Dental CAD Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.33 Billion |

| Market Size (2031) | USD 4.96 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

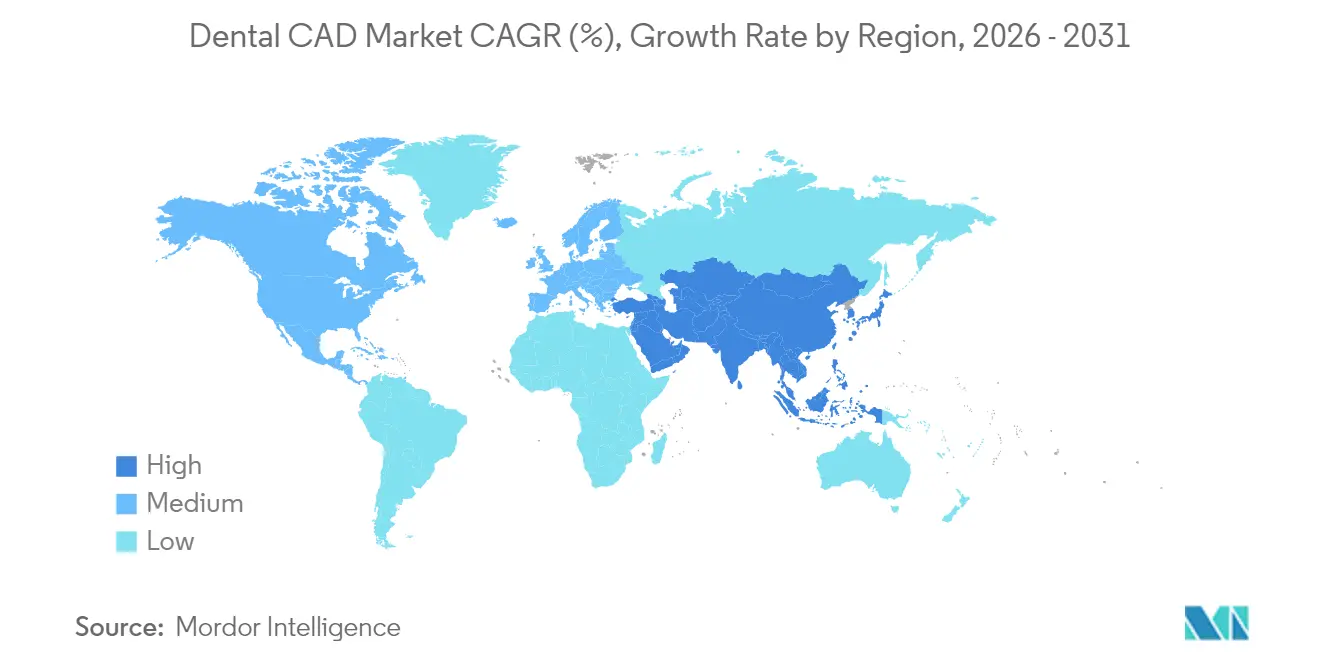

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dental CAD Market Analysis by Mordor Intelligence

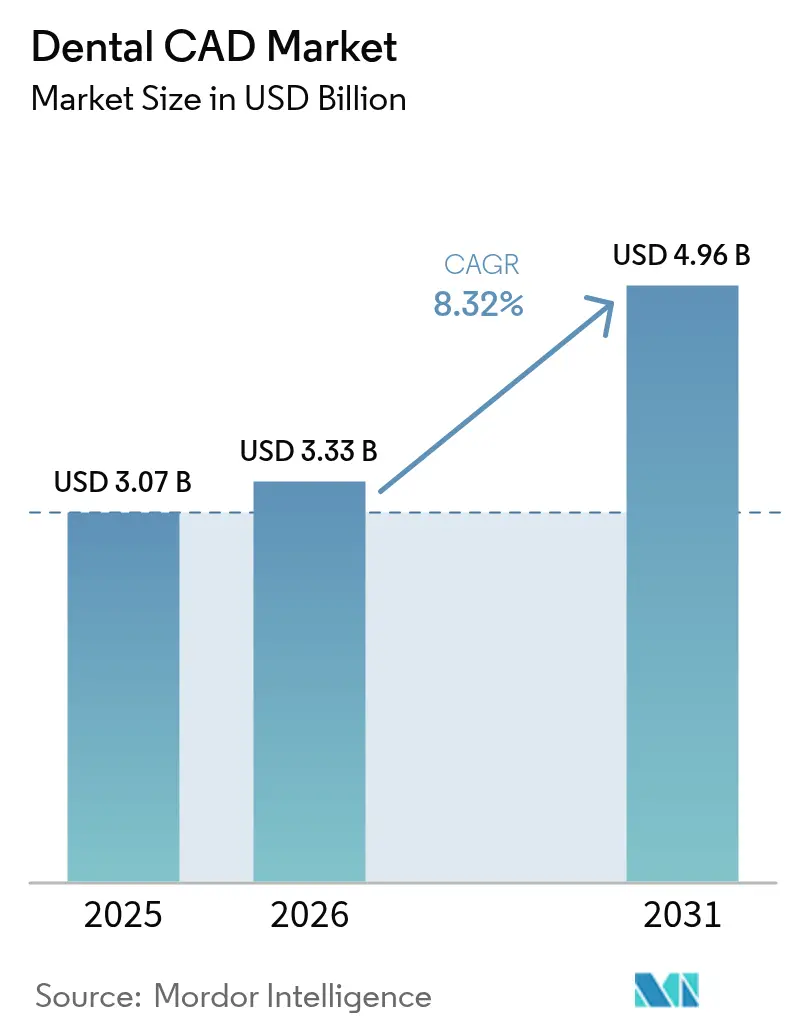

The Dental CAD market size is expected to grow from USD 3.07 billion in 2025 to USD 3.33 billion in 2026 and is forecast to reach USD 4.96 billion by 2031 at 8.32% CAGR over 2026-2031.

Growth rests on the accelerating shift from analog laboratories to end-to-end digital workflows, which shorten crown design-to-delivery cycles from hours to minutes while preserving micrometer-level accuracy. Artificial-intelligence (AI) layers now automate restoration design, suggesting connectors, emergence profiles, and occlusal contacts in real-time, and trim two-thirds of manual CAD time per case. Hardware commoditization is nudging competitive advantage toward software ecosystems that unify intraoral scanners, cloud collaboration portals, and chairside milling units. Demographic aging, rising implant acceptance, and global DSO consolidation further anchor long-range growth as large practice networks standardize procurement and training across hundreds of sites. Europe maintains leadership through stringent quality standards and early digital adoption, yet Asia-Pacific shows the steepest curve as healthcare infrastructure investment coincides with growing patient spending power.

Key Report Takeaways

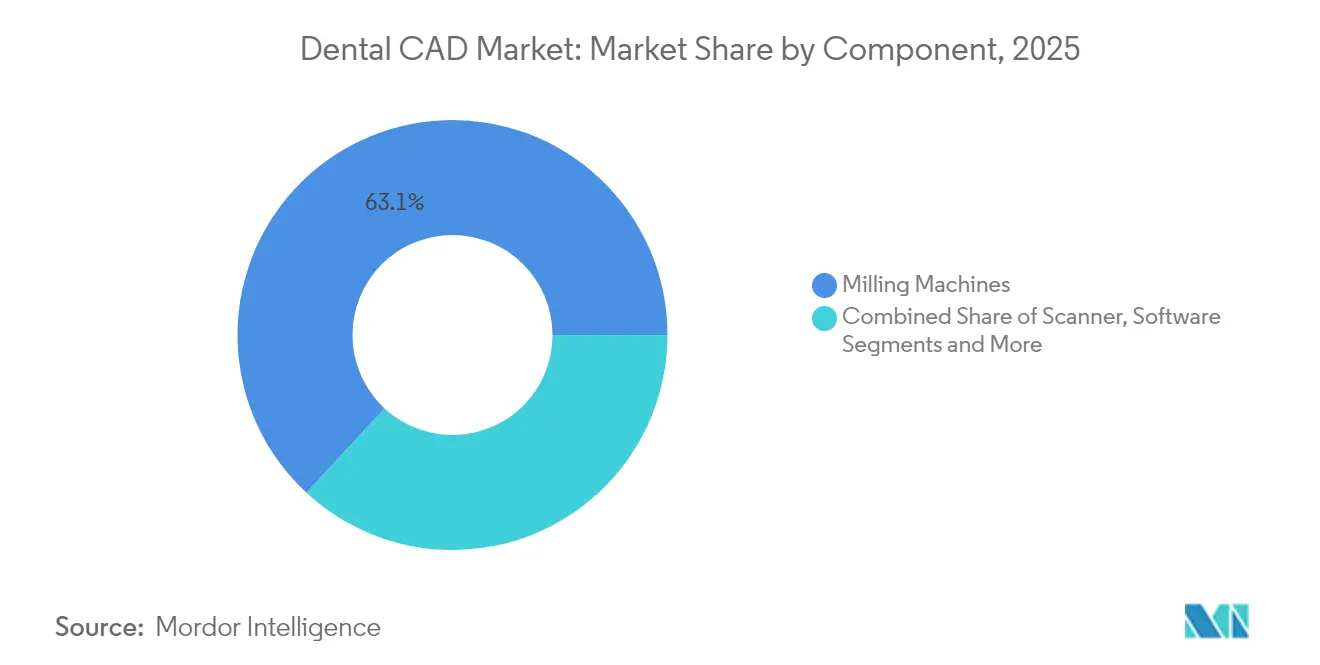

- By component, milling machines led with a 63.12% revenue share in 2025; software is projected to register a 9.48% CAGR from 2026 to 2031.

- By end user, dental laboratories held 42.05% of the market in 2025, while dental clinics and hospitals are set to expand at a 10.05% CAGR through 2031.

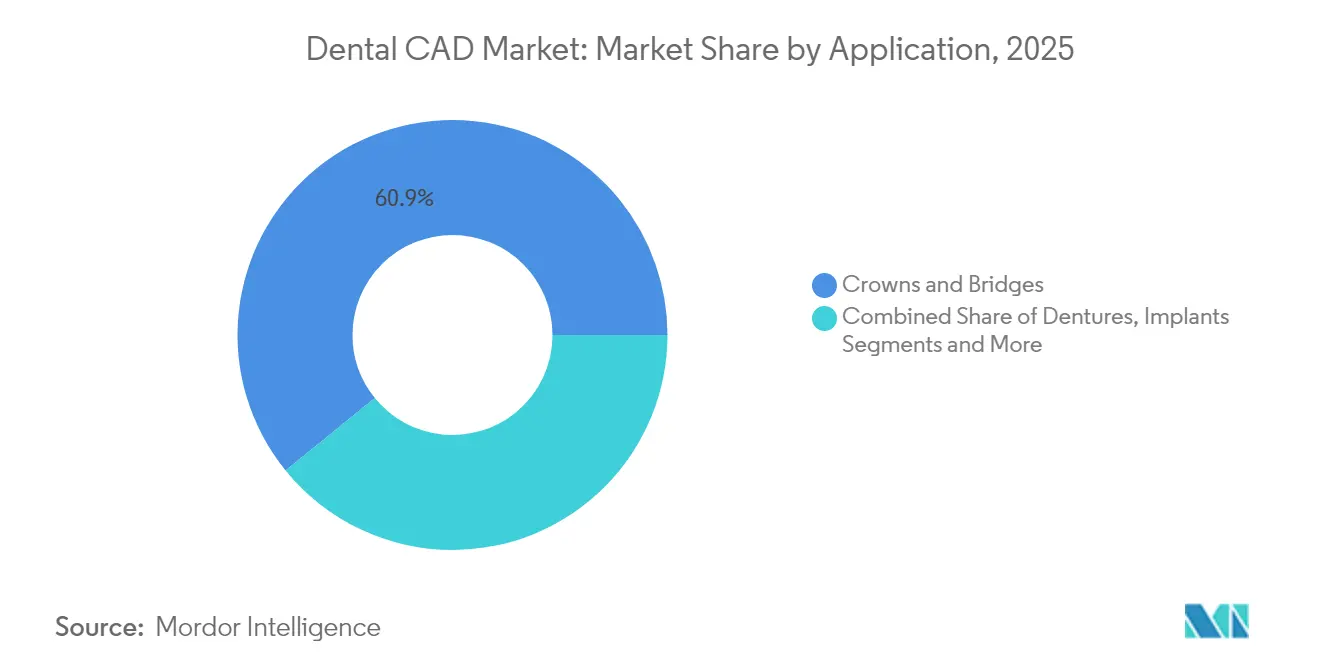

- By application, crowns and bridges captured a 60.85% revenue share in 2025; implants are the fastest-growing segment, forecasted to rise at an 10.62% CAGR through 2031.

- By geography, Europe accounted for 32.20% of the 2025 revenue, whereas the Asia-Pacific region is poised for an 11.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental CAD Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Chairside Digital Workflows | +2.1% | Global, with North America & Europe leading | Medium term (2-4 years) |

| Rising Prevalence of Restorative & Prosthetic Procedures | +1.8% | Global, with APAC showing highest growth | Long term (≥ 4 years) |

| Cost- & Time-Efficiency Versus Conventional Techniques | +1.5% | Global, particularly high-volume practices | Short term (≤ 2 years) |

| Integration with Intraoral Scanning & 3-D Printing Ecosystems | +1.3% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| AI-driven Generative Design for Complex Restorations | +0.9% | North America & Europe initially | Long term (≥ 4 years) |

| DSO Roll-outs of Standardized CAD Platforms | +0.7% | North America primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Chairside Digital Workflows

Same-day dentistry is now tangible because chairside systems link intraoral scanners, AI-enabled CAD engines, and four-axis mills in a single appointment window. Practices deploying a second mill report 145% production lifts within four months as average monthly units jump from 13.3 to 27.5. Patients show strong preference for single-visit crowns, with 85% valuing convenience and half agreeing to premium pricing. Scanner refresh rates of 1.3 seconds and 94% acceptance rates for AI-proposed designs further compress clinical bottlenecks. Nevertheless, offices must synchronize scanning, design, nesting, and milling while adhering to infection-control protocols and insurance coding.

Rising Prevalence of Restorative & Prosthetic Procedures

The proportion of adults aged 65+ is swelling in every major economy, raising restorative workloads that reward CAD precision. Full-arch implant plans merge cone-beam CT with parametric libraries to place fixtures within ±50 µm of intended axes. Surgeons increasingly deploy 3-D-printed titanium meshes shaped by CAD to steer guided bone regeneration, customizing pore width to vascularization requirements and lowering bill-of-materials versus machined alternatives. Digital smile-design modules overlay facial scans on intraoral data, allowing shade simulation and occlusal mapping before irreversible drilling. Integration of photogrammetry devices further expands data richness, enabling bite capture during open-tray impressions without splints.

Cost- & Time-Efficiency Versus Conventional Techniques

Complete chairside rigs cost USD 75,000-200,000, spanning scanners, software, and milling hardware. Practices achieving 30 crowns a month recoup the investment inside 24 months once laboratory fees, shipping, and remake waste are stripped out. Chairside workflows also wipe out the two-week lag tied to physical impressions and resin models, improving case acceptance and reducing second appointments. Material spend for in-house crowns averages 17% of external lab invoices, with AI routines cutting manual design labor by 40 minutes per unit. Low-volume offices, by contrast, lean on leasing or pay-per-use models that neutralize obsolescence risk.

AI-Driven Generative Design for Complex Restorations

Artificial intelligence integration represents the most transformative trend in dental CAD, with generative design algorithms automating complex restoration geometry while maintaining clinical requirements and aesthetic preferences. VideaHealth's FDA clearance for over 30 AI algorithms marks the largest regulatory approval in dental AI history, enabling automated detection and treatment planning across virtually every disease state in dentistry. AI-powered design tools achieve 94% acceptance rates for automatically generated crown geometries, reducing design time through manual processes while improving consistency across different technicians. The technology extends beyond simple automation to predictive capabilities, with AI systems analyzing the creation of ent-specific factors, including occlusal patterns, material properties, and long-term wear characteristics. Machine learning algorithms trained on thousands of successful restorations can identify optimal design parameters for specific clinical scenarios. The integration challenge involves validating AI-generated designs against clinical outcomes, necessitating the use of independent datasets to prevent algorithmic bias and ensure diagnostic accuracy.[1]Food and Drug Administration, "Endosseous Dental Implants and Endosseous Dental Implant Abutments-Performance Criteria for Safety and Performance Based Pathway," Federal Register, federalregister.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure | -1.2% | Global, particularly smaller practices | Short term (≤ 2 years) |

| Limited Reimbursement for CAD/CAM Restorations | -0.8% | North America & Europe primarily | Medium term (2-4 years) |

| Cyber-Security & Data-Interoperability Risks | -0.6% | Global, with stricter EU regulations | Long term (≥ 4 years) |

| Technician Skills Gap in Parametric Modelling | -0.4% | Global, more acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

A premium chairside package can top USD 150,000 and depreciates over three to five years, forcing smaller offices to weigh loan payments against fluctuating case volumes. Annual service contracts and software subscriptions tack on 20-30% of list prices, while frequent firmware updates can mandate hardware upgrades. Leasing, revenue-share agreements, and design-as-a-service portals have emerged to cushion the blow, but each model imposes its own margin erosion and data-sovereignty questions.

Limited Reimbursement for CAD/CAM Restorations

Insurance schedules seldom differentiate between laboratory crowns and same-day CAD units, transferring extra material and equipment costs to patients. Chairside units therefore skew toward fee-for-service geographies or premium patient segments. Compliance adds further drag: digital audits require storage of STL, scan, and mill logs for up to 10 years in some states. Professional associations are lobbying insurers to craft new CDT codes that reflect the demonstrable reduction in remakes and secondary caries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Captures Value as Hardware Matures

Milling units held 63.12% of the dental CAD market share in 2025, underscoring the indispensability of subtractive workflows for final zirconia and hybrid ceramic restorations. Entry-level mills list at USD 20,000-50,000, mid-range at USD 50,000-100,000, and flagship five-axis systems at USD 100,000-150,000, allowing clinicians to scale capacity to patient throughput. Scanner throughput leapt 53% over the last hardware generation, capturing full-arch data in under 40 seconds and pre-segmenting margin lines via embedded AI.

Software, however, is the fastest-growing component, with a 9.48% CAGR. Vendors are pivoting to subscription and cloud license bundles that smooth cash flows while continuously updating their AI models. Exocad’s DentalCAD 3.2 shipped AI Design to auto-generate crown libraries, whereas 3Shape Automate now closes roughly 94% of crown designs without technician touch-ups. Beyond design, platforms integrate case tracking, remote approval, and KPI dashboards, letting multi-site groups compare rounding errors and turnaround-time deltas. Open API philosophies are likewise proliferating to court niche startups that supply AI margin detection or shade-matching algorithms, deepening ecosystem stickiness.

By End User: Laboratories Retain Scale, Clinics Chase Chairside Speed

Dental laboratories accounted for 42.05% of 2025 revenue, driven by industrial-grade mills, sintering ovens, and technician expertise that enables the fabrication of multi-unit bridges and complex anatomical shading. Laboratories utilize robotic loading and 24-hour shifts to meet next-day delivery windows, often bundling design services so that dentists only need to supply scan images. Yet the dental CAD market is seeing laboratories invest heavily in AI-based nesting and auto-sinter scheduling to guard against chairside encroachment.

Dental clinics and hospitals comprise the fastest-growing end-user segment, growing at a 10.05% CAGR. Chairside systems shorten treatment plans, drive higher patient satisfaction scores, and eliminate freight costs. Margin realization rises once clinics exceed 25-30 crowns a month, prompting high-volume offices to internalize milling and glaze units. University hospitals, meanwhile, leverage in-house CAD suites for research trials, customizing scaffold designs for tissue engineering and producing surgical guides for maxillofacial reconstructions.

By Application: Implants Outpace Crowns in Growth Velocity

Crowns and bridges captured 60.85% of the dental CAD market size in 2025, reflecting the elemental nature of single-tooth restorations in everyday practice. AI libraries now house over 10,000 morphology templates that pair with shade recommendation engines, enabling fresh graduates to produce esthetic crowns on par with veteran ceramists.

Implants, though smaller in absolute revenue, are advancing at an 10.62% CAGR. Planning modules integrate CBCT bone-density heatmaps and nerve-canal visualizations to map safe insertion corridors. Immediate-load cases benefit from mucosa-supported guides 3-D printed overnight, delivering provisional crowns within four hours of surgery. Beyond traditional fixtures, CAD workflows also craft patient-specific zygomatic implants and porous titanium meshes tailored for ridge augmentation, expanding the implants' domain into reconstructive niches.

Geography Analysis

Europe retained 32.20% of the dental CAD market revenue in 2025 thanks to substantial reimbursement, rigorous CE marking discipline, and early adoption of intraoral scanners across Germany, the United Kingdom, and France. CE compliance routines drive continuous software validation cycles, compelling vendors to roll out iterative updates and data-protection safeguards. Consolidation among continental laboratories fosters standardized production pipelines that tap five-axis mills and multi-chamber sintering furnaces, reducing per-unit labor overhead. Aging populations are driving demand for prosthetics higher, solidifying long-term volume growth.

The Asia-Pacific region is the sprint leader, forecasted to grow at an 11.08% CAGR through 2031. China and India are pouring capital into community oral-health clinics, while large private chains are opening implant-focused centers that advertise same-day crowns. Domestic hardware manufacturers now supply mid-range scanners and mills at 20-30% lower price points than European imports, augmenting affordability without sacrificing baseline precision. Governments in Japan and South Korea subsidize AI-driven diagnostic projects, enabling hybrid cloud architectures that comply with stringent patient data localization laws. Training remains a chokepoint, so vendors host certified academies in Bangkok and Shenzhen to accelerate clinician onboarding.

North America presents a mature but still dynamic landscape. DSOs consolidate purchasing power, forcing vendors into national tender contracts that bundle hardware, license seats, and service SLAs. FDA clearances for AI design and diagnostic modules are gathering pace, but reimbursement frameworks are lagging, prompting practices to market CAD crowns as premium elective offerings.Data security compliance under HIPAA and state data breach statutes compels cloud providers to employ zero-knowledge encryption and redundant backups within continental borders. Market focal points have therefore moved from raw adoption to interoperability, uptime, and analytics-rooted ROI metrics.

Competitive Landscape

The dental CAD market exhibits moderate concentration, with the top five suppliers controlling an estimated half of the annual revenue, balancing between legacy manufacturers and AI-centric entrants. Align Technology’s EUR 376 million (USD 435.09 million) acquisition of exocad in February 2025 formed the world’s most comprehensive CAD-CAM ecosystem, combining clear-aligner leadership with laboratory-grade design breadth. Dentsply Sirona doubles down on vertical integration, pairing the Primescan 2 intraoral scanner with DS Core cloud to court DSO chains that prize distributed access control and MAC-agnostic interfaces. 3Shape focuses on open-architecture leadership, courting third-party AI plugins and offering pay-as-you-go design portals for small practices.

Start-ups like VideaHealth, Pearl, and Imagoworks focus on AI diagnostics that integrate into existing workflows, offering immediate chairside caries detection and auto-margin identification. White-space remains in geriatric and pediatric digital solutions, where morphology libraries and occlusion parameters must account for mixed dentition and compromised bone density. Competitive advantage hinges on speed to FDA clearance, dataset size, and the ability to integrate with lab ERP systems via standardized REST APIs. Vendors also compete via educational ecosystems, offering certificate pathways that teach scan capture best practices and AI result validation, thereby fueling downstream hardware demand.

Notably, cloud uptime and cybersecurity credentials now rival spindle RPM and micrometer precision on RFP documents. ANSI/ADA 1110-1:2025 provides a compliance benchmark for AI claims, prompting incumbents to open their algorithms for third-party auditing. Companies that ride this compliance curve early stand to win multinational accounts wary of liability exposure.

Dental CAD Industry Leaders

-

Dentsply Sirona

-

ZimVie Inc.

-

3Shape A/S

-

Align Technology (exocad GmbH)

-

Planmeca Oy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: VideaHealth deepened its partnership with Henry Schein One, embedding AI radiograph analytics into Ascend Academic for 7,000 annual hygiene graduates.

- January 2025: Imagoworks raised USD 17.8 million in Series A funding to hasten US market entry for its AI treatment-planning suite.

Global Dental CAD Market Report Scope

According to the report's scope, dental computer-aided design (CAD) is a field in dentistry and prosthodontics that utilizes CAD to enhance the design and fabrication of dental restorations. CAD technology facilitates the delivery of well-fitting, aesthetically pleasing, and durable prostheses for patients.

The dental CAD market is Segmented by Component (Scanners, Milling Machines, Software, and Other Components), End User (Dental Laboratories, Dental Clinics & Hospitals, and Academic & Research Institutes), Application (Crowns & Bridges, Dentures, Implants, Orthodontic Appliances and Other Applications), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions. The report offers the value (in USD million) for the above segments.

| Scanner |

| Milling Machines |

| Software |

| Other Components |

| Dental Laboratories |

| Dental Clinics & Hospitals |

| Academic & Research Institutes |

| Crowns & Bridges |

| Dentures |

| Implants |

| Orthodontic Appliances |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Scanner | |

| Milling Machines | ||

| Software | ||

| Other Components | ||

| By End User | Dental Laboratories | |

| Dental Clinics & Hospitals | ||

| Academic & Research Institutes | ||

| By Application | Crowns & Bridges | |

| Dentures | ||

| Implants | ||

| Orthodontic Appliances | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value and growth outlook for the dental CAD market?

The dental CAD market is worth USD 3.33 billion in 2026 and is projected to reach USD 4.96 billion by 2031, reflecting an 8.32% CAGR driven by AI automation, chairside workflows, and global DSO consolidation.

Which component leads spending today?

Milling machines dominate revenue with 63.12% share in 2025 because subtractive manufacturing remains essential for zirconia and hybrid ceramic restorations, even as software delivers the fastest growth.

Why are implants the fastest-growing application?

Implants benefit from demographic aging and CBCT-integrated CAD planning that enables micron-level accuracy; the segment is forecast to advance at an 10.62% CAGR through 2031.

Which region has the biggest share in dental CAD market?

In 2025, the Europe accounts for the largest market share in dental CAD market.

How do DSOs shape technology adoption?

DSOs leverage purchasing scale to standardize CAD platforms across multi-state networks, trimming training costs and boosting data analytics while steering vendor roadmaps toward cloud interoperability.

Page last updated on: