heightened promotional activity, and competition from resale platforms that offer lightly used premium bags at comparable price points. Premium handbags, generally priced between USD 500 and USD 2,000, occupy a strategic middle ground where brand heritage, superior materials, and craftsmanship support price premiums without the deterrent effect associated with ultra-luxury pricing. Brands such as Coach, Michael Kors, and Kate Spade have refined their product and distribution strategies by limiting outlet exposure and prioritizing full-price sell-through, acknowledging that persistent discounting weakens brand equity and conditions consumers to delay purchases.

The premium segment also benefits from a resale-driven halo effect, as strong secondary-market liquidity reinforces perceived value and lowers the entry barrier for first-time luxury buyers. Meanwhile, the mass segment’s durability depends on capturing impulse purchases, gifting occasions, and replacement demand, areas increasingly challenged by direct-to-consumer brands that exploit social commerce and influencer-led marketing to avoid traditional wholesale margins. To reinforce value propositions, premium brands are investing in experiential retail formats such as pop-ups, trunk shows, and customization services, strengthening customer engagement beyond simple transactions. This segmentation also mirrors regional consumption patterns: North America favors accessible luxury, with most handbag units priced between USD 250 and USD 500, while Asia-Pacific demonstrates stronger demand for entry-level offerings, particularly handbags priced below USD 250.

By End User: Women Lead, Men Accelerate

Women accounted for 89.14% of handbag demand in 2025, though the men’s segment is projected to grow at 5.79% through 2031, fueled by changing workplace norms, the mainstreaming of carry accessories, and marketing that positions handbags as functional tools rather than mere fashion statements. Growth in men’s leather bags reflects a shift away from traditional briefcases and backpacks toward crossbody bags, totes, and weekenders that suit hybrid work schedules. Male consumers prioritize functionality, durability, neutral colorways, minimalist hardware, and brands with heritage credentials, such as Louis Vuitton, Prada, and Hermès. The declining interest in nylon bags highlights a preference for long-lasting, resale-friendly materials.

Women’s demand, though dominant, is becoming increasingly segmented across various use cases: professional totes for work, compact cross-body bags for errands, and statement pieces for social occasions. Trends toward capsule wardrobes and conscious consumption are steering purchases away from trend-driven impulse buys and toward investment pieces with multi-seasonal longevity and resale value. Small leather goods, including cardholders, pouches, and belt bags, saw growth in China in 2024, as women trade down within luxury portfolios to maintain brand engagement. Gender differences also appear in shopping channels: women lean on social commerce and influencer-driven discovery, while men prefer direct brand websites and in-store consultations emphasizing craftsmanship. Brands are responding with gender-neutral designs and unisex campaigns to expand reach without alienating core female consumers.

By Distribution Channel: Online Gains Share Despite Offline Resilience

In 2025, offline retail stores accounted for 62.68% of distribution, but online channels are expected to expand at a 6.07% CAGR through 2031, driven by the rise of buy-now-pay-later options, augmented-reality try-ons, and social commerce features that shorten the path from discovery to purchase. Physical stores continue to play a key role in high-consideration purchases, where customers evaluate leather quality, hardware weight, and interior construction before making a purchase. However, their function is shifting from purely transactional spaces to experiential destinations that host events, provide personalization, and offer post-purchase services such as monogramming and repairs. Many luxury brands are scaling back their wholesale partnerships with department stores and multi-brand boutiques to regain margin and control over brand presentation, instead investing in flagship stores and pop-up locations that immerse shoppers in the brand narrative.

Online retail, encompassing brand-owned e-commerce, third-party marketplaces, and social commerce, benefits from lower overhead, a wider geographic reach, and data-driven personalization, enabling tailored product recommendations and dynamic pricing based on browsing behavior. According to the US Census Bureau, US apparel and accessories e-commerce reached USD 134.5 billion in 2024 and is projected to grow to USD 219.3 billion by 2029, with handbags leading the category due to standardized sizing and lower return rates compared to apparel. While offline stores still offer advantages in building brand loyalty, capturing foot traffic in high-traffic locations, and satisfying consumers who prefer immediate gratification, their share is expected to gradually decline as digital-native brands grow and omnichannel strategies increasingly integrate online and offline experiences.

Geography Analysis

Asia-Pacific accounted for 43.06% of the global market in 2025 and is expected to grow at a 6.23% CAGR through 2031, though performance varies significantly across the region. China’s luxury market contracted 18%–20% in 2024, with LVMH’s fashion and leather goods division posting a 5% organic revenue decline in Q3 amid property-sector challenges and rising youth unemployment. In contrast, India is experiencing rapid expansion, driven by urbanization, increasing female workforce participation, and growth in organized retail. Japan continues to benefit from inbound tourism, while Southeast Asia’s rising middle class is fueling demand despite infrastructure limitations and regulatory complexities.

North America remains a key profit center due to high per-capita spending and a mature e-commerce ecosystem. US apparel and accessories e-commerce reached USD 134.5 billion in 2024 and is projected to grow to USD 219.3 billion by 2029, with handbags performing particularly well due to standardized sizing and lower return rates (US Census Bureau). Buy-now-pay-later solutions have increased average transaction values, while the USD 250–500 price range captured the majority of handbag unit sales in 2024. Canada and Mexico provide additional volume, with Mexico benefiting from nearshoring trends, and the robust US resale market pressures primary sales, prompting brands to emphasize exclusivity, personalization, and post-purchase services.

Europe, the Middle East, South America, and Africa present a diverse set of opportunities. Europe faces structural challenges, with luxury conglomerates losing USD 240 billion in market capitalization since March 2024, although imports and exports remain strong (European Commission), and ultra-luxury brands such as Hermès continue to perform well through controlled distribution. The Middle East, led by the UAE and Saudi Arabia, is a high-margin growth market, with the GCC luxury sector projected to reach USD 15 billion by 2027 (Chalhoub Group), supported by high-net-worth inflows and tourism. South America faces volatility and elevated import costs, while Africa, particularly South Africa, represents an emerging but fast-growing market, with handbag e-commerce showing strong potential.

Competitive Landscape

The handbags market is moderately concentrated, with the top five players, Michael Kors, L.L.C., Prada, LVMH, Hermès, and Kering, holding a significant but not dominant share. This structure allows agile newcomers to carve out niche segments through direct-to-consumer strategies, sustainability initiatives, and influencer-driven marketing. European luxury conglomerates, which control many heritage brands, are facing margin pressure due to China’s consumption slowdown, diminishing pricing power, and rising investment requirements in digital capabilities and circular-economy programs. LVMH’s fashion and leather goods division saw only 1% organic growth in Q3 2024, down from 21% a year earlier, while Kering and Hugo Boss lost about 50% of market capitalization from March 2024 peaks, and Burberry declined 70%, reflecting the sector’s sensitivity to macroeconomic shifts and changing consumer preferences. In contrast, Hermès reported 9.6% sales growth in Q3 2025, demonstrating that ultra-luxury brands with controlled distribution, waitlist scarcity, and artisanal positioning can remain resilient.

Across the industry, vertical integration is becoming a key strategy, with brands acquiring tanneries, ateliers, and logistics networks to secure supply, ensure quality, and reclaim margins previously lost to third-party suppliers. Emerging opportunities are visible in men’s handbags and bio-fabricated materials, where early adopters can secure supply agreements and intellectual property before commoditization. Disruptors like Dagne Dover, which emphasizes functional design and direct-to-consumer distribution, and Charles & Keith, which focuses on accessible luxury with trend-responsive assortments, are gaining market share by leveraging social commerce and data-driven inventory management. Technology is playing a growing role in competitive advantage, with augmented-reality try-ons, blockchain-based authentication, and AI-powered personalization engines enabling tailored product recommendations and dynamic pricing.

Sustainability and resource efficiency are increasingly becoming differentiators in the market. LVMH’s Nona Source platform, originally reselling deadstock fabrics and trims, has expanded to leather offcuts, giving smaller brands access to premium materials at lower cost while reducing landfill waste. Compliance with the EU Digital Product Passport mandate, effective 2027, will require NFC tags or QR codes that disclose material origin, carbon footprint, and end-of-life instructions, giving first movers a competitive edge (European Commission). Overall, the market is evolving toward vertically integrated, digitally enabled, and sustainability-focused models, favoring brands that combine heritage, innovation, and operational control.

Handbags Industry Leaders

-

Prada Holding BV

-

LVMH Moët Hennessy Louis Vuitton SE

-

Hermès International SA

-

Kering SA

-

Michael Kors, L.L.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nicola Morris has introduced MAIA, a special collection of rare Hermès handbags now available in Dubai. This exclusive, appointment-only service is hosted at ExecuJet, Al Maktoum International FBO, giving collectors and fashion lovers a chance to explore unique heritage pieces in a private and discreet environment.

- March 2025: Stoney Clover Lane expanded its presence in the accessories market with the debut of its first leather collection, signaling a notable move into the luxury space. Best known for its playful and personalized nylon travel accessories, the brand is now introducing leather pieces at a higher price point in response to increasing demand for more refined, premium materials.

- February 2025: Perfect Moment Ltd. has launched its new puffer tote bag collection, combining functional design with fashion-forward style. Inspired by a “throw in and go” mindset, these jumbo padded totes are perfect for travel, gym days, or ski trips.

- February 2024: Jacquemus and Nike co-launched “The Swoosh Bag,” a limited-edition silhouette that merges luxury craft with athletic design, marking a high-profile cross-category product collaboration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global handbags market as the annual retail value generated by all newly manufactured bags purposely designed for carrying personal essentials, tote, satchel, bucket, clutch, sling, and comparable styles, sold through offline and online channels to men and women across every price tier. We, Mordor Intelligence, treat each bag's first sale to the consumer as the economic event that triggers market value capture.

Scope note: travel luggage, backpacks, wallets, and non-fashion utility pouches stay outside this evaluation.

Segmentation Overview

-

By Product Type

- Satchel

- Bucket Bag

- Clutch

- Tote Bag

- Other Product Types

-

By Category

- Mass

- Premium

-

By End User

- Women

- Men

-

By Distribution Channel

- Offline Retail Stores

- Online Retail Stores

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with Asian contract manufacturers, European artisanal workshops, U.S. department-store buyers, and digital-native brand founders. These conversations clarified factory gate prices, defect return rates, and online penetration targets, helping us validate desk numbers and refine assumptions for premium versus mass segments.

Desk Research

We first built a fact base from open data sets such as UN Comtrade shipment codes for HS 4202, Eurostat PRODCOM 1512, and U.S. Census retail sales, which reveal international trade flows and sell-through patterns. These were blended with insights from industry bodies, Leather & Hide Council of America, China Leather Industry Association, and Fédération de la Haute Couture et de la Mode, which publish production, pricing, and sustainability guidelines. Company 10-Ks, IPO filings, and specialty press articles added channel margins, average selling prices, and emerging material shifts like mycelium leather. Select licensed databases, notably D&B Hoovers for brand financials and Dow Jones Factiva for deal tracking, supplied further granularity. This list is illustrative; many other secondary sources were referenced throughout the build.

Market-Sizing & Forecasting

A top-down reconstruction starts with production plus net imports for each major region, adjusted for average retail mark-ups to reach consumer spend. Results are cross-checked through a bottom-up roll-up of sampled brand revenues and channel checks. Key variables inside the model include female labor-force participation, urban disposable income per capita, tote-bag share of units, online share of sales, average selling price progression by material, and counterfeit seizure statistics that signal gray-market leakage. Forecasts rely on multivariate regression blended with scenario analysis; GDP outlooks, fashion search-interest indices, and raw-hide price trends drive the independent variables. When bottom-up evidence diverges beyond a specified band, we revisit import data or recalibrate mark-ups before locking the curve.

Data Validation & Update Cycle

Each draft model passes a three-step peer review, anomaly checks against historic ratios, and leadership sign-off. We refresh every twelve months and issue mid-cycle updates if material events, regulation, major M&A, or currency shocks, shift the baseline.

Why Mordor's Handbags Baseline Commands Reliability

Published market values commonly differ because firms choose distinct product scopes, mark-up ladders, and refresh cadences. We acknowledge those variances up front so users see how alternate choices move the needle.

Key gap drivers include whether backpacks and wallets are blended into totals, the point in the value chain used for valuation, currency conversion cut-offs, and how aggressively future online pricing deflation is modeled. Our study isolates pure handbags, converts all figures at the average IMF 2024 exchange rates, and applies a moderated ASP trajectory vetted by channel buyers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 74.33 bn (2025) | Mordor Intelligence | - |

| USD 56.46 bn (2024) | Global Consultancy A | Excludes premium micro-brands and uses factory-gate prices without retail mark-ups |

| USD 63.07 bn (2024) | Industry Publisher B | Blends wallets and small leather goods into totals; last update mid-2023 |

| USD 81.79 bn (2024) | Trade Journal C | Applies uniform 2.0× mark-up and assumes constant USD; limited primary validation |

In short, our disciplined scope, dual-layer model, and annual refresh give decision-makers a balanced, transparent starting point that can be traced back to concrete variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the handbag market in 2031?

The handbag market is forecast to reach USD 101.06 billion by 2031.

Which product type held the largest share in 2025?

In 2025, tote bags commanded 41.21% of global demand, reflecting their everyday versatility.

How fast is online retail for handbags growing?

Online sales are expanding at a 6.07% CAGR to 2031, propelled by buy-now-pay-later and social commerce.

Which region led in market share in 2025?

In 2025, Asia-Pacific held 43.06% of revenue and is still growing at above-global rates.

Why are premium handbags outpacing mass-market growth?

Premium lines balance heritage and attainable luxury while benefiting from strong resale liquidity and higher margins.

How are brands combating counterfeits?

Leaders deploy blockchain provenance, NFC tags, and forensic markers to protect authenticity and sustain brand equity.

Page last updated on: