Healthcare Contract Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

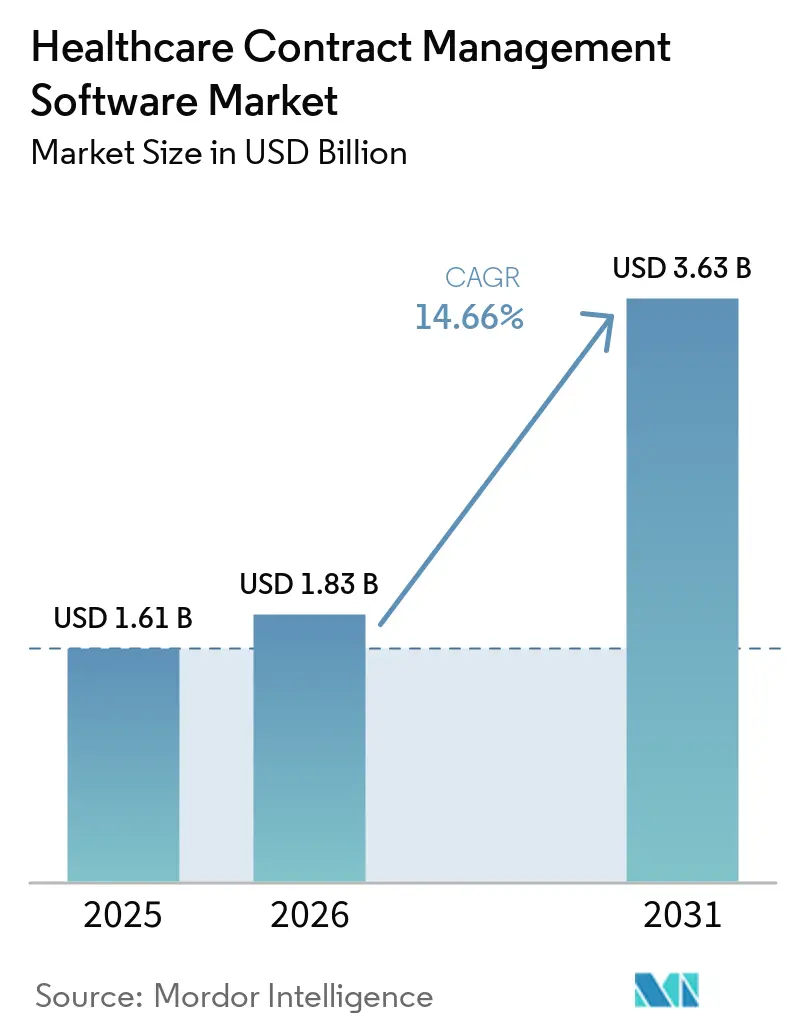

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 14.66% CAGR |

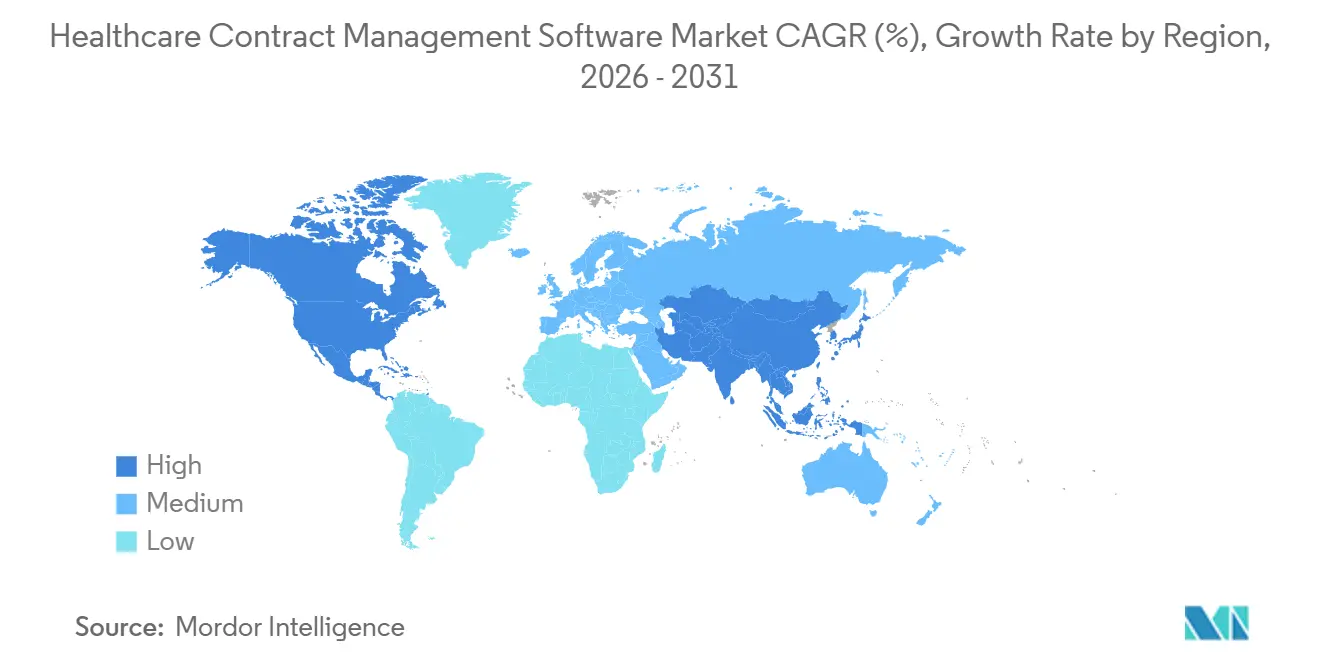

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

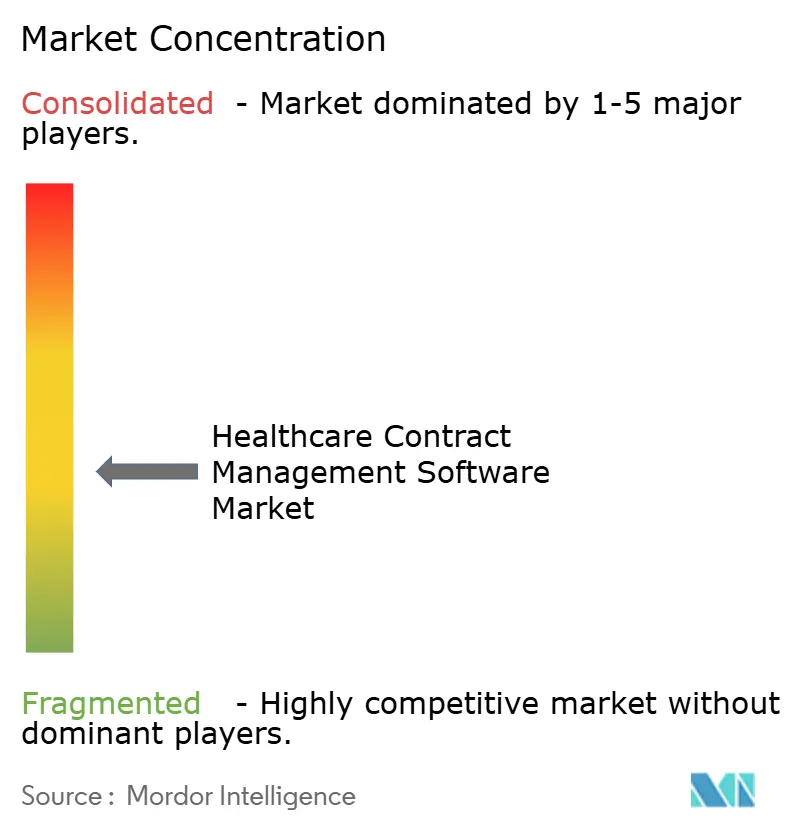

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Contract Management Software Market Analysis by Mordor Intelligence

The healthcare contract management software market size is expected to increase from USD 1.61 billion in 2025 to USD 1.83 billion in 2026 and reach USD 3.63 billion by 2031, growing at a CAGR of 14.66% over 2026-2031. Digitization of healthcare contracting continues to accelerate as providers and payers respond to rising regulatory scrutiny and the need to curb administrative costs, with many teams replacing scattered repositories with centralized, auditable systems that strengthen governance and reduce risk. Cloud-first rollouts and subscription pricing shorten time to value by removing upfront infrastructure spend and expanding access for lean IT teams that need secure, scalable deployment patterns. AI-enabled clause extraction, obligation tracking, and risk scoring compress review cycles and expose revenue leakage in near real time, which elevates analytics from retrospective reporting to proactive decision support. Integration with EHR and ERP systems links contract terms to spend controls and reimbursement logic so that organizations can enforce pricing, reconcile payments, and harden audit trails across complex supply and payer arrangements. Vendors are pushing deeper healthcare-specific capabilities and connected workflows, reflecting how the healthcare contract management software market is becoming a core system of performance and compliance rather than a point tool for document storage.

Key Report Takeaways

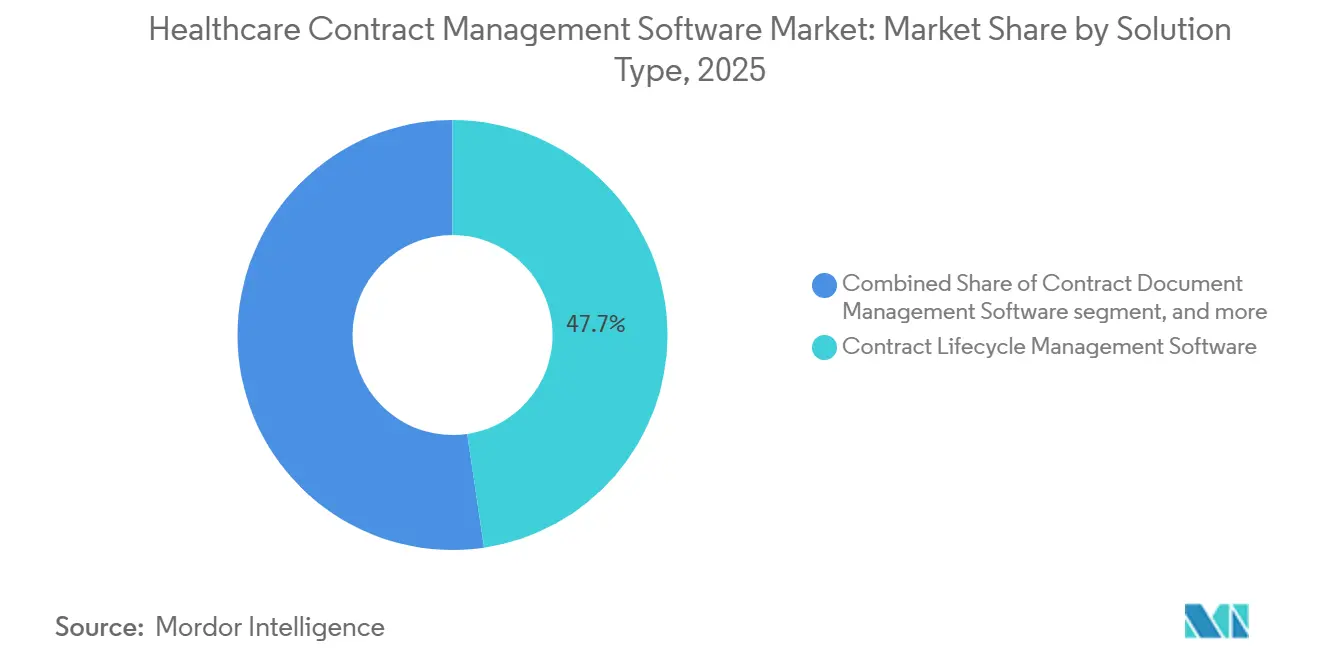

- By solution type, contract lifecycle management software captured 47.66% in 2025, and contract document management software is projected to grow at a 14.74% CAGR through 2031.

- By deployment, cloud-based solutions accounted for 50.48% of revenues in 2025 and are set to expand at a 16.23% CAGR through 2031.

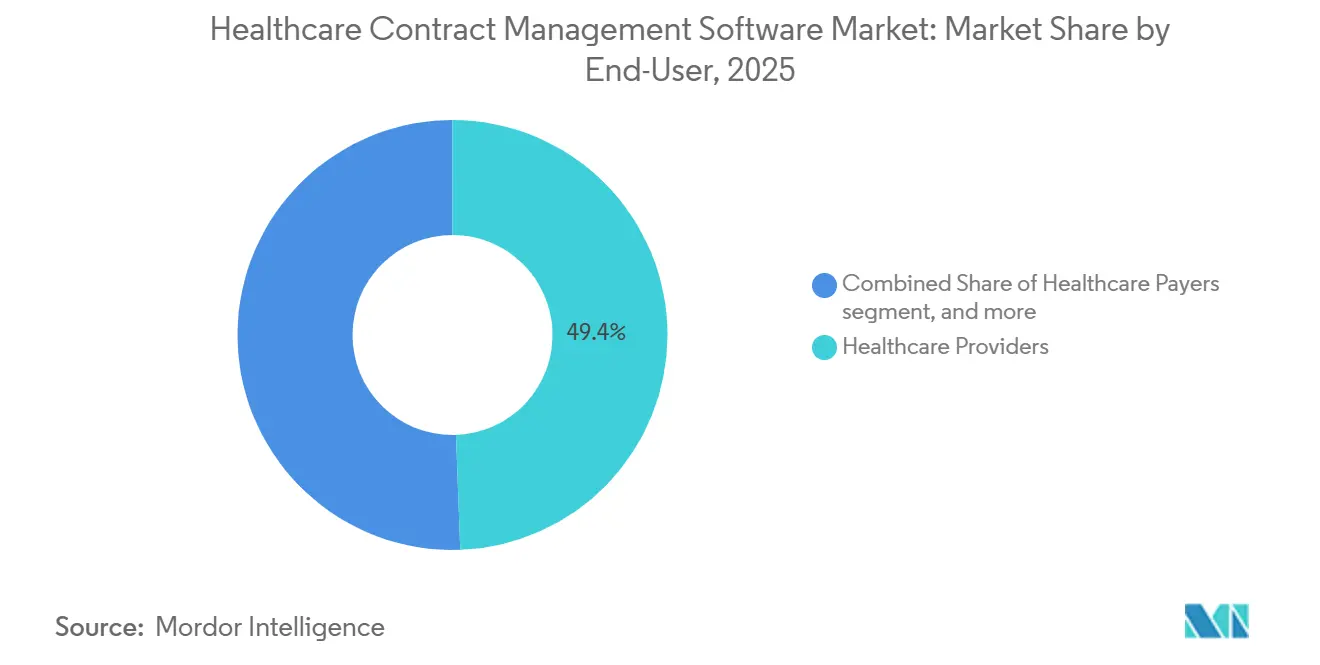

- By end-user, healthcare providers led with 49.43% of 2025 revenues, and healthcare payers are projected to grow at 14.89% CAGR through 2031.

- By organization size, mid-market enterprises commanded 43.70% in 2025, while small enterprises are forecast to rise at 15.44% CAGR to 2031.

- By geography, North America held 45.56% share in 2025, while Asia-Pacific is projected to post the fastest expansion at 15.34% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Contract Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance-First Digitalization In Healthcare (HIPAA/GDPR-Driven CLM Adoption) | +2.8% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Cloud-First Rollouts And Subscription Pricing Ease Deployment & ROI | +3.2% | Global, early gains in North America, rapid uptake in APAC | Short term (≤ 2 years) |

| Operational Efficiency And Cost Containment Imperatives In Providers & Payers | +2.5% | Global, with acute pressure in North America & Europe | Short term (≤ 2 years) |

| AI-Enabled Contract Analytics, Obligation Tracking, And Risk Scoring | +3.0% | North America & EU lead, APAC following | Medium term (2-4 years) |

| Value-Based Care And Payer-Provider Contracting Complexity | +2.0% | North America core, EU exploratory | Long term (≥ 4 years) |

| Procurement–EHR/ERP Integration Linking Contract Terms To Spend & Reimbursement | +1.5% | North America & EU mature, APAC emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Compliance-First Digitalization in Healthcare (HIPAA/GDPR-driven CLM adoption)

Heightened privacy and security oversight keeps pushing organizations to standardize contract governance, with HIPAA requirements elevating the need for executed Business Associate Agreements across cloud providers, EHR vendors, billing services, and other partners to reduce breach exposure.[1]Scott Sbihli, “Building a Responsible Future for AI in Healthcare Contract Management,” symplr, symplr.comAs audit and incident reporting expectations increase, hospitals and payers are phasing out folders, shared drives, and email-driven authoring in favor of centralized repositories with role-based access and immutable audit trails that document every action on sensitive records. Automated compliance checks and renewal alerts help teams surface missing BAAs and outdated clauses before they turn into penalties, which preserves time for higher-value negotiations and reduces the probability of non-compliance during reviews. The same governance pressures apply in other regulated jurisdictions that enforce strict privacy and security standards, which reinforces the case for automated clause libraries, approvals, and evidence capture across the healthcare contract management software market. As system access, identity management, and segregation of duties policies mature, organizations align legal, compliance, procurement, and IT to maintain a single version of truth for contracts and associated obligations, reducing manual handoffs and hidden risk.

Cloud-First Rollouts and Subscription Pricing Ease Deployment & ROI

SaaS platforms remove the need for dedicated hardware, database administration, and disaster recovery buildouts, which helps lean IT teams stand up enterprise-grade CLM with predictable operating spend and faster time to value. Subscription pricing and simplified UX lower barriers for ambulatory clinics and behavioral health organizations, while scalable tenancy and continuous updates keep security baselines current without lengthy patch cycles.[2]HyperStart Editorial Team, “Business Associate Agreement: Complete HIPAA Guide,” HyperStart, hyperstart.com Healthcare teams also benefit from integrated eSignature, workflow routing, and identity services that connect common productivity suites and line-of-business systems to keep negotiations moving and documentation complete.[3]Contract Review Intelligence AI Agent,” Domo, domo.com As decision-makers weigh alternatives, they see that cloud CLM accelerates approvals, enables remote collaboration, and surfaces analytics on cycle times and bottlenecks that were difficult to quantify with on-premises silos. These fundamentals support broader adoption of the healthcare contract management software market among mid-market and small enterprises seeking lower-risk modernization paths.

Operational Efficiency and Cost Containment Imperatives in Providers & Payers

Margin pressure from reimbursement dynamics and denials has pushed health systems to seek measurable productivity gains from contracting automation and analytics, which redirects staff hours from manual tracking to negotiation strategy and performance management. Automated extraction of commercial terms and obligations reduces missed renewals and helps enforce rebates and service credits, which recovers value that often leaks when documents are scattered and untracked. When CLM integrates with ERP, organizations can align pricing and fee schedules to claims and purchasing events, reduce payment errors, and present audit-grade evidence of compliance to internal and external reviewers. Real-time dashboards give leaders transparent views of throughput and risk, and standard clause libraries speed legal review while enhancing consistency across vendor, payer, and provider agreements. These improvements underpin sustainable adoption in the healthcare contract management software market as executive teams look for tools that free capacity and safeguard margins.

AI-Enabled Contract Analytics, Obligation Tracking, and Risk Scoring

Vendors now embed machine learning to extract clause data, compare deviations from playbooks, and surface ranked risks that focus attorney attention where it matters most, improving compliance without slowing deal velocity. Contract intelligence agents answer natural-language questions, track deliverables, and trigger alerts for time-bound commitments so that teams can manage complex portfolios without constant manual reconciliation. Production deployments in healthcare show AI can execute rule checks at high accuracy, cut review time, and reduce per-contract handling costs when agreements contain many conditional clauses.[4]Jamiere Mitchell, “Control Costs Without Cutting Staff: How AI-Powered CLM Boosts Healthcare Margins,” Icertis, icertis.com As these capabilities mature, portfolio-level analytics expose cross-contract patterns in risk and performance that inform negotiations and counterparty management. The healthcare contract management software market increasingly treats AI as an embedded control layer rather than an external add-on, aligning with governance, privacy, and audit needs in regulated settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy IT Integration, Data Migration, And Security Hurdles | -1.2% | Global, acute in mature markets with entrenched EHR systems | Medium term (2-4 years) |

| High Implementation/Customization Costs And Change Management Gaps | -0.9% | Global, pronounced in mid-market and small enterprises | Short term (≤ 2 years) |

| Fragmented Ownership Across Legal, Supply Chain, And Compliance Slows Governance | -0.7% | Global, especially North America & Europe with complex organizational structures | Medium term (2-4 years) |

| Overlap With Revenue-Cycle/Payer Contract Modeling Tools Creates Substitution | -0.5% | North America primarily, emerging in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy IT Integration, Data Migration, and Security Hurdles

Heterogeneous estates that include multiple EHRs, ERPs, and custom revenue-cycle systems complicate data mapping and interface design, which can extend rollouts and create parallel-process burdens during migration. Teams must normalize legacy fields, clean archival repositories, and validate clause metadata to ensure downstream analytics are reliable and auditable at scale. Security certifications such as HITRUST and SOC 2 Type II are often table stakes in healthcare procurement and can disqualify vendors or delay approvals if evidence and controls are not current. Implementation timelines may stretch for organizations with heavy customizations or sovereign data needs, which can slow near-term ROI as staff balance transformation with daily operations. These realities remain a headwind for the healthcare contract management software market when buyers underestimate the effort required to centralize scattered documents and align integrations with clinical, financial, and supply workflows.

High Implementation/Customization Costs and Change Management Gaps

Enterprise deployments touch many functions, which requires project management, training, and governance to standardize templates and approvals across legal, compliance, supply chain, finance, and clinical leadership. Without strong sponsorship and change strategy, teams may resist new steps in authoring or approval flows before automation benefits show up in cycle-time and error-rate metrics. Organizations that budget for configuration, role-based access design, and analytics buildouts see smoother adoption and more durable value capture from the healthcare contract management software market. Clear definitions of ownership and escalation reduce friction and prevent proliferation of off-template agreements that erode consistency. Adequate enablement for attorneys, analysts, and contract managers is necessary to move from document chasing to data-driven governance, which helps teams adopt new workflows with confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Full-Cycle CLM Platforms Anchor Provider Adoption

Contract Lifecycle Management Software held 47.66% in 2025, reflecting demand for end-to-end authoring, negotiation, execution, and obligation management across diverse healthcare agreements. The category’s breadth positions it as the control center for templates, clause libraries, and analytics that legal and commercial teams use to scale consistent governance across providers, payers, and suppliers within the healthcare contract management software market. Contract Document Management Software is projected to grow the fastest at 14.74% CAGR to 2031, in part because many mid-market hospitals prioritize central repositories with AI-powered extraction to consolidate legacy folders and email-based storage into a searchable single source of truth. Vendor and supplier contract management capabilities that connect to ERP and purchasing systems increase value by enforcing catalog pricing and flagging off-contract spend for corrective action that curbs leakage. Compliance-oriented solutions remain essential for BAA management, physician compensation checks against fair-market-value benchmarks, and monitoring of conflicts and attestations at the system level.

"Others" includes AI-driven analytics modules that parse conditional rules and produce payout simulations for value-based arrangements as well as procurement-integrated platforms that feed real-time dashboards for spend governance. Life sciences use cases continue to grow, with large pharma and device companies automating chargebacks and rebates at scale and reporting error-rate reductions that translate into rapid ROI. Contract Logix and other specialists support long-standing pharmaceutical workflows for complex supply agreements and rebate tracking through granular line-item management. DiliTrust’s GxP-focused features and analytics have been associated with cycle-time and cost improvements for European pharma clients, showing how regulated workflows benefit from structured templates and governance. These solution types collectively expand the healthcare contract management software market as buyers match capability depth to their maturity and scope.

By Deployment: Cloud Migration Accelerates Amid EHR Interoperability Push

Cloud-based deployments accounted for 50.48% of 2025 revenues and are growing at a 16.23% CAGR, which reflects a shift to SaaS operating models that ease updates, integration, and security baselines. Teams benefit from elastic scale, managed services, and frequent feature releases that reduce the lifecycle burden on internal IT while expanding access to AI features and eSignature workflows that accelerate contracting in distributed care settings. Cloud adopters also see faster cross-functional collaboration because legal, compliance, and commercial teams route work from a shared system that logs activity and extracts analytics without manual reconciliation. These factors help the healthcare contract management software market broaden reach among providers and payers that need to operationalize VBC and procurement policies through orchestrated workflows.

On-premises and hybrid models remain relevant for organizations with legacy estates, local residency mandates, or extensive customizations, which can extend migration paths. Hybrid approaches help large systems harmonize HR, finance, and supply chain modules with on-site clinical systems to reduce disruption as they modernize contracting and commercial governance. Integration blueprints that reduce identity and access risks, streamline approvals, and centralize audit artifacts remain central to adoption, regardless of hosting choice. Over the forecast period, interoperability requirements and distributed work models are expected to keep cloud-first momentum strong within the healthcare contract management software market as organizations pursue standardization without heavy on-premises overheads.

By End-User: Provider Complexity Drives Uptake, Payer Segments Accelerate

Healthcare providers led with 49.43% of revenues in 2025, reflecting the breadth of agreements they manage across physician services, outsourced functions, facilities, equipment, pharmaceuticals, and research. Providers prioritize systems that enforce standardized templates, track obligations across departments, and integrate with EHR and ERP platforms to align contract terms with care delivery and spend oversight. Examples include operational analytics that surface cycle-time bottlenecks and automation that reduces missed obligations, which supports audit readiness and value-capture from negotiated terms. Health systems also invest in detailed clause libraries and change controls that reduce variation and strengthen governance during expansion and network integration, a pattern that advances the healthcare contract management software market.

Healthcare payers are projected to grow at 14.89% CAGR through 2031 as value-based care, attribution rules, and blended payments introduce operational complexity and financial risk that demand reliable obligation tracking. Payer teams deploy logic that reconciles real-time claims against performance metrics and settlement schedules and use AI to flag deviations before payout cycles close. Case studies also show how centralized platforms reduce reconciliation effort and improve decision speed by consolidating timelines and surfacing next-step recommendations in-line with daily work. These improvements reinforce confidence in the healthcare contract management software market as payers evolve contracting from static documents to executable programs governed by data and policy.

By Organization Size: Mid-Market Leadership Gives Way to Small-Enterprise Surge

Mid-market enterprises held 43.70% in 2025, reflecting demand for healthcare-specific templates, strong integrations, and measurable ROI without long and costly implementation cycles. Vendors emphasize pre-configured workflows, guided setup, and simple pricing that help mid-sized organizations reduce email volume, standardize approvals, and accelerate deployment. Buyers favor platforms that unify eSignature, authoring, and analytics so staff can resolve routine issues quickly while routing complex exceptions to legal teams. These traits have helped vendors build strong mid-market momentum within the healthcare contract management software market as organizations balance capability and speed.

Small enterprises are projected to expand at 15.44% CAGR through 2031 as mobile-first experiences and per-user pricing democratize access to enterprise-grade functionality. Shorter implementation timelines and low-code configuration make it feasible for ambulatory clinics and behavioral health practices to adopt standardized governance without large IT teams. Digital consent, credentialing, and onboarding workflows connected to HR and scheduling platforms streamline operations and reduce administrative burden across small, distributed teams. These trends underpin durable interest in the healthcare contract management software market among smaller buyers that seek predictable costs and simple experiences without sacrificing compliance controls.

Geography Analysis

North America commanded 45.56% in 2025, supported by stringent privacy enforcement, mature EHR adoption, and early movement into value-based models that increase obligation tracking needs. Regulatory emphasis on BAAs and security certifications sustains adoption of centralized repositories, automated controls, and rich audit trails across providers and payers. Contract intelligence tied to payer models helps U.S. organizations interpret complex quality measures and payment structures without slowing claims or reimbursement timelines. Organizations also focus on streamlined eSignature and workflow orchestration to improve throughput and reduce paper-based risk and waste, which supports continued modernization of contracting practices. These factors keep the healthcare contract management software market central to performance and compliance initiatives across integrated delivery networks and regional systems.

Europe shows steady momentum as privacy, security, and interoperability priorities continue to advance digitization agendas at national and enterprise levels. Life sciences and device manufacturers in the region emphasize GxP-aligned controls, audit readiness, and analytics that demonstrate value from standardized clause libraries and governance. Vendors serving regulated industries offer multi-language support and privacy certifications that fit regional requirements, which encourages cross-border deployments and consistent policy execution. eSignature and integrated workflow adoption also expands as organizations streamline agreements with suppliers, research sites, and partners under unified controls. These capabilities strengthen the healthcare contract management software market as European buyers coordinate contracting alongside broader data governance programs.

Asia-Pacific is projected to be the fastest-growing region at 15.3% CAGR through 2031 as health systems pursue digital-first care models and data readiness for analytics and AI. Regional partnerships highlight how provider networks align contracting with connected-care objectives, such as initiatives to co-design AI-enabled workflows and predictive data management for operational readiness. Adoption of eSignature, centralized repositories, and out-of-the-box integrations grows as organizations eliminate manual routing and paper-heavy processes in favor of standardized workflows. As providers and payers scale program participation and digital operations, the healthcare contract management software market gains from demand for secure cloud platforms, structured metadata, and strong analytics to govern diverse agreements.

Competitive Landscape

Enterprise vendors and specialized providers compete across a spectrum of needs, with unified platform players focusing on end-to-end financials, HR, and supply chain alignment and specialists emphasizing rapid deployment, healthcare templates, and targeted analytics. Integrated suites use embedded CLM to manage large portfolios and connect agreements to transactional systems that enforce pricing and payment logic, which appeals to multi-site health systems with complex operations. Specialists differentiate through per-user pricing, guided configuration, and healthcare-native workflows that lower risk for mid-market and small enterprises adopting digital governance for the first time. The breadth of buyers and use cases sustains a dynamic healthcare contract management software market where interoperability, compliance, and analytics strength often outweigh generic features in selection decisions.

AI-enabled capabilities are a key vector of competition as vendors embed drafting assistance, deviation detection, and risk scoring into everyday workflows to increase speed and control. Providers that invest in contract intelligence agents empower staff to query portfolios in natural language, monitor deliverables, and reduce missed obligations without exhaustive manual review. Life sciences and device manufacturers evaluate vendors on support for regulated workflows and analytics that document value from consistent playbooks and global template governance. Companies that can pair AI with transparent controls and strong integrations are well positioned to win in the healthcare contract management software market as buyers demand both speed and auditability.

Ecosystem reach also matters, since customers seek pre-built connections to EHR, ERP, CRM, and identity providers to reduce integration risk and accelerate adoption. Vendors supporting robust eSignature and orchestration can move organizations from document chasing to data-driven governance while maintaining user-friendly experiences across legal and operational teams. Healthcare-focused providers that integrate with Epic, Cerner, Workday, and Oracle close gaps between contract policy and execution, such as ensuring compensation alignment and access deprovisioning as roles change. Case-based evidence from payer implementations that consolidate timelines and reduce reconciliation tasks highlights the value of targeted solutions that fit real-world workflows. These dynamics point to continued innovation and partnership in the healthcare contract management software market as buyers prioritize tangible outcomes and interoperability over generic breadth.

Healthcare Contract Management Software Industry Leaders

Icertis

Agiloft

Oracle

Workday

DocuSign

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Workday announced a multi-year contract with Fairview Health Services, a Minnesota nonprofit health system with 34,000 employees, to modernize HR, finance, and supply chain operations on one AI-powered platform, integrating contract workflows with clinical systems like Epic.

- February 2026: Royal Philips and SingHealth, Singapore’s largest public healthcare cluster, signed a Memorandum of Understanding to co-design AI-integrated imaging workflows, next-generation predictive enterprise data management, and smart-ICU capacity optimization over three years.

- January 2026: Sirion in the 2025 Gartner Magic Quadrant for CLM, received majority investment from Haveli Investments to accelerate AI-native contract lifecycle management capabilities, reinforcing its position managing over 7 million contracts in more than 100 languages.

Global Healthcare Contract Management Software Market Report Scope

According to the report’s scope, Healthcare contract management software refers to digital platforms that help hospitals, clinics, and healthcare organizations create, store, track, and manage contracts across payers, suppliers, service providers, and internal departments. It streamlines contract lifecycles, ensures compliance with regulatory and reimbursement requirements, reduces administrative errors, and improves visibility into obligations, renewals, and financial terms, all within a centralized, audit‑ready system.

The healthcare contract management software market is segmented into solution type, deployment, end-user, organization size, and geography. By solution type, the market is segmented into contract lifecycle management software, contract document management software, vendor & supplier contract management systems, compliance & regulatory contract management systems, and others. By deployment, the market is segmented into cloud-based and on-premises. By end-user, the market is segmented into healthcare providers, healthcare payers, pharmaceuticals & medical devices, and others. By organization size, the market is segmented into large enterprises, mid-market enterprises, and small enterprises. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Contract Lifecycle Management Software |

| Contract Document Management Software |

| Vendor & Supplier Contract Management Systems |

| Compliance & Regulatory Contract Management Systems |

| Others |

| Cloud-Based |

| On-Premises |

| Healthcare Providers |

| Healthcare Payers |

| Pharmaceuticals & Medical Devices |

| Others |

| Large Enterprises |

| Mid-market Enterprises |

| Small Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Contract Lifecycle Management Software | |

| Contract Document Management Software | ||

| Vendor & Supplier Contract Management Systems | ||

| Compliance & Regulatory Contract Management Systems | ||

| Others | ||

| By Deployment | Cloud-Based | |

| On-Premises | ||

| By End-User | Healthcare Providers | |

| Healthcare Payers | ||

| Pharmaceuticals & Medical Devices | ||

| Others | ||

| By Organization Size | Large Enterprises | |

| Mid-market Enterprises | ||

| Small Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected growth for the healthcare contract management software market to 2031?

The healthcare contract management software market is projected to reach USD 3.63 billion by 2031, growing at a 14.66% CAGR from 2026 to 2031 based on the current forecast.

Which deployment model is expected to lead growth in this space?

Cloud-based platforms lead and are forecast to expand at a 16.23% CAGR, supported by faster deployments, simpler updates, and integrated eSignature and workflow capabilities.

Which end-user segment shows the strongest near-term momentum?

Healthcare payers are projected to grow at 14.89% CAGR through 2031 as value-based arrangements drive adoption of systems that translate complex clauses into executable logic.

Which regions present the strongest opportunities through 2031?

Asia-Pacific is expected to post the fastest growth at 15.34% CAGR while North America remains the largest region due to mature EHR adoption and stringent privacy and security governance.

Page last updated on: