United States Dental Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 174.20 Billion |

| Market Size (2026) | USD 183 Billion |

| Market Size (2031) | USD 234.11 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

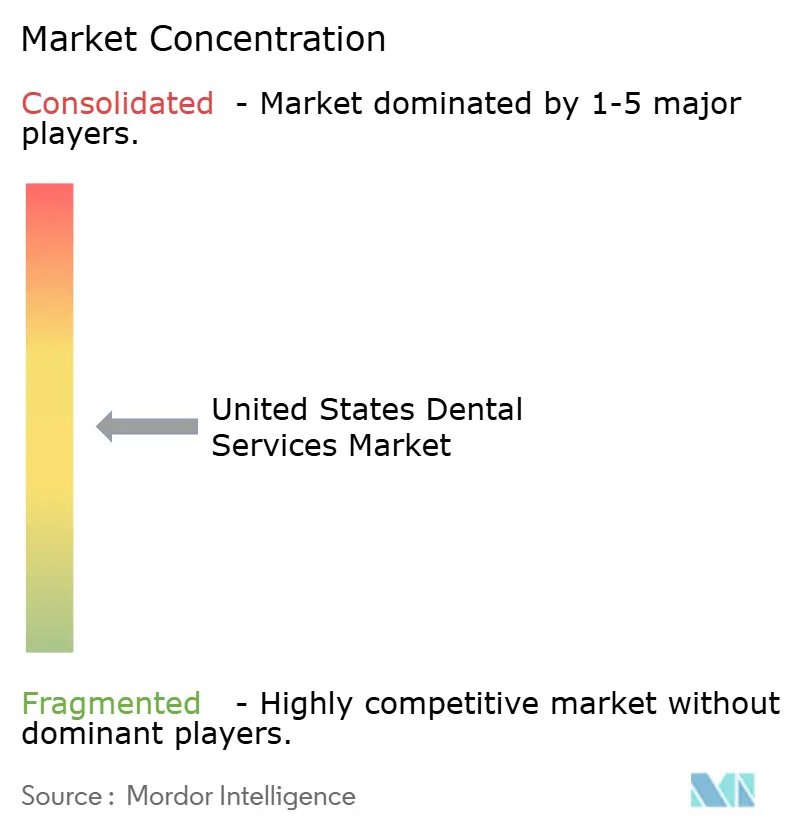

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Dental Services Market Analysis by Mordor Intelligence

The United States dental services market size was valued at USD 174.2 billion in 2025 and estimated to grow from USD 183 billion in 2026 to reach USD 234.11 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031). Consolidation among private-equity-backed dental service organizations (DSOs), the expansion of Medicare Advantage and Medicaid adult dental benefits, and rapid uptake of AI-enabled imaging systems are redefining competitive dynamics and throughput efficiency across the United States dental services market. Provider groups that centralize supply-chain procurement and deploy digital workflows are compressing chair time, lifting case acceptance, and improving labor utilization. At the same time, payer policies that embed routine benefits are pushing utilization higher among seniors and low-income adults, widening the patient funnel. Persistent workforce shortages and inflation-linked input costs temper these tailwinds but disproportionately affect smaller independent practices, reinforcing the scale advantages enjoyed by DSOs.

Key Report Takeaways

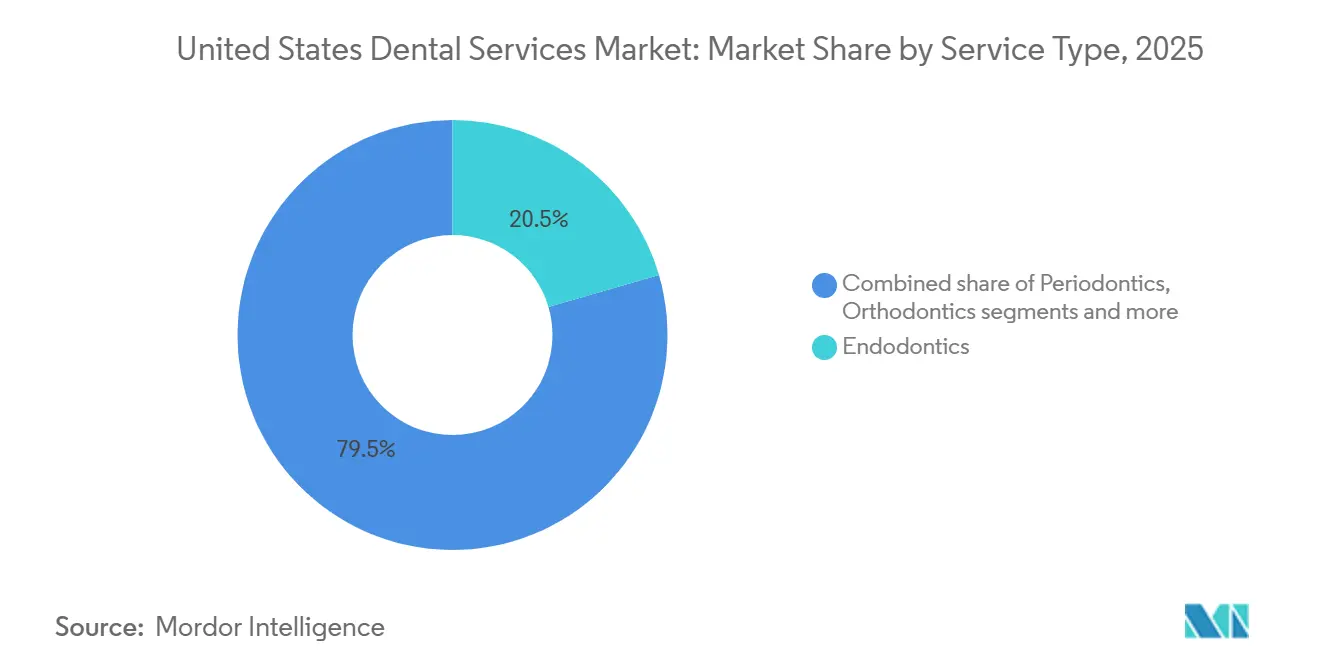

- By service type, endodontics commanded 20.55% of the United States dental services market share in 2025, while orthodontics is projected to register the fastest 6.25% CAGR through 2031, reflecting clear-aligner adoption among adults.

- By patient age group, 18-64-year cohort represented 52.53% of patient volume in 2025; the ≥65-year segment is forecast to expand at 6.35% CAGR, buoyed by near-universal Medicare Advantage dental coverage.

- By provider model, independent solo and group practices held 54.15% share in 2025, but public and federally qualified health center (FQHC) clinics are growing at 10.82% CAGR as Medicaid mandates steer underserved populations toward safety-net providers.

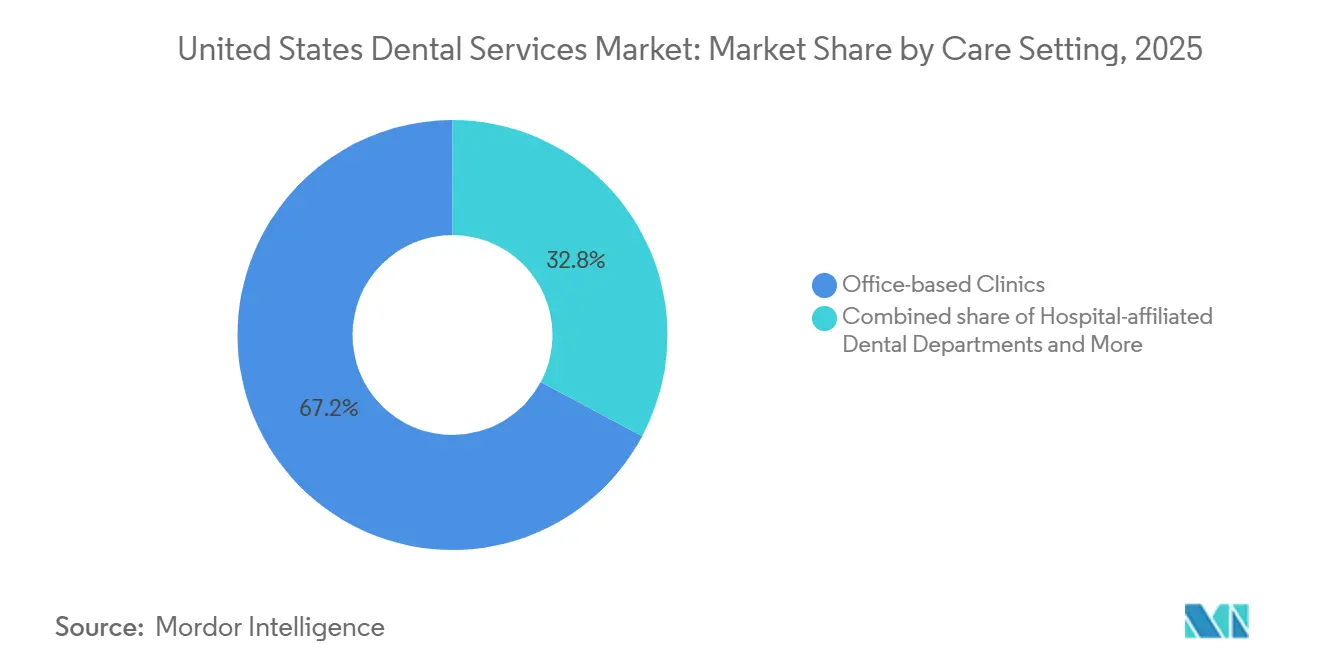

- By care setting, office-based clinics dominated care delivery with a 67.25% share in 2025, yet retail health clinics located inside pharmacies and big-box stores are expanding at 6.56% CAGR on the strength of convenience-oriented preventive visits.

- By payment method, private insurance accounted for 46.65% of payments in 2025, but out-of-pocket spending is advancing at 6.32% CAGR as high-deductible health plans shift cost burdens onto patients and cosmetic procedures remain uncovered.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on dental services market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Dental Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of untreated oral diseases | +0.5% | National, disproportionately affecting low-income and rural communities with limited provider access | Long term (≥ 4 years) |

| Rapid uptake of clear-aligner & digital workflows | +0.9% | National, led by urban and affluent suburban markets with high commercial insurance penetration | Short term (≤ 2 years) |

| Growing DSO penetration & private-equity funding | +1.2% | National, with highest concentration in Sun Belt states and suburban metros | Medium term (2-4 years) |

| Expansion of Medicare Advantage dental benefits | +0.8% | National, with outsized impact in Florida, Arizona, and states with high senior populations | Medium term (2-4 years) |

| AI-driven intra-oral imaging slashing diagnosis time | +0.6% | National, early adoption concentrated in DSO-affiliated practices and academic dental centers | Short term (≤ 2 years) |

| Retail-clinic roll-outs by big-box stores | +0.4% | National, with initial focus on urban and suburban markets near existing pharmacy and retail locations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing DSO Penetration & Private-Equity Funding

DSOs backed by private equity are executing an aggressive roll-up strategy that mirrors the urgent-care playbook, accelerating consolidation across the United States dental services market. Investment exceeded USD 3.5 billion in 2024, spanning 137 add-on deals that pushed DSO affiliation to nearly 13% of all practices. Heartland Dental, Aspen Dental, and Pacific Dental Services collectively manage about 4,000 offices, giving them leverage to negotiate 15-20% supply discounts, deploy enterprise resource-planning systems, and cross-train hygienists for higher chair utilization. These scale economies shave costs that independents cannot match, steering more practices toward affiliation. While regulatory caps on non-dentist ownership in a handful of states slow momentum, analysts estimate 75-80% of practices could be affiliated by 2035. The land-grab concentrates in Sun Belt suburbs where commercial insurance penetration and discretionary spending are strongest, reinforcing regional disparities in competitive intensity.

Rapid Uptake of Clear-Aligner & Digital Workflows

Clear-aligner systems have dismantled aesthetic barriers that historically confined orthodontics to adolescents, catalyzing the fastest-growing service line in the United States dental services market. Align Technology shipped 8% more cases year-over-year in Q4 2024, with adult adoption outpacing teen uptake[1]Align Technology Inc., “Q4 2024 Earnings Release,” aligntech.com. Digital impression scanners rose from 48% to 57% practice penetration between 2023 and 2024, and AI-assisted treatment planning nearly doubled, trimming setup time by up to 40% and enabling same-day simulations. The FDA cleared multiple chairside 3D printers for aligner fabrication, allowing large DSOs to bring production in-house and undercut lab fees by 20-30%. Independent practices that cannot finance on-premise mills face eroding margins unless they partner with laboratories offering rapid turnaround. Over the near term, continued price declines and direct-to-consumer marketing will broaden the addressable base of adults seeking discreet orthodontic correction.

Expansion of Medicare Advantage Dental Benefits

Ninety-nine percent of Medicare Advantage (MA) enrollees had embedded dental coverage by 2025, up from fragmented availability three years prior[2]Centers for Medicare & Medicaid Services, “Medicare Advantage Dental Coverage Landscape 2025,” cms.gov. This benefit expansion is steering seniors back into routine preventive visits and high-value prosthodontic care, lifting utilization among the ≥65 cohort at a 6.35% CAGR. States may add adult dental services to Medicaid essential benefits starting in 2027, potentially channeling millions of low-income adults toward FQHCs and hospital-based clinics. Practices that credential with MA plans are capturing incremental crown, implant, and periodontal maintenance revenue, though reimbursement rates trail commercial plans by 30-40%. The policy shift intensifies competition for chair capacity in retiree destinations such as Florida and Arizona, where seniors already top 20% of the population. Over the medium term, MA insurers are expected to refine risk adjustment models that reward providers who document and manage chronic oral conditions, nudging the market toward value-based contracting.

Rising Burden of Untreated Oral Diseases

Untreated caries affect 21% of adults and half of school-age children, with prevalence doubling among households earning under USD 35,000. Deferred restorations escalate into endodontic or surgical interventions, inflating downstream costs and emergency-department visits estimated at USD 2.7 billion annually. Recent Medicaid expansions in Oregon, Washington, and New York aim to pivot care from acute to preventive settings, but 65% of U.S. counties remain dental health professional shortage areas. Federal grants are funding mobile clinics and school-based sealant programs, yet scope-of-practice limits on dental therapists in 37 states curb workforce elasticity. Over the long term, public-health initiatives and water-fluoridation compliance are expected to reduce disease incidence, but near-term demand for restorative and endodontic procedures will stay elevated, supporting revenue growth across the United States dental services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost & limited cosmetic coverage | -0.5% | National, disproportionately affecting middle-income households without comprehensive dental insurance | Short term (≤ 2 years) |

| Staffing shortages of hygienists & assistants | -0.7% | National, most acute in rural areas and secondary metros with limited training programs | Medium term (2-4 years) |

| Inflation-linked surge in lab & consumable input prices | -0.6% | National, affecting all practice types with greatest margin pressure on independent operators | Short term (≤ 2 years) |

| State-level scope-of-practice caps on mid-level providers | -0.4% | Concentrated in 37 states that prohibit or restrict dental therapist practice, limiting workforce expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Staffing Shortages of Hygienists & Assistants

Roughly 225,000 hygienists were employed in 2024, yet vacancy rates hover near 15% in many metros, driving median wages to USD 87,530 and squeezing margins for smaller offices[3]U.S. Bureau of Labor Statistics, “Occupational Outlook for Dental Hygienists and Assistants 2025,” bls.gov. Dental assistants show similar churn, with turnover topping 20% as physically demanding roles push workers toward better-paying allied-health positions. Temporary staffing agencies charge 30-50% premiums, inflating operating costs. DSOs blunt the impact through centralized recruiting and cross-training that allows assistants expanded duties under supervision, whereas independent practices must curtail hours or delay new-patient appointments. In rural counties, unfilled roles translate directly into reduced access, widening the urban-rural care gap that already plagues the United States dental services market.

High Procedure Cost & Limited Cosmetic Coverage

Dental inflation outpaced the broader consumer price index at 3-4% annually in 2024-2025, fueled by 5-7% jumps in zirconia and ceramic inputs. Out-of-pocket spending averaged USD 1,514 per adult in 2023, and 13% cited cost as a care barrier, the highest among all health services. Employer plans typically cap annual benefits at USD 2,000, forcing patients to shoulder 30-50% of major procedures. High-deductible health plans, now covering 88% of insured workers, exacerbate the burden, nudging providers to offer membership plans and point-of-sale financing. Cosmetic services remain almost entirely cash-pay, creating a bifurcated demand curve where affluent households pursue whitening, veneers, and smile makeovers while lower-income cohorts defer even medically necessary restorations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Endodontics Leads, Orthodontics Surges

Endodontics held 20.55% of revenue in 2025, the highest of any category within the United States dental services market. Bioceramic sealers, cone-beam computed tomography, and AI-guided file systems have lifted success rates and cut chair time, spurring retreatment demand among aging root-canal cases. At the same time, orthodontics is logging a 6.25% CAGR through 2031, fueled by adult uptake of clear aligners that bypass the stigma of metal brackets. Align Technology’s 2024 shipments underscore this momentum, and FDA clearance of office-based 3D printers further trims unit cost. As aligner platforms extend to younger teens, orthodontics is positioned to erode fixed-appliance share steadily, reinforcing its status as the fastest-growing service type.

Restorative dentistry remains the procedural backbone of the United States dental services market, yet reimbursement lags material inflation, pressuring margins. Periodontics benefits from growing recognition of the oral-systemic health link, with cardiologists and endocrinologists flagging periodontal inflammation as a modifiable risk factor. Prosthodontics is migrating from removable dentures toward implant-retained overdentures as seniors prioritize lifestyle quality, a shift amplified by declining implant prices amid competitive manufacturer entry. Preventive and diagnostic services underpin revenue stability but require upsell to higher-margin categories to offset stagnant fee schedules. Cosmetic treatments cater to discretionary demand concentrated in affluent zip codes, adding episodic revenue spikes during economic upswings.

By Patient Age Group: Working-Age Dominates, Seniors Accelerate

Working-age adults (18-64) generated 52.53% of patient volume in 2025, underpinned by employer-sponsored insurance and discretionary spending on restorative, orthodontic, and cosmetic care. Utilization peaks in the 35-54 bracket, when cumulative wear intersects with disposable income, supporting high revenue per visit. Yet the ≥65 cohort is the fastest-growing at 6.35% CAGR, reflecting demographic aging and embedded Medicare Advantage dental benefits. The United States dental services market size for seniors is projected to expand robustly as the population aged ≥65 swells toward 73 million by 2030.

Child and adolescent care hinges on insurance coverage and provider availability. Although sealants and early orthodontic assessments reduce future disease burden, Medicaid-enrolled children still encounter limited access in low-reimbursement markets. Mobile FQHC clinics and school-based programs partly bridge this gap, but provider shortages in rural counties persist. The working-age segment will stay the volume anchor, yet revenue growth potential skews toward seniors given their higher incidence of complex restorative and prosthodontic needs.

By Provider Model: Independence Erodes, FQHCs Surge

Independent solo and group practices controlled 54.15% of revenue in 2025, but their share is slipping as DSOs accelerate acquisitions and FQHCs widen service footprints. Heartland Dental alone opened 105 offices in 2024, leveraging centralized procurement to keep supply costs 15-20% below independent averages. Meanwhile, FQHCs are clocking a 10.82% CAGR through 2031, buoyed by federal grants that subsidize low Medicaid reimbursement. The United States dental services market size attributed to public clinics is therefore rising faster than the overall market, reflecting policy-driven patient redirection.

DSOs cluster in suburbs where commercial insurance penetration supports premium fee schedules, while independents linger in Medicaid-heavy rural and urban pockets. Corporate practice of dentistry restrictions in states like California temper the pace of roll-up, but workarounds such as management-service organizations still enable capital inflow. Ultimately, independents must choose between affiliation for capital access or a niche strategy grounded in community relationships and personalized care.

By Care Setting: Office-Based Prevails, Retail Clinics Emerge

Office-based practices captured 67.25% of the United States dental services market share in 2025, thanks to comprehensive service menus and equipment capable of complex procedures. Hospital-based departments focus on medically complex cases requiring anesthesia or multidisciplinary oversight, serving a vital yet narrow role. Retail clinics embedded in pharmacies and big-box stores are expanding fastest at 6.56% CAGR, capitalizing on convenience, transparent pricing, and extended hours.

These retail outlets handle preventive cleanings and simple restorations, freeing chair capacity in traditional offices for higher-acuity work. However, scope limitations prevent on-site surgical interventions, so referral networks remain essential. As consumer expectations tilt toward same-day service and price transparency, hybrid models that blend retail front-ends with back-office specialty hubs could emerge, further fragmenting the care-setting landscape across the United States dental services market.

By Payment Method: Private Insurance Leads, Out-of-Pocket Surges

Private insurance funded 46.65% of spending in 2025, propelled by employer plans covering 100% of preventive care. Yet out-of-pocket payments are growing at 6.32% CAGR—the quickest among all channels—because high-deductible plan adoption shifts first-dollar responsibility to patients and cosmetic procedures remain largely uncovered. The United States dental services market size tied to self-pay therefore expands faster than the insured base, particularly in elective cosmetic and orthodontic segments.

Public insurance penetration is set to climb as Medicaid adult dental becomes an essential benefit in 2027. Reimbursement gaps remain stark, but FQHC cost-base subsidies close part of the margin deficit. Practices increasingly advertise membership plans at USD 300-500 annually to stabilize cash flow and cultivate loyalty, while third-party lenders extend treatment affordability for credit-worthy patients at the expense of finance charges.

Geography Analysis

Regional performance within the United States dental services market diverges sharply. Sun Belt states such as Florida, Texas, and Arizona experience the fastest expansion, buoyed by senior migration, Medicare Advantage uptake, and regulatory climates conducive to DSO growth. Counties like Sarasota and Maricopa now count seniors as more than 20% of residents, boosting demand for prosthodontic and periodontal maintenance. Conversely, Rust Belt and Appalachian regions struggle with dentist-to-population ratios below 1:5,000, classifying more than 65% of counties as dental health professional shortage areas. FQHC investments in mobile units and tele-dentistry partially offset gaps, yet travel distances and limited chair capacity keep unmet need high.

Coastal metros—New York, Los Angeles, Boston—boast dense provider networks but fierce competition and elevated overheads. DSOs often bypass urban cores for adjacent suburbs where real-estate costs are lower and parking plentiful, allowing extended hours that resonate with working professionals. Regulatory variation also shapes growth. Minnesota, Maine, and Alaska authorize dental therapists, expanding reach in rural villages, while most states still restrict mid-level providers, limiting scalability. Medicaid expansion status further widens geographic disparities, with non-expansion states like Texas shouldering larger uninsured populations and higher emergency-department dental visits.

In the Midwest, employer concentration in manufacturing has historically offered robust dental benefits, but plant closures have eroded coverage, shifting patients into self-pay or Medicaid categories. Western mountain states, including Colorado and Utah, attract young, affluent populations keen on cosmetic and preventive services, spurring boutique practices and aligner-focused startups. Overall, the United States dental services market exhibits a mosaic of hyper-competitive suburbs, underserved rural interiors, and policy-driven safety-net clusters, demanding location-specific strategies from stakeholders.

Competitive Landscape

The competitive fabric of the United States dental services market is weaving from fragmentation toward an oligopoly. Heartland Dental, Aspen Dental, and Pacific Dental Services now manage roughly 4,000 combined locations. Their centralized procurement alone yields 15-20% consumables savings. In 2024, Heartland partnered with VideaHealth to roll out AI radiograph analysis across its network, cutting diagnosis time and uplifting case acceptance. Aspen Dental integrated connected toothbrush data from Philips Sonicare into patient portals, reinforcing preventive compliance and recall scheduling.

MB2 Dental secured a USD 2.34 billion debt facility to finance additional roll-ups, underscoring investor confidence in dental’s recurring cash-flow profile. Tele-dentistry platforms are nibbling at orthodontic monitoring and second opinions, but state licensure rules limit full virtual care. White-space opportunity persists in rural counties where DSOs lack scale incentives; FQHCs partially fill this gap, yet funding cycles and workforce shortages constrain expansion. Independent practices retain competitive relevance by emphasizing personalized service, continuity of care, and community ties, though rising labor and supply costs challenge capital reinvestment.

Looking ahead, technology partnerships will define winners. DSOs able to standardize AI imaging, chairside milling, and cloud-based practice management will widen efficiency moats. Corporate practice statutes may slow the pace in states like California, yet management-service-organization structures offer legal avenues for continued consolidation. The race for talent looms large; entities that offer tuition reimbursement, career ladders, and flexible scheduling will attract scarce hygienists and assistants, solidifying operational resilience.

United States Dental Services Industry Leaders

Aspen Dental Management, Inc.

Dental Care Alliance

Great Expressions Dental Centers

Pacific Dental Services

Smile Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The National Association of Community Health Centers and the National Network for Oral Health Access formed a strategic alliance to integrate comprehensive oral health services within Community Health Centers.

- July 2025: Sunstar Americas and Dentistry.One unveiled GUM Virtual Care, an AI-powered platform offering 24/7 virtual consultations and oral-health scans nationwide.

United States Dental Services Market Report Scope

As per the scope of the report, dental services refer to several treatment options to maintain oral health and manage several dental disorders, including cavities, tooth loss, and gum disease.

The segmentation for the United States dental services market is categorized by service type, patient age group, provider model, care setting, and payment method. By service type, it includes preventive and diagnostic services, restorative services (fillings, crowns, bridges), periodontic treatments, endodontic procedures, orthodontic services (braces, clear aligners), prosthodontic services (dentures, implants), and cosmetic dental services. By patient age group, it is segmented into ≤17 years, 18-64 years, and ≥65 years. By provider model, it includes independent solo/group practices, dental service organizations (DSOs), and public/FQHC clinics. By care setting, it is divided into office-based dental clinics, hospital-affiliated dental departments, and retail health clinics. By payment method, it includes private insurance, public insurance, and out-of-pocket payments. For each segment, the market sizing and forecasts have been done based on value (USD).

| Preventive & Diagnostic |

| Restorative (Fillings, Crowns, Bridges) |

| Periodontics |

| Endodontics |

| Orthodontics (Braces, Clear Aligners) |

| Prosthodontics (Dentures, Implants) |

| Cosmetic Dentistry |

| ≤17 Years |

| 18-64 Years |

| ≥65 Years |

| Independent Solo / Group Practices |

| Dental Service Organizations (DSOs) |

| Public / FQHC Clinics |

| Office-based Dental Clinics |

| Hospital-affiliated Dental Departments |

| Retail Health Clinics |

| Private Insurance |

| Public Insurance |

| Out-of-Pocket |

| By Service Type | Preventive & Diagnostic |

| Restorative (Fillings, Crowns, Bridges) | |

| Periodontics | |

| Endodontics | |

| Orthodontics (Braces, Clear Aligners) | |

| Prosthodontics (Dentures, Implants) | |

| Cosmetic Dentistry | |

| By Patient Age Group | ≤17 Years |

| 18-64 Years | |

| ≥65 Years | |

| By Provider Model | Independent Solo / Group Practices |

| Dental Service Organizations (DSOs) | |

| Public / FQHC Clinics | |

| By Care Setting | Office-based Dental Clinics |

| Hospital-affiliated Dental Departments | |

| Retail Health Clinics | |

| By Payment Method | Private Insurance |

| Public Insurance | |

| Out-of-Pocket |

Key Questions Answered in the Report

How fast is demand for clear aligners growing in the United States dental services market?

Orthodontics, powered chiefly by clear aligners, is advancing at a 6.25% CAGR through 2031, the fastest pace of any service line.

What share of dental spending comes from out-of-pocket payments?

Out-of-pocket payments accounted for 46.65% in 2025 and are rising at 6.32% CAGR as high-deductible plans shift more costs to patients.

Which provider model is expanding most quickly?

Public and FQHC clinics are growing at 10.82% CAGR, the highest among provider types, supported by federal grants and Medicaid expansions.

Why are DSOs focusing on Sun Belt states?

These states combine high senior migration, favorable regulations, and dense commercially insured populations, delivering attractive margins for consolidated groups.

How are staffing shortages impacting practice operations?

Hygienist and assistant vacancies nearing 15% force many offices to reduce hours or rely on costly temp agencies, squeezing smaller practice margins.

What is driving senior utilization growth?

Near-universal Medicare Advantage dental benefits and demographic aging are lifting senior patient volumes at a 6.35% CAGR through 2031.

Page last updated on: