Hand Gloves Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

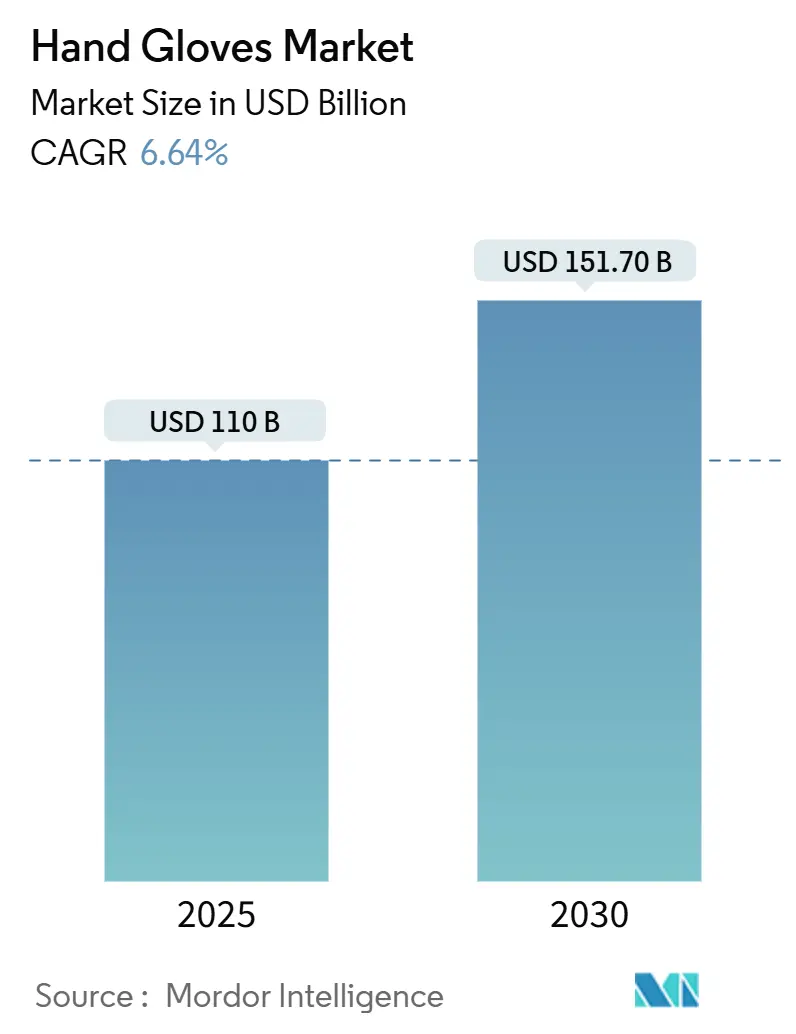

| Market Size (2025) | USD 110 Billion |

| Market Size (2030) | USD 151.70 Billion |

| Growth Rate (2025 - 2030) | 6.64% CAGR |

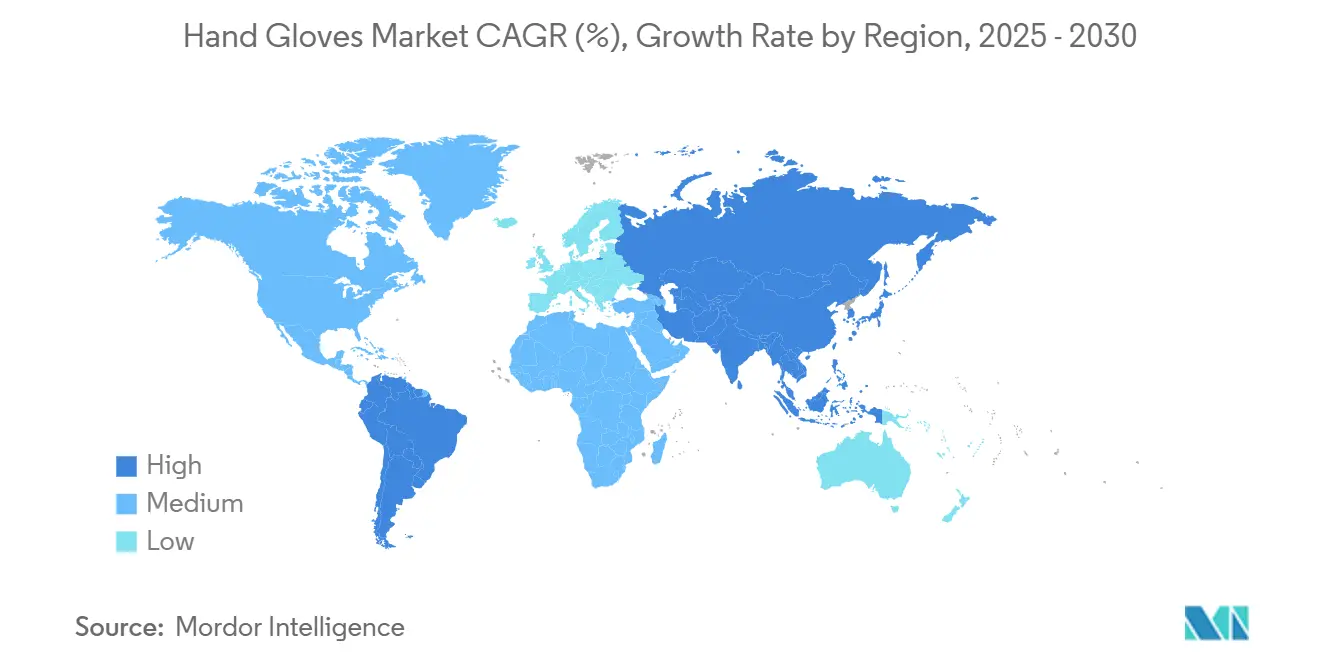

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

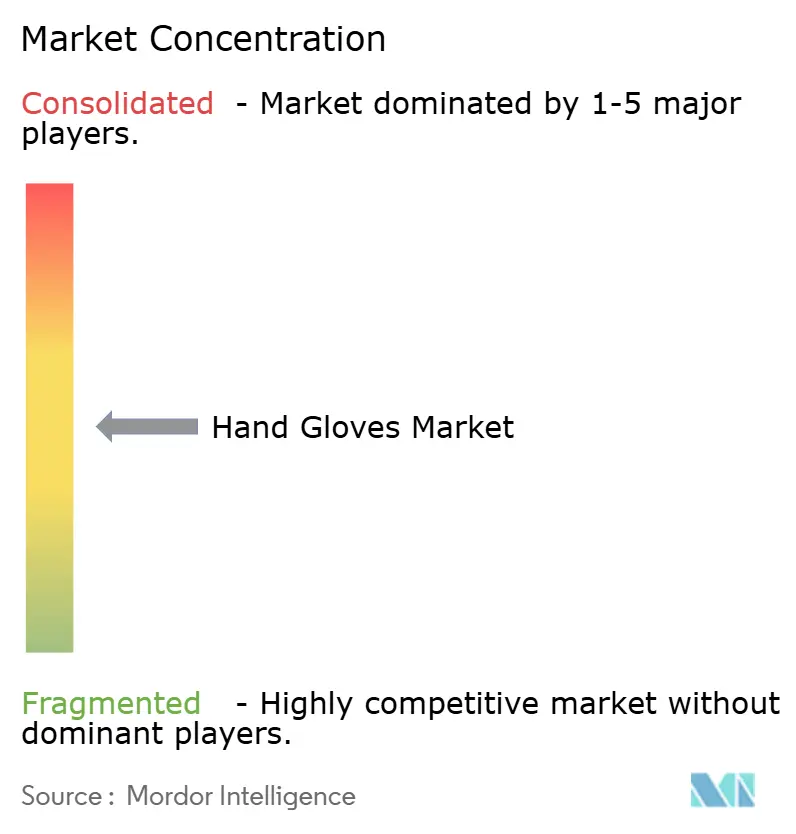

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hand Gloves Market Analysis by Mordor Intelligence

The hand gloves market size is USD 110 billion in 2025 and is forecast to reach USD 151.7 billion by 2030, advancing at a 6.64% CAGR. The demand for disposable and reusable gloves is experiencing significant growth across the global market, driven by a confluence of factors including heightened hygiene awareness, stringent safety regulations, and a growing emphasis on sustainability. In the medical and healthcare industry, regulations from bodies such as the United States Food and Drug Administration (FDA), which categorizes medical gloves as Class I devices, and the European Union's updated EN 455 standards are enforcing stricter requirements for product integrity and physical properties, thereby driving demand [1]Source: NEN, “NEN-EN 455-1:2020+A2:2024 en”, nen.nl. This is supported by strategic product developments, such as Kimberly-Clark Professional's launch of the high-protection Kimtech Polaris Nitrile Exam Gloves in January 2024 for laboratory settings, and Ansell's September 2024 launch of the GAMMEX PI Plus Glove-in-Glove System, a revolutionary two-in-one double gloving solution designed to enhance compliance and save time.

Key Report Takeaways

- By material, rubber-based gloves led the hand gloves market with 48.28% in 2024, while biodegradable variants are projected to grow at a 11.27% CAGR through 2030.

- By product type, disposable gloves held 73.28% of the market in 2024, while reusable gloves are projected to grow at the fastest CAGR of 8.16% through 2030.

- By end-user, medical and healthcare applications accounted for 39.41% of the hand gloves market in 2024, and industrial safety is projected to grow at an 8.96% CAGR through 2030.

- By geography, North America accounted for 33.53% of the revenue in 2024; however, the Asia-Pacific region is expected to achieve the fastest growth, with a 7.82% CAGR, by 2030.

Global Hand Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in HAI-prevention regulations | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Increased occupational-safety mandates in emerging industries | +0.9% | Asia Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Rapid growth in ambulatory surgical centres | +0.8% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Rising e-commerce private-label glove brands | +0.7% | Global, led by North America | Short term (≤ 2 years) |

| Accelerated biotech-lab expansions | +0.6% | North America and Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| Sustainability shift toward biodegradable materials | +0.5% | Europe and North America, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in HAI-prevention regulations

With the CDC underscoring the importance of glove usage in patient care, preventing cross-contamination has emerged as a regulatory mandate. Highlighting the market's evolution, the Food and Drug Administration's prohibition of powdered gloves, citing risks of severe airway inflammation, underscores the primacy of safety over traditional performance metrics. Research from Antimicrobial Resistance and Infection Control indicates that improper glove usage can paradoxically heighten infection risks. This revelation has spurred a demand for superior training programs and high-quality products that uphold barrier integrity, even during prolonged procedures. Such regulatory scrutiny is especially intense in surgical settings, where lapses in sterile techniques can lead to dire consequences. Compliance now hinges on the shelf life of hand gloves. ASTM D7161-16(2023) has set the benchmark for assessing storage longevity, emphasizing typical warehouse conditions. To bolster patient safety, healthcare facilities are turning to automated inventory management systems, ensuring glove integrity and averting the use of expired products.

Increased occupational-safety mandates in emerging industries

OSHA's 2025 regulatory updates require that all personal protective equipment, including gloves, fit each employee properly. This addresses historical gaps in protection for diverse body types. The "proper fit" requirement goes beyond just selecting the right size. It also includes ergonomic considerations to prevent hand fatigue and ensure dexterity during prolonged use. The construction industry is rapidly expanding its applications, with specialized cut-resistant materials like PolyKor and ATG fibers becoming the norm for high-risk tasks. Under updated OSHA standards, chemical processing facilities are under increased scrutiny. They now require gloves that meet specific permeation resistance criteria for handling hazardous substances. In food processing, operations must adhere to 21 CFR Parts 174 and 177. These regulations classify gloves as indirect food additives, making them subject to FDA specifications. As safety mandates converge across industries, there's a growing demand for multi-functional gloves. These gloves not only meet diverse regulatory requirements but also prioritize cost-effectiveness.

Rapid growth in ambulatory surgical centres

Ambulatory surgical centers (ASCs) are poised to increase surgical procedures by a minimum of 25% over the coming decade, capitalizing on cost benefits that enable procedures at a staggering 144% lower expense than traditional hospital outpatient departments. In a move to further incentivize this shift, the CMS's 2025 final rule established a conversion factor of USD 54.895 for ASCs that adhere to quality reporting standards. Highlighting the growing prominence of ASCs, MedPAC's March 2025 report to Congress indicated that, for the year 2023, approximately 3.4 million fee-for-service (FFS) Medicare beneficiaries were treated in Ambulatory Surgical Centers (ASCs)[2]Source: MedPAC, " Ambulatory surgical center services: Status report", medpac.gov. This upward trajectory highlights a robust demand for sterile surgical gloves, particularly those that adhere to stringent leak resistance standards. Notably, FDA regulations set an acceptable quality level of 1.5 for surgeons' gloves. With the baby boomer population aging, the momentum for outpatient surgical procedures is poised to continue, underscoring the need for dependable supply chains for top-tier protective equipment. ASCs are also shifting their focus, increasingly adopting value-based purchasing programs that emphasize quality outcomes over sheer volume. This shift presents a golden opportunity for premium glove manufacturers, especially those equipped to showcase superior performance metrics.

Rising e-commerce private-label glove brands

Online platforms are reshaping procurement patterns in digital healthcare supply chains, enabling direct-to-consumer sales that sidestep traditional distribution channels. Amazon's foray into medical supplies has reshaped competitive dynamics, empowering private-label brands to seize market share through aggressive pricing and swift delivery. The pandemic hastened the e-commerce uptake in healthcare, leading many facilities to adopt hybrid procurement strategies, blending traditional suppliers with online platforms for non-critical items. Innovative market offerings now feature smart gloves equipped with sensors for rehabilitation and eco-friendly variants that decompose in 1.5 years. Private-label manufacturers are harnessing advanced materials science, crafting Food and Drug Administration-compliant products that undercut established brands on price. This online procurement trend is especially evident in smaller healthcare facilities and research labs, which often lack the clout to negotiate with traditional suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile latex and nitrile raw-material prices | -1.5% | Global, with highest impact in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Regulatory scrutiny on PFAS and chemical additives | -0.8% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Natural-rubber-latex allergy prevalence | -0.4% | Global, with higher impact in healthcare-intensive regions | Long term (≥ 4 years) |

| Waste-management burden of disposable gloves | -0.3% | Europe and North America, spreading to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile latex and nitrile raw-material prices

For the fifth consecutive year, in 2025, natural rubber production is expected to fall short, with output rising by a mere 0.3% against a 1.8% increase in demand. Adverse weather in Thailand and China has driven rubber prices to a 13-year high, significantly increasing costs for manufacturers of latex-based gloves. While the Association of Natural Rubber Producing Countries noted a global production rise of 2.4%, bringing the total to 12.7 million tons, demand outstripped this at 13.9 million tons, highlighting a structural supply deficit. For instance, according to Statistics Indonesia, in 2023, Indonesia's rubber production, the world’s second-largest producer of rubber and a member of the International Tripartite Rubber Council, along with Thailand and Malaysia, decreased to 2.24 million metric tons from 2.27 million metric tons in the previous year[3]Source: Statistics Indonesia, “Statistical yearbook of Indonesia 2025”, bps.go.id. The European Forest Institute highlights agroforestry practices as a potential boon for production resilience, but cautions that such implementations require substantial capital and time. Amidst this raw material volatility, manufacturers are not only diversifying their sourcing strategies but also turning to synthetic alternatives, albeit with their own set of cost and performance challenges.

Regulatory scrutiny on PFAS and chemical additives

Starting January 2025, California's PFAS ban will reshape the landscape for outdoor and industrial glove applications, where water-repellent properties are paramount. Under the new regulations, manufacturers must ensure their products are devoid of PFAS. Enforcement will be stringent, with fines imposed on each item found to contain the banned substances. In response, companies are pivoting to materials certified by Bluesign, ZDHC, and Oeko-Tex 100 standards. However, many of these alternative treatments come at a cost, often sacrificing performance. Meanwhile, the FDA's draft guidance on chemical analysis for biocompatibility assessments adds layers of testing, potentially stalling product approvals and inflating development costs. Research in art conservation has spotlighted the inconsistency in glove compositions across manufacturers. While some accelerator-free formulations pass safety tests, others have been linked to metal corrosion. This intricate regulatory landscape poses challenges for smaller manufacturers, creating hurdles that established players, with their deep pockets for compliance and research and development, can more easily navigate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Rubber Dominance Faces Biodegradable Disruption

Rubber accounted for 48.28% of 2024 revenue in the hand gloves market due to its reliable elasticity and barrier strength. Rubber gloves (natural rubber latex and synthetic rubber like nitrile) dominate the global market, driven by superior performance, widespread adoption, and regulatory standards. Natural rubber gloves are preferred for high-precision applications like surgeries, while nitrile gloves address latex allergies with chemical and puncture resistance. Major players like Ansell and Top Glove leverage production capacities in countries like Malaysia to meet demand. Regulatory measures, such as India's Medical and Surgical Gloves (Quality Control) Order, 2024, ensure consistent demand for certified rubber gloves.

Biodegradable gloves are growing at an 11.27% CAGR due to environmental concerns over disposable glove waste. The U.S. EPA highlights billions of gloves contributing to landfills annually, driving demand for eco-friendly alternatives. Recent launches, such as ShieldON EcoSeries biodegradable nitrile gloves by United Global Trading Corp. in June 2024 and Top Glove's biodegradable nitrile gloves in January 2025, reflect this trend. Consumer preference and potential regulations favoring sustainability push manufacturers to innovate, while rubber gloves maintain dominance due to functionality and cost-effectiveness.

By Product Type: Disposable Pre-eminence Confronts Reusable Innovation

Disposable gloves accounted for 73.28% share of the hand gloves used for various industries market size in 2024, whereas reusable formats record the highest projected CAGR at 8.16% through 2030. Disposable hand gloves dominate the market due to their critical performance needs and stringent regulations across various industries, while biodegradable reusable gloves are growing at the fastest rate, driven by global sustainability efforts. Disposable gloves are essential PPE in healthcare to prevent cross-contamination and disease spread, as mandated by the WHO, U.S. FDA, and European standards (EN 455). Their reliability and barrier properties are vital for procedures from routine exams to surgeries. In industrial safety and food processing, OSHA and FDA Title 21 CFR Part 177 regulations require single-use gloves to protect workers and prevent foodborne illnesses, making disposability a necessity. Manufacturers like Top Glove and Ansell ensure cost-effective, large-scale production to meet demand.

Biodegradable, reusable gloves are rapidly gaining popularity due to environmental concerns over plastic waste from single-use items. Consumers and industries are adopting eco-friendly solutions aligned with global sustainability goals like the UN SDGs. Recent innovations support this shift. In April 2025, INTCO Medical launched Syntex synthetic disposable latex gloves, offering superior performance and biodegradability. Similarly, in May 2023, Cranberry introduced Bio Nitrile Biodegradable Nitrile Powder-Free Examination Gloves for sustainability. Manufacturers are using organic additives to accelerate decomposition in landfills from over 100 years to 1-5 years without compromising performance. These innovations and a cultural shift toward environmental responsibility are driving the high CAGR of sustainable alternatives, even as disposables maintain market dominance due to functional and regulatory advantages.

By End User: Industrial Safety Ascends Alongside Healthcare Core

Medical and healthcare institutions account for 39.41% of 2024 revenue, reflecting the stringent sterility codes and high procedure volume. Yet industrial safety lines are accelerating at an 8.96% CAGR as OSHA heightens enforcement and insurers tie premiums to PPE compliance. Construction, metal fabrication, and renewable-energy installations require cut-resistant and impact-absorbing designs rated ANSI/ISEA A6 or higher. Concurrently, food processors integrate antimicrobial treatments to conform with 21 CFR Parts 174 and 177, creating multipurpose glove specs.

Household cleaning maintains stable volumes, but premium SKUs—such as odor-resistant or touchscreen-friendly products—capture incremental value. Sports and winter categories remain lifestyle-oriented slivers, yet cross-pollinate material science into industrial prototypes. Pharmaceutical cleanrooms are driving demand for accelerator-free nitrile, supported by Merck’s EUR 300 million expansion of its research and development complex. These end-user segment shifts are diversifying revenue streams and lessening the hand gloves market's dependence on clinical channels.

Geography Analysis

In 2024, North America commands a 33.53% market share, driven by stringent FDA oversight and the expansion of ASCs, leading to increased sales of sterile gloves. The FDA's alignment of its Quality Management System Regulation with ISO 13485:2016 by 2026 incentivizes early compliance, benefiting domestic manufacturers. With a 24% tariff on Chinese imports, orders are shifting to factories in Malaysia and the United States, potentially raising average selling prices by 50% in 2025. Demand in Canada surges, fueled by the growth of its life-sciences cluster, while Mexico's automotive industry ramps up its procurement of cut-resistant gloves.

Asia-Pacific is rapidly emerging as the dominant market for industrial hand gloves, boasting a robust 7.82% CAGR. Countries like Thailand, Malaysia, and Vietnam are expanding their facilities, eager to secure contracts driven by U.S. reshoring. While Thai latex exports see a resurgence, thanks to local investments countering tapping declines, unpredictable weather keeps the supply chain on edge. Despite facing tariffs, China continues to cater to its substantial internal demand, largely fueled by its pharmaceutical sector's expansion. In India, a new biotech policy is paving the way for increased consumption of sterile nitriles, while Japan's aging population ensures consistent demand for medical gloves.

Europe's regulatory landscape is intricate: bans on PFAS are steering research and development towards water-based coatings and necessitating upgrades to production lines. Both Germany and France are championing sustainability, launching pilot programs for glove recycling in line with hospital sustainability initiatives. Meanwhile, Eastern European manufacturers are carving out a niche in the OEM supply chain, benefiting from lower labor costs and direct access to the EU market, all while navigating the compliance challenges faced by their Western counterparts.

Competitive Landscape

The hand gloves market is moderately fragmented, showcasing a balanced competition. Established multinational corporations vie with emerging regional players, the latter often capitalizing on cost advantages and specialized skills. A notable instance of strategic consolidation is Ansell's USD 640 million acquisition of Kimberly-Clark's PPE business in July 2024. This move not only bolstered Ansell's foothold in the cleanroom and laboratory markets but also set the stage for projected annual cost synergies of USD 10 million by the third year.

As labor costs rise and regulations tighten, technology adoption emerges as a pivotal differentiator. Companies are channeling investments into automation, smart materials, and sustainable manufacturing to stay ahead. There's a burgeoning interest in biodegradable materials and the integration of smart textiles. Here, traditional players find themselves challenged by nimble, technology-driven startups adept at swiftly refining product designs and manufacturing methods. A case in point is Rhino Health's USD 58 million expansion in Fort Worth, Texas, underscoring the trend of emerging players amassing substantial funding to establish domestic manufacturing. These new facilities aim to rival established suppliers from Asia.

Meanwhile, Top Glove's impressive turnaround, boasting an 80% revenue uptick and a staggering 325% profit leap in Q1 FY2025, serves as a testament to how market leaders can harness operational prowess and strategic positioning to benefit from favorable trade winds. Regulatory compliance is becoming a pivotal factor in the competitive arena. The FDA's recent updates to the Quality Management System Regulation pose entry challenges for smaller manufacturers, inadvertently giving an edge to firms with established quality systems and international certifications.

Hand Gloves Industry Leaders

-

Top Glove Corporation Bhd

-

Hartalega Holdings Berhad

-

Ansell Limited

-

Kossan Rubber Industries Bhd

-

Supermax Corporation Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Top Glove, in a move aligned with its comprehensive sustainability strategy, unveiled biodegradable nitrile gloves on World Environment Day. These innovative gloves are engineered to decompose in anaerobic environments, underscoring the company's commitment to environmental, social, and economic sustainability.

- July 2024: Ansell Limited completed its USD 640 million acquisition of Kimberly-Clark's Personal Protective Equipment business, enhancing its position in the Scientific and Industrial segments under the Kimtech and KleenGuard brands.

- June 2024: Top Glove launched biodegradable nitrile gloves designed to decompose in anaerobic environments around World Environment Day, aligning with the company's sustainability strategy that encompasses environmental, social, and economic aspects.

Global Hand Gloves Market Report Scope

| Kevlar |

| Nylon |

| leather |

| Cotton |

| Rubber (Natural and synthetic Rubber) |

| Nitrile |

| Neoprene |

| Biodegradable/Plant-based |

| Others (Polyethylene, Vinyl, etc..) |

| Disposable Gloves |

| Reusable Gloves |

| Medical and Health care | |

| Industrial Safety Gloves | Chemical Industry |

| Food processing Industry | |

| Construction | |

| Others | |

| Household | |

| Sports and fitness Gloves | |

| Winter Gloves | |

| Fashion Gloves | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Material | Kevlar | |

| Nylon | ||

| leather | ||

| Cotton | ||

| Rubber (Natural and synthetic Rubber) | ||

| Nitrile | ||

| Neoprene | ||

| Biodegradable/Plant-based | ||

| Others (Polyethylene, Vinyl, etc..) | ||

| By Product Type | Disposable Gloves | |

| Reusable Gloves | ||

| By End User | Medical and Health care | |

| Industrial Safety Gloves | Chemical Industry | |

| Food processing Industry | ||

| Construction | ||

| Others | ||

| Household | ||

| Sports and fitness Gloves | ||

| Winter Gloves | ||

| Fashion Gloves | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global hand gloves market and what is the expected growth rate?

The global hand gloves market is valued at USD 110 billion in 2025 and is projected to reach USD 151.7 billion by 2030, registering a compound annual growth rate (CAGR) of 6.64% during the forecast period.

Which factors are driving the growth of the hand gloves market?

Key growth drivers include surge in healthcare-associated infection (HAI) prevention regulations, increased occupational safety mandates in emerging industries drives the market.

What is the split between disposable and reusable gloves?

Disposable gloves dominate the market with 73.28% share in 2024, reflecting their convenience and infection control advantages in healthcare settings.

Which region dominates the global hand gloves market?

North America maintains the largest market share at 33.53% in 2024, driven by stringent healthcare regulations and advanced manufacturing capabilities.

Page last updated on: