United States Dental Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.62 Billion |

| Market Size (2026) | USD 2.86 Billion |

| Market Size (2031) | USD 4.42 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Dental Software Market Analysis by Mordor Intelligence

The United States Dental Software Market size is projected to be USD 2.62 billion in 2025, USD 2.86 billion in 2026, and reach USD 4.42 billion by 2031, growing at a CAGR of 9.12% from 2026 to 2031.

The market is moving ahead as dental practices replace disconnected tools with integrated platforms that can manage scheduling, billing, imaging links, and patient communication in one workflow. The United States dental software market is also being shaped by 3 linked shifts, which are the rise of DSO ownership, the move away from server-based deployments, and the wider commercial use of AI in front-office and claims functions. DSO affiliation among U.S. dentists rose from 7.2% in 2015 to 16.1% in 2024, and the figure reached 26.5% among dentists within 10 years of graduation, which is pushing larger groups toward standardized software across acquired sites. Consumer spending on dental care rose 4% in 2024, and 75 dental schools are now producing record graduating classes, which supports treatment demand and adds operating scale across the care system. At the same time, average dentist net income declined to USD 207,980 in 2024 from USD 267,168 in 2010, so software vendors in the United States dental software market must show clear revenue, labor, or reimbursement benefits before practices commit to higher recurring spend.

Key Report Takeaways

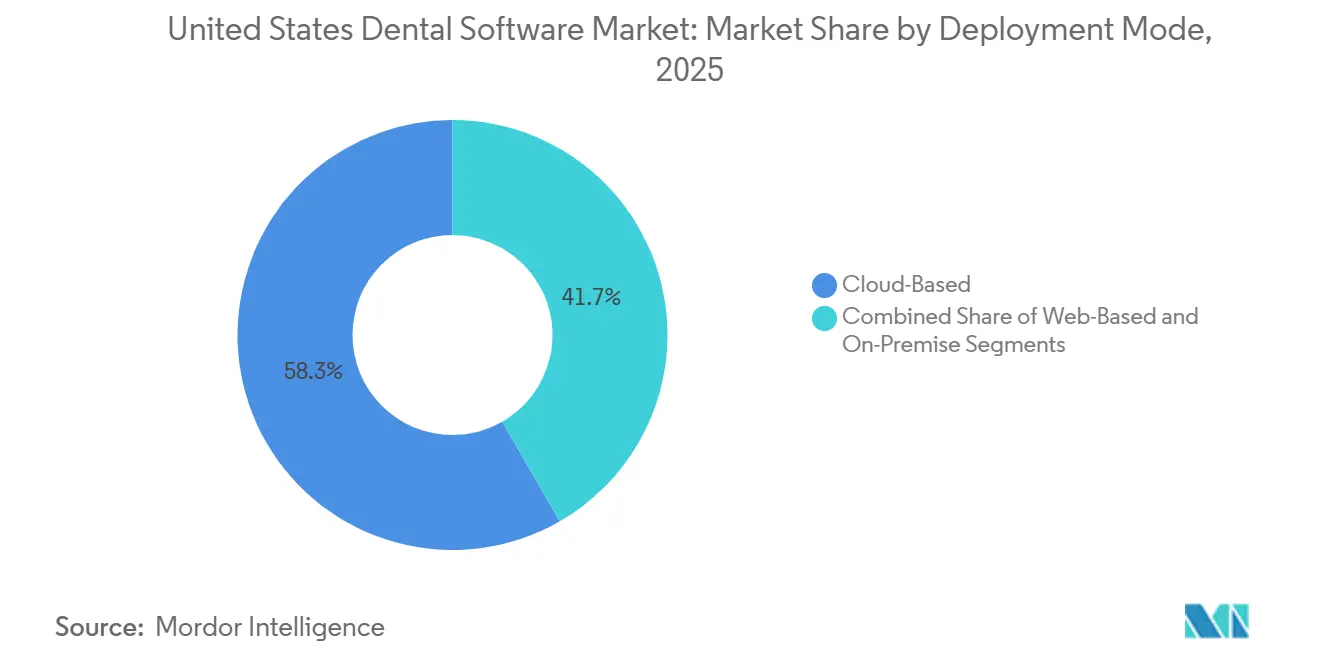

- By deployment mode, cloud-based deployment held 58.31% of the United States dental software market share in 2025, while cloud-based deployment also recorded the highest projected CAGR at 11.38% through 2031.

- By application, appointment scheduling and calendar management accounted for 26.24% of the United States dental software market size in 2025, while patient communication and engagement is forecast to expand at a 12.52% CAGR through 2031.

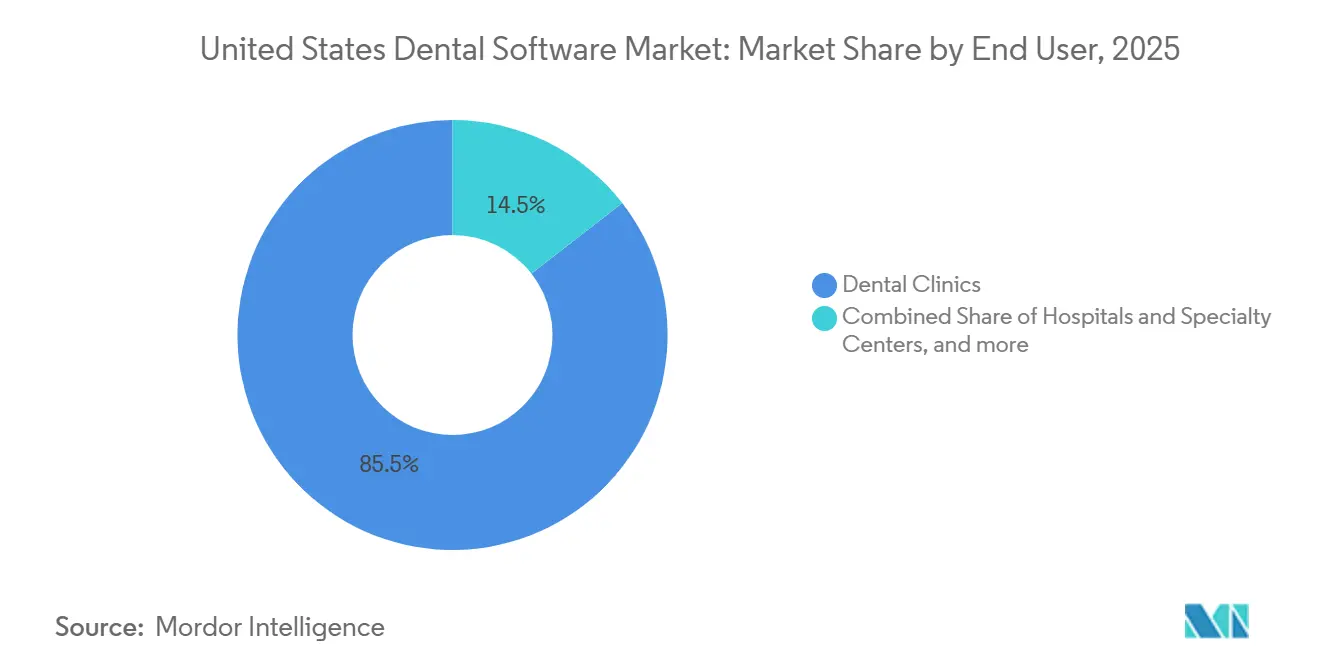

- By end user, dental clinics held 85.52% share in 2025, while hospitals and specialty centers are projected to grow at a 13.25% CAGR through 2031.

- By practice size, solo practices held 38.24% share in 2025, while large DSOs and enterprise chains are projected to grow at a 12.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Dental Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workflow automation demand in busy practices | +2.0% | National, with early gains in urban/suburban metro clusters | Short term (≤ 2 years) |

| Cloud migration to reduce server overhead | +1.7% | National, highest acceleration in Sun Belt and Western states | Short term (≤ 2 years) |

| AI-assisted scheduling, billing, and analytics | +1.5% | National, led by DSO-concentrated states such as Texas, Florida, Arizona, and Colorado | Medium term (2-4 years) |

| DSO consolidation and standardization | +1.3% | National, with concentrated activity in the Southeast and Southwest | Medium term (2-4 years) |

| Interoperability pressure across imaging, claims, and EHRs | +0.9% | National, with stronger compliance relevance in federally qualified health center markets | Long term (≥ 4 years) |

| Teledentistry and digital patient engagement expectations | +0.8% | National, with stronger relevance in rural and underserved regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Workflow Automation Reduces Administrative Overhead Across Practice Sizes

The United States dental software market is benefiting from a stronger automation case as practices try to do more with tighter staffing and more pressure on margins. VideaHealth stated that its AutoVerify launch in January 2026 connected practices to 350+ payers, saved up to 40 hours per week, accelerated reimbursements by 40%, and reduced claim denials by 50%, which gives buyers clear proof that workflow tools can change daily economics. This matters because many practices are no longer looking at automation as a convenience layer, and are instead using it to reduce repetitive tasks that absorb front-desk time. The same logic is spreading into claim review, eligibility checks, and reminders, where errors and delays create lost revenue rather than only extra work. As a result, the United States dental software market is seeing stronger demand for products that can document direct savings in staff time, payment speed, and production capture.

Cloud Migration Shifts Practice Economics Toward More Flexible Operating Models

The United States dental software market is moving steadily toward cloud infrastructure because multi-site reporting, automatic updates, and remote access are becoming basic operating needs rather than optional features. Henry Schein One introduced tiered Dentrix Ascend packaging in March 2026 to serve de novo practices, growing groups, and enterprise DSOs through a single cloud platform structure, which shows how vendors are aligning product design with practice scale. In April 2026, Henry Schein One also opened the Dentrix Ascend MCP layer to AI agents and custom workflow builders, which shows that cloud platforms are developing into operating environments that can support new tools without separate data connectors. This shift is especially important for DSOs because standardized cloud systems reduce variation across locations and make newly acquired sites easier to bring onto one workflow. The United States dental software market is therefore rewarding vendors that can combine lower local IT burden with centralized visibility and a clear upgrade path.

AI-Assisted Scheduling, Billing, and Analytics Create Clear Performance Separation

The United States dental software market is entering a stage where AI tools are being judged by measurable operating outcomes rather than experimental value. VideaHealth and Aspen Dental reported in February 2026 that VideaAI was deployed across 1,100+ Aspen Dental locations in 6 weeks and increased acceptance of recommended care by 12%, especially for early-stage, non-invasive treatment. Henry Schein One launched Image Verify in February 2026 to assess image quality within Dentrix and Dentrix Ascend before claims are submitted, which ties AI directly to reimbursement workflow rather than to a separate clinical add-on. Planet DDS also expanded voice-enabled charting in 2026 through AI Voice Perio and AI Voice Restorative Charting, which shows that AI is spreading across both front-office and chairside documentation tasks. That is raising the bar in the United States dental software market because platforms that do not embed AI into core workflow are becoming harder to justify to buyers who now expect proof of financial or clinical lift.

DSO Consolidation Reshapes Technology Procurement Across the Value Chain

The United States dental software market is being reshaped by DSO expansion because ownership concentration changes how software is chosen, deployed, and renewed. DSO affiliation rose to 16.1% of U.S. dentists in 2024, and 26.5% of dentists within 10 years of graduation were DSO-affiliated, which shows why enterprise purchasing structures now have more influence over platform selection. Henry Schein One said in March 2026 that it supports 48,000+ U.S. practices and 90% of the top 50 DSOs, which highlights the advantage of vendors that already sit inside the largest buying networks. When a DSO adds locations, software decisions can shift from local choice to portfolio-wide standardization, which compresses sales cycles for the incumbent vendor and makes displacement harder for smaller rivals. This is why the United States dental software market increasingly favors platforms that can support a practice from single-site setup through multi-state scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HIPAA, HITECH, and state privacy compliance cost | -1.20% | National, with a disproportionate burden on solo and small-group practices | Short term (≤ 2 years) |

| Legacy migration and vendor lock-in friction | -0.90% | National, with the highest friction in practices with custom imaging integrations | Medium term (2-4 years) |

| Upfront software, implementation, and training costs | -0.80% | National, concentrated among rural and sub-5-location practices with limited capital budgets | Short term (≤ 2 years) |

| Sparse dental IT support in smaller practices | -0.60% | Rural and exurban markets, with a stronger effect on solo and small-group practices outside major metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HIPAA, HITECH, and State Privacy Compliance Disproportionately Burden Smaller Practices

The United States dental software market still faces resistance from compliance and security demands that smaller practices cannot spread across a large administrative base. Solo and small-group offices often carry the same documentation, access control, and audit expectations as larger organizations, but they do not have the same internal IT support or purchasing leverage. That cost pressure is pushing more buyers toward vendors that can present security, user permissions, audit logs, and claims-related controls as part of the core subscription. State-specific privacy rules add another layer because multi-state groups need tools that can operate across different legal settings without separate manual work at every location. This slows some buying decisions in the United States dental software market, even though it also strengthens the case for modern platforms over legacy systems.

Legacy Migration Friction Delays Adoption but Does Not Stop It

The United States dental software market continues to face switching friction because dental practices often depend on years of patient history, imaging links, payer setup, and custom workflow habits. That friction is strongest when the existing software is tied to imaging devices or treatment workflows that staff use every day and do not want to interrupt. Henry Schein One expanded integration with Align Technology's iTero intraoral scanners in February 2026, which shows how deep workflow ties can reinforce loyalty once a platform becomes central to day-to-day operations. At the same time, vendors are trying to reduce that lock-in effect by widening interoperability, as seen in Henry Schein's LinkIt launch in August 2025 and in broader moves toward connected ecosystems[1]Henry Schein One, “Henry Schein and Henry Schein One Launch ‘LinkIt’, Enabling Industry-First Seamless Digital Workflow Within Dentrix,” Business Wire, investor.henryschein.com. This means migration still slows platform changes in the United States dental software market, but the barrier is becoming less durable as buyers place more value on long-term workflow flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Infrastructure Consolidates Its Position as Practice Standard

Cloud-based deployment held 58.31% of the United States dental software market size in 2025, and it is also the fastest-growing deployment mode with an 11.38% CAGR from 2026 to 2031. The lead reflects a deeper shift in the United States dental software market toward centralized administration, remote access, and easier updates across growing practice networks. Cloud systems fit the needs of both independent practices and DSOs because they remove local server dependence and make reporting easier across more than 1 site. They also give vendors a faster path to release new billing, workflow, and AI features without waiting for local hardware changes.

Henry Schein One's March 2026 Dentrix Ascend rollout with Essentials, Pro, and Accelerate packaging showed how cloud vendors are using tiered design to cover every practice stage from startup to large DSO. In April 2026, the company opened the Dentrix Ascend MCP layer to AI agents and custom workflow development, which moved the product beyond software access and into a broader platform role. Web-based products still occupy a middle position in the United States dental software industry because they improve access compared with server-based tools, but they do not always offer the same depth of multi-site control or native AI readiness as cloud-native products. On-premise platforms remain present in established groups with embedded imaging and billing links, yet their position is weakening as buyers place more value on centralized management and easier integration.

By Application: Scheduling Leads Revenue While Patient Communication Leads Growth

Appointment scheduling and calendar management held the largest application share at 26.24% in 2025, which keeps it at the center of the United States dental software market because patient flow, chair utilization, and front-desk throughput all start there. Scheduling has become more than calendar administration because it now supports reminders, cancellation recovery, and production planning. Planet DDS said in its 2026 Dental Industry Outlook that cancellations fell 17% and no-show rates also declined year over year across data drawn from 8,500+ practices, which reinforces how central these tools are to day-to-day performance[2]Planet DDS, “2026 Dental Industry Outlook,” Planet DDS, planetdds.com. In the United States dental software market, that makes scheduling one of the clearest functions where software can be linked to visible revenue capture.

Patient communication and engagement is projected to grow at a 12.52% CAGR through 2031, the fastest rate among application segments, because patients now expect digital convenience that matches other service categories. Planet DDS launched MyTooth in January 2026 as a native Denticon patient experience layer that writes booking and intake data back into the live practice management environment in real time. Billing, payment processing, and treatment planning remain essential, but growth is shifting toward tools that reduce friction before and after the clinical visit. That pattern is strengthening in the United States dental software industry because patient retention and communication quality now affect both practice efficiency and treatment acceptance.

By End User: Dental Clinics Anchor Demand While Hospitals and Specialty Centers Accelerate

Dental clinics held 85.52% of end-user demand in 2025, which reflects the size and breadth of the office-based care network inside the United States dental software market. The ADA reported 135,333 dental practice establishments in 2025, which explains why clinic workflows still drive most software purchasing across scheduling, claims, charting, and communication. This part of the United States dental software market ranges from independent solo offices to large affiliated groups, but the broad need is similar because each location must keep administrative work, patient volume, and reimbursement flow under control. The difference is that larger clinic groups are now placing more value on centralized reporting and standard operating models than on isolated site-level customization.

Hospitals and specialty centers are projected to grow at a 13.25% CAGR from 2026 to 2031, which makes them the fastest-growing end-user segment. NextGen Healthcare positions its dental EHR and practice management offering around dental workflows that must connect with broader medical settings, which matters in community health, integrated care, and compliance-heavy environments. In May 2026, NextGen Healthcare was chosen by Chestnut Health Systems to deploy enterprise EHR and practice management tools across integrated dental, primary care, and behavioral health programs in Illinois and Missouri, confirming that medical-dental coordination is becoming a stronger purchasing factor. Dental Service Organizations and related enterprise buyers remain smaller in count, but their technology decisions influence many affiliated practices at once, which gives them outsized weight in the United States dental software market.

By Practice Size: Solo Practices Hold the Largest Share While Enterprise Chains Post the Fastest Growth

Solo practices held 38.24% of the market in 2025, and this remains an important base for the United States dental software market because many dentists still operate independently. The ADA found that 34% of U.S. dentists still worked as solo practitioners, which helps explain why affordability, usability, and low local IT burden continue to matter in buying decisions. For this group, the best-performing vendors are often those that combine scheduling, billing, and patient messaging in a simple monthly subscription rather than through separate modules. That keeps solo demand active even as larger organizations capture a growing share of new software upgrades.

Large DSOs and enterprise chains are projected to grow at a 12.82% CAGR from 2026 to 2031, and this is the most important structural growth pocket inside the United States dental software market. The same ADA workforce update showed that DSO affiliation was already especially strong in Arizona, Colorado, Georgia, Nevada, Oklahoma, Texas, and Florida, where 25% of dentists were DSO-affiliated in 2024. As enterprise groups add locations, they tend to standardize software across acquired sites, which favors vendors already proven in multi-location reporting, training, and claims workflow. This part of the United States dental software industry is therefore expanding faster than the rest of the field, even though the broader customer base remains widely distributed.

Geography Analysis

The South and Southwest represent the most concentrated enterprise demand pockets in the United States dental software market because several states in these regions already show high DSO penetration. In Arizona, Colorado, Georgia, Nevada, Oklahoma, Texas, and Florida, 25% of dentists were DSO-affiliated in 2024, which gives software vendors a larger base of buyers that prefer standardized, multi-site-ready platforms. These states matter because a single DSO technology decision can affect many affiliated offices at the same time. They also combine large population centers with active practice expansion, which keeps replacement cycles moving in both general and specialist settings. For the United States dental software market, that makes the Sun Belt one of the clearest regions where enterprise workflow design and rollout speed can shape competitive outcomes.

The Western United States combines strong group-practice density with a large installed base of digitally active providers. Colorado and Arizona each had more than 20% of dentists working in 100+ location practices, which supports steady demand for cloud-native software built for centralized control and cross-site visibility. California adds another layer because privacy and compliance expectations are more demanding, so vendors with stronger controls and integration design have a clearer advantage. The Northeast differs because it contains a dense concentration of specialty practices, urban referral centers, and academic environments where imaging links and EHR compatibility carry more weight in the buying decision. Pennsylvania and New York also recorded some of the sharpest declines in dentist-per-capita ratios, which increases the value of software that helps practices use staff time and chair capacity more efficiently.

Rural markets remain the most underserved opportunity area in the United States dental software market because provider density is much lower than in urban areas. Rural counties had 32.7 dentists per 100,000 population in 2024, while urban counties had 64.7 per 100,000, which means many rural practices must do more with smaller local care networks. These offices are also less likely to be inside large DSO structures, so modernization depends more on simple deployment, remote support, and patient communication features than on enterprise mandates. That leaves the United States dental software market with a meaningful long-term opening for vendors that can deliver low-complexity platforms with mobile access, digital intake, and flexible communication tools.

Competitive Landscape

The United States dental software market is moderately fragmented at the practice level, but it is more concentrated in the DSO and enterprise layer where a few vendors hold stronger positions. Henry Schein One stated in March 2026 that its Dentrix and Dentrix Ascend franchise supports 48,000+ U.S. practices and 90% of the top 50 DSOs, which gives it a clear installed-base advantage in larger accounts. Planet DDS has also built a strong position around an open platform approach, and its 2026 Dental Industry Outlook said the company supports 13,000+ practices and 118,000 users through connected workflows. Cloud-native challengers such as CareStack, Curve Dental, and Planet DDS are gaining traction by focusing on migration ease, total ownership cost, and embedded AI rather than on legacy feature depth alone. This leaves the United States dental software market open at the small and mid-sized practice tier, even while large enterprise accounts show stronger vendor concentration.

Competitive strategy is now converging around 3 priorities, which are embedded AI, deeper interoperability, and product structures matched to practice size. CareStack and Overjet introduced the Smart Dental Platform in March 2025, combining cloud practice management, clinical AI, VoIP, and revenue analytics into a single operating model that reflects the push toward unified platforms[3]CareStack and Overjet, “CareStack and Overjet Introduce First-Of-Its-Kind Smart Dental Platform,” CareStack, resources.carestack.com. Henry Schein One launched Image Verify in February 2026 to improve claim quality inside existing workflow, which shows how leading vendors are placing AI directly inside reimbursement and operational tasks. The company had already introduced LinkIt in August 2025 and expanded Dentrix integration with Align Technology's iTero scanners in February 2026, which shows a deliberate effort to strengthen workflow continuity across imaging and planning steps. VideaHealth and Henry Schein One also launched the Impact Panel in November 2025, adding AI-driven patient education to Dentrix and Dentrix Ascend, which further shows how vendors are trying to keep AI inside the main software environment instead of in separate tools.

A clear white space remains in sub-10-location groups that have outgrown basic solo-practice tools but do not want enterprise-level complexity or pricing. Vendors that can serve 5-site to 50-site organizations with stronger analytics, central billing visibility, and manageable onboarding have room to gain share during the forecast period. The United States dental software market also favors companies that make data movement and third-party connectivity easier, because buyers are becoming less willing to accept closed systems that limit future workflow changes. That balance between concentration in the top DSO accounts and fragmentation in the long tail explains why no single vendor controls the full United States dental software market today.

United States Dental Software Industry Leaders

Henry Schein One

Open Dental Software

Patterson Dental

Planet DDS

Curve Dental

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: NextGen Healthcare was selected by Chestnut Health Systems to deploy NextGen Enterprise EHR and Enterprise PM across integrated dental, primary care, and behavioral health programs in Illinois and Missouri, demonstrating growing demand for cross-specialty, ONC-certified platforms in community health settings.

- February 2026: Synchrony and Planet DDS expanded their partnership to designate CareCredit as the preferred patient financing solution across all Planet DDS platforms including Denticon, extending to 2,500+ orthodontic practices under a multi-year agreement.

United States Dental Software Market Report Scope

As per the scope of the report, dental software refers to specialized computer programs designed to assist dental professionals in managing various aspects of dental practice operations. It typically includes features for patient record management, appointment scheduling, billing and insurance processing, treatment planning, imaging, and clinical documentation.

The United States dental software market is segmented by deployment mode into cloud-based solutions, web-based platforms, and on-premise systems. By application, the market includes patient communication and engagement tools, appointment scheduling and calendar management, billing and invoicing services, payment processing solutions, treatment planning and charting tools, imaging and diagnostics integration, and other relevant applications. By end user, the segmentation covers dental clinics, hospitals and specialty centers, dental service organizations, and additional end users. By practice size, the market is categorized into solo practices, small group practices, mid-market multi-site practices, and large DSOs/enterprise chains. For each segment, the market size and forecast are provided in terms of value (USD).

| Cloud-Based |

| Web-Based |

| On-Premise |

| Patient Communication & Engagement |

| Appointment Scheduling & Calendar |

| Billing & Invoicing |

| Payment Processing |

| Treatment Planning & Charting |

| Imaging & Diagnostics Integration |

| Other Applications |

| Dental Clinics |

| Hospitals & Specialty Centers |

| Dental Service Organizations |

| Other End Users |

| Solo Practices |

| Small Group Practices |

| Mid-Market Multi-site Practices |

| Large DSOs / Enterprise Chains |

| By Deployment Mode | Cloud-Based |

| Web-Based | |

| On-Premise | |

| By Application | Patient Communication & Engagement |

| Appointment Scheduling & Calendar | |

| Billing & Invoicing | |

| Payment Processing | |

| Treatment Planning & Charting | |

| Imaging & Diagnostics Integration | |

| Other Applications | |

| By End User | Dental Clinics |

| Hospitals & Specialty Centers | |

| Dental Service Organizations | |

| Other End Users | |

| By Practice Size | Solo Practices |

| Small Group Practices | |

| Mid-Market Multi-site Practices | |

| Large DSOs / Enterprise Chains |

Key Questions Answered in the Report

What is the current value of dental software demand in the United States?

The United States dental software market was valued at USD 2.62 billion in 2025 and stands at USD 2.86 billion in 2026, with growth supported by cloud migration, DSO expansion, and AI-enabled workflow tools.

How fast is dental software spending expected to grow through 2031?

The United States dental software market is projected to reach USD 4.42 billion by 2031, growing at a 9.12% CAGR from 2026 to 2031.

Which deployment model is leading adoption across dental practices?

Cloud-based deployment led with a 58.31% share in 2025 and is also the fastest-growing model at an 11.38% CAGR through 2031, reflecting demand for easier updates, lower local IT burden, and multi-site visibility.

Which software application is most important for revenue and workflow control?

Appointment scheduling and calendar management held the largest application share at 26.24% in 2025 because patient flow, reminders, and chair utilization all depend on it.

Why are DSOs so important for vendor strategy in this space?

DSO affiliation reached 16.1% of U.S. dentists in 2024, and 26.5% among early-career dentists, so enterprise buyers now influence software standardization across many affiliated practices at once.

What is the strongest growth opportunity by customer type?

Hospitals and specialty centers are projected to grow at a 13.25% CAGR through 2031, supported by integrated medical-dental workflows and broader reporting requirements in community health settings.

Page last updated on: