U.S. Dental Practice Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

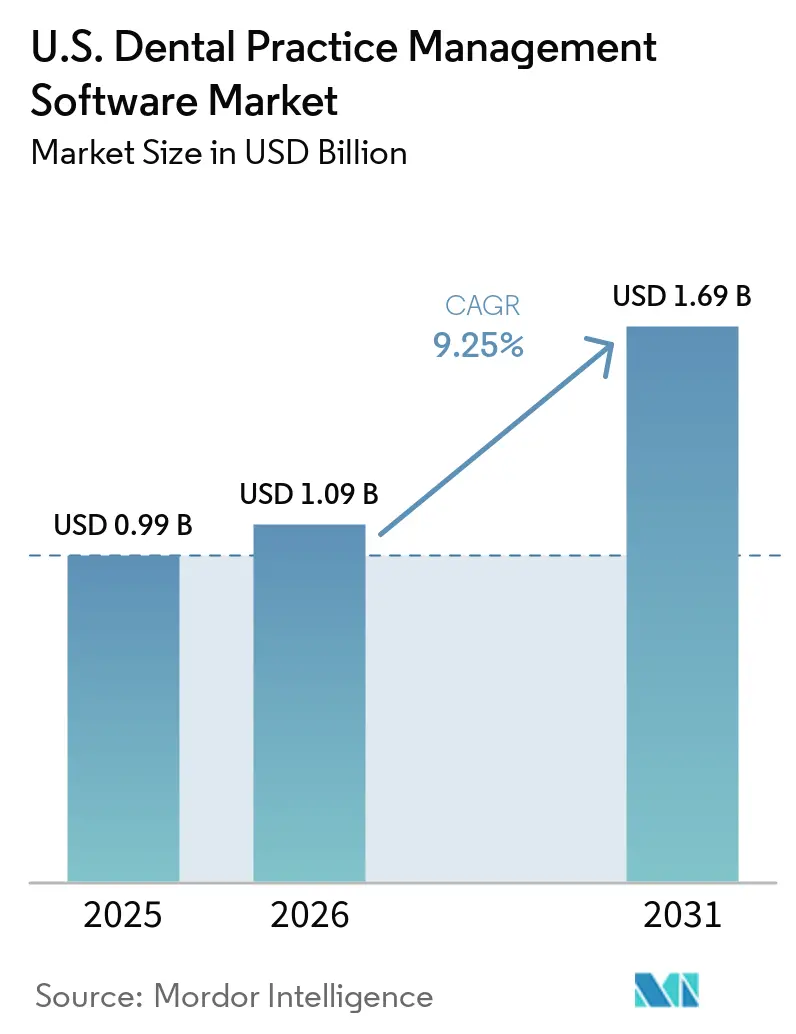

| Base Year Market Size (2025) | USD 0.99 Billion |

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Dental Practice Management Software Market Analysis by Mordor Intelligence

The U.S. Dental Practice Management Software Market size is projected to be USD 0.99 billion in 2025, USD 1.09 billion in 2026, and reach USD 1.69 billion by 2031, growing at a CAGR of 9.25% from 2026 to 2031.

The shift toward digital dental care delivery is accelerating, with practices under pressure to manage claims, scheduling, treatment records, billing, and patient communication through advanced workflows that surpass the capabilities of older systems. In 2025, 23.3% of dentists in the United States invested in new practice management software, exceeding the 20.3% initially planned, despite high overhead and reimbursement pressures.[1]American Dental Association Health Policy Institute, “State of the U.S. Dental Economy Q4 2025,” American Dental Association, ada.org Growth is becoming more concentrated, with DSO-affiliated dentists showing stronger software investment intentions for 2026 compared to non-DSO dentists. This indicates that near-term expansion in the United States dental practice management software market is primarily driven by organized groups, vendor-led migrations, and standardized rollouts, rather than widespread replacement demand among independent clinics.

Key Report Takeaways

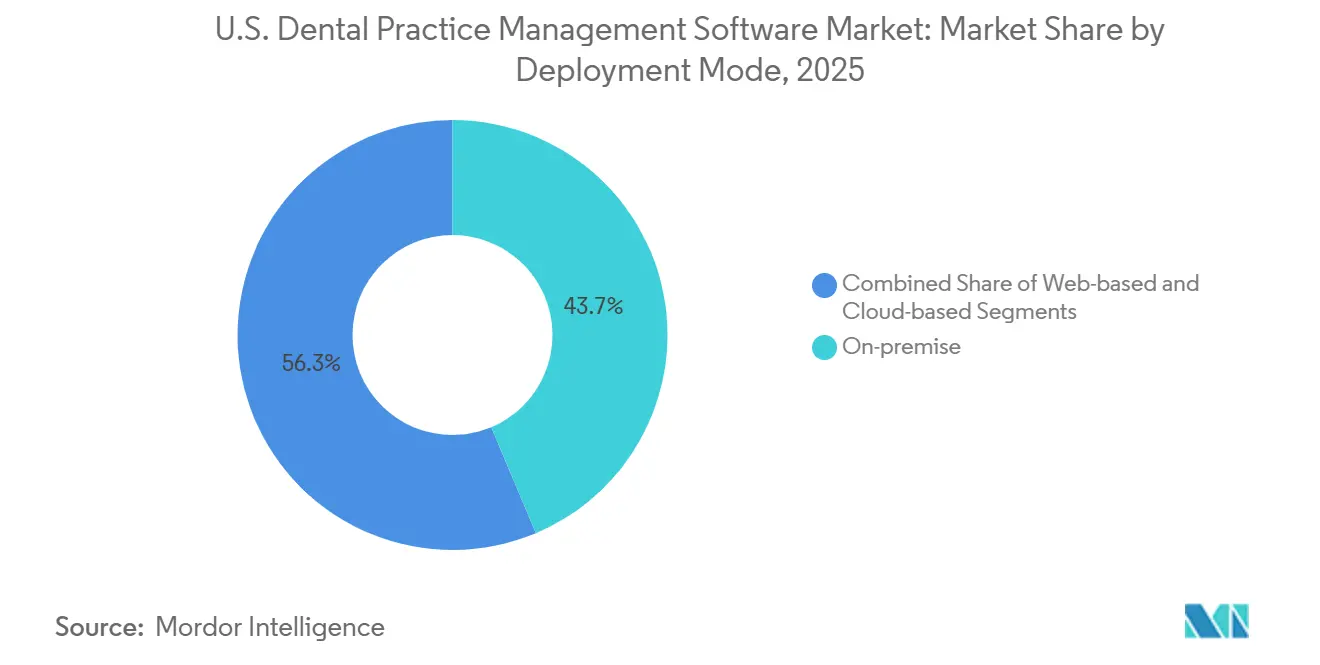

- By deployment mode, on-premise systems held 43.65% of revenue in 2025, while cloud-based deployment is projected to expand at an 11.95% CAGR through 2031.

- By subscription model, subscription and SaaS arrangements captured 59.76% of revenue in 2025 and are projected to grow at a 10.25% CAGR through 2031.

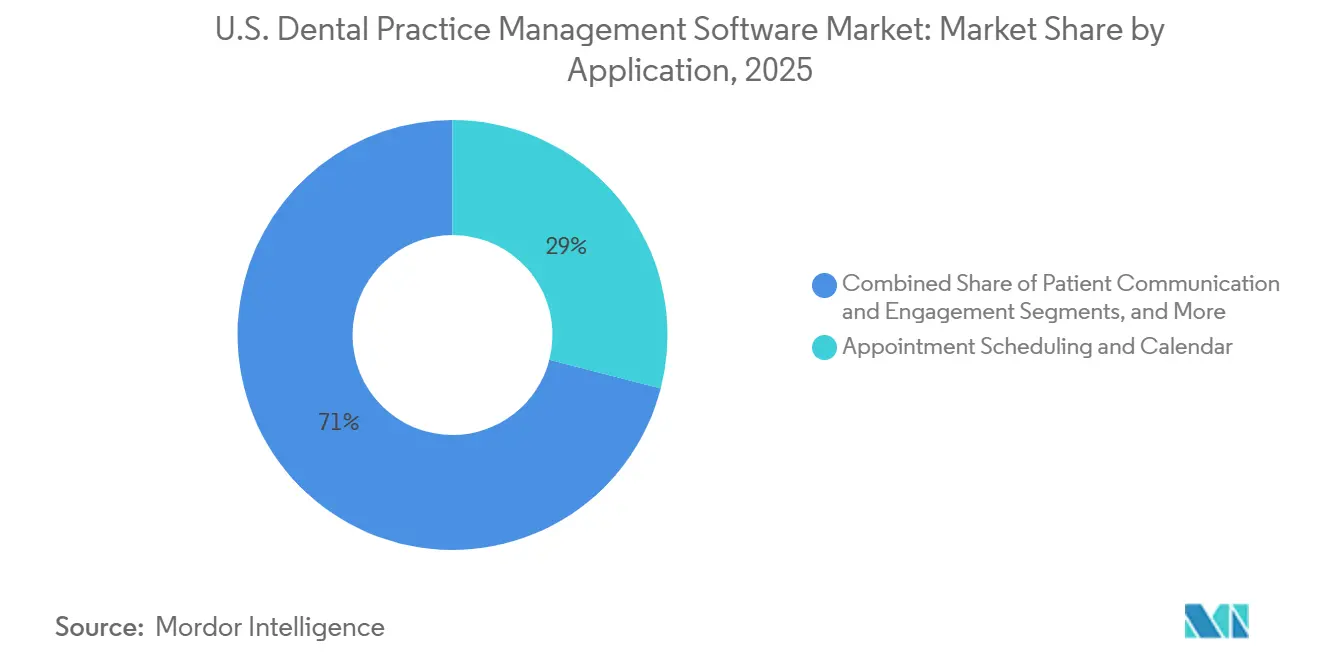

- By application, appointment scheduling and calendar tools accounted for 28.99% of revenue in 2025, while analytics and business intelligence is projected to record the fastest 12.75% CAGR through 2031.

- By end-user, dental clinics held 82.35% of revenue in 2025, while hospitals and specialty dental centers are expected to grow fastest at a 10.10% CAGR through 2031.

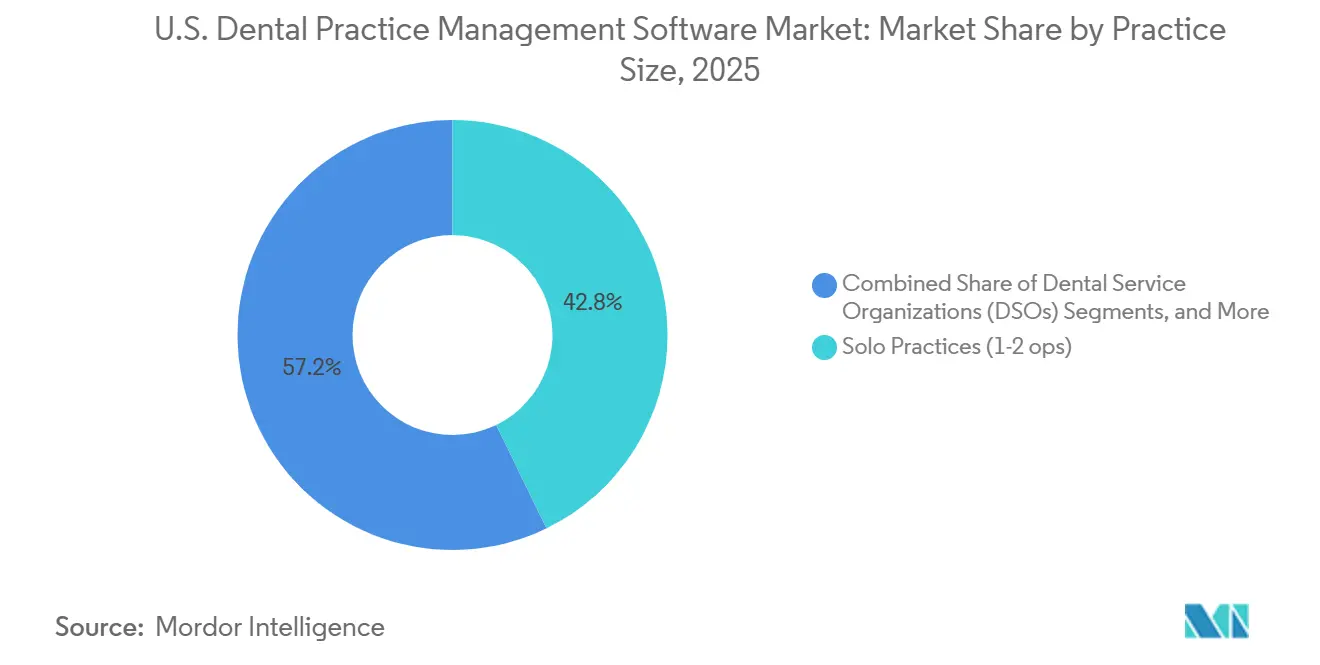

- By practice size, solo practices represented 42.76% of revenue in 2025, while DSOs are projected to expand at a 12.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Dental Practice Management Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cloud migration from server-based to browser and cloud platforms | +2.0% | National, with early gains in Sun Belt and Pacific Coast DSO corridors | Short term (≤ 2 years) |

| DSO standardization and multi-location visibility requirements | +1.8% | National, with highest velocity in Sun Belt and Mid-Atlantic acquisition markets | Short term (≤ 2 years) |

| AI-enabled verification, analytics, and workflow automation | +1.5% | National, concentrated in enterprise DSO and multi-location group practices | Medium term (2-4 years) |

| Revenue-cycle optimization under reimbursement pressures | +1.3% | National, particularly acute in states with constrained payer mix and fee-for-service shifts | Medium term (2-4 years) |

| Medical-dental data exchange needs for medical cross-billing | +0.8% | National, with early adoption in specialty dental and hospital-based dental segments | Long term (≥ 4 years) |

| Tech-stack standardization as a DSO valuation lever in M&A | +0.7% | National, concentrated in PE-backed DSO platforms targeting recapitalization | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud Migration from Server-Based to Browser and Cloud Platforms

Cloud migration from traditional server setups to cloud-based platforms is transforming software purchasing in the United States dental practice management software market. Organizations using modern cloud PMS infrastructure report a 40-55% drop in IT support tickets, an hour less weekly system downtime, and 83% fewer critical IT incidents. Legacy server setups can cost dental organizations 8-12% of annual revenue due to disconnected systems, outdated hardware, and IT inconsistencies. Cloud vendors are gaining traction by simplifying updates, standardizing workflows, and reducing technical reliance, especially for multi-site groups requiring centralized operations.

DSO Standardization and Multi-Location Platform Visibility

DSO standardization is driving repeated migrations in the United States dental practice management software market. Data shows 29% of DSO-affiliated dentists plan to invest in new software in 2026, compared to 16.3% of non-DSO dentists. Planet DDS supported 14,500 practices by 2025, expanding its presence in 100+-location DSOs through partnerships with Sage Dental, Coast Dental, Altius Dental, and Choice Healthcare.[2]Planet DDS, “2026 Dental Industry Outlook,” Planet DDS, planetdds.com Preferred platforms enable DSOs to consolidate operations, offering unified views of collections, utilization, and provider performance, creating a concentrated growth path for enterprise vendors.

AI-Enabled Verification, Analytics, and Workflow Automation

AI is becoming integral to the United States dental practice management software market, enhancing daily administrative and clinical tasks. Henry Schein One reported 191 million eligibility checks and 22 million AI-assisted digital forms processed in 2025.[3]Henry Schein One, “Henry Schein One Unveils the Next Era of Dentrix Ascend for DSOs and Growth-Focused Practices,” Business Wire, businesswire.com Pearl’s integration with Dentrix Ascend in 2026 introduced FDA-approved radiograph analysis directly into workflows, eliminating adoption barriers. Planet DDS noted 60% of practices use AI for insurance verification and claims processing, reducing administrative errors by 30%. Bundling AI tools in subscription packages is boosting adoption and recurring revenue.

Revenue-Cycle Optimization Under Reimbursement Pressures

Revenue-cycle optimization is a key driver for system upgrades in the United States dental practice management software market. From 2023 to 2025, revenue-cycle management integration with dental EHR systems increased by 40%, improving billing accuracy and claim throughput. RCM optimization can recover up to 3% of annual production lost to write-offs and under-collections. With 35% of dentists planning to exit some insurance networks in 2026, demand is rising for integrated solutions that streamline eligibility checks, claims management, and patient financing.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data privacy, HIPAA, and right-of-access compliance costs | -1.5% | National, most acute for solo and small-group practices without dedicated IT compliance resources | Short term (≤ 2 years) |

| Legacy data migration, retraining, and workflow disruption | -1.2% | National, most pronounced in Midwest and Mid-Atlantic markets with high on-premise installed base | Short term (≤ 2 years) |

| Fragmented interoperability with medical records systems | -0.8% | National, concentrated in colocated medical-dental and community health center settings | Long term (≥ 4 years) |

| Small-practice ROI friction and subscription fatigue | -0.6% | National, most acute in solo (1-2 ops) and small-group (3-9 ops) practice tiers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy, HIPAA, and Right-of-Access Compliance Costs

Data privacy and compliance costs remain a significant barrier to adoption in the United States dental practice management software market, particularly for solo and small-group practices without dedicated IT or compliance teams. Older systems often require additional investments in encryption, access controls, audit logs, and workflow adjustments to securely handle sensitive patient and claims data. Large DSOs can distribute these costs across multiple sites, while independent offices must absorb them within smaller revenue bases. A single healthcare data breach averages USD 10.93 million, keeping cybersecurity a top priority for dental organizations. Compliance pressures drive long-term replacement demand but delay near-term purchases for budget-constrained practices.

Legacy Data Migration, Retraining, and Workflow Disruption

Legacy data migration slows adoption in the United States dental practice management software market, as system changes impact patient histories, imaging files, claims records, and more. These transitions affect front-desk, clinical, and back-office workflows, creating challenges for practices reliant on uninterrupted operations. DSO-affiliated dentists are more willing to invest in new software than independent practitioners, as larger groups can better manage temporary disruptions. Consequently, growth in this market is primarily driven by organized groups and vendor-led migrations rather than independent practice replacements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Acceleration Displacing Entrenched Server Installs

In 2025, on-premise systems accounted for 43.65% of the United States dental practice management software market, reflecting their entrenched presence rather than future demand for server architecture. Cloud deployments are projected to grow at an 11.95% CAGR through 2031, outpacing the overall market. Practices and DSOs prefer cloud models for reduced server maintenance, simplified remote access, and integrated workflows. Organizations adopting cloud PMS environments report fewer IT incidents, supporting the operational benefits of migration.

While on-premise systems will decline gradually, enterprise rollouts increasingly favor cloud solutions for streamlined onboarding and consistent workflows. In 2025, major additions like Sage Dental (140 locations) and Coast Dental (88 locations) highlighted the scale of cloud conversions. Web-based systems occupy a shrinking middle ground as buyers commit to full cloud platforms or retain older setups. Over the forecast period, replacement cycles and uptime needs will drive demand toward cloud-first platforms.

By Subscription Model: SaaS Entrenchment Reinforces Per-Practice Revenue Growth

Subscription and SaaS models captured 59.76% of 2025 revenue in the United States dental practice management software market, with a projected 10.25% CAGR through 2031. Vendors now bundle updates, analytics, and AI tools into recurring plans, as seen in Henry Schein One’s 2026 launch of Dentrix Ascend packages. Subscription plans reduce upfront costs for practices and increase lifetime contract value for vendors by layering additional features over time. SaaS models also enable steady delivery of updates and new functionalities, making them the primary revenue model.

By Application: Scheduling Anchors the Platform While Analytics Drives Up-Market Revenue

Appointment scheduling tools held a 28.99% revenue share in 2025, emphasizing their role in daily operations like chair-time management and front-office efficiency. Analytics and business intelligence, projected to grow at a 12.75% CAGR through 2031, are becoming critical for DSOs seeking real-time insights into productivity and financial performance. Improved cancellation and no-show rates further highlight the demand for smarter scheduling and patient communication workflows. Integration of imaging and diagnostics with treatment planning is also gaining traction, while billing tools are increasingly important as more dentists exit insurance networks.

By End-user: Dental Clinics Dominate but Specialty Demand Reshapes the Horizon

Dental clinics accounted for 82.35% of 2025 end-user revenue in the United States dental practice management software market, driven by their role in outpatient care. Hospitals and specialty centers are projected to grow at a 10.10% CAGR through 2031, reflecting rising demand for complex care environments. Spending within clinics is shifting toward DSO-managed organizations, with 29% of DSO-affiliated dentists planning software investments in 2026 compared to 16.3% of non-DSO dentists.

By Practice Size: Solo Practices Lead by Volume, DSOs Drive Technology Velocity

Solo practices held a 42.76% revenue share in 2025, leading the United States dental practice management software market by volume. DSOs, with a projected 12.88% CAGR through 2031, are driving technological adoption due to their scale and need for centralized oversight. ADA data shows 41.5% of dentists cited overhead costs as a top challenge for 2026, with non-DSO dentists less inclined to invest in new software. Advanced features like analytics and claims automation are spreading faster among larger groups and DSOs.

Geography Analysis

The United States dental practice management software market is experiencing strong growth in the Sun Belt, driven by DSO expansion, practice growth, and multi-location management needs. States like Texas, Florida, Georgia, and Arizona attract large dental groups requiring shared scheduling, centralized claims handling, and consistent reporting across widespread offices. Planet DDS’s January 2026 update highlights additions such as Sage Dental, Coast Dental, and Altius Dental, which strengthen its presence in high-growth corridors where cloud deployment supports centralized operations.

The Northeast and Mid-Atlantic remain key revenue centers for the United States dental practice management software market due to dense practice networks and complex payer environments. These regions demand robust billing, reporting, and administrative coordination. Many long-standing practices in these areas, historically reliant on server-based systems, now represent a significant replacement market as older deployments age. Henry Schein One’s installed base of over 75,000 locations and approximately 100 million claims processed annually reflects the continued influence of legacy platforms.

Cloud-native adoption is advancing in the Mountain West and Pacific Coast, supported by practice groups favoring browser-based workflows, integrated imaging, and digitally connected clinical operations. Henry Schein One’s February 2026 integration of Align Technology’s iTero scanners with Dentrix, Dentrix Ascend, and Dentally demonstrates the focus on enhancing imaging-to-record workflows in regions prioritizing digital chairside processes. Smaller and rural markets are slower to adopt due to staffing challenges, reimbursement pressures, and cost control priorities.

Competitive Landscape

The United States dental practice management software market exhibits a dual nature: it is moderately concentrated at the enterprise level but fragmented among independent practices. Numerous smaller vendors compete for budget-conscious customers with slower refresh cycles. Henry Schein One leads with Dentrix and Dentrix Ascend, serving over 75,000 locations and processing approximately 100 million claims annually. The company also supports 90% of the top 50 United States Dental Service Organizations (DSOs), reinforcing its dominance in large-group procurement. Planet DDS, the primary cloud-native competitor, aims to support 14,500 practices by 2025 and has the highest number of 100+-location DSO customers among cloud providers. The market is thus led by two enterprise players, while smaller vendors cater to budget-constrained independent practices.

Competition now focuses on ecosystem breadth, AI functionality, and workflow depth rather than just billing and scheduling. In March 2026, Henry Schein One introduced tiered Dentrix Ascend packages with features like Voice Notes, Image Verify, and Eligibility Pro, embedding AI into core subscriptions.

Planet DDS strengthens its position through cloud scalability and strategic partnerships, extending its platform into financial workflows and specialty settings. Its multi-year agreement with Synchrony made CareCredit the preferred patient financing solution across Denticon and Cloud 9 Ortho, covering 14,500 practices and tying the platform to checkout, treatment acceptance, and payment workflows. In January 2026, Planet DDS expanded its orthodontics and multi-site dentistry presence by adding customers such as The Smilist, Dental Care Alliance, Sage Dental, Coast Dental, Altius Dental, and Choice Healthcare. The market is shifting toward AI, integration depth, financing links, and multi-location visibility, while smaller vendors remain reliant on slower-spending independent offices.

U.S. Dental Practice Management Software Industry Leaders

Carestream Dental LLC

Henry Schein One, LLC

Patterson Companies, Inc.

Planet DDS, Inc.

iDentalSoft, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Pearl integrated its FDA-cleared diagnostic AI with Dentrix Ascend, enabling real-time radiograph pathology detection within the clinical interface, streamlining workflows, and expanding AI access in the US cloud dental practice market.

- March 2026: Henry Schein One launched three AI-driven Dentrix Ascend packages: Essentials, Pro, and Accelerate, targeting diverse practice sizes and collectively supporting over 48,000 US practices with approximately 100 million claims processed annually.

- February 2026: Synchrony and Planet DDS expanded their partnership, embedding CareCredit as the preferred patient financing solution into scheduling and checkout workflows for 14,500 US practices.

- February 2026: Henry Schein One integrated Align Technology’s iTero intraoral scanners with Dentrix, Dentrix Ascend, and Dentally, automating scan imports into patient records and eliminating manual uploads for North American customers.

- January 2026: Planet DDS expanded its portfolio in 2025 by adding major DSOs, including Sage Dental, The Smilist, Coast Dental, Altius Dental, and Choice Healthcare, solidifying its leadership in 100+-location DSO cloud adoption.

U.S. Dental Practice Management Software Market Report Scope

As per the scope of the report, dental practice management software (DPMS) is a comprehensive digital platform that manages the business, administrative, and clinical operations of a dental practice. It centralizes daily tasks like patient scheduling, billing, insurance claims, and clinical charting into one streamlined system.

The U.S. dental practice management software market is segmented by deployment mode, subscription model, application, end-user, and practice size. By deployment mode, the market includes web-based, cloud-based, and on-premise solutions. By subscription model, the market is segmented into perpetual license and subscription/SaaS. By application, the market is categorized into patient communication & engagement, appointment scheduling & calendar, billing & invoicing, insurance & claims management, treatment planning & charting, imaging & diagnostics integration, and analytics & business intelligence. By end-user, the market is segmented into dental clinics, hospitals & specialty dental centers, academic & research institutes, and others. By practice size, the market is segmented into solo practices (1-2 ops), small group practices (3-9 ops), large group practices (10+ ops), and dental service organizations (DSOs). The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Web-based |

| Cloud-based |

| On-premise |

| Perpetual License |

| Subscription / SaaS |

| Patient Communication & Engagement |

| Appointment Scheduling & Calendar |

| Billing & Invoicing |

| Insurance & Claims Management |

| Treatment Planning & Charting |

| Imaging & Diagnostics Integration |

| Analytics & Business Intelligence |

| Dental Clinics |

| Hospitals & Specialty Dental Centers |

| Academic & Research Institutes |

| Others |

| Solo Practices (1-2 ops) |

| Small Group Practices (3-9 ops) |

| Large Group Practices (10+ ops) |

| Dental Service Organizations (DSOs) |

| By Deployment Mode | Web-based |

| Cloud-based | |

| On-premise | |

| By Subscription Model | Perpetual License |

| Subscription / SaaS | |

| By Application | Patient Communication & Engagement |

| Appointment Scheduling & Calendar | |

| Billing & Invoicing | |

| Insurance & Claims Management | |

| Treatment Planning & Charting | |

| Imaging & Diagnostics Integration | |

| Analytics & Business Intelligence | |

| By End-user | Dental Clinics |

| Hospitals & Specialty Dental Centers | |

| Academic & Research Institutes | |

| Others | |

| By Practice Size | Solo Practices (1-2 ops) |

| Small Group Practices (3-9 ops) | |

| Large Group Practices (10+ ops) | |

| Dental Service Organizations (DSOs) |

Key Questions Answered in the Report

What is the forecast value of the US dental practice management software market by 2031?

The US dental practice management software market is forecast to reach USD 1.69 billion by 2031 from USD 1.09 billion in 2026, growing at a CAGR of 9.25%.

Which deployment model is growing fastest in US dental practice management software?

Cloud-based deployment is the fastest-growing model, with an 11.95% CAGR through 2031, while on-premise systems still held the largest 43.65% revenue share in 2025.

Why are DSOs important in dental software adoption across the United States?

DSOs are the fastest-growing practice-size segment at a 12.88% CAGR through 2031, and 29% of DSO-affiliated dentists planned software investment in 2026 versus 16.3% of non-DSO dentists.

Which application area is expanding fastest in dental practice management systems?

Analytics and business intelligence is the fastest-growing application at a 12.75% CAGR through 2031, while appointment scheduling and calendar tools led 2025 revenue with a 28.99% share.

What is the biggest barrier for smaller dental practices when switching software?

Smaller practices often face a combined burden of compliance cost, migration disruption, retraining needs, and tighter ROI thresholds, which slows replacement decisions compared with larger DSOs.

How are leading vendors differentiating themselves in 2026?

Leading vendors are using AI, cloud scale, imaging integrations, claims automation, and patient financing partnerships to deepen workflow control and improve retention across multi-location dental groups.

Page last updated on: